So, you have been reading a lot about CIBIL these days and you have got the impression that having a high credit score like 800 or 850 is a key to get your kind of loan?

If that’s the case, let me break your myth that having a high credit score is not a guarantee that you will get a loan from a company. Look at the following comment and you will understand what I am talking about

Dear Sir,

I have taken the PL of Rs.1.5 L from HDFC and get settled of amount Rs.15 k in 2013. In March 2015, I checked my CBIL score, it is 813 however loan status is settled.

Recently I applied for PL of Rs.5 L in ICICI but it gets rejected based on previous settled loan. I don’t get this, when my CBIL score is 813 then how its get rejected. Kindly guide me how could I get PL as its v.urgent for me.

Regards

What is CIBIL remark and score?

In case you are new to this CIBIL concept. I suggest you read this article or watch this video below from the Cibil team.

It will help you understand the concept of the credit bureau and credit report. Once you view the video, then you can move ahead.

Your credit report remarks matter more than your Credit Score

Let me share with you a personal experience. My brother had taken a bike on loan a few years back and I was with him in the Bajaj showroom where I asked the executive if they really looked at CIBIL score (CIBIL was new around that time). The executive shared with me that they don’t look at a credit score, instead, they look at the remarks on the report and that is what matters most along with your other factors.

It was really a new thing for me to know that a credit report does not have that much Importance compared to the credit score in your loan approval process.

Credit remarks vs. Credit Score

Let’s understand both the concepts and the meaning of these two things

What are Credit Remarks on your report?

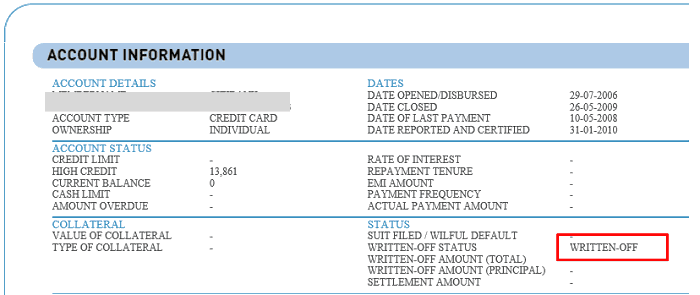

If you have 3 different kinds of loan accounts (1 home loan, 1 car loan, 1 credit card). In that case, you will have the remarks for each of these loan accounts and the current status. Imagining you have closed the loan accounts, the remarks may say “Settled” , “Written Off” or “Closed”, out of which the first two are bad remarks. At times, if you are not able to pay off the loan, the loan guys will try to persuade you to settle the loan with a lesser amount and close the chapter.

However note that it’s a short term solution to just get away with the problem. Eventually, the remark will be marked as “Settled” or “Written Off” and in future when another lender looks at your report, he will come to know that you didn’t pay the full/partial amount of loan outstanding.

At this point in time, even if you have great salary or a good credit score (we will look at it below), they are going to reject your loan application.

What is a Credit Score?

Credit score is a number between 300 and 900, which signifies your credit worthiness and how likely are you to default on paying your loan installments. A low credit score means that there are higher chances of you defaulting on the loan payments. This credit score calculation is a trade secret and no one knows the algorithm of how it’s calculated, but there are various factors that are considered by the credit bureau which its calculation.

So one can still have a high credit score (the chances of paying their future EMI’s regularly), but still their past remarks will have a greater impact on their loan evaluation process. While a score of 750+ is desirable (as per CIBIL around 79% loans were given to those with CIBIL score of more than 750), don’t think that just because your score is higher than 750 means that you will surely get a loan.

In the same way, if yours is less than 750 (like 600 or 720), but if your credit remarks are clean, you will most probably still get the loan, considering you qualify on other parameters like (salary, other EMI etc)

So while credit score gives a future insight, the credit remarks gives insight into the history.

4 other factors because of which loan application rejection can happen?

- If you are a guarantor for a loan which is already defaulted. Though you have not taken the loan directly, your application might get rejected if you have become the guarantor of a loan by your friend/relative and they have defaulted.

- If you are too dependent on credit already (means if you are over-leveraged). Imagine if you are already paying 50% of your income on EMI’s and have many different kinds of loans running. Even then your application might be rejected.

- You don’t have enough tax payment history. If you have not been paying your taxes regularly, then it’s tough for the company to ascertain your paying capacity, hence, make sure you file your returns regularly and properly

- Too many unsecured loans, if your loan portfolio has too many unsecured loans (credit card, personal loans) then it’s not a good sign and makes you look a credit hungry customer. This might lead to rejection.

So what’s the learning?

So what’s the learning out of this?

The main thing you should focus on is to make sure that your credit report does not contain any bad remarks and if there are any, then you should take actions to rectify it. It will by default help you in improving your credit score. Don’t get obsessed with increasing the credit score. If your credit score is above 700 and your report is clean, you are 95% good to go. Beyond that, if your score is higher, it’s a great thing. But don’t over-focus on it.

Before applying for any kind of loan, make sure you apply for your credit report and score before few months and analyze it to find out if you need to fix it or not. Over the long run, just keep paying your dues on time and do not abuse your credit utilization and you should be good in the long run.

Let me know if you have any queries about this.