I am happy to share this news with you all, that my 2nd book is going to release in next few weeks, whose title is “How to be Your Own Financial Planner in 10 Steps” . The book is published by CNBC 18. The book is now ready for pre-order, so you can order it now, it will be delivered to you as soon as it hits the stores which will happen in just few more days.

About the Book

By the time you complete this book, your financial life will have taken new shape!. You will have worked on 10 different areas of your financial life, in the same way a certified financial planner works with you. The book has the ability to guide you on how to plan the 10 most important areas of your financial life. There are two types of investors in India, those who plan their financial life and those who plan nothing and just let their financial live move with the flow. The second group is extremely large, and this book is targeted at this group.

Many investors who are DIY (Do It Yourself) investors can use this book to plan their financial life and be their own financial planners at some basic level. The book has the 3 elements of education, planning and action items all packed into one. Written for the common person, in simple language, the book deals with the most important financial worries and questions.

What are you waiting for ?

Anyone who feels that he can do his own financial planning and with a little support and direction he/she can plan his financial life, then one should buy this book. There are 10 chapters which cover 10 different areas of your financial life and helps you understand those areas, what you need to do about it, how you should mess it up and guides you to plan it out in simple and easy language. Each chapter has action oriented exercise at the end of each chapter, so while you go through each chapter, you will keep on making your action item list and finally complete things. I would say grab the book today, because this is the best it can be. If you need external support, you can always go for our online financial advisory services.

UPDATE – First Book Name is Changed

I have one more news to share. My first book “Jagoinvestor – Change your relationship with money” was a great success. However we are changing its name to “16 personal finance principles every investor should know” to make sure that the name of the book reflects what the book is all about. The book content is exactly same, just the name is changed now. So its now in new avatar.

Thanks for your love and support, because of this awesome community, it was possible to give shape to these 2 books. While the first book is more on the principles of personal finance which every investor should know, the second book is all about planning and taking action. I would be waiting for your reviews about the book.

You might have seen a section in your Cibil Report which says DPD (Days Past Due). While Loan Status and Credit Score matter a lot when it comes to getting a loan approved or rejected, a big myth among people is that a clear report (without SETTLED or WRITTEN OFF status) and a credit score above 750/800 are the only two things that they need to get a loan.

at

That’s not true. While a clean report and a good score are definitely primary level requirements for getting a loan approved, there are finer details which a bank looks at, before deciding if they want to give you a loan or not; and Days Past Due or DPD is one of those important metrics. Lets understand this then …

What is Days Past Due (DPD) on a CIBIL report ?

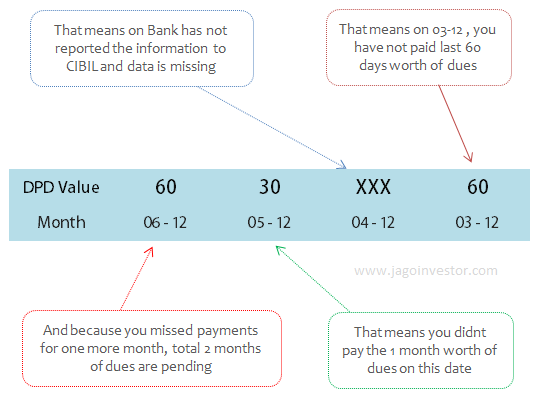

Days Past due or DPD means, that for any given month, how many months worth of payment is unpaid. And this information is for each account . Which means that if you have 3 different loans going on, then you will have DPD information for each of those accounts. For each account you can see Days past due information for each month for the last 3 years , i.e., 36 months.

You might already be aware that your cibil report contains the past 36 months of your credit information. Each and every month, your lender who is a member of CIBIL, will update the CIBIL with the latest information like Did you pay on time or not? How much outstanding loan do you have at that moment? How many months worth of loan is remaining and other micro details are shared on monthly basis by banks and lender to CIBIL. So each month, a new month’s data is added and the oldest month (36th month) is removed from the cibil report and this way a sliding window of 36 months data is available on your cibil report at any given point of time.

Example – Date 06-12 and DPD value is 90

If DPD value is 90 for a date say 06-12, it means in June 2012, the payment is due for last 90 days, which means 3 months dues! So you can now understand the the DPD in the last month (May 2012) would be 60 and for Apr 2012 would be 30.

When you default on any payment or do not make the full payment, this DPD value will start getting a number and it will be a negative thing. So if there is a cheque bounced from your side and the loan not paid on time, you can expect one entry of DPD for the latest month with value 30 – which says one month of dues are not paid. If you clear it on time before the next cycle comes, it will help you to improve your bad credit score and the DPD value for next month again will be normal, but if you do not make the payment and keep those dues , then the DPD value for the next month will increase to 60, which implies that from 2 months you have not paid the dues. See the graphic below to understand more examples of DPD

What does XXX means as DPD Value ?

There are certain values which can appear in DPD section and each of them has some meaning, however the safest values are 000 and XXX . If you have the value as 000, it means the dues are totally clear on that date and nothing is outstanding. And if the DPD value is XXX, then it simply means that bank has failed to report the data for that month to bank, and it does not impact you at all . At times instead of 000, the value can be STD which means that the dues are for less than 90 days . While any other number other than 000 is a negative thing, but make sure it does not go above 90 days , because then its super negative.

At times, some lenders also report DPD values in a different way, as per asset classification norms set by RBI. In that case, the values which appear under Days Past Due section are STD , SUB , DBT or LSS which denotes good to bad , where STD is good and LSS is the worst one. Here is what each of them denotes

STD (Standard)

Payments are being made within 90 days. Note that any delay of more than 90 days is seen as Non Performing Assets (NPA) by banks

SUB (Sub – Standard)

An Account which has remained NPA for upto 12 months

DBT (Doubt ful)

The Account which has remained Sub Standard Account for a period of 12 months

LSS (Loss)

An account where loss has been identified and remains uncollectible

Can DPD values be changed ?

There have been cases that lenders have rejected loan applications based on DPD information even though the credit report was clean and the score was quite good. And the common worry at the time is “Can’t I change my DPD information somehow?” and the answer is NO . You can’t change DPD information like you can change SETTLED or WRITTEN OFF status by taking some action. All you need to do is wait for some time and as time passes, new month information will get added to your report and old data will keep getting phased out. So if you have some bad DPD data before 12 months, then it will go out in next 24 months, and if you have some DPD data 2.5 years old, it will go out in 6 months period.

For those who like to learn through video’s, we have a 40 min course on Credit Report and Scores in detail on our Jagoinvestor Wealth Club, which will explain all the aspects of the subject in a clear manner and great detail

Did you understand the meaning of Days past due or DPD which appears in CIR (Cibil Report) ?

Let’s talk about Women and Inheritance today. Our Indian culture, has for thousands of years treated men as someone who lead families and be the heads of next generation and women as someone who will go to some other family after marriage and start a new life. This has been deeply rooted in all our minds for years and years. This is one big reason why women in India are not aware about inheritance laws and their rights in property.

Some families, where there are sons and daughters both, do not even raise the point of dividing the property equally among all of them equally. Daughters who are married are not even in picture at the times, the wealth is divided and it’s considered natural and something that makes sense. Women on the other hand also do not take any lead or don’t bother asking for their fair share in the family wealth.

Brothers do not share wealth with Sisters

You must have seen cases like these and might be experiencing them in your family as well.

Case 1 : I know a family which had 1 brother and 3 sisters and who had a huge property in Mumbai at a central location, lots of shares, mutual funds and bank accounts, When the father died, people cried and after a month every body was back at home, all 3 daughters who are married didn’t even think for a second that they have a huge 25% share in the wealth, which is a decent amount by today’s standards. All 3 daughters are not so well off and struggling day in and day out, but they are just not considering the option to ask for their share. Legally if they want, it would be just a matter of a few months or years and some bitter experiences, but they might reach their financial freedom if they go to court. But they are too emotional to take that step and worry about relationships and the problems which arise out of it.

Case 2 : In another case, there are 2 brothers and 2 sisters (all married), and after the father’s death, the brothers are fighting with each other for property “Father spend so much on your education, my career was affected because of that, So I should logically get more now.” Fair point logically, but from legal point of view, it does not matter much how father treated whom . The sad part of this story is that brothers are fighting for their share and also sharing their plight with their sisters, but not for a second do they think that even sisters are legal heirs and should also get their share. (Incase you didnt knew – Hindu Succession Law is applied when a WILL is not written)

It’s not Fair!

Just because now they are part of another family, they are not seen as valid heirs. I am raising this point today because this is wrong practice. Women now have to raise their voices and ask for their share from their parents and brothers. If required, ask for it legally. Just because father has spend lot of money on wedding of sister and given her gold does not mean she can be cut off from the family wealth sharing.

If father writes a WILL saying that he wants to give his wealth in some specific proportion, then it’s fine, it’s your father wish. But if a WILL is not present, then you are a valid legal heir, you should ask for your share and you will get it.

Look at it as part of your Financial Plan

If you are a man, your wife might be entitled for her share of wealth from her parents’. In today’s world where money has become so important, see if you can convince her to ask for her share. It might get her valid share of money and can help you in leading a better financial life. I am not saying this because you should be money minded, but because its a fair thing to ask for.

We have created a 2 part video program for Women and Money for our wealth club members. If you are a member there, please show this video series to your spouse.

Do you have any personal experience like this? Can you share?

Do you make a choice or take decisions in your financial life ? A lot of people have not taken lots of important actions in their financial life, which they should have taken long back!. You have to understand that you are making a choice by not taking those actions. When you take some action or do not take an action, deep down you are actually making a choice in your financial life, which we will see now.

Let me give you some examples

1. Buying Endowment & Moneyback Policies

Most of the people who take the decision of buying endowment and moneyback insurance policies , they say that they are buying it because they trust the company and want safe returns. Now that’s their decision, however they have to be understand that deep down they are making some choices which are unspoken …

They are choosing to get below inflation returns on their investments

They are choosing to put money in something which is illiquid and might not help them in emergencies

They are choosing not to cover their family with a higher life cover

2. Not buying a Term Plan

“I don’t think I will die” or “It does not give back money at the end” – this is the general reasoning behind not taking a term insurance plan by many people. Now, again, it’s their decision based on their belief, but deep down they are making some choices which are

They are choosing a life of struggle for their family, in case they are no more in this world

They are choosing to pass on all the debt and tension to their spouse and children in future

They are choosing that their children and family might not lead a great comfortable life in future if they are not around.

3. Not buying Health Insurance

“I will take is next month” and “I drive carefully and I am healthy , so I don’t need it” are the top most reasons given by those who avoid taking health insurance. Again, they feel it’s a right decision and I am not commenting if it’s right or wrong, but surely they are choosing few things in their life and for their family …

They are choosing to get into a situation where they might have to run around for money to fund health related expenses

They are choosing to constantly worry about big ticket health related expenses if any

4. Not creating a WILL

It’s a decision taken by almost all of us. “We are still young”, “I will do it once my net-worth is at least 1 crore” etc., are the common reasons behind not making a WILL. However deep down you are making few choices and you have to accept them …

You are choosing a lot of frustration, chaos and running around for your legal heirs

You are choosing, that your family will have to meet lawyers, go to courts and spend lots of money and effort to get what they deserve

You are choosing to create a confusing situation, where your legal heirs fight with each other and try to justify who deserves what

5. Not hiring a Financial Planner (when you really need it)

“I can do it myself, I was a bright student all my life”, “They charge a lot for what they do”, are some of the reasons given by investors for not hiring a financial planner for themselves. It’s their decision based on their beliefs, but deep down you are making some choices …

You are choosing to still do trial and error and play with your financial life

You are choosing to not organize your self and get into a dedicated structure which can improve your financial life

You are choosing to focus on what you will spend rather than what you will get out of the whole exercise.

You are choosing to delay your actions and rely on yourself for taking actions and get disciplined which most fails most of the times

6. Over spending right now like there is no tomorrow

“Life happens NOW”, “If I don’t spend, whats the point of earning well”,“I will earn more in future, let me enjoy today” – These are the top most things you will hear people saying who over spend (more than they should). One can comment easily if it’s right or wrong, but let’s not get into it, it’s their decision and there is nothing wrong in it, just that these people need to understand the choices they are making without realizing them

They are choosing to have a struggling financial life in future in case tomorrow does not turn out to be like what they imagined

They are choosing to have a better today at the cost of tomorrow

They are choosing to be working for more years in future, because they will not have wealth when they are old.

They are choosing to have a less comfortable life later in life, when responsibilities increase and opportunities decrease

Conclusion

At the end of the day, you always choose something in your life out of the decision you make. This is true for all the aspects of life, including your financial life. So understand that you are fully responsible for what you get.

Can you share your story in short and share what choices have you made in your financial life ?

Do you have any idea about your income tax refund status ? Have you filed your Income tax return long back, but have no idea when will you get your tax fund?

This is one issue faced by millions of tax payers in India. They file an income tax return where they claim back their income tax refund, but have no idea what happens to their cases after that!

For months and years, they keep waiting for the refund status, but they have no idea when they will get their money back. Ideally they should get it back in few months, but in many cases they wait for as long as 3-4 yrs.

In this article, we will see how you can find out your income tax refund status online and how you can use RTI application to find out the status of your tax refund and speed up the process of getting it back.

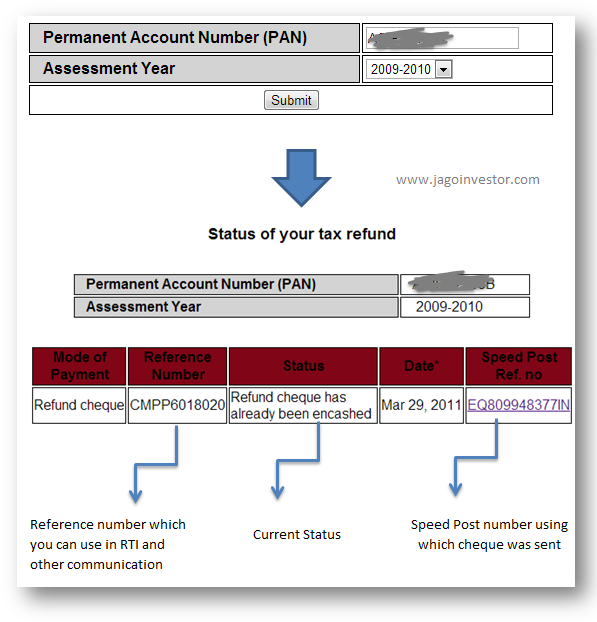

How to find income tax refund status online

If you have filed income tax return asking for your tax refund, and you have no clue about the current status, the first thing you do is track its status online. All you need is your PAN number and assessment year for which you have applied for refund. Here is what you need to do

You can also track your income tax refund status by contacting the help desk of SBI at 080-26599760 or contacting the Aaykar Sampark Kendra at 0124 2438000

File RTI application for income tax refund status

If you are not able to do much and you feel that just finding out online status is not helping you and you want to now get 100% clarity about your tax refund status, the next step is to file RTI application against income tax department.

We have earlier seen how one can use RTI to find EPF withdrawal or transfer status and how their issues were solved within weeks and months of filing a RTI against EPFO. So your next step is to file RTI in your tax refund case also. But you should wait for at least a year before you file for RTI against the income tax department.

Note that the RTI application has to be addressed to CPIO officer. Now the next question is how to find out the CPIO information. It’s actually not organized in a clean manner, but you need to start by going to this website https://www.incometaxindia.gov.in and then on that page you need to choose your state (your jurisdiction) from the drop down and click on “go.”

It will take you to the next page where you need to click on “CPIO/CAPIO” and play around to find out the exact place where they have dumped all that information. Below you can find a RTI template which you can use.

You should ask for name and designation of the officer who is supposed to process your income tax refund claim

Also ask for the officer official address and his contact number

Also ask for how long the refund is pending with the officer and the reason for the delay

Ask if some senior authority has instructed for delay and the certified copies if any

Also ask for the name, telephone number and address of the higher officer with whom you can file the first appeal

These above mentioned 5 things if asked in RTI, will be enough to move the earth below the concerned authorities feet and they might act faster on your case, because in most of the cases there are no valid reasons for delay. The delay is created just because of lethargy and at times in expectation that someone will visit them and bribe them to process the request!

Note that only the concerned person can file the RTI, no one else on his behalf can file it. In case you have tax refund for different years, better file separate RTIs for each. Do not mix them into one.

Tips while filing for Income Tax Refund

There are few well known mistakes people do while filing returns, because of which income tax refund delays happen. Let’s see those points and make sure you don’t do them.

1.Make sure your give permanent Address

A lot of salaried people, who live on rent, give their present temporary addresses while claiming tax refund, and when after 1-2 years their tax refund cheque arrives, in many cases the person has moved out of the current location. This causes the cheque to return back and the person is not there on the given address.

So make sure you always give the permanent address where you or your family lives and there are almost no chances of cheque returning back.

2. Give accurate Account Details, IFSC code

There have been cases where the account number given was inaccurate by 1-2 digits or the IFSC code was wrong, and that created the problem. This small thing can result in lot of frustration later, so double-triple check these details.

3. Try to do E-filing of your tax returns, if possible

As far as possible, try to file your income tax returns online and apply for tax refund, because the tax refund is much faster if e-filing was done. In case you are filing offline manually, make sure you fill form 30, contact your CA if you want to delegate this totally to someone else!

Conclusion

If you have been waiting for your tax refund from years, it’s the time to file a RTI application for it and find out why your income tax refund has been delayed for so long.

Are you leaving India in next few months or planning to move abroad sometime in future? Then you should be clear with a few points you should complete before you become an NRI. A lot of NRI readers come up with various issues they face, because they never thought about completing few tasks which could have saved them from lots of worries and paperwork. Lets look at 10 things which a person should complete before he/she becomes a NRI (Non resident Indian)

10 things to complete before you become NRI and Leave India

1. Take a Term Insurance

One of the big issues NRI’s face is taking a term plan through a Indian insurance company. It’s always a good idea to take a term plan and then leave the country, otherwise later it gets really tough to get a term plan, for which you will have to visit India and also it also gets quite difficult to opt for online term plan.

So before you become a NRI (Non Resident Indian) , complete this step. The premiums you will pay will be lower.

2. Take Health Insurance

Just like term plans, it’s tough to get health insurance once you become a NRI. After becoming a NRI, you will have to visit India for health checkups and there is more documentation and hassles in the process. Health Insurance is something, you should take anyways , so why wait? Just take it anyway.

3. Open PPF Account

NRIs cant open a fresh PPF account, so before you become a NRI and leave India, open a PPF account. You can open PPF account in ICICI bank, SBI bank or at the Post office. NRI’s can always invest money in their existing PPF account which was already opened by them before leaving India.

4. Convert your Saving bank account into NRO account

A lot of people leave India only to realize later, that they need to open a NRO account in India, and then get into the whole process. Rather than doing it later, why not convert your existing saving bank account into NRO account just before leaving India? NRIs can deposit all the Indian income into their NRO account and also make payments like EMI payments, and other kind of investments from their NRO account. All it takes is 2 photographs, and a copy of your passport and visa.

5. Connect your Loan Account with your banking account for online payment

A lot of people who become NRI (Non Resident Indian), have a home loan running, for which they have to still pay EMI’s . At times, they want to prepay home loan as fast as possible, because they earn more money outside India. But then the issue is – how to make prepayment when they are outside India? The best option here, is to connect your home loan account with your bank account, so that you can make prepayment to your home loan using NEFT transfer. Its a good idea to do this before your leave India and try some prepayment just to make sure it works. It might happen that you might need to visit the bank for this, so better complete this before you leave India.

6. Prepare a Power of Attorney

There can be many things which require your presence in India after you have become an NRI, like if you want to make any real estate transaction or want to operate your bank account etc. It’s always a good idea to have a bit of foresight and see if you might want to prepare a power of attorney. Power of attorney is a legal way of giving power to someone to act on your behalf. Just choose some trusted family person or a friend. You can also make a power of attorney which expires at some stipulated time.

7. Make your mutual funds accounts online

A lot of people still want to transact in mutual funds after they become NRI, but they have no easy way out at that time. It’s always a great idea to make sure that you open a online account for mutual fund investing while you are in India. For this, you can open a online account with Jagoinvestor team and have all your transaction online

8. Open a NRE account

If you want to invest your earnings into India and want to get it back in the foreign country (repatriation) , then you would need a NRE account. You can not deposit the local money like interest from FD, rental income etc into the NRE account. So if you have this kind of requirement, then better open a NRE account. The Fixed Deposits rates on NRE accounts are quite attractive in Indian Banks.

9. Sell your shares and open a new NRI demat account

Once you become an NRI, you will not be able to sell off your existing demat account shares which you bought before becoming a NRI. You can open & operate a NRI demat account. So before you become an NRI, a good idea is to sell off the existing shares and take back the money or the another option is to open a NRI demat account and transfer your existing stocks to this new account.

10. Update your KYC

There are different processes for residents and NRIs for various kind of financial products. Like, if you become an NRI and want to do something with banks, mutual funds, life insurance policies (traditional or ULIPs), you will first have to update your KYC and only then can you do something. So its always a good idea to update your KYC, before you become an NRI. This will save you with lots of hassles.

Conclusion

If you follow these 10 things before you become an NRI, you will have a really peaceful time abroad and will not have to get involved into the mess of completing the things, most NRIs miss. While you might be excited to go abroad, better not miss out on these points.

Are you planning to leave India and become NRI Soon ?

One of the most used financial products is the Credit card. We all spend so much time to get best credit card, but I have never seen someone, who has spend his time to fully understands the importance of the CVV number, One time password, Signatures on the back of credit card or how secure their credit card is overall ! .

There are so many credit card frauds going on, and yet each of us thinks, that our credit cards are fully secure and it cant happen with us. However, this is really far from the truth, because of the 4 big myths people have about their credit cards and we will bust them today for you, so that you become a more powerful and informed investor!

Myth 1 – My Credit Card is secure, because no one knows my PIN/Password

When you make a transaction through a credit card in India, at the end of the transaction, you are asked to enter one more final PIN number, which makes your transaction more secure and gives you an additional layer of security. RBI had come up with this additional password requirement just last year. While you needed credit card number, expiry date and your CVV number to make a transaction earlier, now as an extra security layer, you need this additional PIN too.

However note that this is limited to online transactions on Indian websites only. When you make a transaction outside India, this additional step is not compulsory. This means that someone having every other detail of your credit card other than your PIN can also do transactions even if he does not know your PIN . You must have realized this yourself, if you have done any transaction outside India.

Myth 2 – No one knows my CVV number, so I am secure

One of the biggest myths about credit card is that, if no one knows your CVV number, its impossible to do the transaction. Take a small breath, while I tell you this.

“CVV is not always mandatory on all websites to make an online transaction.”

Yes, you heard right!. You can make a online transaction on few websites out of India with only the Credit Card number, the expiry date and obviously the name of the credit card holder. If you don’t believe me, here’s a small example.

Try to book a domain name at godaddy.com. I was almost numb, when I booked a domain name some time back, only to realize that the domain name was booked, but the site never asked me my credit card CVV number and I was like – “What ?! Seriously ?!” . I then found out, that asking for CVV number is just optional for credit card merchants. While some countries make it mandatory, others don’t. It’s just a choice!

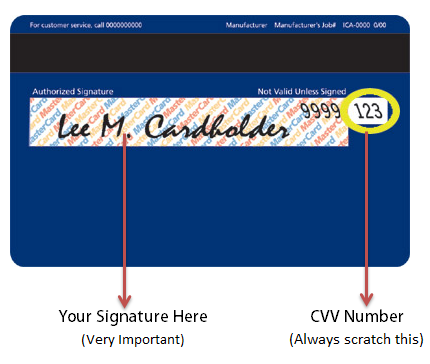

So make sure you are safe, do this

Scratch your CVV number on the back of your credit/debit card

Always make sure the swiping happens in front of your eyes! , I know, it can be a little embarrassing for you, but its just an extra mile security, see if its possible for you

Better do not use Credit Card at all , use Debit card instead!

Myth 3 – My credit card can’ t be duplicated.

Yes, your credit card can be duplicated and it happens in India. A card (credit or debit) might be using something like EMV chips or Magnetic strips, and that’s where the problem is at. While EMV chips are more secure, the magnetic strips are not!. If your card has magnetic strips, it can be duplicated.

Here is how it works …

Your card has a lot of data inside it and it sits on the magnetic strip. When the card is swiped, all the data is extracted from it, for verification purposes. Now some expert hacker with bad intentions, can extract all this data from the swipe machine and make a new card using a technique called Cloning. There are machines called “skimmers” , which helps in extracting the data from the swiping machines to a new card. If you are still wondering if this all happens in India, here is a story excerpt from Hindu website

According to the police, the machines were used to swipe cloned cards by one Rahul. The cloned cards were arranged by Pankaj Deewan, Yogesh Mahajan and Yasin through their contacts. The amount transferred to Dheeraj alias Rohit’s account was shared by the machine holder and cloned cards holder at 40:60 ratio respectively.

Following this, the police launched a hunt and subsequently arrested Dheeraj, Pankaj, Yogesh and Yasin. They purportedly told the police that the domestic cards were cloned by one Kamal and international cards by Devender Chauhan of Agra with the help of a professional hacker. The cards were cloned by obtaining information of genuine customers and then copying the same on a plain card having a magnetic strip. According to the police, the accused used skimmer (a device used to copy data from credit/debit card) for the same.

And if you still don’t believe all this, here is a video you might want to spend time on

Myth 4 – The signature on the back on credit card does not matter much

One of the most misunderstood and unknown facts about credit cards is the signature on the back of the card. Let’s understand the rule today and lay this to matter to rest. If a credit card does not have a signature on the back, it’s an invalid card. As per the agreement between card issuer and merchant (the shops and hotels which give you the facility to swipe the cards), the merchant is supposed to check the signature on the back of card with the signature on the bill, and only if they match, the merchant should allow the card to be swiped.

However almost all the merchants avoid checking it, as if it does not matter at all. This is violation of terms and conditions and if you have lost a credit card which was SIGNED, and some transaction takes place, you are not suppose to be charged, because the merchant should have checked the signatures on card with the signature on the bill. What this means is that if there has been ever a fraud on your credit card, and you are asked to pay the money (Like this Incident) , just ask your card issuer to check the signature on the bill with your specimen signatures with them and if they do not match, they are not suppose to pay the merchant at all and let merchant take the loss for not doing their duty of checking the signatures.

This explains why you should sign your cards on the back and not leave them blank, because if someone steals your card and puts his signature on the back, then the transaction can be done successfully even if the merchant does his duty of checking the bill signature with the signature on card and in that case you are bound to pay the money to card issuer.

MYTH 5 – By paying minimum balance, I do not have to pay Interest

As you have used your credit card and now it’s time to pay your bills of Rs 15000. But you don’t have money to pay back the bill. You are in tension because if you don’t pay your bill you will be charged penalty. So to avoid penalty you pay minimum balance of Rs 3000 and now you will not be charged penalty. So now the left over bill amount is Rs 12000.

You must be happy that you will have to pay Rs 12000 only but let me tell you that you will have to pay Interest of 3 to 4% on this 12000. So even if you pay your minimum balance to avoid penalty but you cannot avoid the interest charged on the left over amount.

MYTH 6 – Too many credit card will improve my credit score

Many people think that if they opt for more than one credit card then there credit score will increase eventually. But this is other way round. If you opt for too many credit cards you won’t improve your credit score but you end up being more dependent on these credit cards, which is not a good sign. Managing too many credit card becomes burdensome.

Tips to Secure your Credit Card

I hope, now that these myths are busted, you are a more informed and powerful person who the rules of the game of credit cards . To summarize, lets put out some tips to secure your credit card

Do not share your one time credit card password (IVR) with anyone ever

Scratch your CVV number and remember it in your head !

While making any online transaction, make sure the website starts with https://

While making any transaction offline like on petrol pumps , hotels etc, make sure its swiped in front of you as far as possible.

Make sure the card is swiped on a machine which is issued by authorized banks and not some machine which looks suspicious , it can be a “Skimmer” machine which steals your data.

Put a signature on the back of your credit and debit card, so that unauthorized transactions are not done and you are protected a card holder

If possible, better use a credit card which has a small limit like 10k or 20k for shopping.

There are virtual credit cards these days, you can use them for online transactions

If you ever had any incident that was mentioned here, please share it with others and if you have some thing to teach others, please share it here with everyone.

Do you know that only 1% of world wealth is owned by women , while women constitute 40% of the global workforce ? – World Bank . This is a little disturbing fact, and question now is, when women are working so much, giving a lot, have equal capability, then why they have so much less owned on their name ? When it comes to the area of money, Men are so much involved in personal finance, but women are not and that creates a big imbalance. Here is a small example to show how women suffers in her financial life because of this imbalance in understanding and knowledge of money

We at jagoinvestor want to start our 2013 with a vision of increasing financial literacy among women in India and we are looking at how we can reach 1 million women and teach them importance of financial literacy in their life. Now how is this related to you ? When we say “women” here, it also includes your wife, sister, mother, daughters and if you want to increase your financial life quality, you need to make sure that they learn about money. 2 years back, when I wrote about women and their personal finance knowledge, it was shocking to learn that 84% of educated, urban women dont have any knowledge or very minimal understanding of personal finance concepts.

Lets see why Women are not interested in personal finance matters

From decades and generations, it has been dominated by men and only men, women are not even consulted or informed ever

Women feel that their income is secondary to men, hence whats the use of managing it

Women are so involved with children, cooking and other household work , that they don’t get time

Women feel personal finance is complex and do not like numbers

But what happens when Men is not around ?

The best way to make you imagine what happens to women life if she does not have any idea about managing money is to ask you to imagine about your own case, Just imagine in your absence what is going to be the scene ? You have never encouraged women at your home to learn about money , neither they took any interest, but someday they might have to take charge and that day it will be very frustrating experience for them. We are trying to do some work in the area of financial literacy for Women and once we create something useful for women investors, we would like to share it with you all, so that women at your home can use it and take the first step towards financial literacy, but we need some help from you on this.

We have created a small survey which needs inputs by women, we want to know what they feel about this subject, how much ready are they and what is stopping them to learn about money. If you are a women reader of this blog, please fill up the survey. However if you are a male reader, we need your support, please ask your wife, mother, sister and daughter to take up the survey and spend 5 min on this, tell them they have to do it for you and their future. Just carry your laptop to them and insist them to spend 5 minutes and complete the survey. And if they complete take them out for dinner on our behalf (Bill paid by you of course) … Following is the survey questions