Online Term Insurance Plans in India

POSTED BY ON June 3, 2011 COMMENTS (337)

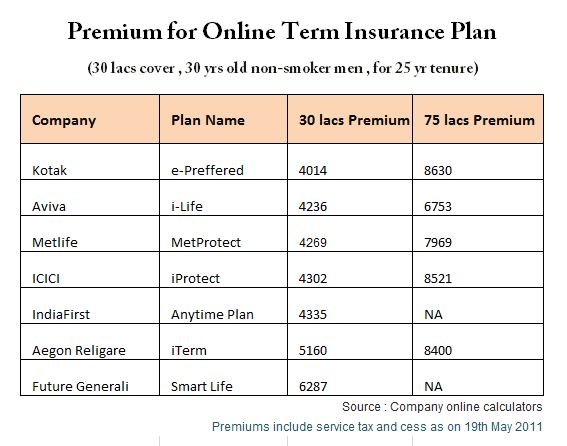

Do you have any idea how many Insurance companies are providing online term plans in India at the moment ? There are total 7 Insurance providers have launched their online term plans and the premiums are highly competitive .

Online Term insurance Plan in India

Aegon Religare was the first company to come up with their iTerm plan which was the cheapest term plan of that time , after that ICICI came up with iProtect . There was a huge response for these policies for cheaper premiums , but both the companies didn’t meet the customer service expectations of customers. A lot of readers even on this blog bought policies from Aegon Religare and ICICI , but faced horrible service when it came to getting policies on time , communication with customer care and its officials , mess of documents etc . A lot of readers suggested that they will never recommend other to go for it.

On the other hand there were customers who didnt face any issue and they got their policies on time . They are recommending others to go for it . However their numbers are smaller than those who faced bad experience. Bad customer service is not desirable by any customer , but I think we can see it improving over time with increased competition and with more better processes . Right now seven companies have come up with online term insurance plans and I am sure more companies are in process of launching it soon . I am not sure if LIC would join them in launching the online term plan , because their offline network is so big and dependent on non-term plans

How Online term insurance plan works

Step 1 : Offline

You go online and calculate your premium , then you start the process of buying the policy and submit your name, age , tenure , sum assured and medical information which affect your premium . After all this you get a premium quote and you pay it online . Most of the people take the premium amount very seriously and believe that its final premium , where as it’s not the case .

Step 2 : Online

After you have paid the premium, there are few things which are yet to be completed . You will get a mail from company or get a call from company that some representative of company will come to your residence and collect the important documents , the documents are also required for KYC . As per your age and given information , the insurer can decide if you will have to appear for medical test or not . If there is anything wrong in medical examination which can affect the premium (increase companies risk of insuring you) , then they can increase the premium (loading) . You can then decide to continue with them by paying the additional premium or cancel the policy .

Update – Apart from Kotak epreffered, Aviva ilife , Metlife metprotect, ICICI iProtect, IndiaFirst anytime Plan, Aegon Religare iTerm and Future Generali Smart Life there are 3 more online term insurance plans introdued in the market which are HDFC Click2Protect, DLF Pramerica – UProtect and Edelweiss Tokia – Life Protection

Comments ? Do you believe in online term plans ? What can motivate you to buy life term insurance online ?

Hello Manish,

I’m looking for a term insurance and cant make up my mind. I’m looking for a cover of 2 crores and have the below queries.

1. Do I take individual or family plan.

2. Will i get coverage if I become a NRI.

3. Waivers like Waiver Of Premium, Critical Illness, Terminal Illness

Do you have any policies to recommend as I did come through a couple of them but the claim settlement ratio are below 80%.

Hi Sunil

I can see that you are thinking of buying a term plan. ALl you need to do is leave your details at http://jagoinvestor.dev.diginnovators.site/solutions/buy-life-insurance-plan

Our team will get in touch with you

Manish

Manish, Thanks for giving many suggestion on insurance. I am going through policy bazaar. Found two policies Religae and PNB metlife, both cover till the age of 75, I selected PNB metlife and added accidental and illness, it routed me to PNBmetlife site. after entering all detail i see 1cr is split in to two portion one lumsum and another monthly.. so i am confused. Also i noticed accidental and illness add on was not there. I stopped there the premium was coming around 22k as i included my wife too.

Can you suggest based on the claim rate, coverage and till whatever maximum age should i go with Metlife? I am now 37 years old.

You can go with them if you trust the name. I would be able to help you with HDFC if you want it, see our service on that http://jagoinvestor.dev.diginnovators.site/services/life-insurance

Hello Manish,

I need answer on following:

1.What should be my anual salary -CTC or Taxable income.

2.For existing any insurence detail which kind of insurence should be considered :

a)Insured for death benifit for Dhanraksha Policy taken with Home Loan :current death cover is 16 lacs .do I need to consider exact figure like 1620550.

b)LIC jeevan anand where death cover is 5 lacs

c)Oriental Health Ins policy -2 Lacs cover for Family

d)Death cover in Car insurence Policy

e)death cover in two wheeler Ins Policy

3.Is it Mandatory my nominee should be dependent on me ?If my wife is earning ,can I show her as nominee?

4.”medical test is mandatory over 50 Lacs ” is this IRDA gudelines or Insurence company specific ?HDFC is giving term insurence of 75 Lacs without medical Insurence?Is it under IRDA norms?

5.Is it good to have riders in term Insurence policy ?If yes then which rider like accidental ,Critical illnes etc?

6.If today I am earning and based on that I can buy a term insurence for a limited sum assured .Like if earning 5 Lacs annual then can take max 60 Lacs term Insurence .Right ?If after buying trm policy ,next year I became job less then do I need to inform Insurence company ?

7.I bought term insurence from Bharti .Now next year I am buying another term plan from HDFC .Do I need to infrom Bharti about this?

Thanks,

1. Taxable income would be a good thing

2. all the policies which has LIFE INSURANCE element

3. yes you can show her as nominee

4. this is company specific, but all companies do this now

5. Your choice purely

6. no you dont need to communicate anything to company

7. No

I am looking for term plan for 30 yrs, 50lc amount for y current age 30 yrs.

I checked quotes from different companies and found that Aviva has 94% good claim settlement ratio, lowest premium, long policy period, good customer service before policy buying.

Compare to that I found HDFC is also second good and it has strong fundamentals in the market but only case is that its premium is approx. 6770 compare to Aviva is 4750.

Manish, Can you please guide me should I go for Aviva or HDFC? I am thinking to go with Aviva. Is it stable and trustable company.

And also Thank you very much for sharing such useful information and also your view points for many users. I have also shares your post to my friends so that they can aware about term plan.

Tushar Patel.

If you ask me, I personally have no issues going with AVIVA , however if you have trust issues, better go with HDFC

I have found claim settlement figures from web for year 2011-12. When 2012-13 data would be released any idea?

I want to go with Max life instead of Aviva and HDFC and thinking to have SA of 50lc for now and in future will take another policy based on requirement with another company. Do I think correct or any suggestion?

You can still go with them. Just make sure that the data given by you to them is 100% correct and no hiding !

Claim settlement numbers will come on IRDA , but you never know the dates , It should arrive after the year ending for sure !

sir,

main ek term plan lena chata hun

mere pariwar main 5 member hain.

mata-pita, wife(private job) or 1-1/2 saal ki ladki.

main uttarakhand main state gov. ka employe hun

meri annual income 450000/- ha

mare gov ka health insurance ha jisme puri family cover ha.

sath hi mere pass 54000/- annual ki lic ha

to mujhe kitne ka or kis company ka term plan lena chahiye.

Abhijit

You can take a term plan for 50 lacs or 1 crore from HDFC

Hi Manish,

Help me to understand if there are difference in exclusions with different Insurance Provider’s

I was told that company charging less premium may have more exclusions compare to other charging higher premiums

regards,

Anil

No , generally its not like that . They might have less riders than others, but in general all term plans cover exactly same things . Read this article to understand why their premiums are different from each other – http://jagoinvestor.dev.diginnovators.site/2013/05/how-insurance-companies-work-and-the-business-model-behind.html

hey Manish,

I am around 26 years old now (1986 born). I have LIC Anand and LIC Amrit of 5lacs SA. I am planning for Online term insurance now for cover of 50 or 75 lakhs.

1) should i go for reliagare considering its service and do u think its worth trusting them for next 30 yrs

2) should i go for aviva i term instead?

I will nominate my mom as of now as i am unmarried still.. planning to add my wife in future as extra nominee.

plz suggest if this ok.

I would vote for Aviva !

I went for Bharti Axa eProtect policy for 50 lakhs SA and 25 years tenure. Actually I went through policybazaar. They suggested choosing between Axa and Aviva, though they pushed a bit more for Axa. I agreed because the premium was the lowest as per my independent research too. Also thought if I went by all reviews I would never end up buying any policy!

They were there on phone to help while filling up the online Bharti Axa form. After paying the calculated premium online, I had to upload a few docs as id, address and salary proof, etc. After that, within 1 or 2 days, I got a call from Bharti Axa that a medical was scheduled for me and that would be done through a home visit.

Got a phone call from the health check up provider for the test and scheduled the check up. They came promptly and finished the test in 15 mins. Ten days after that, I received the policy and with no change in premium.

All in all, had a smooth experience and got the policy in two weeks after the online payment. Now all that remains to test is a smooth claim process, but I won’t be around to post my review on that 🙂

Great .. thanks for sharing your views on Bharti Axa !

Hi Manish,

I am 31 years old and planning to buy my first Term Insurance policy.

Please suggest and clarify my few doubts:

1. Which company shall I go with?

2. What is the difference in bying policy online or from agent, I mean, is there any drawback bying policy online?

3. Do we have LIC term policy available online? if yes, what is the plan name?

Thanks in advance.

Regards,

Bhaskar

1. Aviva or HDFC

2. from agent it will be of high premium, as their commission is to be given

3. NO

Thanks for answering my questons Manish..

So, I should go with HDFC online plan first and LIC online plan later once it’s available. is it correct?

But,I was reading about LIC online term plan in an article published long back in 2011. Is it still not launched?

Thanks & regards,

Bhaskar

Yes , online plan from LIC will not come it seems

With the recent announcement on Aviva selling its stake, does it make sense to go for Aviva?

It will be bought by someone else. If you are fine with it . then please go for it , else someone else !

Hello Manish,

My age is 28 and i need health insurance for me and my MOM(52) & DAD(57) can you please suggest which plan is better.

For you , Religare Care and Oriental for Mother

Hi Manish,

I have recently bought ur 2 books “16 personal finance principles every investor should know” and “How to be your own Financial Planner in 10 steps”. I have never read such type of good explanation with example. If i read it 5 yrs back then now i could be a good investor. Thanks Manish.

I have one question about term insurance. I want to take term insurance of 1 cr so please advice which company is better to go for this. i am 33 old. i have family of 5 member and only i am the source of money. I was suggested from one executed that go for Bharti AXA…. is it good?

I also want to by one health policy for my entire family so please advice for that also.

please advice….

Jatin

Good to know that Jatin

YOu can go with Aviva Term plan ..

Thank for your reply….

But shall i know why only Aviva? is there any strong reason behind this?

Why not other? is it secure?

Please advice…

Jatin

there are other options as well . HDFC , KOtak , ICICI .. but I give you 3-4 other names, you will still ask which one is the best, which is not the way you have to look at it . Just go with anyone you TRUST .

Hi Manish,

I am planning to take online term insurance. I am 24 Yrs old.

Which plan should I go for?

Which types of deaths are covered in online term insurance plan as there are no riders?

Thanks,

Vikram

All deaths are covered in term plan .. go for Aviva or HDFC

Dear Manish,

I am 34 year old and planning to take term plan. i have gone through your site and it’s really help full. I have some question. Can you please help me to get the answer these questions?

1. which online term plan is good? As we are in 2013, do you still think offline term plan is better than online term plan policy?

2. I was smoker earlier and stopped smoking for almost 3 months, still i will be consider as smoker?

3. As per guide line they required Age proof, Address proof and Salary Proof. But From last year i came to South Korea on employment contract for 2 years. Will my salary proof be sufficient? As its Korean company’s salary proof. Do i need to notarize something? I am little bit confused in this point.

Please let me know, if you need any more information or clarification.

Mayukh

1. It can be especially for NRI who dont get online plans

2. Yes, you are a smoker .. once smoker , always a smoker is the funda for insurance companies

3. that will be told to you by insurance company

will it matter if a person moves out of country for long term after taking online policy i.e. at the time purchasing the policy person is in India.

No , not much .. but there is a question while taking the policy that are you having any plans to travel in immediate future, if you are sure about it, then better tell them …

Manish,

last week I purchased “how to be your own financial planner in 10 steps” book, and working on step#1 🙂

now I’m looking for increasing life insurance, age of 39yrs for self with “online term insurance”, can you please suggest 1 or 2 with following my expectations;

1. lowest online insurance premium for 1 cr SA

2. trustworthy insurer / high claim settlement ratio

3. easy / painless claim settlement process for dependents

thanks for your active blogs and book, which is easy to read and understand the personal finance nuisance 🙂

Jay

Thanks Jay .. you can go for Aviva or HDFC Click2Protect !

Hello Manish,

My age is 28 i want to buy Term Plan and i need 750000 lacks cover so please can you suggest which plan is best for me.

Aviva iLife

I read your suggestions and impressed,

Well i just want to know is there any minima criteria of income on papers for term plans and if yes where i can get that?

2. we do business and in that we don’t show more income on papers for tax saving purpose and its also cash business thats why so what should i do to buy 1 cr policy?

waiting for your answer

Rohit.

Sadly

You need to give proof about you income level , only based on that you get term plan for high cover. Ideally you get around 20 times your annual income on max side. So if you have atleast 5-6 lacs of income on papers, then only you will get 1 crore of term plan

Hi Manish,

Thanks for your articles and comments. I am already having a term plan from Kotak & Metlife. I a planning to take another from Tata AIA, new online plan. What are your views regarding this.

Why so many ?

I want to increase my coverage amount.

Hi. I’m planning to take Aviva Term Insurance but I’m confused which particular plan to take??There is Aviva LifeShield Plus, Aviva LifeShield, Aviva LifeShield Advantage, Aviva LifeShield Platinum, Aviva i-Life. Which one should I go for?? I’m looking for 50 Lacs SA for 35 years.

Aviva iLife

Hi Manish,

First of all thank you very much for providing such useful information.

I have taken LIC-Jeevan Anand and already paid 4 premiums in 2 years (15412 Rs quarterly). But the premium is very high. The policy lock period is 3 years so I will

surrender this policy after 1 year.

Now I am planning to buy term insurance. My DOB is 13-Apr-1985, non-smoker.

is it best time for me to buy term plan? Because I have LIC policy now.

Please suggest me good plans.

Thanks

Yes .. go for term plan .. the best time if when you are NOT SUFFICIENT COVERED , which is true right now !

Dear Manish,

Presently I am living at Renwal , 70 K.M. far from capital of Rajasthan(jaipur). If there is any company which offer online term plan at Renwal. I mean any company which offer term plan all over India.

Bharti Axa Life, HDFC and ICICI pru, and maybe SBI LIfe

Hi Manish,

I have been reading your blog for quite some time and have taken some of the investment suggestions.

Currently I was reviewing the term insurances for 50 L and was also checking all my policies including CI, AD, etc riders.

I have taken a home loan and along with it also took a policy called Home Suraksha Plus from HDFC ERGO for 5 years.

In this policy it shows that

Major Illness is covered for the entire Loan amount

Personal Accident for the entire Loan amount

My Question

Can I go for only the term insurance excluding the riders as it is already covered in the Home Suraksha Plus or is this different to the ones mentioned in Term Insurance?

Please enlighten me

But why you need a temr plan then , your death is also covered in that ?

Manish

Thanks a lot for your insights, quite helpful. I have question regarding an Aviva policy, which I own right now, but want to discontinue and move to online i-life policy.

I had taken this policy last year – Aviva Lifeshield Advantage. I paid a premium of about Rs 61,000 (for 1 cr). At that time, I was convinced that most of the premium will be returned after policy term (25 years).

Later I did some math and found that aviva i-life policy will workout better with much lesser premium, though I don’t get any money at the end of the policy term.

With i-life, Aviva is offering for about Rs 4300 (for 50 lacs).

I am 40yrs old. My question is, should I change?

I’ll increase the policy coverage to 1 cr for i-life as well.

Thanks for advice in advance.

Yes you should change ,but are you sure its 4300 for 50 lacs for a 40 yrs old person ? It should be the charge for a much younger age .

I stand corrected, it is for 6 months. Thanks for your response, I appreciate it.

Hi.. tell me why is it that LIC’s term plan is so expensive against Pvt Companies..??

Is there any flaw with the Private companies..?? Waiting for your reply.. you can also email me your reply.

LIC is charging premiums as per old data on claim settlements also they are offline and after all they know htey are king !

Hi Manish,

I have purchased Aegon Religare’s i-term plan (a term plan) for 1 Cr cover for 30 years. As a part of the process,they asked me to submit age proof,address proof,photo & salary proof.

While I have submitted 3 out of the 4 above, I’m not comfortable in sharing my salary slips(3 months) or Form 16 -as I have under declared my actual salary & sharing slips/form 16 is confidential & a possible compliance issue from the employer prospective.

Is it mandatory to submit these salary proof documents?

Thanks

Vibhor

Its manadatory , and which compliance are you talking about ?

Hey Manish,

I am 30 yr old and planning to buy a 1 cr online term plan.

1. I have read through all these post that in this case two policy providers can be a bet option. is it just to avoid the risk? and eny other logic behind this?

2. If a split, Aviva will be one of the choice. Can you recomment other? and should the percemtage be 50-50? any recommendation on the split too?

Its a personal choice .. its not always needed, but you can go for 50 50 .. HDFC is another good option

Hi Manish,

I found this site most useful.

Please guide me, Currently i am in India. and i want to take term insurance, I plan to have 50 Lk cover from AViva and 50 Lakh cover from HDFC. I just received job offer from Oman. Please guide me if i opt these Insurance, whether those will be valid for my stay in OMAN and for period after return to india . I plan to stay 4 years there. that means my whether my NRI status invalidate my policy ? any in case of unfortunate event of death in foreign country can my family get insured amount.

No it will not invalidate it .. but the point is , while taking the plan, there will be a question like are you planning to travel out of india because of your job in next x yrs, then you will have to say YES, and that can increase your premium

Thanks.

I purchased 50 Lakh HDFC Click to Protect Plan. I mentioned in policy application about travel overseas, I will wait for final policy approval. if i received the policy at nil/nominal increase in premium i will also purchase AVIVA 50 lakh.

thanks

ok

Dear Manish,

I received call from HDFC that policy is approved at same premium.

Also they said Medical is not required for 50 Lakh. I am perfectly healthy as on today’s date. So though Insurance Company is dening to do Medical. Whether i need to insist on Medical. or its OK not to have medical. Please reply.

What if one already has a term policy and has to travel overseas for employment in the near future ? What then ? Will the policy still stay in effect ? At the time of applying for the insurance policy I did not know that I might have to consider overseas employment.

Yea , its going to be valid , if your employment is going to last very long , better inform your insurer about it .. just for their records

Thanks for the reply, Manish .. appreciated. And yes, I will inform the insurance company.

Dear Manish,

I am a 27 yrs old nonsmoker. I have applied for term plan of aviva for 50 lakhs. They offered me a plan with Rs. 7135 yearly premium for 33 years of term period. During their medical agency’s medical examination I told the doctor that my parents are diabetic. All tests were done that time. After few days they asked me to give in writing about my medical history mentioning that my parents are diabetic. I did what they asked for. Later they asked another medical examination of urine which I got done by their medical lab agency. Now the company has increased my premium by around Rs. 1600. Is it correct. They have not even told me results of my medical checkup. On what grounds they can increase premium amount.

the premiums are increased based on your medical + family medical history . they will share with your the medical reports if you are ok with the premium increasre and go for the plan . I think you should take it , because any company will go through the same process . Dont get stopped by Rs 1600

Hi Manish Sir,

I am 29 yrs old and want to buy a term insurance of 50 lakh I have seen HDFC Clik 2 protect, Aviva and Bharti Axa.

Premium(6500) & claim Settalement is high in case of HDFC and

Premium(4000)& CSR is low in case of Aviva & Bharti Axa.

Plz give a final push by Selct one For Me I give Thanks With Deep Heart. Plz don’t say no and any thing like it.

Go for Aviva !

Thanks a lot……………….

Now I purchase the policy with confidence

Good work Manish !

I have taken a term plan from HDFC Life for 1 Cr.

Now I want to take a Medical insurance and health insurance for my family (4 persons) me, my wife and parents.

Please advise from where I can get the complete information.

Hi Jitender,

I got a max bupa family plan from this new site zibika.com, they have a lot of online plans and I found the process of comparing policies very simple here. What I liked best was the fact that I did not get any calls form them till I put in a call request on their listing page after i searched for policies, and their person who called was very helpful in making my decision. They said that they are still in early stage so more policies and features they will be adding. I found their online order completion email very useful.. you will have to try to buy to see what I mean 🙂

Manish

please you suggest the best life insurence online plan for me

My DOB is 15 Dec 1983 nonsmoker, unmaried central govt employe

and i also would like to know diffrence bewween online and offline insurence plan

and whether in life insurence acccident cover is included or having some difffrent plan for than

Thanking u

What is the definition of best for you ?

hi manish…

last year my husband took the aviva i-life of 50 lakhs (medical not done)…wen i asked to dept then they said they don,t do the medical test for 50 lacks at the age of 32. we have 5 years old lic of 25 lacs where medical was done. so i was little concerned abt that…

one more thing i want to know from you…my mother-in-law was expired at the age of 55, she had gall bladder stone which later diagnosed last stage of cancer becoz of that stone. since she died at home in village so we don’t have doctor death certificate to prove the reason. so we wrote cause of death is natural in both plans.

as i read in the artical that we shud fill every information true…so worried …pls tell me is that fine or this can create problem?

Yea . ideally you should always give the correct information . If later company comes to know about it then there will be a rejection of claim , you can always argue that how come companies can know about it, but thats the risk you are taking then

Sir

I am planning to buy a term plan for 1 crore but very confused which one to pick as the real problem starts when the claim is to be made. I want to ask whether i can take 2 term plans from 2 different companies of 50 lac each or not and what things to consider in this matter?

Yes you can do that, just choose 2 companies, there is no much concern , if you disclose all the information

Hi Manish,

Great service you are doing to people by giving invaluable advises!

My query is that suppose I take an online term plan today as a resident Indian and after one month, go on an international job assignment for say 4-5 years continuously. What will happen in this case if any untoward happening occurs during my assignment abroad? Can my insurance provider put any block during claim settlement?

Yes you can go , generally there is nothing to worry about this, but ideally read the policy document carefully and see if its mentioned specifically that you need to inform them if you go for more than X days outside india , generally its not the case, but still just check !

Which Company is the Best( Over all) for Term Plan?

No one

at least you give a 3 or 4 best company name for term plan?Which would i trust u?

Kotak , HDFC, Aviva , LIC

which company is good for child plan?

No one ..

at least you give 3 or 4 company name?..

Samarth

We dont support investments in child plans . Read this – http://jagoinvestor.dev.diginnovators.site/2012/02/create-best-child-policy.html

Is it better to go for online plan through any third party website as policy bazaar or do it at the company website? also u mentioned its better to split 1cr policy into 2 under different companies-is this only to decrease the risk ? Won’t it increase my premiums if I do that?(supposing I go for kotak and hdfc)

It will increase the premiums a bit , but the amount of risk comes down is good enough.

Hi Manish,

I have following queries:

1. I am 30 yrs old & a non smoker, currently with no medical problem.I want to buy term plan for 1 Cr for myself shall i split into 2 (50 Lac each) and take 2 policies or i should stick with one.

2. If I opt for 2 term plans from 2 different companies. How the settlement is done, can my family can claim from both the insurance companies?

3.Currently which one is trusted most as I am a newbie in this, i dont have much idea about the claim settlements.

Can you suggest?

Shilpa

1. Yes you can do that

2. Yes , you can claim from all companies

3. There are many like HDFC , Aviva , Kotak

Your articles are really awesome.. full of information and i cant even get these information from insurance companies or agents.

Good to hear that Rajendran ! . Keep reading !

Good to hear that Rajendran !

Hello Manish,

Is there a website whereby one can get a comparison of premium for 50L & 1Cr from all the policy providers ???

Cheers

Vatsal

Yes you can see the article, but they are a bit old data .

Please provide me the link for my reference.

Thanks

I am 37 yrs old & my younger child is 4 yrs old I have purchased a term policy of 1 cr. with a policy term of 15 yrs.

Is this policy term is appropriate for me or should I go for a policy term of 20 yrs.

Please advice

Thanks

Dipak Choudhari

Higher tenure is better , why did you take it for 15 yrs only ?

Dear Manish,

I applied for a 50L policy from Aviva and declared my medical conditions truthfully. I was asked to go in for a medical test. After the medical test was done, I got a mail that the extra premium to be paid was Rs.4500/-, i.e., 127% more than the original amount of Rs.3533/-, with the reason that I have Diabetes. All the reports were in the normal range. I declined to pay and now I have been advised (read threatened) to pay the extra premium or amount will be paid after deducting the medical expenses. This was not mentioned prior to online application.

I now understand that Aegon Religare does not ask for medical tests. Do you suggest that I go ahead with a policy from them, by declaring the medical condition?

SN

Obviosuly you should go ahead . you should be thankful that you are allowed to get apolicy right now ., if you dont take it right now , you will face a lot of issue later .

Another thing is that its a very standard rule that in case you opt not to take the policy you will be given back your money after medical tests expenses and other charges if any . insurance policy is a proposal and not a push product

Hi Manish,

As in India not many people are aware of term plan,

I really appriciate the work ur doing by guiding the people & clarifying their doubts about the term plan.

I have 3 questions for u.

1. Can I take a Plocy of high premium from one insurence and low premium from the other company.

like I take 10Lacs from LIC & 50Lacs from anyother PVT. online term policy.

2. What are the chances of claim being rejected or approved from both the companies?

3. Is it true that if LIC approves the claim, then the other company also has to approve the claim.

Thanks & Regards

Adi

Adinarayana

1. Yes

2. That is independent , no relation between two companies

3. No

Adi

Hi Manish,

Came across your website while looking for some answers around buying a term plan for my husband. I am still confused hence putting them forth here for your suggestions –

1) Which channel is better – offline or online? I figured that online channel offers much less premium given that no agent is involved. But am also told going through a broker (not an agent but a broker) is beneficial in the longer term, as in case of any unfortunate situations they help u during claim processing and settlement too. So even though i pay a higher premium i’ll have someone to help me with claims settlement, in case. Also as I understand the online forms are not as detailed as an offline form especially in terms of questions relating to physical health. Hence there may be a chance of the claim being rejected if the form is not very thorough.

2) Which player to go with? Private and new players like Aviva, Aegon, Bharti AXA offer much lower premiums. Are they safe to go with?

3) If we want to take a 1 cr policy shld v take one policy of this amt with one player or split it into 2 policies of 50 l with two players?

thanks

NIdhi

1. Nothing like that .. Its a myth that going offline means there is someone for you . In real life you dont experience it , because agent is not supposed to help you as per his work ? His job is mainly to assist you in buyinh the policy , thats all . Go for online term plan, they are exactly same, just that they are online , no difference

2. Yes they are safe , but you need to read more on this first , and then buy the one which you trust most

3. split in 2

Hi Manish,

Thanks for your prompt reply.

I believe a broker works for the customer while an agent for the insurer. Hence it is said that a broker like Bajaj Capital provides you with after-sales service too. What say?

also how about the thoroughness of the proposal forms in online and offline modes? Is there any difference?

how do i decide which insurer I can trust?

thanks

No , in case of term plans , agents are not liable to help you later , thats a different thing that some of them might want to choose ,. however in real life it does not happen . agents leave customers most of the times after making you buy the policy (he gets maximum commission in first year) . Also why should an agent help you later , what is he getting ?

I think you should buy it from online companies , if you have some trusted agent which you helps later , you can then go with them

Hi Manish,

How is Aviva India’s online term plan – Aviva i-Life?

Please guide..

Its totally fine .. one can go with it

Hi Manish I finally bought Aviva i-Life.

My experience was great 🙂

Thanks for recommending.

Good to hear that !

Thanks a ton, Manish 🙂

Hi Manish,

I am on medication for High BP. The BP condition was diagnosed as part of routine check up in July 2011 and post all blood/urine tests, Echo and TMT, everything is normal except the BP as per the doctor. The high BP issue is also under absolute control (120/80) with the medicines and I just need to be on medication with a 6 monthly doctor follow up.

I am a 32 years old male, non-smoker and left alcohol consumption 6 years back (2006) and applied for Metlife’s Metprotect term insurance in April 2012 for 30L, 35 years period and shared all my health related documents with them. However, the company sent a denial note stating medical conditions as the reason.

So my query is:

1. Is it possible that other companies issue me a policy, if applied with same details or now that Metlife has rejected, I can be sure to see rejection by all companies?

2. I was expecting that Metlife may offer the policy with increased premium but now am not sure if I should apply to other insurance companies?

2. Last, any hope that I can get a cover from companies offering term insurance offline, which usually are costlier?

Thanks a lot in advance for your advice!

Best regards,

Harsh

Harsh

1. Yes, other companies might give you the policy, all companies have different rules of how they look at your issues.

2. No , you should apply for other companies. Try offline versions also

3. Already covered in 2 .

Dear manish,

We are planning to take a Term Insurance for my husband covering CI , worth value of 50 Lacs and with IndiaFirst Life Insurance , after reading all ur comments. But how can we apply as we r NRE. Kindly suggest.

Regards..

Not sure if it would be available for NRI’s … if it is then you will have to be physically present here in India

If a person has single kidney, will it increase the term plan premium?

Manish

Yea may be, mostly the term plan will be denied !

To add to that most of the people born with a single kidney:)

Does Aviva i-Life has riders??

I want to buy i-Life

Sunny

I dont think

Hi Manish,

Wanted to quote a real life incident. I was discussing insurance cover with one of my prospect and he was inclined towards ONLINE TERM PLAN. He says that he will be able to save premium plus all the hassels. He also states that his wife is also well-educated and metro lady and can handle the things on her own.

I asked her plain and simple question – when is the last time your wife visited your insurance companies branch and deposited the premium. Let alone this thing, does she know which is the servicing branch of their policy?? How many times has she visited government office to get the documents ready (Birth certificates/death certificates etc) or banking procedures like getting the draft made or stop payment of the cheque..quite obviously, answers to most of these queries was in NEGATIVE.

..and then it dawned upon him that “human factor” is quite important in these types of transaction (More so in case of TERM PLAN – when the actual thing will start only when you will not be around to guide her).

Might be me being an AGENT will be sounding as biased or something, but i really get scared at the thought of someone taking ONLINE TERM PLAN where the wife does not even that such a policy is there in the cupboard.

Please give it a thought..

Dhawal

Yes , its really a scary thought when wife is not even aware about the policy and has no idea about the overall procedure . But then if people can really take some effort to educate the wife and other family members on those 2 things , it would really help .

Hi Manish,

I am planning to buy an online term insurance. However, I have few queries regarding term insurance plan as mentioned:

1.I do have insurance policy from my employer towards me and my family. Also, I am covered in my husband’s policy by his employer, so do I need to mention this information while filing the online form for this online term insurance?

2. We are planning to move out of India may be in an year or two. How does the online term insurance will impact in that scenario?

It would be very helpful if you could help me out with my queries.

Thanks

Kalyani

Kalyani

1. No , group cover through employer is not to be mentioned

2. There wont be any issues, you can go outside India and it will still run as it was running !

but can you buy DLF online?

you mentioned in above note that even DLF Pramerica – UProtect and Edelweiss Tokia – Life Protection have launched their online term plan. I can not find the same on their website. Can you please assist?

Animesh

http://www.dlfpramericalife.com/Product~Protection%20Plans~DLF%20Pramerica%20U-Protect

Note able to find Edelweiss one myself .

I purchased the Aegon Religare iTerm plan in 2 yrs back when it was newly launched and was the first to go online. Needless to say I saved a lot of money by way of premium. The service was excellent …. I got a confirmatory call the very next day from their head office. They fixed up my appointment for medical test as per my convenience at a centre near my residence. I also got reminders for the same via SMS and e-mail. Recently, the company upgraded my cover by nearly 25% and added an accident rider free of cost (the premuim remaining same) . I will pay my third premium shortly. A definite recommendation for all those who wish to buy a term plan online !!!

Parag

Thanks to update that .. I have heard the same thing from many people 🙂 . Congratulations !

Dear Manish,

Two months back, I have taken preferred term plan of Rs.50.00 Lac from Kotak Loife Insurance. Premium is about Rs.9500.00 per annum. Now I wanted to go for online term insurance plan as premium is very less.

1. Whether it is possible to switch to online plan in different company without breaking the policy? Like MNP in case of cellular service.

2. Whether I can purchase online term insurance of additional Rs.50.00 Lac from Kotal Life Insurance?

Santosh

1. No

2. Yes

dear manish,

let me first thank u for doing such a noble task of enlightening and helping investors like me who have very little knowledge regarding all these financial planning.

plz clarify one of my doubts:

i m serving in an armed force. can i buy the term plans like any other person or there is any restriction for a person like me due to the hazardous nature of job i do.

thank u.

Mithilesh

Yes .. due to the hazardous job of yours, many company will reject your application , but some of them may give it to you on higher premium (which is fair) .. So apply in some of the companies and see what happens .

Manish

thanx manish for the quick response……can u plz tell me which companies can offer me the insurance……i have got one ANMOL JEEVAN-1 frm lic….i want one more frm pvt coy…..plz help.

thank u.

Mithilesh

I guess you can keep applying to all companies , You cant be sure at this point , which companies will be ready to insure you .

Manish

what if the company doesnt ask u for a test as in case of iCare and gives me a 40L cover just on basis of my knowledge…can such plans sustain and can a customer like me believe that they wil settle my claim w/o knowing my medical condition at time of taking the policy…Im 48 and icare is my second option…SHOULD I TRUST IT GIVEN THEY ARE ABIDED BY THE CONTRACT or donot consider taking icare…i dont understand the psyche behind such a “no medical plan”

Amish

These policies assume that the medical issue will be with the group and price the premium higher , so those who dont have any issues, pay more and those who have , pay less. so overall there is no distinction between the premiums for unhealthy and healthy person, If you do not have faith in these systems, better avoid it .

Manish

Hello Friends.

I am 41 years and without insurance but now i want to buy term plan. I am planning to buy policy for 50 lacs for 25 year terms. I found premium if aviva I protect for 55 lacs with 29 years terms as Rs9915/-. Should I go for it or try for some another plan? Please advice me.

I found that if i decrease sum insured in above plan from 50lacs, premium increases. I dont know why?

thanks

Param

Paramjit

You have different options .. A new plan from Bharti Axa called eprotect is also there .. You can look at that too .. Go for the company which you trust !

Also regarding premium going up if you decrease the SUm Assured is a common question , without going into much detail , understand that high sum assured policies get discount and the medical covers are there to insure that high quality life is being insured .

Manish

Sir,

It’s is eye opener by Jago Investor. I am the subsriber of jagoinvestor for a year or two and have got opportunities to read dozens of useful articles which has been quite useful and knowledge booster for me.

Good to hear that Ram 🙂 .. Keep reading !

I am a smoker and found it is expensive when you declare urself as smoker while buying a term plan. This might be a stupid question, what if I show myself as a non smoker? How they track in medical test if an individual is not smoking since couple of months.

Ravi

Dont do that .. i dont know exactly , but I am sure you appreciate the technology and medical advancement 🙂 .. Also dont dare to try this, because you will not be present to verify your tricks 🙂

Yes,

being precise in blood test there is nicotine test which can detect nicotine usage even for past 12 months

which one is the best online term life insurance plan that has good record of customer satisfaction and the riders associated therewith?

Aviva , HDFC are good options as per your criteria .. LIC is best in claim settlement

i have signed up for several times for enlightening me with the light of benefits of buying a online term insurance but of no avail as if remained in darkness. despite that a beam of ray from very distantance is still left out in me.

Ujjawal

Your comment is not clear to me

Hi,

I checked all the insurance policies from different providers and found that AEGON RELIGARE is providing the cheapest policy (Smoker and non-smoker both) and does include all forms of death including terrorist attack. It is available for upto 75 age. My age is 26 yr so that means I can get insurance for next 49 yrs at today’s price.

There is one additional rider ‘waiver of premium in critical illness’ available which I feel should be selected because it cost very less.

Namit

yea thats true .. if you are fine with them , go ahead , no issues on that !

Hi Urvek,

I have taken online policy from Aviva. The process was ok, Once you get the ID, they will try to call you and get the details and after the payment on line, medicals will be through. I found that is working fine. No additional charges after the medical is through for me.

i am 22 yrs of age……….. i hav to put a life insurance policy of around 12-16 thousands of premium — time period of 15 – 20 yrs of scheme ………..

i am confusing whch scheme i hav to be choose ………. can u give me a suggestion with more money back return scheme

Ashok

Better start investing Mutual funds

@Manish,

Here is good news for our blog readers. The latest player to enter the ONLINE TERM PLAN ring is BHARTI AXA

http://economictimes.indiatimes.com/personal-finance/insurance/insurance-news/bharti-axa-life-launches-its-first-online-plan-iprotect/articleshow/11743958.cms

I am 33 yr Married with one Angel. I wilsh to go for 75 Lacs of Term plan. Please suggest which compay i should look for .

Hi Manish , Which is better option – Icici or Aviva

Hi Manish,

I am 39 yrs interested in buying 1 crore policy.

Between Aviva (maximum term 31 years, premium 14,659) and Religare (maximum term 36 years premium 14,659) what would you recommend.

Thanks

Hi Manish,

I am 39 yrs interested in buying 1 crore policy.

Between Aviva (maximum term 31 years, premium 14,659) and Religare (maximum term 36 years premium 14,400) what would you recommend.

Thanks

Hi all,

I have also evaluate both of the above aviva and religare. Religare offered max term more with lower premium. but the settlement ration is lowest in Religare which the only and most important factor for confusion to choose a right term policy…? 🙁

Urvek

There has to be a balance between all the things .. you can go with kotak or Aviva or HDFC also

Dear All,

I want to buy a term plan from aviva i-life. but i have read lot of comments on other website against this plan like they increase their premium amount after medical test and all..

can anybody help me out in this matter based on their personal experiences to decide should i go for it or not?

Thanks,

Urvek

Its not always the cases. . the premiums increase after medicals only if some issue is there in health or family history , else there is no issue

Manish

Hi,

Thanks for a very illuminating article, your site helps layman understand the intricacies of this complex insurance business. From your site only I have learnt a lot about how and why of Insurance.

I have one question regarding life insurance- They ask for history of previsou illness, so while giving that information how long back are we needed to disclose. For example if one had some infection say, Jaundice some 15 years back and was completely recovered should we still disclose this information. I dont wan’t the insurance guys to jack up the premium for these harmless things.

Kiran

You need to mention those illness which you are still having and if you went ahead with some big size hospitalization , not small one’s

Manish

Hello Manish,

I have been reading your articles and must admit you give a good overview on the queries asked.

I was looking for Aviva on the term plan and must say its a pretty good offer in the market for the online plan,but there are no riders that one can opt for.

Can you suggest a combination of a cheaper term plan & riders options available.

Jay

Kotak has some riders and comes cheap , other option is SBI , but thats not too cheap

Thanks Manish, but between kotak and aviva, what is your suggestion?

The premium which is given in the above article not correct. While I am trying to buy the policy they are shwoing a different amount altogehter.

Giri

yea .. thats an old article

hiiiiiiiiii Manish

I want to buy term plan and i just checking the site of IRDA i see the HDFC plan is also good and KOTAK,ICICI is also good. and the claim ratio of that plan is soooooooooooooooooooooo gooooooooooooooooooood. LIC is gone down in 2011.

Manish

You can go with them .. but LIC claim settlement is better than thos

Manish

Hello , I am seeking for Term Plan apprx 75 lacs for 30 years.I also taken Home loan app 18 lacs.Now I am 31 years old.

Please suggest , which Insurance provider is good.Also let me know How much sum of Rider we have to add in this.

Dheeraj

You should go for options like Aviva iLife, Kotak epreffered

Manish

Hi . I am 33 and had chosen ICICI i-care with ADB. Online option…for 35L.

Unfortunately My application is rejected by this company.

I guess that happened because I opted for YES in column asking about hazardous activity.

YES i do a lot of trekkings and plan to do rock climbing and mountaineering for sure and hence I honestly declared.

Well in that case what are the options left to me. Can another company also reject my application because of my hobby. I am little upset with this.

Harish

Ideally they should only increase the premium and not decline it .. check with offline options if it does not work out with online options like kotak , aviva etc

Manish

Manish ,

Thanks for the suggestion. I could purchase term plan from Aviva i-life and HDFC click2protect.

Online process to buy these was smooth with help of policy bazaar.

Next is, the respective companies will shall provide me further documents and will write how the process and my experience goes.

Jagoinvester forums are helping me in planning and directing my finances well.

BTW Manish, I read somewhere you too like trekking. Trekkers are health people. and wish you all a happy new year 2012.

Harish

Good to see you moving with your actions 🙂 . good going ..

I love trekking and have done few treks in and around Bangalore and Pune , but not a lot 🙂 . Now a days I am not doing a lot because my wife does not allow 🙂

manish

thanks Manish. Could you please let me know among Kotal e-preffered and aviva which one is better. A bit confused . kindly help me to choose the correct one.

Hi Manish,

I have a endowment policy with LIC which was taken 5 yrs back, then i used to sail on ships and so my premium was high. But now i have settled down with the college, so will my premium be redueced as the risk factor has come down.

Satheesh

It will not come down just because your job has changed now , it always is fixed based on when you had taken the policy .

Its recommended that you stop the policy now and take a term plan for your insurance needs

manish

Hi i am about to take a term policy. LIC is my first choice but the premium is very high. Whereas Aviva is giving the sane SA in very cheap rate. Is private company company like aviva is reliable in India. If yes then which one is the best in term of claim settlement.

Manish waiting for you feedback. Thanks in advance

Addy

Aviva is a good option … you can take that , but LIC has the best claim settlement ratio

Manish

Hi Manish,

after reading ur replies to my earlier emails, i went ahead with aviva i-life, and the experience has been good so far. it was quick, and their cust support was cooperative. thank you.

L thomas

Good to hear that .. but make sure this decision was yours and you take its responsibility

Manish

Hi all, I was thinking of going ahead with Aviva Life Insurance offline. Suddenly I saw in the website about the e-life. So I started the process, I was able to complete the two pages in the process but after that there was some disturbance. But I am getting calls from the customer executives to fill in the form and go for that policy. After reading this I have made up my mind to go ahead with Aviva e-life policy. I’ll do the entire process and let me tell you how my experience was, I hope it should be good, Thanks

Geetha

Good to know that .. note that the policy name is iLIfe and not e-life .. you can go ahead with the policy

Manish

Manish

I could read lot of info in the site, really gud to know about so many financial aspects where I was neglecting; (Bahut Achhee tharaf likha hua hai!) By the by, I don’t know much Hindi; so pls don’t reply me in Hindi; just I’ll use some words here and there; that’s it;

Really very interesting to read and to know more on financial matters,

Regards

Geetha

Geetha

Good to hear that you learned a lot of things 🙂 .

Manish

Hi Manish,

Thanks a lot for very useful information.(As usual..)

Anyone that I come across and has a question on financial planning; I am suggesting to visit your blog. 🙂

I have a question.

I want to buy term insurance plan ASAP. (I am 29 and probably already late)

The problem is, currently I am out of India and dopnt plan to visit India till Dec 2012.

I dont want to wait till then to have my term insurance.

I tried buy i-protect online; but for the reason I am not in India they denied me to offer policy.

Also, there will be mediacal examination in case of any other insurer.

I dont know how I can get it done by being out of India.

Any Suggestion?

Nitin

Sadly , almost all the companies need you available in India for medical for issuing a term pla , also you would need income and address proof in India ! ..

iProtect is now called iCare and it does not have medical examination . You will have to visit india and only then you can take a term plan

Manish

Dear Manish ,

I belongs to asmall town ZIRA in Punjab,I want to buy online term plan but most of companies have this facility in selected cities ,so plese gide me.

Regards,

Prabhjot Singh

Prabhjot

Yea .. online term plans are not there in small cities , you will have to go with offline term plans .

Manish

I have purchased i-life term insurance from Aviva couple of months back for a cover of Rs.60 lakhs by paying a premium of Rs. 9382 without any riders. The entire process was hassle free, smooth & quick. They sent their representative to my residence to collect my blood sample and conduct the ECG. The customer care of Aviva was very responsive and answered all my queries and I was able to procure the policy in 4 days flat. Compared to my previous insurer Metlife from whom I’d purchased a offline term policy 4 years back for a cover of Rs. 50 lakhs with Accidental Death Benefit of Rs 10 lakhs and Critical Illness cover of Rs. 10 lakhs (Premium Rs 29476), the experience with Aviva was far better. Once I received i-life policy I have discontinued my Metilfe pure term policy as the premium I’m paying to Aviva is almost 70% cheaper.

Overall, I would recommend Aviva i-life for their efficient service and low premium.

Regards,

Anil

Anil

Good to hear that you are liking AVIVA 🙂 .

Manish

Hi, Sir

I don,t have any knowledge about online term plan system but I have heard and seen the programme on CNBC channel, Now I have planed to purchase a online term plan, My date of birth is 1st Jan. 1964. I am interested in 10 years plan. I can invest upto 50,000/- (Rs. fifty thousand only) anually, Pl, seggest which is the best plan for me it may be PSU or Private I want my money to be safe and returned should be hassle free.

Shyam

Term plas are not investment proucts , its only a product to give you security for a fee .. thats all . So you can pay 10k per year and get 50 lacs worth of insurace . thats all the product is

Manish

Dear Manish,

Thanks for attend my mail. last week one of the LIC agent approached me to take a Jivan Anand Policy, I have two policy from LIC, Now I don’t want to go for LIC, so, will you advise me which companies / Bank policy premium is competitive and high insurance cover.

Shyam

You can go with LIC term plan , there is nothing wrong in that .. but just understand that there are pvt companies with much cheaper premiums , there are several reasons why LIC term plan premiums are higher than others, but lets not get into that .. you can try out AVIVA and KOTAK

Manish

Aviva i-life seems to be the best term plan. I am going to apply for this and let me see how the experience is 🙂

Sure .. we will look forward to your experience

Manish

Hi Manish,

I am a bit confused, I am trying to buy a term insurance but the variation in premiums is a lot. I was searching the net for feedback but could not get a clear picture. Also there is a difference of 30 to 40% between online and off line term insurance premium quote from the same insurer. Why so much difference, I fail to understand. Can you please shed some light as to the reliability and dependability on purchasing online term insurance.

The quotes for a term insurance are as follows:

for a Male / 35 Yrs Age /Smoker / 1 Cr / Term 25 years

Quotes are inclusive of Service Tax except for MetLife

Aviva / iLife / Rs 17,542

ICICI / iCare / Rs 19,192 (Income Protection Plan) / Rs 21,839 (Home Loan Protection Plan)

Kotak / ePreffered / Rs 26,003.23

India First / Anytime / Rs 9,945 *** For Rs 49 L cover ***

MetLife / MetProtect / Rs 26,300 + S Tax

Religare / i Term Plan / Rs 20,900

Future Generali / Smart Life / Rs 11,910 (Cover Rs 49.99 L)

Alok

Online plans are same as offline plans , just that the premiums are lower because of absense of agents and also becuase of the market segment

Manish

Hi Manish,

I’m a 29-yr old working woman, married and a mother of one.

I’m looking for a term insurance for myself (50L), and 33-yr old hubby(75L). Although we’re both inclined towards LIC obviously because of the trust factor, am also considering the pvt players, because of the cost .My questions :

1. Am confused whom to go with, between HDFC/Aviva/ICICI/SBI.

2. Also, whats your say on online policies of Aviva/ICICI ?

3. Is it better that hubby goes for a mix of LIC and one of these?

I understand that these are purely personal decisions, but would appreciate your experienced opinion.

L thomas

More options means for confusion , still you need to look at each of them and understand which you trust most and are comfortable with their options. Go for mix of LIC and one more pvt player , Aviva and Kotak can be good options

Manish

Thanks!

I agree that more options = more confusions..

Are Aviva’s and Kotak’s online policies just as fine as the offline ones?

L Thomas

As Online term plans are as good as offline term plans .. you dont need to worry about them

Manish

Whats your take on HDFC’s sampoorna samriddhi plan.. Looking at it from an investment point of view, it looks too good to be true.

Thanks manish for your reply.

What would you advise for offline or online mode.

Rahul..

Rahul

There is no general rule for that . Depends totally on your faith and expectations

Manish

Hi Manish,

Waiting for your advise.

Rahul.

Hello Manish,

I am 26 yrs, married, will be 27 on this 29, My DOB is 29/09/84. I am already having one term plan of 40 Lacs from LIC. I am looking for one more term plan of 65 Lacs. I am in confusion to go for it from which company either Aviva I-life or Kotak e-preferred.

Aviva I-life premium for SA 65Lacs for the period of 35 yrs is around Rs.5327 only,

Kotak E-preferred for SA 65 Lacs for period max 30 yrs is 7059 only.

Need your two advise.

1. Whether should i go for online or offline mode. I know its up to person to decide, but i want to you your preference.

2. which one you will recommend Aviva or Kotak.

Aviva giving cover upto more yrs with less premium, whereas kotak is more.

Is it only the fact that Aviva is new. Somebody told me Aviva is good, they are pure into only into Insurance bussiness, nothing else.

Looking forward to your kind advise.

Rahul.

Rahul

You can go with Aviva, they are good. Please read the fine prints !

Manish

Hi manish

can u pl guide me a good term insurance where I can pay monthly or quarterly premiums my dob 08051957

thank you and regards, Joseph Joseph1957@gmail.com

Hi one more question to all,

my birthdate is 13th Sept… if i start formality for any term plan today.. wht will be my age considered… age as at today if i pay online today or as at date whe policy is issued, which will definately make me one year elder?

thx

JR

Mostly the date of birth considered is hte closest one .. so as your closest DOB is near , it will be taken , so you take term plan today or after 2-3 months , your 13th Sept age will be considered . Dont delay your action because of this .

Manish

Hi all,

couple of questions

1)as of now Aviva seems cheapest… as rightly mentioned by one of the reader, lesser by around 20-30%…. why no one else is talking about it? why is it not that popular compared to ICICI? who are the Owners in Aviva?

2) for claims on ICICI one can go to ICICI lombard offices… how about Aviva.. not seen its infrastucture properly spread across city..

3) Aviva offers lesser premium for 50 L compared to 40L/ 45L… how does tht work..

4) though LIC is joining the race… wht readers thinks can be their premium range… way cheaper than Aviva/ ICICI?

thx!

JR

1) Aviva is pretty new in this compared to ICICI . ICICI has been doing offline term plans from years and it started online one long back (1 yr) .. aviva is new .. so hence not many talk about it , may be less trust factor

2) You dont have to go to ICICI Lombard offices to claim , because you have LIFE insurance policies , ICICI LOmbard is their Loan related department , you have to go to ICICI PRU offices .. The Infra will depend on how old the company is in India and how much reach they have . .ICICI has wider reach

3) Thats totally ok .. dont get into that , just accept it for now .. its a complicated thing to understand

4) LIC will not be cheaper than Aviva or ICICI .. they will be higher priced .

Manish

I will look forward for a better customer service in on-line term plans which it seems almost all Insurance Companies are lacking.

For sake of hundred rupees, I cannot go for a insurance company which has till date not provided any customer service..

LIC is set to join the gang.

Information at this link..

http://tinyurl.com/3kommny

Dhamodharan

Thanks a lot of the news … Its a great news 🙂 . Waiting for it

Manish

Hi Manish, Nice post!

In my view currently Aviva India’s iLife is the best online term plan as it has the lowest premium compared with post on them.

Hello Sir,i’m of 18 & planning for opting a term plan at this age.as i’m too young but i’m interested in this stuffs….its all about safety…can anyone suggest me a term plan with normally low premiums & high claiming with good customer’s services.,.i’m in a huge doubt about it……..please,,,,,i want the reply soon..

Ashish

Are you working and earning ? Because you will not get a insurance plan (dont mistake it with LIC policies) if you are not earning and there is no financial dependent .

Manish

Hello Manish..This site has been very helpful for all kinds of insurance/investment information.As I happened to wake up suddenly that I am not adequately insured (I am blessed with kid 3 months back), thought of taking control of Financial planning, I stumbled upon your site.After days (and nights) of reading thru’ experts opinions and discussions, I made up my mind not to listen to LIC guys’ sugar coated words/policies (child plans, endowment, retirement plans etc).

I decided to take online policy for 50 Lakhs (to start with). After dilly dallying a lot and being persuaded by PolicyBazaar guy, I have shortlisted ICICI – iProtect.I know this itself a daring decision given the complaints I got to hear from many of our friends on this site.Just I decided to go with “Known Devil” as I have Banking account with ICICI since 10 years.

I have a question for you.

As I filled online form with the help of Policy bazar, he checked with me if I have already any Insurance cover. I told him I have LIC Triple cover, LIC Jeevan Sree (took in 2002) and ICICI Lifetime Pension. But he insisted if any Pure Term Plan which I said No.

Are the above plans doesnt count as Life cover plans?In the Proposal document, he has finally filled as No.

Q) Do you have any existing life insurance cover with other companies?

A) No

Is this OK , or will it count as wrong information?

If this is wrong, what’s the recourse I have now as I have paid the premium online and expected to send the proof documents and some medical tests yet to be conducted.

Thanks.

Kiran

No ,its not ok , He should have mentioned “YES” .. The reason he was asking for other polcies is because term plans have high cover, and yoour current policies dont have very high cover , but still it should be “YES” , why didnt you ask him the reason ? Why didnt you fill up the form yourself ?

Manish

Manish, regarding the existing policies, which got skipped on the Proposal form of ICICI-iProtect, I put a mail to Customer care of ICICI Pru life, they asked me to send a Letter to their manager with the details of the Existing policies, which I sent and got acknowledgment for the same.I received the Policy Bond(certificate), but with the xerox copy of the initial proposal form which had the “Existing Policy” information as No.There is no mention of existing policies in the Policy document.Should I always keep the “acknowledgment mail” with the Policy document as a proof, for future reference, in such case?

Kiran

you should keep all the documents anyways … Are you saying that even after updating the info , you dont have the information in the documents ?

Hi Manish,

Thanks a lot for the informative article and your answers to the various queries.

I am 39 years old from Bengaluru. I am a non smoker and have a term policy from Metlife (Met suraksha) purchased 4 years ago with a cover of 50 lakhs, critical illness cover of 10 lakhs and accidental death benefit of 10 lakhs. The half yearly premium is around 15000.

I plan to discontinue this policy and instead purchase 2 online term policies from different insurers (aviva/icici/kotak) with a cover of 50 lakhs each. Can you kindly guide me on the following?

1. What is the maximum cover I can buy policies for? My annual income is around 10 lakhs,

2. When I apply online for a new term plan, should I inform that I plan to discontinue the existing met life policy?

Thanks in advance

Anil

1. That would depend from company to company , you take what you want to take , anyways company will put the limit if its above the threshhold

2. at the time of taking the policy all you can mention is which one are currently running , there is nothing like “I am planning to discontinue it” . what if you dont ?

So better terminate your poliocies and then take a fresh one’s

Manish

My experience with aviva:

-insurance amount – 50 L, age 33 yrs , annual premium – 5000

– filled form easily on 28 june

– medical done at home on 30 june

– i am a reformed smoker, quit approx 3 years ago, so i paid the premium in non smoker category but clearly mentioned my past smoking.

– now the problem started, received calls daily from dumb cust care execs,that my premium is wrongly ticked as annual,either 5000 is half yearly premium or i had to pay 3200 as extra as annual premium, on asking them why??? the answers were:( a) decision of underwriting department and they had no clue about basis of decision( b) website was not working properly when i filled the form. These cust care people promised that underwriting dept would call me for exact reason for increase in premium.

– I emailed them on 15 or 16 about final decision/call from underwriting dept/reason for premium increse ( although it had been obvious throughout that it is because of of doubt my smoking status), again a dumb cust care exec called that it is because of my medical reports( it could be high cotinine levels )when i asked her that it cant be true and i can challenge their report, since i am a non smoker for 3 yrs and other blood tests have to be normal ( i am a doctor myself and get my bld tests done regularly). i wrote an email asking about clarification on medicals.

-After that the things have been smooth since i am in contact only through email with them,they enquired again about my smoking status which i confirmed as per my proposal form( the truth). they have finally issued policy in non smoker category.

My final impression about aviva is –

– Obviously they were confused about putting me in which category, so it took long. ( i was even prepared to pay premium as a smoker if thy conveyed it to me clearly, i mentioned this to them in email.)

– there cust care execs are illinformed and dumb but i think that is the case everywhere.

– Finally i am satisfied with them completely since mine is a slightly different case.

Parikshit

Thanks for sharing your case with Aviva .. its really a nice thing to hear about others’s experience and learn 🙂 . Didnt you check the premiums of others like Kotak or ICICI ?

Manish

yes aviva is cheapest, almost by 20-30%.

Hi Manish,

Let me first thank you on such a wonderful website which is really doing wonders for people like me who never concentrated on Financial planning in detail. Now after going through with articles posted on Jago Investor, I got to know lot of things.

I have a question for you and need your help in this.

Iam 32 Married with No kid. I have home loan running of around 50 Lakhs and my CTC is 15+ . I am looking out for good term insurance plan to hedge home loan. For past few days iam going through with lot of websites (Policybazaar.com, Aegonreligare, Aviva, HDFC Life, Kotak Insurance etc) which again made me confused. Which Policy I should prefer Offline or Online?

As I read lot of feedbacks online that Insurance companies response for Online is not prompt. Can you suggest me which policy I should go with Online or Offline and from which Company?

regards

Varun

1) In term insurance policy apart from nominee who else will be the stake holder(s) legally. In my family I have my wife( home maker now), my father ( going to retire in one year from PSU) and mother ( home maker), sister ( married and home maker now).

2) I’m working in pvt sector and staying in other city with my wife in a rented house.

3) I want my niece to be nominee and sister as appointee

4) Whether after my dismal my wife would be able to claim it or not?

5) If yes, then should I go for two separate policies with one my niece as nominee and sister as appointee and in other with only my wife as nominee (in order to avoid the monetary dispute, if incase it happens after my dismal)

Pls provide any link where in the qauestionier of medical may be seen

Ashish

I am not sure of that , why dont you get hold of some agent

Manish

Dear Manish,

First I would appreciate you for your dedication, devotion, knowledge and prompt replies for Term policies.

Request you to pls provide your expert guidance for the following queries:

I’m sept’81 born, working in pvt sector and married for last 1 year and my spouse in a home maker. I don’t have any kind of insurance and my ctc is around 6 L. and I do smoke only 1-2 cigarette per day and very rare occasionally social drinker. i want a term insurance policy for 50 L for 35 years. Also I want to make my niece (1.5 years) as the nominee of the policy with my sister (31 years) as appointee. I want to know in case of my death

(1) Would my wife would be able to claim on the insured amount or not? if yes, then

(2) Is there any clause(s) I can make in the policy doc so that my wife would not be able to claim for the claim amount?

(3) Also does consuming 1-2 cigarettes per day may increase the policy premium if yes then by how much %age.

(4) Also in case of suicidal death would the money would be paid to nominee

Regards,

Ashish

I really love to answer questions which are numbered 🙂

1) Yes , if you just put your niece as nominee and thats all , the final amount will not go to your neice , but your wife + your other legal heirs

2) The simplest way is to create a WILL and mention clearly that your niece should be getting the money from Insurance : http://jagoinvestor.dev.diginnovators.site/2010/11/how-to-make-a-will-in-india-and-its-importance.html , Note that nominee is not the final one to get it .

3) Yes , it will definately increase the premium and you should be mentally ready for it , your premium increase will depend from company to company depending on how serious they feel your case is . But considering term plans are so cheap these days , I would say you can take loaded premium also .

4) Nominee always revieves the money , its legal heirs or the person mentioned in the will gets the money , only if you mention that yhou want your niece to get the money , then only she will get it , else not . Suicide is covered after 1 yr, but I would recommened that if you plan to suicide , do it after 2-3 yrs of taking the policy, the claim process will be comparatevely faster .

Manish

Manish

please read this

http://www.moneylife.in/article/online-term-plans/17600.html

@manish

i m still in 2 mimds whether i shud really go for a life cover policy or i shud wait for 8-10

yrs (till i get married 🙂 ) nd then look to get a life cover.

Or one option cud be to buy 1 cover now nd wen i really hv dependnts after 10 yrs i can buy another cover. Wat wil u suggest?

Mohit

Yes , that looks good , but I would recommend buying the cover much before that so that there is nothing called early claim in your case

Manish

Hi Manish,

I am probably the youngest person at 22 looking for a term plan for myself. and one reason for me looking to buy it is to save on my taxes. I started earning from last year and my annual income is 3 lakhs. I have few questions in my mind. please help me out.

1. should i really look to buy a term plan at my age(22). my logic is if i start it so early , i would end my policy term in my fifties considering that most companies offer term plans for maximum term of 35 years. so what really is the best age to take a term plan?

2. is it legal and if legal, then advisable to go for 2 term plans from two diff companies in place of a single plan. are there any advantages/disadvantages in it? and while buying my 2nd term plan, do i need to declare that i already have one to the 2nd company?

thanks in advance

Mohit

1) You should decide taking the term plan based on how many people are dependent on your financially , What will you do of that insurance if you dont have financial dependents . Calculate your cover using this calculator : http://jagoinvestor.dev.diginnovators.site/calculators/html/Insurance-Calculator.html

2) Yes you can take 2 plans from 2 companies and you will have to declare about your 1st company to the 2nd company .

Manish

Dear Manish,

Thanks for the link. I will read it and get back to you.

Thanks,

Rajat

Dear Manish,

Is ICICI i-protect is the only one that include accidental death as rider?

Is there be any other online term plan that includes accidental death as rider?

Best wishes,

Rajat

Rajat

There are many more , have a look at this article : http://jagoinvestor.dev.diginnovators.site/2010/12/term-insurance-plans-comparisions-india.html

Manish

Hi Manish,

Could you clarify if rhinoplasty i.e. for cosmetic purpose is missed out while filling proposal form in a term plan can make the policy void at the time of claim settlement.

Is it ok to inform insurer later or one can go for other insurer if only 1 premium has been paid with complete information.

Regards

SPM

Sanghmitra

I am not very sure . rhinoplasty doesnt seem to be a life threatening thing . I dont think it would affect the premiums and hence companies decisions in case of claims payment .

Manish

hi manish,

am 33 and wantd to take 80l coverage via term plans. decided to break it into 50l and 30l 2 polices for risk sharing. zeroed on to aviva and kotak as cheapest premiums for respective coverages in category.

thought of getting second opinion from policy bazar online platform assuming they are unbiased since they get equal comission from all insurance providers.