HDFC Life Sanchay Par Advantage – Review, Features and Benefits

As and when we approach different stages in life, we set certain dreams and aspirations for ourselves and our family members. We also have to take care of day to day responsibilities like running the family, paying for health expenses, children’s school fees, etc. With so much uncertainty in life, it is important that we secure a source of income that takes care of these expenses, more so after our retirement or in case of unfortunate demise.

To help you achieve your goals, “HDFC Life Sanchay Par Advantage”, is a perfect life insurance solution that allows us to live an uncompromised life. This policy is a participating life insurance plan that provides an option to avail cover for the whole of life (till the age of 100 years) and helps generate a regular income and build a corpus to achieve the planned goals.

Features of this Policy –

- This policy provides life cover with protection up to age 100 years.

- The policyholder can choose between Immediate Income or Deferred Income options as per their needs.

- The policyholder has the flexibility to accrue* the survival benefit payouts.

- The policyholder also gets the flexibility to choose the survival benefit payout date.

- There is an Enhanced benefit for policies with Annual Premium more than or equal to INR 100,000.

- Tax benefits on premiums paid by an individual or HUF as per the Income Tax Act, 1961.

Note – Accrue* means – You have an option to defer the Survival Benefit(s), arising out of declared Cash Bonuses and/ or Guaranteed Income and accrue them instead. The accrued payouts will be accumulated monthly at Reverse Repo Rate published by RBI and will be reviewed at the beginning of every month.

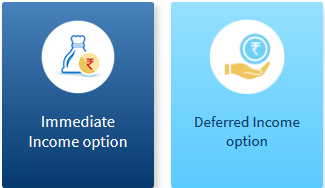

2 Plan Options in this Policy –

a) Immediate Income Option –

- This is an option that provides regular income by way of cash bonuses (if declared), from 1st policy year and also provides lump sum at maturity thereby creating a legacy for your loved one.

b) Deferred Income Option –

- This is an option that provides Guaranteed Income for a guarantee period, and also provides regular income by way of cash bonuses (if declared) throughout the policy term. It also helps in creating a legacy for your loved ones by providing a lump sum at maturity.

Benefits of this Policy –

a) Survival Benefit –

i) Under Immediate Income Option –

The policyholder would be eligible to receive Cash Bonus (if declared) at the end of each Policy Year and payable from the 1st policy year until death or end of the policy term, whichever is earlier.

- Cash Bonus payable = Cash Bonus Rate x Annualized Premium.

*Annualized Premium is the premium amount payable in a year chosen by the policyholder, excluding the taxes, rider premiums, underwriting extra premiums, and loadings for modal premiums, if any.

ii) Under the Deferred Income option –

The policyholder will start receiving Guaranteed Income plus discretionary Cash Bonuses (if declared) in arrears one year after the end of the Premium Payment Term.

- Cash Bonus payable = Cash Bonus Rate x Annualized Premium

- Guaranteed Income is expressed as Guaranteed Income Rate x Annualized Premium

Guaranteed Income Rate will be known to the policyholder at inception. Guaranteed Income would be payable for 25 years or Policy Term minus (Premium Payment Term + 1) years, whichever is lower, subject to your survival during this period.

b) Maturity Benefit –

i) Under Immediate Income Option –

For a policy where all due premiums have been paid, the maturity benefit payable at the end of the policy term is defined as the following –

- Sum Assured on Maturity plus

- Accrued Cash Bonuses, (if not paid earlier plus)

- Interim Survival Benefit, if any plus

- Terminal Bonus, (if declared)Sum Assured on Maturity is total Annualized Premium payable under the policy during the premium payment term.

Where,

- Interim Survival Benefit = Interim Cash Bonus Rate * Annualized Premium * Months elapsed since last Survival Benefit payout date / 12

On payment of the Maturity Benefit, the policy will terminate and no more benefits will be payable

ii) Under the Deferred Income Option –

For a policy where all due premiums have been paid, the maturity benefit will be the aggregate of the following –

- Sum Assured on Maturity plus

- Accrued Guaranteed Income and Cash Bonuses (if declared), if not paid earlier plus

- Interim Survival Benefit(if any) plus

- Terminal Bonus, if declared

Sum Assured on Maturity is total Annualized Premium payable under the policy during the premium payment term.

Where,

- Interim Survival Benefit = (Interim Cash Bonus Rate * Annualized Premium + Guaranteed Income) * Months elapsed since last Survival Benefit payout date / 12

On payment of the Maturity Benefit, the policy will terminate and no more benefits will be payable.

c) Death Benefit –

i) Under Immediate Income Option –

In case of death of Life Assured during the policy term, the death benefit shall be equal to Sum Assured on Death plus Accrued Cash Bonuses (if not paid earlier), plus Interim Survival Benefit (if any), plus Terminal Bonus (if declared).

The Minimum Death Benefit shall be 105% of Total Premiums Paid as on date of death.

Sum Assured on Death is the highest of the following –

- 10 times the Annualized Premium, or

- Sum Assured on Maturity, or

- Death Multiple x Annualized Premium

Total Premiums Paid is the total of all the premiums received, excluding any extra premium, any rider premium, and taxes.

ii) Under the Deferred Income Option –

In case of death of Life Assured during the policy term, the death benefit shall be equal to Sum Assured on Death plus Accrued Cash Bonuses and Guaranteed Income (if not paid earlier), plus Interim Survival Benefit (if any), plus Terminal Bonus (if declared).

The Minimum Death Benefit shall be 105% of Total Premiums Paid as on date of death

Sum Assured on Death is the highest of the following –

- 10 times the Annualized Premium, or

- Sum Assured on Maturity, or

- Death Multiple x Annualized Premium

Under both options, upon the payment of the death benefit, the policy terminates and no further benefits are payable

d) Rider Benefit –

The policyholder can opt for anyone among the 2 rider benefits in this policy by paying an additional premium. The rider names are as follows –

- HDFC Life Income Benefit on Accidental Disability Rider

- HDFC Life Critical Illness Plus Rider

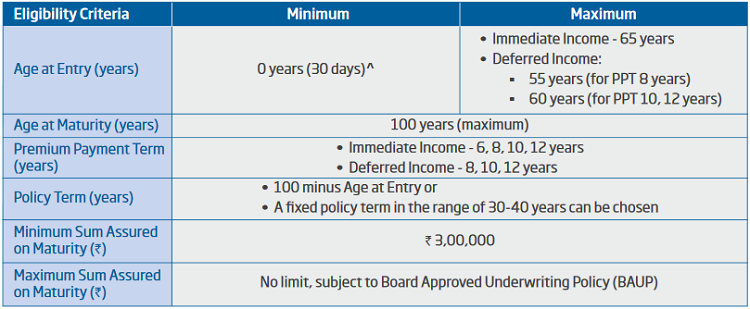

Eligibility Criteria of the Policy –

Is there any grace period in this policy?

Yes, there is a grace period of 15 days for the monthly frequency of premium payment and 30 days for other frequencies to pay the premium without any penalty. The policy is considered to be in-force with the risk cover during the grace period without any interruption.

If the premium is not received before the end of the grace period, the policy will lapse or become paid-up. In case of a valid claim during the grace period, before payment of due premium, the claim shall be payable after deducting the due modal premium.

When can my policy acquire a surrender value?

The policy shall acquire a Guaranteed Surrender Value (GSV) upon the payment of the first two years’ premiums, irrespective of premium paying term. The Surrender Value shall be the higher of the following –

- Guaranteed Surrender Value (GSV); or

- Special Surrender Value (SSV)

Plus, any accrued survival benefit, if not paid earlier plus interim survival benefit.

where,

- GSV = Max (applicable GSV factor * Total premiums paid – Survival benefits applicable till date, 0)

- SSV = Max (Applicable SSV factor * Total premiums paid – Survival benefits applicable till date, 0) plus Terminal Bonus (if declared)

Once the Surrender Benefit is paid, the policy will terminate and no more benefits will be payable.

Is there any provision where I can revive my lapsed or paid-up policy?

The policyholder can revive their lapsed/paid-up policy within the revival period i.e 5 yrs from the due date of first unpaid premium and before the expiry of the policy term.

For the revival of the policy, the policyholder will need to pay all the outstanding premiums and interest on the outstanding premiums and taxes and levies as applicable. Once the policy is revived, the policyholder will be entitled to receive all the contractual benefits.

Can I cancel the policy if I didn’t like its terms and conditions of the policy?

Yes, the policyholder can cancel the policy within 15 days (and 30 days in case the policy is purchased through distance marketing) from the date of receipt of the policy. The period is known as the Free-Look Period.

On submission of receipt of your letter along with the original policy document, the company shall arrange to refund the premiums paid subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by us for stamp duty, and medical examination if any.

Can I take a loan against this policy?

The policyholder can take a loan against this policy only when the policy has acquired a surrender value and also the policy is active. The loan amount will be subject to a maximum of 80% of the surrender value of your policy.

Exclusion under the Policy –

Suicide Exclusions –

In case of death due to suicide within 12 months from the date of commencement of risk under the policy or from the date of revival of the policy, as applicable, the nominee or beneficiary of the policyholder will get at least 80% of the total premiums paid till the date of death or the surrender value available as on the date of death whichever is higher, provided the policy is in force.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.

Does the non guaranteed benifits be given which is mentioned under 4% and 8% for sure irrespective of any factors. If yes, which is given out, the one mentioned under 4% or 8%?

No , 4% or 8% is because of IRDA guidelines only

You should really go for it unless it doesn’t hamper with your near future expenses. Also, the interest rate might seem high, but it only dips down in course of time. Use the free look period well.

What to do in case I don’t need this policy

Dont buy it 🙂

Why not buy it

Because the person said that he does not need it. So I said “Dont buy it”

Manish

what’s the return on investment and how is this comparable to PPF or Bank FD as an assured instrument ?

Better than FD, Not better than PPF when it comes to returns !

Is that really true? There is no guarantee that it will give even 4% return. Stop fooling around and that too with name jagoinvestor.

When will the cash bonus be declared for HDFC Sanchay par advantage? Every year or every financial year

I guess it is added in the policy, not paid out!

whether HDFC Life Sanchay Par Advantages is related to share /stock Market risk or not

No it is not market linked and that’s what keeps it assured of the returns. It is not fluctuating, hence less risk involved, also not too high returns when compared to some good paying market investments.