Sometime around March of 2010, I was checking my inbox and saw an email from a person from CNBC. The message said that there was an opportunity of me authoring a book on personal finance.

For a moment, I could not believe it.

It was an ecstatic moment for me because I was just 27 yrs old, with 2 yrs of experience in IT industry and 2 yrs of experience running this blog. The world around me was all about python, Perl and servers and here was an email asking me to author a book on money which would be published by CNBC. I was going to be a mini-celebrity and I knew it would be counted as great achievement on my portfolio. This blog was around 2 yrs old at that time.

I replied back that I would surely be interested in this assignment and wanted to know how it works. It was a great coincidence that I had a very rough idea of a book already in place, when I used to fantasize the idea of book writing some day and here was the opportunity knocking my door.

I went to Mumbai, had a quick meet with concerned person and I was all set on the assignment of Book Writing.

Starting of the Book writing journey

The next few days were highly energetic.

I could not believe that I was really writing a book at this age. I had already done more than 300+ articles by that time and had interacted with thousands of investors by that time over comments section of this blog. I had a fair understanding of what kind of book will really help an investor.

I started jotting down all the important points and concepts which I should cover in the book. I thought that writing a book would be easy for me, as I had written so many articles on various concepts already. After all, I just needed to arrange them in a certain manner which looks like a book, change the language of the content to look powerful, add few examples and enough stories to make it interesting and engaging.

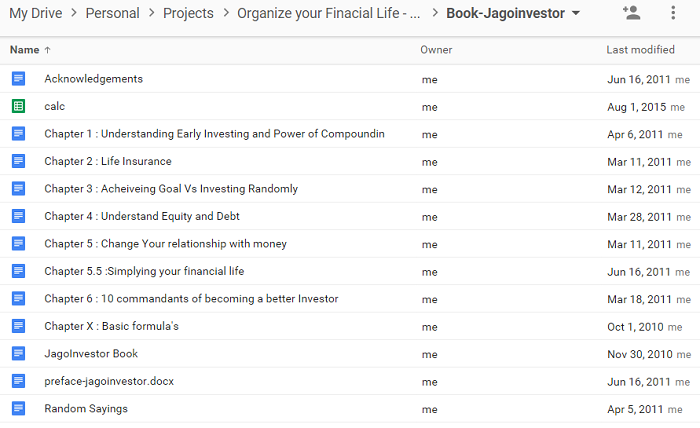

I created a Google doc folder and started creating various chapters’ pages. Here is a snapshot of how it looked like finally…

My initial way of planning and thinking about the book was like this…

I thought, if I wrote 10 pages daily, it would just take 25 days to write 250 pages. If I target the book in 30 days, I would still have 5 days left. I added 1 more month as a buffer period to refine my book and make any changes if required. I thought 2 months would be enough.

The book finally took me 500 days

I know what you are thinking right now. I know I so stupid.

As you must have guessed by now, I had done a very poor job in planning and estimating the time required to write a book. I think it’s not even “poor planning”, it was “pathetic planning”.

I over-estimated my capabilities to the highest level. I finally took 1.5 yrs (500 days) to complete the book and now I will give you insights on why it took so long.

Let me share with you that, I was very clear that I don’t want to do a “good book”. I wanted to write an extra-ordinary book, which is relevant for many years to come and truly helps an investor who is new to the world of personal finance.

I had seen some the other books which were written and they all focused mainly on the “knowledge” part of personal finance. Each of those books had information about various financial products, tax saving avenues etc. I think those kind of books have their own importance and are required. However, I didn’t want to write “just another book” on the shelf, which is giving the same information to investor like others.

What kind of book I wanted to write?

I wanted to do a book, which shakes the investor. A book which shows them the mirror and truly makes them understand some really important principles of personal finance. I wanted to do a book which is ACTION oriented, not just information oriented.

I wanted to write a book which wakes up an investor from their sleep and clears their way of looking at their financial life. A book which acts like a big brother guiding them on how to look at their money matters and builds a guideline for them to follow. And I think, I succeeded in what I wanted to do, the proof is 81 reviews on flipkart, with an average rating of 4.4 out of 5

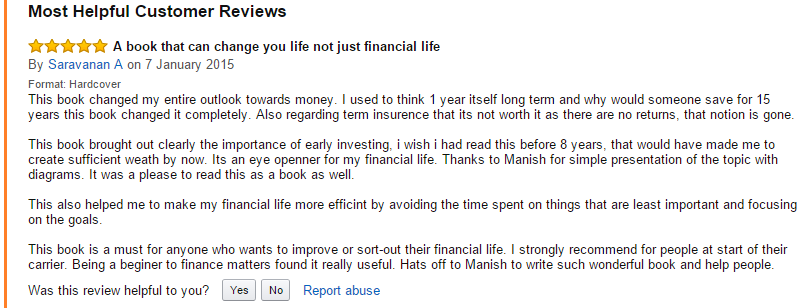

I was like the director of the movie, who had to make sure he casts the right actor, good story, great scenes, and dialogues and at the end, had to connect all these elements and come up with a master piece. Before I move ahead, I would like to check out a review by “Saravanan A” on amazon. It captures the essence of the book beautifully

I started writing the book

When I finally started writing the book, I started building the book skeleton.

I prepared the chapter names and just wrote down what each chapter will talk about. Trust me it sounds very simple, but it took me over a month to just do that part in proper manner. Write one article was easy, but how do I write a book which is 100X times an article? At the same time it had to be interesting, outstanding, full of examples, insightful and had to have a strong flow at the same time. The book was suppose to make sure it hooks the reader till end.

It was not an easy job

I first created the list of chapters, and the number went upto 22 in numbers. There was so much to write in each chapter. I started with first chapter, then 2nd and then 3rd …

Gggrrrr…….

I realized, that I have done everything wrong. After I did 50-60 pages, everything I did looked so damn bad to me. I was not happy with it.

I hit the delete button and all 3 chapters were gone. I realized, I needed to relook at my strategy.

I now started defining the chapter names, sub-topics under each page. I wrote down the headings part of each chapter and what all will go into it. It was like mini-index of the whole book.

This way, it became more easy for me, because now I was actually creating a proper flow and was actually giving the shape to the book. Once I had completed that, I just have to expand each point with 200-300 words and my 800-900 point skeleton book would expand to 100X size and would be a 90,000 words book.

This was a top to bottom approach.

Trust me, it looks the obvious way to write the book NOW. But that time, it didn’t click me. I made a lot of mistakes and lost a good amount of time to just figure out, how to give a good start.

Anyways!

Finally, I ended up with 8 chapters. Some chapters were long, some were very short.

The First Chapter – My best work !

The first chapter I wanted to do was on the topic of early investing.

I was first wondering does this topic deserve a full chapter? After all how long can I write on the point of early investing?

In one line, if you summarize it, it looks like “If you invest early, you can start small , but if you are late, you will have to put more money later to build the same amount of wealth”.

But then were are so many dimensions to this single topic and I was so fascinated with it that I wanted a detailed chapter on this single topic, which is outstanding and goes beyond the simple conversation.

I wanted to give examples, real life analogies and enough data as the backup to prove my point. I found out that though the starting the chapter was very tough, it was not that tough later. Once I was in the flow, I started enjoying the book. I could visualize how a reader will feeling while reading it. What kind of questions they will have and what kind of examples will help them to understand the concept in a better way.

Working in Excel

I did a lot of work on excel, created charts, came up with examples and did a lot of number crunching.

I came up with lots of interesting conversations which would make investors understand the point. I wrote 40+ pages for the first chapter. I read the whole chapter once I completed and I found I can do better, then I went through the chapter, edited it back, and pruned the content, added some more ..

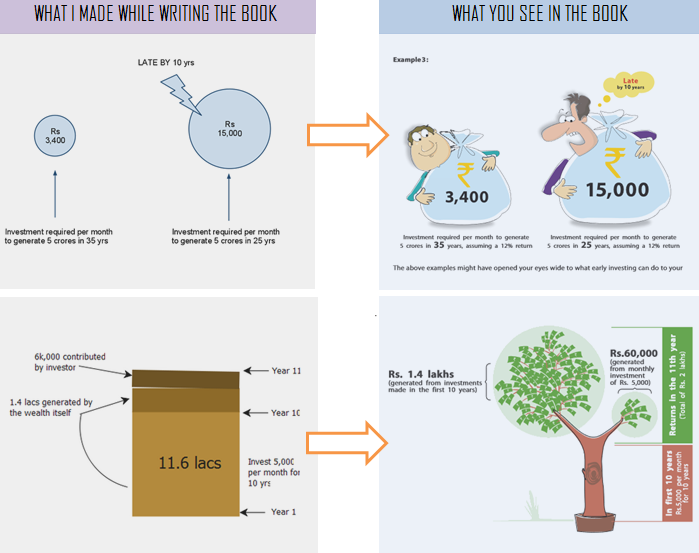

I created the rough sketch of examples and images and the designers at CNBC did an excellent job at recreating nice illustrative pictures which conveyed the same in the book. The eye-catching graphics which they created, increased the richness of the book. Here is a snapshot of what I created and what you see in the book.

I was happy on my achievement

Finally, I was satisfied and happy with my 1st chapter and I was proud of it. I could see the power and impact of the first chapter book on an investors mind.

My goal was simple – “If someone reads my first chapter, he will not delay his investments after that”.

It was as simple as that. Some book readers told me, that they started their SIP just after completing the first chapter, they didn’t even wait for completing the book.

I had done the first chapter in 15 days time and it was the biggest chapter of the book. I recalculated the time I would take to complete the book told CNBC, that I will not be able to complete the book before 6 months. They were happy listening to that 😉 (maybe they knew the reality)

Once I completed the first chapter, I thought of taking the break before I start my 2nd chapter. The short break lasted for 2 months. After working so extensively on the 1st chapter, I was a bit exhausted and was flying high with confidence and every time I thought of returning to the book writing, something or the other came up and made sure I could not concentrate on the book.

My 6 months deadline was about to complete and I was done with just 2-3 chapters only. It was just 40% of the book. For the first time, I was understanding how tough it was to keep your deadlines promises. Whenever someone defined the deadlines for the projects in our projects meetings, I had a dangerous smile on my face.

Finally, I completed the book

Now, let’s cut things short and come to the main point. I finally wrote other chapters on risk and return, insurance, simplicity requirement in next few months.

I also added a chapter called, “Relationship with Money” which touched the point of how our emotions are connected with money and how we see money in our life. It was a very different kind of concept which was introduced by Nandish Desai, my business partner.

So I requested him to write that full chapter because I knew that I will not be able to justify that chapter because of my limited understanding of that subject and I think he did a brilliant job in that. It added a whole new dimension in the overall book and it was aligned with the book mission.

It helped investors to connect with their emotional side of money. Thanks to Nandish to author that chapter (we will soon come up with his 1st book story)

Editing of the Book

Finally, I managed to complete the book in a year. By the time, I completed the 80% part of the book. The editing had started.

I was sending each chapter to CNBC which was now edited by a professional. They checked the whole book for the English language and the sentence duplication. If 3 lines conveyed the same thing, It was merged into one and the sentence was pruned. When the edited version of the chapters came back to me, I was horrified to see how pathetic my English was (I knew it was bad, but SO BAD ?)

With heavy heart when I asked the editor is that was normal? They said – “YES – It was totally normal and it happens with every writer”. I was a happy writer again 🙂

The Polishing of the book content

I saw, how the editor had polished the book language and made it look more professional. They had also suggested some changes (very minor) and I incorporated them. To my surprise, this whole thing again took few months and finally I got one final version of the book to check for one last time before the first print happens.

I started reading the edited version of the book. This was the first time when I was reading my complete book as a reader. That cute little thing as attachment, on my email was one of the most beautiful thing I had seen. I felt like I was a mother who just delivered a baby after 9 months of labor (1.5 yrs in my case).

I started the first sentence, then first page, first chapter … and finally the whole book.

Happy and Proud Moment

I was extremely happy and proud. I could see that the book was able to make an impact. I had taken a lot of time to do the book, but I had not compromised with the content quality. I didn’t write it with rush.

We originally gave the name of the book as “Jagoinvestor”, because the book focus was to wake up an investor and that name looked appropriate, however after an year, we changed the name to “16 personal finance principles every investor should know”, because it was a more clear name and conveyed what the book was all about.

The book has been so powerful, that a lot of investors who read my first book suddenly start acting on their financial lives and some even contact us to do their financial planning. Our best clients came to us by reading our books. A lot of investors who are DIY investors, even they get a lot of value from the book.

What I learned by writing the 1st book (and you should know that)?

A book is a creation, which comes into life after a lot of hard work. There are many dimensions which comes together and then a book takes the shape. Writing a book might be easy, but writing a “good book” is not.

When you read any book, if you get one insight or one learning which can impact your life, I think the author has done his job and you have got your value. A book can have some mistakes, some part of the book might not sound great to you, but be thankful for the good part, ignore the average part.

Now when I read a book, I ask myself if I learned any ONE THING from the book or not? If the answer is YES, I consider the book as great. I have stopped criticizing any author (anyways, I never did) because I now know the other side too. I recently read a book called “Predictably Irrational” by Dan Ariely. My god – What a creation ! .. What a book it was .. If only I was 10% of that author, I would have done wonders!.

Share your comment

Let me know what do you think about my journey of writing the book? What did you learn from it? Also share if you have read my first book or not?