Look around, the world is lovely and bright

Look inside, understand yourself and you’ll see new light

Follow your dreams, follow your heart

Do everything that fills you with delight

Wish All the readers a Happy New Year

In this short post we will see what are te things you should make sure you have completed . We will actually see the points you should keep in mind through the older posts only . Take it as a guide for what you have to do in coming year if you have not done .

New readers can look at Archives to find out Old articles categorised by Month and Category

Important Points

Make sure you have adequate life cover , Calculate how you can calculate your Insurance cover and then take a good Term Plan to cover your self . It is extremely important .

Open your PPF account if you have not done it yet , I know its tough to take action , but there is no alternative 🙂 .

Make sure you understand the concepts and importance of Debt and Equity , understand the importance of Asset Allocation . Understand that Equity is extremely risky in Short term and Debt is extremely risky in long term.

Make sure you don’t buy products which you do not understand. This is important , Don’t get into wrong products . doing nothing is a better thing then doing wrong things . Learn from this blog and other blogs , read before you do . don’t do before you read . This is the common mistake . Read some Tips in Personal Finance .

Share, We cant grow unless you share things. 5 ready to learn, less knowledgeable people are better than 1 Albert Einstein. When you share links, tell your friends about this blog, Give your comments in articles, There is conversation happening and that leads to more ideas, disagreements , which are the essential things in life to grow . Do more of it . If you are silent reader , I can understand that you don’t like to talk much , but occasionally come in and say how you feel about the idea , put 2 lines , that’s enough .

What I Wish for in 2010

All the right decisions we can make in life are “simple” and “extremely tough” to take. We get confused because of lots of choices and the simplicity of products. It does not fit with our complicated environment these days. All the wrong decisions we take in life are easy to take , looks good to us at first moment and hence give an impression that they are great and worth taking. Same thing happens in our financial lives . Simple products like Term Plans , SIP in Mutual funds look too easy and simple and hence make us feel that there is some thing wrong with them , We think that how can they be so simple and so powerful, and when we see them in comparison with complicated products like ULIP’s and money back plans, they make us feel like we are doing some thing wrong by buying something which not much people buy. More than 80% Insurance p9licies sold in India are ULIP’s, Just because 80% people do it , It does not mean they are right product for you . Think and judge your self . Just like the top of the ladder is never crowded in any profession , the same way the best products is not the one which is most sought after . Don’t let 2010 be a year when you make the same mistakes which you have done earlier in life . Making mistakes is one of the greatest gift , Repeating them is the biggest curse . So make a mistake, don’t repeat it 🙂 .

I am not a religious person and I am yet to discover if I am a spiritual one either , but there is some thing inside me which asks me to wish for each and ever reader of this blog that he/she should be more educated , more empowered with the psychology of how to succeed in Financial Planning . I feel like this blog is a platform where any new person can come , learn , discuss the ideas and one day he/she can become his/her own financial planner , who is capable of taking all the right decisions one should be making , you don’t need to depend on anyone , neither this blog nor me , you can be your own master and together we can and we will do it . It might take some time , but its going to happen . I know .

I thank you all for the great support and motivation you have provided to make this blog one of the best financial planning blog in the country today. Happy And Prosperous New year to you and your Family .

Manish

Comments , Give me suggestions on how I should take this blog in 2010 and what are the different things we can do on this blog . You are a part of this Family and your views matters .

Updates

The blog completes 2 yrs

Monthly Pageviews are now touching 70,000 per month

800+ comments in last 30 posts in less than 3 months

Just in case you have not done your tax planning for this year and you are in a rush of doing it for providing documents proof to your employer, I will tell you how you can quickly do your tax planning at the last moment. First of all it’s not advised that you wait for last minute for your tax planning investments but now if you are late, let’s see how you should plan for your investments at the last minute to save your taxes. We will also discuss in this short article what are the things you should not do in hurry.

Don’t get mad about tax saving:If you have short term Commitments and can’t afford to lock your money for long term it’s better you do not put money in Tax saving Instruments. You should never do Investments just for tax savings. I have personally not invested for much tax saving this year apart from my company PF and Insurance. I have short term commitments and I cannot afford to lock my money for another 3 yrs. So I better pay tax on the part which I could have invested. There is no point in locking my money and then again running around for personal loan or credit from Friends and Family when need arises.

Life Insurance: Make sure you have adequate life insurance cover. If not, take a term insurance for amount of the cover your are short of. Protection is the first step of successful Financial planning. Take a Term Plan from two Insurers. Look at how to calculate your Insurance requirement. The cheapest Term plan at this moment in market is iTerm from Aegon Religare.

Planning for Long Term Goals: Make a list of goals for long term like Retirement, Child Education, Child Marriage etc (Anything thing with a target date of 5+ yrs). For these goals you can invest in Tax saving Instruments. If the goal is extremely critical and you are not a risk taker then the best thing would be Tax saving Fixed Deposits. If you can take some amount of risk, you can invest your money in ELSS Mutual funds (here is a list of good Equity Mutual funds). For goals which are 10+ yrs away, you can also put partial money in PPF. Investors who have sound knowledge of Markets movement and can spend time and efforts on switching can go for Low cost ULIP’s (see Wealthsurance and Aegon religare). Short term ULIP investing is a BIG and BOLD No No!!

Health Cover: The next thing you should target is your Health Insurance. Better take a Family Floater Plan for your Family and the premium will be exempted under Sec 80D up to max of 15,000.

So the hierarchy of your products should be like this

Life Insurance

Health Insurance

Long Term Investment products like ELSS and PPF

Medium term Investment Products like tax saving FD

What you should not Invest in?

Another Important Point is what no to do in Hurry? So here are some of the things you need to remember

Do not invest in ULIPS in hurry, the last 3 months of financial year is the time when Agents will give their best performance in luring away investors. Don’t listen to their stories of India Shining and other bakwaas, if you don’t understand the product and you do not have skills to manage ULIP’s. Same applies to ULPP’s or any other market linked products.

Do not invest in Endowment or Money back plans for tax savings. Your Father, your Grandfather or your Uncle might push for it but investing in those policies is a long term commitment and just for saving tax this year you cant invest in those policies.

Evaluate your risk appetite again and then take decision. Most of the people can take risk and their situation allows them but they don’t take risk. On the other hand there are people who’s situation does not allow taking risk, but still they take the risk. They confuse between Willingness to take risk Vs Ability to take risk.

Conclusion

Tax saving should be done at the start of year always so that we dont take wrong decisions in hurry. But if you are late you can take some logical decision and still do your tax planning.

Please share your ideas about what other instruments can be used for long term tax savings. Let other know how early tax saving decision has helped you.

Ever thought of a Social Investing community website in India . I am glad to review Stockezy.com today which has grown to a popular stock investing community in last couple of months in India . Stockezy.com is one of the best online places you can get education, stock tips , great links for other financial resources (mainly stock market related) . Let me point out main features of this website which you can use to increase your knowledge and also contribute . There are different sections in Stockezy , Below is a short description of each of them .

Stock Picks : You can stock picks from members on different stocks in indian stock market . With every stock pick there are important things like target price , target date , Stop Loss . There are picks for Buy and Sell both . Link

Opinions : This is a section where you are read opinions of different members on variety of topics from market outlook , stock movement , Short term view , Long term views about something . In short this is a place where you can get to know what a person feels about a topic . There are different categories for opinions so that its easy to find out some opinion . Link

Questions & Answers : You can consider this as a forum for questions and answers , If you have any question on some stock , market direction or any other similar thing , you can just post a question and anyone who wishes can reply to your question . You can see it as a thread which discusses some idea . Link

Portfolio Tracker : This is one of my favorites , this is a place where you can test your investing skills and buy and sell in real time, Its a great platform to test your abilities before you enter the market . You can get your statement which shows your Profit/loss and all the transactions summary in short . So if you are a new investor who is going to enter the market , its an ideal place to test out your strategies and skills . Link

Share Links : This is a very nice addition recently on Stockezy.com . You can view this as a twitter of Financial Markets . Different Financial blogger post links to variety of topics here with different categories . Even I post my personal Finance posts there . Link

[ad#big-banner]

Other Features

You can subscribe to RSS feeds of any particular sub features like Stock Picks | Opinions | Answers .

You can watch out different top traders for different Time frames like Top day trader , Top medium term Investors etc

Gives you a list of Most active investors and top pickers , which gives you a good idea of whom to listen and whom not .

Stockezy is a fast growing Investors community with close to 1 million page views a month , You can get lots of great bloggers like Nooresh Merani , Arun the Stock Guru and other famous bloggers. If you wanted a platform to show your investing skills , Stockezy is the place you belong to . Register to Stockezy using This Link

Further Improvements

There are couple of things which can make its much better . they are

An online technical Analysis Software system which users can use if they wish . There are many investors who like to technically analyse a stock and hence its a much have .

More data on Derivatives segment . there is lack of quality data on F&O segment , so it can add the segment for that .

How should you use Stockezy ?

There are different ways you can use Stockezy.com , if you are new to stock market and want to learn how to to trading , learn the basics, you should join it and start doing the mock trading and see your porformance over a period of time , there are so many great people with knowledge out there who can give you some wisdom , listen to them . Before that you would like to read my ebook on How a newcomer should start in Stock Market .

Comments, Have a look at it and tell me if you like it , Feel free to give your negative and positive feedback .

Disclaimer : I am part of Stockezy.com Bloggers Network

Personal finance is not only about your saving and investment, it includes tax planning, savings, expenses, debts, retirement plans, investment products and all the insurance and other policies. It is an understanding of how these tools works together and also affects each other.

In this article I will tell some tips which will be helpful for your personal finance.

1) Top most reason is flexibility in Decreasing the cover later. So in case you need cover of 60 lacs now, you can divide the cover into 30:30 or 20:40 and then in future whenever you need that your insurance requirement has gone down you can just stop one of the policy.

2) The second reason is that your risk of claim decline from insurance company goes down, but this is a secondary reason.

2. Invest in Tax Saving Products for long term goals

Most of the people still invest in Tax saving funds for their shot term financial Goals. The fact that the money invested will get locked for long term should be taken in positive way and hence you should invest in these for your Long term goal, so that you don’t feel bad about the lock in period because you anyways need money after many years.

For example– Child Education, Retirement, Holidays abroad after many years. For short term goals like Buying car, paying fees, saving for some short term commitment should not be taken care by Tax saving Instruments.

You should use Fixed Deposits, Fixed Maturity Plans, Debt Funds, Balanced funds and Non Tax saving Equity Funds (Risky) for Short term goals. Once you think like this the lock in period will not matter to you at all 🙂

Watch this video given below to know about the tax saving investment tools in detail.

3. Use Top up’s in ULIP’s to minimize Cost

For investors who are going to buy ULIP’s or using ULIP’s for their long term goals, they should use Top up facility in ULIP to minimize the cost. The Allocation charges are generally linked to the regular premium you pay and not the Top up’s. So if you are investing 60,000 per year as premium, you should rather take a 20,000 policy and top up your policy with 40,000.

This way your will save charges on top up money. You can decrease your cost (charges) by anywhere from 50% – 75% using Top ups.

4. Investing in GOLD ETF’s instead of physical GOLD

Why do you want to invest in Physical Gold? The biggest reason is for Daughter’s Marriage and Jewellery required for the same. But the underlying reason always is capital appreciation.

So why not always invest in Gold ETF’s [ Understand what is ETF ] and whenever you need Physical gold, sell the ETF’s, take the money and Buy the Physical Gold at that time. Most of the people invest in Gold physically for Daughters marriage, but the better way would be to invest in ETF’s and when time comes you buy the physical gold by selling the ETF’s.

That is a better way because its more flexible, safe and easy route.

5. Use your LTA, HRA and Medical Reimbursement

I am amazed to see that many Salaried Employees especially youngsters do not care to take the benefit of LTA, Medical reimbursements and HRA just because of their laziness.

So make sure you take advantages of these even if you partly use these things you will save couple of thousands in Tax. All you have to do is save the bills, take the xerox and walk couple of steps to your Finance department and submit them, don’t you think its worth if its can save you couple of thousands in tax saving?

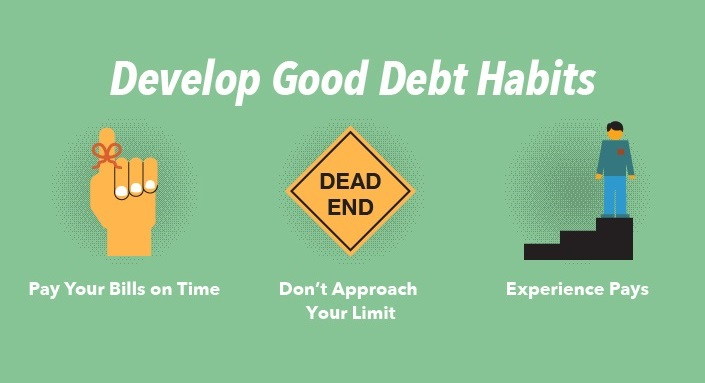

6. Control your Credit taking Habit

Image source: freecreditreport.com

Most of the people take Debt more than they can afford or deserve. Criteria for giving credit is mainly how much you earn. The company never knows your expenses and your future goals, your risk appetite, your future plans etc.

People earning 5 lacs per annam take debt of 30 lacs for Home, unnecessary personal loans for buying LCD’s, going for vacation and other non-priorities in life. This can have ill-effects later on.

Also companies are now keeping an eye on your credit taking behavior and it affects your credit score through which companies in India have started using as a decision making variable. So watch out your credit taking behavior. Don’t over-do it.

7. Dont Over monitor your Portfolio

Keeping an eye over your portfolio is great. You should look at your shares, mutual funds, ULIP’s etc. but overdoing it can be fatal sometimes. Some of us have this obsession of watching shares, mutual funds NAV and ULIP’s NAV on daily or may be weekly basis. See How much time you should invest in Personal Finance.

This is not a good sign for long term investing especially for people like us who are into regular jobs and have no much time to contribute in your Finances.

When you are a long term investor, why keep track of short term movements, these moves will have not much value in your all growth and short term movements will affect you mentally and tempt you take take decisions in short term because your money is either going up or down fast.

More of anything is bad and same things is true for your over involvement. Couple of hours per month or every quarter is good enough. Don’t get a feeling that successful financial life means more action.

8. Share your Financials with Family

If you are dead in another 1 hour, do you think your Family will be able to find out all your investments and Insurance documents and successfully claim them?

Are they unaware of the fact that you took a huge Insurance cover for them or you invested 50,000 in a ULIP last month?

Most of us graduate from novice investors to a good investor but still are left behind in taking care of this extremely critical point of sharing each and every details of our finances and making sure that the documents are within reach.

Let your wife, children have a good idea of where the documents are and where your investments are, have xerox copies of every document and have them at 2-3 different places and make sure people know about them. Emotional pain of losing some one and no idea of the finances which will take care of them is a kind of situation you never want you loved ones to be into 🙂

9. Don’t compare your returns with others

Image source: i.ytimg.com

You are different, be proud of this fact. If your returns are less than your friend’s mutual funds that’s fine. Don’t compare your self with others, there are many things which determines what you get in life like knowledge, luck, skills, timing etc.

So just make sure that you are getting what you try for. Don’t lose focus from your goals, your main aim in life is to achieve your financial goals easily and smoothly. Financial Planning is a race where everyone who reaches their personal target is a winner.

Make sure you don’t hurt yourself by competing with others.

10. Investigate everything before you Buy it

When you buy something, make sure you try to get information on Internet, ask on forums at different websites and make sure you find out maximum about thing product you are buying. Spending 30 minutes investigating your product can save you from lot of trouble.

One person I know recently took a home loan from HDFC and went for additional Life over from same bank for 30 lacs. He didn’t investigate much about the cost. It was around 8k per year for the term Insurance. When some days back we saw quotes from other company, the cheapest quote was around 6,000 from ICICI Prudential.

He was paying 2,000 more for the same thing because he didn’t spend 5 min extra investigating about the product. Just think what is the loss of spending some time investigating your product. How many of you took an ULIP after agent explained it to you and didn’t inspect much about it.

Email This to your Friend:

11. Invest and Spend, not vice Versa

You receive your salary -> then you spend all your money -> then save or invest if you are left with something. This is not a right attitude.

You should change it to Get Salary -> Invest your money as per your future goals -> Spend the rest.

Once you are saving some part of your salary, somehow you will find ways to spend on things which are of first priority and would refrain from spending on things which can be avoided but if you spend first and try to save later, you will end up spending on unnecessary things.

So better change the order of spending and saving. You can definitely live with your 90% salary , so at least save 10%. There is no harm in trying out this. If it does not work, you can go back to spend and save.

12. Build your Emergency Fund now

Make sure you have emergency fund. If you are listening about this from long time and haven’t done it yet, the best thing would be to take a pen and paper right now and plan for it.

This is the money with the aim to provide you immediate access, not growth of money. Don’t concentrate on getting great returns from this part of your portfolio. The aim of this part is just to give you high liquidity in case of emergency. That’s all.

So simple rule is 2 months of expenses in Cash which you can access in minutes from ATM and 3-4 months of expenses in Liquid funds, which you can get back in 3-4 days.

This is preparation for a situation like if you lose your job and need time to search for something you really like, or get a long term illness and cannot earn money in short term or special emergencies. You can always reach out to close friends and Family for money, but why to depend when you can be self-dependent.

Its’ all about strong planning.

13. Equity for Long term, Debt for Short term

I say this again and again, this is the golden rule, one of the fundamentals of Strong financial planning. Long term goals whose target date is more than 7-8 yrs like Child Education and Retirement should always be linked with Equity products like Equity Mutual funds, Direct Stocks, ULIP’s, Index ETF’s, Index Funds.

That’s because you can get great returns in long run from these things with lesser risk. On the other hand short term goals should be achieved by debt products like FD’s, Debt Funds, Recurring Deposit, Short term bonds. You can also use Balanced funds if you have moderate risk appetite and time horizon is 3-4 yrs.

14. If you dont understand, Don’t take it

How many investors understand how their ULIP works and what are different costs and how to use it efficiently? Not more than 3-4 % I believe.

How many people know why they have invested in Mutual funds which had a fancy name and which makes you feel like you have invested in something great and how many Endowment Policy holders know the overall final return they would get from their Policies?

Investors get into products which they do not understand well and then they can’t make best use of it which defeats the purpose. In reality the best products are least complicated one’s like Mutual funds, FD’s, Term Insurance, ETF’s, Gold ETF’s etc.

So if you don’t invest in something which looks fancy, you are privileged and should be thankful to god. Companies come up with complicated things which makes general investors feel that they are dumb and these companies are some big shot high class super knowledgeable in field of finance.

Just ask yourself if you want to eat the best, tasty and healthy food in this world then where will you go? 5 star hotels? I don’t think so 😉

15. Try new products now

There was a time when LIC policies, FD’s, NSC and PPF were the only thing in one’s portfolio. There was not much choice and people were risk averse. That was a different time.

Things have changed today and Finance world is different now and it’s more complicated now compared to olden days because of lots of choices in Financial products for us today. Don’t hesitate by trying out new stuff.

There are different products these days like Index ETF’s, Index Funds, GOLD ETF’s, SIP in Mutual funds, Reverse Mortgage etc. Don’t be stuck in same products like our Fathers and grand fathers have done.

16. Take Personal Loan to pay off your Credit Card Debt

In case you have any Credit card debt and you have converted it to EMI, it would be a better option to take a personal loan and pay off your Credit card debt as soon as possible.

Credit card interest charges are anywhere from 36% to 48% per annum which you don’t realise because it sucks your money slowly and it’s not significant per month so you don’t feel it. So taking a personal loan is a better choice and pay 15-20% interest on that.

You should always try to stay away from Credit card debt at the first place anyways.

17. Educate your self more

At the end, you have to learn stuff. No need to become a pro ,but you should keep updating yourself every month with basic things. Read Personal Finance Magazines like Outlook Money (Link to online issue) and Money Today (Link to online issue) and other blogs on Financial Planning .

Also if you are new to this blog, Subscribe to Email Updates to get fresh content in your Inbox twice a week. .

Readers Contribution

18. If appears to good to be true then probably it is not: So better if something looks great, then make sure you investigate well because there are more chances that it’s not that good as it sounds .There is no free lunch 🙂 – Amit Kumar

19. Learn simple maths : This is very nice point . Learning basic formula’s can help you a lot , you should know CAGR , IRR and Future Value formula .. – Amit Kumar

20. Find a right Financial Advisor : Find some one whom you trustand he is within your budget and you are comfortable with . – Guru

You are a valuable reader and your participation is needed , Please share any tip here like the one I have discussed , even 1 sentence is worth listening to. Also let me know which was your Favorite Point among these 16 points

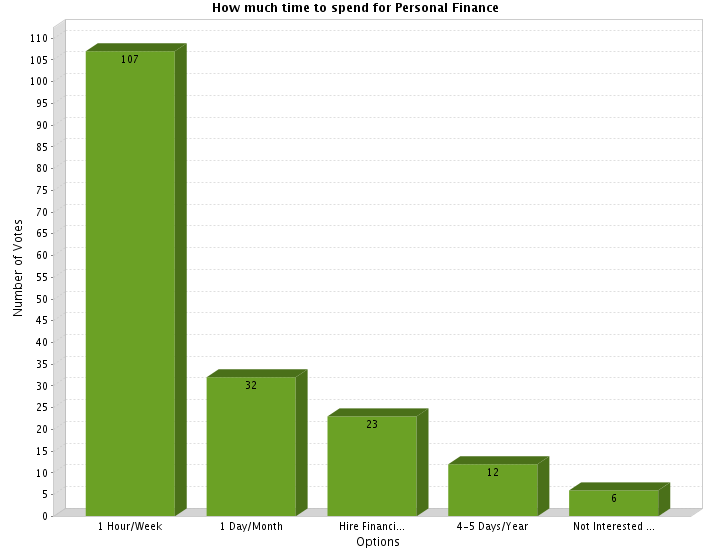

Some months back I wanted to find out how much time a person would spend on his Personal Finance? So I did a poll which asked them this question and gave them some answer options to choose from. Around 180 people participated in the poll. Let us find out what most of the people think about spending time on their Financials.

[ad#big-banner]

Results of the Survey

So the survey asked them a simple question “How much time you would like to spend managing your Personal Finance” and gave them following 5 options

1 Hour/Week

1 Day/Month

I would rather like to hire a trusted Financial Planner

4-5 Days/Year

I have other important things in life

Any Debt funds and Stock Market experts here? Please step in our Forums and help in answering questions like “Best Investment theme for future in Indian Stock Market” and “Debt funds?”

Here is the pie chart which shows all the results

Important Learning’s and Insights

Around 60% people say that they would like to spend around 1 hr/Week. Another 18% said 1 day/month, which is again some how same as 1hr/week in some sense. So I can say that people are interested in spending around 4-5 hrs per month. Personally I feel that 3-4 hrs a month is more than enough. Choose last weekend of month and sit one Sunday or Saturday evening for 3-4 hrs after lunch and look at overall your portfolio. Find out how everything in portfolio is performing, how your mutual funds are performing, track if your investments are growing as per your expectations and plan.

Very small percentage of people said that they have other important things in life than managing their personal finances. This shows that everyone somewhere in their heart recognizes that Personal Finance is an important part of their life. But may be because of ignorance or because its too boring. We don’t get into managing or understanding it and try to ignore it to a level when its too late 🙂

Only a small percentage of people think that they should hire a Financial planner. There are two reasons for this: First, that they don’t feel a need to hire a financial planner and they think that its an easy task which they can do themselves, they think like “why to pay Financial planner?”. Second, that people don’t yet understand what is the goal of Financial planning and don’t appreciate it’s importance in life.

Please put your comments and involve in discussion, What do you think is the best way and time to manage your money?

Note: I feel that I will not be interested in writing a review for any product now onwards. One of the reader feels that I have received Money from Aegon Religare and reviewed iTerm Insurance, see the comment. I don’t say that it looks very unbiased and yes my word seems to be very promotional may be because of my trust in the company and their philosophy.

I am not an emotional person at all but it has hurt me as a writer. I would love to hear your comments on that. If most of you feel the same way feel free to put your comments there without hesitation. If most of the people feel the same way. In that case I will have to refrain from writing such articles, so that it does not put wrong impression. Miss-trust is the last thing I want from readers. If people are not happy, I should also think about removing the ads I put on this blog if it makes people uncomfortable and feel like I am biased. Please accept my public Apology if I have hurt your Trust 🙁

A readers tell me : ” I invested 4 lacs in Sectoral Funds and now its down by almost 45% in one year. Now I need the money for my Sister Education in next 1 month, Should I withdraw it or wait for 1 month ? Manish , please advice ..” I asked “But why did you invest in Sectoral Funds or even Equity” ? Reader : “Because I am a High risk Taker, that’s why”

I call it breach of trust with your common sense. My hands were literally itching to slap this idiot when I heard this. We have to re look “Risk Taking” all together again . I have already talked about Risk here at How much risk you should take and Understanding your Risk Appetite .

[ad#big-banner]

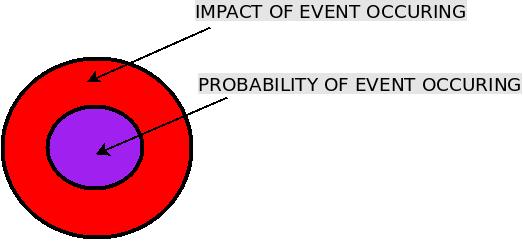

What are the two elements on Risk Taking?

In our country most of the people are willing to take risk. They will say that they are risk takers , they have high Risk appetite , they love challenge, and all kind of nonsense. But they forget to consider their “Ability to take risk”. Its not important enough whether you are willing to take risk or not , your situation should also allow you to take risk. Ignoring your “Ability to take risk” can lead to situation like above example.

So mostly there are two components of taking risk .

Willingness to Take Risk : This depends on our inherent nature, our attitude towards life, finance domain , Knowledge of financial products etc. Our whole upbringing will contribute towards this, because our willingness to take risk will depend on our inherent self , who we are from inside . So you can either be extra cautious by nature and may not be willing to take risks or you can be a big risk taker who is willing to sell his pants and bet money on anything. This is answer to “Can you take risk ?”

Ability to Take Risk : This is the next Important part in Risk taking. Does your situation allow you to take risk or not ? It has nothing to do with your willingness to take risk , you can be very much a risk taker and dieing to bet on the next multibagger or invest in that 100% return a year mutual fund , but you have to consider a worst case at the end. You have to visualize the worst case as if it has happened after you take that risky decision . This is answer to “Shall you take the risk ? “

Boom !! .. So Risk is composed of two parts . Probability of Event occurring should be the secondary thing one should look at and Impact of event occurring should be primary. See the picture below to understand it visually .

[ad#dark_link_unit]

Probability of Event occurring : Most of the people unconsciously think about this. It happens a lot in case of Life Insurance , a general argument is that the probability is very less for them to die and hence they take the risk of not taking adequate risk cover through Term Insurance because they loose money if they don’t die , idiots! (See this post to understand the reason) . Same case with buying a mutual fund which has no credit to itself apart from a 100%return in last 1 yr even though its 8 yrs old fund and have a return of 8.7% since inception. The probability of these mutual funds giving return may be high, but in-case they fail, the impact it can have on your investments can be fatal , especially if you have not considered its impact on your short term goals. So the person in the example above never thought of the impact on his short term goal of Sister Education . He only considered that chances of event happening, which was low (mutual funds going in losses) and if he is a risk taker or not , but he never considered how it will impact his goal. Even though the chances of something bad happening is low and he is personally fine with it mentally by taking risk, the right decision was to better not take that risk because the goal associated with it was very important and the impact is severe overall .

Impact of Event occurring : This is the primary thing one should look at and then take a decision. Until an event happens its very tough to imagine it, that’s the reason you should literally close your eyes and try to visualise a situation and try to feel about it . So if you want to avoid a Term Insurance just because you never get your money back and you want to settle down with a money back policy (Like Jeevan Tarang from LIC) which gives you 10% of the insurance cover you actually require for a premium you can really afford, try to visualise a situation that you died and now your family needs the money after you are gone . Visualise how are they managing , Visualise how your dependents are already emotionally terrified and how they will fulfill their financial goals without you ?

Does it mean we should not take Risk ?

I am not against taking Risk . I love risk taking personally (but my ability to take risk is limited) . We are only talking about taking calculated risk here and being aware of what is the outcome of what we do. Risk comes from not knowing what you are doing. So take calculated risk. Know what can be the impact of taking a decision and be ready to face it when it happens. if you are not happy with the impact, don’t do it . “Not taking a risk” is another very severe risk people do. “Not taking a risk in your life if you are ok with the impact” is equally bad . So not taking risk can also have a drastic impact in your life . Below is a nice video i found for you to get motivated to take Calculated risk .

Conclusion

Recently I came to know that one friend of mine met with an accident while crossing road in Bangalore. He used to cross roads in hurry, because waiting wastes time and meeting with a small accident was not a high probability event ever. Though he was a probability genius , he forgot the impact part of this event . He is safe after this accident but impact could be much worse. Mathematics can never win infront of logic .

Finally at the end I would like to summarize this article in short. We take all sort of decisions in life regarding money , relationship , marriage , health and all of those decision have two parts, First is our willingness and how we feel about it and second is the impact its going to have in our life. This post is to build your FPQ (Financial Planning Quotient , I coined this term 😉 ) and that’s the most important thing. Taking a decision is last thing , understanding what you are doing is of utmost importance . So now their are some questions unanswered , which i will leave to you if its applicable to you .

If you have a Endowment policy , its totally safe and secure , but have you thought of its impact in our life when they mature at the end ?

If you are avoiding Health Insurance of your elder parents because of high Insurance premium , Do you also understand that the Probability of them getting some health problem is very high and the Impact is pretty severe . So when it actually happens you will wonder why you were foolish earlier.

Is the travel Insurance of around Rs 110 worth when you go for air travel within India from one city to another or for that matter from one country to another (charges are not Rs 110 in this case) ?

So if a mutual fund has given 150% return in last 1 yrs, has it happened without taking any risk? and are you ready to face the other side of coin ?

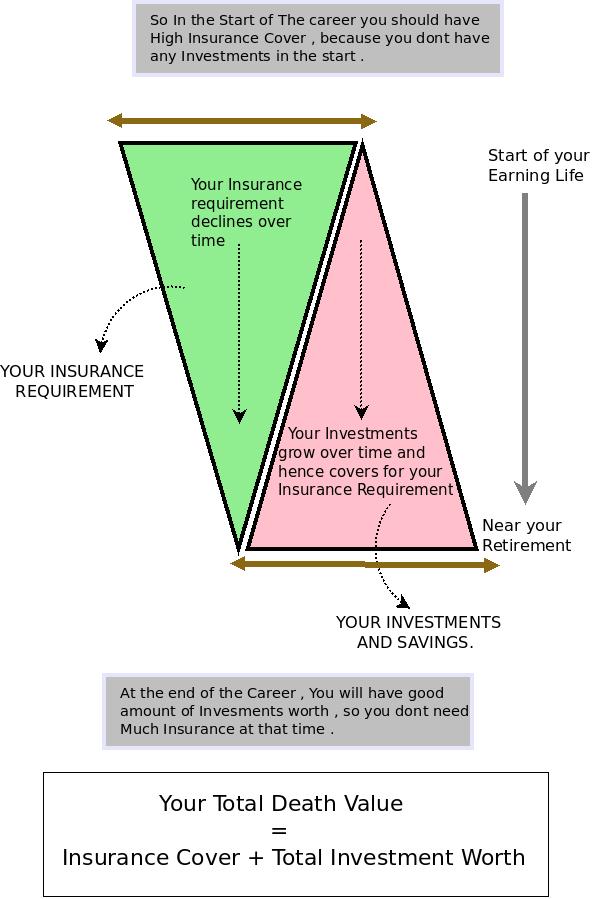

From some last some days I am getting queries that some Life Insurance Policies are not giving cover for more than 65 yrs of age or for Tenure of more than 25 or 30 yrs and why they dont want to take those policies because they want a cover till 70 or 80 yrs of age . So People are confused on which one to take. They generally want a cover which covers them till 70-80 yrs of age or sometimes whole life . Let us talk about till what age should you target your Life cover generally .

Why do we buy Life Cover ?

Now lets talk Logic and think logically , no expertise required here . What is Life Insurance and How much Life cover do you need ? Life cover is to cover the risk of early Death of bread winner and for hedging the risk of loss of income due to the sudden unexpected death of the main earning member . So ideally Life Insurance cover should only be there till the retirement of the earning member , because anyways after that he/she wont be earning , so no one will financially dependent on that person . You only think , If you are 70 yrs old , do you need Insurance cover ? Who is dependent on you by that age , generally ? How many of you are dependent on someone who is in that age ? Are you ?

Hence if a person age is 30 and he is planning to get retired at age of 58 . He requires a policy which covers him till age 58 , not more .. See the Diagram Below …

[ad#big-banner]

So what do we learn ?

Life Insurance is in other terms a replacement of your potential Future earnings. Hence, Insurance amount which your dependents gets should be a substitute of all the amount the bread winner is going to earn in his life time and provide for needs of his Family. Therefore when you are near the retirement and if you die, your potential future income which you were going to bring in the family will be less and hence your Insurance cover at that time should be less . We today have Level Term Insurance where we have the same level of Insurance at that time , which is ok . Note that we also have decreasing life insurance cover and Increasing Life Insurance cover also . So lets see the main points we learnt here

We need to be covered till the time we want retirement .

The day we earn enough money which our dependents need even if you die , you can get rid of your Insurance and then you don’t need Insurance .

So there is no point in having Insurance after your Retirement , unless your intention is to get a big sum of money at the end even if it does not matter much .

This is the main reason why Insurance companies also give Cover till age 65 because that’s the time most of the people on earth get retired anyways .

Whole Life p0licies does not make any sense apart from the fact that they provide pension which is very low. See review of Jeevan Tarang Policy from LIC to understand more on this .

You should have sound Investment Planning so that when you reach your retirement you have grown your Huge Corpus .

Insurance at the end is the hedge against your risk of loosing the earning Potential , its just not a tool to make money on your death .

You have to Notice some imporant point here , Dont take the above diagram by heart and assume that your Insurance cover goes down every year , It can happen that because of other commitments you might have to increase your cover . The main takeaway from this article is that at the end of your career (your retirement life) you should have enough investments and money so that you dont need Life Insurance. Also there can be exception cases where this logic does not apply , we are talking a general case here and not a specific one 🙂 .

Real estate is one of the largest employer after agriculture in India. It is also a globally recognized sector which is witnessing a high growth in recent times because of increasing demands of offices and residential places.

One of my friend has shared his own experience about real estate, let me share it with you.

One of my friends experience about real estate:

“The current market value of my flat in Mumbai is close to 1 crore, I bought it at 28 lacs in year 2000. The returns have been Mind boggling 72 lacs in 9 years, i.e. 8 lacs a year approx. , more than my current salary and now I am planning to invest more in real estate instead of Equity, What do you think”.

A not so close friend was discussing his Real Estate portfolio with me.

He belongs to first category of common sense deprived idiots, who do not understand mathematics well. 28 lacs flat became 1 crore in Value in 9 yrs, the returns are great, but not exceptional enough to make someone eyes pop out.

Simple math’s will tell you that its 15.2% CAGR return over 9 yrs.

Now what’s so great return about this 15.2% Return?

15.2% return over long term is desirable and great and what’s normal return from Real estate in last decade in our Country, The only thing irritating is how people make fuss about it.

Even Gold has outperformed, Gold was $300 per ounce in 2001 and now it’s close to $1100 ounce, that’s 15.5% return, 0.3% more. On the top of that Builders are not keeping their promises of Delivering Projects on Time and with same quality Promised.

Real estate investments have caught everyone’s attention in the past decade and every Tom, Dick and Harry with 5 lacs salary tries to grab a 40 lacs flat. I will try to throw some light on Average Real estate returns in past 8-9 yrs in India.

Coming back to my Friend:

I told him that it’s been a very good return, and I appreciate his timing, good job. But definitely he is bragging more than it deserves. A second person (his friend) suddenly comes to his rescue and challenges me.

“But Manish, I bought a flat in 2003 @20 Lacs with 3 lacs of down payment and rest a home loan. I spent total of 7 lacs till date and the flat is already quoting around 60 lacs, that 40 lacs of profit in just 3 yrs through investment of 7 lacs, that’s 78% return on annual basis”, showing off his fast calculations skills and giving me a “anything-else-you-young-financial-planner” looks his face .

These people are from another category of “common sense deprived and mathematically challenged” people. It is worse than first category. The problem with these people is that they do not understand “leveraging” .

What is mean by Leverage?

A situation of sitting on huge profits by just investing a small amount as down-payment and rest with home loan is pure example of leverage and very common in India, This gives a feel to people that they are very smart.

These people never consider the case when their house value drops by a big margin like say 15 lacs and they have just invested 5 lacs from their pocket, then they are in loss of -300% (absolute). But as you know, investors like to consider a rosy picture; they somehow believe that it can’t be the case with them.

When Real Estate broke in US:

As US citizens who bought Real estate in the middle of the Bubble just because credit was cheap and they could have made a lot of money by taking a Home loan and almost nil Down payment, When Real Estate broke in US, people who has put $10,000 from their pockets for a $4 million house were in losses of $1 million, because they had to pay $4 million as a loan money for something which is now costing $3 million.

That’s an unrealized loss of $1 million in a short time. That’s the problem of Leverage. Investors never think about this, India is a success story and housing is scarce, that’s enough for them to take a chance.

With my amazing quality of self-control, I kept all this in my mind and didn’t argue with him, sometimes your skills of explanation is limited to blogs only.

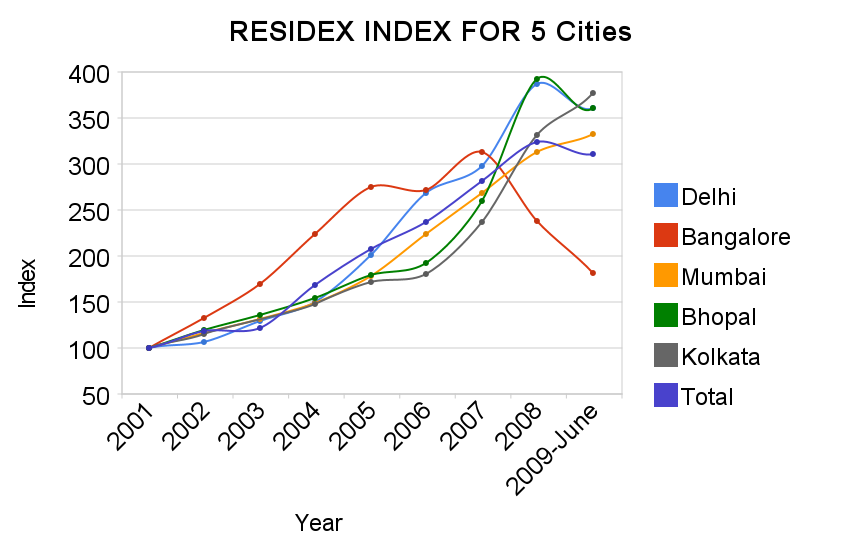

What is RESIDEX?

Don’t feel amazed if I tell you that there is an Index for tracking Real Estate in India. Its called Residex and maintained by National Housing Bank in India. It’s updated once every 6 months.

It covers all the major cities and the sub-areas in that city. The index Value over time will tell you how real estate prices are doing in some area or city.

Please understand that these prices are average real estate prices and not some general case which would negate what we discuss here today.

I don’t know how that is calculated but a common sense way of calculating it is to take a sample of real estate plots/flats in an area (for example 1000 units) and calculating the appreciation in value from last 6 months .

Lets see the RESIDEX values for 5 cities

Here is the chart of the same table

What is the mistake people do when they calculate Returns?

The beautiful mistake which everyone does is that they calculate pure absolute returns from Real estate which is in many lacs of rupees obviously.

So, if a person invested 30 lacs in a flat and it becomes 60 lacs in 5 yrs, they are sitting on a 30 lacs profit.

That’s a lot of money and people are excited to see that much money, but you also have to see that they invested damn 30 lacs !! for that, which is not every one’s cup of tea and the returns are normal 14-15% return/year on investment if you compare it with Gold or Equity.

You could have made more returns if you had invested in Equity (SIP in mutual funds in some top funds) . If you consider the risk taken for the return people have got in Real estate , personally I am not very much excited then, Investors forget the risk taken to get some return and only concentrate on Return part.

See an Article on GFactor , A tool to find out if an investment suits you.

What you have to see is how much return you got from something after adjusting the risk taken for that . So given a time frame of 1 year .

If you do a FD and make 9%, it’s amazing !!

If you invest in Real estate and make 10%, its ok

If you invest in Equity and make 11%, its just fine.. not a big deal

If you speculate in Options for one year and make your money grow by 500%, I would be personally disappointed a lot .

Some smart (second category people) people think that they can buy Real Estate on loan and make 30-40 lacs in 4-5 yrs from house value appreciation, While that is possible and has happened to a lot of them and definitely the return would be amazing.

But this exposes them to a great amount of risk which they don’t understand, its pure leveraging. There are better ways of leveraging than this. This kind of Leveraging is still nothing in front of Options trading in Nifty or some Stocks.

Not that I discourage people from taking a home loan and invest in real estate , but don’t overdo it , and understand and accept the risk involved, be ready for it.

“Risk happens when you have no idea what you are doing”. If you pre-calculate it and consider it, then it’s called Speculation, which is my favorite 🙂 .

An option trading is something I would recommend who have great risk appetite and dream of millions in short span of time, better than real estate.

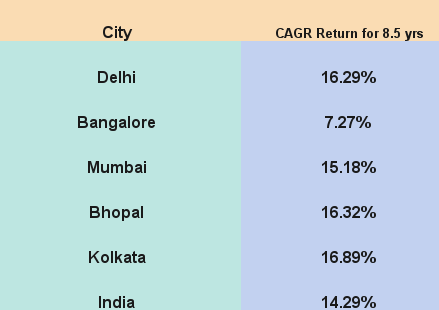

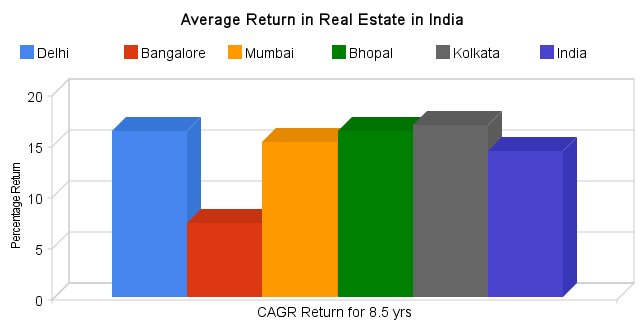

IF we see the above chart of RESIDEX Values (for 8.5 years), you can find out the CAGR return of Real Estate in different cities. Let me show that for 5 cities in India.

Chart f or the same data

Note : I have assigned Index value for “India” by assigning weights of 25% , 25% , 25% , 10% and 15% to all five cities in same order .

What Should you Do ?

First of all, understand that Real Estate is important and you should always invest in it for Diversification of your Portfolio (If you can afford it right now). But that does not mean compromising with your Risk Appetite and investing just for the sake of Investing.

If you want to buy home, make sure you afford it, Buy a 1 BHK which you can afford if you want to live in it. If you want more than 1 BHK, plan for it, take it later. There is no rush. Real Estate is not the last thing in the world.

Don’t feel left out when you see others minting money in Real Estate, believe me they are making similar returns which you can make from Equity, just that the magnitude of profits they are making is high, not the returns on average. So Chill !! .

Note: Understand that whatever we have talked here is based on the RESIDEX index and there will be many specific cases which would make this all talk a nonsense, but we have to look at general case and not a specific case.

Download More data on Residex from HERE (From 2001-2007) and after 2007 at NHB website. Note that you can’t get all data of Residex at one place.

I combined the data from NHB from 2001-2007 and combined it with data on their Website to construct all 8.5 yrs of data. There was a shift in Base year because of which I had to do so.

What do you think about the Real Estate Prices at the moment in India?

I do not feel they are justified and the prices are mainly driven because of unnatural demand created by easy access to Loan. People buy it, but cannot afford it, If things continue for some more years. I would be surprised to see a big bubble burst in India like we saw in 2007.

Leave your Comments and let me know you are reading this blog.

Disclaimer: I have not invested in Real Estate, I am not very much excited about it and I don’t have money for it.

Jagoinvestor is one of the simplest blogs that you can find to kick start your investing.There is such a nice variety of posts that all individuals can get benefits from it.Manish Chauhan the blogger behind it seems to spend a lot of time making his blog perfect for his readers.It is no surprise that his blog is so popular.It is a constant reference for all financial basics, explained in a very light manner.Whether you are a blogger, an investor,analyst or just someone passing by it is definitely worth spending some time here. — Sumayya Shaikh

Jagoinvestor is a great blog on investing. It is extremely rich in content, some of the posts are written extensively. The interesting part of this blog is most of the queries are answered from different posts present here itself. And by the way he’s a great cook…so you can expect a treat J — Charu Gupta

Jagoinvestor blog is an excellent one stop destination for understanding basics on a variety of topics in money management and stock markets.The content is presented in a way that is easy to grasp avoiding the complex lingo that usually scares away readers.This helps in a big way to get those crucial money matters fixed in one’s life without becoming too dependent on other advisors. — Saif Shakeel

This is one of the best blogs i have come across which explains the nuances of financial planning and investing in a way which everyone can understand.Especially the articles on financial planning, compounding power of money and endowment plans are real eye openers. This blog really help me avoid many pitfalls and I have educated my friends also.In a nutshell ,it is a one stop blog for anyone who wants to reap good harvest for their hard earned money. Keep going Manish !! — Swathi Kota

This is a great website ! Thanks for all the information. This website has provided a wealth of information for me and i really appreciate it and look forward to learning more. Now i know no agents can fool me anymore. Thanks Manish for the great job. — Anu Lopez , Dubai

Discover tips on saving money, investing smartly, managing your finances and getting the most for your hard earned money from the Smart Investor blog by Manish Chauhan. This would be the one website I would suggest to anyone who is new to investing or just starting up. — Skandhakumar

It is a must read for the people who want to plan their personal finances using a range products available in market.You would be wrong if you think it is a stock market blog .The title ‘Smart investor’ perfectly suits this blog — Sandip Naidu

I just happened to see Manish’s blog few months ago accidentally while reading other links in famous TA analyst. Manish brings out very simple but important issues on personal finance, stock market, insurance, interest rates etc. I am an Accounts Manager by profession but i never looked in to these aspects in my personal financial planning. After following his blog regularly i could review my financial planning and advise my peers. I appreciate Manish’s efforts — Venkateswara Ravi Prasad

I am putting some questions answered by me to users on “Ask a Question” form . I am putting 3 questions and there answers . If you have any comments or better suggestions please feel free to add as comment . You can see other questions and answers done in the past Here .

You can also ask your questions from other experts on recently started Jagoinvestor Forum

Question 1#

I’d like to invest Rs 5,000 – 7,000 a month through SIP to build a corpus for my child’s education in 20 yrs from now. I think I will need around 20 lakh (which will be around 60 lakh when we count the inflation). I’d like around 80% to go in equities for 1st 15 years and then switch to a more risk averse equation. Which funds do you suggest? Child will be born in Apr 10, can I start rightnow?

I’ve a term plan for 70-80 lakhs. So, ULIP would not be appropriate for this goal, right?

7000 per month can make around 70 lacs assuming 20 yrs and 12% yearly (1%) return . This is as per your requirement , which looks achievable easily , considering you review your investments every year and maintain your asset allocation .. .

You can put some amount (20-30%) in PPF (child name or yours) .. and then rest divided in some 2-3 good funds through SIP .. this should do the job .

you can choose any good fund listed on the article some days back .. You can also look for Balanced funds if you dont want to take too much risk ..

Question 2#

I am planning to invest my money in some CHIT fund scheme where in on an average you get more interest than in SB/Fixed deposits. What is your view on it and can we really trust these chit fund companies.

Following are links of couple of chitfund companies:

Answer 2:

I havent looked at what they have to offer , but without seeing that I am telling you dont invest in these .. Have you every heard these names from more than 3-4 people , Might be they have made some money out of this , but is that under law and are there contracts which are legally binded .

There are cases of frauds in these kind of chit funds . I found some complaints against these chit funds on net .. please go through them .. they might be offering higher returns but always remember that anyting above 8% is with risk 🙂 otherwise everyone will go with them only .. Don’t get into this unless you are ready to loose all your money someday ..

I feel even options trading is safer than these .. because you only loose because of yourself there , not someone else .

Question 3#

I would like to invest Rs.7000/ month by auto SIP ( for 2to 4 Years. My risk profile is moderate and my preference is to invest in Balanced Fund, Debt Fund & Diversified fund. My age is 45 years. Please recommend some of the good fund and amount to be invested per month.

Answer 3:

2-4 yrs is a modetate time frame .. You should go for Equity funds or Balanced funds only if you can take some risk on your investments , Risk does not mean negative return , it means below normal returns also ..

If you are ok to invest 7k per month , then even if you invest in something which gives 10% , you can generate around 4.14 Lacs . If you take risk and target equtiy funds , you can get 15% returns also , which will make 10 Lacs ..

Incase your Goal after 4 yrs can be met by 4 lacs , then i would recommened 10% route which will involve mostly debt funds or Balanced funds .. or Debt funds + Equity funds (30-40%) ..

You have to ask your self if you want your goal to be met or Generate higher returns with RISK 🙂

Look around, the world is lovely and bright

Look around, the world is lovely and bright

Note : I have assigned Index value for “India” by assigning weights of 25% , 25% , 25% , 10% and 15% to all five cities in same order .

Note : I have assigned Index value for “India” by assigning weights of 25% , 25% , 25% , 10% and 15% to all five cities in same order .