I had written my first book “16 Personal Finance Principles Every Investor Should Know“ a few years back and it got very popular among investors. It has close to 130 reviews on Flipkart + Amazon. Now the same book is translated in Hindi Language and is available for sale.

In Hindi it’s called – Ache Niveshak Ke 16 Sutra

The Hindi version is targeted towards those who can read Hindi books and not only for those who cannot read English, because it used enough English words (in Hindi script) at various points.

There are enough number of people in our country who need financial literacy, but they are not able to read English and hence don’t read on internet as most of the content is in English

So if you know anyone who can benefit with my first book in Hindi format. Feel free to share about the book with them

Around 6.5 million Indian Debit Cards have been compromised recently which is one of the biggest security breaches our country has seen to date.

Around 641 customers of 19 different banks have reported frauds worth Rs 1.3 crores in total as of now and after that, all banks started investigating the matter. Some of the banks that are worst affected are SBI bank, ICICI bank, HDFC bank, and Axis bank.

Here is a real incident reported by Vishal Sharma on this article below in the comments section

My card got cloned and my account was wiped out on 5th Sept 2016 by cash withdrawals from china . I immediately informed my bank Standard chartered who then blocked my card. It took 10 days and a lot of following up before they gave me a temporary credit.

SBI alone has reported that it has blocked around 6 lacs debit cards and going to issue new cards soon. This is done as a precautionary measure so that no frauds are done on these 6 lacs cards.

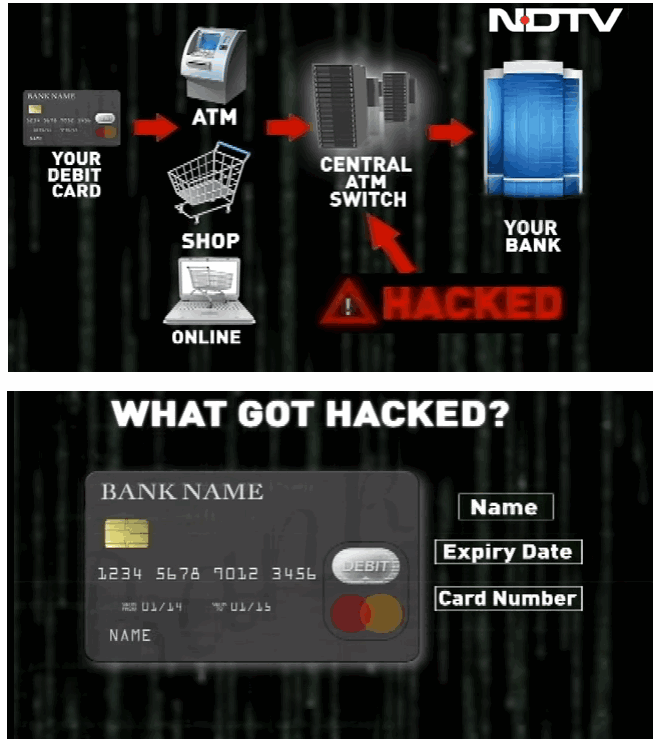

As per the following video, these compromised debit cards were used in the US and China while the debit card owners were in India.

How did this all start?

Around Sept start, various customers started complaining to banks about the fraudulent transactions, and that when banks started reaching out to National Payments Corporation of India (NPCI), which found out that it was a malware-related security breach in various ATM’s and Points of sale systems which were managed by Hitachi Payment Services.

That’s when the banks asked its customers to change their PIN. Banks also blocked cards and started providing the new cards to its users.

The banks are saying that this security breach has happened outside the bank’s network, but still, the investigation is going on right now and more details will come up in coming times.

How did the security breach happen & What got Hacked?

As per the above video from NDTV, almost every detail of the card was hacked like

Name on the card

Expiry Number

Card Number

CVV number

When you use your card at an ATM or a point of sale (in some shop), the data first goes to a central server (central server switch) and that further sends the data to your bank to check if you have balance in your account or not. This central server had the malware sitting and the data was compromised at that point.

Can you take some precautions?

The only thing you can do right now is either change your PIN. Most of the security measures are already taken by the banks, so you can’t do much from your side now other than getting your card blocked (not recommended). You can read more details about this news here

Do you know anyone who faced the card fraud? Can you share that?

What do you think about this issue? What are your views?

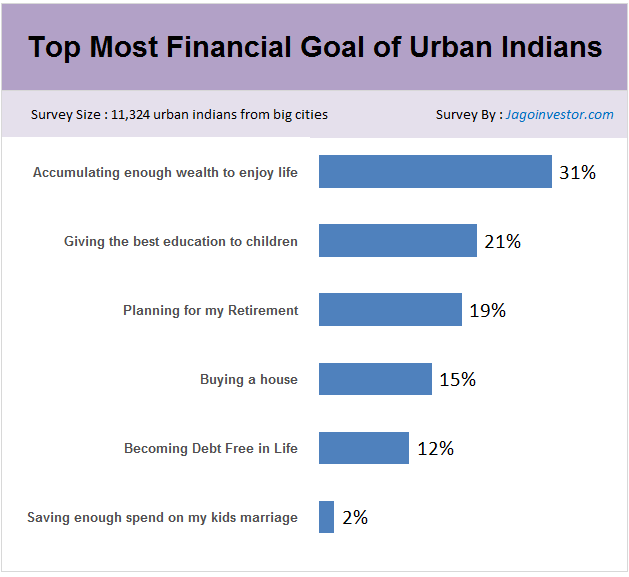

A few months back, I read an article that talked about the biggest financial goals of Indians. As per their survey, the biggest financial goal for 34% of the respondents was “Securing Child Future”. The only issue was that their survey size was just 150.

“Retirement” was the biggest goal for only 2% of the respondents, which means just 3 out of 150 people marked “Retirement Planning” was their biggest goal.

I was somehow not very convinced with their survey size of 150 because it’s not a big enough sample size to decide what most of the people feel. So I thought of conducting my own survey with a big enough sample size, and I was able to get 11,324 survey responses.

The first thing I asked was “Which is your biggest financial goal in life?”

Think about it?

What if I posed this question to you directly and asked – “Which is your biggest financial goal in life?”, what would you say?

I gave 6 options to people to choose from, and below were the results.

Goal #1 – Accumulating enough wealth in life to enjoy

“Accumulating enough wealth to enjoy life” was the topmost goal picked by the maximum people. This was very surprising for me because it was not a small sample size.

We had more than 11,000 people taking this survey and 3553 people out of that (around 31%) chose this option, which shows that somewhere priorities of people are changing these days. Now people want to accumulate wealth not just for retirement, but even to enjoy life before retirement.

They want to travel, experience new things in life, explore new hobbies and spend on themselves. In short, they want to enjoy life before retirement itself and not keep all the money only for retirement.

Goal #2 – Giving the best education to children

The next goal which was voted by maximum people was “Give the best education to their children”. Around 21% marked it as the biggest goal of their life, which confirms that still “children education” is an important and most sought after goal for investors.

It’s a given fact that giving the best education to your children is the best way to care for them and their future. Their life foundation is set by the quality of education you provide for them. It’s surely one of the most satisfying goals for a person.

Goal #3 – Planning for my retirement

I was happy to note that a big percentage (around 19%) said that planning for their retirement was their biggest financial goals. I want to reinforce the point that this survey was taken by people who are net savvy and mostly belong to big cities and earning decent money each month.

If I talk about you – Are you retirement ready? Do you feel you are doing enough for your retirement goal? If you are not sure, You can explore our pro membership program

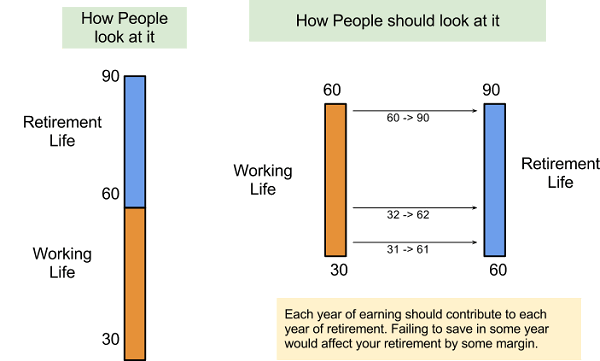

We all have 30 yrs of working life to save money for 30 yrs of retirement on an average. So look at each year of working life-saving as a fuel which will help you each year of retirement. So what you invest in the year 2016 will help you in the year 2046 (2016 + 30 yrs). This concept comes from my book – “How to be your own financial planner in 10 steps”

Goal #4 – Buying a House

15% of people said that buying a house was their biggest financial goal. Given the unaffordable housing prices and the social stigma attached to “owning a house”, I am sure a lot of people feel the “pressure” of owning a house. Only the people who still don’t own home can feel the pressure and the worry associated with it.

No matter how many articles claiming “Renting is better than buying a house in India” comes, still its an emotional decision for people. They feel pressure from family, spouse, and society to buy a house and that’s the reality.

Goal #5 – Becoming Debt-free in life

A big number of investors are getting into a debt trap and a big portion of their income goes into serving the loan or paying off some family debt. It’s surely not a very great feeling to know that a part of your income will just go away somewhere and never return back or form any capital.

A lot of people want to get rid of debt as soon as possible and the high expenses these days make it very tough for someone to close their loan by paying off the debt soon.

Goal #6 – Saving enough money for kids marriage

I am sure we all have this goal in life.

We all want to save some money (or a little) for our kid’s marriage, but 2% of people marked it as their biggest goal in life. I am not sure if they have achieved rest other goals already or not. I do not have much comment on this point, because I don’t want to say if this is wrong or right. Maybe you can share what you feel about it?

So what is your biggest financial goal?

We saw all these 6 goals and how people responded to them. Would like to know what is your biggest financial goal in life and what do you think about this?

70% of people feel that they are “Asset Poor” as per my recent survey.

Are you one of them?

No matter how much you earn or how much wealth you have created until now, you will fall into one of the following 4 categories.

Asset Rich, Income Rich

Asset Rich, Income Poor

Asset Poor, Income Rich

Asset Poor, Income Poor

Suddenly one day, I thought how many people will consider them “Asset Rich” and “Income Rich”? So I thought of creating a survey which asked people just this simple question.

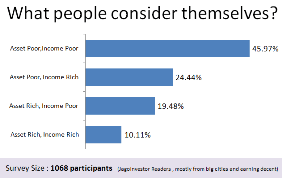

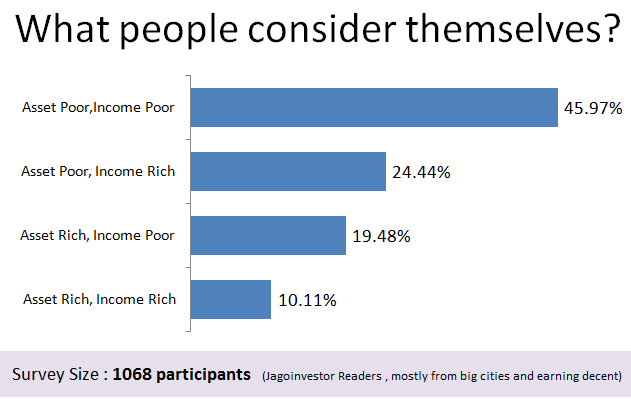

Survey with 1068 people

There is no good information available on this topic, hence I ran a survey for the last few weeks and I got 1,068 responses from various people who visit this blog.

Note that this survey does not represent the general population of the country, but those who work in big cities, have a decent income/wealth (probably) and are net-savvy. Basically our blog readers. So you can safely say that these 1,068 people are like you and me, hence these results are very relevant for you (our readers)

Before I discuss about each category and look more into it. I want to share with you the survey results highlights

Around 70% people see themselves as “Asset Poor”

Around 65% people see themselves as “Income Poor”

Only 10% of people felt they were “Asset Rich and Cash Rich” both

Asset Poor, Income Poor

At the bottom of the pyramid are the maximum people who feel them to be both “Asset Poor” and “Income poor” at the same time. As per our survey, it amounts to 45.97% people, or 45 people out of every 100.

Think about this, a big chunk of people feel they are not earning enough to lead a great life, nor they have built enough wealth to call themselves RICH. This is alarming!

Also note that these people “feel” themselves as Asset Poor, Income Poor. So it’s all about their own perception about themselves. So even a person earning Rs 50,000 per month might feel he/she is “Asset Poor, Income Poor”. It has a lot to do about your relationship with money.

I think people falling in this category must be highly stressed as they might be surrounded by various people who either own some properties or if not, at least earn decent enough to enjoy various materialistic things in life.

One of our old surveys shows that every 1 out of 2 people in India is stressed because of money related matters.

Asset Rich, Income Poor

This is an interesting category of people. A lot of people are asset rich, but Cash poor. You must be wondering how?

The best example of this category are some senior citizens who do not have any source of income, but they have good assets. However, they are either living in that property or it’s used by their kids now.

Another example for this category is families, which own ancestral homes in cities that were bought by their parents, and now those properties are worth crores, however, they still don’t have a decent income source. They might be into a small business or some kind of job, but they still earn enough to run the house.

Also in various smaller cities, there are many people who have a great amount of wealth, but their lifestyle if base minimum and they don’t spend enough on themselves. My own best friend who lives in Varanasi has wealth upwards of Rs 10 crore (total property worth), but they still run around all day each month trying to earn enough to meet the ends meet, because they can’t sell their lands just to enjoy life.

“What will people say”- is what holds them!

Asset Poor, Income Rich

Now comes the third category where 24.44% of people fall. These are mostly those people who have recently upgraded from the middle class to the higher middle class when it comes to income.

They are earning good salaries like 1/2/3 lacs per month (mostly in the IT industry), but they are still struggling to own a house of their own or to create any sizable wealth. Even if they own a house, it’s on a huge bank loan which ultimately makes them just rich on the left side of the balance sheet, but not in totality!

This category finds it very hard to build assets because their expenses are very high because of their lifestyle. As per this article which says “America is full of high-earning poor people”, most people earn a decent income, but they fail to save enough money to build wealth. I think many people in big Indian cities are going on the same path.

Asset Rich, Income Rich

This is simply the people who are at the higher end of the pyramid. With their several years of experience and discipline, they have created good wealth and also earn decent money each month. They are free from debt now (mostly)

A very high-level description for these people would be those who have

A house of their own without any loan

A good car without a loan

A stable and secure income stream of upwards of 1-2 lacs per month

Enough money lying in bank accounts or mutual funds/stocks

So what makes you Poor or Rich?

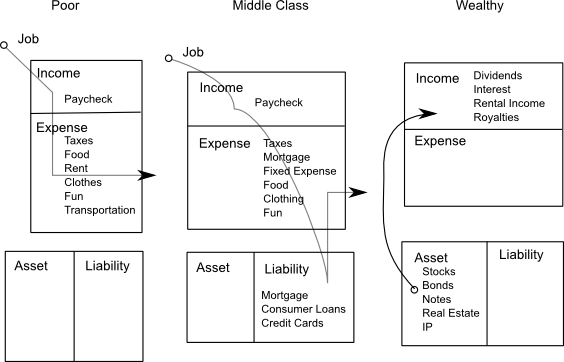

It’s all about how you structure your financial life and what shape you give it over the years. There is a big difference in the cash flow of Poor people and Rich people and the below diagram shows it in a very simple way.

Poor people – Earn and simple Spend that money on expenses, they keep doing this all their life and never build any assets

Middle Class – While middle class earns better income compared to poor people, still, they create enough liabilities which eat up all their income, if anything left after expenses

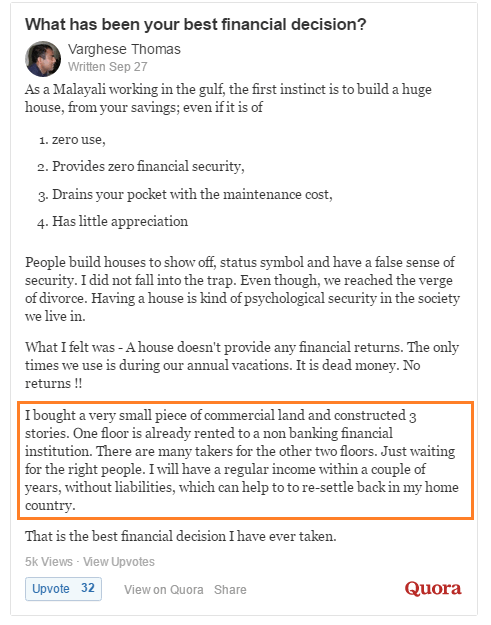

Rich People – Rich people do something different, they focus on creating assets that generate income for them over the years. It can be dividends from stocks, mutual funds or building real estate which gives income. I recently came across a very example of how rich mindset works and here is an example from Quora, where a guy “Varghese Thomas” is sharing his personal life example.

I know he is an NRI and some people might say that because he is an NRI, it’s easy for him to think like that, but still it’s all about the mindset and how far your thinking goes.

How to become “Asset Rich”?

While this is a topic which calls for a separate book, I will want to give an attempt to talk about it briefly.

To become Asset Rich, you need to first become Income Rich. There is no other option here, unless you have a rich relative who might leave his fortune to you 🙂

So you need to first move to the “Income Rich” category from “Income Poor” . When I say Income Rich, I mean you earn enough money each month, which helps you to save good amount of money after all your expenses and EMI’s. Because unless you keep investing good amount of money each month, becoming rich will be tough.

Even if you are generating very good returns like (12% or 15%), you will not build enough wealth if you do a SIP of Rs 3,000 per month. I hope you get my point.

The amount or quantum of money you put in each month is highly important.

So you need to upgrade your skills, work on increasing your income, save a good amount of it with discipline and take decisions which at least doesn’t lose you money, if not make wealth for you. I don’t want to go into details here, because this is a big topic.

What are Assets and Liability?

I really feel you should once watch this 2 min video from Robert Kiosaki where he explains about Assets and Liabilities. This will give you some really good background to start thinking how you want your financial life to shape up.

I hope you got some good insights into how people think about themselves and their financial situation. We would like to know what is your plan for moving to the upper category in the future? Please share more insights on this topic in the comments section.