Buying a house isn’t easy today if you are living in a metro city like Mumbai, Pune, or Delhi. It’s nearly impossible to pay the full price of a house unless you have massive savings or an existing real estate that you can resell. This is the reason why most people take home loans, or rather joint home loans.

What is a Joint Home Loan?

As the name implies, a joint home loan is a home loan that you take with another person, who is usually your spouse or a sibling. There are many reasons why people avail of joint home loans instead of standard home loans, one of which is bad credit.

Let’s understand why.

No matter what kind of loan you apply for, the lenders always check your credit report to assess your creditworthiness. This a standard practice to reduce the risk of non-performing assets. So, if your credit report looks fine which means that you don’t have a history of late payments, loan defaults, etc. and your credit score is high, then you can avail a loan easily.

However, if that’s not the case, not all hope is lost as an alternative option exists! That’s when you can get a co-borrower to take a home loan with you. If their credit score is good, then it can balance yours and make it easier to get your loan approved.

People also take joint home loans when they aren’t capable of repaying the full amount on their own. By dividing the loan’s burden with their spouse or a family member through a joint home loan, the debt can be repaid easily. Now that you know what a joint home loan is, let’s take a look at some of the major pros and cons of the same.

Pros of Joint Home Loan

The chances of getting a home loan at attractive interest rates are much higher in a joint home loan compared to the regular home loan.

As per the income tax regulations, joint home loans allow both co-borrowers to claim tax benefits under Section 80C. They each can deduct up to 2 lakh INR from the interest amount and 1.5 lakh INR from the principal amount from their taxable incomes.

If you are unable to get a home loan due to poor credit score, then a joint home loan can be your best bet.

Cons of Joint Home Loan

If your co-borrower in unable or simply refuses to pay the EMIs, then your credit report apart from theirs is affected.

Joint home loans can raise all kinds of legal problems if the co-borrowers are married to each other and get separated by divorce even as home loan remains to be repaid. If the property is registered in the name of one co-borrower, then after the loan has been fully repaid, he/she will become the rightful owner even if the other co-borrower has also paid their share of the EMIs.

Common Myths About Joint Home Loans

A joint home loan is a massive financial obligation. Apart from the huge EMIs that are particular to these loans, the tenures are not lesser than 15 to 20 years which means you pay the EMIs for a large portion of your life. Thus, it’s a good idea to do extensive research before you finally start submitting applications for a joint loan.

It would help if you also were wary of some of the most common myths about joint home loans that mislead borrowers:

Myth #1: A Co-Applicant is Required Just for “Formality.”

A co-applicant is as much responsible for a loan’s repayment as the primary borrower. In other words, signing on the dotted line imposes legal and financial obligations which is why it’s strongly recommended that both co-applicants read the fine print and ask as many questions as they need until they have a good understanding of the agreement they are about to enter into.

Myth #2: Only One Co-Borrower Can Receive Tax Benefits

People think that in joint loans, only one of the co-borrowers can receive tax benefits. However, this is further from the truth as both co-borrowers are equally entitled to these benefits. This means that you and your co-borrower both get to enjoy lower individual taxable incomes. That said, you must know about Section 24 of the Income Tax Act which sheds light on taxation in joint loans.

As per Income Tax guidelines, a co-borrower can claim tax benefits only if he/she is also a joint owner of the property. This clarification is important because many times, people take joint loans to increase the loan amount and make the process easier. However, merely being a co-borrower doesn’t make you eligible for the tax benefits. You must have ownership rights over the property as well.

Myth #3: Roping in a Co-Applicant is a Sure Shot Way of Getting a Home Loan

It’s true that it’s easier to get a home loan with a co-applicant compared to when you apply just by yourself. However, there is no guarantee that you will get approved for a loan. This is because home loans are highly risky for the lenders, even if they are secured against the homes they are availed for.

So, a co-applicant can’t help with the application if they don’t contribute to your “creditworthiness”. In other words, a co-applicant can make it easier to get a home loan only if their credit score is high and their income big enough to cover the EMIs.

Failing to Prepare is Preparing to Fail!

Joint home loans have their pros and cons as explained above. However, there are many other factors that you must consider including the interest rates, income, financial projections for the future, and buying a new home vs. an old home. After all, once you borrow money from a bank, there is no turning back. So, take your time and pick the right loan at the right time. Good luck!

Do you avoid various actions in financial life which are often suggested as the “right decisions”?

There are countless articles and videos these days which tell you that it’s important to have sufficient life insurance and health insurance. One should start investing very early in life so that they can create some good wealth to take care of their future.

Like these, there are various things that are mostly the building blocks of a good financial life. But often investors avoid taking those decisions. The biggest reason why it happens is that we are all lazy investors who focus on NOW rather than FUTURE.

If it’s not creating trouble for us right now at this moment, we keep postponing it and underestimate the trouble it can give us in the long future. In short, the future trouble or problems we will face is imaginary at this moment.

So today I thought I will talk about the impact of these decisions and how it can trouble you in the future. Let’s start

Mistake #1 – Not buying a health Insurance

Today I will not talk about what will happen if you buy health insurance, but I will talk about what CAN happen if you do not buy health insurance.

At one point in our life, when we start our career, we have ZERO wealth. There is no money in the bank account and we struggle too much to start saving. Our salaries are less and we have just started our career.

Our salaries are not much when we start our jobs, but our expenses start building up. Rent, groceries, Petrol, eating out and whatnot.

After a few years, suddenly we realize that we are just living paycheck to paycheck and we are not saving any money. Years pass by, but you have nothing worth calling “Portfolio”.

In fact, it might happen that you are in credit card debt now and you are wondering if you will ever be able to retire RICH!

Then comes, a point in life when you realize that it’s enough and now you need to start saving money for the future no matter what. Enough is enough.

You start your first investments

Somehow you start your first Recurring deposit or SIP in mutual funds. You start with a basic Rs 2,000 per month. A few months pass and you are happy to see that you have some savings now at your end.

You are excited and want to make sure you do not break this newborn habit. A few years pass by and you have done it! .. Congrats, you managed Rs 5 lacs in your portfolio. It took some years and lots of commitment to reach there.

You feel like a winner and you now truly understand the joy of having a big amount lying in your bank account. What a relief and feeling of safety it provides.

You are even more committed to save now you plan to reach the target of Rs 10 lacs with the next 2 yrs.

You are happy and life is all good.

Then the bad day happens

Then one day, while going to the office, some Rowdy Rathore in a Bolero who is trying to race his car with some unknown person hits your bike while you were on your way to the office. It’s a major accident. You can imagine some other medical emergency in a family if you do not like this example.

The hospital bill comes to Rs 6.3 lacs. There was a surgery done to make sure you survive and you were in a good hospital for 12 days.

You had to take out all your money from the bank or mutual funds and additionally, you have borrowed from your relatives/friends or swiped your credit card to complete the bill payment.

After a few months, you are back to life. But your financial life is back to square one. Your wealth is eroded. You did not protect your wealth from medical emergencies.

You did not take health insurance

We do not think like this about health insurance. We never see health insurance as a financial product that helps us to protect wealth. Buying health insurance is all about transferring the risk of paying the hospital bills to someone else. Health insurance does not protect your health. It can’t.

Remember, starting your savings and investments is easy (not that easy), and consistently doing it for many years it very tough.

Those investors who do not take health insurance over-focus on what is NOT GOING TO HAPPEN. They say things like

What if I never get hospitalized?

What is I drive carefully and never get into an accident

I exercise and eat healthily, why do I need any health insurance?

My company provides health insurance, so why do I need additional health insurance

I will waste my premium if I don’t get hospitalized for next 30 yrs

Sorry, but you need to focus on WHAT IF IT HAPPENS, rather than what if it does not happen.

Note that a health insurance product gives you a protection cover of a big amount every year. So if you buy health insurance with cover of Rs 10 lacs sum assured.

Click here to buy health insurance from our Trusted Partner (special collaboration with Jagoinvestor)

What you are accepting by not buying health insurance?

So finally, as a conclusion – When you do not buy health insurance, you are saying that I am ready to pay the entire hospital bill out of my wealth, every time it happens. I will take the risk of getting my wealth eroded by medical issues.

Mistake #2 – Not saving enough money for future

The next thing I want to talk about is not saving enough money for the future.

You have a nice car, you eat out often and you are able to take care of all your house hold expenses right now. You also take short vacations often. This is all well and fine if you are saving enough for the future. But if your expenses are almost equal to your expenses, remember that one day will come when your income is going to stop permanently.

That will happen when you reach around 60 yrs. And you will probably live for another 30 -40 yrs (wish a long life to you)

But if you do not have enough wealth created by that time, the journey ahead will not be filled with fun. Imagine you retire with just 5 yrs worth of expenses in your bank account.

How cool is that?

How will you feel to find yourself in a situation where you know that you require 100 units of money each money to live a comfortable life which you desired, but your wealth is only capable of providing your with just 40 units of money each month? Or 8 units?

You will have to choose between a vacation and food on the table. Forget food on the table, you will have to choose between “cheaper” vs. “what you like” each time you think of what to cook for dinner.

You will have to decide each time if you want to travel by air or sleeper class on a train (I love both options)

You might have to make excuses each time your friend circle plan a holiday trip

You might have to constantly worry if a restaurant bill will be too much?

It might sound very dramatic right now hearing all this, but the truth is that the future is imaginary and it’s tough to plan for it. I am not saying that you should create enormous wealth by compromising today, but all I am saying that you should be well aware of how your decision of not saving enough today will impact your future.

A little financial planning helps

Most of the people who come to us for financial planning are already late in investing. We can’t fix it fully, nor do we give them false promises that they will retire as a millionaire. But we make sure that they make the best of the years ahead.

We make sure that whatever suggestions we make to them for their wealth creation aligns with what they want in life ahead. We plan for their goals and create a decent strategy to reaching those goals.

Saving money right now does not give you any joy or benefit right now. Saving for the future also means cutting down on something today hence we don’t do it. Saving for future means.

Cutting some part of your shopping today

Cutting down on your eating out today

Compromising a bit on your entertainment today

Buying fewer gadgets today

Buying fewer clothes today (please raise hands, if your closet has something which is not used since last year)

What you are accepting by not saving enough for the future?

So finally, as a conclusion – When you do not save enough for your future, you are saying that I am ready to be dependent partially or fully on others for money and my day to day expenses. I am ready for a lifestyle which might be very different from today. I am ready to live a life which will come with daily struggle and stress about money.

Mistake #3 – Not having a term plan

Accidents are called accidents because they are not planned nor they are expected to happen.

Why are we so over confident that nothing can happen to us and bad things happen only to others?

We all have recently heard about the Kamala mills fire news. Almost a dozen people lost their lives in that fire. One couple who lost their lives were actually sleeping when their friends asked them to join the birthday celebration of some other friends. They woke up and went there, but never to return.

Life is LONG

Life is very long and your loved one needs a lot of money to live comfortably. We need to make sure that we cover this risk by taking a sufficient term plan for which we need to pay a very small premium.

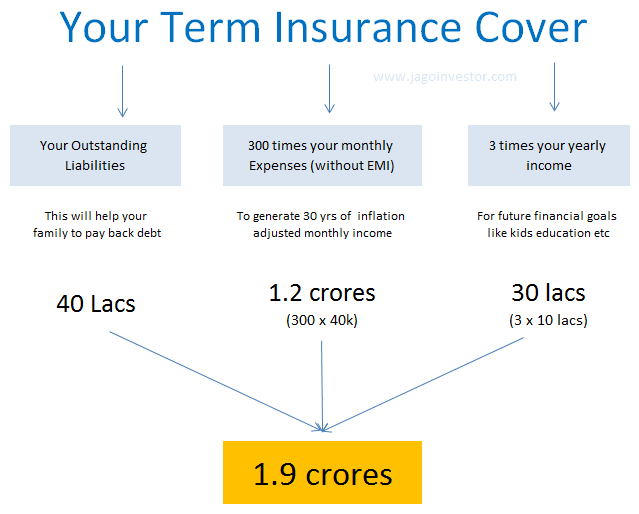

A family whose expenses is around 50-60k per month needs close to 2 crores of life insurance.

If you leave behind a family who is weak financially, you are leaving them with the risk of being dependent on others for their survival. While you can’t prevent the emotional loss, neither you can minimize it. You can surely take action today to minimize the financial impact.

If you have enough wealth and assets which will help them financially in the future, then it’s totally fine to not buy a term plan. But if you are someone who has no assets or wealth, you need to make an arrangement for the worst case. There is a famous saying – “You don’t buy a term plan because you will due, but because your family will live”

Answer this: In your absence (and the money you bring on the table)

How will the next 30 yrs of household expenses come from?

Who will fund for your kids education

Who will repay your debt?

Who will pay for all the desires your family has?

Where will they turn up to when they need money in cases of emergencies?

What you are accepting by not buying sufficient life insurance (assuming you don’t have enough wealth)?

So finally, as a conclusion – When you do buy sufficient life insurance for your family, you are saying that you are ready to let your family face lifelong financial suffering. Your kids and spouse + parents might be suddenly forced to live below the standard of living they are used to. Your kids might not get the same quality of education which would have been possible if you were there.

Mistake #4 – Over investing in Fixed Deposits/PPF

For some people, fixed deposits are the only way to invest their money. It’s a safe and secure way of investing. Our parents did it and there is a visible problem when you invest all your money in fixed deposits or saving bank account (or PPF or Post office schemes)

After all, you park your money in FD/Saving bank and it grows in value over time. What’s the issue in that?

The biggest problem is that your investments do not beat and outgrow inflation over the long term. You get a feeling that your investments are increasing, but your purchasing power does not increase. Its goes hand in hand with inflation.

So if you were able to buy 1 loaf of bread earlier, even today you will be able to buy the same 1 loaf of bread with the money you had invested in FD.

Your life style will remain the same over the years because your money is just growing as per inflation. To counter this, you need to invest your money in something which counters inflation, like equity. It can be stocks or equity mutual funds.

Here is an example

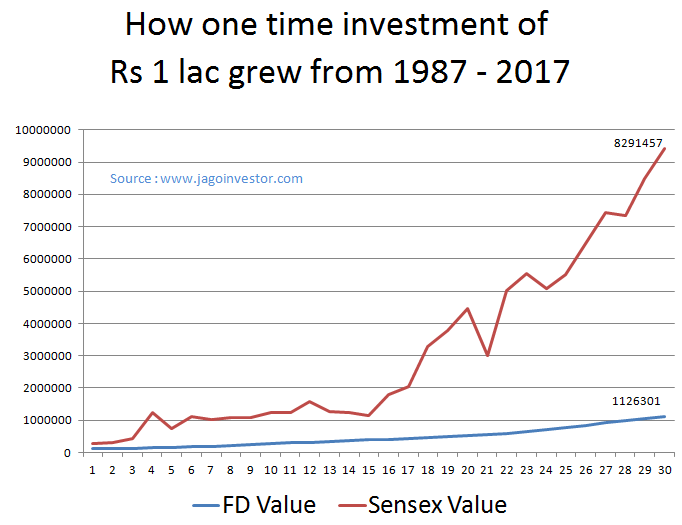

Imagine this, Rs 1 lac invested in Fixed deposits 30 yrs (year 1987) back is worth Rs 11.3 lacs today (the year 2018). Don’t jump out of excitement. 11.3 lacs today is worth Rs 1 lac 30 yrs back in real terms.

Whereas, if one had invested the same Rs 1 lac into Sensex 30 yrs back, it would be worth 83 lacs today, that’s close to 7-8 times than FD

Consider two friends who were 30 yrs old in 1987. They were fresh into jobs and started their career. One invested 1 0 lac into FD for his retirement and other one invested 10 lacs one time in Sensex.

One retires with 1.1 crores in hand and other one with 8.3 crores. One of them will get a monthly pension of 7-8 times compared to the other one. Just image the difference between them and how they will feel about it.

What you are accepting by investing only in Fixed income asset class (like FD, PPF, Post Office)

So finally, as a conclusion – When you only put your money in fixed income instruments all your life, and refrain from equity asset class, you are accepting that you will take the safe and secure path which has no growth element in it. You are ready to retire the middle class itself. You are consciously accepting that instead of 8X money, you are ok with 1X money because you are not ready to take the risk.

Mistake #5 – Taking too much debt in your life

There are two kinds of investors – One who buy things in life mostly with their saved money, and other one buys most of the things with their future income – i.e. LOAN

When we start our career, we have no idea what a devil is this credit card or a personal loan. It’s as simple as BUY NOW and PAY LATER. How bad it can be after all?

We feel we are in control of ourselves self and we will take rational decisions when it will come to money. We think we are not going to make stupid decisions. But only after years, we realize that the game is not so simple.

Once you depend too much on loans and credit cards, it becomes your way of life. You keep shopping and buying things you desire on debt, thinking that you will pay it later.

It’s all about falling for instant gratification and there are millions of people in India who are deep into debt. There are people who have bought cars which does not justify their pay package, and many people have home loans which are much bigger that what they can truly afford.

You will be the slave of MONEY

The biggest problem with this approach is that you become a slave of money. You have promised to pay all your future income, which is uncertain and which is not even earned.

You will be now going to your job to earn money, not by choice but a compulsion. Also, you are going to take less risk in life because you can’t afford to take much risk anyways now. If you do not like your boss, you need to keep quite because there is a sword of EMI hanging. What if you do not get an appraisal? What if you lose your job?

Also, you will be compromising with your wealth creation, because you have already consumed most of your future income through loans. Whatever you earn has to go in servicing your EMI’s and current expenses. There will always be less money for future goals, and this thought will keep on haunting you.

Here is a small 6 min short film on the debt trap which happens by use of credit card. It’s quite a simple short film but gives the message

Do not spend the money you don’t have

We all take a few loans in life and that has become the way of life, which is ok. I am not the person who advocates the concept of “Never take any loan” . But surely you need to control it and define the boundaries. If you get into the debt trap, it will be very tough to get out of it.

There are few signals which will tell you that you are too much dependent on debt, they are

More than 50% of your income per month goes into EMI

Your loan outstanding is more than 4 times your yearly income

You have more than 2 credit cards

You have a revolving credit card from last many years

You have too small savings even though you have worked for many years

What you are accepting by taking too much debt

So finally, as a conclusion – When you start depending too much on debt and overdo it, you are accepting that you will be working for money out of compulsion to repay it back. You agree to be constantly living under pressure and feeling frustrated about your debt. You agree to be living a life where you will not be able to take much risk and do what you wish for because you have EMI’s to take care about.

Do let us know how many mistakes are you committing right now in your life? Was this article useful for you?

Did you think that your nominee is the person, who will get all the money legally from your Life Insurance Policy and Mutual funds investments? Ha! That is exactly what you’d think if you aren’t aware of the legal aspects.

We assume a lot of things which sounds like they’re obvious, but are not true from the legal point of view. Today, we’ll concentrate on nominations in financial products.

For whom are we earning? For whom are we investing? Who, do we want to leave all our wealth to, in case something happens to us? It might be your children, your spouse, parents, siblings etc., or just a subset of these. You also might want to exclude some people from your list for beneficiaries!.

So you think you will nominate person X in your Insurance policy, and when you are dead and gone, all the money goes to person X and he/she becomes the sole owner? You’re wrong, dude ! It doesn’t work that way.

Let’s see how it actually does!

What is a nominee?

According to law, a nominee is a trustee not the owner of the assets. In other words, he is only a caretaker of your assets. The nominee will only hold your money/asset as a trustee and will be legally bound to transfer it to the legal heirs. For most investments, a legal heir is entitled to the deceased’s assets.

For instance, Section 39 of the Insurance Act says the appointed nominee will be paid, though he may not be the legal heir. The nominee, in turn, is supposed to hold the proceeds in trust and the legal heir can claim the money.

A legal heir will be the one whose is mentioned in the will. However, if a will is not made, then the legal heirs of the assets are decided according to the succession laws, where the structure is predefined on who gets how much. For example, if a man during his lifetime executes a will.

In the will, he mentions his wife and children as legal heirs, then after his death, his wife and children are the legal owners of his assets. It is essential that one needs to execute a will. It is the ultimate source of truth and replaces the succession law. Nominee can also be one of the legal heirs.

Important

Mention the Full Name, Address, age, relationship to yourself of the nominee.

Do not write the nomination in favour of “wife” and “children” as a class. Give their specific names and particulars existing at that moment.

If the nominee is a minor, appoint a person who is a major as an appointee giving his full name, age, address and relationship to the nominee.

Why is the concept of nominee?

So you might be wondering, if the nominee does not become the sole owner, why does such a concept of “nominee” exist at all? It’s pretty simple. When you die, you want to make sure that the Insurance company, Mutual fund or your shares should at least get out of the companies and go to someone you trust, and who can further help, in process of passing it to your legal heirs.

Otherwise, if a person dies and hasn’t nominated anyone, your legal heirs will have to go through the process of producing all kind of certificates like death certificates, proof of relation etc., not to mention that the whole process is really cumbersome! (For each legal entity! The insurance company, the mutual funds, for the shares, for the real estate..) .

So, to simplify, if a nominee exists, these hassles don’t happen, since the company is bound to transfer all your money or assets to the nominee.The company the goes out of scene & then, it’s between nominee and legal heirs.

Example of Nomination

Ajay was 58 years old who died recently in an accident. As his children were settled, he wanted to make sure that his wife is the sole owner of all the monetary assets. This includes his insurance policy and mutual funds.

So during his lifetime, he nominated his wife as a nominee in his term insurance policy and mutual funds investments. However, after Ajay’s death things didn’t turn up the way he wanted. The reason being Ajay did not leave a will.

Though his wife was the nominee in all his movable assets, as per the law, his wife, along with children, were the legal heirs and all of them had equal right to Ajay’s assets.

One simple step which could have saved the situation was that Ajay should have made a will which clearly stated that only his wife was entitled to get all the money and not his children.

#Nomination in Life Insurance

A policyholder can appoint multiple nominees and can also specify their shares in the policy proceeds. Nomination in life insurance has one limitation, as insurance policies are bought to secure your financial dependents, your first choice of nominee has to be your family members.

In case you want to nominate a non-family member like a friend or third party, you will have to show/PROVE the insurance company that there is some insurable interest for the person. This happens because of a Clause called PRINCIPAL OF INSURABLE INTEREST in insurance.

Note that provision of nomination in life insurance is related to Section 39 of the Insurance Act. Note that as per LIC website

Nomination is a right conferred on the holder of a Policy of Life Assurance on his own life to appoint a person/s to receive policy moneys in the event of the policy becoming a claim by the assured’s death. The Nominee does not get any other benefit except to receive the policy moneys on the death of the Life Assured. A nomination may be changed or cancelled by the life assured whenever he likes without the consent of the Nominee.

Make sure, you have a nominee for your policy for easy settlement of the claim, if you do not have any nominee mentioned in the policy, it can turn out to be a disaster for your dependents to get a claim.

#Nomination in Mutual funds

In case of mutual funds, you can nominate up to three people, who can be registered at the time of purchasing the units. While filling in the application form, there is a provision to fill in the nomination details. Even a minor can be a nominee, provided the guardian is specified in the nomination form.

You can also change nomination later by filling up a form which is available on the mutual fund company website. Nomination in mutual funds is at folio level and all units in the folio will be transferred to the nominee(s). If an investor makes a further investment in the same folio, the nomination is applicable to the new units also.

A non-resident Indian can be a nominee, subject to the exchange control regulations in force from time to time.

Watch this video to know what is nomination in Mutual Funds

#Nomination in Shares

Quiz for you :). Now you know what a nominee means and who actually gets the money. So if there is a husband H, with wife W and nephew N, and he has nominated his nephew N to be the nominee of his shares in demat account, who will have the legal right to own the shares after husband’s death?

If you answer is wife, you are wrong in this case! In case of stocks, it does not work the usual way, if a will does not exist.

In the verdict, Justice Roshan Dalvi struck down a petition filed by Harsha Nitin Kokate, who was seeking permission to sell some shares held by her late husband. The Court noted that as she was not the nominee, she had no ownership rights over the shares.

Ms KokaThe’s lawyer had argued that as she was the heir of her husband who had died intestate (without a will), she should have ownership rights of the shares, and be able to do anything with them as she wished.

In this case:

Ms Kokate’s husband had nominated his nephew in favour of the shares. Justice Dalvi however noted that under the provisions of the Companies Act and the Depositories Act, Acts which govern the transfer of shares, the role of a nominee was different.

“A reading of Section 109(A) of the Companies Act and 9.11 of the Depositories Act makes it abundantly clear that the intent of the nomination is to vest the property in the shares which includes the ownership rights thereunder in the nominee upon nomination validly made as per the procedure prescribed, as has been done in this case.”

It means that if you have not written a will, anyone who has been nominated by you for your shares will be the ultimate owner of those stocks, The succession laws on inheritance will not be applicable but in case, you have made a will, that will be the source of truth.

#Nomination in PPF

If the subscriber dies and there is no nomination at the time of death, the balance in the account, if it is upto one lakh, will be paid by the Accounts Office to the legal heirs of the deceased on receipt of application in Form G supported with necessary documents without the production of succession certificate. If the balance is more than one lakh, the production of Succession certificate will be necessary. (source)

#Nomination in Saving/Current/FD/RD Account in Banks

FD’s also come with nomination facility. While opening a new account, there is a column for nomination in the same form and you should fill it. You can nominate two persons with first and second option. Note that in case you have not done any nomination till now, you should request Form No DA-1 from your Bank which is used to assign a nominee in future. (Examples of ICICI Bank , HDFC Bank) . In the same way to change/cancel the nomination you need to fill up Form no DA-2. Read about Corporate Fixed Deposits

As per a famous case, A Bench of Justices Aftab Alam and R M Lodha in an order said that the money lying deposited in the account of the original depositor should be distributed among the claimants in accordance with the Succession Act of the respective community and the nominee cannot claim any absolute right over it.

Section 45ZA(2)(Banking Regulation Act) merely put the nominee in the shoes of the depositor after his death and clothes him with the exclusive right to receive the money lying in the account.It gives him all the rights of the depositors so far as the depositors’s account is concerned. But it by no stretch of imagination make the nominee the owner of the money lying in the account,” the Bench observed.

Conclusion

Now you know! Taking Personal finance for granted can be fatal 🙂 Just investing knowledge, isn’t enough to have a great financial life. You also need to be well versed with basic legal aspects and make sure you carry out all due arrangement .

Nomination is one important aspect you should seriously consider, when checking for the financial products you have bought or plan to buy in future. Mistakes in Personal Finance

Its important to make sure that your loved one’s do not face legal issues and only say and think lovely thoughts about you when you are not around, rather than crib & grumble 🙂 . Fix your nominee in all the financial products

Today you are going to read 10 truths about your job and why you should accept them and act upon them as soon as possible. We all start our jobs with big dreams and future, but somewhere we are so lost in our daily routine that we do not observe some important things.

This is a guest article by Mr. Hory Sankar Mukerjee, who has been working in the industry for the last 15 years. He has worked with banks, FMCG, media and Information Technology companies. He currently trains people. He is an author for Oxford University Press. He blogs, trains and loves to travel.

So let’s see some lessons which you should keep in mind. Detailed description of these 10 points is done later.

[su_table responsive=”yes” alternate=”no”]

Lesson #1

Jobs are a transactional relationship between you & employer

Lesson #2

Hiring and firing are two sides of the same coin

Lesson #3

You may need to a plan B anytime, be ready with it

Lesson #4

Promotions stagnate at one point, hence invest in yourself

Lesson #5

Start investing your money – Don’t depend on your active income forever

Lesson #6

Don’t get ‘caged’, ‘institutionalized or ‘comfortable at your workplace

Lesson #7

Work on a second income, while working in your current job

Lesson #8

There is a life beyond the job

Lesson #9

Live within your salary

Lesson #10

The biggest lesson – Understand how companies work!

[/su_table]

Lesson #1 – Jobs are a transactional relationship between you & employer

If you ask, ‘why did your organization hire you?’ The answer is obvious. You were probably the best choice, the right fit and there was work for you in the organization. It also implied that the organization where you are currently working has hired your ‘skills’ and have agreed to remunerate you for your ‘time’ and ‘skills’ in exchange for money.

Another hypothetical but obvious logical question, therefore, is: What happens if the organization, ‘does not need your skill set, or you, or your time’? You simply get ‘FIRED’.

[clickToTweet tweet=”Love your job but don’t love your company, because you may not know when your company stops loving you” quote=” Love your job but don’t love your company, because you may not know when your company stops loving you” theme=”style2″]

Relationships in and with organizations are transactional. You can be fired for anything. (E.g.: Global unrest because of North Korea firing a nuclear missile on USJ). Jobs are about: ‘give and take’. You give your time and skills and they give you money in exchange. The day they do not need you, they will not keep you.

Implication #1: Never ever get emotionally attached to your organization.

Lesson #2 – Hiring and firing are two sides of the same coin

You have been hired and you can also be fired. While this was not so common, while my/your parents were working in the government sector, this is true today, especially for private-sector employees.

If your arguments are otherwise and you feel, my sector or my company is the safest, you need to re-think.

Take this example – Teaching is considered to be one of the safest professions. Unfortunately in my career, I have come across many educational institutes, which have fired people on a days’ notice. Across my experience in multiple industries, hiring and firing is just another process for the organization.

The trauma is for the person and his family who have been fired. Firing can cut across industries, roles, skills, technology, and jobs. Firing does not need a reason. Therefore there is no need to ‘feel secure’.

Implication #2: Just as you have been hired, you can be fired. Be ready.

Lesson #3: You may need to a plan B anytime, be ready with it

Jobs, like life, is very capable of throwing ‘surprises’. We may like some of them but would love to dislike most of them. In ‘jobs’ that we are in, we also need to mitigate the ‘uncertainty/unpleasant surprises’. We, therefore, need a Plan B.

PlanB is a plan that you keep close to your chest, (a ‘good’ hidden agenda) while playing a game of cards or a plan which helps the hero of a movie escape in case the rogues have understood your earlier plan. That is your ‘escape route’.

While in a job be ready with your Plan B. It could be teaching, opening a road side restaurant, wedding photography or a rental income. It could also being an entrepreneur, life coach, and writer, encouraging your spouse to work or selling homemade pickles online.

Your Plan B essentially has the power to bring ‘food back to the table’ in case you face the risk of losing your job. It is also capable of taking care of your ‘needs’ during an emergency.

Implication # 3: Ask yourself ‘what is your plan B’? Have you started working on it? Do you have something to fall back upon if you lose your job today?

Lesson #4: Promotions stagnate at one point, hence invest in yourself

Wouldn’t it be great if our employers had granted us lifelong employment, secured jobs, yearly growths, and lifelong benefits? We all love ‘risk-free’ and ‘guaranteed returns’ like our love for FDs, KVPs, PPFs, LICs, and NSCs. However, returns from these like any other investments are either not guaranteed nor risk-free.

[clickToTweet tweet=”There is only 1 investment that gives ‘guaranteed and risk-free’ returns: ‘INVESTING IN YOURSELF'” quote=” There is only 1 investment that gives ‘guaranteed and risk-free’ returns: ‘INVESTING IN YOURSELF'” theme=”style6″]

Any investments that you do on yourself, like walking, hitting the gym, learning new technologies, not eating junk, staying healthy, getting up early, quit smoking, getting certified, learning to cook, getting back to the college to earn a higher degree, learning about stocks and mutual funds, pay you in the long run. Some other day this skill comes very handily.

Let me give you an example

The global head of an organization met me for a coffee and told me about his interest to do a doctorate. I asked him, ‘what motivated him to do that?’ He said, ‘I do not see a future for myself anymore here. Our organization is getting top-heavy.

Promotions are stagnating.

However since I am extremely interested in teaching, (Plan B) I want to quickly pursue it and move into teaching.’ After a year or two, I saw him getting registered into a doctoral program and working seriously on it.’

Implication #4: While you are in the job, do not stop investing in yourself. What is that you wanted to learn and you could not do it? Get back and re-start investing in yourself. This could be your Plan B.

Lesson #5: Start investing your money – Don’t depend on your active income forever

Would you not love it, if your employer kept paying you even after you left the company? Wow…I would love to die to join such a company.

But it never happens.

The money that you earn not only takes care of your today but also takes care of your tomorrow when you stop earning. (Retirement)

Earning is essential but not sufficient. It loses value. Start investing. Investing helps to save you from the rainy days of your future. Saving and investing, therefore, are not one and the same.

When I started working in 2003, had I invested Rs 1000 a month, in Franklin India Bluechip Fund, the fund value today, would have been Rs 5.4 lakhs. Unfortunately I did not.

I did invest. But the investments were in ‘stupid financial products’. Choose the right products. When you need term insurance, do not buy a traditional life insurance policy. When you do not have the expertise to invest in stocks, invest in mutual funds.

When you do not need a house, do not take a loan to buy it, especially when you are young. There is no dearth of financial products. But choose the right ones, which you understand.

Lead a frugal life.

Frugality is not depriving yourself.

Frugality is living simple and with a minimal. Many rich people are known for their frugal lifestyle. Frugality has its own advantages. The best of course is to ‘achieve financial freedom’.

Showing off could be deadly. Make a list of things ‘you have bought’, which you never made use of. It will throw a lot of surprises. Remember that an elephant has two sets of teeth. One is for eating and the other for a ‘show-off’. It gets ‘killed’ for the one it shows off.

On a thumb rule, invest (not save) what you spend.

Implication #5: Saving money is useless unless you invest it. Even more useless, is to save in the wrong set of products. The most ‘useless’ thing, is planning to invest after you have spent. Trust me you will never be able to.

Lesson #6: Don’t get ‘caged’, ‘institutionalized or ‘comfortable at your workplace

Three things that kill employee’s morale, growth and prospects of doing great. First is getting caged, second is getting institutionalized and third the idea of being comfortable at work. Let us understand them.

Caged: ‘Who will hire me after 10 years in the banking industry? I am lost and I cannot get out of this mess. Even if I want to, my family problems are not allowing me to.’

Institutionalized: ‘I am so comfortable with this place that I do not feel like changing. This company gives me respect and I am happy. Everyone knows me in this company. Let it go on. I am planning to retire from this place.’

Comfortable: ‘This place gives me peace. I am happy doing whatever I am doing. I do not want to change. It is the same soup everywhere. Why do you want to change, when things are so good here?’

Getting caged, institutionalized and being comfortable is when we set boundaries to ourselves. We are unwilling to try new things, find new solutions or unwilling to look beyond the ordinary.

Remember that the relationship with the organization is transactional. The day they do not need us, we are all gone.

Physical boundaries, mental and emotional boundaries tie us up.

A couple of my colleague’s hometown is in Kolkata. They intend to settle in Kolkata, post-retirement, however, they have bought homes in Gurgaon, where they currently work. Some of them are getting better opportunities in other cities of India, are unable to move, because of their emotional attachment to their newly-bought houses. (And the banks’ love for their home loan interests.)

Implication #6: Set yourself free. Do not get attached to your organization and look beyond the boundaries. Any change will initially bring discomfort and then things will settle down. You will then start enjoying it.

Lesson #7: Work on a second income, while working in your current job

My father retired from the Indian Army without a job in hand. In those days, getting a job was difficult. One day while he was worried, my mom said, ‘Why are you worried? You should not be. I have mine and that will be good enough till the time you do not find another one.’ This comforted my father. However, within 3-4 months, he got a new one.

The lesson to be learned is that, a second income is not bad. It gives you a cushion. This is very true especially for people with non-working spouses. Second income, gives you some extra luxury, some extra investments, and faster financial freedom.

Remember not to splurge the extra income that you generate, but invest a significant part of it. Also, ensure not to overburden yourself with that ‘extra work’. It should be something that you would enjoy doing.

Implication #7: A second income is great. It gives you comfort, extra savings and after all a place to fall back upon in cases of emergency. In a world of uncertainty, this is surely a cushion.

Lesson #8: There is a life beyond the job

The work that you do was there before you joined the organisation. The work will be there after you leave. Work will never get over. Therefore there is no reason to panic. It is not a sprint, but a marathon. Have a life beyond the office. Spend some time with your GF, spouse, family or children.

They are the ones who will support and cushion you in your bad times. Spend some time in a week doing charitable work, teaching the poor, helping your wife cook or taking your old parents for a walk.

It will help you learn ‘life skills ’and make you more ‘humane’. Someone had asked Dalai Lama, what surprises him the most. He said, ‘Man…Because he sacrifices his health in order to make money. Then he sacrifices money to recuperate his health.

And then he is so anxious about the future that he does not enjoy the present; the result being that he does not live in the present or the future; he lives as if he is never going to die, and then dies having never really lived.”

Implication #8: Family is equally and more important than your job. Your work can wait. The time that you did not see your child grow up, will never come back.

Lesson #9: Live within your salary

Jobs and salaries do not imply living beyond your means. It gives you a right to spend, but not the authority to splurge. It is not only about you, but the ecosystem supported by your salary- Spouse, child, parents, grandparents, maid, milkman and the driver.

It also does not authorize taking more loans because the banks are willing. It also does not authorize purchasing five shirts or trousers, when you already have ten. Living a life, ‘paycheck to paycheck’ is risky and unworthy. It disturbs the ecosystem surviving on you.

Keep it simple – One house, one car, one bank account, a few shirts and trousers, one credit card, one debit card, one health, and one term insurance. Spend all the remaining time that you are left with into something more meaningful.

Every Diwali, when the newspapers are filled with offers and bargains, ensure that you are not the ones jumping in to buy. When you buy at a discount, you save, 50 percent, but when you choose not to respond or buy, you save, 100%. Ask, ‘Is it really needed?’

Implication #9: Debts are needed but not at the cost of destroying our mental peace.

Lesson #10: The biggest lesson – Understand how companies work!

The day Cyrus Mistry was fired, I learned the biggest lesson of my life. If a person of his stature can be fired, we are no one at our jobs? For the organization, we are dispensable.

If we feel that we are ‘assets’ for the organization we work with, the organization may think of us as an ‘ass’ (minus the ‘et’). After all, organizations are run by people. People change and so does their culture, values, and priorities.

Implication #10: Stop treating yourself or pretend to treat yourself as an asset and make sure you understand the realities of working with an organization.

Can you add another point?

I would like to know if you have any more point from your side? Can you add the 11th point in the comments section?

The year 2017 is coming to an end and I would like to share some of the common mistakes which I have witnessed in some investors financial life.

You can never have a perfect financial life but you can always live a regret-free financial life. I take this opportunity to thank those who opened up their heart while I was helping them in designing their financial life.

While you are reading the article look into your own financial life and keep your own financial life under a scanner.

The person works in a bank and at that time he was least interested in having his own health coverage. In 2017 he calls me and says, “I have got a serious health issue, cancer detected in my kidney and doctors have suggested me to cut a portion of my kidney”.

He said, the Bank is ready to give only 3 Lakh and the actual expense is of 8-10 Lakh. He requested, can something be done to buy a backdated health policy to which I said NO.

There are many people who rely heavily on their company health cover and sometimes end up paying a huge cost. One illness and it has the power to eat away all your savings. See that you are having health cover of your own.

Mistake #2 – Addiction to credit money or loans

You see so many advertisements these days talking about buying things on EMI and low-interest rates offered on personal and credit card loan. One of our clients tried to learn the craft of shuffling money using different credit cards.

He will take a loan from Credit Card A and then use Credit card B to pay the outstanding. Initially, he got some success but eventually, he got into a debt trap. He was already having a home loan and car loan while discussing his plan we suggested him not to add any more liability and to stay away from credit card and personal loans.

He did not listen and eventually, he had to stop his SIP, his savings got NIL and is now regretting.

Mistake #3 – Overspending because of Social Pressure

One of our clients kept aside 30 Lakh for his daughter’s marriage but eventually ended spending 70 lakh. All the extra spending took place in the name of “trying to look good”.

Under the pressure of relatives and on the name of customs, he ended up spending heavy money. The extra money spent took almost 10 years to accumulate and it was part of his retirement corpus.

I see many buying a bigger house, a bigger car etc to show they are successful. It’s time to get rid of such social pressure, as no one is going to come to fund your retirement or future goals.

Mistake #4 – Heavy Spending Habits

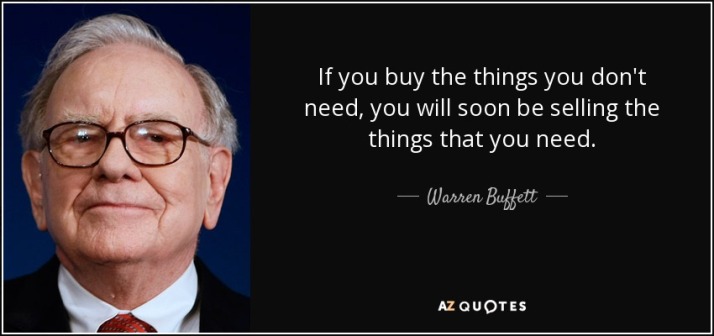

A lot of people like to spend on gadgets and things which they really do not need. As Warren Buffet once said, “If you buy things you don’t need, very soon you will have to sell things which you actually need”.

The words and advice by him are precious and everyone should check their spending habits. What are you spending your money on? And what value is it creating in tangible form? Stay away from instant gratification and impulsive buying habits.

It can be buying an expensive gadget, Treadmill or some fancy home equipment.

Mistake #5 – Over relying on Robo Advisory

There are many Robo advisory companies in the market. Now, using technology is not a bad thing but one has to check the quality and not the price of using some platform.

A few months back I accidentally happen to get on call with a person called Shubham Kapoor (his actual name), he said he has got some advice from robo advisory firm and he is not confident about his Mutual Fund investments. He shared his portfolio with me and the funds suggested were all shit. I immediately asked him to take corrective actions.

His current portfolio is designed by me and the funds are doing excellent. As I was writing this article I asked him to share his experience and he immediately shared his experience with me. I have not edited a single word, we do not hold any grudge against any robo advisory firm but at the same time it has to deliver quality advice.

Hey Nandish,

Hope you are doing good, my experience with Robo advisory is underlined…..feel free to edit

” After Reading through numerous blogs mentioning the benefits of fee only financial planners I came across a Robo advisory firm (Let’s call it ABC ) which guaranteed Advice free from any Bias and manual intervention. I agreed to the concept and after paying the fee plugged in my input details in their software tool.

The financial advisor from the firm fixed up a meeting with me via skype and the suggested portfolio to me(Auto generated) carried out 8 MF’s(SIP in total was 20K/month).I was not comfortable with the cluttered portfolio and also with the choice of funds.

after deliberating for couple of months, I went ahead with the suggested MF’s as it was Robo advisory which hopefully knew better than me!

the review was six monthly and every time my question on choice of funds(as they were performing very poorly compared to benchmark) were unanswered, the responses were vague and confusing.

I was not expecting immediate gains but after 3 such reviews in a period of 18 months i was still not getting the comfort and trust level, this is when I decided to stop my investments via them.

I am still baffled whether suggestions made through Robo Advisory were free from any bias or whether they were for their own commissions, your call!!”

Now, if you are investing your money with help of a robo advisor or a real human advisor, you have to make sure that there some quality advice delivered to you and some alpha is generated (extra performance, which you can’t bring on your own)

Mistake #6 – Getting attracted with FREE advice

This one is my personal favorite, many people get tempted to free advice.

It comes from the person known to you, your relative, your friend or some uncle who calls himself or herself your well wisher. One of my relative sends a pdf to me on whats app to check whether he should continue with his ULIP policy or not? The ULIP was sold as free advice.

I and my team did some working at our end and sent below email to him.

Hi XXXXX,

The return given by Reliance ULIP policy is only 6.75%. ( Extremely bad performance). You have accumulated only Rs. 354591/- after investing 3 Lakh

The policy has no loyalty benefits nor any extra benefits. If you complete whole policy period, the return will be equivalent to FD.

If you would have done SIP of 5500 per month for 57 months you could have accumulated Rs. 392000/- at the rate of 12%.

SA is only 15 lakh ( It is not giving you any higher cover)

Coming to charges:

Upfront charge is 6 % as premium allocation charge. You paid 3 Lakh and they have charged upfront Rs. 18300/-

Fund Management charges, mortality charges is around 4 % annually. These charges gets deducted from the amount accumulated at the yearend.

Better to come out of this policy as it has completed 5 years ( in this December) and there is no lock-in

Nandish

Guys, there are no free lunch in this world, go to a professional and look for authentic advice (if you cant take it on your own). Sometimes we also go wrong with a few suggestions/advice but the intention is never wrong. If you are taking free advice from some website, Facebook group, whats app free group stop the same immediately.

Mistake #7 – Thinking that DIY is for everyone

There was this one person who was on our client list and on one fine day he decided he will start managing his money on his own. I was happy with his decision but somewhere I was not sure about his money management skills.

I had many plans for him on how I can help him to grow his money but he concluded things very fast. He read a few books, did some seminars and is also active on various blogs and forums.

His portfolio grew from 0 to around 75 Lakh in a span of 7-8 years. I do not have his current numbers but if the portfolio is not taken care of his profits will get eaten away by the market.

I have seen people losing huge chunks of money because they focused on buying 5 star rated funds but somewhere forgot to control the risk on their portfolio. You don’t just need to learn the craft of money management but you also need to master it.

In India every Indian is a teacher, preacher, financial advisor and a doctor. Just ask any 5 colleagues about , “How to reduce weight? and you will get different answer from all sides” .

There is no athlete in this world without a coach. If performances matters you can’t do it with DIY model. You can take a few decisions on your own but cant paint the entire picture on your own. DIY is for a set of people who have high understanding of subject, great control over their decisions making, and a lot of passion and time.

Mistake #8 – Start-up ka bhoot

I remember when I and Manish started our business.

I asked Manish to continue with his job till we are not 100% confident about our venture. In Jan 2011 finally he decided to leave his job and got full time into blogging and writing. I have worked with a few entrepreneurs who jumped into business without any homework on personal finance front.

I always feel business is about taking risk, it is always like a free fall. My only request is, do not get overwhelmed by your business idea and do not mix your personal finance with your business journey. It’s not always compulsory to leave your well paying job and start a business because its “Cool”.

Final words

The year is coming to an end and it’s time to embrace your financial mistakes. In just a few moments the page will turn and we will step into the year 2018. Don’t be afraid of making mistakes but at the same time have courage to accept your mistakes and work on them.

Wealth creation is all about becoming honest with your own self in the area of money. If you wish you can share some of your mistakes of 2017 and fresh commitments you are ready to make in 2018.

Thank you, each one of you for being our partner in spreading financial awareness. There is a lot more coming up in the coming year and we look forward to your same love and partnership.

From last 8 yrs, I have been talking and dealing with investors & I can see some progress on how people see their retirement these days. They have got more “serious” about retirement planning.

Almost all the clients we have, for them retirement is a big goal and their focus on it is worth appreciation. But that’s a very small number, few hundred may be.

If we talk at the mass level (All India level), there is almost no seriousness for retirement planning. At the mass level, people are very short sighted and plan for their short term goals, but not “long term goals”

5 reasons why investors don’t plan for their retirement?

What about you?

Have you started your retirement planning?

Is some money being invested for retirement goal each month?

By “Retirement planning”, I mean a well thought investment plan (it might not be written) for your future. Are you consciously thinking about create a big enough corpus at your 60, which will support you for next 30-40 yrs?

Please do not confuse “retirement planning” with buying some random policy for your 80C deduction, which had a word “retirement” in the name. It’s mostly a well marketed product sold to you on the name of retirement.

Now, let’s see some of the top most reasons why people don’t invest for their retirement seriously!

Reason #1 – It’s a “Selfish” Goal

I recently attended a session where the speaker asked this question – “Which is the most important financial goal of your life?”

To this, there were many answers like ..

Retirement

Children Education

Buying a House

Getting Debt free

Stating own business

Daughter Marriage

But the trend was clear… “Retirement” was not in majority.

The group age range was between 30 – 50 yrs. The speaker was silent for a moment, but then he said something which really hit me.

“Most of the people know deep down that Retirement is their biggest goal, but they refrain to accept it because it’s a SELFISH Goal”

Planning for Retirement is a “selfish goal”

Yes, retirement is about you and your requirement. Your retirement is the most costly financial goal and long duration goal, which will have to be provided for not just years, but DECADES.

It feels very odd to openly accept this and say this, especially in a society where we are always taught to first provide for others and think of others needs. We are taught from childhood that we should not think about yourself, we should not be self centered, we should think about others, we should think of others before thinking about yourself.

“Others” here can be our parents, children, friends, relatives, husband, wife or anyone else.

It’s a taboo to tell someone that “I want to first think about my own happiness and requirement at the cost of others”. You suddenly become “self-centered” and “rude”.

This is one major reason why a lot of people think of their own retirement at the end, only when other goals are planned for.

I think this is changing slowly and the way people are prioritizing things is slowly taking a new shape. I can now see a trend, where people have started giving importance to their own dreams and desires, compared to our parent’s generation.

While, you plan for important financial goals of your life, like buying a house, your kid’s education, children marriage etc, you need to give first priority to your own retirement.

It does not make sense to not plan for your own retirement, at the cost of other goals.

Reason #2 – Because it’s too early to plan

Imagine you are 30 yrs old.

It’s been just few years since you started your career. The top most thing in your mind right now is “how to buy the house?” and how to get the better pay package in the next job?

You are so engrossed into the hustles and bustles of life, and suddenly something says to you “Are you saving for your retirement?”

“Dude, I am just 30” – You feel !

Let’s be honest, it’s very tough to get serious about retirement at such a young age.

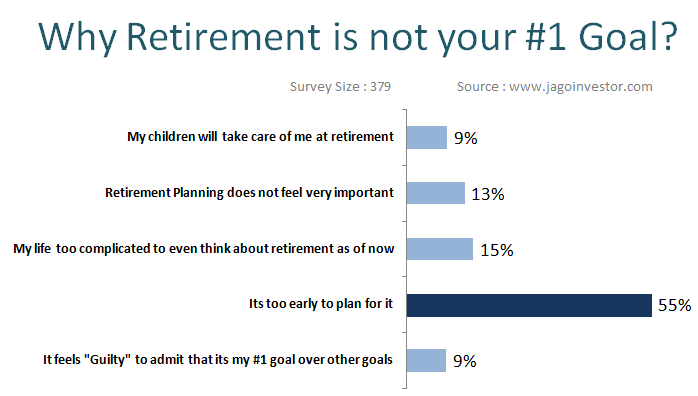

Some days back, we did a small survey with 379 people where we asked them what was the biggest reason why they did not consider retirement planning as their #1 goal in life, and the top most reason they choose was “It’s too early to plan for it”, the average age of this group was 30.4 yrs.

Most of the youngsters never get out of that “I am still young” mode for decades. And one day when they hit 40-45, they feel they made a mistake of not starting early. Some people realize this at 50.

And then by that time, it’s very late.

So even though your retirement is very far away, you need to get this once and for all that you would need a big sum of money at the end, and early you start, better it is. You might not give high priority to retirement saving in the start, but start with something at least and increase the allocation later in life as you move from 30 to 40 .. and so on.

Reason #3 – They are not able to visualize the “Retirement” goal

We all are very bad at predicting how our lives will turn out to be after 10 or 20 yrs old. Just think about your past for a moment. 10 yrs back, did you have even a slight idea of how your life would have been today?

Not at all!

So it’s tough to predict how good or bad the future will be.

This is the reason, why most of the people do not plan for retirement. They are not able to visualize how serious it is to plan for retirement and how tough it will get if they do not have enough retirement corpus.

Most of the people who earn sufficient money right now never realize that one day the SMS – “Your salary XXXX amount has been credited in your account” will permanently stop and they will be left with another approx 40 yrs to be alive.

Your health will not be at the best level and your kids may not be in position to take care of you in the same way you imagine them to take care of you. They will be busy and struggling with their own life issues.

It’s not easy to look far ahead in future and visualize it especially when you have a very active income right now. Just like its very tough to image how it feels to be hungry, when you are easily getting 3 meals each day.

There are various examples of successful people who died poor and struggled in their retirement life. If you do not have enough money in your retirement, you do not have power with you. People do not treat you well, and that’s the harsh reality of life.

Don’t be that guy !

Subra has written a great piece called “Retirement Failure”, where he talks about how a retirement life looks like, if you do not have enough money at retirement. He is one of the best authors and writers on the topic of retirement, so you can trust him 🙂

So start getting serious about future and plan for the D-Day !

Reason #4 – Not able to save enough money

People also don’t save for retirement for the simple reason that they just don’t have any surplus left at the end of month. It’s fairly logical!

Incomes are not increasing, while expenses are growing like amoeba in all directions. It’s getting tough to save in today’s times especially if you are single earning member in family with 5-6 people in a big city.

It’s true that you are not able to save much, but that’s something to get altered to and act on it, rather than hide behind that fact and just let years pass by.

Just because you were not able to save enough for future, no one is going to give you money at your retirement.

So take charge of your future now, and act on it. Work on your income, work on your expenses and make a start. Start saving with Rs 1,000 a month first, then Rs 2,000 and eventually go up and up.

Even if you are able to save Rs 5,000 or Rs 10,000 a month at minimum, a good retirement corpus can be generated. You will not be a RICH guy, but you will have something to fall back on at least.

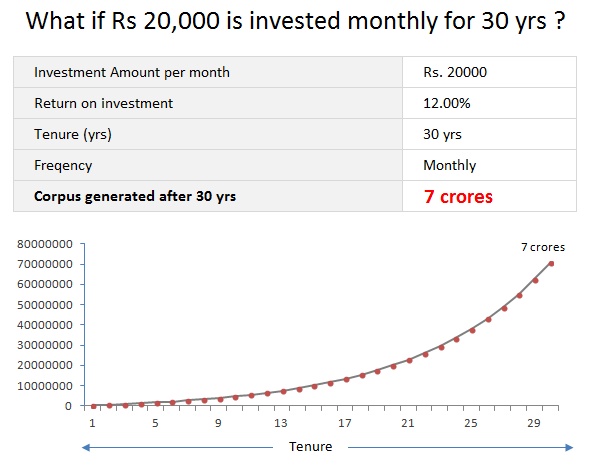

What can you do with Rs 10,000 per month?

Below is a graph which shows you the power of investing Rs 10,000 per month on a regular basis for next 30 yrs. You can create close to 4 crore at retirement if you are a 30 yr old person.

It can be a slow start, but that’s OK.

If you want to talk to our team for your retirement planning, just leave your details on this page and our team will call you to discuss about your retirement planning.

Reason #5 – They see their kids as retirement corpus

I am not giving my own comments on this point, it has to be written by you.

Yes, I do not want to give my comments on this point because it’s such a sensitive topic that various people will have very different style of thinking on this topic.

From my side, I can only say that I can see lots of people in big cities these days who are very clear that they do not want to depend on their children for anything. They want to give the best to their kids and raise them as amazing people, but then they do not expect anything back from them.

But from the small city I have come from (and many of you) , it’s almost a crime to think like that. Most of the people really see their children as “Budhape ka Sahara” and literally expect them to take care of them “because” they have also raised them and spend on them all their life, so it’s now their turn to return back.

How do you see the relationship with your kids?

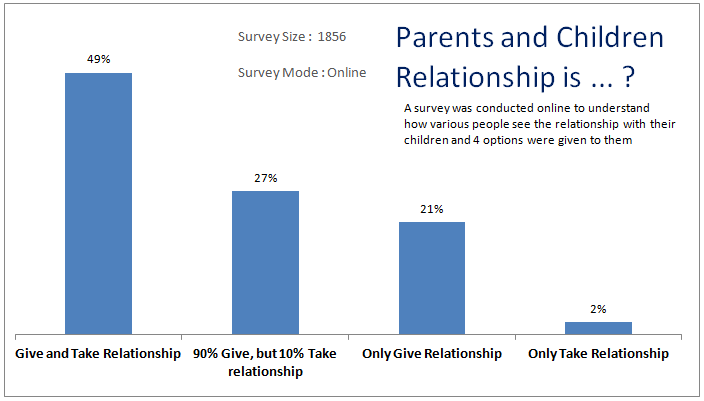

Few months back, we did one online survey on this website to understand how do people see their relationship with their children. 49% participants in that survey choose the option which said “Give and Take Relationship”, where as only 21% felt that it’s only a “Give Relationship”.

I can’t comment if it’s right or wrong, but would like to know from everyone, what they feel about this point? Please expand this 5th point in comment section and have some fruitful discussion.

If you are living in a rented house and using any fake documents for HRA claim then be careful.

Because from now on there will be a big trouble for those who are using fake rent receipts to claim HRA, as Income tax department have started asking for more document.

Many times it is seen that people claim for HRA by submitting fake rent receipts. This also helps to get them tax benefit. But now as there is increase in the number of fraud HRA claims, IT department has started to ask for some other legal proofs.

Documents which IT department can ask in case of verification

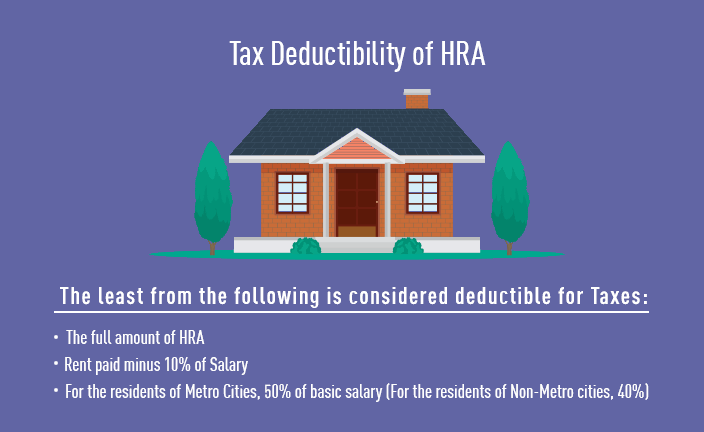

Before you know about the documents needed for verification purpose, lets understand what is HRA (for those who are new to this)

HRA i.e. House Rent Allowance is an amount or we can say a part of salary of an employee which an employer pays if the employee lives in a rented house. It is beneficial for the employee as it lowers the tax which he/she pays on accommodation per year.

If you claim for HRA exemption then you need to submit some legal documents like a receipt or an agreement and ID proof of landlord. You can also claim for HRA exemption on your income tax by filling 12BB Form

If the IT department suspects that a person is providing fake receipts for HRA then they can ask for some other related documents. The list of documents which IT department can ask is as follows –

5 documents which IT department can ask in case of verification

Copy of leave and license agreement

Electricity bills

Water supply bill

Agreement or a letter from housing society

PAN card of landlord if the amount is above Rs.,1,00,000.

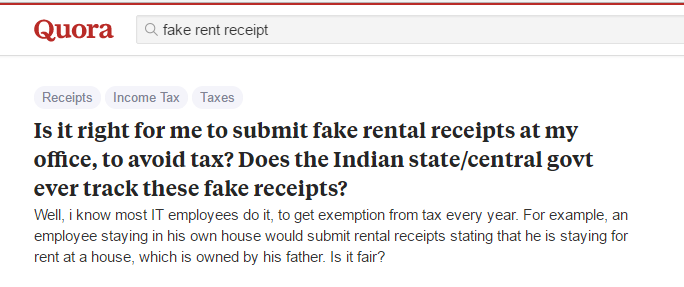

Is there any risk in submitting fake rent receipts to claim HRA?

People are asking various question related to fake rent receipt. You can see the snapshot given below…

The verification process is going to be more strict day by day so there is a risk in claiming for HRA exemption by providing any kind of fake documents. If a person wants to apply for HRA with fake receipt by knowing all the risks he has to prepare all the fake documents and as we know submitting each and every document fake is not that much easy.

In many cases employees asks their parents or relatives to sign the documents for HRA claim or sometimes employees shows the higher amount on their rent receipt than they actually pay so that they can get the exemption. In case IT department suspects your case as fraud, in that case you will have to go through verification

Some example where enquiry can happen

If a person has a house loan and also applying for HRA.

If a person living with parents without paying any rent but still apply for HRA and says that he pay rent.

Adding higher amount in receipt than he actually pays.

To know about this in detail you can watch this video..

IT department has stared cross checking the address on ITR ( Income Tax Return) form and the receipt submitted. They are also checking the records so that they can know who is the legal owner of the house to verify the Leave license agreement.

What are your thoughts on this issue? Do you know anyone who is submitting fake rent receipts?

This article is a guest post by one of our readers Vikram Agarwal, who wanted to share his experience on the concept of “Early Retirement”. Vikram was generous enough to share his story and some of the real-life things which will make you think hard about this concept. Like Vikram, if you feel you can write on jagoinvestor, please click here

Over to Vikram.

—

Most of my friends in my friend circle in late 30’s ask me one question – “How much money I should have now, so that I don’t have to work anymore while maintaining a decent standard throughout of my life, with all the future expenses taken in to account?”

They want to ‘Retire Early’

In fact, I also used to be an ardent follower of the concept of ‘Early Retirement’ but now have realized that the concept is more like a mirage, which does not exist in reality and once you reach there, it vanishes.

Moreover – in my view, it is quite dangerous for an individual to run after this concept. In my opinion, you achieve retirement either ‘NOW’ or ‘NEVER’ irrespective of your current level of income or financial state.

Early Retirement is a state of mind

It is a state of mind, rather than a stage achieved. The moment you achieve early retirement as per the physical criteria set by you five years ago taking inflation, life expectancy and all major and minor expenses in your monthly calculations, by the time you achieve retirement as per your old financial definition, all those things become sub-normal or default.

Your mind will have another definition that looks normal for you in today’s context for example for future kids’ education, your house quality, the type of car you own, facilities you desire and all other such expenses.

My personal example

For example, five years before, owing a 2 BHK house in the newly developed area with Marti Dzire hatchback car and with the kids going in a decent school used to be a life I wished for and I had done calculation for the amount required to maintain the same standard throughout rest of my life without working.

And that was ‘Early Retirement’ according to me and as per standard definition.

But, now it seems owing a 3BHK house (one extra room for parents or for guests) in a good location of a metro city, a nice Honda sedan and a ‘good’ school for kids throughout their education duration is ‘Normal’ for me. Now it’s the standard, I would like to maintain before retirement and after retirement.

My next target!

My new “target” might be owing to a villa or bungalow, and a nice SUV and kids in the ‘best’ school of the area. And once I achieve it, I think it will become a new normal with time.

The next level

And who knows, a car for wife will be a standard I will look for in the future, as I will not be able to manage all the household activities on my own and an extra car becomes a necessity. (I did all my retirement planning calculations with taking decent return on investment as 10% which is quite modest in the long term, so as not to fall in the trap of exuberant returns which might be temporary and actual return might spoil all your calculation.)

Even with a slight increase in any of the above ‘wish’ list (like the possibility of sending you kids abroad for his or her graduation) will push you back in time and you will not be able to achieve you ‘wished’ retirement any time and this carrot and stick game continues.

When your desires convert to your “needs”

You would not know when your ‘desires’ got converted into your ‘needs’. And now it looks like there is a meaning in the sayings of wise old man that “There is enough in this world for one’s needs and not for one’s desires”. I can sense the truthfulness in these lines with some financial literacy and practical experiences.

If at all early retirement could mean anything for a ‘disciplined’ guy is thru’ a windfall gain from lottery or legacy, otherwise if one tries to achieve early retirement from normal gradual process where mind and hard work is involved, his thinking mind will quickly adapt to current situation and will turn the old desired standards in to ‘Normal’ or ‘Below Standard’ life in today’s’ terms.

The word ‘discipline’ need stress here because there is an old saying that irrespective of the size of the pot, if kept isolated all the water will drain out eventually if not refilled on time and only a disciplined life can control this drainage process and can prolong it (Read, why we are overspending these days by Manish)

Or you can become a hermit in deep forest, secluded from this physical world and concepts of ‘Future Expenses’, ‘Inflation’ become meaningless for you, one can think of early retirement stage.

But, I guess this is practically impossible and this article is not intended for those who might be thinking of this stage as one of their future possibilities.

Story of my seniors – Real-life case

I personally know two of my seniors who after working at very senior positions in the company left their jobs as they thought they had enough money to sustain the rest of their lives and tried to follow new pastures in future life.

But, eventually, they had to join back in their respective jobs in order to meet their monthly bills and continue with their other passions in life.

It is human psychology to get adapted to the current situation and at present it looks like achievable calculations on paper and unreal confidence of being satisfied in case you achieve current target, but in reality it does not happen and by your own nature and human being’s reason of existence, you will always be pushed to work.

Basic foundation of human existence is WORKING

This wish of ‘ Not working’ one day will take you away from ‘Karma Yoga’ which is the basic foundation of human being’s existence. Even in GITA, it is mentioned that all of us have to work one way or other and this is the law of life.

I remember a recent discussion with a prominent businessman in my home town. He told me that he used to ‘struggle’ a lot to book rooms in his locality for any private family functions for his guests they had to ‘adjust’ sometimes as per hotel terms and conditions.

Now, he has built his own guest house and no need to be ‘dependent’ on the hotels any more for bookings, etc. and I was thinking that if this rich man thinks booking rooms in 5 star hotels as per their terms and conditions is a compromise in life, what independence could mean for him ?

Don’t buy anything less than a BMW

A few years ago I was having a discussion with one of my friends and in his views, having something below Mercedes or BMW is a compromise as all other brands do not give importance to safety standards and life is precious more than anything else.

At that time owing a Honda city and maintaining it was the kind of life I wanted to live for all early retirement calculations and now since I can afford Honda City easily, I have a choice, either to keep working to be able to buy Mercedes or BMW one day or put my life always at risk while driving mass-produced cars!

We can retire the day we are BORN

On second thought, I achieved financial freedom years back, the moment I had enough money to be able to afford public transport all through my life. In fact, to take it to one extreme side, we have the potential to retire the day we born and it is only afterward that we enter into the working force in this world, fall into the financial trap and again want to get rid of it.

This wish of ‘Not working one day’ can make you lazy, averse to work and afraid of accepting challenges as in your thought process you are always after something else and it is quite natural that you will not focus on the very basic aspect of life you want to get rid of one day.