We have planned a 1 day paid workshop across different cities in India, starting with Pune. The first workshop will be on 25th Mar (Sunday) in Pune and it will be a full day event. It was not easy to decide what should be covered in the workshop, but we really want to make sure it is of extremely high value and should leave an experience. So, after a lot of discussions and brainstorming we designed the workshop which we are calling as “Design your Financial Life”.

Contents of Design your Financial Life

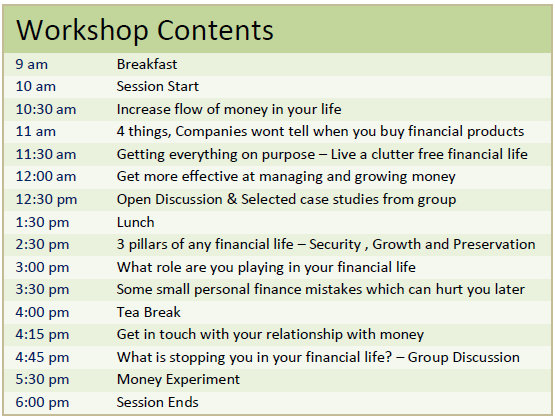

The workshop will start at 9:00 am and will go up to 6:00 pm in the evening. The focus of the workshop is, that any one who attends has a clear understanding of how he should lead his financial life. The talks will be a rich mix of mentoring on how to think about money and what mistakes to avoid (coaching aspects) and it will also have some talks on how one should look at various dimensions of their financial lives and get the ground rules clear about them. There will be 2-3 group activities and exercises which will enrich the program. Here is the table which gives a full day time line.

Pune Workshop Registrations are Closed now

Who should attend the workshop

This workshop is targeted at those who are beginners and have made a start in area of personal finance and they would like to spend a full day to hear and experience rich conversations on money and learn the ground rules of most important area’s of personal finance. The workshop will assume that participants are beginners/moderate knowledge about money related matters and they would like to build on it from that point. The session will be a mix of mentoring & insights on how to think about personal finance related things.

By the end of the session you should be capable of charting out your Financial Roadmap and be self-sufficient in basic level of thinking in personal finance.

This session is not for experts who know it all. This session is also not for those who wants any stock or mutual funds tips or any kind of get rich-quick kind of tips. Financial Planners or advisors should also refrain from attending the workshop.

There are different kinds of insurance riders and the common question is “Which insurance riders should I take?” . This is not a question I or anyone else can answer for you. This has to be decided by you and no one else. All you need to know is what exactly a rider is and what it is going to provide you.

What are different kind of Insurance Riders ?

Insurance Riders are the extra benefits that can be purchased and covered for under the life insurance policy. Apart from the basic Life insurance cover, you can choose to add some extra benefits to the life insurance cover, but you will have to pay extra premium to get such add-on benefits. The basic premiums will then increase. Note that the base policy features are always there and you get the base Sum Assured in case of death. Addition of these riders has nothing to do with the original rules of the policy. Let us see all the insurance riders one by one.

1. Accidental Death Rider

In this rider, you get additional sum assured if the death occurs due to an accident. The biggest myth which investors have is that they will get the money if death is due to accident only if this rider is added, else not. This is not true. If you don’t take this rider, still the base Sum assured will be paid to you. This rider is only for the extra sum assured in case of death due to accident at additional cost, nothing else. So if you take a policy of 50 lacs sum assured with accidental rider of 25 lacs. You will get 50 lacs in case of death other than accident and 75 lacs in case of death in accident. A lot of policies cover you from disabilities which arise out of accidents. See Accidental Insurance Policies

2. Permanent & Partial Disability

This rider is helpful in case you are disabled permanently or temporarily due to accident. In that case most of the policies pay periodically for next 5-10 yrs a certain percentage of Sum Assured. For example, 10% of Sum Assured per year for next 10 yrs. This way this rider acts like an income generation insurance most of the times. However note that the rider is helpful only incase the disability happens due to accident only. Read the policy document of the company for exact wordings. Most of the times, this rider is combined with Accident Death rider.

3. Critical Illness

This rider gives you a lump sum amount if you are diagnosed with an illness which is pre-specified and is mentioned in the policy. Generally all the major illnesses are covered in Critical Illness cover. Some of the examples of critical illness mentioned are Heart Attack, Cancer, Stroke, Coronary artery by-pass graft surgery (CABG), Kidney failure and Paralysis for example. After the critical illness is detected, the policy might continue or terminate as per the policy document. At times, the policy coverage reduces by the amount paid to you. So better read the policy document to know exactly what will happen in this rider.

4. Waiver of Premium

This rider makes sure that in case you are not able to pay future premium due to disability or income loss, the future premiums are waived off but your policy is still in force like always. This is in a way insurance of the premium payment till your policy expiry date. In case this rider is not present and you are disabled and not able to pay the premiums, then the policy will expire and you will not get any benefit later when you die because due to non-payment of premium the policy expires and the cover stops.

5. Income Benefit Rider

This rider is present in some policies and it’s mainly for the income generation after the death of the policyholder. If this rider is present, the policy holder’s family will get additional income per year for 5-10 yrs along with regular Sum Assured. For example, 10% of Sum Assured for next 10 yrs will be received by the policy holder’s family.

These Insurance Riders come with cost and exclusions

Note that riders come with cost, so just because they are present in the policy as add-ons, don’t jump and include every kind of rider possible. Ask yourself why you need a rider and if there is really a need for it. Read about the rider rules in details and read what is not included in that rider. Also compare the cost of insurance riders from different companies to take a better decision.

Everyone is so desperate to buy a child plan (example). The features of so-called children plan are bundled in a way that it looks magical, as if there can’t be any other product like a child plan and hence, we pay much more than the price it really deserves most of the times. So today we will see how we can create your own child policy by combining term plan and other investments like PPF, FD or a Mutual Fund.

When you hear “Child Policy”, It looks extremely attractive. It gives you money on your death, It gives yearly income and it also gives you money on the maturity of the plan (generally when you child is ready for higher education) . So the point is that a child policy is so much in demand and attracts investors because of its features. However there are some issues with child plans in market. They come with high costs, rigid structure and very less control over it. Traditional Children plans (which are endowment or money back type) mainly do not deliver of returns front and ULIP children plans come with high cost .

So what can you do now ? Can we create a child policy on your own by combining Term Plan and Investments in some separate instrument, in a way that the Term Plan will take care in case of your death and investments will take care of higher education cost in case you survive.

So just like you pay a yearly premium for a Child policy, even in this case you will pay a fixed amount every year. A part of it will go as Term Insurance Premium and rest will go into investments. But in this case the term plan will also open ways for yearly income, as well as future big time expenses for child higher education as well.

When you are not there, the amount received by family from term insurance can be invested in such a manner, that it can provide a yearly income + lumpsum money NOW + Lumpsum money in FUTURE. Lets us take an example and see how it will look like. Suppose you have a 1 yr old daughter for whom you want to create a Child Policy like structure, and you want to achieve these 3 things.

1. Lumpsum Money

If you are no more , family gets 50 lacs upfront as lumpsum.

2. Regular Income

After your death, your family should get Rs 50,000 per year separately for your daughter education for next 20 yrs and this Rs 50,000 should increase every year by 9% (so that inflation is taken care of) and assuming this money will grow at 8% return (FD)

3. Money for Higher Education

When your daughter turns 21 yrs old and is ready for her higher eduction, she should get another 25 lacs at that time.

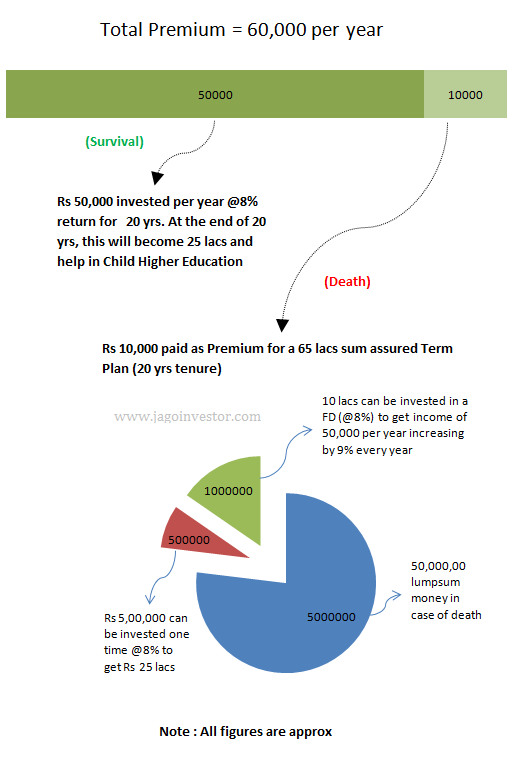

In order to achieve the 3 things mentioned above , you need to buy a term plan for Rs 65 lacs (Sum assured) and start investing Rs 50,000 per year in something which gives 8% return on annual basis. Apart from this, you will need to clearly define to your family what actions they need to do once you are no more (these are simple tasks like opening a FD or investing money in PPF or balanced funds). The yearly premium for this structure would be around Rs 60,000 (50,000 investment + 10,000 premium for term plan) . Lets us see how this structure will be helpful .

If case of death (Your family gets 65 lacs)

50 lacs can be taken out as lumpsum

5 lacs can be invested one time to get 25 lacs at the end of 20 yrs

10 lacs can be invested one time to get a yearly income of 50,000 increasing by inflation figures!

Incase you survive

Your investments of 50,000 annually will create a corpus of 25 lacs at the end of 20 yrs anyways

Lets us see this same example through a picture, which will clearly illustrate how this 60,000 premium payment will create a Child policy kind of structure and how it will help you in case of death and survival.

So using this structure you can achieve what a child policy provides. However this whole method has its own pros and cons. There is a lot of flexibility in this structure which a child policy does not have. However this kind of structure would need some level of trust and you will need to instruct your family about it and what they need to do incase you are not around. I think if you are preparing a will, you can clearly mention what needs to be done with the term plan money, so that family members can take those actions.

Download the Calculator and Start Planning your child Policy

Below is a calculator which you can download and punch in your numbers, the calculator will tell you how much term plan you need to take and how much investment has to be done per year. The expected return and inflation is decided by you. So if you want your family to put the money in FD or PPF after you are there around, then put the return expected as 8%, if you want it to be in Balanced Funds put 10-11% and incase of Equity Mutual Funds, put 12-15%. Also note that the premium for term plan will depend on the company you choose for taking a term plan (LIC is coming up with its term plan in few weeks as declared by them recently).

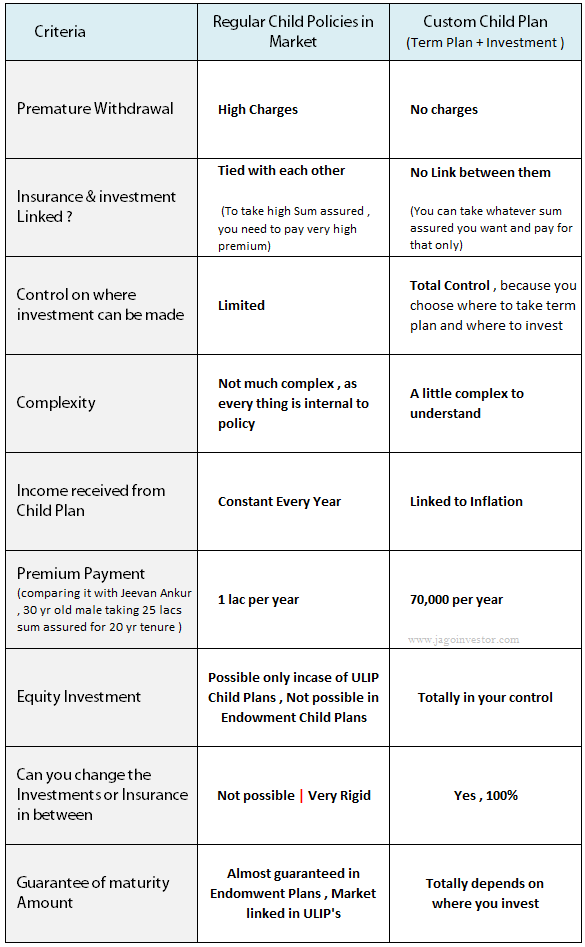

It’s important to see what is the difference between the child plans in market and this custom-made child policy by combining term plan and investments

Comparing it with LIC Jeevan Ankur

Lets compare this with LIC Jeevan Ankur Policy. If a 30 yr old male has to take a 25 lacs policy for a tenure of 20 yrs, He will have to pay premium of Rs 1,00,000 per year (approx) . In case of death, his family will get 25 lacs + 2.5 lacs income per year till maturity + 30 lacs of maturity (assuming 20% loyalty addition) , incase the person survives, he will get 30 lacs anyways on maturity.

This same thing can be achieved if a person does a 60,000 per year investment in PPF or FD (assuming 8% yearly return) and taking a term plan for Rs 55-60 lacs for a premium of say Rs 10,000 per year (for most company, the premium is 5,000 but lets assume LIC online term plan is taken which will come in few weeks now). So he has to pay total 60k + 10k = 70k per year to achieve the same results, with a lot of flexibility.

Do you think this whole strategy of creating your own child policy is of any use? Do you think it’s too complex? Share your views.

Today I want to show you how 2 fellow readers of this blog were in a fix when it came to their hard-earned money and they were struggling to get justice from their respective banks and financial institutions. They mailed me and commented on this blog and when I saw those comments, I thought – “lets see what can be done!” This is a post where you can learn what kind of things can be done if you are having issues at times and then try to resolve it further.

Case 1: How an old lady got justice from ICICI Prudential

Some months back an old lady named “Nita” commented on this blog how ICICI Prudential representative have taken advantage of the situation and played around with her money. It was not a case of miss-selling, it was actually unethical behaviour (or call some kind of fraud). So I decided to help her in whatever way I could. Here is what she wrote

Dear Sir,

I was holding ICICI Prudential Life Time Super policy (Policy number: XXXXXXXX) and have already paid two premiums. The third premium was due for payment in July 2009. Due to delay, there were frantic calls from ICICI Bombay office for making the payment. On 28th December 2009 when called again from ICICI Prudential Bombay office, I requested them to get the premium collected as assured by their officials at the time of issuing the policy. I was told by their office that a representative would come on 29-12-2009. On 29th Mr. K N Pandey mobile No XXXXXX a representative of ICICI prudential came and after verifying his credential from Dehli office in-charge Mr. Mratunjay Sharma Mobile No XXXXXXXXXX a cheque for Rs.50000/- was given. He demanded that a photo and a signed copy of form was required to get the lapsed policy restored. these were given to him.

Later on, finding that instead of a receipt of the premium paid for the old policy (policy number: 05225842),a new policy “LifeStage Assure Pension- policy number: 13129468″ was delivered. This was issued under forged signature.(photocopy attached). Soon after the receipt of the new policy in 3rd week of jan-2010, the matter was reported to the company’s representative Mr. K.N. Pandey and his immediate superior Mr. Akhilesh Gupta Financial adviser of ICICI prudential Mob. no 09838506002 and Delhi office Mr. M Sharma. They accepted their mistake and I was assured that the new policy will be closed and the amount of the premium will be transferred in my old policy no: 05225842.I trusted them since they begged saying that if the matter was reported, they were to lose their jobs.

But, having failed in my efforts the matter was reported to the chairman ICICI Prudential in September 2010. I never got the reply but when I presented all the documents before ICICI Prudential Manager at Kanpur office I was given a copy of reply sent by the Bombay office in Sept 2010.

(photocopy attached)

The local office after having gone through the records and finding my complaint genuine, they again sent the complaint to Bombay office and I was asked to wait. Again there has been no communication from Bombay office but on my approach to local office I have been given a copy which is ditto of the previous reply.(photocopy attached). On the advice of local branch manager to save my one Lac rupees deposited earlier in policy No. 05225842, I have borrowed the money to deposit Rs ONE Lac i.e. two years premium to get the policy revived. The amount has been debited from my account on 26/05/2011 but I have not yet received any communication regarding revival of my policy.

The fraudulently (under forged signature) issued new policy No 13129468 is still hanging in abeyance and my Rs.50000.00 is at stake. Since I am an old lady with meager source of earning I cannot afford to operate two policies and that’s why I have been trying to get the amount of the second policy credited for the old policy. Since now, I have come to know about IRDA can help in such matters I therefore request your good office to look in to my case and help me to get justice.

Yours faithfully,

NITA TRIPATHI

06/12/2011

What I did

I tried to find out who is the current CEO of the company and tried to find his email id, but failed. Then I found him on facebook and left a message to him (didn’t get any reply). I then contacted a PR agency in Mumbai who earlier contacted me on behalf of ICICI Pru and I knew they must be knowing someone at ICICI Pru who could help the lady. This worked and I got a mail from ICICI saying that they will work on this and get back with their response. I replied back to them on email like this –

If it was a normal misselling case , I would have let this go , as misselling is same as misbuying . but here it was fraudualant activity and without any reason the old lady is harrassed and she is not able to do anything . Please take up this case with priority and more than professional grounds , help the lady on human ground . It would be appreciated if you can follow up with the concerned people who were send to collect the money from lady and even their seniors .

I am cc’ing Mr Kunal Pradhan and lady Nita Tripathi .

Thanks Manish

The case was resolved and Lady got her money back

After that there was no activity for few days and some weeks back I got a mail from the lady and she confirmed that the things are resolved now.

Dear Mr Manish,

Wish you a VERY HAPPY HEALTHY AND PROSPEROUS NEW YEAR.

I am extremely sorry for not writing to you earlier about the progress in the matter. In fact after your intervention, ICICI Pru immediately responded. They have now cancelled the mis- sold policy and have credited the amount to the old policy account after getting the formalities completed locally.They have issued the receipt and provided the number by email but I have not received the hard copy as yet.

Honestly speaking I have no words to express my gratitude and thanks for all the help. I pray to GOD to give you all the success and happiness in life.

Thanks once again.

Nita Tripathi

Case 2 : How Bharat Kamble got his Rs 24,000 back from ICICI

One reader Bharat Kamble was struggling to get back his money from ICICI Bank. His credit card was charged twice and ICICI was making him run around here and there without any valid reason. Here is the problem he was facing. I thought of using twitter to communicate this issue to ICICI bank and ask them to act on priority.

Within 24 hours, I got a message from ICICI stating a reference number and they asked Bharat to reply back to ICICI and mention that code number in the message subject (I guess they take it with priority and seriousness). Bharat did exactly that and then he got his money back. I asked him to write a testimonial for us and here is what he sent back in email (problem and solution both).

Dear sir,

I am a 29 year old Geotechnical enginner from mumbai. I am planning for migration to Australia and have already applied for an Australian PR (Permanant Residence). On 21st June 2011, i have paid the fees for PR application to the IEA (Immigration Engineers of Australia). The amount was Rs. 24603/-. I gave the details of credit card in the application form and the amount of Rs. 24603/- was deducted from my ICICI credit card. This amount was reflected in my July month statement. Later in the August month statement i saw the same transaction been done again on 22nd July 2011. I called up to the IEA department for clarification. They said that the first transaction was unsuccessful and hence they did the second transaction which was successful.

I told them that the money has been deducted for both the transactions. They said that ask your bank to talk to our bank (commonwealth bank) for the unsuccessful transaction, also they me the reference file number for the failed transaction as a proof. Later daily i had been calling the customer care of ICICI bank for the problem and solutions. but i got only one answer from all of them stating ” its the mistake of commonwealth bank and they have to sort out the issue. The only alternative for this is that to raise a dispute against this amount”). I was really very tensed and worried about this problem. I showed them the reference file number which was given to me by the commonwealth bank , but they said that we cant check this reference number.

On 23rd Sep. 2011, i file a dispute against this transaction with ICICI bank. They told me that it will take 45 days to solve this dispute and also the result make not be in your favour. i was really suffering from a bad time in that period. after 45 days on 18th november, i called the CC of ICICI bank for the status of the dispute and they said that it will take another 45 days to solve the issue.

Finally while surfing on the solutions on internet i came across “jagoinvestor”. I read all the comments (some of the problems were similar to mine one but not the same exactly and thought lets put up my problem over here. Within 24 hrs i got a valuable feedback from Mr. Manish Chauhan. He gave me a code number and said that put this in the subject matter and send this email to [email protected]. I did the same thing and after 3 days i got a reply to that email mentioning that the amount has been debited on your account. I felt like my feets were not on the earth. I was relaxed and happy.

What should i say about this guy. I am very thankful to him. I would like to inform you all that beware of such kind of theft and use of credit card has to be limited.

What you can learn from this?

This post was to show you that one should reach some key people in the company and then communicate the issue to them. Just talking to customer care wont help. Reach to CEO, MD directly, mail them and expect some help. Leave messages on twitter or facebook pages of these companies. At times it works. However I am not saying that this will always work, but nothing to lose if you try!

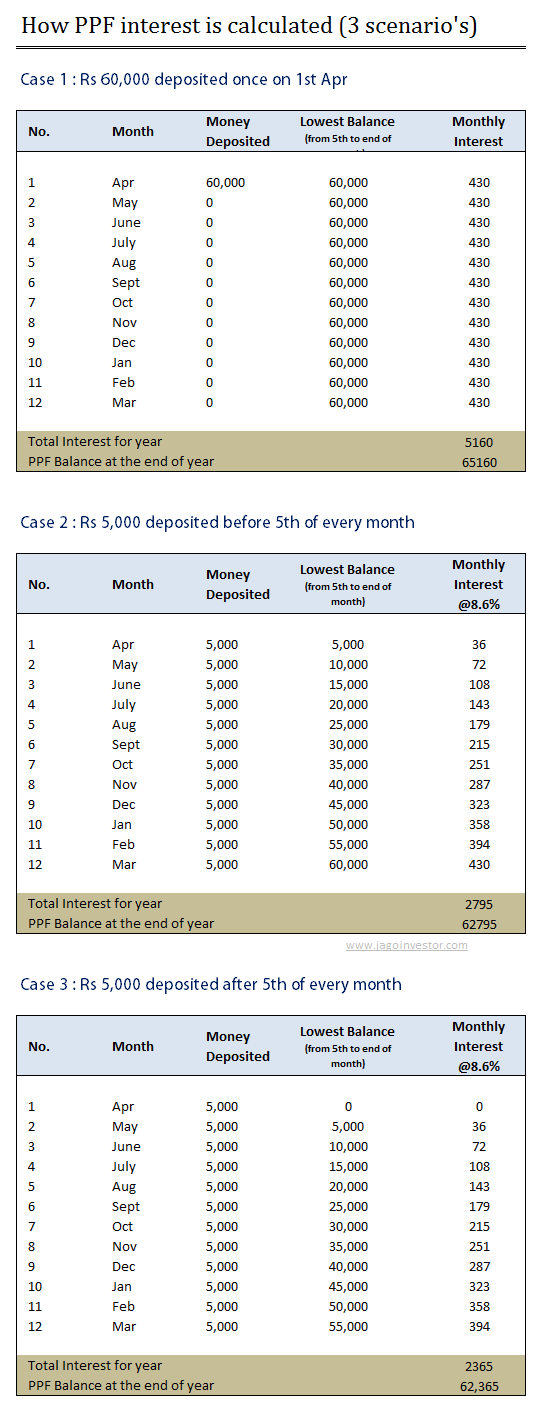

There is a great confusion among investors on how PPF interest is calculated ? Just because a lot of investors don’t know this , they have questions like “what is the best time to invest in PPF to get maximum interest” or “Should they invest in lump sum or monthly?” . Once you know the procedure and exact ppf interest calculation method, life will be easy. Let me explain with examples how its done and also give you a ppf interest calculator in a excel sheet format at the end.

To explain in one line – “PPF interest is calculated monthly on the lowest balance between the end of the 5th day and last day of month, however the total interest in the year is added back to PPF only at the year-end”

Excerpts from Official PPF page

8. Interest – Interest at the rate , notified by the Central Government in official gazette from time to time, shall be allowed for calendar month on the lowest balance at credit of an account between the close of the fifth day and the end of the month and shall be credited to the account at the end of each year

What this means is that the interest is not compounded monthly ! . While there is no ppf interest calculation formula, but the way its calculated is very simple ! . The interest earned in a year will added back to final amount only at the end of the year. Thats the only catch ! .

So lets see 3 different kind of cases where money is invested in PPF differently and see how the interest is calculated and added back to PPF account at the end of the year. We will see these 3 cases

Case 1 : Rs 60,000 deposited once on 1st Apr

Case 2 : Rs 5,000 deposited before 5th of every month

Case 3 : Case 3 : Rs 5,000 deposited after 5th of every month

The following examples give all the 3 cases examples assuming investment of Rs 60,000 in a year , but invested differently. I have taken interest at 8.6% per annum . Recently the PPF interest rate was increased to 8.6% and the limit was raised to Rs 1,00,000 and its now applicable from Dec 1, 2011 . So if you have invested Rs 70,000 earlier in this year , you can still invest Rs 30,000 more in your PPF account.

Note : Interest assumed is 8.6% for all the 12 months. However in reality it might happen that it may change in between for some months due to changes from govt.

Some Important Points on PPF Interest Calculation

If you are investing in PPF on monthly or several times a year, before 5th or after 5th will not matter a lot , it would be just few hundred rupees.

If you are investing your money in lump sum on yearly basis, it would be better if you can invest before the 5th of April, this will make sure that you earn interest on more balance for the month of Apr.

The interest on a particular month depends on the interest rate applicable for that month, if PPF interest rates change in between , then there might be different rate applicable from a point onwards.

A lot of us do not have even an idea on how much money we have in our Employee Providend fund account (EPF) and how to check EPF Balance online or offline. So in this post we will see how one can check his EPF balance online and get the details back through sms . Earlier I used to search a lot on checking EPF balance online and I came across some links , but most of them never worked. But few months back I successfully got sms with my EPF balance status. Let me show you that.

How to check your EPF balance online ?

Go to this EPFO website link

There will be a link below the page to check your EPF account balance status online , click on that (direct link)

You will see a drop down there to select the PF Office State ( like Maharashtra, Karnataka , Delhi etc) . Select your PF office .

Once you select the State , you will see a list of different cities office, like for Karnataka , you can see one of the options as “Bangalore” along with the “data available upto” date , so you can get your PF balance till that date only .

Choose the city office

You will be taken to the page where you will have to fill in EPF account number , Your Name and mobile number and Submit.

How to enter your EPF account detail ?

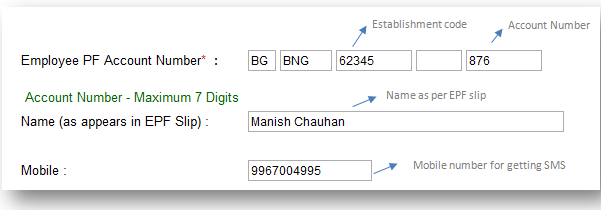

For an example lets say Manish Chauhan worked in Bangalore and had a Employee Providend Fund account with number KN/62345/876 . This name “Manish Chauhan” is the name appearing in EPF slip .

In that case 62345 will be the Establishment Code (which will be first blank column) and 876 will be the account number (third column) . The second column will be blank in most of the cases , it’s actually the sub code or extension of the establishment code.

Important Points

Note that the name should be exactly same as it appears in EPF slip

The office and state have to be selected properly , In a single start there can be many offices , make sure you choose the right one.

The SMS can come a little late , so please be patient

The amount can be only upto a certain date which will be mentioned in the SMS

Can you share if you have are waiting for your EPF money from long time ? Are you facing problem in getting right information on why your EPF money has not reached you ? Were you successful in the enquiry of EPF Balance online ?

Replying to comments teaches me many things, so I want to share one useful learning today. One of the NRI reader called Rahul was facing a strange problem, He had taken a home loan from ICICI bank few year back and now he wanted to pre-pay his home loan. However the problem was that he was outside India and bank wanted him to visit in person to pre-pay the home loan. The other way was to go through a Power of Attorney route which is extremely lengthy process. So Rahul was really stuck, however Manu appeared and shared that he has been pre-paying his home loan by adding his LOAN account as third-party account and then doing a normal NEFT transfer.

One big reason why you should connect your loan account for prepaying your home loan or other kind of loans is because at times we get some spare cash in our life through bonus or some other reason but because prepayment needs some effort and physically going to bank takes away our excitement and all that money finds its way to some other expenses which could have been avoided. I was aware of this trick earlier but really wanted some more confirmations from other readers before writing it and now I have got 3 confirmations from different readers that a LOAN account can be added as third-party account in your online banking account and you can do a NEFT transfer to your loan account. This is a simple and powerful way of pre-paying your home loan or any other kind of loan because it’s at your finger tips and you don’t have to delay the decision of prepaying your loan just because of inconvenience caused by visiting the bank.

Let me share with you some instances where readers have confirmed about this trick –

Proof by Manu on Home Loan Prepayment through NEFT

I have done the similar way for SBI. In the last few months I have paid off a substantial chunk online without visiting the bank – in fact they themselves suggested this option. What Manish said should be possible with ICICI bank. It’s like setting up an account to which you transfer funds – lets say you send some money to your parents every month. You would have added their account in third-party transfer section. Same applies to loan account. Hope this helps.

I have a Home loan from state bank of travancore. I have online access to the loan account and part-paying is simply initiating a neft transfer from any of my saving accounts to this loan account. It has been very convenient so far.. Since its online, i can see the outstanding principal amount i have on any given day.

Apart from PPF and other instruments, you can make part payment of your home loan or loan EMIs through NEFT also. Well I am doing NEFT transfer to my OBC Home loan a/c every month. Initailly it was paid through post-dated cheque.

Steps of adding your Loan Account to your online Banking account

1. Make sure you have internet banking enabled and the branch where you hold the loan account also accepts the online payments (mostly this is always true)

2. Just like you add a third-party account , in the same manner add your loan account as third-party account so that you can make the NEFT payment later. Once the account gets added , you should be able to see it as one of the added accounts

3. Once the account gets added, you can then make the payments to your loan account , it would be considered as your pre-payment .

Note that this home loan prepayment online through NEFT should be possible for all kind of loans, not just home loan.

Why only pre-payment, you can also pay your regular EMI’s using online options instead of post dated cheques. So ask your bank to allow/enable this option.

It might happen that this does not work in some banks. But we have seen 3 confirmations from different readers for 3 different banks , so mostly this should work on all the banks.

If you have bank account and loan account in same bank , it should be more easy process of just linking the accounts, ask your bank on this to guide you.

So If you have a home loan, you should definately explore the idea of connecting your loan account with your bank account so that whenever you have some spare amount , you can quickly do home loan prepayment the loan by a click of the button , otherwise that “extra” cash can evaporate very soon. Are you going to do this ? Try it out and let us know in comments section if home loan prepayment worked for you through NEFT

Do you want to a FREE book – Jagoinvestor book (The name of the book is changed now and its now called “16 Personal Finance Principles Every Investor Should Know”) without spending even a penny from your pocket ? Believe me thats possible now. Yes, moneysights.com is making it happen. Moneysights is giving away the JagoInvestor Book worth Rs 499 for FREE, to each one of you who is going to open & activate an Online Mutual Fund Investment account with them. It’s a limited period offer. However, there is NO LIMIT on how many of you can get it! , if 100 people sign up , 100 will get it ! , if 1000 people sign up , all 1000 will get it and if 10,000 people sign up , all 10,000 will get it ! . No limits !

THIS OFFER IS CLOSED NOW

But what does activation means?

Activation means sending the signed application form with mandatory supporting documents . Thats it. It’s that easy. All you need to do is get to a stage where you are ready for making transactions and you will get the book delivered to your doorstep once your account gets activated within 10 days of activation.

Are there any terms & conditions?

No. Everyone gets the book. However, you need to be careful that the signed application form along with the valid supporting documents should reach moneysight’s Bangalore office within 7 days from the date of form filling. Your application should be complete so as to get your account activated. Thats it. The only condition apart from this is that there is no condition 🙂

2 reasons why should you do it now?

You are getting the book for free

PLUS, its the tax-season. You may be planning & postponing your Tax-saving Mutual Fund investments. Now you don’t need to find another excuse to postpone your tax-saving investments.

There are 3 critical things that all participants should be doing while filling the form

Make sure that the name is full. It has to be complete name. For e.g. – Manish Chauhan’s name can’t be Manish (unless PAN card of individual has the name as Manish only)

Bank account name filed should contain the name as per bank records only

The correspondence & permanent addresses should also be accurate. The best way is to write the address as per the proof.

8 steps for winning assured Jagoinvestor Book for FREE ?

Step 1

Register with moneysights (click here) . If you are already registered, just login by clicking here

Step 2

Fill-up the account opening form online. Enter the promo code JAGOINVESTOR in the promo-code field (The offer is closed now)

Step 3

Submit the form

Step 4

Moneysights verifies the online application instantly & sends you the pre-filled application form

Step 5

Take a print out, fill-in requisite info & sign your application form carefully

Step 6

Enclose your application form & supporting documents in an envelope to send to moneysights office

Step 7

moneysights will verify the physical application form & supporting documents. If everything is in order,your account would be automatically activated

Step 8

You get the book delivered to your doorstep within 10 days

Let your friends know about this Offer

We want to spread this message to each and every person , so please share this news with your friends and anyone you know and they can also get a free book by opening an account with moneysights.com

I had done a review of moneysights.com some months back and now they offer online investments in mutual funds also. So you can open an account with them and start buying & selling mutual funds online with a click of a button. There are no account opening or transaction charges to be paid, so its 100% FREE. There are no limits on how many people can win the book, no random selections or no tricks. Just make sure your application is complete and documents are in order so that the account opening formalities are over. If your documents aren’t in order, then your account won’t be activated & you won’t get the book.

Are you going to open moneysights account and activate it soon ? Put your comments incase you are going to !