We are happy to announce, that our next full-day workshop in Bangalore is scheduled for 16th Sept 2018 (Sunday).

We invite you to come and participate with your friends and family. It is an opportunity for you to block one full day for your financial life where you get a chance to work on your financial life. We do not teach tricks and tips to build wealth, but in fact we help you to discover your own personal process of creating wealth.

Why we do these kinds of offline event/workshops?

We do these events because they make a positive difference in people’s financial life. The conversations we do, create an impact on people’s thinking and they are able to re-invent themselves as an investor. The event is not about financial products and numbers, it is about learning and mastering the principles of wealth creation. It is about learning realizing your past mistakes and about creating a powerful future for yourself.

Register for Bangalore workshop on 16th Sept 2018 (SUNDAY)

Ticket Type

Pricing

Ticket Link

Single Ticket (Early Bird)

(First 10 tickets only)

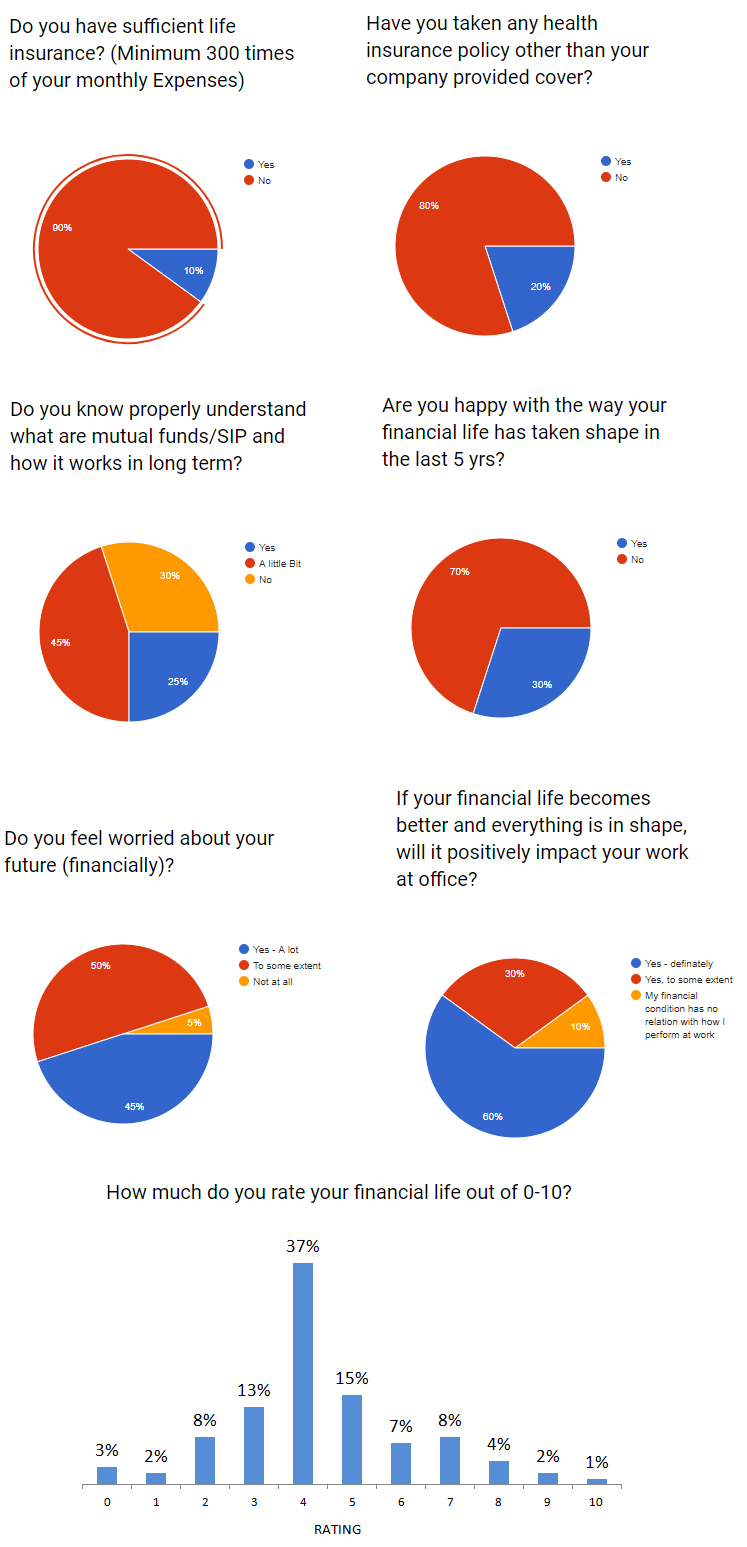

Let us share our survey findings (Survey was done on 10000+ Investors)

We did a survey with more than 10,000 investors some time back and here are the results of the survey.

The survey is LOUD and CLEAR – It’s time to re-invent

The theme of our workshop is going to be re-invention, you will get a chance to examine your financial life and will explore ways to re-invent your financial future.

The results from survey seem alarming and the best gift we can to the investor’s community is our workshop Your real wealth is your clear mind as once the mind is clear all the good decisions will happen on its own, the workshop will leave you with a clear mind and with new openings of action.

Our Vision to do Workshop in different cities and organizations

This year we intend to do the workshop in maximum cities and in more and more organizations. The content and design of workshop are powerful and we want the workshop conversation to touch more lives. If you want to do a workshop in your city or in your organization you can share your details in the below Google form, we will get in touch with you at the earliest.

It’s time to add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and each time it has been a very fulfilling experience for us. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation.

This time we want more and more couples to participate so that they can get on the same page when it comes to personal finance. It is extremely important that the husband and wife both take an equal interest when it comes to money management. We are offering a special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct is highly interactive, it has lots of activities and fun exercises which help you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short, there is something for everyone in this workshop.

If you have never participated in any personal finance workshop let this one be your first experience. If you have any questions you can write in the comments section or you can email on [email protected]

A few days back, I was sitting with financial planning in our Pune Office and we did a very detailed discussion on his financial life. We looked at various parameters and did basic number-crunching which gave a deeper understanding to this client about financial status.

The first step was to record all his financial details in one place and that exercise alone took more than 40 min because it’s a task in itself to just bring all the financial details in one place.

For the next 2 hours, the husband and wife were totally into discussing some of the aspects of their financial life which they had never thought of or never dealt in detail. It was a wonderful experience in itself.

2000+ Families have gone through the process

My team has done this same exercise with more than 2,000 families to date across the world (Indian residents and NRI’s). Most of these discussions have happened online and few of them have happened face to face. But overall, what matters is the interest and dedication of the client and not the medium of communication.

While we were doing this exercise with the client, I thought that there are many things which are so common among the clients we deal with. I can see a lot of things which get repeated all the time and there is a pattern with the majority of the cases.

So I thought why not share some of common observations and I made a list of 10 points which is true for almost 80-90% of the clients we have dealt till now.

These 10 points will give you a good idea of how a typical financial planning case looks like and you can also check if these points are true for you or not.

Let me put these points now one by one.

1. No idea of their exact expenses

One thing which is most common is that most of the people do not have much idea of their own expenses and how much they are spending in different categories. Now you will feel – “How is it possible, that a person does not know their own expenses?”

The point is that most of the people have a very vague idea of how much they are spending on various categories because most of the people do not note down and follow a stringent budget. People have a high-level idea for everything, but once they put down all the numbers – They get surprised on their own expenses and feel like – “Ohh .. I spend so much!!, Never realized that”

2. The legacy of LIC policies

Almost everyone who comes to us for financial planning always has 2-3 LIC policies which were taken long back for tax saving purpose. If not for tax saving purposes, it was bought by their parents and they are now continuing it and paying the premium.

They have a high-level idea of the Sum Assured and when it’s maturing and hardly a few people recall the exact policy name.

3. People are Surprised

When we do the detailed analysis and show where they stand in their financial life (backed by data and proper reasoning), most of the people are surprised on how bad or how good they are doing.

Mostly we all are so consumed in our life that we never realize the status of our finances. We have a very fuzzy understanding if things are going bad or good.

Some of the people realize that they are worrying too much, where as they are well placed and are on right track (very few people are like that) and majority of people realize after meeting us that they have underestimated how bad they are in their financial life and its HIGH time they need to quickly take action.

4. Confused on how much they would need to retire today

When we discuss their retirement planning, almost everyone fails to reach a number which will be enough for them to retire today.

Just think about it.

If I ask you today that assume you retire today and you have to spend another 30-40 yrs of your life without any debt or EMI burden and no commitment like children related expenses. Assume you are 60 yr old today, and now need a big amount to live your life till you die, how much money would you need?

Just think about this for yourself and you will realize that it’s a tough question to answer. Will it be Rs 2 crore? 5 crore? 10 crore?

5. No clear Financial Goals in life

Most of the investors we see are mostly living in present and dealing with financial goals as and when they arrive. They know they would need “lots of money” in the future. But almost no one has properly planned for their financial goals.

One of the couples we met recently wanted to plan for their kid’s related goals. The wife was clear that the education was the biggest goal, but the husband was confused if they should also plan for the Marriage goal or not.

6. Decisions are taken based on “Instant Gratification”

We see that almost everyone has taken lots of decision-based on “instant gratification” or “the short term benefit” . Someone called from the bank and said they will save tax on a product, and they buy it.

The gold prices were rising and it “felt” right decision at that moment, so they bought lots of gold and not from the last 4 yrs gold has given a 0% return.

Like this, we see that decision is not carefully thought of with all pros and cons, but rather a very narrow approach.

7. “I could have done much much better” – The feeling of Regret

Every 1 out of 2 people we dealt with told us that they regret what they have done with their finances in the past and they wish if they could have done things differently.

More than doing “right things” , these people have done many “wrong things” and that has a higher impact (in a negative sense) in their financial lives.

8. The biggest part of Net worth is the House on loan

Almost always the house was the biggest part of the net worth, not the mutual funds, or stocks or fixed deposits .. I think it’s because we mostly deal with middle class or upper-middle-class salaried investors and the house is generally there in the portfolio.

Almost everyone had a big home loan.

9. Too many financial products

Another common issue which we see in most of the cases is that they have too many financial products. Many Fixed Deposits, many LIC policies, too many mutual funds (if any), various policies.

These people are more of product collectors who have added something new in their financial life each year when the tax season comes or whenever they had surplus money.

This is one reason that their financial lives get very complex.

10. Unable to meet Financial goals with current resources

When we check if these investors will be able to achieve their financial goals or not. We find that most of the people are not going to reach their goals easily .. and in some cases, they are seriously short of money and are in very bad shape.

It’s like a disaster waiting to happen. Investors are already in the age range of 40-45 yrs. They have some portfolio, but looking at their financial goals, it feels like they will be able to reach just 30-40% of it ..

We are happy to announce, our next full-day workshop in Mumbai is scheduled on 22nd July 2018 (Sunday). Generally, we give 30-35 days for people to register but this time the gap is less and so check your schedule at the earliest and book your seat.

The workshop is an opportunity for investors to work on their financial life. We will share all that we have learned about personal finance with all participants. The workshop is only for the action takers and it will start the moment you will register.

Register for Mumbai workshop on 22nd May 2018 (SUNDAY)

Ticket Type

Pricing

Ticket Link

Single Ticket (Early Bird)

(First 10 tickets only)

How do you know if the workshop is meant for people like you? Put your hand on your heart and get honest with yourself. Read the following points and see if these points are true for you.

If you find personal finance boring (like my wife)

If you convince others and yourself that personal finance is not your cup of tea

You hate numbers and are a big-time avoider when it comes to money management

You are PhD when it comes to procrastination

You want to get into action but you don’t know from where to start

You are confused with what to do and what not to do because of the overall bombardment of information on the name of investor education

You really want to move beyond planning and want to learn how to design your financial life.

You want to make 2018 your BEST FINANCIAL YEAR

The New Structure of the workshop

Step 1 : Book your Seat – The first step is to book your seat by paying the fees

Step 2: Financial Health checkup – Once you register, a certified planner will give you a welcome call and start the detailed financial health checkup with you

Step 3: Participate in Full Day workshop – After the financial health checkup you will be more clear on where you stand in your financial life. Its time to attend our full day workshop

Step 4: Get 2 Financial counseling calls – Finally after the workshop, you get personalized attention from us and you get 2 financial counselling calls to make sure you complete your pending important financial life actions.

Last Pune workshop experience

We had a total of 93 participants in our last Pune workshop (it was held on 20th May 2018) and the experience was amazing. We got an opportunity to learn and share with investors and clients from Pune. Our entire team travelled from Ahmedabad to be a part of the event.

We all had one intention, helping participants in creating an awesome financial life forwarding them in taking actions in their financial life. All the participants were able to identify 5 core actions in their financial life and we as a team helped them in completing those actions.

Why the workshop is now more action-oriented?

It is because the only ACTION produces wealth. We started with a day workshop but now after working with a

few hundred investors we realized that the one-day event needs something more to it. Our intention is not to get a fee from investors, we want their full commitment and we want them to produce some amazing results in their financial life.

The workshop is strictly for investors and not for advisors or finance professionals. If any advisor/IFA/CFP is found to be registering for the workshop, he/she will not be allowed to participate.

If you have never participated in any personal finance workshop let this one be your first experience. If you have any questions you can write in the comments section or you can email on [email protected]

We are happy to announce, that our next full-day workshop in Pune is scheduled on 20th May 2018 (Sunday).

We invite you to come and participate with your friends and family. It is an opportunity for you to block one full day for your financial life where you get a chance to work on your financial life. We do not teach tricks and tips to build wealth, but in fact we help you to discover your own personal process of creating wealth.

Why we do these kinds of offline event/workshops?

We do these events because they make a positive difference in people’s financial life. The conversations we do, create an impact on people’s thinking and they are able to re-invent themselves as an investor. The event is not about financial products and numbers, it is about learning and mastering the principles of wealth creation. It is about learning realizing your past mistakes and about creating a powerful future for yourself.

Register for Pune workshop on 20th May 2018 (SUNDAY)

Ticket Type

Pricing

Ticket Link

Single Ticket (Early Bird)

(First 10 tickets only)

We have also created a facebook event for this workshop. Do click on Interested if you want to join it.

Why should you come to the workshop?

You will learn how to improve your financial life with your current set of resources and income.

You will learn how to plan for your financial life goals

You will interact and learn from other’s people’s financial life

You will dedicate one full day to get better with money management

You will learn to add new dimensions to your financial life

To understand that personal finance can also be fun

To give a whole new direction to your financial life

Let us share our survey findings (Survey was done on 10000+ Investors)

We did a survey with more than 10,000 investors some time back and here are the results of the survey.

The survey is LOUD and CLEAR – It’s time to re-invent

The theme of our workshop is going to be re-invention, you will get a chance to examine your financial life and will explore ways to re-invent your financial future.

The results from survey seem alarming and the best gift we can to the investor’s community is our workshop Your real wealth is your clear mind as once the mind is clear all the good decisions will happen on its own, the workshop will leave you with a clear mind and with new openings of action.

Our Vision to do Workshop in different cities and organizations

This year we intend to do the workshop in maximum cities and in more and more organizations. The content and design of workshop are powerful and we want the workshop conversation to touch more lives. If you want to do a workshop in your city or in your organization you can share your details in the below Google form, we will get in touch with you at the earliest.

It’s time to add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and each time it has been a very fulfilling experience for us. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation.

This time we want more and more couples to participate so that they can get on the same page when it comes to personal finance. It is extremely important that the husband and wife both take an equal interest when it comes to money management. We are offering a special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct is highly interactive, it has lots of activities and fun exercises that help you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short, there is something for everyone in this workshop.

Super Bonus Launch of Finscore Tool

We will be launching our newly designed scoring system with all our workshop participants. The scoring system is going to be a game-changer for many investors. It has taken around 6-7 years for us to design the whole system and we are all set to raise the curtain. We are so happy to share our scoring system with the investor’s community, it is simple, easy and extremely powerful in nature. It is more like a technology to live a good financial life.

After the workshop, participants can sign-up for our paid service to get complete access to the tool. We will give free financial health check-up access to all participants so that they can check up their scores.

The workshop is strictly for investors and not for advisors or finance professionals. If any advisor/IFA/CFP is found to be registering for the workshop, he/she will not be allowed to participate.

If you have never participated in any personal finance workshop let this one be your first experience. If you have any questions you can write in the comments section or you can email on [email protected]

So I was talking to this reader and came to know that her husband’s investments are done by his father. I was curious to know the reason of this and to my surprise, the biggest reason that came up was that he (the husband) has no interest in Investments and personal finance and hence he has outsourced this decision-making part to his Father!

So this guy’s father does all his mutual funds, LIC policies, PPF and other tax saving instruments, apart from that he does his non-tax saving part too. He has bought some Child ULIP’s to “secure” his grand children’s future.

Let us see this serious disease which is killing our country slowly .

Problems Which can arise due to “Papa Kehte Hain” kind of situation

Unsuitable Psychology : As we discussed earlier, today’s world needs better way of handling investing decisions and a better psychology, A person has to be more updated these days than what our Fathers were in their days. So today’s father generally do not handle money in right way as it should be because of lack of knowledge and a different attitude.

No Idea of Investments and documents : You may also not be aware of where your parents are investing your money ! They might not tell you about it or they may forget to tell you where the documents are kept, when is the maturity of some products and issue like these which look small but can become very major when some bad things happens.

No Self-dependency and hence lack of knowledge: It might look rude but believe me, your parents will go some day and all of it is going to come at you some day and not knowing a lot of things that time will be a horrible situation. You don’t know how to invest, where to invest, you not knowing the rules of investing, you don’t know where you took insurance from, when is it maturing, etc,etc. It’s like starting all over again. It can be painful, you are always dependent on your parents then. Its a bad thing.

An Important question you have to ask

In today’s world most of the fathers and Uncles have no idea how to take investing decisions. It’s a new and different world now compared to their days. They have not much idea of how things should happen in today’s world.

Our fathers, grandfathers and Uncles have come from a very different time when there were no choices other than LIC polices and FD’s. The education was cheap, every one’s desires were limited and people were happy with their limited environment.

Things have changed today and now we are in a different world which has added pressure, high expectations from life, Education needs lacs today, the costliest one is for the kids these days, forget adults :). People are eating out more, people are spending more, want more (not need more) and to achieve all that we need to grow our more smartly.

Buying simple FD’s and Endowment policies will Kill you some days without letting you know.

“Most Parents today do not understand how to take investing decisions in today’s world and environment. Trusting them with this skill can be very costly in today’s world. There is no harm in evaluating if they should take it in their hand or not. Be bold!!

Why are you letting your Father take the decisions? What’s the reason for it? Is it respect and just because he is the oldest one you know in your family and he has seen more life than you? Do you think it makes him more better investor and decision taker than you or some one else? It’s not right!!

May be he is totally not suitable, Respect and “experience” is fine, but you can’t just let them take decisions just on these two criteria. It’s dangerous.

Counter Scenario

On the other hand, we have Father or elderly relatives who are really good, they are experts in field of direct stock investing. Understanding financial planning and have good experience of investing with today’s environment, it’s always advisable to take their help or at least the guidance in many cases.

At the end you have to decide if your parents are the right one’s to take decisions for your money or not? It’s a personal evaluation to be done.

Has this Happened to you? Do you know of any one who is facing similar issues? Please share your views and personal experiences.

Today we are sharing a very different money story, where one of our readers is going to share his life journey of becoming a middle class from being RICH years back. Yes – you heard it right.

As per his request, we are not revealing his name and identity. I thank him to share his story with a bigger audience.

Here it goes…

My story starts with an assumption that most of the jagoinvestor readers belong to a middle-class background or from a humble background. Most of the readers have either already moved to a level higher or are trying to move to a level of lifestyle better than what was available to them in their childhood.

My story is a complete reversal

Yes, I moved from affluent background to a mid-income kind of family (from a big city perspective and not on pan India basis)

My story is a lesson on why financial planning and diversification are important. I was born in a rich business family of a small town (population of 1 lac), my father was a well known and socially connected/respected person in society.

I still remember we used to have a car (when there were only two or three cards in the whole town), BSNL landline with a two-digit number (i.e. less than 100 connections in the whole town!). Money was the last thing to worry about in our family. Things were very smooth in my childhood, and we used to discuss how to take the next leap towards the ultra-rich families.

There was more than sufficient money, my family used to give donations to temples, hospitals, etc. I had an elder brother (1 year) and I never wore his used clothes, never used his books (same school), and never used his toys.

How we lost money

Unfortunately such was the turn of time that the business suffered three-four very bad years, which eroded the entire family wealth.

This coupled with the lavish wedding of my sister left almost nothing for us two brothers. My brother decided to join the business and I was banished to a poor software job 7 yrs back. I initially faced a lot of troubles, but gradually managed to come out of the situation and did an MBA and now I am doing well. Even the family business is doing great under my brother’s leadership.

It still gives me a nightmare, that we had a substantial loss in the family business. Probably I would have never discovered blogs like jagoinvestor and subramoney had that loss not occurred. The virtues of financial planning were learned at a great cost.

Did it impact our social life?

Not much…

One very good (some may consider it wrong) thing which my father did even when business was downhill, he never cribbed in front of society. He never let the lifestyle go down.

So society never knew that the problem is so deep. When my brother joined the business, the total net worth of our business excluding the house and gold was just ~20 lacs (We lost 96% of business value, down from 5-6 crores in real terms. note that this was many many years back) with two marriage and my MBA still pending. But still he was able to conduct business by borrowing (unsecured) and credit, only because our credit rating in the society was still AAA.

Had the society knew about this, we would be ostracized. Luckily my brother turned around the business and things became much better going ahead.

My childhood and money

My first good experience with money was when I got pocket money from my grandfather. I used to get 1 rupee a day and my brother 2 rupee, and we used to get candies from the shop. The pocket money gradually increased to Rs 30 rupee a week on Sunday, and we used to feel like Tata/Ambani on that day.

Not even a single incident I remember, when my parents refusing to give me money. Even during the bad days they maintained the lifestyle, paid for my college, held lavish wedding for my sister. I as an individual was not a spendthrift and that helped a lot.

I was educated in the best school in the nearby city, but education was just a formality since the ultimate goal was to join business. But very early in life, being from a business family, we were introduced to the importance of money very early.

My lifestyle NOW vs. THEN

Although financially I am comfortable now, there is no more that kind of luxury in my life. I am very frugal now. Here are some points which can give you all an insight into how my life has changed.

I live in a rented 1-bed room flat in Mumbai.

Consciously own no car and live a frugal lifestyle.

Earlier the minimum we traveled was 2AC, now the maximum I travel is 3AC

I avoid overseas holidays which my colleagues frequent

Although I do not complain, I wish I should have more wealth. I have done full financial planning (and also my family’s) with the help of blogs like Jagoinvestor.

Since I cannot afford the mistake which my family had done, I am completely opposite to them.

And I am seeing the good result to my net worth, with 5-7 years of job and though my salary is not high, my net worth is high. The only reason is being frugal and financial planning, avoiding toxic products like LIC policies etc. I have never touched ULIPS, endowments, FD ever in my life (totally my views)

How important is Money in life – My views!

Money is very important, as important as health. The emotional trauma of not having enough money is unbearable. When I was young money was always there and I thought it would always be there in abundance. I just have to graduate and join the business, but life had other plans for me.

After the tragic losses in business, we decided as a family that one of the brothers should find a stable job; while others will try to revive the business (which is now revived by God’s grace). All the while, I never felt the urge to study since the ultimate destination of father’s business required no qualification; I suddenly was required to study and find a decent job.

So I pulled up my socks and did engineering and MBA and landed a good job in the financial sector now.

I fantasize regaining old glory days and become a wealthy person, and I believe courtesy the financial education I may or may not live rich but I am sure I will die rich. I think if I can accumulate 5 crores (in today’s terms), it will make me feel that my future is secured.

Stupid mistakes people do in area of money

Everyone has their own way of looking at things, but having seen a lot of money in life, I think a few mistakes people do are

Mistake #1 – No financial planning, just random investing

Most of the people just randomly invest in some policies or open few FD’s without any concrete planning for future. They think life will continue in the same way like last 5-10 yrs. But life can have lots of surprises at times. One should always be 2 steps ahead and plan for their bad times. Start doing your financial planning. If you are not smart enough to do it yourself, accept it and hire a professional.

Mistake #2 – Invest/consume gold/jewellery

Do not see gold and jewelry as investments. Some of it should be just used for personal consumption, but nothing more than that. Try to invest your money in robust financial products which create wealth for you over long term.

Mistake #3 – Invest in fixed deposit

Fixed Deposits are not for investments, It’s to just park your money for 1-2 yrs and nothing more than that. If you want to create wealth, fixed deposits are not the best thing in today’s world. By the way, I am yet to meet someone who has become a millionaire by putting money in FD’s , unless you put millions in FD!.

Mistake #4 – Invest in property without proper due diligence

I can’t understand, how people invest their hard earned money in real estate without proper due diligence. There are enough cases where lakhs and crores are stuck in bad deals and people have just lost money. If its real estate, catch a lawyer, pay his professional fees and check things in detail before committing your money.

Mistake #5 – Same with stocks

It is just beyond my understanding that people think they can do stock investing and trading successfully for years and generate consistent profits. If it was so easy, everyone would be doing that by now. Leave things to professional and don’t do stock trading (unless you are really a pro and into it full time)

My father suffered from Mistake # 1. There was no financial planning done at that point in time. Most of the money was either plowed back in business or invested in PPF.

There was a belief that business would always be very good, so no land was bought and no equity investments were made. Some PPF investments were done for tax planning. Even my mother didn’t buy gold.

Such was the belief in business that no investment was made for a kid’s future education and marriage. Two-three big losses and there were no backup assets. So diversification is very important, never put all your eggs in one basket.

I also lost Rs 10 lacs recently!

I would also like to share one incident from my life where I lost money personally and learned an important lesson.

As I come from a business background, I wanted to get into some kind of business. But, I recently lost around 10 lacs in a business I started in partnership with my friend. A business plan was good but somehow it did not work out as per the plans. I learned an important lesson that “Slow and steady wins the race”.

Had I kept the money in my equity Mutual funds, they would have yielded good returns, but that’s fine. You learn from your mistakes. I took a calculated risk, hence the impact on me was less.

Don’t be afraid of making mistakes especially when you are young and have lots of time in your hand in the future.

One suggestion for your future

Manish asked me if I can share one insight I want to share with every one of you out of my years of experience and from my life.

So here it goes…

One should always have a plan B in life, like what will I do if tomorrow my company kicks me out, I have plans like starting a business, someone in IT may be looking at re-skilling or someone can survive on rent/dividend, etc.

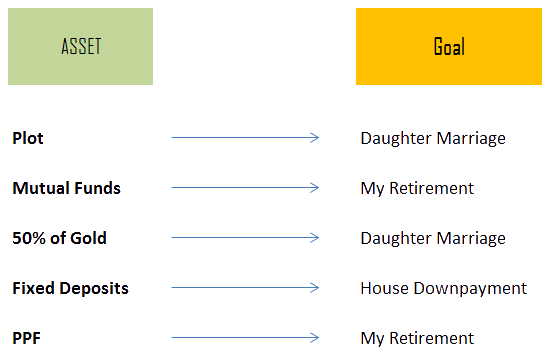

There should be a little basket for every goal, as a plot of land for my daughter’s marriage which I will not touch, in my case, we thought that the running money in the business would be sufficient enough to meet all kinds of expenses or emergencies.

All this is a part of financial planning, so even if you are very talented today and earning much more than you require for your expense, you may feel that financial planning is for the poor or middle class, but that thought is not right. In fact when the going is good; that’s the best time to amass assets.

A real-life example of my friend family

One of my father’s friends with a similar profile, good business which subsequently went bust had a lot of good shares like HUL, SBI at IPO pricing (imagine HUL @10 INR) and he never sold. Can you believe he gifted AUDI to his daughter only from the wealth created by equities (he showed us the Demat slip the day he sold shares)?

If you are low in wealth right now, then I have just 2 things to say

Be Frugal, don’t copy your friends and cousins and overspend

Try to increase your income, learn some extra skills, work overtime, etc…

Is your happiness linked with money?

Yes, For me it is linked; in the sense that I should be able to provide. There should always be enough money to support the family, health, education, retirement.

One should not ignore the value of good health, relationships, and friends. Even if one has all the money and there is no health or family to enjoy, then what is the use of all the wealth in this world? Given a choice, I will choose the later over money.

I feel very good after writing my story. Jagoinvester is providing a very good platform to share your life story. Even if few of the readers can take away a few lessons I will feel that the effort is worth.

What is your money story?

If you want to write your money story, Leave your details here and Jagoinvestor team will get in touch with you with the next actions.

What do you think about my money story? Did you enjoy it? Can you share your views about money and how it changed over the years?

Today you are going to read “money story” of Priyanka Jadhao from Pune. She is 26 yrs of age and just started her career few months back.

She will be discussing about her life journey till date from the money perspective. I mean she will talk about her view about money, the incidents from her life which shaped her mindset about money. What she feels about money and how some incidents made her realise if money is important or not.

The special thing about her is that she is from Jagoinvestor Team 🙂

Few days back, when we were discussing on what kind of new writing we can do, we relised that we should start a series called “My money story” where a person jots down their journey of life from financial perspective and they felt about money all these years.

So I asked Priyanka to write her own money story. I think she has done an excellent job. This is the first post in the series we are going to call “My Money Story” where anyone can contribute with their stories.

Over to Priyanka from here.. I hope you will enjoy her money story.

Written by : Priyanka Jadhao, 26 yrs, Pune

My Story

I belong to a small town in Maharashtra, where most of the people are either government employees like teacher and regional officers or farmers. Other major businesses are very rare there, because most of the people have fear of taking risk, while others want to go on with the traditional ways of earning. In short, they want to play very safe game in life.

I was my parent’s first child, so it is obvious that everyone in my family had showered all their love on me. My family was not too rich, but it was financially stable enough, so I never faced any major hardships because of lack of money.

We should put limit on our needs

From my childhood, my parents taught me to put a limit on our needs, so that we can save for future. Everytime we needed something, the first thing we heard was to limit it or rethink about it before spending money on that.

This was the way of life and this had deep impact on my thinking. I slowly started beleiving that this is the absolute truth of life and it just got ingrained in my belief. Hence from childhood, I also started avoiding any extra spending, and always lived in limits.

Fortunately, I was never a spoiled child due to this mindset.

I can remember clearly, when I was a child, whatever things I needed like books or other study materials, my parents never gave me money directly in my hand. I had to ask for it and then only they used to buy those things for me.

People around me

I have seen people from my childhood considering money as a matter of pride, because of which they keep on collecting it and putting in their bank, rather than spend it on things. The focus was on just increasing wealth in numbers and not to make use of it for their happiness.

I grew up in an atmosphere, where earning money and saving it for future was the only motive. I have seen people who earned a lot, but never spent it to complete their dreams or for their hobbies because this was considered as a stupidity.

It was the way of life for them and they all thought that this is the “Right” way to live a life. They were satisfied and had no regrets about this. But that was because they had mastered the art of “controlling the need” and live with the most basic things.

My childhood experience with money

I was a shy child then, I never asked my parents more than what I actually needed. But when I used to see my friends buying dolls or fancy frocks, I always started thinking that ‘when I will grow up, I will earn lots of money and buy so many dolls and new dresses just like that friend of mine have’.

One incident I can still remember, I was in 5th std, one of my friend had a very beautiful lead pencil (lead pencils were very rare in those days, we were “Natraj Pencil” kids 🙂 ) having a beautiful less tied with eraser and two small Ghungroo’s on its cap. I wanted it so badly, but I didn’t have the courage of asking it to my parents.

Then I realized, that my birthday was coming in 2 months and my parents will definitely buy a new dress for me. So I waited for 2 months. And when my birthday came, I asked my parents to buy me that lead pencil instead of a dress. I can still remember its price, it was Rs.12.

Parents perspective about money

Both my parents are teacher. They earned a lot and invested it for only two goals, one is my brother and second one is me. I had never seen them spending money to complete their dreams or hobbies or even their basic wishes which were within their reach.

Whenever I asked them why do they work this much hard and can’t even take some time for themselves, the only answer I got was “Because we need to earn and save money, for both of your bright future”.

One more experience I would like to share. From my childhood I was fond of traveling. But as I told you earlier both of my parents were employed, we never had a family trip till date. My father had his own passion of farming.

Every day after job he used to go our farm (even today) and returned home late night. Whenever I asked him to plan a family trip, he always had his own reasons. He never said – “NO”, but he just always used to postpone it for next vacation.

When I was in school, one day I stared asking my father to plan a trip now. I was literally annoying him. So finally he said Yes, but I knew my father very well.

So, I took a page from my notebook make it look like an agreement paper by sticking a Rs.10 note on it (because I had seen picture of Rupee on some agreement papers before) and I wrote down on that paper – “We are going on a trip this time, papa already has approved it and so papa will now sign this paper” and then I actually took my father’s signature on it.

This time I was sure that the trip is going to happen as there was a written “agreement”.

But, that trip didnt happen till date.

This may look like a very small funny incident to you, but I was kind of shaken because of this. Even after an “agreement” was there, the event didnt happen. The focus was still on making more and more money and not on the trip.

And this incident made my belief stronger that earning money is more important than everything and everyone else.

All these circumstances made my mindset that I should also go on the same path, earn a lot of money, keep it in my bank account or invest all of it into some property like land or real estate so that one day I can had over it to my kids.

My belief become more stronger during my college days

In my college days, when I was completing my post-graduation, I always had to hear one common sentence from everyone – “Study hard beta, you should get good scores otherwise you will not get job and will have to spread your hands in-front of others for money”.

I was very afraid of this statement because of my over imagination, I was actually imagining myself begging for money and only started working hard because of this.

I started relating everything with money. I started seeing everything around me though the lens of “money”.

I started realizing on every point of my life, that without money there is no life. If I wanted to live a happy life, we need money.. and it became my behavior that I actually could not live without money. Whenever the money in my wallet was approaching ZERO, I become uncomfortable. I start feeling like “Oh My God.. What should I do.. ?”

I could not see my existance without money. If money is there, I am there. If money is not there, I thought I will not be able to live life.

I started feeling like if money is this much important then how can I ask for it to anyone? Including my parents!

And this feeling increased my hesitation in asking for monthly pocket-money to my parents.

I started feeling so helpless without money. But fortunately, I never had lack of money in my bank account and was satisfied with whatever I had.

How I turned a money minded person?

I was post graduate and still jobless. I had less money compared to my friends. I want to be on par with me. I wanted to have same lifestyle like them.

So getting a high class and well paid job was my dream just like every other youngster.

Now looking at my friends who had already started working and here I am still unemployed was quiet frustrating. I started feeling awkward, while asking for pocket money to my parents and a cycle got started in my mind asking same question repeatedly – “How to earn more and more money?”

One of the funniest moment which happened with me, is when my mother took me to a numerologist, who was suggested by my father’s friend.

That person asked for my details like date of birth, education etc. and then while predicting about my career and personal life he said – “She does not have dreams like a common girl, She is totally a money minded person and wanted to live just for earning money”.

I started smiling and thinking in my mind “Isko kaise pata chala?”

I used to get lots of free advise from people (Our uninvited financial advisers) that money is not everything, dont run after money, money is evil and things like that.

Which made me confused. If money is not everything, then why all these people are running behind it?

When I lost all my pocket money

5th September 2013, it was my first week in college – Modern college, Pune. I was new in Pune at that time and hardly knew anyone. On that day, all students including me were busy in the arrangements for the event of teacher’s day. I placed my bag on one of the bench.

Meanwhile I got a call from my mother. I went out to receive the call and came back to class finishing the conversation very shortly.

After that event and one lecture, I went to a snack center which was on my way to home to buy some food. I realized that my wallet was missing. I called a friend of mine and asked him to take me back to college, because I didn’t even have money for buying a bus ticket or for lunch.

I searched for it a lot, asked all my friends if they had seen it, but I was not able to trace the money. I couldn’t find it back.

I had a bad habit of carrying cash all the time instead of using card.

I lost all my pocket-money of that month and some other important things in one moment. But luckily my cousin was also living in Pune, so he came and helped me in that situation.

Since then, I used to carry less cash and started using card as much as possible. I learned that I should keep my money in various forms and at different places.

I started earning and my perspective changed towards money

A year after completing my PG, I started earning as a freelancer and I was little bit relaxed as I was not dependent on others for money. But my earning was not much, whatever I earned used to get spent.

Every month, money came in bank account and it just vanished in my expenses. Though, I was happy because of the feeling of independence, but still something was missing.

I wanted to earn more and more money, so that I can save for future.

Then, I joined Jagoinvestor Team

Before I joined Jagoinvestor team, I saw money as something which is to be earned and invested, and not for spending it for enjoying life.

But then my life changed and my perspective about money totally shifted. I came across various dimentions of money.

I used to hear my teammates talking to clients about their investments for their goals. At first I was completely unaware about goal based investing, which is what is practiced at Jagoinvestor (click here to get help from our team). I even created an audio related to goal based investing which you can hear below.

Only after creating that audio, I really understood why linking your money with goals is important and how it gives real meaning to your money and investments.

I had never looked at my money from this point of view.

We started having conversations at tea time and lunch time which made my ideas more clear about money. I started looking at money with a completely new perspective and in a more healthy way..

After that, when I looked at my bank balance it was looking like meaningless money, which was just lying in my account without any purpose, because of which it just got spent here and there without any planning, this this resulted into increasing my monthly expenses.

But now I have understood that the money is to be used for my important goals and has to be spent in a meaningful way.

I decided to give a purpose to that money.

My previous perspective about money have changed and I now realize that money is not just for earning or investing for future, but also to spend it for things we love and desire. Just accumulating money into bank account without any planning is meaningless.

There has to be healthy balance between spending and investing both.

We should keep a part of it for ourselves apart from our routine expenses and savings, so that we can live the life which we dream about.

How money is related with happiness?

Last week Manish Sir, gave me a 30 min video to watch and asked me to watch it till end, as it will give some new ideas around money.

I watched this video from Mr. Nilesh Shah about money, investment and Mutual funds. In that video one statement he made which took my attention was

“Money is not important – Make this statement once you earn enough money to spend your life smoothly”.

I strongly suggest you to watch this 30 min video below.

Happiness does not come just from accumulating more and more money, but how you make use of it. If you think of it logically then you will realize that money has become an inseparable part of our life. We cannot buy happiness directly with money, but still we depend on money at some point to be happy.

Writing, traveling, designing various crafts are the things that I want to do more than anything else. It’s my passion. But if I think of following any of these things, I can’t do that without money. Also, I need to have enough money with me, so that I dont have to worry about my basic needs and desires in life, so that I can find time to do things I love.

In short, money has has its own place and value in our lives.

My current opinion about money

I saw everyone around me just earning and passing on to future generation by compromising on their desires and wishes.

I think thats not the correct way to deal with money. If everyone will pass their own wealth to next generation, then who will use it?

If I earn a lot of money just like my parents did and in future my future generation (my child) also choose to earn his own money then what will happen with my investments or savings?

I now want to save for future, but at the same time, I also want to spend it wisely so that I do not regret fulfilling my hobbies and dreams. If I earn Rs 100, I will use Rs 30 for my basic needs, spend another Rs 30 for my wishes and desires (like travelling, shopping, eating out, entertainment) and save Rs 40 for future, which can be used by me only or can be passed to my children.

How I feel after sharing my story

When I took this post to write on, at first I thought I may not be able to write much on this topic. But once I actually started writing, it became more exciting than I thought about it.

I started realizing, how different I was earlier and what have I became now. Meaning and importance of money has changed completely for me throughout all these years and I didn’t even realize it.

Now when I read this article myself, I feel like I was completely a different person before. All these changes happened because of the experiences in different situations and the environment where we live.

This was my experience about money throughout my life.

What is your money story?

If you want to write your money story, Leave your details here and we will get in touch with you with next actions.

What do you think about my money story? Did you enjoy it? Can you share your views about money and how it changed over the years?

On 23rd September, we received an email invitation from Deputy Commandant (Dr. Lokesh Khajuria) for leading a personal finance session specially designed for Border Security Force officers and jawans. We immediately accepted his invitation and started our preparation for the same.

Manish flew from Pune, we packed our bags, prepared the presentation and started our Road Trip from Ahmedabad to Jaisalmer. Two more special people who joined us was our business coach Mr. Ravi Iyer and Abhikumar.

We were happy to know that people from defense follow jagoinvestor, it is popular amongst many officers and they had full faith in our work and philosophy.

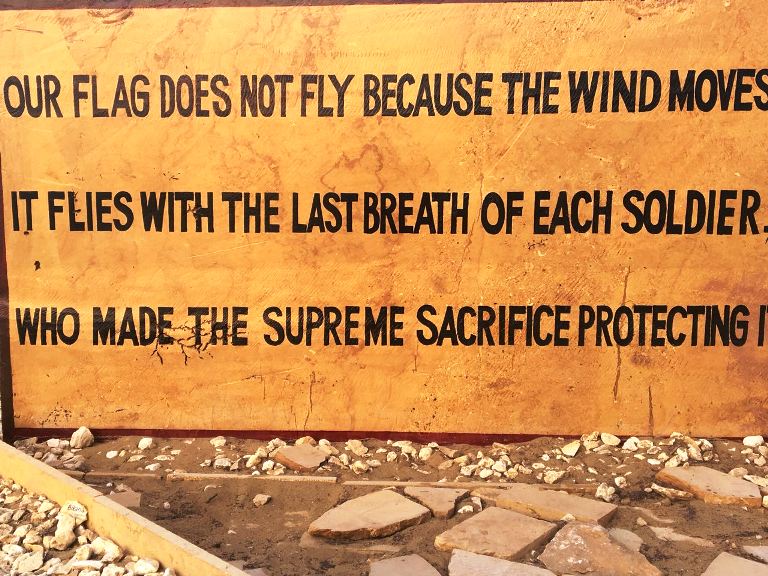

Our Intention

The intention was to give something back to our nation. I and Manish simply wanted to make a difference in the financial lives of those who are guarding 7000 km of Indian border.

The context set was very simple – “Ek nayi pehel, ek nayi soch ki shuruat”

The context got fulfilled and we could see that the participants got clear about things they should do and not do in their financial life. We went with an open heart and mind and shared all that we knew or have learned about personal finance in the last few years.

Download and read Over 250 messages for defense personnel

We wanted our readers to be a part of this journey and so we invited them to share one message for the border force and along with the message we also asked them to share one “Money Tip”. We got some amazing messages and some very interesting Tip from over 250+ Investors.

We do not have words to share what we experienced in those 4 Days. It was a space of discipline, commitment, and service.

The event positives were

Overwhelming Response from 100+ Participants

Curiosity to Learn more about ways to manage money

Event facilitated and supported by higher management

Check out our journey and some pictures

We would also like to share our journey to Jaisalmer and all the things we experienced there.

Some Thoughts shared by Dr. Lokesh Khajuria

We got an early morning Whatsapp message and I could not stop myself from sharing the same with you all.

Some years back, in the thinking mood, seating alone at BOP KHARIA… thoughts were flowing spontaneously..!!……

Desert has a natural and divine relationship with all human beings.

Almost all the major religions, prophets, saints originated from the desert. Immortal legendary love stories which are invoking human love even today originated from the desert. It is strange to find out what is it that desert wants to teach human beings?

……but if he searches hard enough, he returns with Oasis in his within !!!!! Deep in the desert, she is blessed with divinity… could make flowers bloom in the desert !!………

Dr. Lokesh

The circle of financial awareness is expanding

I and Manish are so happy to witness that the circle of financial awareness is expanding.

Very soon we intend to create the little army of people who are committed to spreading financial awareness. We will need your support in this work and we will ask for your help and support in the same.

If you wish to organize financial awareness program in your organization or company you can get in touch with us on [email protected]. Let’s get together and create a world that works for everyone.

Once again we thank Mr. O.P Sharma, Dr. Lokesh Khajuria, Birbal Sir, Manoj Sir and BSF Jaisalmer Team Gladiators

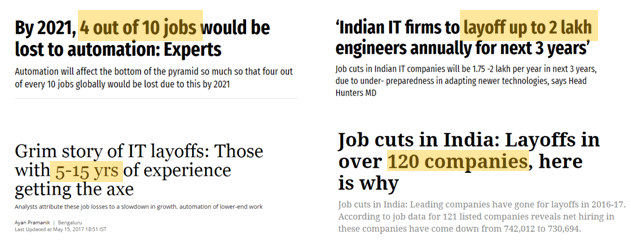

Job loss is a scary situation because it’s a big disruption in your life. If you lose your job, you need to suddenly look for another job quickly because you have to meet your household expenses and also deal with the emotional crisis.

In case of a layoff, you also lose self-confidence and start doubting yourself and keep wondering what the future is going to be now. Look at these news headlines which talk about so many job losses in India. While all the sectors have layoffs, these headlines are more from the IT sector.

Are you prepared enough for a job loss?

Have you ever thought about this situation? Have you ever visualized about losing the job?

We all are so confident subconsciously that something like a job loss is never going to happen with us. We hear that it has happened in someone else life, but we consider ourselves so lucky for no reason.

Our lives are smooth and our planning for the future is perfect, but it’s critical to check if you can take the bad news of job loss? Is your financial life strong enough to handle that situation?

Have you ever thought about this?

Have you ever thought about how you will be paying your EMI’s, your kid’s school fees, rent, various other household expenses and how you will deal with stress and the insecurity which will come with the job loss. If we pick the software industry, there is enough bad news coming in from the last many years.

The industry is going through tough times (and even good times) and it’s not very uncommon to hear that thousands of employees got a pink slip and lost their jobs!

If we talk about you, are you skilled enough to find a new job in the same industry with the same pay package? Can you afford a lower salary? Do you have enough savings to deal with the stress of living without a paycheck for the next 6 months?

I found some real-life experience of people who are sharing about their job loss and how they felt about it. Please read them to understand how it feels and what it means.

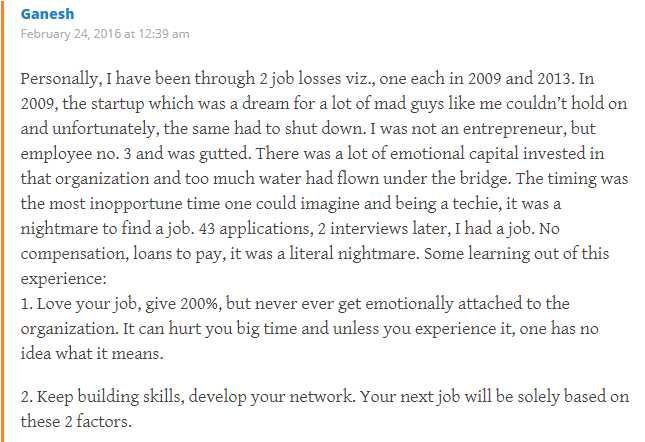

Story #1 – How Ganesh felt when he lost the job in a startup

Below is an experience of Mr. Ganesh who shares how he lost the job and had to face issues in his life.

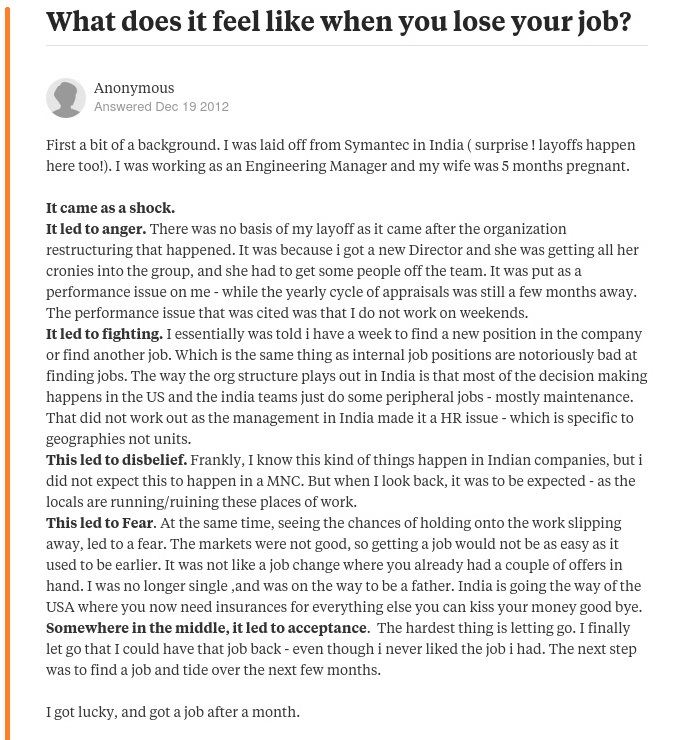

Story #2 – How a software engineer felt after a job loss

Here is another experience of a quora user who worked for Symantec and lost a job when his wife was 5 months pregnant.

How to prepare for bad times?

We don’t wear a helmet while driving because we want the accident to happen. We wear it so to make sure we are protected if something goes bad accidentally.

In the same way, we should design our lives in such a way that even if we lose our jobs, the impact is limited and the emotional and financial loss is in control.

I know losing a job is not a great thing. Most of the wake up when they actually lose the job and start thing on what to do.

Don’t be that guy!

While you can’t stop someone from fire us, you always have control over what you can do to face that situation. So let’s talk about a few things you can and should do today to be ready for that scenario.

Action #1 – Have 6 months worth expenses in an emergency fund

When you lose the job, the immediate question which comes to your mind is – “How will I pay my bills?”

You have EMI’s, household expenses and many more things to deal with. You already know how messy it can get. I don’t want to get into details of it, but you need to pay all the bills. At best you will be able to stop a few things for a while, but how long?

You should have enough liquid money with you which can last for a few months. It’s like the emergency fuel (6-month expenses) you need in your car to reach the petrol station (new job).

One more reason why you need to have enough emergency funds with you is that it gives you more power to choose your next job.

If you do not have money at your end to last another month, you are too scared. It’s a panic situation which forces you to choose any job which comes next. It’s like being desperate for marriage and then saying YES to the first person you meet. Not a good thing for the long term.

Action for you: Just multiply your expenses by 6 and keep that amount invested somewhere which can be available at short notice (like few days). The focus has to be more on availability and not returns. You can choose a debt mutual fund or a simple fixed deposit for this.

Action #2 – Don’t have a neck to neck expenses

A good habit for any investor is to make sure that their income is 1.5 times of their expenses. You should not be living a life where every penny you earn is getting spent.

I know it’s easier said than done for many people, but at least start taking action towards this.

There are two benefits here.

Benefit #1 – You will have good surplus each month which you can invest in for the future. It keeps you worry-free and you also can save good amount.

Benefit #2 – When you lose your job someday, you at least have an option to take up a job that is paying you less. Imagine you are earning Rs 1 lac per month. In case your expenses are neck to neck, you will not be able to accept a job that is offering you Rs 80,000 a month. Can you?

I strongly suggest that your total expenses (including EMI and everything) should not cross 60% of your income. It’s a good habit to practice in your financial life.

Action for you: Find out the ratio between your income and expenses. How much are you saving each month right now? If it’s less than 40%, focus your energy on earning more income. If not immediately, give yourself 2-3 yrs of time when you will increase your income to the next level.

Action #3 – Be awesome in what you do

Don’t be mediocre in what you do. Don’t be average in what you do.

Are you a java developer? Then be the one who knows everything inside out and make sure you are among the top 5% in the entire world

Are you a marketing guy? Then make sure you are the one who can really transform the marketing of a company if you take that task in your hand.

Are you a chef? Then make sure you are worth inviting to master chef show!

Whatever you are doing right now in your life, just make sure you are ONE OF THE BEST.

I am not saying that you should do something extra ordinary in life, but whatever you are doing, strive to be one of the best in that field.

If you focus on this, then you probably will never lose your job. And even if you do, you will quickly get another, And if you don’t get another job quickly, you will at least be calmer and composed than others who know that it’s just a matter of time. Your panic level will be low.

Action for you: Make a list of things you need to do to go to the next level in your profession. List down which are the training you need to attend, list down which all certifications you need to complete. List down if you need to change your job to learn new skills? List down if you want to ask for help from someone more awesome than you. List down all the points and complete that in the next 12 months.

Action #4 – Start saving money and build a good portfolio

There is this concept of human capital and money capital.

Human capital is our ability to work and earn money, it’s about the potential and how much you will bring in the future.

Money capital is your portfolio which gets build over time, you keep earning money and save from it and start increasing your money capital.

When we start our career, we are high on human capital and zero on money capital. When we retire, we have money capital and very low human capital (maximum cases).

Start building a good portfolio

Focus on investing and saving money from a long term perspective. It’s better to lose a job with 50 lacs lying in your mutual funds and deposits in the bank. It’s a much better panic situation compared to just having some money in your bank account.

I know it’s very tough to have any portfolio at the start of the career but do whatever best you can do. Focus on creating your first 1 lac, then first 10 lacs, then first 50 lacs.

But at least take actions to reach there.

If you have good amount in your portfolio it feels safe. You can fall back on something which can last you for many years in the worst case. Imagine not having much in your portfolio and losing a job. Even Rs 10,000 invested per month can give you 25 lacs in 10 yrs if done in the proper way.

So ask yourself, if you have enough money capital as per your situation? Have you built and saved your money capital or not?

In the case of job loss, most of the people who are in extreme panic are those who have no sufficient money capital and human capital. Even if you save 10% of your money income on a consistent basis over your working life, it’s going to be a very huge amount. But most of the people even fail there.

Action for you: First slow down. Then see how much is your monthly surplus each month? Are you investing that money on a regular basis? If not, it’s time for you to start your SIP (our team will help you in building wealth in a systematic manner).

Don’t make these 5 mistakes at your work

Let’s quickly look at a few points which lead to a job loss. Many people just do wrong things at work and expect to never get fired. If the points below are true for you, its time you relook at your approach and take corrective steps.

Not updated yourself as per job requirement – Are you still acting as if you are in 2007? Are you refusing to learn new skills that are required in your job? Are you into that comfort zone? If yes, it’s a signal that you may lose your job because you are getting stale day by day.

Not able to work with others – Are you a team person? Any work is done by a group of people and not a single guy. Make sure you know how to have good relations with your teammates and work with others. If you are not a team guy, you might not be part of the team soon.

Failure to do your work – This is a no brainer. Are you consistently failing in the work assigned to you? Are you not able to complete it in a given time and with the expected results? Get more trained, ask for help from others if that’s the case. It’s ok to fail once in a while, but if it’s happening very frequently you are on a list of non-performers and you might get a pink slip very soon.

Failure to take initiative – Are you just doing what you are supposed to do? That’s all? Are you taking new initiatives yourself and showing that eagerness to go out of your way and surprise your employer? Remember, the pyramid is smaller at the top and you want to move to the top like many others. You will be the first tree to get cut if things get ugly.

Failure to demonstrate productivity – Are you busy or productive? A lot of people do lots of things at work only to produce very little at the end of the day. Make sure you are doing more and highly useful productive work. Also, make sure you show that to your employer. Get it noticed and recorded.

I hope I was able to reignite your thoughts on these points. Do let me know how many marks out of 100 will you give to yourself on preparedness for job loss?

If you are 100% prepared and ready to cope up with it, you score 100/100, else 0/100 at the extreme end. I would like to hear about this from you and what you are going to do about it.

Today you will read one of the fascinating stories of one of our readers (Naren from SavingHabit.com) who has shared his personal journey on early retirement and also gave a step by step path on how to change your mindset about it. This is a long article, but quite deep on the topic of early retirement. I suggest you read till end.. Over to Naren

–

A few weeks back, I had shared my comments on early retirement on the “Myth of Early Retirement” article and Manish asked me to to elaborate on my comment and also do a guest post on this topic.

In this post I will go in detail on how to plan for early retirement and also share my personal early retirement journey.

Disclaimer : This article is purely the author’s personal opinion. The author is not a certified financial planner. Seek the help of a certified financial planner for your individual situation.

When mid-level IT employees in their 40s are being forced into early retirement anyway through layoffs, it has become a necessity for our generation to pro-actively plan for an early retirement. As early as 2011, JagoInvestor reader Ujjwal working in IT predicted this exact scenario and recommended planning for early financial freedom.

How I discovered Early Retirement?

I graduated in computer science straight into a recession caused by the double whammy of the dot-com bust and the 9/11 attacks. My father had recently retired from his public sector job and I did not have any job offer on hand as campus hiring dried up completely. It felt like I was being tossed around by economic forces beyond my control.

When I finally entered the workforce at a Big Company, I was soon frustrated by the usual job stress and job insecurity.

I decided to end this “working for money” problem once and for all by joining an early-stage internet startup. Joining a startup was also my dream since college and I had plans to start my own later. The idea was when the startup will sell for millions, I would strike it rich and never have to work again. Well… 6 years later when the startup was sold, my services were no longer needed. I was out of a job without striking it rich 🙂

Around this time, I discovered the early retirement community online that talked about focusing on the one thing I could control : my savings rate. All along I had focused on things outside my control and failed to solve the “working for money” problem. Out of all the options available to salaried employees to achieve early financial independence, early retirement offers the highest chance of success because its success or failure is under your control: how much you save each month.

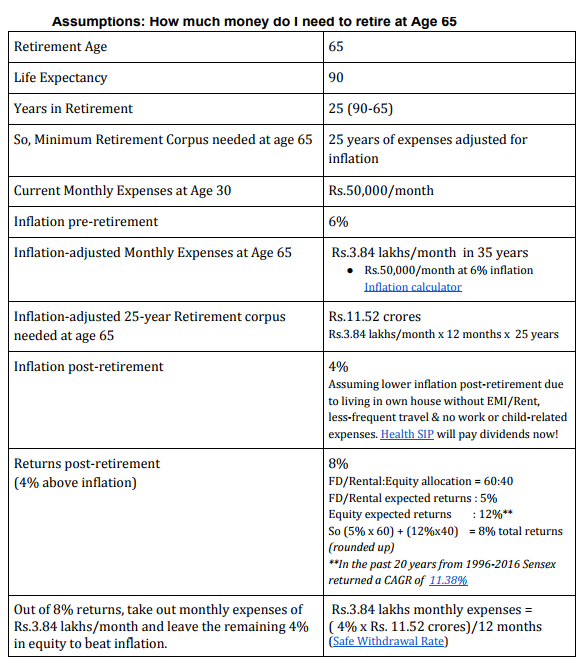

WHAT IS EARLY RETIREMENT?

Most of the Early Retirement literature online is from the U.S which is understandable because they have a longer history of regulated stock markets & mutual funds compared to India.

In this article I’ll do my best to translate Early Retirement for Indian conditions as we have our cultural differences when it comes to money like parents paying for child’s college expenses, joint families where children take care of parents in their old age etc and recent cultural changes mirroring the U.S like home loan EMI, SIP, credit card spending, low savings rate etc

Let me first start with what most people think when they hear the term “Early Retirement”:

It is a stage by Age 40 when you are able to meet all your expenses through passive income from investments like Real Estate (rental income), Mutual Funds, Stocks (dividends) etc.

So you don’t have to work anymore to meet your expenses.

You can easily live on only investment returns post-inflation so your corpus will last forever beating inflation…theoretically.

While this is the “popular dream”, in reality Early Retirement simply means achieving financial independence early in life so you can focus on achieving your important goals in life. This is popularly abbreviated online as FIRE : financial independence/retiring early.

You can be employed at this stage, but in alignment with your life goals for example:

To do something you love

To spend more time with loved ones

To earn money with less stress & more work-life balance

To lead a healthy & active lifestyle

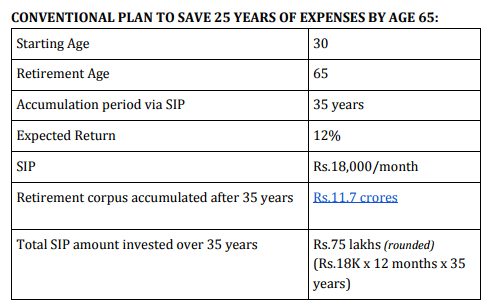

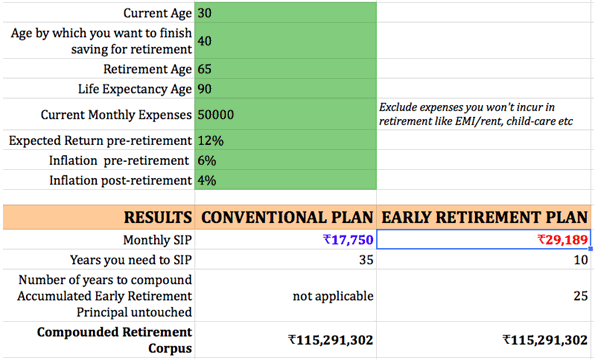

It is possible to retire early by age 40 but only if you aggressively save at least 50% of your income starting early in your earning life instead of doing a small monthly SIP with the goal of retiring in old age at 65.

Save 50% of my income??!! I can barely meet my expenses each month

Relax! You are already saving more than you realize. You already contribute 12% of your basic income mandatorily to your EPF and get another 12% employer match. That is a 24% savings rate on your basic income. So calm down and I’ll discuss some strategies for increasing your savings rate later in this article.

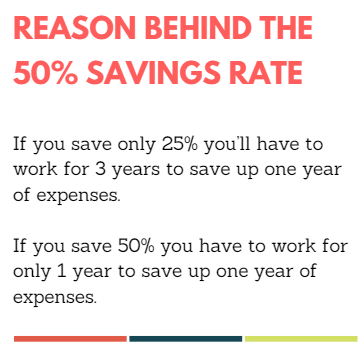

There is a reason behind the 50% savings rate

This is the simple idea behind Early Retirement before inflation & investment returns enter the picture. 50% savings rate may not be possible immediately for people whose income is low or expenses are high but early retirement is not possible unless you increase your savings rate to at least 50%

Here are some inspiring real-life people saving close to 50% :

Here is the link to the “Family Finances” section from ET Wealth magazine. Make sure to look for households who fit your profile and are saving at least 50%. Ask yourself : If people similar to me can save so much, why shouldn’t I save more than my current rate?

Let’s step back here for a minute

First, you need to be very determined to retire early.

When you truly want something you will come up with solutions rather than excuses and you’ll get inspired instead of finding faults. Imagine in your mind’s eye for a moment all the positive reasons why you want to retire early like Family-time, Freedom, Health, Low-Stress, Travel, Security etc.

Now get yourself into an optimistic “can-do” frame of mind before reading further.

Early Retirement is an improved version of Conventional Retirement

Around 100 years back even conventional retirement at age 65 was not possible for everyone. What was once a fantasy is a reality now. Now everyone believes it is perfectly normal to retire at age 65.

Similarly, for the first time in history, due to innovations like regulated stock markets, mutual funds & SIP, even the salaried middle-class can now retire early which was previously possible only for high-earning executives or businessmen. So if you try and understand Early Retirement you too can take advantage of it and enjoy a better quality of life.

Be ready to take some tough decisions on what is important to YOU in life rather than just going with the flow of what everybody else is doing with their life.

Can I just retire early and never have to work ever?

The typical dream of Early Retirement is to “sit and eat” from the retirement corpus without having to work for money from age 40 to age 90 which is a long span of 50 years which no one can predict.

It is a difficult feat to pull off as Life has a habit of springing surprises especially when you have kids and elderly parents. But it is possible if key variables outside your control like the stock market returns work in your favor and there are real-life success stories like Mr.MoneyMustache.

Two big problems with this “I never want to work again” Early Retirement thinking:

UNCERTAINTY:

If a family member has a major health expense not covered by health insurance, how will you meet that expense if you are not earning any additional income?

If you cannot find a tenant for your rental income house for more than a year, how will you meet household expenses if you are not earning any additional income?

If the stock market crashes by 15% and goes into a 5-year recession, will you have the stomach to withdraw money for monthly expenses from an already depleted corpus?

What if all of the above happen simultaneously in your life like the expression “When it rains, it pours” ?

STRESS: you’ll replace the stress of a job with the stress of obsessing over running out of money every single day of your early retirement.

My Alternative Early Retirement Plan for Indian conditions

Stop working for “money” but don’t stop working

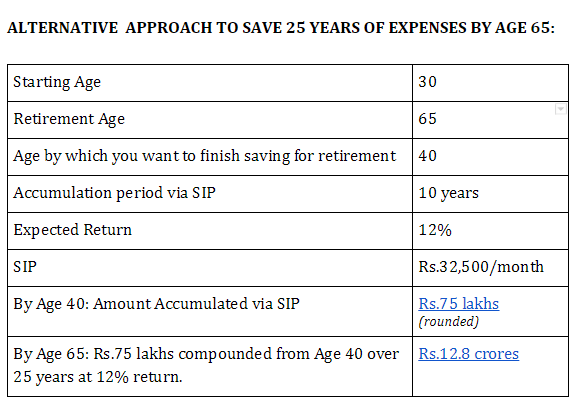

By Age 40: Finish saving up for retirement by saving at least 50% of your income in retirement SIP.

After Age 40: Stop your retirement SIP & switch to work that you truly enjoy in order to cover monthly expenses.

From Age 40: Let compounding double your retirement corpus every 6 years until age 65!

The idea is to permanently secure your comfortable lifestyle by age 40 so you can follow your dreams without fear. Even in the worst case scenario you’ll always be guaranteed to enjoy the comfortable lifestyle of your 30s.

The benefits of this alternative approach

FREEDOM: Free by Age 40 to do work you truly enjoy

While saving up for retirement your monthly budget at 50% savings rate will look like this:

By age 40 once you finish saving up for retirement, you don’t need the retirement SIP anymore and your budget will look like this

Income Rs.1 lakh = Rs.50K Expenses + Rs.50K Surplus

After age 40, you can work for a 50% lesser salary at jobs that are more fulfilling and less stressful but fully pays for your monthly expenses including support for kids & elderly parents:

Income Rs.50K = Rs.50K Expenses

Most people who want to retire early simply are tired of the job stress and deep down are not averse to working if there is work-life balance and they are working on something they truly enjoy.

SECURITY:Your retirement fund is actually a 25-year emergency fund!

If you ever lose your job before age 65 like the TCS/Cognizant/Infosys mid-level managers in the headlines : you can use a small portion of your retirement fund to fund monthly expenses for even 3-4 years while you re-skill and find another job after which you can replenish the amount you took out during the jobless period.

Instead of trying to live off the retirement fund for life from age 40, you strategically use the retirement fund to build a safety net for uncertain times and take calculated risks like starting a business or a new career.

LESS STRESS: Not having to worry about money running out

It is an open secret that even the pioneers of early retirement that I hero-worship like MMM & ERE bring in active income in their “early retirement” from working on their passions like building houses by hand or working as a quant trader/researcher leaving their retirement corpus to compound meaning they are not solely living off of their early retirement corpus themselves.

So if the early retirement gurus are bringing in active income why shouldn’t you factor in the active income from your dream-job in your early retirement plans? Why assume that working on something you enjoy won’t cover monthly expenses even after working at it for 3-4 years?

You’ll be sitting on a 25-year emergency fund in the form of your early retirement corpus for God’s sake! If you are still unsure, you can start working on your dream-job as a side-project while you are still working at your day-job to give yourself enough runway and confidence that it will make money by the time you quit your day-job.

PRACTICE: Great Training for “full retirement”

Scaling down your work by 50% by age 40 is a great way to get a preview of what “full retirement” will look like at age 65. You will get a lot of wake-up calls mostly around the state of your health, investment returns , wasteful expenses and whether you really have any true passions in life or were you just lying to yourself about “dreams & passions” to mentally escape from job stress 😉 So while planning for Early Retirement also work on your passion on the side to prepare yourself for the post-40 life.

4 STRATEGIES TO INCREASE YOUR SAVINGS RATE