Aditya Birla Sun Life Insurance Fortune Elite Plan – Review, Features and Benefits

Over the years, you have achieved success and accumulated wealth. Your priority now is to ensure your wealth and assets remain protected for your future generations, while you enjoy the lifestyle you have worked hard to attain.

Specially designed to cater to your financial and estate planning goals, ”Aditya Birla Sun Life Insurance Fortune Elite” is a unit-linked plan that provides insurance coverage and the opportunity of wealth preservation and enhancement.

Features of this Policy –

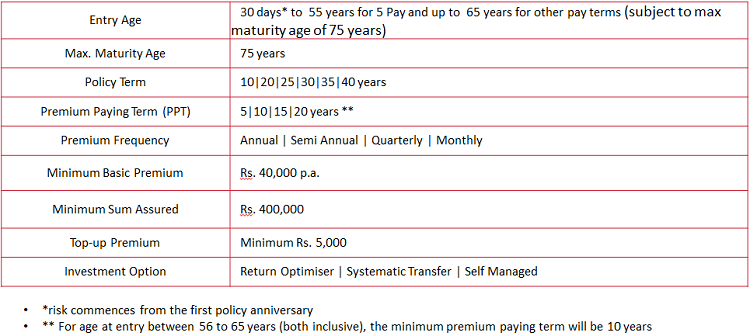

- The flexibility to choose policy term of 10 | 20 | 25 | 30 | 35 | 40 years

- The flexibility to choose premium paying terms of 5 | 10 | 15 | 20 years

- The flexibility to choose from 3 investment options to suit your investment needs

- The flexibility to add top-ups whenever you have additional savings

- No Loans can be taken against this policy

- The flexibility of partial withdrawals to meet any emergency fund requirements

- Tax benefits under section 80C and section 10(10D) of the Income Tax Act, 1961

Investment Options under this Policy –

a) Systematic Transfer option –

- Safeguards your wealth against the market volatilities.

- Available only if you have opted for annual mode.

- Basic premium (net of premium allocation charge) shall be first allocated to Liquid Plus fund option.

- Thereafter monthly 1/12th of the allocated amount shall be transferred to up to 4 segregated fund(s) of your choice viz. Income Advantage, Enhancer, Creator, Maximiser, Multiplier, Super 20, Value & Momentum, and MNC as per the investment proportion for the chosen funds.

- Transfers to your chosen segregated fund(s) will take place monthly on 1st, 8th, 15th or 22nd of the month as selected by the policyholder.

- It helps to mitigate any risk arising from volatility and averages out the risks associated with the equity market, reducing the overall risk to your portfolio

b) Self Managed Option –

- Gives you access to our well-established suite of 16 segregated funds viz Liquid Plus, Income Advantage, Assure, Protector, Builder, Enhancer, Creator, MNC, Magnifier, Maximiser, Multiplier, Super 20, Pure Equity, Value & Momentum, Capped Nifty Index, Asset Allocation.

- Complete control on how to invest your premiums.

- Full freedom to switch from one segregated fund to another.

- Diversify your risk, by allocating your premium in varying proportions amongst the 16 segregated funds.

- Full flexibility to redirect future premiums by changing your premium allocation percentages at any time.

c) Return Optimiser Option –

- It enables you to take advantage of the equity market.

- Protect your gains from the future market volatility and create a more stable sequencing of investment returns.

- Basic premiums (net of allocation charges) are invested in the Maximiser fund.

- It will be tracked every day for each policyholder for a pre-determined upside movement of 10% or more over the net invested amount (net of all charges).

- When the gain from the Maximiser fund reaches 10% or more of the net invested amount, the amount equal to the appreciation will be transferred to the Income Advantage fund at the prevailing unit price.

- This ensures that your gains are protected from any future market volatilities.

- If the gain is less than the pre-determined upside movement of 10%, no transfers will be made.

Benefits of the Policy –

a) Maturity Benefit –

The Maturity Benefit shall be the Basic Fund Value plus the Top-up Fund Value as of that date. At the end of the policy term, provided the policy is still in force, the company shall pay the Maturity Benefit.

b) Top-Up Premium

You may wish to invest additional amounts as top-up premiums anytime during the policy term as long as all due basic premiums have been paid. The minimum top-up premium is Rs. 5,000 and at any point the total top-up premiums paid cannot exceed the total basic premiums paid to date. Top-up premiums cannot be withdrawn for five years unless in case of complete surrender of the policy. Top-up Sum Assured will be 125% of the top-up premium being paid

c) Death Benefit –

In the unfortunate event, the life insured dies while the policy is in effect, the company will pay to the nominee

The greater of the following –

- Basic Fund Value as on date of intimation of death; or Basic Sum Assured and

- Top-up Fund Value as on date of intimation of death; or Top-up Sum Assured

The Basic Sum Assured will be reduced to the extent of partial withdrawals made during the two-year period immediately preceding the death of the life assured from the Basic fund value.

However, the Death Benefit after partial withdrawals shall never be less than Annualized Premium multiplied by 10.

At all times, if the policy has not been discontinued, the Death benefit shall never be less than 105% of total basic and top-up premiums paid up to the date of death reduced to the extent of partial withdrawals made, both from the Basic Fund Value and Top-up Fund Values, during the two-year period immediately preceding the death of the life assured.

In case of death of the life insured, if the life insured is different from the proposer/policyholder, the proposer /policyholder will receive the policy proceeds. Where a policy is issued on a minor life, the policy will vest in the life insured after attainment of the majority of the life assured

In the case where the death of the Life Insured takes place prior to the risk commencement date, only the basic premiums paid (excluding GST, if any) shall be payable as the Death Benefit.

d) Rider Benefit –

For added protection, ABSLI Fortune Elite Plan can be enhanced by adding a rider to the policy at an additional cost-

i) ABSLI Accidental Death Benefit Rider Plus

In the unfortunate event of the death of the life insured due to an accident within 180 days of the occurrence of the accident, we will pay 100% of the rider sum assured to the nominee. Also, we will refund the premiums collected after the date of Accident till the date of death, with interest as declared by us from time to time, along with death benefit payable.

ii) ABSLI Waiver of Premium Rider

In case of the following conditions:

- Policyholder becomes completely disabled due to an illness or accident

- The policyholder is diagnosed with any of the specified critical illnesses

- Death of the policyholder (only if other than the Life Insured)

The company will waive off all the future due to premiums and all the other benefits will remain unaffected. This benefit is applicable only once during the entire premium paying term.

e) Guaranteed Benefits –

In the form of additional units will be added to your policy –

- On the 10th policy anniversary and on every 5th policy anniversary thereafter, Guaranteed Addition is 2.00% of the total premiums paid in the last 60 months.

- In addition to the 11th policy anniversary and every policy anniversary thereafter, Guaranteed Addition is 0.35% of the average Policy Fund Value in the last 12 months

Eligibility Criteria –

Is there any partial withdrawal allowed in this policy?

Yes, the policyholder is allowed to make unlimited partial withdrawals any time after –

- Five complete policy years or

- Life insured attains the age of 18, whichever is later.

The partial withdrawals shall first be adjusted from Top-up Fund Value (except any top-up premiums paid in the previous five years immediately preceding the date of withdrawal); if any. Once the Top-up Fund Value is exhausted, partial withdrawals would be adjusted from Basic Fund Value. The top-up sum assured will remain unchanged after any withdrawal from the top-up fund value.

The minimum amount of partial withdrawal is Rs. 5,000. You are required to maintain a minimum Basic Fund Value of one basic premium chosen plus any top-up premiums paid in the previous five years immediately preceding the date of withdrawal. The total amount of partial withdrawal during a policy year shall not exceed 25% of the total Policy fund value at the beginning of the policy year.

Can I surrender my policy?

In case of emergencies, the policy can be surrendered anytime during the policy term. If the policy is surrendered after completion of five policy years, Fund Value will be paid immediately. If it is surrendered before lock In period, the proceeds of the discontinued policy shall be payable at the end of the lock-in period.

Is switching of funds allowed in this policy?

The policyholder has full flexibility to switch money from one segregated fund to another at any time provided the switched amount is for at least Rs. 5,000. You can change from one investment option to another investment option anytime after the first policy year.

Is there any premium redirection in this policy?

To meet your ever-changing investment needs, the policyholder will have the full flexibility to redirect future premiums by changing your premium allocation percentages at any time.

Is there any option of Reducing the premium payment term?

The policyholder shall have an option to reduce the premium payment term provided the policy is active for full sum assured and provided that such reduction is subject to boundary conditions of the product. This option shall be available only after the first five policy years.

Can I return my policy if I didn’t like its terms and conditions?

Yes, the policyholder has the right to return the policy to the company within 15 days (30 days in case the policy is purchased through Distance Marketing) from the date of receipt of the policy. This 15 day period is known as the Free Look Period.

The company will pay the policy fund value + the non allocated premiums + charges levied by cancellation of units once they receive in written the notice of cancellation (along with reasons thereof) together with the original policy documents.

The company may reduce the amount of the refund by the proportionate risk premium and the expenses incurred by us on the medical examination of the proposer and stamp duty charges.

Various charges in the policy –

a) Policy Administration Charge –

The policy administration charge is deducted at the start of every policy month by canceling units proportionately from each segregated fund you have at that time. The charge is 0.6% of basic premium p.a., subject to a maximum of Rs. 6,000 p.a.

b) Miscellaneous Charges –

Rs. 50 per request is charged for a change in investment option, premium re-direction, fund switch partial withdrawal or any additional servicing request. We do however reserve the right to charge up to Rs. 500 per request in the future.

c) Premium Allocation Charge –

- A premium allocation charge is levied on the basic and top-up premiums when received.

- A premium allocation charge of 2% is levied on any top-up premium when paid.

When can my policy terminate?

Your policy will terminate at the earliest of the following –

- The date when there is complete withdrawal as per the Policy Discontinuance Provisions;

- The date the Policy Fund Value becomes zero; or

- The date of settlement of the death benefit; or

- The date of payment of the surrender value, if any; or

- The date when the maturity benefit is paid

Exclusions under the policy –

In case of death due to suicide within 12 months from the date of commencement of the policy or from the date of revival of the policy, as applicable, the nominee or the beneficiary of the policyholder shall be entitled to the Policy fund value, as available on the date of intimation of death.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.