We are happy to announce, that our next full-day workshop in Pune is scheduled on 20th May 2018 (Sunday).

We invite you to come and participate with your friends and family. It is an opportunity for you to block one full day for your financial life where you get a chance to work on your financial life. We do not teach tricks and tips to build wealth, but in fact we help you to discover your own personal process of creating wealth.

Why we do these kinds of offline event/workshops?

We do these events because they make a positive difference in people’s financial life. The conversations we do, create an impact on people’s thinking and they are able to re-invent themselves as an investor. The event is not about financial products and numbers, it is about learning and mastering the principles of wealth creation. It is about learning realizing your past mistakes and about creating a powerful future for yourself.

Register for Pune workshop on 20th May 2018 (SUNDAY)

Ticket Type

Pricing

Ticket Link

Single Ticket (Early Bird)

(First 10 tickets only)

We have also created a facebook event for this workshop. Do click on Interested if you want to join it.

Why should you come to the workshop?

You will learn how to improve your financial life with your current set of resources and income.

You will learn how to plan for your financial life goals

You will interact and learn from other’s people’s financial life

You will dedicate one full day to get better with money management

You will learn to add new dimensions to your financial life

To understand that personal finance can also be fun

To give a whole new direction to your financial life

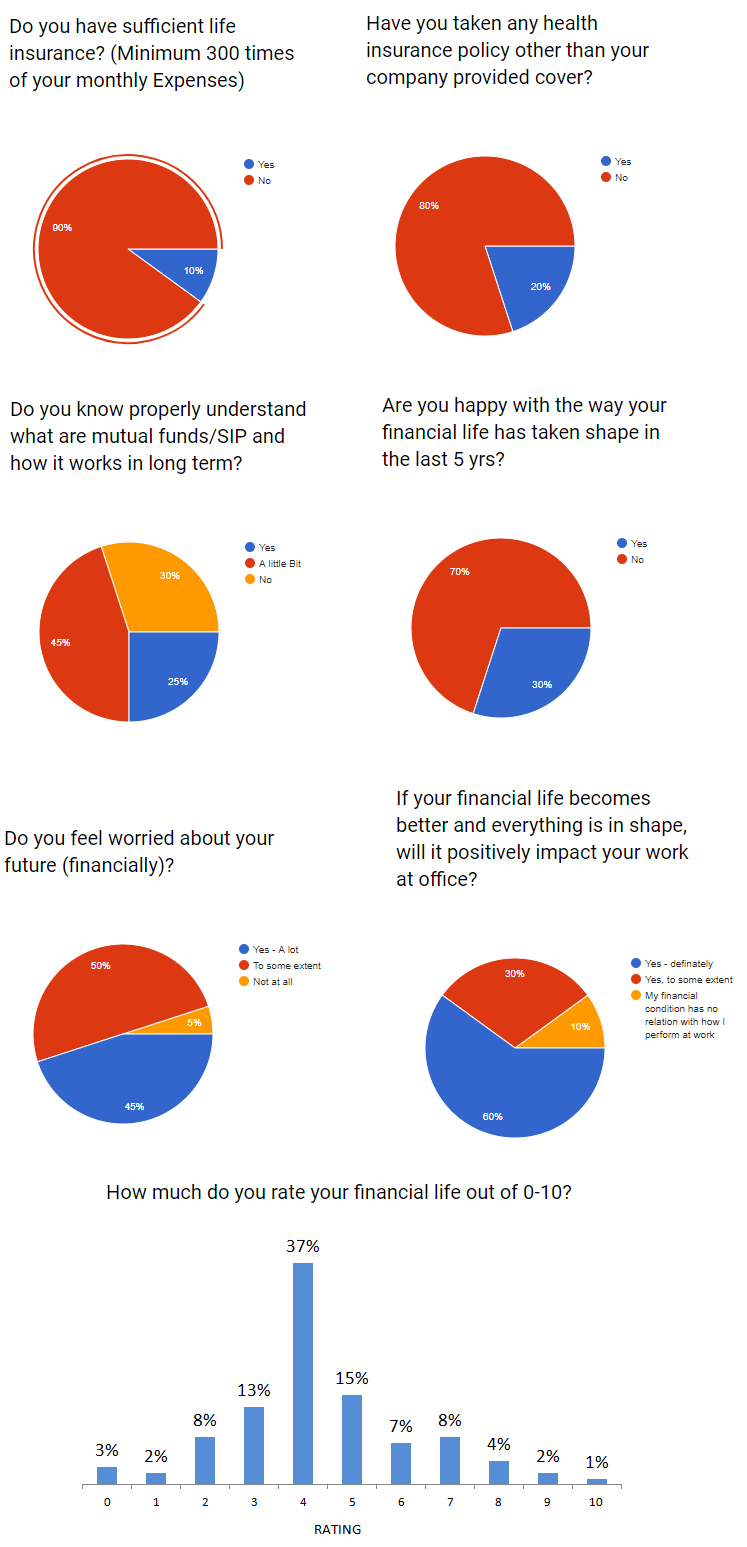

Let us share our survey findings (Survey was done on 10000+ Investors)

We did a survey with more than 10,000 investors some time back and here are the results of the survey.

The survey is LOUD and CLEAR – It’s time to re-invent

The theme of our workshop is going to be re-invention, you will get a chance to examine your financial life and will explore ways to re-invent your financial future.

The results from survey seem alarming and the best gift we can to the investor’s community is our workshop Your real wealth is your clear mind as once the mind is clear all the good decisions will happen on its own, the workshop will leave you with a clear mind and with new openings of action.

Our Vision to do Workshop in different cities and organizations

This year we intend to do the workshop in maximum cities and in more and more organizations. The content and design of workshop are powerful and we want the workshop conversation to touch more lives. If you want to do a workshop in your city or in your organization you can share your details in the below Google form, we will get in touch with you at the earliest.

It’s time to add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and each time it has been a very fulfilling experience for us. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation.

This time we want more and more couples to participate so that they can get on the same page when it comes to personal finance. It is extremely important that the husband and wife both take an equal interest when it comes to money management. We are offering a special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct is highly interactive, it has lots of activities and fun exercises that help you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short, there is something for everyone in this workshop.

Super Bonus Launch of Finscore Tool

We will be launching our newly designed scoring system with all our workshop participants. The scoring system is going to be a game-changer for many investors. It has taken around 6-7 years for us to design the whole system and we are all set to raise the curtain. We are so happy to share our scoring system with the investor’s community, it is simple, easy and extremely powerful in nature. It is more like a technology to live a good financial life.

After the workshop, participants can sign-up for our paid service to get complete access to the tool. We will give free financial health check-up access to all participants so that they can check up their scores.

The workshop is strictly for investors and not for advisors or finance professionals. If any advisor/IFA/CFP is found to be registering for the workshop, he/she will not be allowed to participate.

If you have never participated in any personal finance workshop let this one be your first experience. If you have any questions you can write in the comments section or you can email on [email protected]

Do you avoid various actions in financial life which are often suggested as the “right decisions”?

There are countless articles and videos these days which tell you that it’s important to have sufficient life insurance and health insurance. One should start investing very early in life so that they can create some good wealth to take care of their future.

Like these, there are various things that are mostly the building blocks of a good financial life. But often investors avoid taking those decisions. The biggest reason why it happens is that we are all lazy investors who focus on NOW rather than FUTURE.

If it’s not creating trouble for us right now at this moment, we keep postponing it and underestimate the trouble it can give us in the long future. In short, the future trouble or problems we will face is imaginary at this moment.

So today I thought I will talk about the impact of these decisions and how it can trouble you in the future. Let’s start

Mistake #1 – Not buying a health Insurance

Today I will not talk about what will happen if you buy health insurance, but I will talk about what CAN happen if you do not buy health insurance.

At one point in our life, when we start our career, we have ZERO wealth. There is no money in the bank account and we struggle too much to start saving. Our salaries are less and we have just started our career.

Our salaries are not much when we start our jobs, but our expenses start building up. Rent, groceries, Petrol, eating out and whatnot.

After a few years, suddenly we realize that we are just living paycheck to paycheck and we are not saving any money. Years pass by, but you have nothing worth calling “Portfolio”.

In fact, it might happen that you are in credit card debt now and you are wondering if you will ever be able to retire RICH!

Then comes, a point in life when you realize that it’s enough and now you need to start saving money for the future no matter what. Enough is enough.

You start your first investments

Somehow you start your first Recurring deposit or SIP in mutual funds. You start with a basic Rs 2,000 per month. A few months pass and you are happy to see that you have some savings now at your end.

You are excited and want to make sure you do not break this newborn habit. A few years pass by and you have done it! .. Congrats, you managed Rs 5 lacs in your portfolio. It took some years and lots of commitment to reach there.

You feel like a winner and you now truly understand the joy of having a big amount lying in your bank account. What a relief and feeling of safety it provides.

You are even more committed to save now you plan to reach the target of Rs 10 lacs with the next 2 yrs.

You are happy and life is all good.

Then the bad day happens

Then one day, while going to the office, some Rowdy Rathore in a Bolero who is trying to race his car with some unknown person hits your bike while you were on your way to the office. It’s a major accident. You can imagine some other medical emergency in a family if you do not like this example.

The hospital bill comes to Rs 6.3 lacs. There was a surgery done to make sure you survive and you were in a good hospital for 12 days.

You had to take out all your money from the bank or mutual funds and additionally, you have borrowed from your relatives/friends or swiped your credit card to complete the bill payment.

After a few months, you are back to life. But your financial life is back to square one. Your wealth is eroded. You did not protect your wealth from medical emergencies.

You did not take health insurance

We do not think like this about health insurance. We never see health insurance as a financial product that helps us to protect wealth. Buying health insurance is all about transferring the risk of paying the hospital bills to someone else. Health insurance does not protect your health. It can’t.

Remember, starting your savings and investments is easy (not that easy), and consistently doing it for many years it very tough.

Those investors who do not take health insurance over-focus on what is NOT GOING TO HAPPEN. They say things like

What if I never get hospitalized?

What is I drive carefully and never get into an accident

I exercise and eat healthily, why do I need any health insurance?

My company provides health insurance, so why do I need additional health insurance

I will waste my premium if I don’t get hospitalized for next 30 yrs

Sorry, but you need to focus on WHAT IF IT HAPPENS, rather than what if it does not happen.

Note that a health insurance product gives you a protection cover of a big amount every year. So if you buy health insurance with cover of Rs 10 lacs sum assured.

Click here to buy health insurance from our Trusted Partner (special collaboration with Jagoinvestor)

What you are accepting by not buying health insurance?

So finally, as a conclusion – When you do not buy health insurance, you are saying that I am ready to pay the entire hospital bill out of my wealth, every time it happens. I will take the risk of getting my wealth eroded by medical issues.

Mistake #2 – Not saving enough money for future

The next thing I want to talk about is not saving enough money for the future.

You have a nice car, you eat out often and you are able to take care of all your house hold expenses right now. You also take short vacations often. This is all well and fine if you are saving enough for the future. But if your expenses are almost equal to your expenses, remember that one day will come when your income is going to stop permanently.

That will happen when you reach around 60 yrs. And you will probably live for another 30 -40 yrs (wish a long life to you)

But if you do not have enough wealth created by that time, the journey ahead will not be filled with fun. Imagine you retire with just 5 yrs worth of expenses in your bank account.

How cool is that?

How will you feel to find yourself in a situation where you know that you require 100 units of money each money to live a comfortable life which you desired, but your wealth is only capable of providing your with just 40 units of money each month? Or 8 units?

You will have to choose between a vacation and food on the table. Forget food on the table, you will have to choose between “cheaper” vs. “what you like” each time you think of what to cook for dinner.

You will have to decide each time if you want to travel by air or sleeper class on a train (I love both options)

You might have to make excuses each time your friend circle plan a holiday trip

You might have to constantly worry if a restaurant bill will be too much?

It might sound very dramatic right now hearing all this, but the truth is that the future is imaginary and it’s tough to plan for it. I am not saying that you should create enormous wealth by compromising today, but all I am saying that you should be well aware of how your decision of not saving enough today will impact your future.

A little financial planning helps

Most of the people who come to us for financial planning are already late in investing. We can’t fix it fully, nor do we give them false promises that they will retire as a millionaire. But we make sure that they make the best of the years ahead.

We make sure that whatever suggestions we make to them for their wealth creation aligns with what they want in life ahead. We plan for their goals and create a decent strategy to reaching those goals.

Saving money right now does not give you any joy or benefit right now. Saving for the future also means cutting down on something today hence we don’t do it. Saving for future means.

Cutting some part of your shopping today

Cutting down on your eating out today

Compromising a bit on your entertainment today

Buying fewer gadgets today

Buying fewer clothes today (please raise hands, if your closet has something which is not used since last year)

What you are accepting by not saving enough for the future?

So finally, as a conclusion – When you do not save enough for your future, you are saying that I am ready to be dependent partially or fully on others for money and my day to day expenses. I am ready for a lifestyle which might be very different from today. I am ready to live a life which will come with daily struggle and stress about money.

Mistake #3 – Not having a term plan

Accidents are called accidents because they are not planned nor they are expected to happen.

Why are we so over confident that nothing can happen to us and bad things happen only to others?

We all have recently heard about the Kamala mills fire news. Almost a dozen people lost their lives in that fire. One couple who lost their lives were actually sleeping when their friends asked them to join the birthday celebration of some other friends. They woke up and went there, but never to return.

Life is LONG

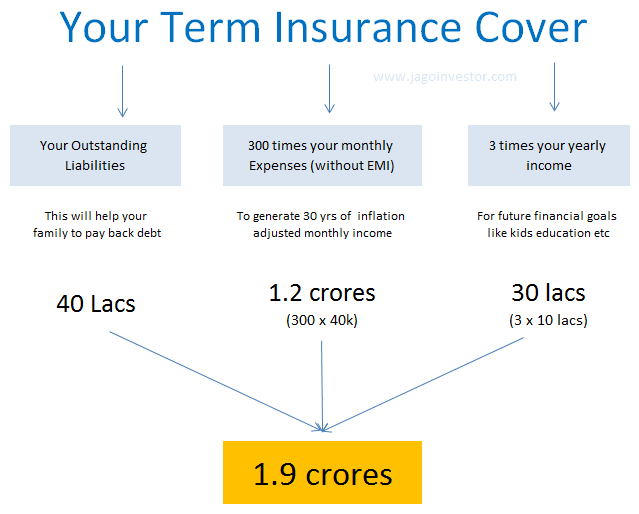

Life is very long and your loved one needs a lot of money to live comfortably. We need to make sure that we cover this risk by taking a sufficient term plan for which we need to pay a very small premium.

A family whose expenses is around 50-60k per month needs close to 2 crores of life insurance.

If you leave behind a family who is weak financially, you are leaving them with the risk of being dependent on others for their survival. While you can’t prevent the emotional loss, neither you can minimize it. You can surely take action today to minimize the financial impact.

If you have enough wealth and assets which will help them financially in the future, then it’s totally fine to not buy a term plan. But if you are someone who has no assets or wealth, you need to make an arrangement for the worst case. There is a famous saying – “You don’t buy a term plan because you will due, but because your family will live”

Answer this: In your absence (and the money you bring on the table)

How will the next 30 yrs of household expenses come from?

Who will fund for your kids education

Who will repay your debt?

Who will pay for all the desires your family has?

Where will they turn up to when they need money in cases of emergencies?

What you are accepting by not buying sufficient life insurance (assuming you don’t have enough wealth)?

So finally, as a conclusion – When you do buy sufficient life insurance for your family, you are saying that you are ready to let your family face lifelong financial suffering. Your kids and spouse + parents might be suddenly forced to live below the standard of living they are used to. Your kids might not get the same quality of education which would have been possible if you were there.

Mistake #4 – Over investing in Fixed Deposits/PPF

For some people, fixed deposits are the only way to invest their money. It’s a safe and secure way of investing. Our parents did it and there is a visible problem when you invest all your money in fixed deposits or saving bank account (or PPF or Post office schemes)

After all, you park your money in FD/Saving bank and it grows in value over time. What’s the issue in that?

The biggest problem is that your investments do not beat and outgrow inflation over the long term. You get a feeling that your investments are increasing, but your purchasing power does not increase. Its goes hand in hand with inflation.

So if you were able to buy 1 loaf of bread earlier, even today you will be able to buy the same 1 loaf of bread with the money you had invested in FD.

Your life style will remain the same over the years because your money is just growing as per inflation. To counter this, you need to invest your money in something which counters inflation, like equity. It can be stocks or equity mutual funds.

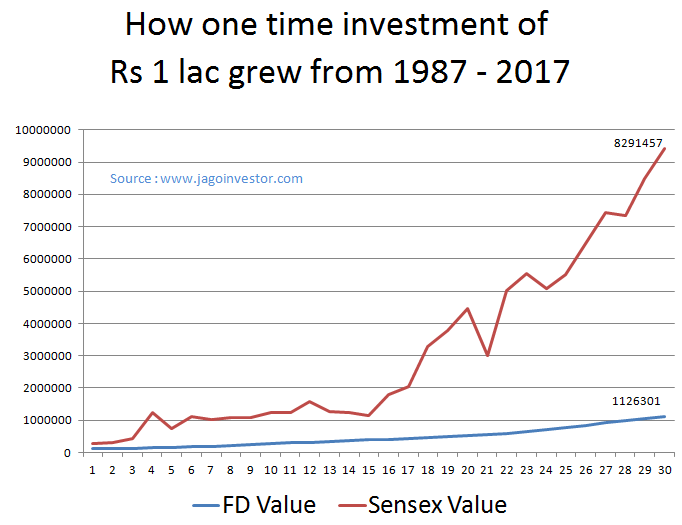

Here is an example

Imagine this, Rs 1 lac invested in Fixed deposits 30 yrs (year 1987) back is worth Rs 11.3 lacs today (the year 2018). Don’t jump out of excitement. 11.3 lacs today is worth Rs 1 lac 30 yrs back in real terms.

Whereas, if one had invested the same Rs 1 lac into Sensex 30 yrs back, it would be worth 83 lacs today, that’s close to 7-8 times than FD

Consider two friends who were 30 yrs old in 1987. They were fresh into jobs and started their career. One invested 1 0 lac into FD for his retirement and other one invested 10 lacs one time in Sensex.

One retires with 1.1 crores in hand and other one with 8.3 crores. One of them will get a monthly pension of 7-8 times compared to the other one. Just image the difference between them and how they will feel about it.

What you are accepting by investing only in Fixed income asset class (like FD, PPF, Post Office)

So finally, as a conclusion – When you only put your money in fixed income instruments all your life, and refrain from equity asset class, you are accepting that you will take the safe and secure path which has no growth element in it. You are ready to retire the middle class itself. You are consciously accepting that instead of 8X money, you are ok with 1X money because you are not ready to take the risk.

Mistake #5 – Taking too much debt in your life

There are two kinds of investors – One who buy things in life mostly with their saved money, and other one buys most of the things with their future income – i.e. LOAN

When we start our career, we have no idea what a devil is this credit card or a personal loan. It’s as simple as BUY NOW and PAY LATER. How bad it can be after all?

We feel we are in control of ourselves self and we will take rational decisions when it will come to money. We think we are not going to make stupid decisions. But only after years, we realize that the game is not so simple.

Once you depend too much on loans and credit cards, it becomes your way of life. You keep shopping and buying things you desire on debt, thinking that you will pay it later.

It’s all about falling for instant gratification and there are millions of people in India who are deep into debt. There are people who have bought cars which does not justify their pay package, and many people have home loans which are much bigger that what they can truly afford.

You will be the slave of MONEY

The biggest problem with this approach is that you become a slave of money. You have promised to pay all your future income, which is uncertain and which is not even earned.

You will be now going to your job to earn money, not by choice but a compulsion. Also, you are going to take less risk in life because you can’t afford to take much risk anyways now. If you do not like your boss, you need to keep quite because there is a sword of EMI hanging. What if you do not get an appraisal? What if you lose your job?

Also, you will be compromising with your wealth creation, because you have already consumed most of your future income through loans. Whatever you earn has to go in servicing your EMI’s and current expenses. There will always be less money for future goals, and this thought will keep on haunting you.

Here is a small 6 min short film on the debt trap which happens by use of credit card. It’s quite a simple short film but gives the message

Do not spend the money you don’t have

We all take a few loans in life and that has become the way of life, which is ok. I am not the person who advocates the concept of “Never take any loan” . But surely you need to control it and define the boundaries. If you get into the debt trap, it will be very tough to get out of it.

There are few signals which will tell you that you are too much dependent on debt, they are

More than 50% of your income per month goes into EMI

Your loan outstanding is more than 4 times your yearly income

You have more than 2 credit cards

You have a revolving credit card from last many years

You have too small savings even though you have worked for many years

What you are accepting by taking too much debt

So finally, as a conclusion – When you start depending too much on debt and overdo it, you are accepting that you will be working for money out of compulsion to repay it back. You agree to be constantly living under pressure and feeling frustrated about your debt. You agree to be living a life where you will not be able to take much risk and do what you wish for because you have EMI’s to take care about.

Do let us know how many mistakes are you committing right now in your life? Was this article useful for you?

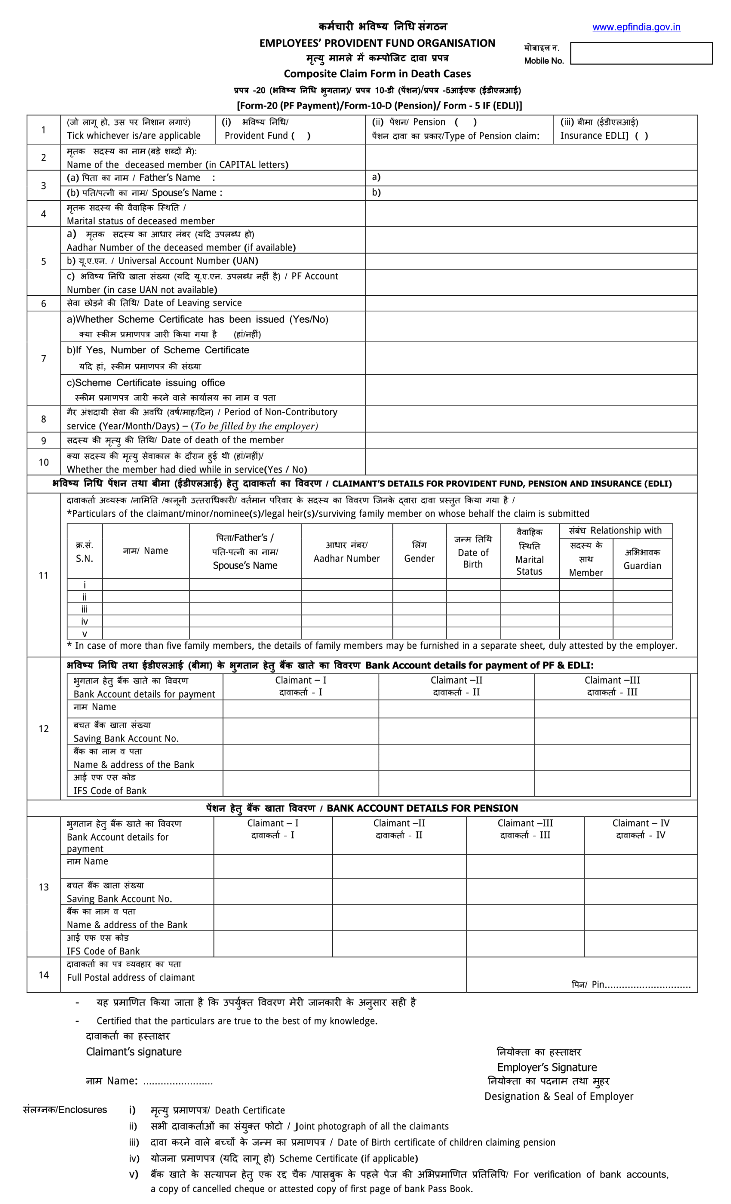

A lot of EPF accounts are lying unclaimed after the death of an employee. Families have no idea how to claim the EPF money and what is the process?

Today I will share with you how your family will be able to withdraw the EPF account money in case something happens to you.

How to claim EPF money after the death of an employee?

Once a person is dead, the beneficiaries of the dead employee can proceed with the process of withdrawing the EPF money. The first right is of the nominee who was mentioned in the EPF by the account holder. Mostly it’s a father or mother as most of the people are unmarried when they start their careers and they mention one of the parents as a nominee.

Here are the documents one need to submit

[su_table]

1

EPF Composite Form

The first form is called the Composite form for death cases, which is a single form to be filled to claim EPF, Insurance money and any pension amount.

2

Death Certificate

You need to provide the death certificate of the EPF account holder who had died.

3

Birth certificate of children claiming pension

If there are children of the deceased who are claiming the EPF, they need to provide the birth certificate for each of them

4

Joint photograph of claimants

One has to provide a joint photograph of all the claimants together. This is to make sure that there is no fraud in the name of claimants.

5

Copy of cancelled cheque or attested copy of the first page of Bank Pass Book

To make sure there is proof of the account where the money is is going, one has to provide a copy of the cancelled cheque or the first page of the bank passbook

6

EPS Scheme certificate (only if applicable)

This is a certificate which is a document that has all the details of who will get the pension etc after the death of a member. It’s issued by EPFO and this is applicable only when there is a pension part applicable.

[/su_table]

How does the EPF Composite form look like

Here is a snapshot of how the EPF composite form in death cases looks like. This is the main document that one has to fill if they want to claim the EPF amount.

As you can see, that the process of claiming EPF is lengthily and painful, you should make sure that you make it easy for your family members to claim back the EPF money. Hence please do the following things

Keeping all of your important information in one place which is safe and accessible to your family

Please update the nominee of your EPF to someone whom you really want it to go

If you have a WILL, mention the beneficiary who should get the EPF money

I hope you get a clear idea about the EPF claiming process now. If you have any query please reply in the comment section.

Today we are going to look at the Money story of Mr. Rajat Agarwal. He has been kind enough to share his story in detail and we all will learn some important aspects of financial life from his sharing.

Over to him…

I was born in 1982 into a wealthy Marwari joint business family, with combined sales of about ~5500 Crs (as of 2017). My father retuned to India in 1980 after completing his MBA from the University of Austin, Texas and was asked by my grandfather to start an aluminum extrusion company, which was founded in 1981.

The aluminum business was in addition to the joint family’s other businesses like – Transportation, Gases, Steel, Power, etc. My mother was from an average middle-class family which helped keep my brother and I grounded in reality while growing up. Even though we had domestic help all the time, we were taught to do our work on our own and not depend on anyone for daily chores.

My father always made it a point to schedule monthly short vacations and longer annual international vacations and spend a lot of time with the family each evening – playing cricket, watching movies, taking us for sports activities, etc.

Luckily I grew up in a wealthy family

As it was a joint family (until the late ’90s), we did have a budget to adhere to, but it was more than sufficient to have a comfortable upbringing. We never splurged on luxury items – the only cars we had back then were Maruti’s and a Contessa.

Having said that, my father never compromised on vacations wherein we used to always stay in the best of hotels and fly business class to international destinations.

My first Pocket Money

I started getting my first pocket money once I graduated high school and started college. This is the first time I experienced the joy and thrill of money and what it actually symbolized. Until then, everything was provided for and I had never felt the need to ask/save money.

I had the same experience after completing my undergrad degree in 2004 in Boston, USA. My father made it clear that from this point on, I would have to provide for myself. This was one of the most stressful periods I had experienced to date. I spent weeks doing interviews and a few part-time jobs until I finally landed my first full-time consulting job after 3 months of graduation. I was working 10-12 hours a day, hardly meeting friends and spending my weekends just trying to recover from the grueling week. Though it was really hard and painful at the time, it turned out to be a blessing in disguise, as it prepared me for the tough times that were just around the corner.

I started my earning through family business

After working for 4 years in the consulting role, I returned to India in 2008, joined the family business and started working under my father. Based on my experience with money in the US, I was adamant that I will draw a salary based on my education, experience, market trend etc and will pay for all my personal expenses other than housing as I was still living under the same roof as my parents. This is also the time I got married, which again is a life-changing experience and taught me a lot more about money than I had hoped for!

And then we lost major part of our wealth overnight

Due to various events between 2008-2011 the aluminum division was declared an NPA overnight, resulting in our selling the company 100% to a Japanese conglomerate by 2013. This entire experience of losing most of the family wealth overnight and having to sell the company and my house in Bangalore, which I had bought in 2008 upon my return, further made me realize the importance of savings.

My father never separated business and personal finance and therefore after almost 30 years of running a business, he did not have any personal savings to fall back on. I was glad that I made the right call in 2008 of drawing a salary and keeping my personal income personal.

I had started reading Jagoinvestor around 2010 and was following a disciplined investment approach through SIPs in Mutual Funds, Gold ETFs, PPF, etc. Most importantly as I was drawing a formal salary based on my worth, the Japanese acknowledge this during the transition and made me an attractive offer to stay back as a Director for India looking after daily operations.

Money is very important, but finally, a means to an end

My first experience with money was when I started getting my pocket money after high school. Then in 2004 when I started my first job and again in 2013 after having sold the aluminum business and going from a promoter-director to a salaried director.

I don’t harbor any specific fantasies about money and realize that it’s a means to an end. Yes, money needs to be appreciated, valued and respected. It is important to save for the future and have an emergency fund. It is important to be aware of the reality that nothing lasts forever and one can lose assets, jobs, health overnight.

Being able to lead a healthy, comfortable and dignified life and giving back to society is what is most important.

Unfortunately, the world we live in today does not give us the luxury to harbor idealistic beliefs such as this. Money is and will always be the most important thing in life as it akin to the blood in our veins or the oxygen in the air.

My parents point of view towards money

Both my parents always respected money and never splurged on wants. However, they used to always tip heavily at restaurants, travel tours, domestic help etc and it gave me the feeling that they never had a desire to accumulate wealth.

I have come to believe that money/ wealth only come to those who desire it and plan for it.

Money – Now and Then

In both phases of life, I knew that money was and is important, as it was the only way I could fulfill my needs and wants. It’s just that when I was in high school, my inability to fulfill my needs and wants to effect only me and now when I am 35, it affects my family, domestic help or anyone dependent on me.

As one grows older, the number of people dependent on us also increases and so does the importance of money!

How do I look towards people having more or less money?

I think less/more is a function of income/expenditure and savings/growth. It’s a very subjective notion.

For example, I know people living contently earning 50,000/month and earning 50,00,000/month. Each one is wired differently and if one has the desire to grow financially, they need to make a conscious sustained effort and not leave it to chance.

The biggest mistake people make with money

I think one of the biggest mistakes people make wait a lot and not start saving at a younger age! I know so many people at the age of 21-25 who are starting their first jobs and they just don’t believe in or understand the concept of savings. I think its a big mistake! If you cant save much, that’s fine, but at least start with some amount and start building the discipline.

In the US for example, parents demand that their kids start paying for their own expenses from the age of 16 and by the time they are adults, most of them come to appreciate the magic of savings and compounding!

How money is linked to happiness?

I think for one to embrace happiness, the person needs to be in a peaceful state of mind. For one to be in a peaceful state of mind, you need to be healthy, provide well for your family and have a fallback corpus for the unknowns which again requires money

How I’m feeling after writing my money story?

Writing my money story makes me more determined in continuing on my path of spending intelligently and looking for more ways in which I can contribute to today’s youth who are just joining the job market by helping them understand the value and the various avenues available to them for saving and investing.

What is your money story?

I thank Mr. Rajat to share his story on this platform. Hope everyone has learned a lot from his story.

If you want to write your money story, Leave your details here and Jagoinvestor team will get in touch with you with the next actions.

What do you think about my money story? Did you enjoy it? Can you share your views about money and how it changed over the years?