Most of the people who apply for a credit card in India, do not pay much attention at the time of taking the card, but later get frustrated by the card itself for various reasons high bad customer service, hidden charges, and several other factors. The obvious question then is, which is the best credit card in India? We did a survey on credit cards and tried to do a review of credit cards based on participants experiences. We will see how these cards rate in 6 important parameters. There were 654 participants who took the survey, hence you can safely assume that the collective responses will give a near reality results.

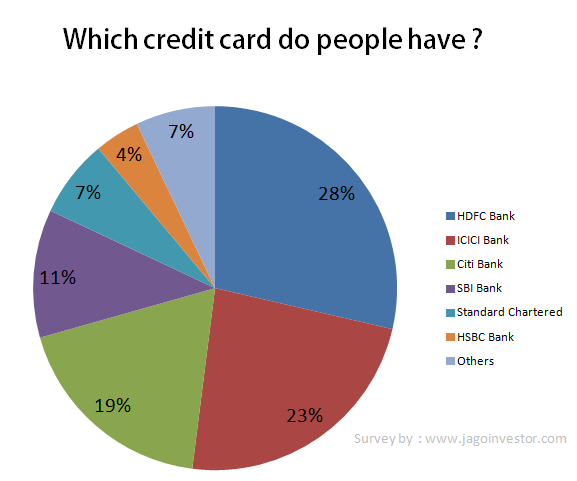

If you see the chart above you will know that the 6 top credit cards in India are –

- HDFC Bank Credit Card

- ICICI Bank Credit Card

- CitiBank Credit Card

- SBI Bank Credit Card

- Standard Chartered Credit Card

- HSBC Credit Card

6 factors to look at before you apply for Credit Card In India

Let’s see those 6 parameters which you should look at before you apply for a credit card in India. At the end of this article, we will see the detailed results of the credit card survey and find out how different credit cards performed on each parameter so that if some particular parameter is more important for you, you can just pick a card based on that parameter.

1. The interest rate charged on credit cards

The first parameter to look at while choosing a credit card can be the interest rate charged by the credit card company. It can range from 1.99% on the cheapest credit card to as high as 3.5% per month on the most expensive credit card. For most of the people who pay their bills on time, this parameter will not matter much, but you never know when you might get into a debt trap kind of situation where you start using your credit card to the maximum limit and pay the interest per month, at that point of time this factor will really matter. Note that interest rate charged is mentioned on a per month basis, but a small difference of 1% can be very big, considering it on a yearly basis.

For example, a 1.99% monthly interest rate actually means 27% Yearly and 3.5% monthly means 51% yearly CAGR.

51% yearly CAGR ! … means your Rs 1 lac of credit card debt can actually increase to 7.9 lacs in just 5 yrs if you don’t do something about it and obviously you will run around to improve your CIBIL score later!

2. Annual Fees & Other charges

A lot of credit cards charge yearly fees and renewal fees (at the time of renewal). Now a lot of people hold a Free credit card for lifetime, but that’s just bunch of people who were given the credit card on a telemarketing call, mostly because they are working in some big company and chances are higher that their usage of credit card will be much higher than an average customer, hence the free credit card.

But, a lot of people apply for the credit card themselves and for them, there are yearly charges (annual fees) and another kind of charges which is applicable to everyone. For example, the penalty charges if you don’t pay your dues any due date. There are tons of customers who do not pay their dues on last time and just pay the minimum payment. If this happens a lot with you, then there is a great chance that you also live with the myth of minimum payments on credit cards. So apart from annual charges, there can be charges like

- Charges when you pay your credit card bill by cash in any bank branch

- If you make a demand draft from your credit card

- If you request for a duplicate statement

- And many other credit card charges .. the list is not a small one 🙂

Note that if your credit card is FREE as of now, it might carry annual charges when it expires and you apply for renewal – and credit card company says – “Sir, we gave it 100% free only till the card is valid, now its renewed! “

3. Rewards and Offers on Credit Card

There are a lot of advantages of using a credit card in the form of benefits and reward points. For example – You get PAYBACK points which you can use to redeem at various places like www.bookmyshow.com, and book movie tickets by redeeming those points. You also get cashback benefits if you use the card at selected HPCL petrol pumps and you don’t pay the fuel surcharge too.

There are many other kinds of benefits that many credit cards in India offer and those can be different from one credit card to another. This is one very important factor before you choose a credit card because a big number of people just take credit cards for these benefits and even if you are not looking for these, you might want it in the future at some point in time.

4. Customer Service and Transparency

Once I called my credit card company (which is ICICI Credit card) because I wanted to know if there will be any annual charges on my credit card as the expiry date is over and I wanted to renew the credit card. They gave me a very clear and satisfactory step by step answer which made me feel – “Great” .

There was no renewal charges and no annual charges even after renewal. So I was happy. Now it was not the FREE thing here which made me happy alone, It was the way customer care talked to me and treated me like a human:).

While there are instances when I was not that happy, but overall on average, I would still rate the customer service of my ICICI credit card as “good” . Well, that’s my experience only and others can have a bad or worse experience with the credit card company. Before you apply for a credit card, you need to look at this very critical aspect of customer service and how transparent are they overall.

5. Convenience to pay the bills

Something which you will deal with each month is the payment of your credit card bill. Now almost all the credit card companies allow paying by net-banking, cheque, cash and other ways. But still, some banks can be really torturing and not that supportive. It can be cumbersome at times. There have been instances when people paid by cheque before time and it was not processed on time and the person had to suffer because of that and had to run around to get back those charges reversed.

Here is the example

I got the CIR and there is absolutely no big hiccups except one in ICICI bank credit card (I had lot of issues with this bank and some late payments od 1-7 days in some credit cards in very few months. Never listens customer and pathetic customer care executives) of which the DPD is consistently not (000) good for last 5 months. But hey it wasn’t my fault. I dropped the cheque of overall due (about 12000/-) and they never bothered to inform me that my payment was not credited (god knows what they did with cheque). After 5 months when they made a balloon of charges and the whole amount jumped to 19000/- they called me and threatened me of CIBIL. I was never in the mood to not pay the due hence paid the whole amount 19000/- notified by them. Could this lead to this much low score?? – Link

Not to mention the unfair update on CIBIL report which affects you for years. So it’s a critical factor to look at before you apply for a credit card in India.

6. How easy was it to apply for credit card

Have you gone through a frustrating time applying for credit card, really had to run around to get a credit card even when you were totally eligible to get one. While this criterion is not that big, as its a one-time event still you can consider it before you apply for one. I recently had a hard time opening a saving account for my brother with ICICI bank because they had no way to accommodate people living on rent with friends, however, Kotak bank did it for me, at that point of time, the “ease of opening the account” was really a big thing for me. In the same way ease of applying for a credit card can be one important factor at times.

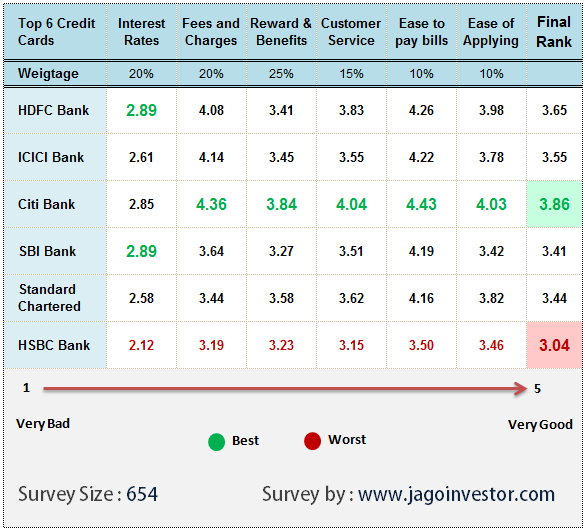

Best & Worst Credit Card in India as per Survey

Below are the results of the survey which we conducted on credit cards. Have a look at it.

If you look at the above chart you will see that the best credit card in India turns out to be Citibank Credit Card and the second best is the HDFC Bank Credit card overall. However, this does not mean that other credit cards are not good at all the parameters. ICICI Bank credit card is very close to all the other cards in several parameters.

While the SBI Bank credit card and HDFC Bank credit card top the list when it comes to interest rates charged (means they have lower interest rates compared to others), but HSBC Bank credit card comes last. HBSC bank credit card has not done well in any parameter as per the survey and has the lowest ranking in all of them.

Average Credit Card bill for the last 6 months

86% of people are paying less than Rs 20,000 per month as there credit card bills, that’s last 6 months average. Whereas only 2% of people had more than Rs 50,000 bills per month. I suspect that these people must be using their credit card for various mandatory expenses which are required anyways. Lots of reward points and benefits to them:).

Credit Card Reviews from participants

Ramakrishna says on his Citi IOC Card – I am using credit cards from past 9yrs. If u use the credit card in the right manner, u get the most out of it. And make sure you pay your outstanding amount before the due date. Most of the times, by end of month I am barely left with the liquid and credit cards used to save during that bad times and used to pay the outstanding by the due date. I never ended up paying any interest until now. The best credit card to date to my knowledge is Citi IOC card. I had made use of the rewards and offers at the extreme.

Kriprabha on Axis Gold Card – Very, very bad – due to careless service. 1) Not pointing out auto-debit facility – I missed one annual fee, so from 300/- bill went up to 1000+. 2) Not applying their own rules about marking a lien on my FD Receipt — my card was blocked for weeks and no one seemed to know this requirement, and they kept assuring me the card would be activated soon. As of now, the card is inactive – reason unknown. I am snipping up a card today – want to avoid AMC which they will apply happily! These bankers live and work in air-conditioned comfort which is possible due to high ABQ. I will soon terminate my “relationship” with them. I am a senior, living on savings, so these visits to the bank cost a lot in auto fares.

Raghavendra on HDFC Credit Card – Experience with HDFC Cards has been good. I have never looked at the interest option since I’ve always paid the outstanding amount by the due date. Was charged a penalty a couple of times when I paid the outstanding a couple of days after the due date ( had not even paid the minimum amount by the due date, owing to travel), but the same was reversed after a detailed email to HDFC Cards requesting for the same, in light of good payment track record except for the 2 instances. On the rewards front, HDFC Bank does not have a very good rewards scheme as compared to others. But customer service is excellent. They also have two billing cycles, one of the 25th and the other on the 5th and allow customers to choose any one of them. This is useful for those who already have a card and choose a second to make optimum usage and take advantage of the alternate billing cycles

Atri on HSBC Credit Cards – I am using HSBC gold credit card for more than the last 7 years. I always submitted payments in time and even insured the card purchases. It was as good at their services and also at the part of mine but I do not know why in their review they decided to cancel my card and stop their services to me. I even asked HSBC CUSTOMER representative but they could nor reply satisfactorily. I now feel I should have to get a credit card from the Public Sector Bank only and wasted my time and money. My message to all public is to use Bank Account / Credit Card only of Public Sector Banks like SBI, Canara Bank, Central Bank of India, etc. for a good governance in the nation. Thanks and Regards.

Some more data out of credit card survey

- Only 10% of people had 4 or more credit cards

- Around 42% of people had exactly 1 credit card with them

- The average number of credit cards held by one person was 2.03

Other Credit Cards

Note that this survey is focusing on top 6 credit cards and their comparison with each other only, which came out as the result of the survey, but there are several other banks credit cards in market which can be considered, but due to small amount of feedback in the survey, it was not sufficient to conclude anything about them nor do any kind of review about these credit cards. Here is the list of those other credit cards

- Axis Bank Credit Card

- Amex Credit Card

- Kotak Credit Card

- Bank of India Credit Card

- Indian-Bank Credit Card

- Bank of Baroda Credit Card

- IndusInd Credit Card

- RBS Credit Card

- Syndicate Credit Card

- Andhra Credit Card

- Canara Credit Card

- Corporation Credit Card

- PNB Credit Card

- ABN Credit Card

Did this article help you in choosing the best credit card in India? Is there any other parameter to look at before you will apply for a credit card? Do you think this survey helped you in choosing a good credit card in India?