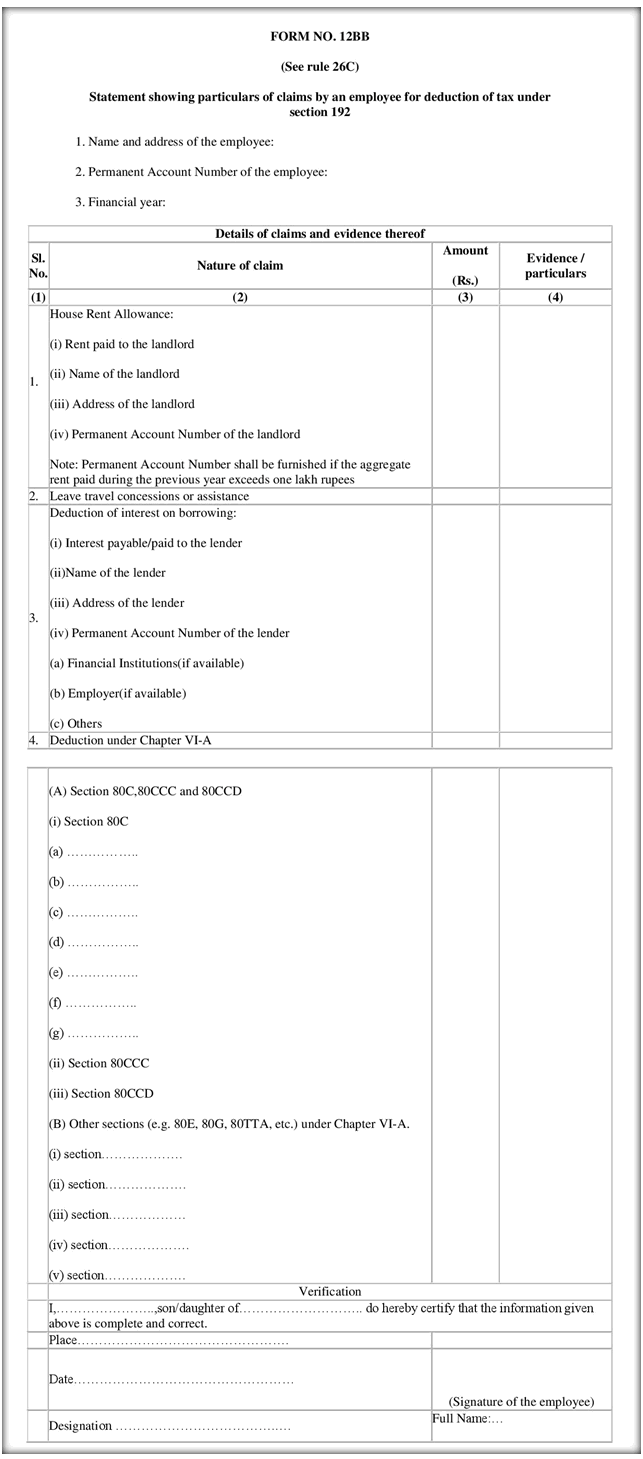

In a recent notification, income tax department has come up with a new form 12BB, which from now onwards has to be submitted if you want to claim your LTA, HRA and Interest on Home loan interest.

It’s a single form, which you need to fill and attach all proofs and furnish all information related to these exemptions. This form will be applicable from June 1, 2016.

What all information is asked in Form 12BB?

Following is the list of various things you need to arrange before you fill up this form 12BB form

LTA (Leave Travel Allowance) – One has to provide all the proofs of travel like tickets, invoices, boarding pass (in case of flight). More info here

HRA (House Rent Allowance) – For claiming HRA, If the rent paid is above Rs 1 lacs a year, one has to provide Name, Address and PAN of the landlord and Rent receipts.

Interest on Home Loan – To claim this, one has to furnish the name, address and the PAN of the lender organization

Deductions under 80C & Others – You will also have to furnish the details and proofs of the actual investments done under Sec 80C and others

You can download form 12BB here, It’s a PDF version (We don’t have excel format). Below I have provided a snapshot of the form 12BB format, so that you can have a look at it and see what all fields you have to fill up.

Main reason to introduce this form 12BB?

The primary reason why this new form is being introduced is that till now there was no standard process to collect all the proofs and information regarding the various deductions.

IT department thinks that with this new change, fraud will go down. Here is what Financial Express says on this point

You may no longer be able to provide fake bills to claim income tax deductions for leave travel allowance (LTA) and house rent allowance (HRA).

Changes announced on Tuesday in reporting format for individuals claiming tax deduction on leave travel allowance (LTA), leave travel concessions (LTC), house rent allowance and interest paid on home loans is aimed at plugging leakages on account of fake bills, experts say.

So with this form, all the information will be captured in one place and even the employers will be made accountable for checking all documents and if the proofs are genuine or not.

Please share what do you think about this new form? Do you think that this will add more work and headaches for salaried employees?

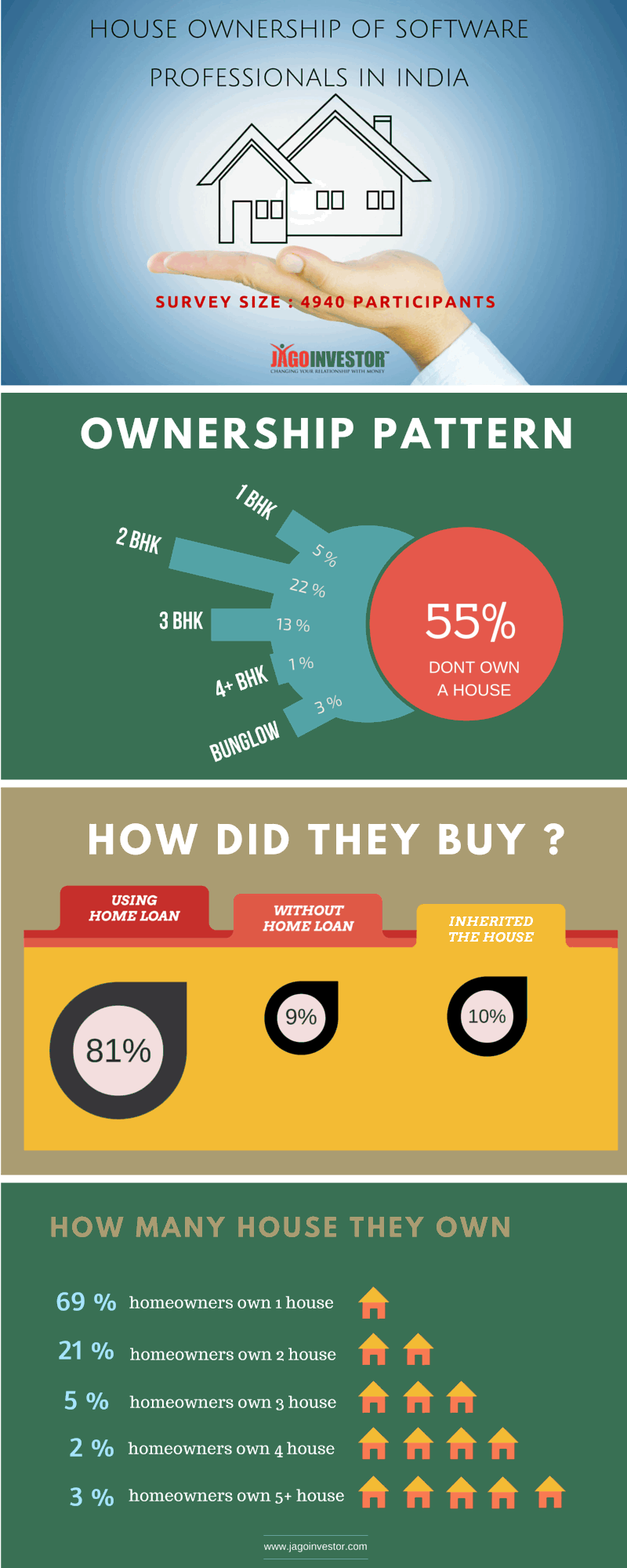

Today I am going to share with you some data related to software engineers and their home ownership pattern. But before you move ahead, I want to share with you that approx 55% of the software engineers who took our survey did not own a house.

Survey with 10,917 participants

Recently I ran a very large survey which was taken by around 10,917 participants. Out of those 4,940 people were from the IT Industry. I had asked many questions related to real estate ownership like how big houses they own If its bought with a home loan or not and if they don’t have a house, what kind of rents are they paying apart from many other questions.

As a big portion of this blog visitors is software professionals, hence I thought let’s do an article only for software professionals in India as of now. I will publish a detailed report later on the overall data, but as of now, you can look at 3 big and important information.

[su_animate type=”flipInY” delay=”0″] [su_button icon=”icon: facebook” url=”https://www.facebook.com/sharer/sharer.php?u=http%3A//www.jagoinvestor.com/2016/05/software-industry-real-estate.html” icon_size=”48″ size=”6″] Click Here to Share this on your Facebook profile[/su_button][/su_animate]

So what did I find in this survey? I found out that out of 4940 software professionals who took the survey, 2706 of them said that they don’t own any house or real estate property. That around 55%.

Majority of software professionals in India bought house with home loan

I know this is not a finding. Almost everyone buys a house on loan only because very few people can pay the full amount on their own and this gets confirmed by this survey. Around 81% IT professionals said that they took home loan for buying the house, however 10% people got the house in inheritance and only 9% people paid the full money out of their pocket, which I think is a good number.

90% of the house owners (IT professionals only) own either 1 house or maximum two house. Only 10% house-owners have more than 2 properties.

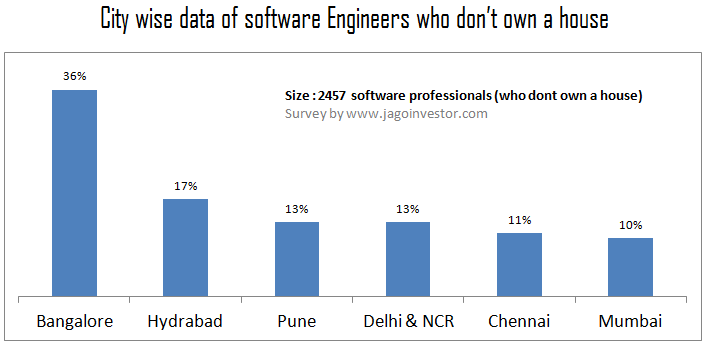

Out of 100 software engineers who dont own a house, 36 work in Bangalore

If we look at the top 6 cities which are into software jobs creation, we found out that the higher the cities reputation into IT Industry, higher is the number of non-home owners % wise.

I mean out of 4940 software engineers, 1533 work in Bangalore and out of those 886 said that they dont own a house, which is 36% of the total IT population which took the survey. So 36% of software engineers who dont own a house, live in Bangalore, compared to only 10% in Mumbai or 11% in Chennai. Here is the full data

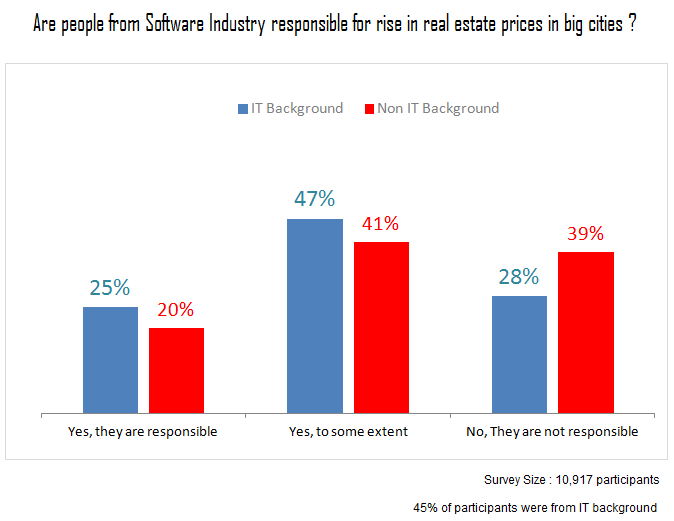

Who is responsible for the high real estate prices in big cities?

In this article, I want to understand what you all think about high real estate prices? What is the reason behind it? Can we say that to some extent (if not fully), the IT professionals contribute to the real estate prices increase?

I know not all software professional earn very high salaries, but in all the big cities, there is a section of IT class which earns a very handsome salary and they suddenly use it to take home loan and buy a house either for consumption or for investment purpose.

This is true for many other Industries as well, but do you think IT sector contributes much more than other industries? I do not want to make any judgment here, but I want to hear from IT professionals who read this blog about what they think about this?

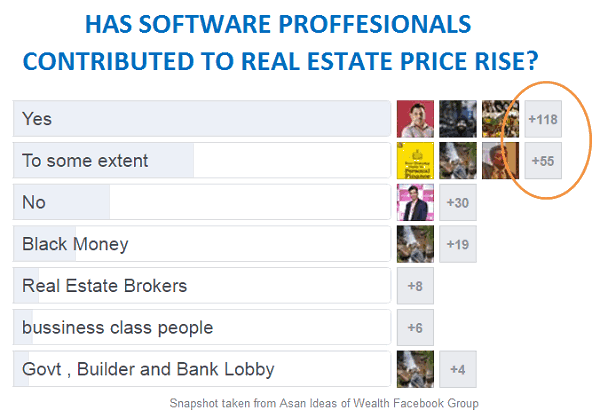

Some people told me that we can’t blame software professionals for high prices in real estate, which I agree. No one can blame anyone, but I wanted to know what thousands of people from IT background and non-IT background think? What is the perception?

So I separated non-IT and IT people from the survey and I asked them the same question and looks like people from IT industry are of stronger opinion that real estate prices are high because of IT industry. While 39% people from non-IT background said clear “NO”, only 28% people from IT background denied that IT industry has contributed to rise in property prices. Below are the results of survey by around 10,917 participants out of which 45% are IT professionals themselves.

What people have to say about this?

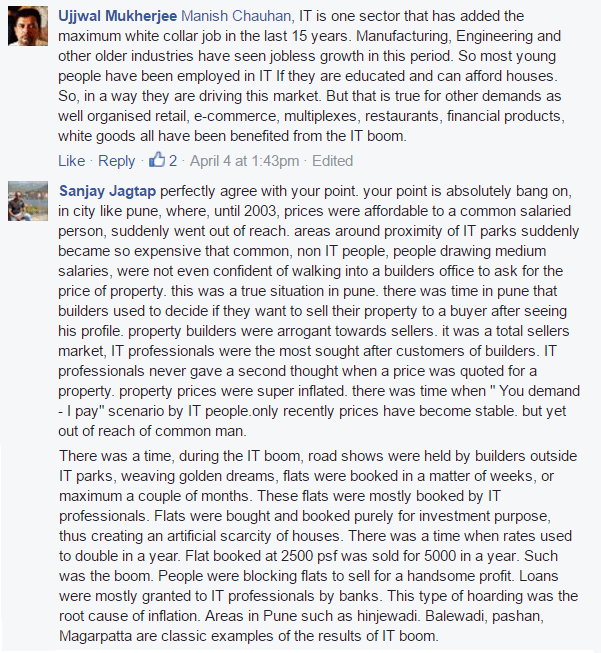

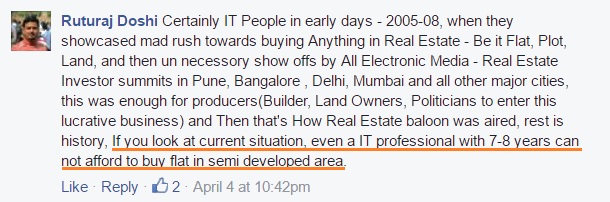

Let’s hear some people who have shared their views about this topic and how they feel that IT industry is somewhat responsible for high real estate prices.

But 55% of Software professionals still don’t own a home

At the same time, we have a big number of software professionals who cannot afford a house because they don’t belong to that very high earning class. Software industry like every other Industry has its own issues. A big percentage does not earn very high salaries and that is confirmed by the survey also.

Salaries in IT industry is highly skewed

Only 12% of IT professionals who were surveyed, are earning more than 20 lacs per annum where as 57% of the participants are earning below 10 lacs. Now that’s just 80,000 per month and I am sure, if one is living in a city like Bangalore, Pune or Hyderabad, it will not be considered as a very high income because given the expenses these days, people at that salaries would hardly be saving anything significant.

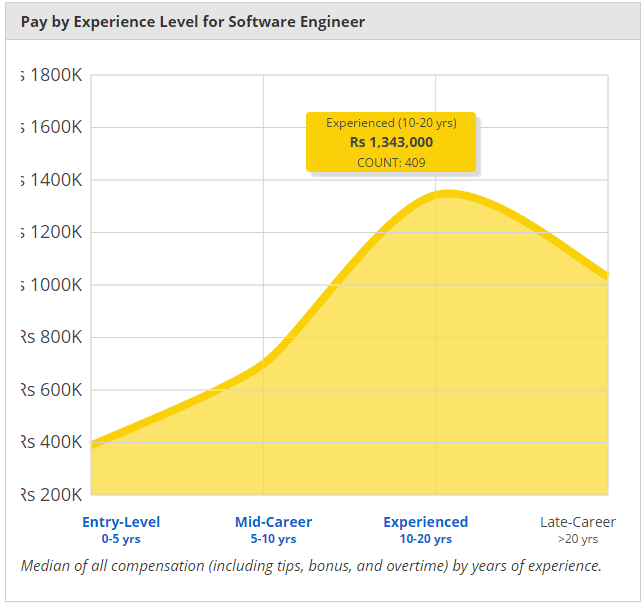

As per a website payscale, which has an extensive database of various jobs related information like the skills needed, salaries etc. The average Salary of an experienced Software Engineer in India is close to 13 lacs (with experience of more than 10 yrs) . Note that this is an average number

Hence, while there are many IT engineers who earn big amount (many a times double income family), and who can afford to buy a house easily. At the same thing, there are many software engineers who do not earn a big amount and are struggling to manage their expenses. Here is one perspective

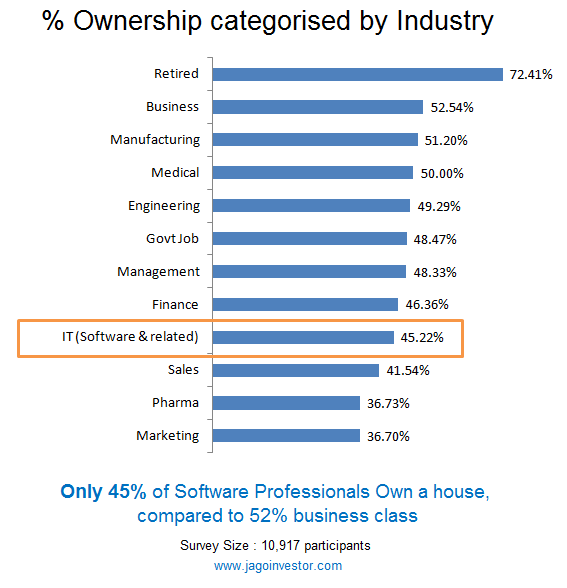

I analyzed the results of 10,917 people who took the survey and found out that if you look at the percentage home ownership industry wise, then software industry is not at all at the top. Infact, it’s quite below average. But then we are talking of only big cities (top 10 cities of India). On top of it, IT Industry has somewhat slowed down in last 5 yrs and its not at its peak now. You can read this long thread on IndianRealEstateForum where people discuss about the impact of IT slowdown on the real estate market.

So basically we are trying to see that out of 100 people who belong to XYZ Domain, what percentage of them owns a house. Domain here means Software, Medical, Govt Job, Business, Marketing, Sales, Engineering * Finance. There are many other domains, but we are not considering them, because there was not enough data. For each of the above domains, we had at least 200 data points each and at times more than 500 or 1000. Here are the results.

I had kept Retired also as one of the categories, because that would be a big number. So we found that the those who are retired have the highest home ownership which is kind of obvious, but after that business class has the highest home ownership ratio of 52% , followed by Manufacturing and Medical, but they are not having very big margin.

IT Industry ownership stands at 45% and we can be kind of very assured of that because that comes form 4940 people data, which is quite huge.

Also, note that the lowest home ownership is among Sales and Marketing Professionals & Even Pharma, I don’t have much interpretation for that, but may be it’s because they might have a big variable component in their salary and that might be a deterrent in their home buying. If you have insight on this, please put them in comments section.

Question for you ?

We want to know from you, what is your views on increasing real estate prices in most of the Indian cities and do you see IT industry contribution to it? Please share what you think in comments section.

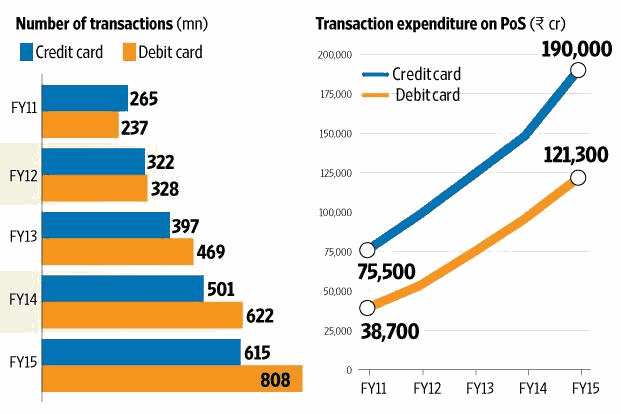

1,90,000 crore was spent using credit cards in India in the year 2015. Over the last decade, the usage of cards has increased many folds and while that’s great for the economy, it also means more and more people getting into credit card debt as many people are now dealing with credit cards.

In the graph below which was published by Livemint, it shows the growth in the card usage in our country

How investors get into Credit Card Debt Trap?

Credit cards if not used properly can get you into debt trap very easily. We get several emails and comments regarding how to handle credit card debt. Below is one of the comments

“I have a SBI card in which I have an outstanding balance of Rs 100000 so I went for settlement and they offered me a settlement amount of Rs.78000. Can it get it still reduced? Because I am not in a position to pay this amount”.

A lot of investors who do not use credit card in a wise manner end with a large outstanding on their cards and finally have to go for credit card debt settlement which lowers their credit score and puts a black mark on their credit report and this inturns hampers their chances of getting loans in future.

In this article, I am going to share some of the options which one can explore. If you want to quickly look over those 6 points, you can just watch the video below

Note that these points to be looked in order. I mean first, you see if option 1 is applicable to you or not. If not, then you move to option 2, if it still does not help you then you move to another option.

[su_table responsive=”yes” alternate=”no”]

Option #1

Break your investments and pay the bill

Option #2

Pay off the credit card debt in 5-6 payments

Option #3

Take a loan from friends/family and pay off the credit card outstanding amount

Option #4

Take a personal loan to pay off credit card debt

Option #5

Convert your credit card loan to EMI

Option #6

Use a Credit Card Balance transfer facility

[/su_table]

So here you go

Option #1 – Break your investments and pay the bill

There are many people who keep rolling their credit card debt, and at the same time have money in their bank account or a fixed deposit. It does not just strike them that they can just pay off the full outstanding by breaking their FD or cash into the account.

This happens out of ignorance most of the time.

So if you can restructure your money here and there and can pay off the credit card debt, it’s the best option.

Option #2 – Pay off the credit card debt in 5-6 payments

If option #1 is not feasible for you, then the next best option is to pay off the debt in 5-6 parts. Most of the people get too attached to the minimum balance amount and then they just stick to it because that’s the minimum required to be paid to save the penalty.

But then the interest is anyways to be paid, which makes sure you never get out of the debt.

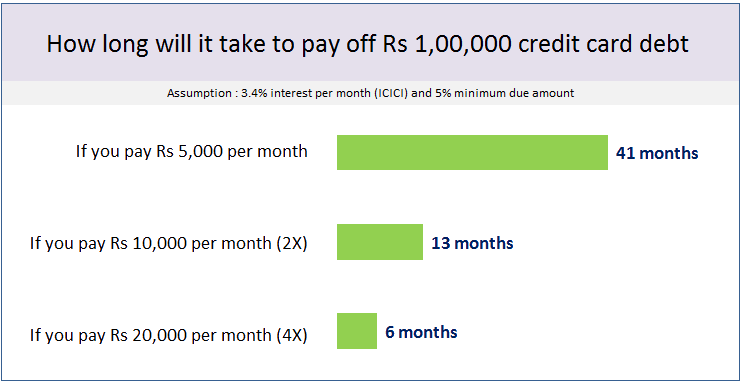

So go beyond the minimum balance amount and pay 3-4X of the minimum balance each month. For example, if your credit card debt is Rs 2 lacs and the minimum due amount which can be paid is Rs 10,000.

Then try to pay 2-3X of that amount, which is Rs 30,000 or Rs 40,000 per month. If not that much, then at least 20,000. That way at least you will pay off the entire debt in next 1 yr if you are disciplined enough.

Option #3 – Take a loan from friends/family and pay off the credit card outstanding amount

The 3rd option is to try to get some loan from friends or family members and pay off the credit card debt in one go and then pay back the person later as per what you agreed with him/her. One can often get free loans without any interest from a close friend or a sibling if you communicate your problem well.

Make sure you pay them back exactly within the time frame mentioned.

Most of the people have burned their fingers by giving money to their friends and relatives because it gets very tough to ask back the money and it can bring sourness in the relations due to money matters.

So you can also choose to pay some interest because the person can anyways earn some money from FD, so better offer to pay 10% interest per year. It’s a win-win situation if it works out!

Option #4 – Take personal loan to pay off credit card debt

If you don’t get loan from someone close in family/friends, then you can go for a personal loan and use that money to pay off the card outstanding. Interest will be in the range of 14-18%, but still, it’s better than paying 40% on a yearly basis.

This does not clear your debt, but just shifts your debt from credit card to a personal loan. Much better option. For those who already have a home loan going on, they can also look at the top-up loan facility which will be much cheaper to a personal loan.

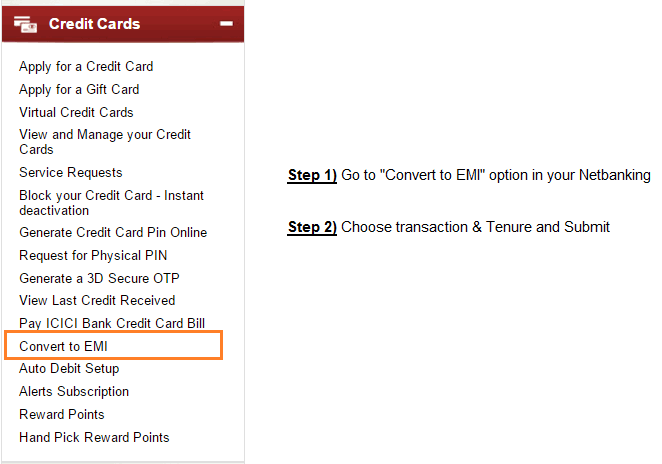

Option #5 – Convert your credit card loan to EMI

If you are not getting a personal loan, then you can convert your debt to an EMI option from the same lender. Almost all the big banks give an option to convert the credit card debt to EMI for tenures like 3/6/9/12/24 months. The interest can range between 13-18% depending on the lender.

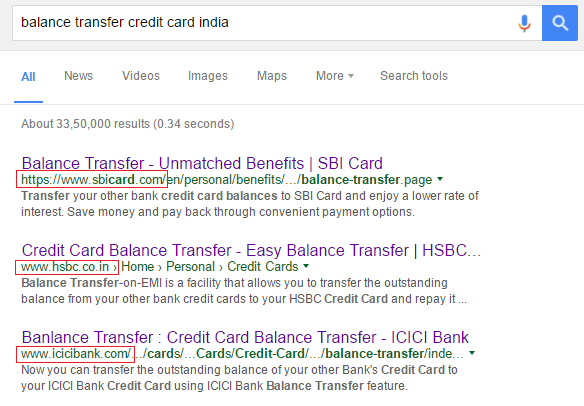

Option #6 – Use a Credit Card Balance transfer facility

There is a facility called Balance Transfer provided by many credit card companies, where you can switch your current credit card outstanding to a totally new credit card. In this case, the new credit card will pay off your old credit card and will also offer you some benefits like an interest-free period of 3 months or low interest for the first few months.

Almost all the major credit card companies like SBI credit card, ICICI credit card, and HSBC have this credit card balance transfer facility service with them. SBI credit cards even provide 0% interest for the next 60 days.

However, before opting for this option, please check if there is any processing charge or not? It might happen that the lender is providing free interest period, but then high processing fees will nullify the advantage 🙂

However, note that this is a temporary solution for the next 2-3 months and by that time you should look for further solutions.

Use your credit card wisely

Below are some high-level points which will save you from getting to credit card debt

Pay your Credit Card 3 days before the due date, keep a reminder on the phone if it helps

Don’t spend much more than you can afford.

Carry debit card instead of credit card, You will pay only what you have

Don’t keep very high credit limit, if you can’t control yourself when it comes to spending

Today I am going to talk about some mistakes which young investors make in their early life. Many experienced investors would be able to relate to it, because often we make these mistakes because there was no one to guide us when we started our journey of wealth creation.

“Young investor” here means any person who has just started their careers. Most of them would be below 30 yrs of age. I will share 7 mistakes in this article. You can consider these 7 points as the words of wisdom from experienced investors.

Mistake #1 – Not Focusing on increasing the income

Nobody became rich by only controlling their expenses!

“Low income” is probably #1 reason, why most of investors are unhappy in their financial lives. Low income means low/no savings, restricted life style and constant worry about future. A small financial mistake can turn very costly if one has small income.

Imagine a guy living in Mumbai & earning just Rs 35,000 a month (or even Rs 80,000 now a days) and have to support a family of 4 people? Can you imagine how “tight” his situation is?

For most of the people, salary increment “happens” naturally and never worked on consciously. Most of the people take whatever comes their way for many years, only to realize that rather they should have come out of their comfort zone and worked “actively” on increasing their income.

They could have relocated to a new place with better opportunities, changes their jobs, asked for a salary raise, or could have worked on an alternative income, but most of the people don’t do that. They just go with the flow thinking – “I will get, what I deserve”

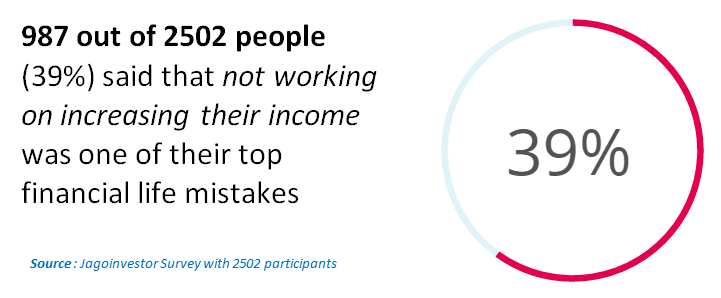

In one of the survey’s I have done recently, I asked participants to choose the top most mistake of their financial life. I gave them 8 different options to choose from and 39% of the people chose – “Never worked on increasing my income seriously”.

As a young investor, the best investment you can make it not some mutual fund, or a policy, but you yourself. Invest in yourself and develop skills which makes you “valuable”. Make yourself so employable that people run after you.

Remember, if you earn a big income, you can still make a lot of mistakes, spend like hell and choose not to control your expenses.

Mistake #2 – Getting into Debt Trap Early in Life

Don’t get me wrong!

I am not against taking debt.

But, a large number of young kids who start their career have bad relationship with money and credit facilities.

They start using credit cards as if it’s a money toy. It all starts with a small outstanding credit card bill, and soon it starts rolling up every month and soon they find themselves paying minimum due amount and finally when things go out of control, they take a personal loan to close off the loan or convert the outstanding amount to EMI’s and starts how their debt trap starts!

Then follows car loan, home loan, another personal loan, another credit card and this way a person gets into deep debt cycle. I am sure if you look back, you will realize that the debt trap started very small.

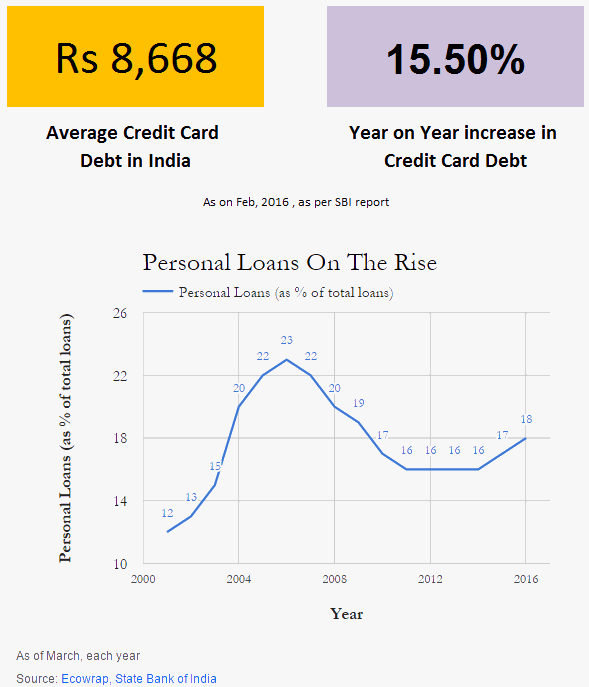

Let me share some data with you on this. As per this report, personal loans as % of loans stands around 18% as in the year 2016 (Out of every 100 loans, 18 are personal loan).

As a young investor, you can still do mindless spending, but that should happen with cash money and not credit. Because getting into debt is easy, but coming out of it is not that simple. So as a young investor try to take debt only if you don’t have any choice. As far as possible, take responsible credit which helps you in life (education loan or home loan).

Mistake #3 – Not taking risks in start of your career

I am not saying that everyone should go and start taking some risk without planning. All I am trying to convey is that its more easy to take risk when you start your career, rather than middle of your career or when you turn 40, because in your early days you have less responsibility and enough time to fix your mistakes if any.

Think of these options below!

Want to move out of your industry and try something else?

Want to try a start up?

Want to try that online business idea?

Want to change your career path because you don’t feel you belong to current job?

Want to ask for a salary hike, but too afraid to lose the job

The above 5 things can be tried at any point of career, but practically you have more appetite to try out these things in the start of your life, when you have less responsibilities and enough time in hand to correct the mistake if any.

If you are still confused about this, you should listen to this YouTube video about best practices in Career Risk-Taking. It will help you

Once you have already spent significant number of years in your job, you will get married, have kids, get into the cycle of “life” and it will become very difficult to come out of the comfort zone. I get many mails which starts with “Had I tried it 10 yrs back … ” and I can see how people feel so stuck into their jobs and now they can’t take much risk at this point of life.

Mistake #4 – Buying policies from your relatives/friends

There are millions of investors in India, who have lost a lot of money in bad products which were sold to them by someone close to them. It was often an uncle, aunty, father’s friend, distant relatives or even your siblings at times.

A lot of products are bought in India based on trust and goodwill. Often relatives pressurize you to take a policy.

This is particularly true for Endowments policies, ULIP’s and other insurance products. You will often find someone in your close circle who is an agent and your parents trust them like anything and force you to buy a policy from them.

Years later you realize that you have burnt your fingers and can’t express your dissatisfaction openly. So what is the way out? Either research on things on your own or directly buy form the companies or if you need external help, better hire an advisor or an external agent, but not a relative

Mistake #5 – Investing in a product you don’t understand yourself

On an average, 90% of the investors can’t explain what exactly they have bought. I was once talking to an investor in our workshops (the upcoming one is in Pune on 22nd May, 2016) and the guy said he has few policies. When I asked how many? He had no idea

When I asked what are the names of the policy, he didn’t even know that.

He said that he had bought them few year back for tax saving and does not exactly know what they are !

The problem is that investing in products, which you don’t understand blocks your financial energy. Your money is stuck in a rotten product and takes away a lot of time.

So if you are buying a financial product, please learn how it works and how it’s going to benefit you at the end of the day . Find out everything about return, risk, liquidity and taxation. If possible, better know which financial goal it’s going to fund.

Mistake #6 – Not saving early in life

After spending many years in your job, you will realize as an investor that “I will save when I will have more money” is an illusion.

When you start earning money, your income is less and you are not able to save money at all because you are hardly left with anything at the end of the month.

However note that this is going to be true always. While your income will rise in future, so will your expenses. You will get married, have kids, your lifestyle will improve. You will get a car, buy a house and what not. You will enough feel that you have enough to save.

The graph for expenses is set to rise and this feeling of “I will save in future, when I earn more money” will be intact. This is the reason a lot of investor never save enough money which they deserve.

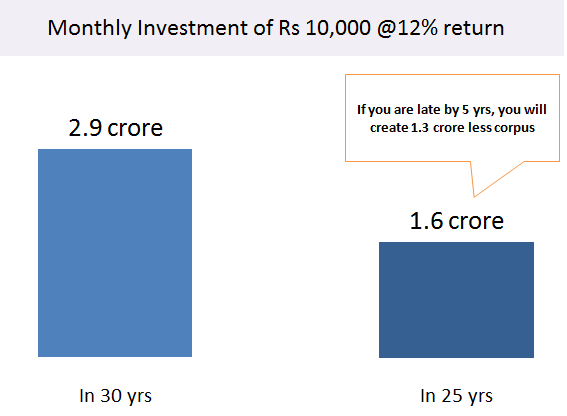

The graph below shows you if a person starts investing Rs 10,000 a month, they can accumulate around 2.9 crores in 30 yrs. However if they delay it for 5 yrs, and then start the same thing. They will accumulate only 1.6 crore by the same time. That’s a big difference because of the delay.

As a young investor, you need to understand that habit of “saving money” is more important than how much do you save. If you can’t save anything, start with Rs 100 per month.

I know it sounds like a joke. But once you do it for 5-6 months, you at east know that you can save Rs 100.

Then upgrade the number!

Upgrade to Rs 500 or Rs 1000 a month. Continue for another 6 month.

Soon, you will realize that you have reached Rs 5,000 or Rs 10,000 because you are just increasing the number, the “habit” was already in background.

Mistake #7 – They neglect their health

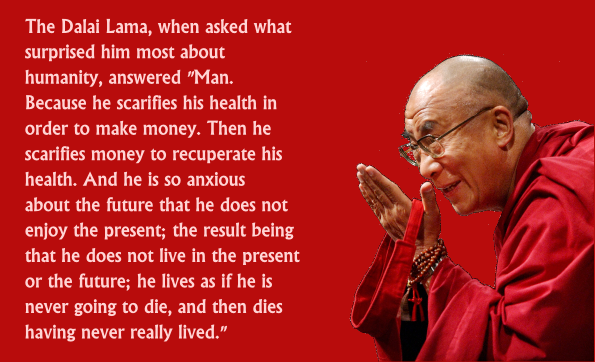

If you do not have good health, it will not matter how much money you have earned, because you won’t be able to enjoy that money at all. It does not make sense to lie down on a bed made of gold in your retirement.

While earning money is important and required, make sure you also pay attention to your physical and mental health. These days, the jobs are too demanding and there are many money matters which will take the peace out of your life. You might get lost in the rat race and forget that you have a body to take care for years.

Only years later you will realize that it would have been better to earn a bit less and have a healthy body, rather than having bad health with money.

The quote from Dalai Lama is worth reading

Learn from others mistake

At this point of time, internet is flooded with the mistakes other investors have done. It’s a wise thing to learn from those mistakes and not repeat them.

A good and healthy start of one’s financial life helps a lot and if you are a starter, I strongly suggest you take a note of the points above and implement them.

Please share your views on the points above. Were they helpful to you as a new investor?