Anna is not a name it is a mammoth movement in itself. He has created a wave and has impacted thinking of every common man.

Me and Manish in one of our discussions saw something and thought of sharing how you can bring “ANNA MAGIC” in your financial life. We are not going to discuss any political or country level corruption; we are addressing your habits of casualness and procrastination of being corrupt, it is a slow poison that can damage or corrupt your financial life.

Ask yourself how corrupt is your financial life? Or How Corrupt you are with your personal finance promises and commitments? Where do you sell yourself cheap in your financial life? (We procrastinate on concepts and take things casually; at time we don’t pay to get the right advice)- Today let’s be honest and face it.

We all start almost in the same fashion:- Going to college, getting a job and start earning and still, we all live a different kind of financial life. We all have the same core foundation & aspects of financial life what is different is how we live our financial life.

3 Things to keep your financial life in control

Let’s invest our time and energy in removing the internal corruption of our financial life. To have ‘more’ you need to become ‘more’ and so we are asking you to be the stand that ‘Anna’ in your financial life.

This may not change the world but it will surely change your world if you practice these things in your financial life. One request don’t deviate from the topic we are very clear this is not at all about Anna or Indian politics it is purely about your financial life.

1. Be a leader in your financial life

You can either live a corrupt Financial Life or as a leader choose to live a Non- corrupt Financial Life. The moment you start holding financial products in your financial life which are not on purpose your financial life starts getting corrupt.

If you lose things with a “chalta hai” attitude your financial life starts getting corrupt in that moment itself. Don’t follow blindly to what you see and what your friends invest in. Don’t be a follower of ‘hot tips’ and schemes of making fast buck (remember Speak Asia) .

Take a rock solid stand to remove all non-purpose products from your financial life. Your financial life is a clear reflection of how corrupt or non-corrupt you are.

2. Be a creator

You can create and pass your wealth-pal bill now . If your financial life is in your hands than what are you waiting for, if you are the driver of your financial life than what are you waiting for?

Get one thing very clearly that your wealth-pal Bill is in your hands, it needs your signature and alignment. The bill can get your financial life back on track and will keep you focused all the time. Here you are the standing committee as you need to take a stand for your financial life to be great.

3. Be accountable

Make yourself accountable for the financial life you have. Make yourself accountable for the income level you are having. And also Make yourself accountable for your current financial position that you are having. Being accountable is the third pillar of designing and living a great financial life.

If you have a low say-do ratio you are living a corrupt financial life. If you maintain a high say-do ratio you start having more power in the way you live your financial life. You start getting more confident about your investments and more committed with your financial goals.

Make yourself accountable for. See the above three areas as a “Law” and implement it as a law in your financial life religiously and see the changes that happen in your financial world.

The action month is on. (readers on email can fill up the form here). More than 1050 (till the moment) different tasks are going to be completed by hundreds of participants and they are choosing to remove all the corruption “laziness” and “casualness” from their financial life.

If you want to choose the movement you don’t need to go to ramlila maidan you can join the movement by filling in the below form and let the magic of being Anna begin. This article is also dedicated to one of our client who is a stand like Anna for bringing change in peoples financial life.

Tell us what do you think about this article. Do you like it? If you want to ask any question you can leave a query in our comment section.

There are so many LIC policies with different names ? For example – LIC Jeevan Saral , Jeevan Anand , Jeevan Tarang and many more LIC policies. So almost every person in India holds some LIC policies, but majority of them do not know how these LIC policies works ?

How LIC Policies Work ?

Most of the investors just take things for granted and keep dragging the policies assuming it would be the best thing in their financial life. In this article I will show you how Life Insurance Corporation (LIC) policies work and talk about few aspects like LIC bonus, LIC premiums and different other aspects which will help you in understanding how these policies work.

Moneyback Plans or Non-Moneyback Plans

A lot of LIC policies pay you on a periodic basis like at the end of 4th, 8th and 12th year, and then finally at the end of the maturity period. These policies are Money back policies, the example can be LIC Jeevan Surabhi or LIC Komal Jeevan. A lot people get attracted to these moneyback plans because they get money “many” times in between and it looks attractive to them, but the premiums are generally higher for these policies.

Then there are LIC policies which do not pay you back periodically but only pays you at the end of the maturity period. They are generally termed as normal Endowment plans. Some examples are Jeevan Anand and Jeevan Tarang

LIC Bonus & Additions to your Policy

The biggest confusion I see is generally in Bonus by LIC. One thing which investors in these policies don’t know and don’t care for to find out is that there are different kinds of bonuses in LIC policies and they are calculated differently. Let’s see them one by one.

1. Simple Reversionary Bonuses

Generally when we say “Bonus”, it is this “Simple Reversionary Bonus”, which is declared per thousand of the Sum Assured on annual basis at the end of each financial year. This bonus is declared today, but is paid at the end of maturity period only or on death, whichever is earlier. So for example if you hold a policy of Rs 10,00,000 Sum assured and the bonus for this year is Rs 60 per thousand sum assured, then your bonus amount is Rs 60,000 for this year, but you will only get it at maturity (after many many years) or on death, but by then it’s worth would be much lesser than today (this 60,000 today and 60,000 after 20 yrs).

A very important point to note here is that, if you surrender the policy, you don’t get the actual accrued bonus because it’s the future value, you will only get its reduced amount in today’s term and its very less. Also note that you are eligible to get reduced Accrued Bonus only if your policy has completed 5 premium paying terms. (This thread on our forum discusses Jeevan Anand in good detail)

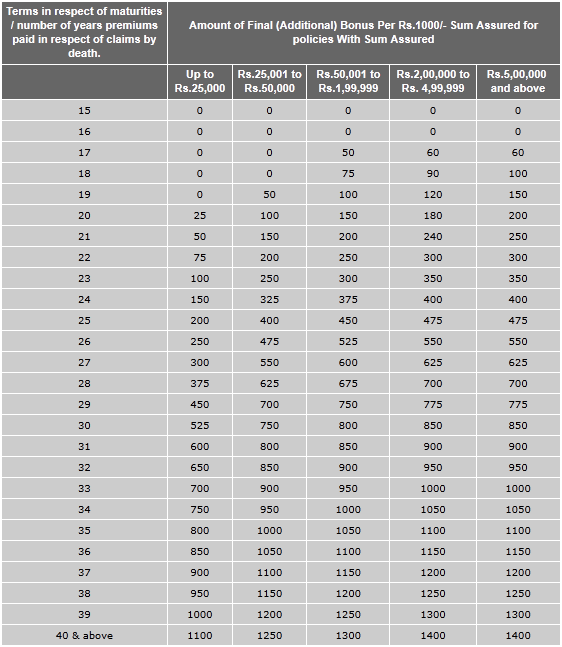

2) Final Additional Bonus (FAB)

There is another kind of bonus in LIC which is generally called as “FAB” or Final Additional Bonus and it’s paid to those policies which are of a longer duration and has run for more than 15 yrs (The premiums are paid for all 15 yrs). This is generally a token of appreciation for being with the policy for long duration. The FAB is generally not paid for policies which have “Guaranteed Additions” (explained below). Here is an indicative list of FAB.

3. Loyalty Additions

This is again a bonus which is declared for being loyal to the LIC and completing a longer tenure. Generally it’s declared at the end of the policy, but for some policies it might be applicable after completion of 5 or 10 yrs. For example – In Jeevan Saral, the policy holders will earn such additions after a minimum of ten policy years have been completed. This is usually an amount declared per thousand of sum assured depending on the corporation’s performance. Loyalty additions are totally non-guaranteed.

4. Guaranteed Additions

For a lot of LIC policies there is a term mentioned like “Guaranteed Additions”. These are assured sums which are given to policyholders for a specific period at start or end of some event along with the sum assured at the end of the term. Like for example, , Jeevan Shree-1 policy provides for the Guaranteed Additions at the rate of Rs. 50/- per thousand Sum Assured for each completed year for first five years of the policy. The Guaranteed Additions are payable along with the Basic Sum Assured at the time of claim.

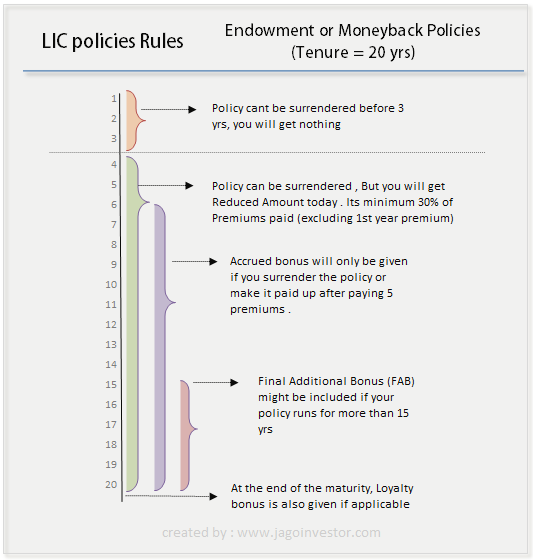

Surrender Value

Most of the people who buy any Traditional Policies from LIC or any pvt companies’ don’t think a bit about terms and conditions on exiting the policy much before maturity. A general assumption is that they will at least get their paid premiums back with sum interest. I have seen so many cases like that where people are literally shocked to hear that they will get peanuts or nothing from their policy if they choose not to continue the policy. Surrendering of the policy works this way –

You will not get anything back if you stop your policy without paying for 3 years. Almost every traditional policy attains minimum surrender value after the policy has run for 3 yrs.

After 3 yrs, if you surrender your LIC policy, still you will only get a small fraction of your total paid premiums that too excluding first year premiums. So suppose you have a policy which has Sum assured of 10,00,000 for 20 yrs term with Rs 50,000 premium per year. If you have decided to surrender your policy after paying 5 premiums (you paid 2,50,000 in 5 yrs i.e. Rs 50,000 each year), then you will get around 30%-40% of 4 premiums paid (first year premiums are excluded), hence the total would work out to be only Rs 60,000 – Rs 80,000 only + proportionately reduced amount of accrued bonus if any (only because you completed 5 yrs, else you will not get this also).

A very important point to Note : A lot of people do not like to close their LIC policies after paying for 1-2 premiums because they will not get anything back for the 1-2 premiums already paid. They think that they will surrender the policy after completing 3 yrs, so that they will get at least something back. This is total emotional decision and not mathematical, because if you do maths you will see that surrendering the policy after 3 yrs is the worst decision if you have already realised that you should not continue with the policy. For example, if you are paying Rs 10,000 premium per year and completed 2 yrs, you paid Rs 20,000, If you close this policy now, you will lose all money (Rs 20,000), but you can save Rs 10,000 as third premium. If you choose to complete 3 yrs and then surrender, then you have paid Rs 30,000 and you will get back 30% of 2 premiums (first year premium not included), so you get back Rs 7,000 (loss of 23,000 as you paid 30,000 and got back 7,000). Do the math if you completed 1 yr only yourself, its more worst!

Note that surrender value is nothing but your future maturity value reduced to today’s value, so if the maturity value is Rs 10,000 after 20 yrs and if you want it before LIC will pay you the Net present value as per today’s term.

Paid up Policy

A lot of times when you have completed 3 yrs of policy, you might not want to get your money back immediately, in which case you can made your policy paid up (just stop paying premium and it becomes Paid up). When you do this, you can stop paying further premiums but you will get your total premiums paid + accrued bonus any at the end of the maturity period. This might work out better sometimes compared to surrendering if you were going to invest the proceeds in some debt instrument.

What are mortality charges

A lot of agents advertise these policies under the head “Free Insurance Cover“, But all the policies charge premium or charges for providing Insurance cover and it’s called “Mortality Charges”, these are the same charges which are there in Term plans and ULIP’s, but may be in a different way, so nothing is free, some part of premium goes in covering you and rest of it is invested in Debt instruments which can give you assured returns at the end of the maturity.

Loan on LIC Policy

You can also get loans at the time of crisis on your LIC policies, but the maximum loan amount available under the policy is 90% of the Surrender Value of the policy (85% in case of paid up policies) including cash value of bonus. The rate of interest charged on loans is at 9% to be paid half-yearly. Is there any other terms and conditions which you dont understand in your LIC policies ? We can all help you understand it in comments section .

Are you looking for surrendering your LIC Policies ?

By now you must have got a good understanding of your LIC policies and how they work. You can find out the return of your policies using the IRR method taught in this article. If you feel that you want to continue your Policies then well and good. But if you feel that you want to close your policies, do it soon because delaying the decision will cost you a lot in long run. I hope its clear to you how your LIC policy works for you .

Which Portfolio Management Softwares do you use ? Some of the Portfolio Management Softwares in India are MProfit, Perfios, Intuit and Investplus and we will see a detailed review of these portfolio trackers in detail. Portfolio Management & monitoring is an important part of managing a good financial life and if your financial life has different components like Real Estate, Loans, Life Insurance Policies, Mutual funds, stocks and ULIP’s. You can also track your portfolio using Excel and there are lot of templates also, but it can be a tedious task to monitor which part of your financial life is doing well and how much worth do you have at each level using an excel template for Portfolio management. Hence, you can use portfolio management software which suits your needs. There are tons of Free portfolio management softwares which you can start with

There are many paid as well as free portfolio trackers available in the market which you can use to track and manage your financial data. I really recommend using one of these so that you have all the data at one place and you don’t need to struggle every time to find out your own information. Once we put all the information at one place, we get a clearer and a complete picture, which we don’t get otherwise… We are amazed to see our clients find out that they are worth so much or worth so less once we start discussing with them their financial life data.

Some important features of Portfolio management softwares

Now we will discuss some of the most important aspects of portfolio management softwares in India . These points are top level concerns of customers.

Data Security of Portfolio Management Softwares

A very big concern which most of the people have is where will their financial data be (example) ? Will it be on their local computer or will it is at third-party server and this becomes a big blocking point for them to go for those products which stores their data at their end itself. Here I am not talking about the login & password, but the actual numbers of their financial details. A lot of people don’t want their info to reside on other servers. I personally don’t buy that argument, but that’s a big concern for a lot of people. In a survey done by JagoInvestor last month, the number one concern which people had was data security, ahead of pricing and features.

Regarding the security of login credentials, with the advancement in technology and strong security advancements, it has become virtually 99.999% secure if not 100%. A lot of solutions also give an option for users to link their bank accounts, credit card and other online accounts by providing the passwords. A lot of people do not know how it works internally…

An online money manager will work well only if you provide online access to banking accounts for a one-time setup. This raises security concerns, but here is how it works. The login username and password for individual online banking accounts is used to retrieve read-only data. The ‘transaction password’ for online banking should be different from the ‘login password’ for greater security. You don’t have to reveal your ‘transaction password’. Customers do not have to give any personally identifiable information, making the process safer. Moreover, the account is completely anonymous and requires only a username and password. All the banking accounts are linked to provide consolidated data. In the consolidation process, vendors will have access to your financial records on a read-only basis, but privacy policies of these entities should prevent abuse of information. – source : moneylife

Features provided

I was surprised to see that in our survey, most of the people voted for high features and less on simple features. I personally thought that most of the people will love to have something which provides them less, but rich data. But actually people look for lot of features giving them number of reports and graphs. It’s very important for someone using the software getting more analysis and suggestions on what one should do in their financial life rather than just getting some plain info which they would have done on their own. Most of the software providers give good analysis along with different type of reports and charts which you can download in excel formats.

Easy to use

It’s extremely important that the softwares are easy to use because no one would put a lot of time to feed the data at the start and on ongoing basis. A lot of players provide statement upload facility where you can just upload your Bank Statement, Credit card statement or other demat statements and the software will put out the information and feed it automatically, thus reducing your work. Some softwares like Perfios allow you to link your accounts with them so that they can pull your information and feed it themselves (read only).

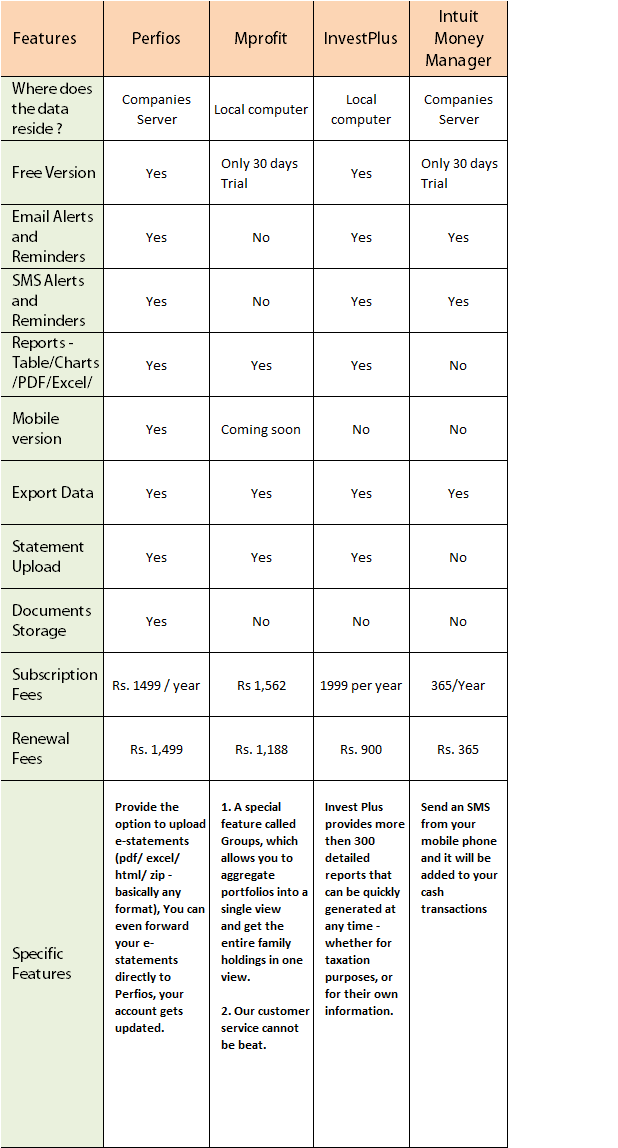

Below is a comparison of 4 major Portfolio management software’s in India market and used by thousands of people (you can read their reviews on their website). They are Perfios, mProfit, Investplus and Intuit MoneyManager

Look at the above video done by me and Manish Jain from Mprofit .

Free and Trial versions

I would say you should take advantage of Free and Trial versions of softwares, Like Mprofit gives away a full functional 30 days trial, where as Perfios and Investplus have free versions which are good enough. If you don’t want to use any software, you can manage your finances at very basic level in an excel sheet, but you will have keep updating the values etc from time to time as the situation changes, which is not the case with softwares, as they auto-update the values.

Free tools for Portfolio management

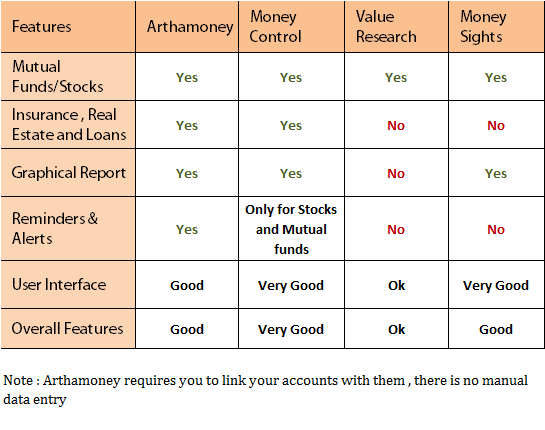

A lot of people don’t go for advanced tools and use free tools available in market which does a good enough job. Tools like money-control tracker and Valueresearchonline tracker are used by lacs of people to track their mutual funds and stock holdings. But they do not give you all the functionalities which fully fledged software’s give to you. Below is the chart explaining Arthamoney, Moneycontrol , Valueresearch and Moneysights portfolio trackers. I hope liked this review of Portfolio management softwares !

I would say you should definitely try out some softwares which provide a free version and also explore the free options, there is lot they provide free of cost and all you need is to put your data there. Some other tools which you can use are rediff money (only for stocks and mutual funds, but I like the UI), myirisplus, yodlee and rupeex.com. Please share what more do you look from these softwares and what do you think about the value you get out of these management softwares?

6 Free Portfolio Management Software Licence from Perfios

Update 12 Aug : The 6 winners are selected and this giveaway is not valid now

Perfios is willing to give away 6 free Platinum licences to Jagoinvestor readers for the first year (worth 1499). The first 10 commentators who share this article on their Facebook profile will get those licences (just cc manish at jagoinvestor dot com) (to share it on Facebook, just “like” this article below and put your comment in the box which opens).

Health Insurance sector is such a new thing in India that a lot of people have dozens of health insurance myths regarding various things and because of that they feel that this whole thing is so complicated. Today I will burst some of your long-term medical insurance myths which will help you choose right products and also build right expectations from health insurance policies.

24 hours Hospitalization is necessary for making a Health Insurance Claim.

This clause always reminds me of an incident. A little over a year ago, we were having our weekly meetings, when a doctor friend who owns a hospital in Mumbai frantically called us. A woman was making a ruckus in this friend’s hospital, insisting doctors continue hospitalization of her son and discharge only after 24 hours, as her “advisor” had informed her that they would get the claim only if the hospitalization is over 24 hours. This incident brought to light the magnitude and the level of fallacies customers have about Health Insurance. Advisors, Representatives, Telemarketers, and even hospitals and customers have frazzled their throats out on the 24 hours clause, while explaining or even using the product.

Though, the policy does mention this as one of the clauses, the 24 number in real world of claims holds lesser importance. The clause, in spirit, requires the hospitalization to be “necessary” more than it to exceed “24 hours”. This was purely from the general understanding that most hospitalizations less than 24 hours are treated under “Out-patient” (treatment at the Doctor’s Dispensary) not covered under a Standard Mediclaim. Hospitalizations (like Cataract), though required 2-3 days earlier, which are now possible due to advancement in medical science in less than 24 hours are covered, while, hospitalization by an insured for more than 24 hours for getting his routine diagnostic tests done, while no active treatments are being carried out, would not be payable under Mediclaim.

Conclusion

The thumb rule of a whether a claim is payable is not 24 hrs hospitalization but whether the hospitalization was medically “necessary” or not?

You must compare Pre-existing waiting period, always.

This is a clause that most people looking for a Mediclaim are confused about (17 Most asked questions in Health Insurance). I speak to many customers whose requirement with mediclaim is that they do not want a waiting period for pre-existing ailments. This, in spite of their entire family being completely fit, without any ailment, whatsoever. Somehow, the clause again being so popular has brought in its own confusions for customers. In reality, the 4 year Pre-existing exclusion on ailments is applicable to ailments existing at the time of applying for the policy, and not any other ailments. If you do not have any ailments or conditions, you have no pre-existing waiting period.

Conclusion

When applying for a Mediclaim, if you are completely healthy, the Pre-existing exclusion clause is not applicable to you

Cashless is an on-call Emergency Service.

Ever since it was introduced as a value addition to Mediclaim, Cashless has remained a buzz word. To a level, that for a lot of people, Cashless became a prefix, or, even synonymous to Mediclaim. The reason for the cashless concept getting popular was obvious; it was a great value add, which helped customers tide away the burden of large payments on their bank account, documentation and of course, the stress of waiting for the claim cheque. Yes, Cashless can do all this, but expecting it to work when there are emergency funds required for Hospitalization is asking for too much.

You should understand the Cashless mechanism as a concept to know why it cannot be depended on at the time of emergencies. Cashless is an arrangement between the Health Insurance Company/TPA and the Hospital where, the Hospital agrees, under contract, to grant credit facility to the Insurance Company/TPA against authorized claims. Such an arrangement is only for authorized Claims, and not for all claims. TPAs/Insurance Companies, hence, need to assess every claim received, against the policy terms and conditions, to authorize payment. Such an authorization could require additional information as well as documents and hence can take anywhere for 4 hours to 2 days of time. In their role, the TPA or the Claims Team at the Insurance Company would have to do its job of evaluation of the claim, irrespective of how urgent the medical admission or treatment is. Cashless will help you save the burden of processing a reimbursement claim, but it cannot provide you the convenience of on-call emergency funds.

Moreover, one should also note, unlike the hospital cashier, Insurance Desks in hospitals (which coordinate for cashless claims) have fixed work-hours from 10.00 AM to 7.00 PM. Cashless process and approvals after 07.00 PM are processed by the Hospital the next day. Hence, though the TPA provides 24/7 service, the cashless process may not move, once the Hospital stops working on it.

Conclusion

Expecting Cashless to work as an on-call Emergency Service is foolish. You should plan your emergency medical fund, as well as ensure you have good unutilized credit card limits, always.

You must compare no. of Day Care Procedures covered

Most Insurance Companies (specially the Private ones) flaunt a large list of more than 100 Day Care Procedures being covered under their policy. In fact, it is a highlight of their product pitch. The truth is comparison of such numbers can be very misleading. One company could list every procedure, while another could list macro-level treatments, including the listed procedures of the former. For instance, a person who compares Apollo Munich’s Easy Health Insurance which covers 140 Day Care procedures, with an Oriental Happy Family Floater which covers only 26 procedures would feel that Apollo has wider cover on Day Care Procedures. Believe me, but it could actually be the reverse. How? Oriental promises to cover Eye Surgery (a broader definition) in its daycare list, compared to say an Apollo which lists 15 specific eye treatments, which results in a larger number. Now, if the treatment being carried out is an eye surgery, which is day care but not a part of the 15 specific treatments, Apollo or many other Private players may not pay, whereas, in the case of Oriental it would get paid in the broad definition of eye surgery. By providing a specific list of surgeries instead of a macro area of treatment, the coverage under Apollo may actually be more restrictive in the long run than Oriental’s wide area of treatment wise list.

Conclusion

A short list of procedures could be wider than a long one. Do not compare the no. of Day Care Procedures.

You should check the list of Network Hospitals.

Many customers, we have interacted with demand Hospital network lists. They select the mediclaim product depending on whether their preferred hospitals are part of that Insurance Company’s list. What they fail to realize is that a Hospital Network is ever-changing. Insurance Companies regularly blacklist defaulting Hospitals. Hospitals blacklist or refuse cashless of certain Insurance Companies/TPAs for delayed payments. What is clear from this is that there is no fixed or contracted list of hospitals between your Insurance Company and you – which means there is no assurance that the hospital name in the list, which you are depending when you buy the policy, would exist in the network when you have a claim, say 4 years down time.

Conclusion

Network List of Hospitals are not fixed or contracted through policy terms. Do not depend on the network hospital list to decide a suitable product for your family. The list could change even tomorrow, in fact it could change any moment.

Capping on Room Rent is bad:

Public Sector (PSU) Mediclaim products and their current terms and conditions are evolved from experiencing and analysing millions of claims spread over more than 20-25 years. Hospital Rooms are classified into various categories like General, Shared, Private and Deluxe Rooms. Earlier without the room rent limits, for the same treatment, a person with a sum insured of 1 Lakh paying a measly premium of say Rs. 2000, would have access to the same category of room, as a person who pays 5 times the premium, and takes a Rs. 5 Lakhs cover for himself. The 1% and 2% Room Rent Limits in Mediclaim brought a clear sync between the kind of premium one pays and the eligibility of room. With such cappings, an individual who pays a high premium gets a better room, than one who pays a smaller premium, for the same treatment, which is fair. It’s like any other product with categories, like Indian Railways, providing you better facilities/services, as you move from 2nd Class to 3rd AC to 2nd AC and so on. In my opinion, sooner or later, Insurance Companies would either have to hike premium for lower sum insured or bring in a capping of some kind. For instance, the newest health insurance company – Max Bupa, has a restriction on the type of room according to the sum insured selected, instead of a “no capping on room rent” feature.

Conclusion

Cappings are good for Health Insurance as a community fund. Cappings could actually be helpful to customers in the long run.

Health Insurance Plans sold by Life Insurers are the same

The highly advertised Health Plans from LIC are Defined Benefit Health Insurance Plans, sold as “hassle free” alternatives with guaranteed payments. These plans should not be considered as a substitute to Standard Health Insurance plans sold by General Insurance Companies. These plans provide fixed benefits against no. of days of hospitalization and/or surgeries. These plans do not take care of healthcare inflation. For instance, with 18-25% healthcare inflation, a fixed benefit for Angioplasty at say, Rs. 1,50,000/- would miserably fall short in 10 years. Defined Benefit products are actually supplementary plans which provide a cover over allied costs of hospitalization including loss of earnings, if any, but such products surely cannot be a substitute to the good ol’ traditional mediclaim. Read more about the difference here.

Conclusion

Beware of what you buy. A Traditional Mediclaim should be the first product you buy to cover the financial risk of healthcare expenses of the future. Defined Benefit Products are supplementary and not substitute to Traditional Health Insurance.

Health Insurance is a Tax Saving Tool:

A large Healthcare expenditure can severely affect your financial planning for the future. The goal when you buy Health Insurance should be to financially insure your family against such large scale healthcare expenditure. Buying a health insurance product blindly, for the 80D tax benefits, is a wide-spread fallacy, which has left a large no. of people underinsured or insured with products which are not suitable. The worst part is most of them are unaware of this.

Conclusion

Health Insurance at its core is not a Tax Saving Instrument. It could save you much more than your tax, if you invest wisely.

There will be no changes in the terms of the Mediclaim I bought:

Expect changes in your product, terms. Don’t be surprised. The Health Insurance companies and other stakeholders in India are going through a mindset change. Losses in Health Insurance are no longer acceptable by key stakeholders at Insurance Companies. A lot of streamlining and normalizing in premium, terms, benefits and procedures, which have already begun, is expected in the next 5 years. Group products would turn expensive, and restrictive. Parents would be out of most Sponsored Employee Mediclaim Covers. Large and small tweaks are expected in Retail/Individual products and processes, especially from new and private players who are till experimenting and understanding how to make a long term sustainable (read profitable) product for the Indian market.

For instance, last year, PSU Insurance companies tightened the procedure of intimation and submission of reimbursement claims. Customers who were not aware of such a change faced harsh action of denial of claims, and lost good money.

Conclusion

Ensure you are updated with changes in the terms and procedures of your Mediclaim Product. Ensure you have recruited a good advisor who keeps you posted on such changes.

I can destroy Mediclaim Policies once they have expired.

Don’t know how many of you have observed at the time of renewals, but PSU companies and their divisions are infamous in the industry for changing their TPAs year over year. With TPAs being the custodian of claims, change in TPAs could result in scattered claims information amongst various TPAs across years of continuous renewals. Hence, when there is a claim, the TPA in all probability won’t have information regarding how long you are continuously covered, an essential data point to approve claims, especially, and those treatments which had a waiting period at entry into the policy. TPAs for evaluation of continuity may demand policy copies of past 3 to 4 years. Hence, destroying policy copies records have cost many customers lot of stress in proving continuity of cover. Yes, we know that it is ridiculous for the Insurance Company or its representative to ask for their own record from the customers, but then this is how it is. A good health insurance advisor knowingly would keep a repository of all policy copies, to ensure such queries do not create roadblocks in a smooth claim settlement.

Conclusion

In addition to the current one, keep copies of at least 3 previous year policy copies. Ensure your advisor also records them.

My Friend, My Health Insurance Advisor

No offence to agents, but in our interaction with Customers, we have noticed time and again, that most customers, who were found with a wrong health insurance product, bought these either from a friend, a friend’s relative, or a relative, or a relative’s friend. Most of these customers did not spend enough time in selecting an advisor, and relied on pure reference. Most of these agents selected were Life Insurance agents, who did not have a detailed understanding of mediclaim products, neither were they providing any real expert assistance (beyond picking of forms, and providing the TPA’s no.) at the time of claims. The advisor selected should have the capability and the intention to provide unbiased advice, the advisor should forever own the product they sold you, and provide services across the Health Insurance service cycle, including Purchase Assistance, Records management, Claims Assistance and Renewals. A good advisor would be able to hand hold you through the dynamic transformation that the Health Insurance industry in India, is witnessing and will continue to witness for the next 2-3 years.

Conclusion on Health Insurance Myths

Select an advisor on merits and the services he demonstrated, and just not merely on reference.

What was the biggest and most valuable learning for you out of this article ? How many of your health insurance myths were really broken ? Please share it on comments section .