Category 1– Those who invest their money manually at the end of each month

Category 2 – Those who auto-invest at the start of each month.

Today we will discuss which option is better than others and what are the benefits of choosing the auto investment mode at the start of the month

While investing at the end of the month manually is very intuitive and sounds comfortable to most of the investors, we think that investing in the auto mode at the start of the month is much better and beneficial for an average investor.

Most people adopt the “Save whatever money is left at the end of the month” approach in their financial life, but there is enough research and proof that it does not work for the larger masses. The best option is to put your investments in auto mode and let it happen automatically each month.

Now let’s looks at the benefits of investing in auto mode at the starting of each month

Benefit #1 – You can manage your lack of discipline

Can you trust yourself in investing each month manually for the next 5-10 yrs?

If you decide to invest Rs 10,000 on the 25th of every month for the next 10 yrs, will you be able to do it consistently for the next 120 months (10 yrs X 12 months)?

Trust me, it’s a lot of work and very hard to act in a robotic fashion.

Sometimes, you will postpone it

Sometimes, you will feel – “Let’s do it next week”

Sometimes, you will skip it for the sake of other expenses

Sometimes, you will just be involved in some other tasks

Sometimes, you will actually follow it

And most of the times, you will just forget it

Compare this will an auto mode, where you have set up your SIP (automatic monthly deduction in mutual funds) or a recurring deposit (for those who don’t think mutual funds are their cup of tea), and the money automatically gets deducted from your bank account (considering you have the balance) and then gets invested without your intervention.

Which one of these options do you feel will be in your interest?

Most people think that each month of a certain date they will invest some X amount on a regular basis, but they are not able to do it on a consistent basis. They either lack in discipline or they are so consumed in other areas of life, that they are not able to follow what they promised themselves.

Due to this, their financial life suffers. The money does not get transferred from the bank to the investments and eventually gets spent.

Trust me, even if you are the KING of indiscipline, the auto investing will create wealth for you!

Benefit #2 – You avoid unwanted expenses

“Supply creates its own demand” – a classic principle of economics. If you have money lying available in your bank account, you will find enough reasons for spending that money.

Hence, if you think – “Let me first spend, if anything is left, I can always save/invest it at the end of the month” , it’s almost guaranteed that you will not find any money at the end (unless your income is very high compared to your expenses)

This is the reason why you should create a structure that takes away some part of your salary from your savings bank account to somewhere else which is not easily visible to you (like PPF, RD, or mutual funds).

I have devised something called a “10% margin system”, which can truly transform the way you manage your cash flow. It’s one trick that will help you save more money each month.

Under this system, you only keep your monthly expenses + 10% more in your bank account and invest everything else at the start of each month. Click here to read more on this 10% margin system.

So if you invest at the start of this month, you will shop only limited to your needs, you will not overeat outside, and to a great extent, you save on the unwanted expenses.

The whole idea is to “cut” the excess supply of money to yourself by investing it at the start of the month itself.

[su_button size=”6″ radius=”square” background=”#306bf1″ url=”https://www.jagoinvestor.com/mutual-funds#account”]Start your FREE Mutual Funds Account with Jagoinvestor[/su_button]

Benefit #3 – It develops the Habit of Saving

One of the biggest challenges for new investors is to develop the “habit of saving” in them.

The world these days is such that it’s very easy to SPEND money on things you don’t really need. You spend on mobiles, gadgets, parties, traveling and consuming various things (nothing wrong in these things). However, beyond a point, you start crossing the limits and you start “wasting” money at the cost of the future.

Most of the investors find themselves not saving any money and living paycheck to paycheck for the simple reason that they never develop the saving habit and eventually end up in the never-ending cycle of earn -> spend -> earn -> spend

You should check this excellent simple video by Brain Tracy on why you should save at least 10% of your salary if you are a beginner investor.

Some time back, I had written an article for beginner investors and how they should manage their financial life. Please go through it.

If a person sets up the auto investing at the start of the month, then at some level the habit of saving starts. If one is able to continue that for a few months, the overall expenses will get adjusted with the leftover money in the bank account. If you are a new investor, the primary reason to start your SIP or RD is not to save money, but to develop the habit of saving.

Benefit #4 – You reduce the risk of investments

If you do not spread your investments across months, then there are good chances that if the markets fall suddenly, its impact will be high on your wealth. In the same way, the upside potential is also high. But let’s focus on the risk part here.

If your investments are happening each month on a regular basis, then your investments are spread over all kind of markets like bull and bear market (assuming your investments are happening in mutual funds SIP)

So if you want to control the risk part, it’s a good idea to let your investments happen on a monthly basis and not a one-time basis. A good example of this is SIP in ELSS vs. One time investment in ELSS for 80C.

For example, consider two friends Ramesh and Dinesh

Case 1: Ramesh invests Rs 1.5 lacs in one go for tax saving during the month of Feb, but the markets in next one year go up and down and eventually go down by 10% . In this case, the investment done will be having high risk, because all money was invested in one go (which also means that potential returns can also be high if markets do well) and all the ups and downs impact will be on the total money.

Case 2 :However, Dinesh does a SIP of Rs 12,500 per month in ELSS, and in 12 months he invests total of Rs 1.5 lacs. In this approach, the investments are spread over 12 different months and risk (and returns) will be more controlled. If markets go down in the first few months, then it’s only for the amount invested before that event.

Benefit #5 – Guilt-free Spending

This is one benefit that is often not appreciated enough.

When you save your money at the start of the month, then the rest of the money is available for your expenses. Now you can spend it freely, without any guilt.

Most of the people who do not save enough or save at the end of the month, keep worrying and thinking while spending their money. They keep feeling “Bahut Kharcha ho Gaya is Baar” while going for outings or movies etc. This is because they have not allocated money for the future.

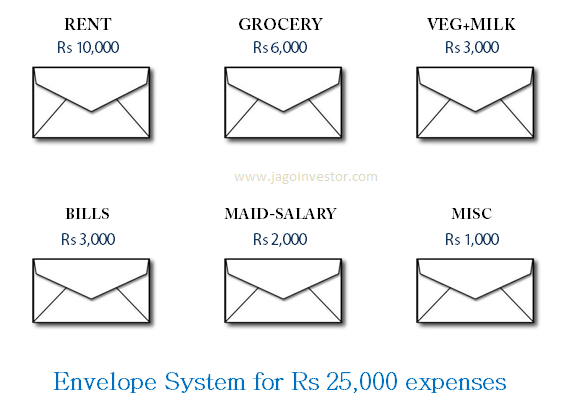

So you should start your auto investing (SIP is one of the best way of doing that) and once you have done that, I suggest you adopt the envelope style of expenses where you create few envelopes for each expenses category and put the cash in the envelope and use only that till the end of the month.

However once you setup your automatic investments at the start of the month, you then just have one agenda – “Spend rest of the money” guilt-free.

Are you starting your investments in Auto mode Now?

So what are you waiting for?

If you have not yet started your investments in auto debit mode, you should immediately start your investments. You can either start your SIP with our team or reach out to your trusted advisor who can guide you on this.

[su_button size=”6″ radius=”square” background=”#D8180A” url=”https://www.jagoinvestor.com/mutual-funds#account”]Start your FREE Mutual Funds Account with Jagoinvestor[/su_button]

Do you have any life insurance? And are you really very sure that it will protect your family?

Majority of people who buy life insurance in India, buy it for the sole reason of protecting their family’s future. But is taking the life insurance a sure shot way to protect your family (I mean your immediate family here, which is spouse + kids)?.

If the primary breadwinner dies because of any reason, the family will have to suffer in absence of a regular income. The spouse will suddenly not get any income and might have to start earning. Your family and kid’s future is also at risk.

Let’s see some risk your family has

What if you are businessmen and you owe money to someone? After you are dead, the creditors will approach the court and they will get the money out of your life insurance proceeds

Consider you have a big home loan which you have not accounted for while taking a term plan. If you die, the first right will be of the home loan lender because the loan is on your name. The right of the family comes only when your loans are paid off.

What if you have not created your will and there are family members who claim their right in your life insurance proceeds?

What if you yourself change your mind later and don’t want to give the insurance proceeds to your own family?

Are you prepared for this situation? If not then think about it. There is a way which will help you at some points if this such situations appears in-front of your family in your absence and the solution is MWP Act.

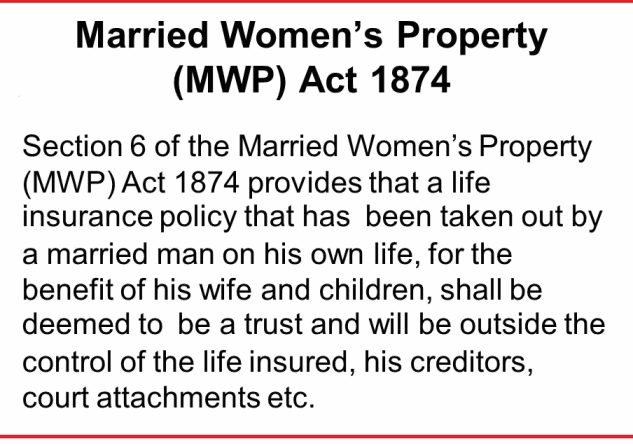

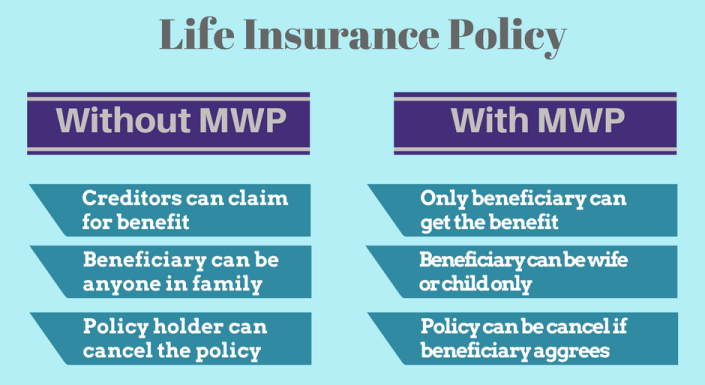

MWP means Married Women’s Property Act. This act is prepared by taking into consideration the rights of a married woman on her property. According to MWP Act . the earning of a married woman in India is considered as her own property and this Act Protects the property owned by a woman from Creditors, relatives and even from their husbands.

Buying Life Insurance Policy under MWP Act

MWP Act 1874 under which Section 6 deals with life insurance. If you buy a life insurance under MWP Act, then it will protect the women’s right on the life insurance proceeds money in all the cases. Even the husband can’t do anything about it once the buying is bought under MWP act. This applies to all kind of insurance policies be it a term plan or an endowment/money back plan.

Who can be the Beneficiary and Trustee?

When a policy is bought under MWP Act, the policy is treated as a TRUST and its guarantees that the proceeds from life insurance policy are free from any creditors or court attachments.

The first right is of the family only (women and kids). Imagine if you buy an endowment plan which matures in 20 years and you bought it under MWP Act. Once the policy matures, then even the person who started it will not be able to claim anything. The first right will be of the beneficiaries mentioned in the policy.

Beneficiaries can be:

The wife alone

The child/ children alone (both natural and adopted)

Wife and children together or any of them

Trustee can be:

Unlike beneficiaries, having trustee is not mandatory for this MWP Act. The policy holder can mention one or more trusties. Having a Trustee is not compulsory but if the beneficiary is minor then in that case it is compulsory to have a Trustee. The Trustee should not be minor. The Trustee can be change whenever the policy holder wanted. The Trusties can be –

A person

A bank

An institute

Beneficiary herself/himself

How will the beneficiaries get benefit ?

When something wrong happens with the policy holder and the insurance is claimed by the family, the creditors can claim for the insurance benefits. In this case the family members will get less benefit of the policy. Or sometimes the other family members can also claim for the part in that policy if the policy holder does not have will.

But if the policy is covered under MWP Act then the whole benefit will go to the wife or kids (whoever the beneficiary is) of the policy holder.

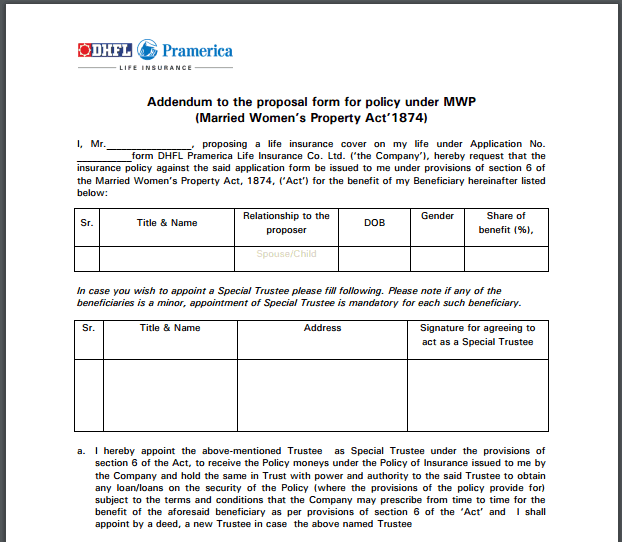

Procedure to buy life insurance under MWP Act

The process is very simple. All you have to do is fill up a MWP addendum form separately at the time of buying the policy. Your agent can help you with that form or talk to the company in case you are directly buying it from the insurer.

However note that it can’t be added separately once you have completed the process of buying the life insurance (means you can’t add the MWP act later)

Who can take a Life insurance policy under MWP act ?

Any married man can take a life insurance policy under MWP Act. This includes divorced persons and widowers. The policy can be taken only on one’s own name, i.e., the life assured has to be the proposer himself. Any type of plan can be endorsed to be covered under MWP Act.

Difference – Insurance With MWP and Without MWP

There is not a lot of difference in taking a life insurance under MWP Act or without MWP Act but we can see some points which shows the difference. See the following picture.

Are there any disadvantages of buying policy under MWP Act?

Yes, There are disadvantages to signing the MWP addendum as well

The Beneficiaries cannot be changed. In case at some point you decide to change the beneficiaries . It won’t be possible if you sign a MWP addendum.

Loan cannot be taken on the basis of the policy. The policy could not be used as a security against loan.

That makes it also necessary for loan providers on Life Insurance policies to check before taking it as a mortgage for lending whether the policy does not contain any MWP addendum, as they will not get the benefits from its proceeds.

This article is a guest post by one of our readers Vikram Agarwal, who wanted to share his experience on the concept of “Early Retirement”. Vikram was generous enough to share his story and some of the real-life things which will make you think hard about this concept. Like Vikram, if you feel you can write on jagoinvestor, please click here

Over to Vikram.

—

Most of my friends in my friend circle in late 30’s ask me one question – “How much money I should have now, so that I don’t have to work anymore while maintaining a decent standard throughout of my life, with all the future expenses taken in to account?”

They want to ‘Retire Early’

In fact, I also used to be an ardent follower of the concept of ‘Early Retirement’ but now have realized that the concept is more like a mirage, which does not exist in reality and once you reach there, it vanishes.

Moreover – in my view, it is quite dangerous for an individual to run after this concept. In my opinion, you achieve retirement either ‘NOW’ or ‘NEVER’ irrespective of your current level of income or financial state.

Early Retirement is a state of mind

It is a state of mind, rather than a stage achieved. The moment you achieve early retirement as per the physical criteria set by you five years ago taking inflation, life expectancy and all major and minor expenses in your monthly calculations, by the time you achieve retirement as per your old financial definition, all those things become sub-normal or default.

Your mind will have another definition that looks normal for you in today’s context for example for future kids’ education, your house quality, the type of car you own, facilities you desire and all other such expenses.

My personal example

For example, five years before, owing a 2 BHK house in the newly developed area with Marti Dzire hatchback car and with the kids going in a decent school used to be a life I wished for and I had done calculation for the amount required to maintain the same standard throughout rest of my life without working.

And that was ‘Early Retirement’ according to me and as per standard definition.

But, now it seems owing a 3BHK house (one extra room for parents or for guests) in a good location of a metro city, a nice Honda sedan and a ‘good’ school for kids throughout their education duration is ‘Normal’ for me. Now it’s the standard, I would like to maintain before retirement and after retirement.

My next target!

My new “target” might be owing to a villa or bungalow, and a nice SUV and kids in the ‘best’ school of the area. And once I achieve it, I think it will become a new normal with time.

The next level

And who knows, a car for wife will be a standard I will look for in the future, as I will not be able to manage all the household activities on my own and an extra car becomes a necessity. (I did all my retirement planning calculations with taking decent return on investment as 10% which is quite modest in the long term, so as not to fall in the trap of exuberant returns which might be temporary and actual return might spoil all your calculation.)

Even with a slight increase in any of the above ‘wish’ list (like the possibility of sending you kids abroad for his or her graduation) will push you back in time and you will not be able to achieve you ‘wished’ retirement any time and this carrot and stick game continues.

When your desires convert to your “needs”

You would not know when your ‘desires’ got converted into your ‘needs’. And now it looks like there is a meaning in the sayings of wise old man that “There is enough in this world for one’s needs and not for one’s desires”. I can sense the truthfulness in these lines with some financial literacy and practical experiences.

If at all early retirement could mean anything for a ‘disciplined’ guy is thru’ a windfall gain from lottery or legacy, otherwise if one tries to achieve early retirement from normal gradual process where mind and hard work is involved, his thinking mind will quickly adapt to current situation and will turn the old desired standards in to ‘Normal’ or ‘Below Standard’ life in today’s’ terms.

The word ‘discipline’ need stress here because there is an old saying that irrespective of the size of the pot, if kept isolated all the water will drain out eventually if not refilled on time and only a disciplined life can control this drainage process and can prolong it (Read, why we are overspending these days by Manish)

Or you can become a hermit in deep forest, secluded from this physical world and concepts of ‘Future Expenses’, ‘Inflation’ become meaningless for you, one can think of early retirement stage.

But, I guess this is practically impossible and this article is not intended for those who might be thinking of this stage as one of their future possibilities.

Story of my seniors – Real-life case

I personally know two of my seniors who after working at very senior positions in the company left their jobs as they thought they had enough money to sustain the rest of their lives and tried to follow new pastures in future life.

But, eventually, they had to join back in their respective jobs in order to meet their monthly bills and continue with their other passions in life.

It is human psychology to get adapted to the current situation and at present it looks like achievable calculations on paper and unreal confidence of being satisfied in case you achieve current target, but in reality it does not happen and by your own nature and human being’s reason of existence, you will always be pushed to work.

Basic foundation of human existence is WORKING

This wish of ‘ Not working’ one day will take you away from ‘Karma Yoga’ which is the basic foundation of human being’s existence. Even in GITA, it is mentioned that all of us have to work one way or other and this is the law of life.

I remember a recent discussion with a prominent businessman in my home town. He told me that he used to ‘struggle’ a lot to book rooms in his locality for any private family functions for his guests they had to ‘adjust’ sometimes as per hotel terms and conditions.

Now, he has built his own guest house and no need to be ‘dependent’ on the hotels any more for bookings, etc. and I was thinking that if this rich man thinks booking rooms in 5 star hotels as per their terms and conditions is a compromise in life, what independence could mean for him ?

Don’t buy anything less than a BMW

A few years ago I was having a discussion with one of my friends and in his views, having something below Mercedes or BMW is a compromise as all other brands do not give importance to safety standards and life is precious more than anything else.

At that time owing a Honda city and maintaining it was the kind of life I wanted to live for all early retirement calculations and now since I can afford Honda City easily, I have a choice, either to keep working to be able to buy Mercedes or BMW one day or put my life always at risk while driving mass-produced cars!

We can retire the day we are BORN

On second thought, I achieved financial freedom years back, the moment I had enough money to be able to afford public transport all through my life. In fact, to take it to one extreme side, we have the potential to retire the day we born and it is only afterward that we enter into the working force in this world, fall into the financial trap and again want to get rid of it.

This wish of ‘Not working one day’ can make you lazy, averse to work and afraid of accepting challenges as in your thought process you are always after something else and it is quite natural that you will not focus on the very basic aspect of life you want to get rid of one day.

Here is a great answer which deals with this issue on quora thread

These days a lot of people think of retirement at an early stage, some talk about retirement in the late ’30s or early ’40s and there are various articles circulating around to tell how to achieve it.

But, this kind of thinking pattern in today’s youth is preventing them from acquiring skills which can help them in their current job profile and make it interesting.

Story of my father

My father achieved his financial freedom just after his retirement and both of his sons are well settled and living a decent life and he does not have any liability in his life, yet he is always focused on ‘working life’ and whenever he gets any chance of making money with guest lectures etc., he always looks forward to it and that’s what he says is the secret of his healthy life.

Had he focused on early retirement, this ‘fire’ or ‘energy’ inside him would have subsided quite early and he could have attracted many lifestyles related diseases like blood pressure and diabetes etc, which is happening these days even to the young generation.

So, one should not focus on achieving early retirement any time but should think of living a simple, satisfied, and an exemplary life and realize that the ‘Work’ is the only thing that matters in life and for this you need continuous practice for sound physical and mental health to keep your body fit and energetic and let other things come on its own without worrying about it.

Watch this TED video which talks about an experiment of living a simple life in a tiny home.

It is a good idea and in fact a necessity to have the habit of saving and investing, but the idea should come from the need to meet future expenses and not to achieve early retirement.

So what should be your plan in life?

The financial goal in one’s life should be to have sufficient inflation-adjusted funds for all major expenses in the future like owing a house, Kids education funds, children’s marriage funds, emergency funds, and retirement funds in present terms and all funds invested properly.

At large, one can think of a ‘stage’ where he or she will not be worried about ‘Net savings’ from the income and can live a life one desires with his current income from job or business and even If he/she spends all of the earnings he should not be worried financially.

The more one earns, the more facilities one can desire and his current lifestyle will remain in accordance with his income levels and this is what I call real ‘Financial Freedom’.

That is an inherent assumption here that the rise in expenses (with inflation) will be taken care of by salary increments/ job changes or business expansionsand for there is no other alternative but to ‘Work’.

What do you think about Early Retirement?

So let us know what you feel about this concept and my points regarding it? Do you agree with them? Is there any point where you can add?

Would you like to share your own story in the comments section and how you have dealt with the concept of early retirement? We would like to thank Vikram for his contribution on this subject on this blog.

Also, if you feel you can write on jagoinvestor and contribute, please click here

Today, I am going to reveal a secret trick that will help you to increase your monthly investments by some margin. This trick is more of a psychological shift in the way you think about money, emergencies and how much should you invest.

However, this is applicable to only those who are already investing some money on a regular basis each month.

Let’s start …

You might be thinking that my secret is nothing but making your savings “automatic”. But no, it’s not the case. Making your investments “automatic” is just the first step, but there is something else that will take your savings to the next level.

Let’s get into it!

Here is how most people invest their money

They earn a salary

They spend money on their regular expenses (Rent, Grocery, Movies, travel)

Some money is left at the end of the month

and finally, a partial amount out of that is invested

Did you see that last line?

Only a “partial” amount is invested in the leftover savings at the end of the month is invested, not FULL.

Let’s dig deeper into this …

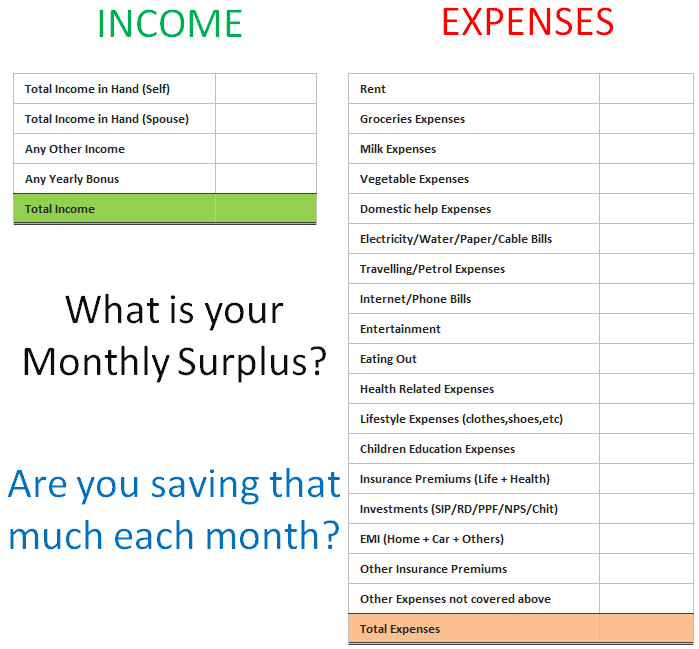

Take a sheet of paper (or open an excel sheet). Write down the total income you get in a month on the left-hand side, and on the right side, mention all kinds of expenses you have. Put Rent, Groceries, Maid expenses, Travelling, Eating out, movies and whatnot.

Now add up all the expenses and find the total expenses and deduct it from the total income you get each month. You will get your Monthly Surplus!. This is the amount you are left over each month and you should ideally invest this whole amount.

Below is a template which you can use for the calculation

What is your monthly surplus?

Will you start a Recurring deposit for that amount or start an SIP?

I guess the answer is NO.

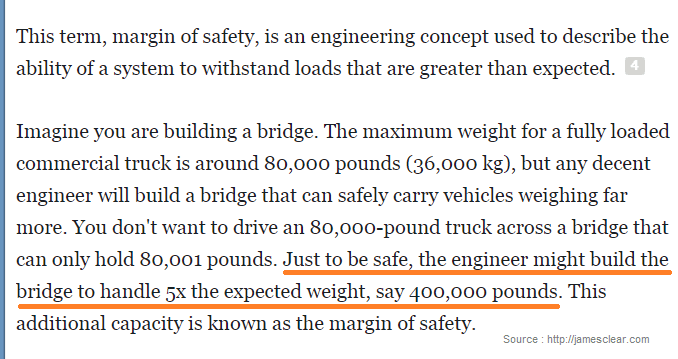

As an example, if a person is earning Rs 1 lacs per month and their expenses are around Rs 60,000, their monthly surplus is Rs 40,000 per month.

But this person will probably invest only Rs 15,000-20,000 per month on a regular basis. They will keep the rest as “Margin of Safety” amount which they might need, because what if they suddenly need it?

The margin of safety is a simple concept, it’s just an “extra buffer” for “what if things go wrong” kind of situations.

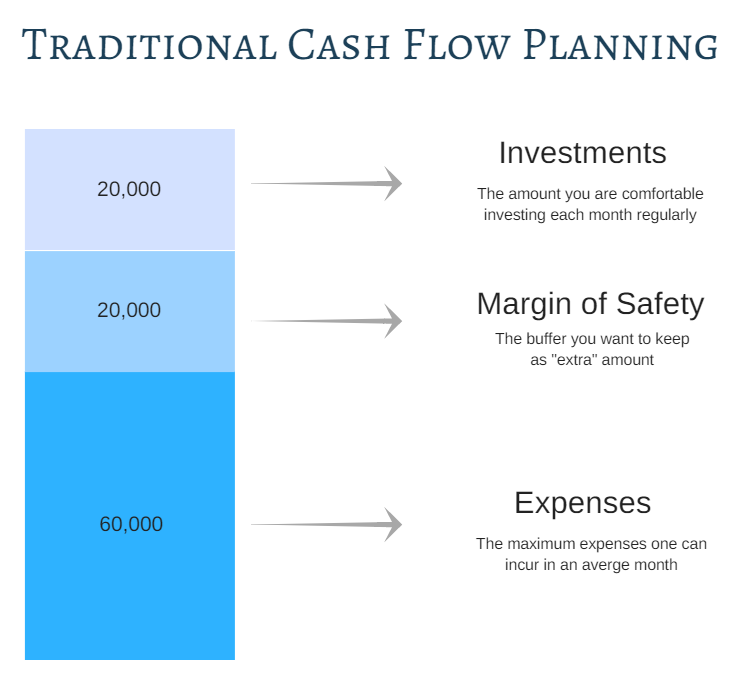

This is called a traditional style of cash flow handling which is a very intuitive and natural way of thinking. We all do it and it feels right!

But there are some problems with this approach

But there is one big problem

While this traditional method looks very natural, there is one big issue with it. Here it is!

Once your investments are set, you feel a sudden excitement that now your investments are in shape, but because you have left a big margin of safety (the extra buffer), your expenses will automatically expand and eat away your margin of safety.

The mere availability of the buffer money will create various short term demands in your financial life and you will use that buffer each month.

Suddenly you will start ordering various things online (most of the time things which are not required), your eating outs will increase, upgrading your phone will appear within your budget, etc.

Supply creates its own Demand – Economics 101

The availability of money will create the demands in your expenses and almost all the time you will justify them. So from Rs 60,000 expenses, you will see that automatically it’s reaching Rs 80,000.

And after some time you will be used to Rs 80,000 per month expenses.

Just imagine, if the person had started a Rs 30,000 SIP and left just Rs 10,000 as a margin of safety? Can you see that here the person still has a margin of safety and invests 50% more amount each month?

What about Rs 35,000 SIP and just Rs 5,000 as a margin of safety?

Welcome to 10% margin Cash flow Management System

This is the crux of the system.

We all feel that we need to keep a big margin of safety because in our mind things will go wrong. And they will!

There is no doubt that things can go wrong in some months and some unexpected expenses can come up which can really disturb your regular investments and that’s why most of the people leave a big buffer between expenses and investments.

However, let’s deal with reality.

Most of the times these emergencies are not real emergencies and if we didn’t have enough margin of safety, we would have justified them as “not important” expenses!

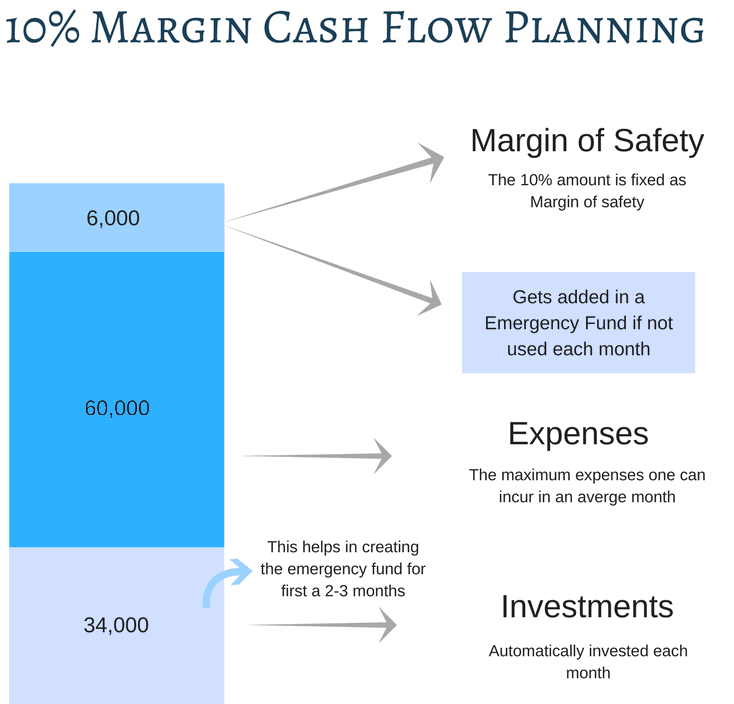

Also, you should not depend on your monthly cash flows for emergencies and have a separate fund that can be touched in case a real surprise expense comes up. I call this new system as “10% margin Cash flow System”

10% margin Cash flow system

Here is how you design this cash flow system

Step 1: Write down all your expenses and make sure you put realistic numbers, neither less nor very big.

Step 2: Calculate 10% of your expenses and that’s your margin of safety. If your expenses are Rs 40,000 per month, then your margin of safety is Rs 4,000

Step 3: This margin of safety amount is the only extra money you will keep with you each month apart from your expenses, and even this money should be auto invested in a liquid fund, which can be redeemed on a short term notice of 24 hours.

Step 4: Make sure that before you start your actual investments on a monthly basis, you create enough emergency funds which can be 3X of the size of your monthly expense. Any sudden surprise expenses which are outside of your regular expenses list will be taken care of from this emergency fund and not your monthly surplus.

Step 5: Set up your investments in an automatic mode (like SIP in a mutual fund, or a recurring deposit or a combination of both) for all the money left other than regular expenses and 10% MOS (margin of safety)

Here is how it looks like

Taking the same example of Rs 1 lac income, the guy has Rs 60,000 expenses in total. His margin of safety is Rs 6,000. Rest amount left is Rs 34,000

For the first month, he puts this full 34,000 in a liquid fund. If any additional money is left from the 6,000 MOS then he puts that in an emergency fund, else he can spend it. For next 2 months, he puts 68,000 more in a liquid fund and his total liquid fund amount is around Rs 1 lacs +

Now, this guy will set up his SIP of Rs 34,000 per month.

Now imagine what happens in 4th month

In 4th month, here is how it looks like

Rs 34,000 SIP is executed and the money gets invested (make sure the SIP date is in the start of the month)

Rs 60,000 is the regular expenses

If there is any need of extra spending, then Rs 6,000 extra is already there (most of the months should be like this)

If for some reason, some surprise expenses come up, you redeem that much money from liquid fund and use it.

Repeat!

Can you see how the whole game changes here?

I hope you got the whole idea of this new model now.

You can always withdraw the money if a real emergency arises

I tried this concept on one of my friends last year. I asked my friend if he will be able to do any SIP?

He said “NO”.

His expenses were almost equal to his income. However, I said that he should start a small Rs 5,000 SIP. He said that he will not be able to because he is not left with any money at the end of the month.

My simple solution was – “Withdraw the money in a month if you really need it”

His SIP ran for the next 12 months

He finally started his SIP with a lot of reluctance and the SIP ran for 12 months straight ! with 1-2 withdrawals in between. However, my friend was proved wrong.

The mere unavailability of money made sure that he had to fit his expenses into this “visible income”.

So don’t worry and dare to start a bigger SIP then you can handle, in the worst case, you can always STOP it, you can always redeem some money back if you need it. But in my experience in most cases, people are able to handle bigger investments each month compared to what they imagine.

Let us know if you liked this article and if you are going to implement this new model of investing?

Do you really think this unconventional way of cash flow management can bring different in your financial life?

Are you one of those investors who are still away from mutual funds investments because you do not have enough understanding about it or have a lot so myths about them?

Every day we get constant inquiries from several of our readers who want to invest in mutual funds and often they have myths, which make us wonder about those myths.

So in this post, I have listed down 33 various myths related to mutual funds and SIP in general. So if you are totally new to mutual funds, reading this article start to end will make you fully knowledgeable about mutual funds.

So let’s start…

Myth #1 – SIP is the name of an investment product

A lot of people think that “SIP” is the name of some investment products other than mutual funds. So they say – “I want to invest in SIP”. However, SIP means a systematic investment plan, which just means a way to regularly invest only in mutual funds. In this, a pre-fixed amount is automatically deducted from your account and gets invest in mutual funds on a pre-defined date.

For example, if you are doing an SIP of Rs 5,000 in ICICI Pru Discovery mutual fund on the 10th of every month, then on the 10th of each month, Rs 5,000 will get deducted from your bank account and will get invested automatically.

Myth #2 – I can’t stop SIP in between once I start it

Another myth that stops investors from entering mutual funds is that they think starting SIP for X yrs, is a commitment they can’t break in between and they will face some penalty if they stop their investments.

A lot of people do not want to give any PROMISE of regular payment. However, the truth is that once you start the SIP, you can anytime stop the SIP in between. So don’t worry while starting the SIP for the next 5, 10 or 30 yrs. The day you want to stop it, it can be stopped with just one notification!

Myth #3 – All the money from ELSS can be withdrawn after 3 yrs if one is doing SIP

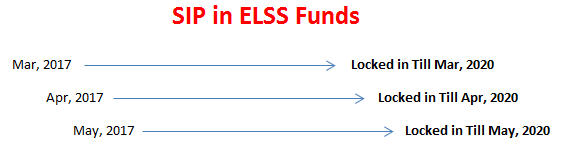

One of the biggest myths of investors is that if they are doing SIP in ELSS (tax saving mutual funds), then after 3 yrs, they can withdraw all their money. However, that is not true. Each investment in ELSS is locked for 36 months from the date of investments. This means that the first SIP which goes in March 2017, will be free of lock-in only in April 2020.

The same is the case with the installment which goes in Apr 2017 (will be free in May 2020)

Myth #4 – Lower NAV is cheaper than higher NAV

Most of the mutual fund’s investors think that a smaller NAV mutual fund is a better deal compared to a higher NAV mutual fund. While this may be sometimes true in case of stocks because a Rs 10 stock has the potential to grow faster than a stock with Rs 10000 stock value.

But in case of mutual funds, NAV has no significance. It’s ZERO!

Because your mutual fund’s appreciation has everything to do with the appreciation in NAV value in percentage terms and not an absolute value. I mean if you invest Rs 10 lacs in a fund with NAV of Rs 10, and if the mutual fund performs great and in the next 5 yrs it doubles in value, then the NAV will rise to Rs 20 and your fund value will rise to Rs 20 lacs.

However, if the NAV was Rs 10,000 per unit, still the effect would be the same for you. The NAV would have increased to Rs 20,000 and your value would have increased to Rs 20 lacs. No difference as such.

So stop thinking that a fund is better (especially NFO’s) just because its NAV is lower.

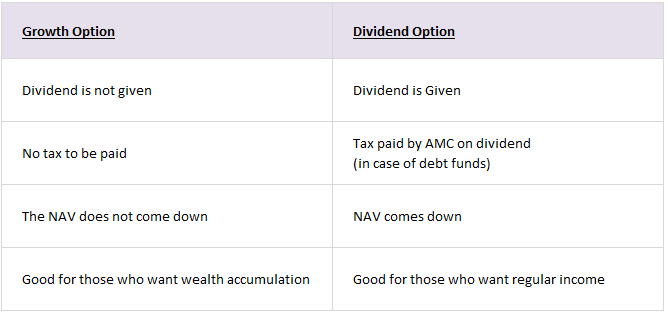

Myth #5 – Dividend in mutual funds is better than Growth option

Dividends are not extra!, The NAV comes down by that margin after the dividend is paid, on top of it, if the fund is not an equity fund, a dividend distribution tax is first paid by AMC, which lowers the return of the investor. However, in the case of growth option, the money remains in the fund itself.

For example, imagine a fund XYZ with NAV of Rs 100 and a dividend declaration of Rs 10

Now in case of dividend option, Rs 10 will be paid to investors and NAV will come down to Rs 90.

However in the case of the Growth option, nothing is paid to the investor, but the NAV is Rs 100.

Myth #6 – Mutual funds means Stock Market

One of the most common myths is that mutual funds are highly risky because they invest in stocks. However, this is half true. Only equity mutual funds invest in stocks and are risky (in fact volatile is the right word, not risky)

There are other categories of mutual funds called debt mutual funds, which do not invest in equities. They invest in bonds, govt securities, and other secured investments. While debt funds have their own risks and even their returns are not 100% stable, still, debt funds are highly stable when it comes to returns and often provide better tax-adjusted returns then most of the bank fixed deposits.

Myth #7 – You have to invest big amounts in mutual funds

Many small investors stay away from mutual funds and stick to recurring deposits and other products because they think that mutual funds are for big investors and one has to invest big money in it. However, you can start a monthly investment of even Rs 1,000 per month in most of the funds. If you want to invest on the onetime basis, the limit is Rs 5,000.

So someone who is just earning Rs 10,000 per month and wanted to invest 10% of his income, can also start mutual funds SIP.

Myth #8 – Mutual funds are always for long term

Mutual funds are marketing as long term investments most of the time. However, it’s not always the case. There are mutual funds called liquid mutual funds and even short term debt funds which can be used for short term investment horizon like 6 months or 2 yrs.

This article from Economic times talks about some of these funds

Only in case of equity mutual funds, it’s suggested that one should invest from a long term perspective to reap the maximum benefits.

Myth #9 – Mutual funds offer guaranteed returns

No, Not always.

Actually never!

Mutual funds never offer a guaranteed return like a fixed deposit. This is one reason why many investors who are totally in love with “assurity” shy away from investing in mutual funds.

Various categories of mutual funds offer various return range. An equity mutual funds can offer return anywhere from -50% to 100% return in a year (just a high level estimate). Whereas a debt fund can also deliver a return ranging from 5% to 15%. And a liquid fund will mostly give a return in range of 6-8%

So the returns are not guaranteed, but highly probably within a range depending on its category.

Also note that as the investment horizon shifts from 1 yr to 10-20 yrs, the probability of getting a stable return within a range increases.

Myth #10 – I will lose my money if the mutual fund’s company goes bankrupt

This is common thinking, but not true

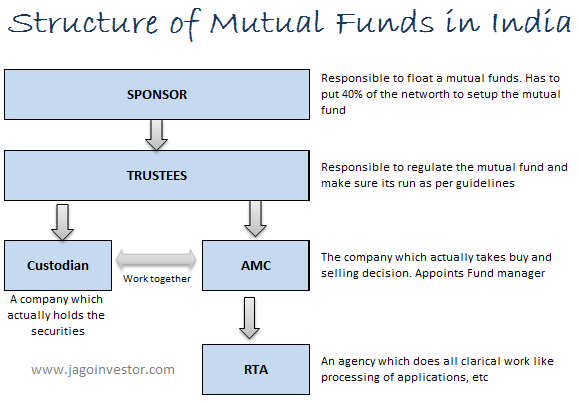

Mutual funds are highly secured in terms of structure. The way it’s designed and regulated by SEBI, it’s almost impossible for investors to lose money due to a scam or AMC going bankrupt. Your mutual fund’s units does not lie with AMC (it just takes the decision of buying and selling). Units and all the money lies with the custodian and highly secure.

Myth #11 – Past returns in mutual funds indicate future returns

Not correct.

While past returns can surely tell you that the fund did very well in the past and there is some probability due to legacy that it will perform well. But it’s not written on stone.

How the fund will perform in future is totally a function of what decisions fund manager takes in future. HDFC Top 200 is a classic example, where the fund who ruled the mutual fund world is now not one of the top 10 funds.

Another example is the SBI Maxgain tax saver which was one of the best ELSS funds some years back but is now replaced by many others.

Here is a study by Yahoo Finance on this topic with respect to funds in the US, which tells that around 92% of top performers do not remain top performers after two years.

Myth #12 – More mutual funds means Diversification

Diversification is an abused word, at least in mutual funds.

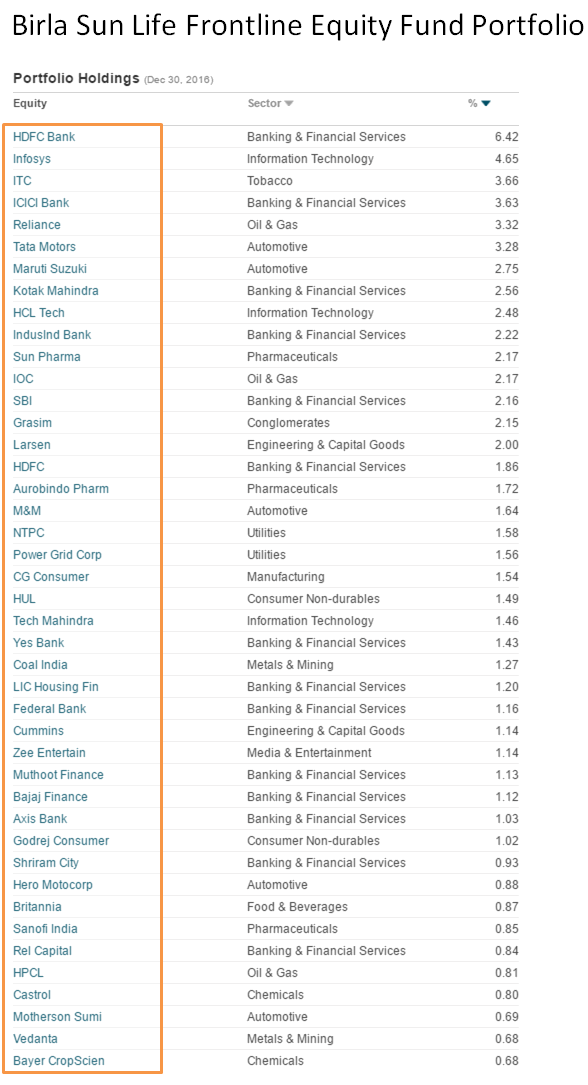

Just because you invest in more mutual funds does not always mean that you have achieved diversification. The reason is simple. A mutual fund invests in close to 50-100 stocks. So when you invest in an equity mutual fund, your money is already well diversified across sectors, types of companies, etc.

When you add another mutual fund, most of the stocks might be the same and also in the same proportion, giving you very little extra diversification. When you add 3rd fund and 4th fund, almost no diversification happens. Below is the portfolio of one mutual fund and you can see how much they have diversified already.

This is one reason why it’s of no use to invest in 10-20 mutual funds of the same category. 2-4 funds of a similar category are the maximum one should invest into. You should add more SIP amount or lump sum in the same fund once you have chosen 2-4 funds.

Myth #13 – I need Demat account to invest in mutual funds

No, it was never the case.

A lot of people think that unless they have a Demat Account, they can’t invest in mutual funds. You can invest in mutual funds from your Demat provider also, but it’s not mandatory.

So when you invest from ICICIDirect or HDFC Securities, you are actually investing via a Demat account and the units you get sit in your Demat account.

So if you want to invest in mutual funds, you can invest directly from the fund house or through an advisor.

Myth #14 – I can start SIP and forget it for long term

A lot of investors think that once they have started a SIP investment or even lump sum investment they can just sit back and relax for next 10-20 yrs. This is not suggested.

Mutual funds need constant review every year. So you should at least keep an eye on your fund performance. Do not overdo it and start looking at weekly and monthly returns, but do that in 1-2 yrs.

Invest in Mutual funds with Jagoinvestor for FREE

[su_button background=”#FF2F3B” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds#sign-up” target=”blank”] Schedule a FREE Call [/su_button]

Myth #15 – You can’t save tax under 80C in mutual funds

Many people who regularly save income tax through PPF or life insurance policies, do not know that even mutual funds have 80C benefits. ELSS or Equity linked saving scheme is the category of mutual funds which gives you 80C benefits up to Rs 1.5 lacs.

Myth #16 – SIP can be done only on a monthly basis

No, An SIP can be done even on a weekly or quarterly basis. While monthly SIP is the most suitable for all (we all get monthly income), but at times if you want to invest on a quarterly basis or weekly basis, even that can be done.

However, note that it depends on a mutual fund if it gives you the facility of weekly/quarterly SIP or not. Most of them do, but at times, some mutual funds might choose to not have that option.

Myth #17 – Mutual funds investments are complicated

While investing in mutual funds is definitely as simple as creating a fixed deposit. But it’s not too complicated. You need to do one-time documentation to start with and once it’s done, After that you can buy/redeem mutual funds online.

One place where you might feel complication is while choosing the funds out of the big pool, but with your own research or with guidance from someone else (like Jagoinvestor), you can get a set of mutual funds to invest in.

Here is a good mutual funds tutorial for beginners by Deepak Shenoy

Myth #18 – I can’t add more lump sum amount in my fund where I do SIP

A lot of investors feel that if they have started a SIP in a fund XYZ, then they can’t add additional money in the same fund under the same folio. It is not true.

When you invest in a fund (either SIP or one time), you get a folio number. This is like an account number. You can anytime add any amount of fund to the same folio. So if you are doing a SIP of Rs 10,000 in Birla Balanced Advantage fund, and now if you want to add another Rs 1,00,000 suddenly, you can do that.

Myth #19 – You need documentation every time you want to invest in mutual funds

Again a big myth.

Once you are done with the first time documentation, after that every time you want to invest and redeem or switch, you can do it online. The documentation comes into picture only when you want to do changes like your email id, phone or address etc.

Myth #20 – Mutual Funds are not for retired investors

This is entirely false.

There are various kind of mutual funds which are suitable for retirement needs. You can invest your hard-earned money in debt funds and keep them secure while it’s growing at a decent return. One can choose an option for a monthly dividend and get an income.

One can also SWP from a fund, and withdraw a fixed amount each month. One can invest in debt-oriented mutual funds, which can have some equity component for some return kick!.

We have helped many clients to plan for their parent’s retirement money deployment.

Myth #21 – I can’t invest in mutual funds because I need high liquidity

Again a myth.

Mutual funds are highly liquid and you can get your money ranging from instant redemption to 3-4 days depending on the fund type. If you want very high liquidity, then you can invest money in liquid funds, from where you can redeem in 24 hours.

Myth #22 – Mutual funds are not that famous among investors

This may be news to many, but the Mutual Fund’s industry will overtake Deposits in Banks very soon (maybe a decade). Right now at the time of writing this article, the money in India mutual funds was around 18 lacs crore, It has doubled in the last 4 yrs, and set to grow very fast in the next decade.

In the US, mutual funds are already several times bigger than Fixed deposits and it’s going to happen in India too over the long term. So if you still think that mutual funds are some alien concept, then you are wrong. It’s very popular now in India and one of the standard investments products.

Myth #23 – Mutual fund redemption needs the permission of a broker or advisor

Your broker or advisor has no control over your mutual funds. You can do redemption on your own by either installing the app of the fund house or through the portal where you have access to.

In the worst case, you can anytime go to the fund house office or CAMS/KARVY office and apply for redemption. This does not need any approval from anyone.

Myth #24 – I can’t skip an SIP payment once started

A lot of people are worried about what will happen if they skip the SIP in a particular month when they are low on funds?

If your bank account does not have sufficient money for a month, then on the SIP date the SIP will not get processed, but from next month it will go fine again. Mutual funds company does not charge any fine or penalty for this, but your bank can levy a small charge for this like Rs 200/300.

I think it’s good, because that way you will be disciplined enough to make sure that your SIP’s go on time, but also does not hurt you too badly in case of emergency

Myth #25 – I should stop my SIP when markets are down

Unless you are an expert in understanding markets and how they will behave (which I think no one knows), it does not make a lot of sense to time your SIP’s. Just let them run in all kinds of markets and focus on your long term goals.

Most of the investors make this mistake that they stop their SIP’s when markets tank. In fact, this is the best time when you should accumulate more Mutual funds units in your portfolio so that when markets are up, you will reap the benefits.

Myth #26 – TDS is applicable when mutual funds are sold and redeemed

Mutual funds are not like Fixed Deposits or Recurring Deposits.

When you sell your mutual funds, there is no TDS which is deducted. You get the full amount in your bank account and then you need to figure out the tax amount and pay it later.

However there is no exception to this. In the case of NRIs, if they redeem their debt funds, then TDS is applicable.

Myth #27 – My money will be locked in mutual funds like other products

Many investors think that in mutual funds their money is locked for a specific period. in case of mutual funds, most of the funds are open-ended funds, which means that you can invest any time and redeem anytime.

There is no lock-in except in ELSS funds (which comes under 80C) and close-ended funds (which specifically tell you the duration for lock-in)

Myth #28 – SIP should not be started when stock markets are very high

Yes, this is actually not a myth, but truth.

But only if you know that stock markets are high. If you are very sure you can figure that out then Yes, it’s better to wait for markets to tank down, and then start SIP. But 95% of the people don’t have time and energy and even expertise to read these signals.

So that’s the reason, why you should not think much when you are starting the SIP. Start your SIP’s irrespective of market conditions. And when markets do down, it’s time to increase your SIP amount

Myth #29 – SIP is always better than Lump sum investments

None of them are better than the other.

SIP’s will outperform the onetime investments in certain conditions and vice versa. SIP’s, however, are more suitable for a common man as it’s a monthly commitment and averages the risk of market volatility.

Here is a good discussion on SIP vs Lumpsum Investments by Monika Halan and Vivek Law in a show called Smart Money

Myth #30 – I can’t switch from one mutual fund to another fund

Many people do not know that it’s possible to move from one fund to another fund across the same fund house. You don’t need to sell the fund, get the money in your account and then again invest in another fund of the same fund house.

So if you have a mutual fund from Birla AMC, you can switch it to another Birla fund without redemption.

Myth #31 – Mutual funds of bigger and trusted brands are always better

Do you know that LIC also has mutual funds business?

However, LIC mutual funds are one of the worst-performing funds across the whole MF industry. LIC mutual funds is not same as LIC insurance.

In the same way, SBI mutual funds should not be confused with SBI bank. A lot of first-time investors in mutual funds investors want to go with trusted brands like LIC, SBI, or HDFC.

Not that mutual funds is a different business, and you need asset management expertise. A small fund house like Motilal Oswal or even Quantum or PPFAS has high-quality funds and should be explored.

Myth #32 – I can’t partially withdraw from mutual funds

Yes, you can. Mutual funds can be redeemed in parts. You just have to choose the number of units you want to redeem or the amount you want to redeem (it will calculate the units required). So that way, it’s a great product. Because in case of deposits it’s either the full amount or none (which is one positive thing also)

Myth #33 – Only humans can invest in mutual funds

Even companies and partnerships can invest in mutual funds. It’s not limited to just humans. So if you are a business owner, you can also go for your business KYC, and then start invest in mutual funds. If you have money lying in current accounts, you can park your excess money in liquid or debt funds and redeem them anytime you want with a single click.

Let us know if you have any more myths or queries related to mutual funds or SIP.

Are you ready to invest in mutual funds?

Are you still waiting to start your mutual fund’s journey? If Yes, then our team at Jagoinvestor can help you start your mutual fund’s journey.

Invest in Mutual funds with Jagoinvestor for FREE

[su_button background=”#FF2F3B” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds#sign-up” target=”blank”] Schedule a FREE Call [/su_button]

We help our clients to set their financial goals, do all the documentation, and give a free portfolio tracker along with mobile apps to check your portfolio.

Here is the real-life story of Umesh, who is one of our long time readers. He agreed to share his life story on how he turned from a successful CA to an Entrepreneur. I am sure it will be an inspiring read for other readers and we all can take some learning’s from his story.

Over to Umesh …

I have been a follower of Jagoinvestor.com for the last few weeks. One post from Manish regarding how he quit his job with Yahoo was catchy and I responded back to him stating that I was happy for him as his story pushed me down the not so distant memory lane of my pursuit to being self-employed.

He has been kind enough to let me share the same with you readers and I hope I can add some value to the time that you will spend in reading the same.

And here it goes

I am a CA with over 25 years of experience. As a child, I had been brought up in the company of CA’s and when I had ceased to be an infant, my father – who is also a CA – joined Air India.

And thanks to his position in the national carrier, from my childhood days, I enjoyed traveling by air, in style and comfort of Maharaja Class… The jumbos of Air India really fascinated me as a child and with each passing year, my interest in them kept on growing. So much so that I decided mentally to become a pilot of one of those 747s.

But I did not become a Pilot

Man’s wish can only progress towards reality when God concurs. In my case, God gifted me with powerful eyes and a nice pair specs and so my dream of becoming an airline pilot is still a dream.

I scored a distinction in SSC and had an alternate desire to become an Aeronautical Engineer – but the burdensome presence of Maths prevented me from opting for that even though I was getting admission. And then, like thousands of others, I joined Commerce and in due course of time the CA blood prevailed over everything else.

I ended up becoming a CA but airplanes and airlines were still part of my hobbies. Even during CA preparations, I used to read airline magazines!

I sent my resume to Singapore Airlines!

So much was the craving that the first CV that I sent was to Singapore Airlines! Knowing very well that it is unlikely that I will get a call. I was not interested in going in for CA practice as I found Taxation and Statutory Audit really taxing. I wanted to do something different – so in that pursuit, I started looking out for a good job or an assignment that I can manage on my own.

I struggled for several months and then my corporate life made a good and healthy beginning. And within a year and a half, I was able to finally enter the airline world on merit and Jet Airways became my third employer and the first in the airline industry. It was a dream come true for me and I simply liked the job.

I never felt that I was working, as airlines and airplanes were my passion and my work was though related to accounting was off-beat when compared to the typical book-keeping type.

I learned a lot in that company and ended up heading its Revenue Accounting unit as a GM at a very young age in comparison to those who were holding that position at the time with decades of experience. I progressed from there and moved on to head the function for 2 other airlines – one in India and one overseas.

I enjoyed the work even with Work Pressure!

Throughout my tenure in the airlines, I was positive and enjoyed the work though the work pressure was enormous, timelines extremely stringent as airlines being in the service industry have to work 24 X 7.

My wife and son and parents have seen me sometimes on the following calendar day but thanks to my passion, I always felt at home.

The best phase of my life was when I was overseas and working for an airline – the work environment was considered to be the toughest within the industry. However, my base was solid and passion too played its role very well and I felt that it was a lot easier than what was perceived.

It was a good exposure in dealing with people from different cultures, countries, and backgrounds. The flow was smooth – but my son was disappointed with the quality of education there and after due pondering, I chose to give his education priority over my professional satisfaction and we returned to India for good.

How I became an Entrepreneur?

By then, I had completed 2 decades in the industry and in my core specialization as well and I decided to do something different and become independent from the clutches of the employers. I had many tempting offers from the industry within India and overseas but I preferred to go the independent way.

My family was with me and backed me solidly – I was in that age frame where if my entrepreneurial attempts fail, I would still have the opportunity to get back with humility to the corporate world. Initially, the going was tough and at times making me wonder if I had taken the right decision.

However, my wife was with and behind me like a rock and I remained committed to getting the first assignment before the bank account reaches alarmingly low.

I got my first assignment

Patience and eternal trust in god always pays and I got my first independent assignment overseas. And all in the house were happy and I was thankful to God for showering his blessings. It lasted for a few months – it was a unique experience as I was the boss of myself and had only the mirror to report to in relation to my work.

It was a great feeling and I still remember the moment when I sent out the first set of FEMA documentation to my bankers to get the inward remittance. Thereafter I have been able to keep the entrepreneurial spirit going with one assignment at a time – though I can manage more than one, I chose to work on my newer passion towards stock markets.

Since the past year, I have again been an active student of stock market and am learning by the day and have been helping a few make money by putting my knowledge to test.

I had my first stint as a trader for 2 years which was full of ups and downs and I had to take a sabbatical from the markets as I got an overseas assignment with my sleep hours slot was the active market hours slot in India.

Once I was back, I invested a significant amount in getting trained by the best in India and have since been working very hard to make this as my next profession – where I do not have to source business as the opportunities come knocking on the doors as long as I ensure that I have capital to take advantage of the opportunities.

From Automobiles to Stock Market!

So in my career so far, I moved from automobiles to IT to airlines to BPOs to TMCs to stock markets – I have learned a lot from the markets – about stocks and related matters and about myself as well.

My ride thus far may seem like an uneventful and seamless but I went through quite a few rough patches and I always remembered the saying – If it were not for the rocks, the stream would have no song and also – Ships are safer in the harbor but they are not meant for the purpose.

In comparison to the present times, my salary was not that high especially after the 9/11 attacks in the US which changed the game altogether. Airlines turned out to be a good place for its vendors and not its employees.

16 habits which helped me become successful

However, I am thankful to some of my habits which helped me reach where I am today.

Few of these are

I always ensured that I am able to pay off any dues immediately on my salary getting credited. Even if the amount was not due, I used to clear it to have surplus identified.

I started investing in Mutual Funds – in NFOs with Dividend Payout Options. Such investments were made on a monthly basis and where there was no NFO in a month, I used to add to my holdings.

I started a couple of SIPs and these ran for 3-5 years one of them was with Dividend Payout Option and one was the Growth Option – this ensured that when the market was up, the value of my investments would also be up.

My father cultivated in me the habit of making sure that I keep making investments in the PPF account that he had opened in my name and then I opened for my wife and son as well and kept depositing whatever possible.

Intermittently, I kept creating FDs – in companies – when the rate used to be 12-15% and in banks and worked hard not to prematurely break them.

I invested in some shares [this was an unprofitable investment though] thanks to the friendly relative sub-broker who was so sure about the scrips recommended by him. I am still an “investor” in those carrying on a burdensome 5% of its original value!

In the last 7-8 years of my corporate life, I started contributing VPF – additional sums as Voluntary Contributions to PF

I had a car loan and 2 home loans – with hard bargaining, I could get a car loan at Zero Interest over a one year period and that helped me save close to 20-22% of the on-road price.

With my above habits and 2 home loan EMIs, I was now having the real pressure to ensure that I do not end up breaking any of my FDs.

Any increase in pay due to revision or change of job was used to either create FDs for home loan EMIs or to part pre-pay the loan.

Sometimes, MFs used to pay handsome dividends and after retaining some for consumption, I used whatever little was left to make ad-hoc loan payments.

Whenever I made an out of turn loan payment, I opted to cut the duration of the loan and not the EMI amount

In the last couple of years of my corporate life, thanks to good revisions in pay, I increased EMI amounts as well which further accelerated the cut in loan term – obviously, the lending banks did not like me as their disciplined customer!

Before I went on my overseas job, I chose to withdraw PF balance and much to the surprise of all, I made a significant part payment of the loans. I am sure many would have wondered if I was in my senses as PF is usually seen as the last resort for a person to touch – to be encashed only when one is retired from the services.

Using up PF for a loan made a happy dent in the loan duration but the end was still far away – but I was feeling a bit relieved.

Out of my final settlement from my last job, I cleared all the home loan dues and began my journey as an Independent Consultant with no hanging commitments.

The above may sound like a well-written script but the journey through these was tough, challenging and at times tense. There are still many who wonder why I am not working with one of the airlines and encashing my experience and knowledge.

I tell them that I am now used to not listening to anyone but my boss in the mirror and he is a tough guy and would not release me.

Should every salaried person become an Entrepreneur?

I have, in the last few years, counseled many regarding several matters, including why one should ultimately work as self-employed – this in no way undermines those who are in service.

Due credit also goes to some of the airlines/entities in India and overseas with whom I was/am associated as they helped me reach the state of Independence. Only those who are born entrepreneurs with no financial burden can start as a self-employed.

People like me and possibly many of you have to toil hard before even thinking of being on our own. Carefully note that since I am on my own, my insurance [car, health, critical illness, travel, term plan, etc.], welfare, administration, travel, infrastructure, capital expenditure, communication and possibly a few more are all on to myself.

Life as self-employed is not rosy!

So, please do not think that life as a self-employed is rosy. I strongly believe in the adage – ”The grass is greener on the other side.”

We have to learn to look at things from a neutral perspective and learn to remain humble, utmost patient and irrevocable trust in God and in our abilities to do the right things.

When we are looking at our future, we need to keep several things in mind – it is not possible to write about all these now, but suffice to say that such decisions have to be thought through and situations 10-15 years from now should also be considered before concluding on a decision.

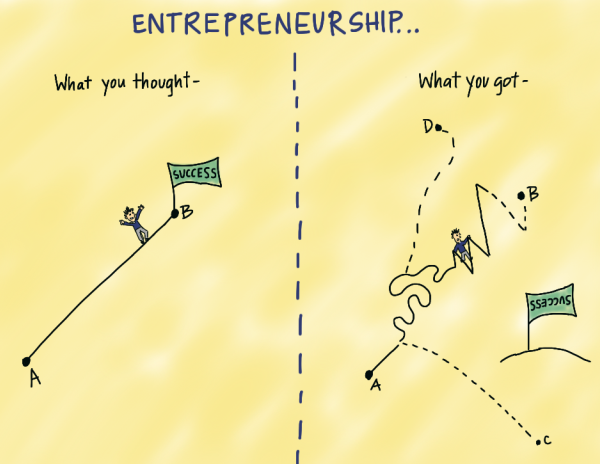

My story is nicely covered by this picture which reflects the dream, the then reality and the present:

I hope my journey and my way of doing things gives the readers some idea about how easy / difficult it is to be self-employed and also financially disciplined. Whether or not you end up being self-employed, please be financially disciplined as money is required by all and the times are going to be tougher as we move along the path of this beautiful life.

Stay Blessed and financially safe!

Warm regards,

Umesh

Conclusion from Jagoinvestor

I think it was a fantastic life sharing and there were many lessons which can give you a great insight into decision making. It’s always a great thing to read someone else story, you get lots of inspiration and see how other people handled some situation. You get an idea of how things look like on the other side, you read about their struggles, achievements and eventually add the learning’s in your life.

I thank Mr. Umesh for this contribution and wish him the best of luck!

If you feel that you can also contribute to this blog (it can be an article, life sharing, valuable info), just get in touch with me using this form

Yesterday I went to watch a movie late night at Amanora town center in Pune. I and my wife had our dinner at a small Italian restaurant and the food there was quite good.

When it was time to pay the bill, I went to the counter and paid the bill. When I got the bill in my hand, I realized that there is a problem. They had charged me a “service tax”. However, the main issue was that there was no service tax number mentioned on the bill.

Charging Service Tax without Service tax number is Illegal

Yes, you heard it right.

The Bill copy did not have any service tax number mentioned on it, but the restaurant had put a service tax charge on the bill. This is Illegal and can’t be done. Hence I told the staff that I can’t pay that service tax unless they give me the service tax number.

The staff, as usual, was ignorant about this and told me that I should talk to “owner” and tried to give me his number. However I told them, it’s not what I will deal with and I will not leave unless they give me service tax number because they are illegally charging service tax.

Finally, after 5 minutes, the staff told me that the Owner is not reachable and they will give me a service tax number later. But I refused to budge and demanded them to pay me service tax amount back and not repeat this, as its illegal.

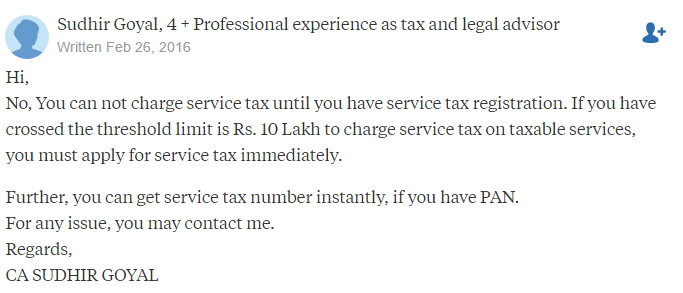

Finally, they had to refund me back and I took the money. Here is what another CA has to say about this on Quora

I realized that not more than 1 out of 1000 people know this rule, and this needs to be spread among people. Many restaurants are misusing the fact that now people know that service tax is an unavoidable tax and has to be paid, however many do not know the rules and conditions under which any business can charge it. Even Service charge is now an optional thing and you decline to pay it.

Note that many restaurants will tell you that they have applied for the service tax number and are awaiting it, but this is mostly a trick to fool you and to save themselves out of the situation and embarrassment. However even in that case, it’s not right, and you should demand to see the proof for that.

The service tax number is mandatory to charge Service Tax

As per service tax rules, service tax can be charged only if you applied and got your service tax number. This service tax number has to be written on the invoice copy. Without that, you cannot charge service tax from your customers.

In the case of restaurants, the service tax has to be charged only on 40% of the FOOD bill and beverages. So if you eat for Rs 1,000 (food + beverages), then only 6% on the total bill is to be charged, which will be Rs 1060.

Here is a sample of a correct bill that mentions the service tax number on the bill itself.

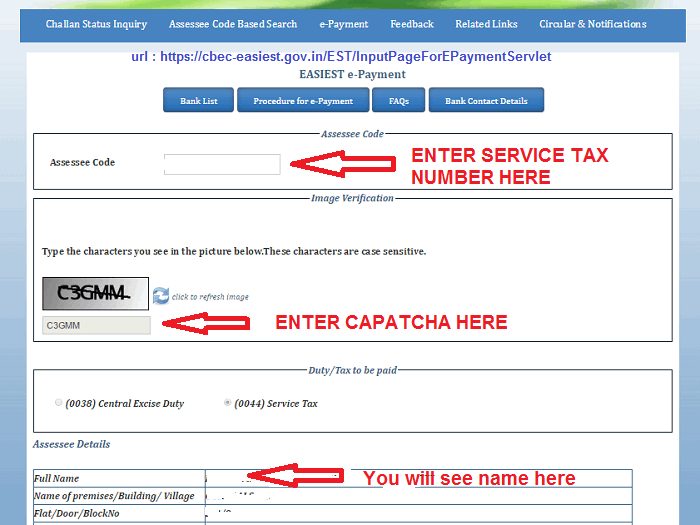

How to verify whether the service tax number is valid or fake?

Few people ask me, how to verify that the service tax number mentioned on the bill is not fake? Because the hotel guy can just randomly put some number, which looks like the service tax number.

The simple solution is to check the name of the person/company under whose name the service tax number is registered. It just take 1 min to verify that.

Step 2: Enter the 15 digit Service tax code (also called Assessee code)

Step 3: Enter the captcha

Once you do this, the page will show you the

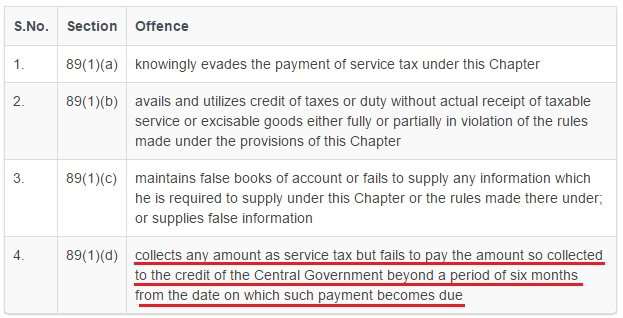

Non Bailable Offence under sec 89 of service tax

If service tax is charged without a service tax number, then how will it be paid to the government? Because you need the service tax number to pay the tax to govt. Sec 89 of finance Act tells that incase an offense is done like this, then the person can be jailed for up to 1 yrs (and up to 2-3 yrs in case the amount involved is above Rs 50 lacs).

Below is a snapshot is taken from Taxguru website which writes about tax-related topics.

Do you need to pay a service tax if you don’t sit in AC?

This is very interesting.

One of the biggest questions people raise is that if a restaurant has AC in one part, but not in other parts and if you are seating in a non-AC section and dined, still do you have to pay the service tax?

Or imagine is AC was not working at that time, even then will you be charged the service tax?

The answer to that is YES.

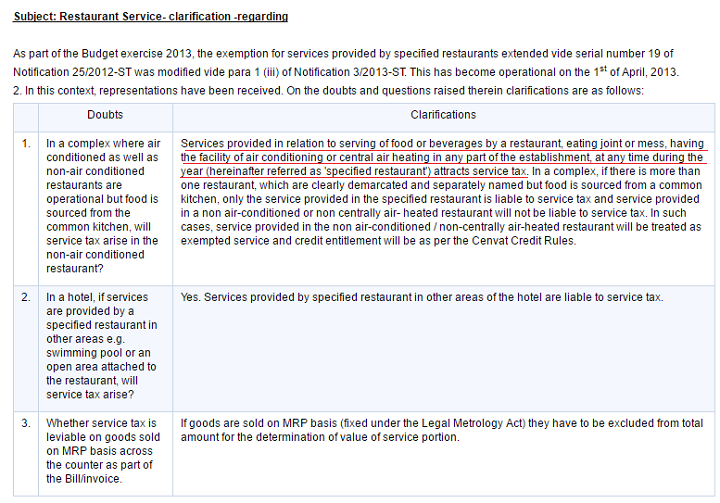

Sorry, but the service tax rules clearly state that. The service tax rules simply say that if the establishment (the hotel or restaurant) has the facility of air conditioning or central air-heating in any part of the establishment, then they have to charge the service tax in their bill.

It does not matter if you got the benefit of the AC at the time of eating. All that matters is that they have AC anywhere on the premises.

This itself is enough for a restaurant to charge the service tax. However, if an establishment is divided into two parts with the two different names and entities, then the non-ac part can’t charge the service tax (where the service was given), even if the food was prepared in the AC part. Here are the exact wordings from the service tax notification on this issue

3 things to remember when you visit a restaurant next time

When you visit the restaurant next time, make sure you keep in mind the following 3 points.

Check if service tax number is mentioned on the bill or not, if they are charging service tax on the bill

Make sure the service tax is charged @6% on the food + non-alcoholic bill and 15% on the alcoholic charges

Make sure there is AC in the restaurant if you are charged service tax.

Spread this Information

There are thousands of restaurants that might be charging service tax illegally without having a service tax number and millions of customers on a daily basis are paying that as they are not aware of the exact rule. This is practiced by many restaurants, small hotels, and many other businesses.

So spread and share this article as much as you can so that more and more people can know about this. Also, share your experience with this.

Do you know that every person is entitled to 1 free credit report and score each year from each of the credit bureaus in India? There is 4 credit bureau in India which are CIBIL, Experian, Equifax and Highmark.

As per RBI guidelines, now each of them have to provide one free report each year. For those of you who do not know, a credit report is a document that has all your past loan repayment history and a score that tells a lender if you should be given any loan or not.

So each lender checks these reports and scores as part of their loan approval process. It’s very important for investors to keep track of their credit scores from time to time.

Step by Step Process to Check FREE Score online

So today I am going to share the process of getting the free report and score online from each CIBIL Transunion, Experian, Equifax, and Highmark credit bureau. I have personally checked my own score + report from each credit bureau and I will teach you the step by step process of how you can do it too. The whole process is online and you do not have to fill any form by hand or send any documents anywhere.

Note that your credit report will be available only if you have taken some kind of loan or credit card. So if you do not have any kind of loan, you will most probably not have it, unless someone has misused your documents and applied for some loan.

So let’s start with CIBIL first.

How to check the FREE CIBIL report and Score?

In order to check your free CIBIL Transunion report and score, you need to follow below steps –

Enter your current details like Identity Details, Contact details etc and continue to step 2

Confirm your email on next page, and then go to your email to click on a link inside for email verification

On the page, enter your voucher number and move ahead

You will then be asked for some verification questions related to your debt.

Once you answer them correctly, you will be taken to your free report

How to Check FREE Equifax Credit Report and Score?

Here are the steps to check your free Equifax report and score

Download the Equifax India mobile app (android or iOS)

Register your email and get temporary PIN number

Enter a temporary PIN and reset a new PIN and then log in to the App

Enter your Name, Phone, Date of Birth and Adhaar Card

An OTP will come to your phone number which is linked to adhaar card

After OTP verification, your KYC check will be complete

On the app, click on the link “Credit Report”

On the page, click on the link “Request Free Credit Report”

Enter all your details and then click on Submit

Now your “Knowledge-based Assessment” will be in the pending stage.

After 24 hours, your knowledge-based assessment will get generated.

Click on the app, and click on the link which says “Knowledge-based assessment”

Give correct answers to the questions asked, after which your credit report will be in the “Initiated” stage

After 24-48 hours, you will get an email with the free credit report as an attachment

Download the attachment and have a look at your report and score.

You can also login to the app and check your report there

For those, who do not have mobile linked with adhaar, they can send their KYC documents along with a filled form to Equifax customer care, and on verification, they will get their free report in 48 hours

How to Check FREE Highmark Credit Report and Score?

Here are the steps to check your free Highmark credit report

Go to https://cir.crifhighmark.com

Register as a new user and set your new password

Activate your account by clicking on the link inside the email

Again login and choose an option to get a free report on the top of the page

Enter all your details and click submit

You will get a notification that inquiry was successful and now wait for the email

After a few hours, you will get an authentication email

Click on the link and verify some of the information asked on the page

On successful verification, you will get an email with PDF attachment after 48 hours

Open you free Highmark report and check it

I hope the above videos must have given a good clarity on what needs to be done to check your report online, totally free of cost.

Why you should check your report every year?

A credit report is fast becoming a very integral part of the credit system in India from the last few years (it’s already is). It’s highly recommended to have a clean record and a fairly good credit score if you don’t want to get rejected for your future loan applications.

Now with one free report from every credit bureau, everyone should check theirs from each company and make sure that all the credit remakes and details like name, age, score, and other details are correct. If you find any problems, immediately raise a dispute with the lender and the credit bureau and start fixing it.

PRO Tip – Subscribe to each report with the gap of 90 days

Don’t subscribe all 4 reports at the same time. Time them one per quarter so you can monitor your credit report for any frauds frequently instead of once every year.

So the point is that if you divide your free reports checks every 90 days, you will be able to find out if there were any frauds happening throughout the whole year. However, if you just apply for all the reports in a single month, then you will be able to apply them only next year.

Let me know if you face any issues while checking your free report

Do you take all your decisions based on facts or emotions? Be it personal or financial life, it’s a well-known fact that 95% of our decision are based on emotions.