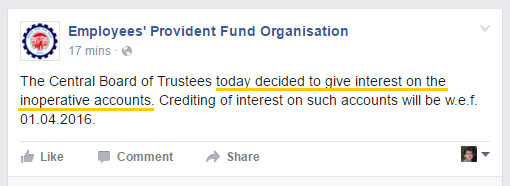

Good news, the inactive EPF accounts will now get interest from next month, i.e. Apr 1, 2016. Around 5 yrs back, under UPA rule, EPFO came up with the rule that any inoperative EPF account will stop getting interest after 3 yrs of inactivity.

So if a person left the job and never withdrew the money, he would stop getting the interest after 36 months. Inactive accounts are those accounts where there is no addition from employer or employee side. Now that old decision is reversed. There was a meeting of Central Board of Trustees at EPFO and this decision was taken.

A lot of employees will be happy due to this change because at a lot of people do not want to withdraw their EPF and still want to earn the interest. Also the withdrawal/transfer process is a bit cumbersome and many investors do not want to take the pain and let their accounts be there.

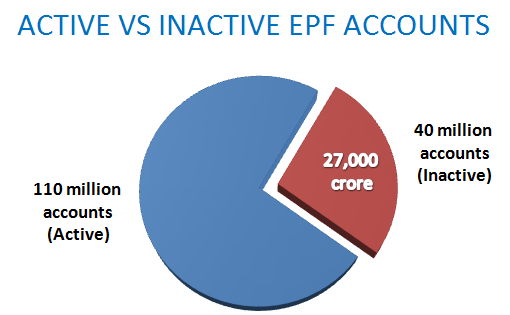

Inactive vs. Active EPF Account

As per a report, around 27,000 crore is lying in 40 million inactive EPF accounts (total accounts = 150 million), This money will now start earning interest.

That time many people were confused if the interest will be given to them or not if the accounts become inactive? Now that confusion is also cleared.

65% investment in G-Sec

As per this report, there is one more change in the way money will be invested by EPF in G-Secs

When asked about a proposal on enhancing proportion of incremental investments of the EPFO in government securities (G-Sec) from 50 per cent to 65 per cent, Labour Secretary Shankar Aggarwal said, “It has already been decided by the Ministry of Finance.”

The Secretary said that the limit of 50 percent was enhanced as they were getting good offers but unable to invest in such instruments as the limit had been exhausted.

“If we get higher returns in G-Secs then we should be allowed to invest more in these instruments,” he said further.

Yes, you heard it right!. I want to just explore the role of money in our life and how it changes our thought process. I want to know how we think about money. I will share some really interesting insights I got by surveying 2440 people on some creative questions related to money.

I am sure you are going to enjoy this article and also get some takeaways at the end on how others feel about money. Our financial lives are very private to us. Our income, our struggle with money, our desires in financial life. All this is very secret to us. You do not know how hundreds and thousands of other people like you think when its related to money.

Do they share the same feelings as you? Do they also feel scared about the future? Do they also have stress like you in their financial life?

I will show you 8 amazing insights I got from this survey

Role of Money is our life

Money has a very important role to play in our lives. In a way, it’s one of the most important ingredients you can say. We need money for almost everything today. What we will ear, how others will perceive us, how famous we might be in our friend’s circle and if a father will be interested to give us his daughter or not?

Money has a big role to play in all these points which I mentioned above.

Money has in a way controlled our lives these days. We start our day going to work for money, a lot of people are into jobs they don’t like, but the EMI’s are to be paid anyways, so we continue.

There are many examples in life, where a person is amazing at X, but they are doing a job in the Y domain. The reason being MONEY. Money turns wonderful people into a monster. Money is a wonderful thing, but at the same thing a very dangerous thing too.

Our interaction with money

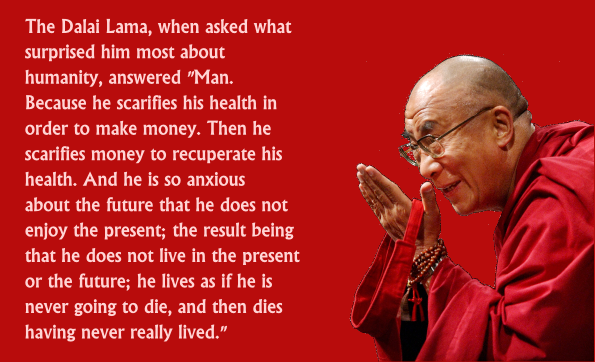

When we were kids, we had very little interaction with money. We got it from our parents and used it, we didn’t earn it and our notion about money was different. But once we get into the role of a breadwinner, only then we realize the game and how money turns us into a completely different person.

One of the best quotes to understand the effect of money in our lives is the below quote by Dalai Lama

Survey with 2440 people – Results

Let me not bore you too much with my views on money and rather look at how people think about money and what impact it has created at their thinking level. I will now take various things I asked in the survey and share the results with you

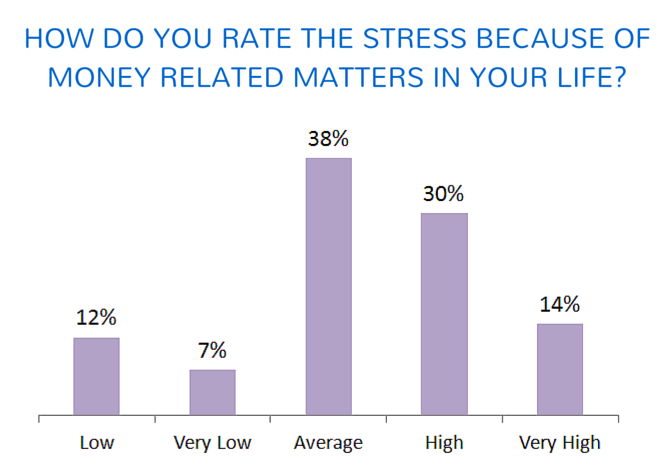

Insight #1 – How do you rate the stress level because of Money Issues?

One of the biggest problems in today’s times is STRESS. Stress at the office, the stress at the home and everywhere and a lot of times, you will realize that money has a big role to play there.

Oh my god, How will I pay my EMI’s if I lose the job?

Will I ever be able to buy a home with this salary?

I am already 38 and have not saved a penny, How will my retirement look like?

Many such kinds of thoughts occupy the minds of today’s generation. When I asked this question – “How do you rate the stress because of money related matters in your life?” Here are the survey results

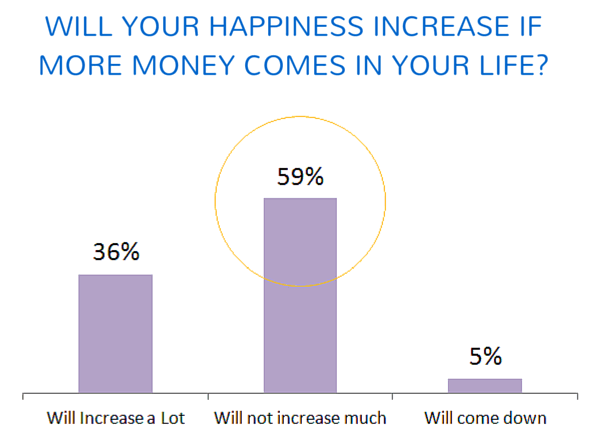

Insight #2 – Does more money means more happiness in life?

So we all are running after money day and night, thinking that money will solve all our worries and problems. However, those who have earned a good amount of money know that it’s true only to some extent. A rather correct statement would be “Absence of money leads to unhappiness”.

Yes, money is very very important and damn!, I also need tons of money and sure it can buy you all those things which can give you lot of happiness and make you feel like the king, but then beyond a point your happiness graph will start to appear flat even if more money comes into your life.

And this is confirmed by the survey results. 59% of people have said that more money will only lead to only a partial increase in their happiness and not beyond a point.

And trust me, if you have not earned a lot of money till now in your life, this statement will look like an idiotic one right now. If you are earning Rs 20,000 a month, surely Rs 2 lacs a month will mean 10X happiness, but will 20 lacs a month mean 10X more happiness from that point? I don’t think so? What about 2 crores a month? Salman also earns that !, Vijay Mallya also earns that as well. I am sure they have many issues in life!

This topic alone is worth a full book in itself, but we will keep it short as of now.

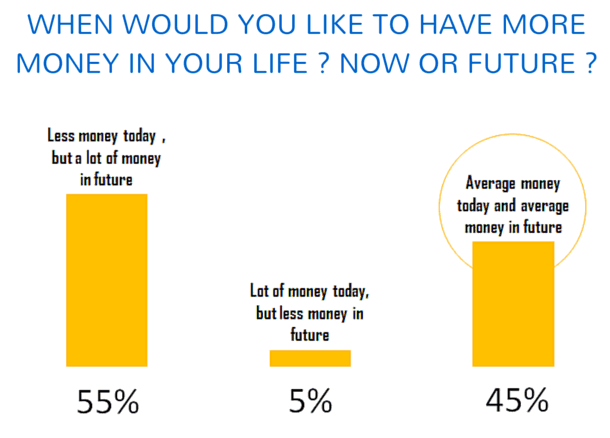

Insight #3 – Which option will you choose, More money Today or in the Future?

Most of us want a lot of money in our life. Surely more than what we have today. But we all know that it’s not going to happen suddenly? You either have to sacrifice your today to build wealth in the future, or you can enjoy all your money and retire poorer. Or there is a 3rd choice that you keep a balance between today and tomorrow. So given a choice between these 3 options, which one will you chose?

This was no brainer question in away. Around 55% of people chose that have a better future and are ready to compromise today, may be because they know that in the future they will have fewer means of earning and it looks natural. We all want an assured future.

However, 45% of people said that they just don’t want their future with lots of money but even their present. So they want average money today and average money in the future also, making sure that there is a good balance today and in the future.

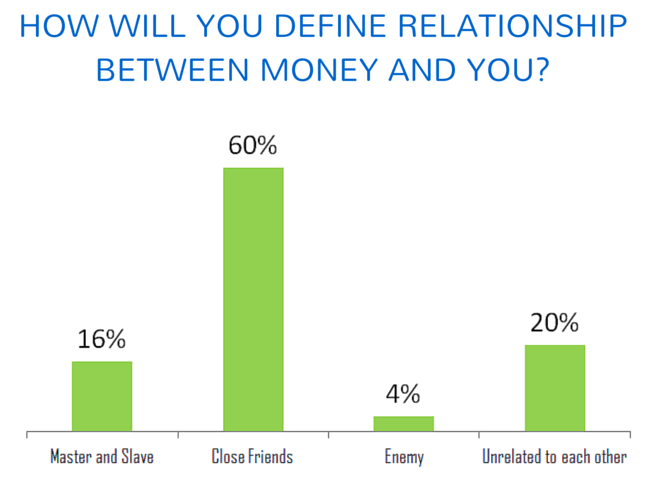

Insight #4 – What is your relationship with money?

Have you ever wondered what your relationship with money is? I first came across the term “Relationship with money” from my partner Nandish Desai, and I am thankful to him to share it with me. I added a new dimension to my thinking. He has also contributed a full chapter on this topic in my first book – “16 personal finance principles every investor should know”

Money or wealth is a non-living thing, but still, we have a certain kind of mindset towards it. We have some kind of “relation” with money. Imagine money as a human standing in front of you, do you see a friend or an enemy? Do you see it as a master and you as slave or you don’t feel any relation with each other.

I was happy and a bit surprised to find that around 60% of people who took the survey identified their relationship with money as “Close friends” . It’s a great thing that most people see a positive relationship with money. However, a lot of people who have messy financial lives don’t share very good relationship with money.

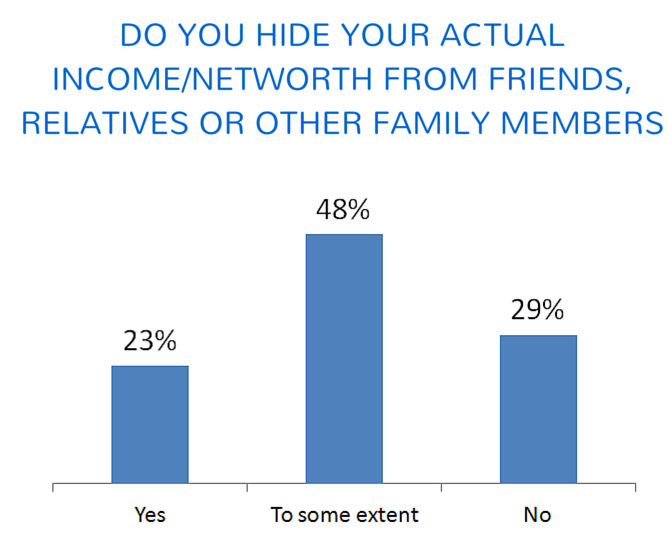

Insight #5 – Do you hide your wealth from others?

How many people know your exact salary? How many people know the exact net worth you have? How much you have in your bank account, or your mutual funds or other assets? Do you under-report it to your friends, relatives or even some close family members like your siblings and even parents? Spouse?

Seems like most of the people do. Only 29% of people said that they don’t hide it from others, but rest others hide it. while 23% said coldly YES to this question, around 48% said that they do it to some extent.

No wonder that this happens. There may be many issues which can happen if the world knows that you have a lot of money. Some might just expect “help” from you, some might ask it directly and unnecessary attention and expectations come across which most of the people want to avoid.

No wonder, most of the people want to keep a low profile when it comes to showcasing their wealth.

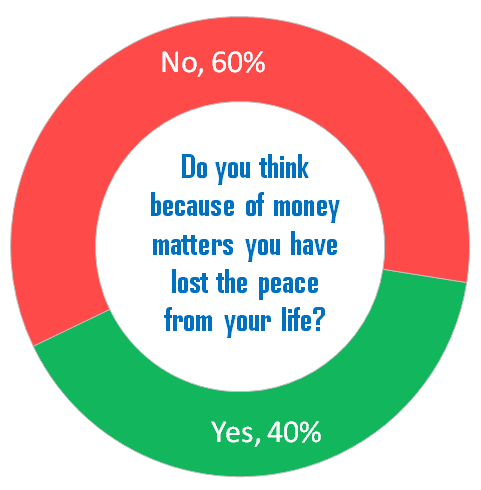

Insight #6 – Have you lost peace in life due to money issues?

A lot of people are very stressed because of money matters. Someone from low income and high expenses, while someone might be due to medical expenses while is costing them all their income each month. Someone might be under debt which was passed to them from their parents and they are paying for it. Someone might have lost money in some scam and someone might not be able to fulfill their loved one’s wishes due to money constraints.

Like I said earlier, lack of money might make the life hell in this competitive world. Around 40% of people say that they don’t find peace in their life due to money issues. They felt they have lost it. Think about it. It’s quite a big number, so every 4 out of 10 people is stressed out and does not feel relaxed.

Let me know what do you think about that?

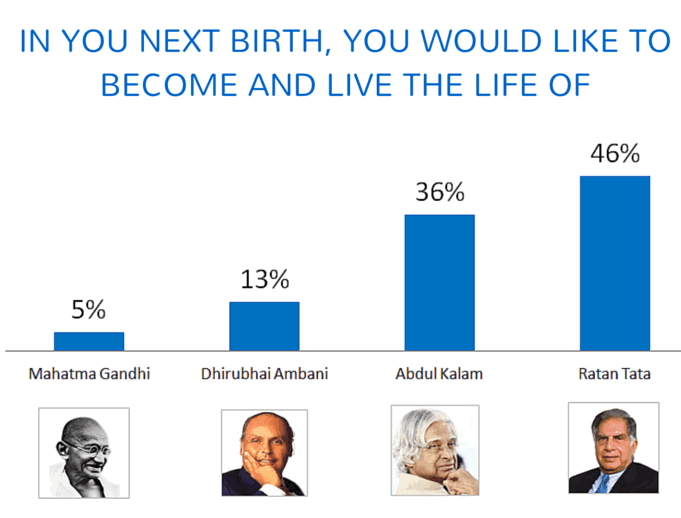

Insight #7 – In the next birth, who would you like to become?

I wanted to know what people aspire to be and what kind of life they want to live in reality. So I asked a very different kind of question, that if they got a chance, then in their next birth whose life they would like to live? I gave 4 options as below who are all very famous for whatever they have done in their life, some are respected because of what they have done for our country and some are known for wealth or both.

The options were

Mahatma Gandhi

Dhirubhai Ambani

Abdul Kalam

Ratan Tata

For a second, without looking at the results below, think for a moment about yourself. If you got a chance, whose life would you like to live in your next birth?

Here are the results and they might surprise a few of you.

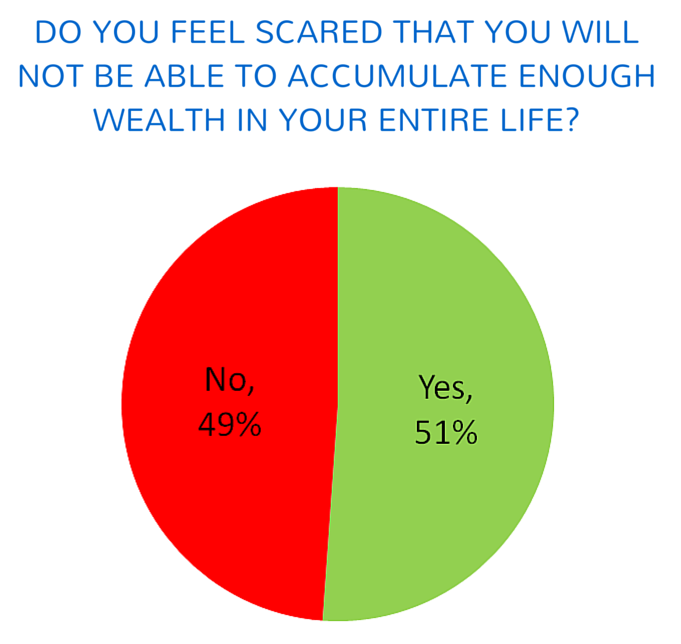

Insight #8 – Are you scared that you won’t be able to accumulate enough wealth in the future?

No matter how good your career is going or if you are earning decent enough right now, there is always a bit of anxiety about the future. We have no idea how things will turn out in the next 10/20 yrs. Because of rising inflation, and multiple expenses people do not save the amount which they deserve and they are always scared if things will continue this way ever?

So I wanted to know how many people are scared of future and they think that there are chances that they might not accumulate enough wealth in their lifetime which is required for leading a great life they desire. Here is what people say.

Around 51% of people said that they are scared of this.

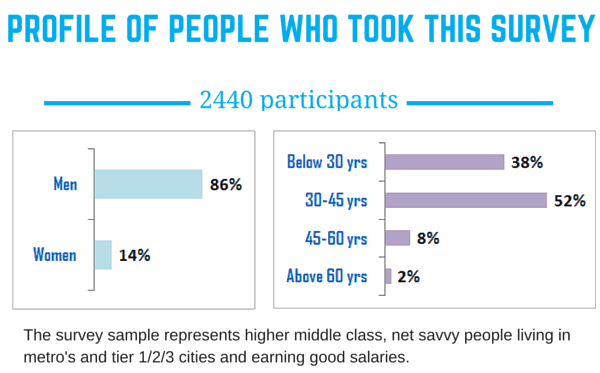

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.

With this, I would like to end this survey here. I would like to know what you feel about this survey and if you got any insights on how other people think in this country. I would like to mention very clearly that the survey size was 2440, which is surely not the representation of the entire country, but it’s a good enough sample size for the net-savvy higher middle-class people who live in big cities earning decent salaries.

The government has cut the interest rate on Public Provident Fund from 8.7%to 8.1% effective April.

This was part of the interest rate cuts in the small saving schemes and apart from PPF, other very famous instruments like Kisan Vikas Patra, Senior Citizen Scheme & NSC interest rates have also come down by a good margin.

These new rates will be applicable from Apr 1st. Please note that this is one of the biggest rate cuts in the small saving schemes in a long time.

Here is a summary of all the rate cuts

Kisan Vikas Patra interest rates down from 8.7% to 7.8%

NSC interest rates down from 8.5% to 8.1%

Senior Citizen Saving Scheme interest down from 9.3% to 8.6%

5 yr NSC (National Saving Scheme) interest down from 8.5% to 8.1%

1 yr time post office deposits has been cut from 8.4% to 7.1%

2 yr time post office deposits has been cut from 8.4% to 7.2%

3 yr time post office deposits has been cut from 8.4% to 7.4%

5 yr time post office deposits has been cut from 8.5% to 7.9%

Postal saving deposits remain unchanged at 4%

Interest rates aligned with market rates

On Feb 16, 2016 (before the budget) itself the govt had announced that they are working towards bring the small saving interest rates closed to the market rates, but that time no changes were done in these schemes.

The government had on February 16 announced moving small saving interest rates closer to market rates. On that day, rates on short-term post office deposits was cut by 0.25 per cent but long-term instruments such as MIS, PPF, senior citizen and girl child schemes were left untouched.

Now the interest on these schemes is closer to the interest rates given by the banks.

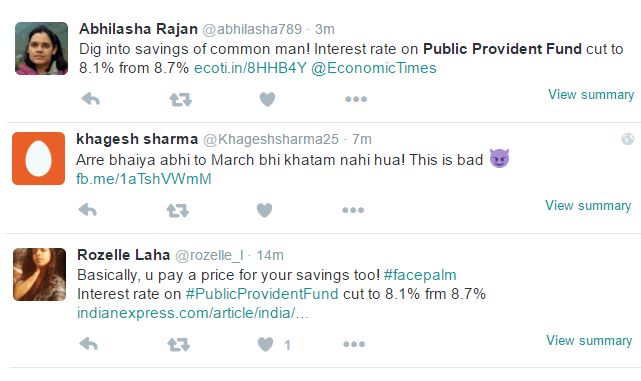

I will leave the decision to conclude if this was a good or bad move by govt on you, however the common man is not very happy with this. Messages against this move are are all over the twitter.

What is your reaction to this?

Majority of investors in India invest in Public Providend Fund (PPF) scheme and it’s very close to their heart. However this move will make many people think if PPF is the best thing they can do with their money or not (learn how PPF interest rate is calculated).

Will they move to equity markets because of this move? Will it make them interested in other kind of financial products?

What do you think? Do you think of this big interest rate cut in PPF and other schemes? Please share your views in comments section.

Are you looking for buying a plot or a piece of land? If not today, maybe you have this dream of owning a plot sometime in the future.

Buying land or plot has in a way to become a premium thing these days especially in big cities because the land is scarce commodity and the pride is associated with having your own plot where you can build the house as per your wish.

In this article I will tell you 10 important things that you should know before purchasing any property in India.

If you happen to visit any real estate exhibition, you will come across many plots projects along with the residential apartment schemes. These plots are generally within 20-100 km of the city radius and often marketed as a second home or vacation home.

On top of it, the pricing is attractive (often within 5-20 lacs) and there is also the facility of installments which makes it too easy to own a plot. The deal is often paying a token amount and pay the rest amount in parts (EMI).

However, a common man is often not aware of the risks associated with buying land and the complexities involved in it. Buying a land is a very different kind of ballgame altogether compared to buying a flat (which is much safer), and today I am attempting to make things easy for you to understand.

My Personal Experience

I have personally visited a few plot schemes myself over the last few years (near Pune). I have interacted with the salespeople and have some experience in this area. Hence, I will try to share what I know with you. If you can also add to my points, I would love to incorporate it into the article.

This article will mainly help a newbie with the simple checklists which they should look at before buying a plot or when they go to visit a scheme or if they are interacting with the salesperson (here is a checklist for buying apartments).

Note that this article is mainly keeping in mind plot schemes or gated communities, but most of the things will also apply for a standalone piece of land.

1. Is the land on the name of the builder?

The first question you should ask the salesperson is that if the builder has legal rights to sell the land or not. Find out who is the current owner of the land? Is it a builder himself or not?

A lot of builders either buy the entire land from the previous owner or enter into a joint agreement with the owners to sell or develop the land and sell the plot scheme. No matter what, make sure that this part is clear. Ask for the documents which clearly show the builder has legal rights on the plot himself.

2. Has the developer taken a loan from Bank for the project?

Builders often take a bank loan for the Plot schemes and even residential schemes. It’s a sign that the builder is more serious about the project and it’s also a positive sign, because if there is the money with builder which will be specifically used for the project development.

The builder is not dependent fully on the advance money the home buyers. It shows that there is a cash flow dedicated to the project and the issue of cash crunch will be minimized.

It’s not always the case the scheme has a bank loan, but still enquire about it. If bank loan is there, it’s proof that the bank has done thorough verification from their side on the legalities and only then granted a big amount (often in crores)

3. Where is the NA order?

By default, all the land in India is ” AGRICULTURE LAND”, unless it’s defined for some other purpose by the govt. So a piece of land is either agricultural or non-agricultural (commonly called as NA in real estate industry)

Agricultural land can be used for Agri purpose, whereas if you want to do any other thing other than agriculture then one has to first convert that Agri land to non-agricultural (NA)

However just because a land has got NA status, does not mean that one can start using it for residential purpose, because there are various types of NA like

NA – Commercial

NA – Warehouses

NA – Resort

NA – IT

NA – Residential (this is the one where one can build a residential house)

So if a plot of land is type NA – Resort, that means that that one can build a resort there, but can’t make a residential scheme. If a plot is NA – warehouse, then one can build a warehouse there for commercial purposes, but can’t make residential schemes and sell to the common man.

So you need to look for “NA – Residential” Plot

So, the point is that you need to ask the builder/salesperson, if the plot of land you are planning to buy is “NA-Residential” or not? Ask them for a copy of that. A lot of other kinds of NA plots are sold as “NA plot, collector approved” which is a misleading thing.

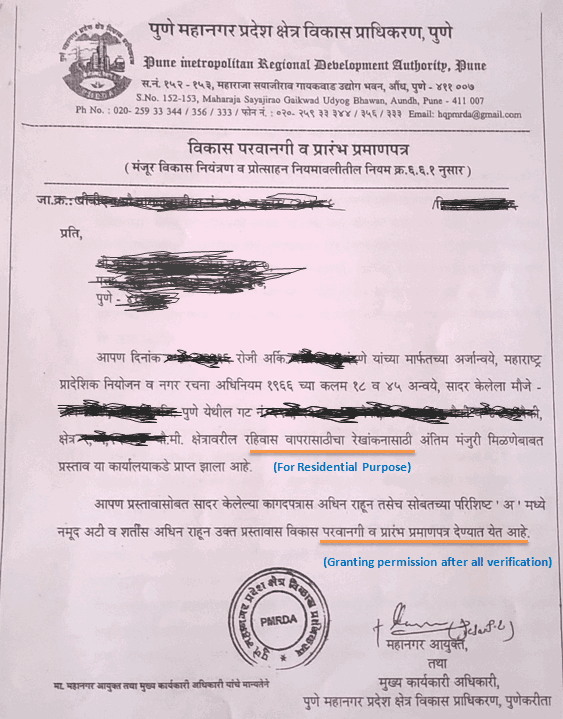

I am attaching a sample NA order below (from Maharashtra) for you too just get a feel of how it looks like

Another thing you have to be very cautious is “Proposed NA” schemes. A lot of builders try to sell a non-NA land telling you that its a proposed NA land, means he has initiated the process of converting a land into NA scheme, and the papers are already in process and “very soon”, the land will become NA-residential and how you will then reap the benefits of the high prices.

While there are chances that the conversion happens, but in most of the cases, its a gimmick to sell a cheap land at high prices and often buyers are stuck in the project, because the land is nothing more than a piece of crap later.

Don’t fall for it, because converting an Agricultural land to NA-residential is a very lengthy process in which a lot of approvals needs to be taken for it. There are cases where it’s been 10-15 yrs and it’s “still in process”

So, ask the salesperson to show you the NA order papers. Have a look at it yourself and do not fall for the promises like its coming in 2 months or next week or anything like that. Don’t get stuck into those kinds of deals.

Understand one thing very clearly, NA plots with clear title are limited and scarce, & often you will have to pay good price for it, If the land price is dirt cheap and it’s promised as NA-residential, there is a good chance that it’s fake or very very far away from the city limits.

4. What is the FSI for the plot?

Suppose you bought a plot of size 2000 sqft for building the house on it.

How much construction can you do?

Here comes the concept of the FSI or Floor space index. FSI simply means how much construction can be done on a piece of land and it depends on the location of the plot.

FSI of 100% means if you have a plot of size 2000 sqft, you can build a house of 2000 sqft on that. If the FSI is 75 %, then you can only build 1500 sqft of house on that 2000 sqft land.

The project I recently came across:

I recently came across a project called Royal Purandar near Pune when I went to visit a plot exhibition. The lady at the counter told me that the plot sizes start from 5000 sqft and go up to 40,000 sqft (which is very big). I was shocked to hear about so big plot sizes because 5,000 and 10,000 sqft plots are quite big.

However, when I asked her what is the FSI of the plot, she told me it was just 15%. So with FSI of 15 %, if you buy a plot of 5000 sqft size, you can just build 750 sqft of house, which is generally a small bungalow.

There is nothing wrong with that, but you should be at least aware of it.

Why FSI is very very important?

So understand that FSI has a very important role to play when you will construct something or even when you will sell the plot to someone else. Imagine 2 plots which are of the same size (2000 sqft), but with different FSI like 50% and 100%

Plot A (50% FSI) – You can make just 1000 sqft home on that, which will be like a 2 BHK)

Plot B (100% FSI) – You can make a 2000 sqft home, which will be like a 4-5 bedroom Bungalow.

But then it might happen that Plot A is selling at 10 lacs and Plot B is selling at 15 lacs, and you might say – “Plot A is cheaper because its less priced and the size is same (2000 sqft)

One important thing you should know is that FSI for agricultural land is very small generally. In Maharashtra, it’s just 4 %, which means even if you buy a 10,000 sqft Agri plot, you can only do the construction of 400 sqft on that land.

You should definitely ask the builder/salesperson to share the document which mentions the FSI on it. Judge the price of land only after learning about FSI, not just the area.

5. What are the other projects done by the builder?

You should ask the salesperson about the other projects done by the builder. Check if they have done other similar projects in the past? What was the response to it? What is the quality of those projects? Were there any legal issues with those schemes? Are the buyers happy with the builder work there?

You can often get some clue about all this on the internet or the online forums. Just go to the website of the builder and find out what are the other schemes he has done. Search with the other project names and see what others are talking about?

If you get a chance, I suggest paying a visit to past projects once. Spending half a day in this will only help you further to take the decision.

6. When will the Sale Deed happen?

You will often hear about the “agreement to sell” which is executed when you book the flat/plot and clear your initial payments (around 35-40%). This is the time when you pay stamp duty and registration charges. Once the agreement to sale is completed, a lot of buyers think that the flat/plot is registered on their name and now they are legally safe.

However, this is a myth and the “agreement to sell” does not make you a valid buyer. The agreement to the sale (often called ATS) is just the AGREEMENT TO SALE, which means it’s an agreement between buyer and seller on the initial points and terms under which the sale will happen in the future.

It mentions the terms and conditions of the deal, how much initial payments are you making along with cheque number and also the future dates, by when you will clear the payments, etc.

What is the “Sale Deed” document?

“Sale Deed” is the document that needs to be registered in the office of sub-registrar in order to make the sale happen. Unless the sale deed is done, you do not become a legal owner.

Hence, ask the builder or salesperson about the sale deed? When is it going to happen? The sale deed is generally done, only when the builder gets all the dues from your end.

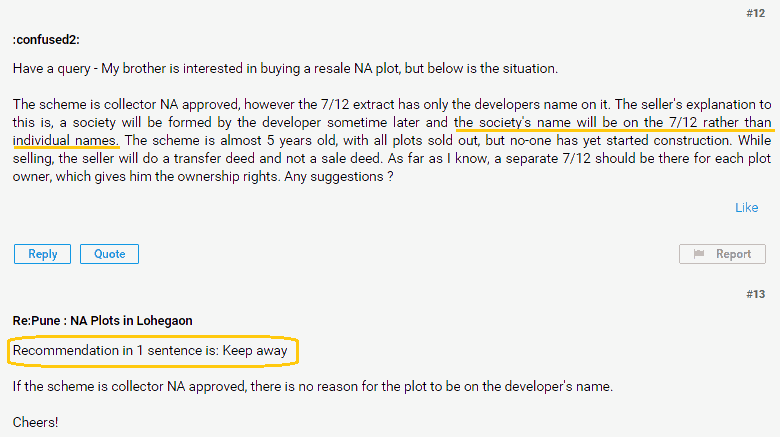

7. Will I get an individual 7/12 extract in my name?

Let me first help you understand what is “7/12 extract”? It’s a term which you will often hear in states like Maharashtra and Gujarat. In Karnataka its called 7/12 Uttara. It’s the document maintained by the revenue department which mentions how the land moved from one owner to another owner in the last 30 yrs.

So in a way, its a history of the land and you will find exactly on which date who sold to whom. This way you will find out who is the current owner of the land also.

For example:

If person A sells the land to person B, then it’s important that the name is 7/12 extract is changed from A-> B. Unless B name is not registered in the 7/12 extract, B will not be a valid landowner.

So it’s important to ask the seller about the 7/12 extract. There are many complications around this, like if you buy an agricultural plot from the seller in the name of “NA plot”, then your name will not be there in the 7/12 extract, because there are restrictions on who can buy the Agri land and even the minimum size restriction is there.

Also at times, the builder will tell you that the name of the builder will be there in the 7/12 extract, and not yours. Or the society name will be there in the 7/12 extract and not yours.

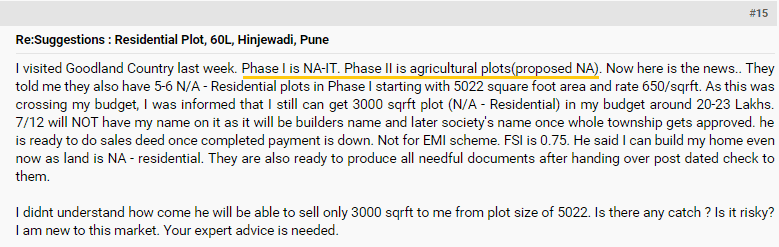

Also at times, what happens is that a big piece of plot is broken down into small land areas and sold to many people and a joint 7/12 is made, where all the buyer’s name is there in 7/12 extract (see the conversation below), which makes things very complex in future.

So make sure you enquire on this aspect properly, and if an individual 7/12 extract will be done or not.

8. What will be the per annum maintenance after buying the plot?

Once you buy the plot, there is annual maintenance that needs to be paid which goes towards maintaining the basic amenities like security, upkeep of the project, gardens, water, security etc. It should not be a surprise for you later. This maintenance is generally paid on a yearly basis and it’s proportional to the plot size. For example, if it’s Rs 4 per sqft and your plot size is 2000 sqft, then your maintenance per year would be Rs 8000.

9. Is the plot on flat land or on a slope?

Don’t assume that your plot is always going to be a piece of flat land. If it’s a big project, it might happen that the overall land which builder has acquired is uneven or has slopes. So when it’s divided into several small plots, many plots might be on the slope or it might be uneven.

You will ask what are the main issues when we build a house on land with slope or an uneven plot?

Below are some important points regarding the land on the slope from this website

If the plot is on a significant slope, either the land will need to be cut and filled, or you’ll need to build a house that takes that slope into account. It’s worth remembering that while these things might make your house more spectacular, they’re also likely to cost a fair bit more.

Depending on the angle of the slope and what’s built on neighboring properties, a slope can also reduce your exposure to sunlight – which in turn can affect how much light you get in living areas, and your potential to harness the sun both for passive solar heating and for collecting solar power.

Where we live in the southern hemisphere a north-facing slope is ideal for solar access – a steep south-facing slope not so much.

Below is how the project brochure looks like when its shown to you (often when the project has not yet launched or into the exhibitions)

By seeing this kind of image layout, you never get an idea if a particular plot is on slope or not. So it’s always a good idea to ask this question and verify it by visiting the site yourself.

10. What are the arrangements for water and other basic amenities?

Always ask how they are going to provide water and other basic amenities. Is it going to come from the municipality or the gram panchayat? Or they are doing their own arrangement for it?

And also ask some other questions like :

What about electricity?

Are they going to arrange for a individual electricity meter?

How much are they charging for it?

If the plot/land is too much away from the main road, then what about the access road?

Who will develop it?

What about fencing of plots?

What about security?

Ask everything in detail and in points.

With this, I think we have completed the main high level 10 things you should ask when you are buying a plot. Below is another video on this topic where some industry-level people are talking about the same issue of buying land and the complexities involved.

I strongly suggest watching the 15 min long video below

Now we will see some important points which you should keep in mind before you buy the plot.

Important tips for someone buying a land

Do not hurry. Period! – Buying land is an emotional decision and often salespeople use a lot of tactics for selling the plots (just like flats). Don’t believe the seller when they say that just 12 plots are remaining or the prices are increasing next quarter when they do their “Mega – Launch” . It never happens.

Make many visits to the plot – Don’t book the plot just after one meeting or without visiting the plot yourself. I would say that one should make at least 3-4 visits before the deal. Try to visit the plot once when your salesperson is not on the site. Just make a surprise visit and ask others on the site about important points and you might find some new information about the plot which was not told to you

Check the nearby development yourself – Don’t believe the salesperson about the nearby development information. If the salesperson says that a new flyover is coming up nearby or if there are 3 colleges within a 2 km radius, just find it out yourself.

Talk to people nearby the plot – If you can go a bit further, see if you can talk to people who live nearby the plot. Make a random visit and then ask the shopkeepers nearby, houses nearby on the points which concern you.

Bargaining for the price – Often the list price quoted for the plot is never the final price. In a country like India, it’s a well-known fact that there is always bargaining. So you can easily assume a 5-10% margin. Ask them to reduce up to 10% price and then settle for at least 5%. Take a lot of time to decide and often you will see the prices coming down. It’s very important that you do not show your desperation on buying and also share with them some names of nearby projects and how you also like them and you need a strong reason to buy a plot from them

Search online about the plot scheme or the area of land – Always search for information about the project or builder online. You will often come across others who have visited the site, or interested in the same project, you can connect with them and discuss it

I hope this article has given a good knowledge to you about the important things you should ask and keep in mind before you buy a plot into some scheme.

Beware of small unknown builders for plot projects

By now I think there is no need to tell that land buying is very complicated and one should not attempt it if you do not have the risk appetite for it.

There are many small flies by night people who know how mad people can get to own a plot of land and they come up with schemes where their sole intention is to make money for themselves and cheat customers. Please see this below video where some buyers are sharing their real-life experience of buying a plot and getting cheated.

I would strongly recommend that you involve a good property lawyer for verification of documents and the legality of the project. It would increase your cost a bit, but then it becomes a more secure investment.

Please note that all the points I have mentioned above, are based on my knowledge and understanding. If there is any correction to be done, please share that with us. Also please share your comments and views in the comments section below.

Have you ever bought the wrong financial product? Or it was mis-sold to you out of pressure from family/relative? Or because you trusted the seller too much? If not these reasons, maybe you wanted to do last minute tax saving and you jumped into buying that policy and gave yourself a life sentence of paying premiums which will not help you much in long run?

We are today going to discuss all sort of issues which arise when you get into a wrong financial product and why you should avoid it at any cost.

Background

Let me first give you some background on how I got started with this article. Here is what happened.

A few days back, I was once watching a TV show and there was a story of a woman who married a guy out of the pressure of family who wanted to get married as such as possible. She fell for the short term tricks and didn’t pay much attention to those points which matter in the long term.

Soon after the marriage, she started realizing that she made the mistake. It’s not what she wanted in life and its not a match which can sustain. Life was a mess. She was stuck in this relationship.

Coming out of it was not easy. She was in depression and all the time was going into regretting the decision. Almost 5 yrs had passed and by this time, a lot of her energy and time had got wasted.

Finally, she came out of that bad marriage. Often she wondered why she took such an impulsive decision? What if she had never got into that bad relationship? How would have her life shaped up?

Investors do the same thing with financial products

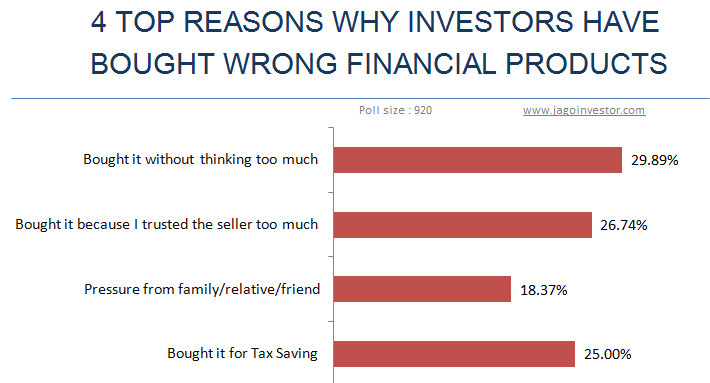

A lot of investors buy unsuitable or wrong financial products in their financial lives and it drains their money and valuable energy. It gives them unnecessary tension, which could have been avoided if they were a little more prudent in their financial life. Below are the top 4 reasons why most of the people have bad financial products in their life. I surveyed 920 people, the top most reason why because they were careless themselves and bought things without much thought. Where pressure from family/friends was not the major reason.

The careless attitude costs them too much trouble. I have worked with more than a thousand investor now, and I can tell you most of the good financial lives which we see are not because of making good decisions, but by avoiding bad decisions. Most of the people who have high net worth or powerful financial lives are those who have not wasted their valuable time and money in wrong financial products and concentrated on simple things.

One bad move can nullify 2-3 good decisions.

Today I want to talk about 4 core problems that arise out of buying the wrong financial product. Let’s look at them one by one.

[su_table responsive=”yes” alternate=”no”]

Problem #1

Waste of money

Problem #2

You feel “stuck” and waste your time and energy

Problem #3

The opportunity Cost

Problem #4

You lose trust and everyone looks like a “cheater”

[/su_table]

1. Waste of Money

Nothing hurts investors more than losing their hard earned money. When you buy a wrong financial product, most of the times, you lose money or do not get the returns your hard earned money deserves. A few years back ULIP’s were one of the most mis-sold financial products. Millions of investors have lost their hard-earned money in these products. The charges in the first year were huge at that time which ate away all the returns one got. On top of it, the returns of the ULIP were linked to the stock market and most of the investors never knew this.

Because of this, a lot of investors lost a big chunk of their money in these products.

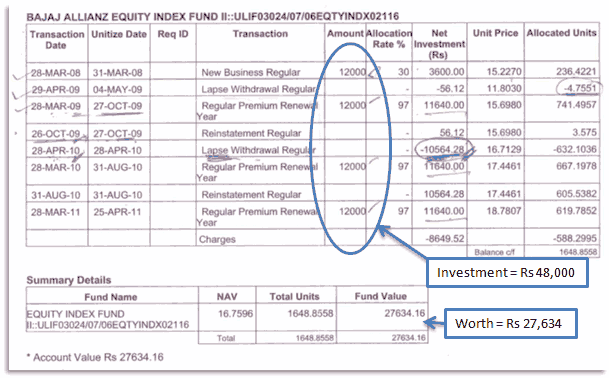

Below is a snapshot of one of our readers who bought a ULIP in 2008, and he paid a total of Rs 48,000 in the ULIP, however when he checked his statement after a year, his fund worth was just close to Rs 27,000.

The value of the fund had come down due to market movements and commissions structure, but the main point is that the investor never expected it. He didn’t know that it could happen because, at the time of selling, there was no communication of the risk part. This is what happens when one buys a financial product without understanding it.

Then there are other kinds of products like endowment insurance policies which does not pay you back your full money if you surrender them in between or very early. Its the product design. If you pay Rs 50,000 per year premium, then in 4 yrs you must have paid Rs 2 lacs in total. Do you know much would you get back, if you wanted to close the policy and take your money back? On average it would be just 40%-45 %, which means only Rs 1 lac you will get back.

Forget financial products, some time back I bought a sim card which was available on purchase of an internet connection and there were some attractive benefits associated. I fell for it and bought it without giving much thought. I spend a good amount of time and energy behind it, paid bills without using it and finally ran around to close the connection. I could have avoided a lot of pain, had I just ignored it. The same is true for various credit cards, unwanted memberships, etc.

2. You feel “stuck” and waste your time and energy

Forget money, what about the time and energy you waste? Once you are stuck with the wrong financial product, you will keep thinking about it. You will keep regretting your decision. The financial product will be part of your life and you will often wonder why you invested in it?

Most of the people anyways take a lot of time to take financial decisions and just imagine what happens if one of those decisions is wrong or bad for you? You will keep cursing the agent, your financial planner, yourself, the system, SEBI, IRDA and every other person (even yourself).

You feel STUCK …

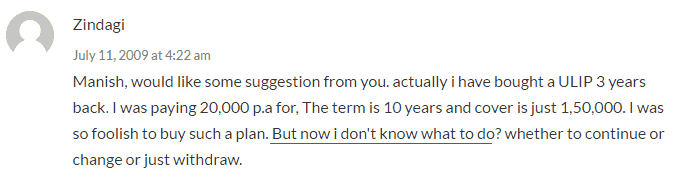

Nothing is more frustrating than feeling stuck and not being able to do anything fruitful. There are millions of investors who are stuck with their endowment policies, ULIP’s, bad credit cards, wrong advisors, other products. They want to get rid of it, but they DON’T.

Also, the world is cruel, you as investors are taken for granted. See how one of the readers, when tried to surrender his LIC policy, was treated.

Hello – I approached the branch manager on cancellation – it’s not even 7 days – he is asking me to get the agent to the branch! is this correct ? I have a question : If I want to surrender the policy or retrieve the maturity amount , is the agent required , this is weird stuff , If this is not true, please help me how this can be escalated and resolved .

Over-analysis leads to more delay

Investors also over analyze what they need to do once they realize that they bought something bad? How to minimize their losses and how to come out clean. But in that process more and more time passes and the situation gets messier compared to the past. Most of the people keep delaying their policy surrendering for years and the damage keeps compounding.

It’s like you bought a bad stock and you didn’t sell it off when you had a 10% loss. You wanted to get out of it at the right time and then it will send down by another 10% and then another 20% and finally out of frustration you sell it at 50% loss wondering why you didn’t take 10% loss itself at the first place.

In the same way, most of the investors keep thinking about the loss they are going to make if they get out of the bad financial product and keep postponing their decision. Here is one comment from our blog where an investor shares his state of mind. You can see that he feels so stuck. This is a very common problem

Our lives are very busy these days and if one pending item gets added to our list, it takes months and years to complete it, even if it’s just a few hours of work!.

So the big problem which happens when you buy a wrong financial product is that you waste your valuable energy trying to fix the issue. That precious time should have gone into earning more money and managing it well.

3. The opportunity Cost

Opportunity cost here means what is the other thing an investor could have done had he not got into a bad financial product. This is a very important thing to understand for financial success. Imagine a bad decision, where you invest Rs 5 lacs and after 2 yrs, your money worth is just Rs 4 lacs. You are in a loss of Rs 1 lac ?

NO, it’s not just Rs 1 lac.

Why?

Because you could have taken the right decision and could have made a profit which you lost in addition to the real loss. In that same example I gave above, you could have invested Rs 5 lacs in such a way that it would have become 6 lacs in 2 yrs. So your opportunity cost is Rs 1 lacs which you didn’t make here. Instead, you are sitting on a loss of Rs 1 lac.

Another example is of a young investor who wants to create a big corpus in the long term, but he/she is maximizing the PPF by investing Rs 1.5 lacs per year in that.

After 15 yrs, they will get a near inflation return only. I consider even that as a bad decision looking at the goal of wealth creation. The same 1.5 lacs can be invested in an equity product and a better inflation-adjusted return can be earned. The final wealth different in case of equity vs. PPF will be quite a big amount. The difference between 8.5% return compared to a 12% return is huge.

4. You lose trust and everyone looks like a “cheater”

Do you know how does it feel when you take some financial decision by trusting someone and you lose money? The tweet below was done by Kalpen Parekh, CEO Of IDFC Mutual funds.

When investors hear us say, it’s cheap so buy more, this is what Dharmendra will say! pic.twitter.com/UIHLdhpzAC

Money is a very private matter and most of people are very very attached to it. When an investor gets a bad experience once, they carry it with them for a very long term. Every other person starts looking like a cheater to them. Everyone seems to be behind their money and it’s tough to trust others.

It’s a very natural reaction, but the problem is that it also damages the investor’s chances to get into a good association too. There are many investors who contact us for their financial planning and many of those who have faced bad experiences in the past never move ahead because it’s difficult for them to trust someone now.

Imagine a guy who has had a bad experience with ULIP, someone who has lost his money due to market movements, will find it very tough to start his SIP’s in mutual funds for his long term wealth creation. This is a big loss for himself based on his past experience.

I know few investors who have vouched to never buy any other financial product other than a fixed deposit because they felt cheated in the past.

So what is the point I am making? If you take the wrong financial product, then it affects the way you think about financial products and advisors in the future.

How to buy financial products?

I am not going into detail here, but one thing is clear. You have to take out the emotions out of it. No greed, no fear, no pressure, no over trust on others. Make sure you understand what you are buying, why you are buying, for which goal are you buying, what are the risk factors, etc.

If you spend just 1 hour before you get into a financial product, I think 95% of the investor’s woes will be solved.

What do you feel about this article? Do you have more points to add?

Before I even start this article, please watch the first 5-6 min of the following video which comes from Ravish Kumar of NDTV and you will get the hottest points of discussion in this budget, which is taxation on EPF withdrawal.

The video below discusses various viewpoints from govt representatives, economists and some other people on why this is a foolish decision from govt and at the same time, why it makes sense to tax the EPF withdrawal. You will listen to the full video if possible for you, or else at least listen to the first half.

So, I was watching Budget 2016 yesterday and desperately waiting for the personal taxation announcement because that’s the main thing I understand :). By the end of the budget speech, it became clear that there were no changes in income tax slabs nor 80C limits and all hell broke loose on the news that the EPF withdrawal will be taxed on the 60% corpus.

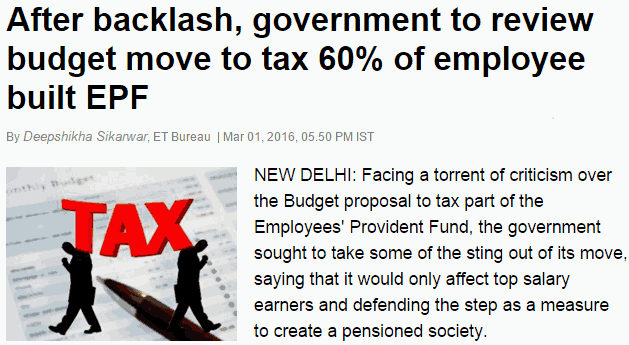

The whole twitter and facebook was full of angry people showing their disappointment on the budget and how it has betrayed the salaried class. The issue went really out of hand and a twitter trend #RollBackEPF started trending and every person from across the country wanted it to be taken back. It was really a crazy day. And today govt has clarified that the tax is only applicable on the interest component only (more on that later in the article)

This budget’s major focus was on the rural economy and farmers which are neglected for decades anyways. Only time will tell if the efforts were taken in this budget work or not and if things improve and get better for farmers and rural economy. Let’s wait for that.

While there were many things in this budget, on the taxation front and other announcements, nothing major was there in this budget for a common man on taxation front and that made the salaried class very very disappointed.

Let’s look at the budget highlights one by one. My focus is to share all the major points which concern or are related to a common man.

1. No Changes in Tax Slab rates or 80C

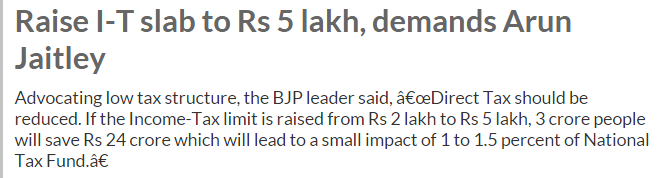

Let me again share it. There was no change in the income tax slabs or the 80C limit. Everything remains the same on this front. Everyone was expecting that the slab will be raised or 80C limits will be increased, but that didn’t happen. There were conversations like the basic exemption limits should be raised to at least Rs 5 lacs from the current 2.5 lacs, and this was, in fact, Arun Jaitley’s demand in 2014 that the limits should be raised. Not sure what’s coming in his way now when he himself is the decision-maker.

2. Up to 40%, NPS withdrawal maturity becomes tax-free

Now 40% of the NPS corpus will be tax-free at the time of maturity, rest 60% corpus will be taxed if you withdraw it fully. However, if you buy an annuity (pension) from the remaining 60% corpus you won’t have to pay the tax. However, note that the pension amount which you will get will be normally taxes as the income in your hands.

This means that if you have Rs 1 crore in NPS at the time of maturity, if you withdraw the full amount, then 40 lacs will be tax-free, but the rest 60 lacs will be taxed. Now if the applicable tax at that time is 20% (just an example), then 12 lacs will go in tax and you will get the remaining 48 lacs in our hand. So a total of 88 lacs you will get out of 1 crore. However, you can choose to just take 40 lacs in hand and leave the 60 lacs in a pension product to generate the monthly income (which I think many will choose anyways).

One good point is that if the NPS holder dies, then the full death claim will be tax-free in the hand of the receiver.

3. EPF Interest becomes taxable for 60% corpus

As I said earlier, the EPF was the center point of discussion after the budget speech and govt has clarified that only the interest component will be taxed at the time of withdrawal and that too only on the 60% corpus. The 40% part will be tax-free fully. Note that this is applicable only on the interest earned after 1st Apr, 2016. The interest earned before this date will be tax-free.

Also, an important point here is that there is a lot of debate and confusion around this point as of now. We should wait for more clarification on this from govt in the coming days.

4. PPF remains tax-free (its still EEE)

PPF is untouched and still remains full tax-free as of now. Yesterday there was this confusion, that NPS, EPF and PPF, all of them are brought at the same level and many worried people whose PPF was going to mature in the coming months/years panicked and started asking if their PPF corpus will also get taxed.

So at this point of time, PPF remains the only investment product which comes under EEE (Exempt, Exempt, Exempt)

5. Employer contribution in EPF restricted to 1.5 Lacs per year

Now an employer contribution is EPF is restricted to Rs 1.5 lacs per year or 12% of the basic salary whichever is lower. Till now there was no limit like that, but with this budget that is changed. Incase employer does contribute more than 1.5 lacs per year, then it will taxable in employees hand.

Also, note that the govt will now contribute the 8.33% EPS part for the employees from its own pocket for the first 3 yrs for the new EPFO members.

6. Health Insurance of Rs 1 lacs for Senior Citizens

There will be a health insurance scheme launched soon which will provide Rs 1 lac of health cover to poor families. Also, the senior citizens who belong to these families will also get an additional Rs 30,000 top-up cover on top of Rs 1 lac. The govt budget documents give the reasoning for this scheme.

Catastrophic health events are the single most important cause of unforeseen out-of-pocket expenditure which pushes lakhs of households below the poverty line every year. Serious illness of family members cause severe stress on the financial circumstances of poor and economically weak families, shaking the foundation of their economic security

7. HRA exemption under Sec 80GG raised from 24k to 60k per year

As per sec 80GG, those who do not get HRA in their CTC from their employer can now claim up to Rs 60,000 per year as a deduction under rent paid. Earlier this was only Rs 2,000 per month. This will help a lot to those people whose employers are not giving them HRA Component. Rs 5,000 though is a less amount, but still a respectable deduction at least.

In other word eligibility will be least amount of the following :-

1) Rent paid minus 10 percent the adjusted total income.

2) Rs 5,000 per month. (this was Rs 2,000 earlier)

3) 25 percent of the total income.

8. First time home buyers to get extra Rs 50k deduction in Interest

The first time home buyers will get an additional Rs 50,000 tax exemption in interest part apart from the current exemption, provided following points are true

The loan amount should not be more than 35 lacs, and the value of the house should not be more than 50 lacs

The loan should be sanctioned between 1st April 2016 – 31st Mar 2017

The home buyer should not have any other residential house on his name

9. Dividends above Rs 10 lakh to attract an additional 10% tax

Now if a person is earning more than Rs 10 lacs of dividend from stocks will have to pay the tax of 10% on it. Right now companies anyways pay DDT (Dividend distribution tax) on the dividends declared. I think this is anyways going to impact only those who have very high investments in stocks and they earn big dividends. A normal investor will mostly be out of this.

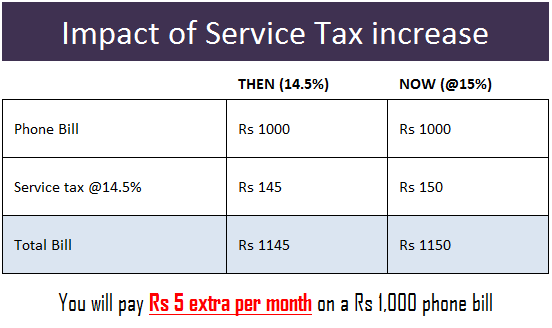

10. Service tax increased from 14.5% to 15% due to Krishi Kalyan cess

A new cess called Krishi Kalyan cess of 0.5% is added to service tax, which is applicable to all taxable services, which simply means that the service tax has now gone up from 14.5% to 15%. While this 0.5% does not look much, its actually going to be a decent amount for a common man in addition to what we pay.

That means an extra Rs 2 in the bill if you have food worth Rs 1,000 in a restaurant.

That means an extra Rs 5 in your phone bill of Rs 1,000

I think it will add a few hundred extras in your expenses if you count entire years of expenses. This will be applicable from 1st June, 2016 so you still have some time 🙂

11. TDS of 1% on buying cars above Rs 10 lacs

1% TDS is proposed on the purchase of luxury segment cars costing Rs 10 lacs or more. The same TDS is also there if one buys any goods or services exceeding Rs 2 lakh. On top of this, an infrastructure cess of 1% is on small petrol cars, CNG cars and 2.5% cess on diesel cars are there, which means that cars, in general, become a bit expensive.

Even the branded clothes and tobacco items will become costlier due to the excise duty increase

12. Possession period for property raised to 5 years for claiming tax benefit

Earlier, if one used to buy/construct a property, one had to get the possession in 3 yrs itself to claim the tax benefits on the interest paid under sec 24. Now it has been raised to 5 yrs. This will help those real estate investors who have not got the possession due to delays from builders.

13. Tax Rebate of Rs 5,000 for those with income less than 5 lacs

For small tax payers with an income of fewer than 5 lacs, the tax rebate is increased from Rs 2,000 to Rs 5,000. This means that if the income tax payable is upto Rs 5,000 for small tax payers, they don’t have to pay it. Rs 5,000 will get deducted from the tax payable. So if a person is earning Rs 4 lacs (taxable income), then as per slab his income tax is Rs 15,000 (10% of the income above 2.5 lacs), out of this Rs 15,000 tax payable, he will get the rebate of Rs 5,000 and he will pay only Rs 10,000. This was earlier set at Rs 2,000 only, but now changed to Rs 5,000

14. ATM’s in Post offices

Over the next 3 yrs, govt plans to roll out the ATM’s in post offices so that more people in rural areas can access the banking services. The department of Posts plans to bring around 25,000 post offices under this in the next few years.

There are many more things in the budget, but I am not going into each of those. The points above are the main highlights which I am discussing here. You can read all the points of budget in this PDF file

Please share how do you rate this budget and what do you think about the move on the EPF taxation?

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.