Let us understand the features and benefits of this account.

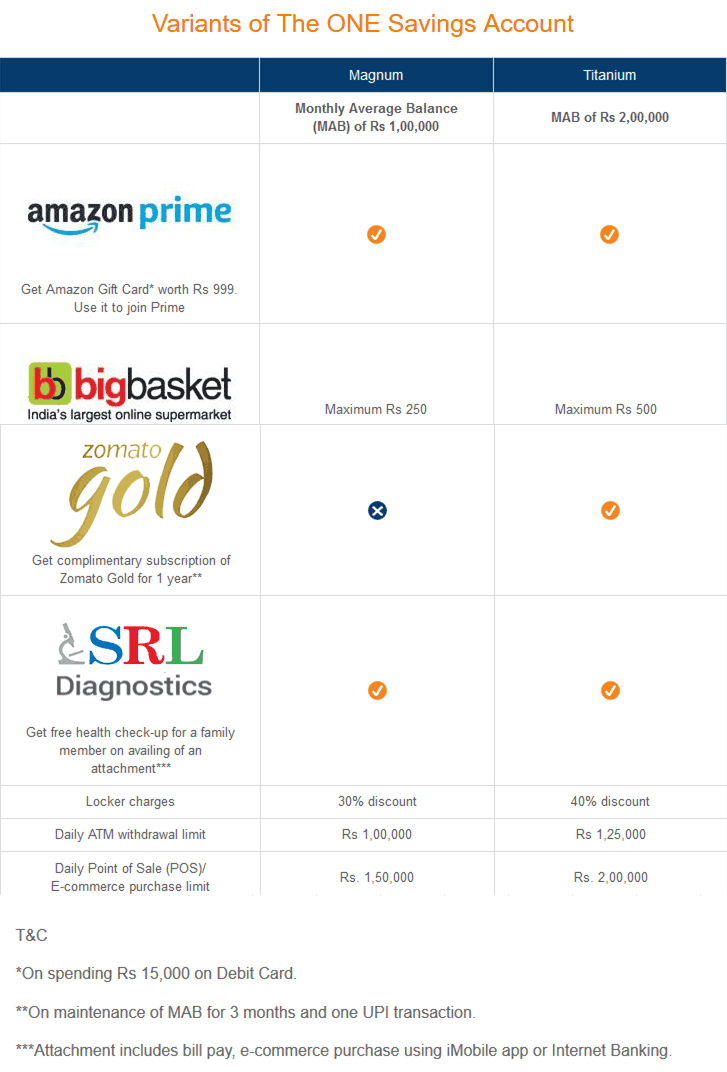

Minimum Balance and Eligibility requirement

Any salaried or self-employed individual can apply for these accounts as per eligibility criteria. It’s not applicable for companies, Hindu Undivided Family or any other corporate body.

There are two variants to this account called Magnum and Titanium. Below are the balance requirement and more details.

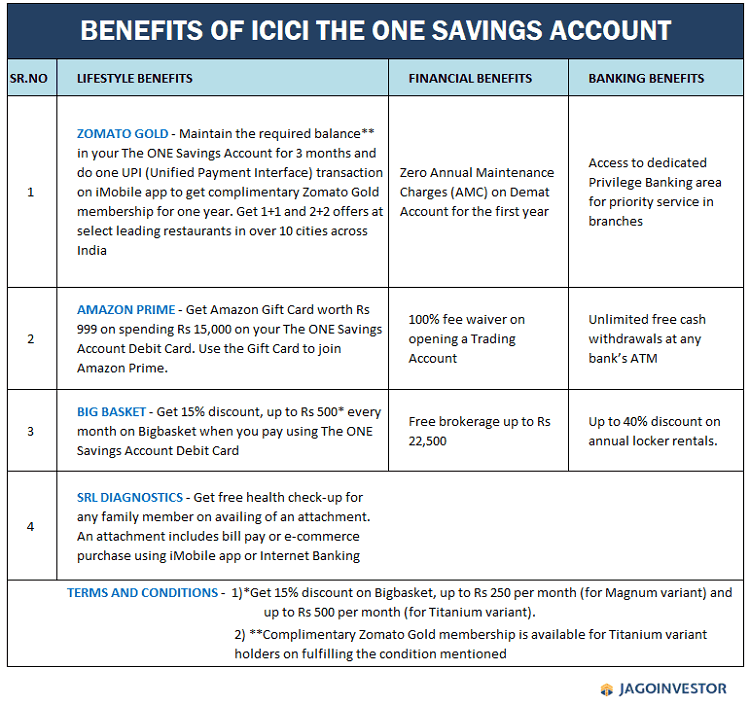

Benefits of this account –

There are a various lifestyle, financial and banking benefits of this account. They are as follows –

Zomato gold subscription of 1 year

Big basket discounts

Amazon prime subscription of 1 year and many more. Below are the complete details of the benefits of this account.

Conclusion

Note that you need to keep a high account base in your saving bank account to be eligible for these benefits, so in a way you are also loosing on the interest part which you could have potentially earned. So keep that in mind, and then take the decision if you want to go for this or not!

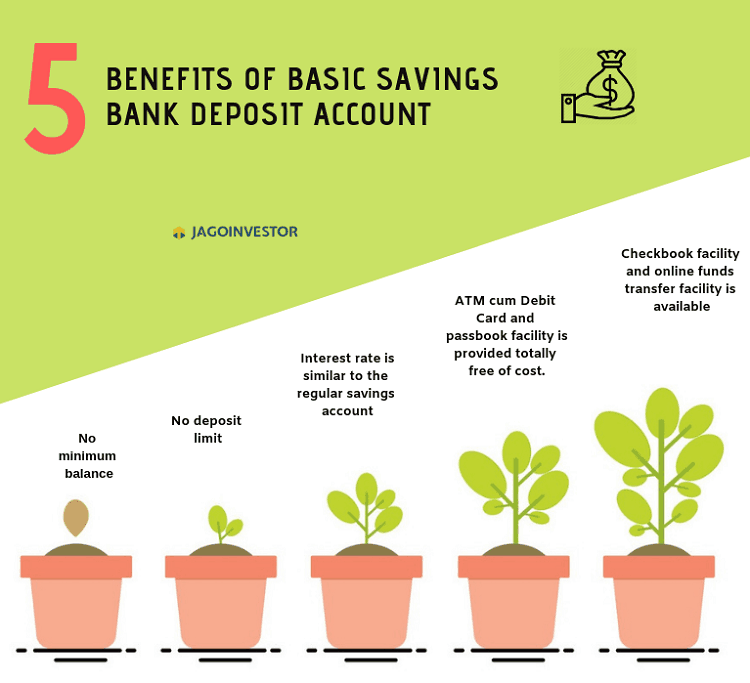

Do you worry about maintaining the minimum balance in your bank account? If that’s the case, then you will be happy to know that now RBI has mandated all the banks to offer something called Basic Saving Bank Deposits Accounts where there is no minimum Monthly Average Balance (MAB) to be maintained.

Let’s know more about the BSBDA account.

You must have heard in the news that a few days back, Banks have collected approx Rs 11,500 cr from customers for not maintaining minimum balance limit. This situation happens with a lot of people. Through this article, we will see how we can prevent ourselves from getting into this situation.

Basic Saving bank deposit account – Meaning

The basic savings bank deposit account (BSBDA) is the zero balance bank accounts. This means you don’t need to maintain any kind of minimum balance limit in this account.

RBI has made it mandatory for all the banks to offer this service to people who are unable to maintain the minimum balance. Criteria to open this account are similar to the eligibility criteria of normal savings bank account. Banks may have their own criteria based on age or income.

However, as per the guidelines of RBI, banks are advised not to impose any criteria of age or income for opening BSBDA.

Features of Basic Savings Bank Deposit Account :

No minimum balance limit.

No limit for a money deposit.

The interest rate is similar to the regular savings account.

Normally there is no upper credit limit (these criteria may vary from bank to bank).

No minimum amount required for opening the account.

ATM cum Debit and passbook facility is provided totally free of cost.

Checkbook facility and online funds transfer facility is available.

No charges are applicable to any kind of transaction (within limit).

As I said earlier this is a zero balance account with no extra charges, but it has some limitations also :

Only 4 withdrawals per month are allowed, including branch cash withdrawal, ATM withdrawal, NEFT, RTGS, online payment, EMI, etc.

It depends on banks to either charge additional fees for extra withdrawal transactions or not.

Your BSBDA will be converted into a normal savings account automatically if the transactions limit increases.

Central KYC (A centralized KYC process to avoid submitting multiple KYC’s) should be done, otherwise, the account will be considered as a BDBDA-small account (explained below).

What is the Basic Savings Bank Deposit-small account?

This is an account that can be opened by a person who is above 18 years of age but does not have any official KYC document (Like Aadhaar Card, PAN or other ID proof and address proof, etc.). For this, a person needs to submit a self-attested photograph and he/she needs to sign the form and also provide thumbprints in the presence of bank officials.

The basic savings account of a person who doesn’t have a CKYC is treated as a basic savings bank deposit small account. Features of this account are as given below :

This account is valid only for 12 months. It can be extended for the next 12 months by providing proof of having applied for officially valid documents.

The balance should not exceed Rs.50,000 at any point.

An aggregate of all credits in a financial year should not exceed Rs.1 Lac.

Mobile banking facility may not be available.

Can I convert my existing savings account into a Basic Saving bank account?

There is no provision till date to convert existing savings account into BSBDA. You have to open a new BSBDA and for that, you need to close your existing savings account within 30 days of opening a BSBDA otherwise the bank will automatically close your earlier account after 30 days. A person can have only one BSBDA in a bank

Banks are restricted to offer any value-added services to the BSBDA account holders by charging any extra cost. If any extra service is given, then automatically the account will be converted to a normal saving bank account.

Documents required for opening Basic Savings Bank Deposit Account

Documents required for opening BSBDA are as follows :

Account opening form.

Colored passport-sized photograph.

KYC documents like – ID proof, address proof, PAN, etc.

Difference between a normal savings account and BSBDA

Normal savings account

Basic savings account

Small savings account

Minimum balance limit

10000

No limit

No limit

Penalty if minimum balance is not maintained

Applicable

Not applicable

Not applicable

Withdrawal limit

Not applicable

Applicable

Applicable

Mobile banking facility

Available

May not be available

Not available

Credit limit

No limit

No limit

50000

Who should open this “Basic Savings Bank Deposit Account”?

Now you must be thinking “What is the use of this account for me? I have my regular account with unlimited transactions then why should I open a basic savings bank deposit account?

Let me tell you, there are lots of people around us who don’t have a bank account because they can’t maintain the minimum balance limit. Like some students, employees who have just entered into their profession, small-scale workers, maid, driver, and so many other people.

There are also some people who have more than one or two bank accounts other than their regular accounts. For these people, the money seems to be stuck in their bank accounts where they have to maintain the minimum balance limit.

Some senior citizens don’t require more bank transactions as they are either dependent on their children financially or they keep cash to avoid visiting banks or ATM’s every time for withdrawals when they need money. For such people, the basic savings bank deposit account is a good option to avoid the penalty and other extra charges for maintaining their bank account.

I hope this information was useful for you. If you have any query then write in the comment section.

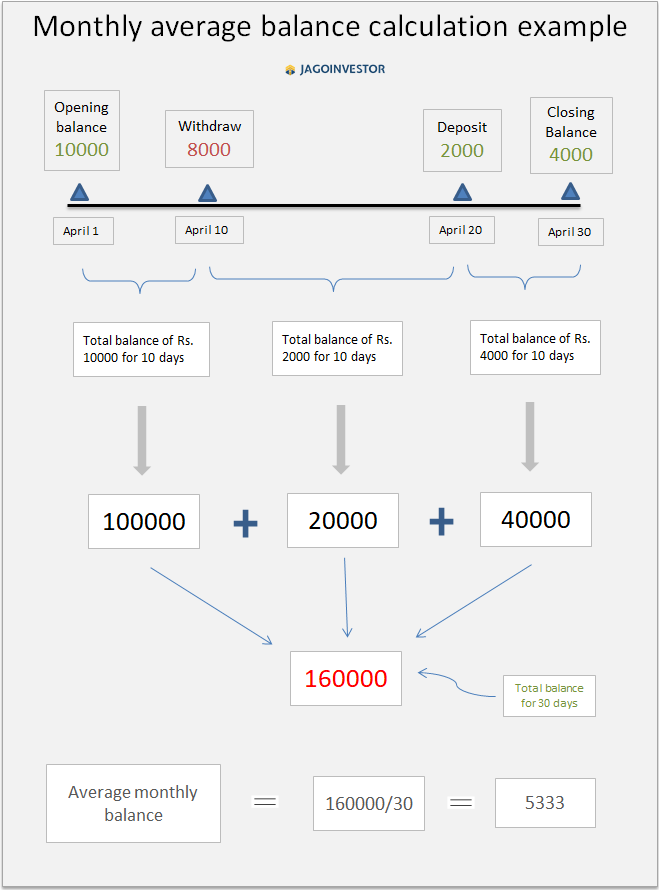

Do you understand what is the meaning of Minimum Monthly Average Balance in your saving account? When you say “Monthly Average Balance of your saving bank account is Rs.10,000”, what does it mean exactly?

A lot of people feel that their balance in saving bank account should not go below Rs.10,000 on any given day, otherwise, there will be penalty charges and they make sure that they have a buffer of Rs.10,000 in their saving bank account all the time.

This means that their account should always have that much surplus. However, the way the monthly average balance is calculated is different and very simple.

Meaning of Monthly Average Balance?

It simply means that the average of the all the closing day balance in a given month. So given a month, add up all the closing day balance and then divide it by the number of days in the month. If you have to put it as a formula it would be

MAB = (Total of all the EOD closing balance)/(number of days in a month)

Let me show you an example. Let us say the month we are talking about is April. The minimum balance limit in your bank lets say is Rs.5000.

Now your balance at the start of the month (Apr 1) is Rs.10,000. You withdraw Rs.8000 on 10th Apr and then Deposit Rs.2000 on 20th April. What will be the Monthly average balance for the April month?

Learning’s & Tips

Keeping Rs.10,000 in a bank account for 15 days is same as keeping 5000 for full 1 month (10k * 15 days = 5k * 30 days)

PSU Banks vs Private Banks

A lot of PSU banks like SBI bank, Bank of India, Allahabad bank generally have a lower monthly average balanceto be maintained in saving bank account, it’s average limit is up to Rs.5000 non-Maintenance Charges are very low around Rs.40-50 only.

However Private banks like ICICI Banks, HDFC bank, Axis Bank etc have Monthly balance as high as Rs.10,000 and charges a high penalty for not maintaining it , It some times can be as high as Rs.750.

So by now, you must have known how the minimum average balance is calculated? Will this information impact your banking in any way? Will you keep less money in your bank account because you now know that Monthly average balance is calculated in a different way than you thought?.

Let us know if you have any query in the comment section.

Do you think corporate fixed deposits are as safe as bank Fixed Deposits? Has come agent convinced you that you will get 2-3% higher returns from corporate fixed deposits without any risk?

If that’s the case, you need to be educated a little more about corporate fixed deposits. I will talk about 5 major things every investor should know before they put their hard-earned money in corporate fixed deposits.

What are Corporate Fixed Deposits?

Corporate Fixed Deposits are deposits that are issued by private and public companies, which work very much like bank fixed deposits. There is an interest rate offered and there is a maturity duration for the company deposit. You can either opt for a cumulative option (where your interest is added in deposits) or you can opt for a non-cumulative option, where you are paid the interest after every fixed duration.

A lot of agents get a good commission for selling these corporate fixed deposits to their clients. Nothing bad in that as such, but you need to be clear about some important and critical points related to company fixed deposits.

Let’s start…

Higher the return, higher the chances of Default

In almost all cases, the corporate fixed deposits offer quite higher returns compared to a bank deposit. If bank deposits rates are 7 %, you will see that company deposits floating in markets are providing your returns in the range of 8-14%.

Always ask the basic question – “Why is a company providing higher returns?”

The logic is very simple, a company needs money for expansion or for some project and to fund that project, they can either take a loan from a bank or raise money from other measures and for that they will have to pay very high interest.

So they float corporate fixed deposits where normal investors like you and me can invest in their deposits and earn higher returns.

But, because you get higher returns, there is also high risk involved in corporate deposits. You never know how the company will do in the next few months or years. You never know how the project of a company turns out and if it’s going to make a profit or loss.

In short, after a few years, when its time for maturity – what will happen if the company’s financial health is not good? Will they repay the money on time? Will they repay the money at all?

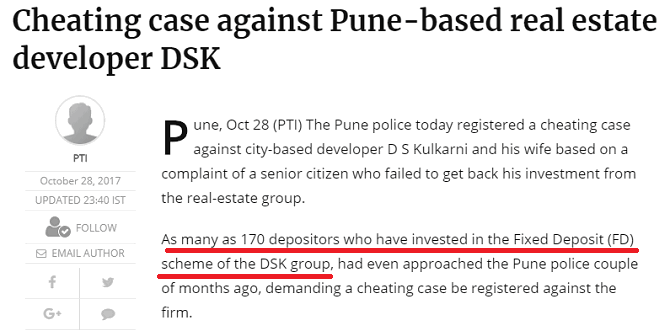

In one of the recent examples, a lot of investors had put their money in DSK group fixed deposits

A lot of senior citizens are lured into parking their hard-earned money into many shady fixed deposits offered by small or medium-sized company fixed deposits by showing them high returns.

Below is a heart breaking case study of a 78 yr old person who had put all his gratuity and PF money into DSK Kulkarni FD (a very big real estate group in Maharashtra). When his FD maturity came, he was told that he should renew it for another 6 months as its tough to repay right now. The video below is in Marathi, but you will understand some words and will be able to make out what is being said!

So please understand that when you are investing in corporate fixed deposits, there are good chances that if it’s offering very high returns, there is a lot of risks involved in that. You cant get higher return just like that.

Many big companies also offer corporate fixed deposits, but then the interest offered is quite lower and looks reasonable. However the risk is still there unlike a bank FD.

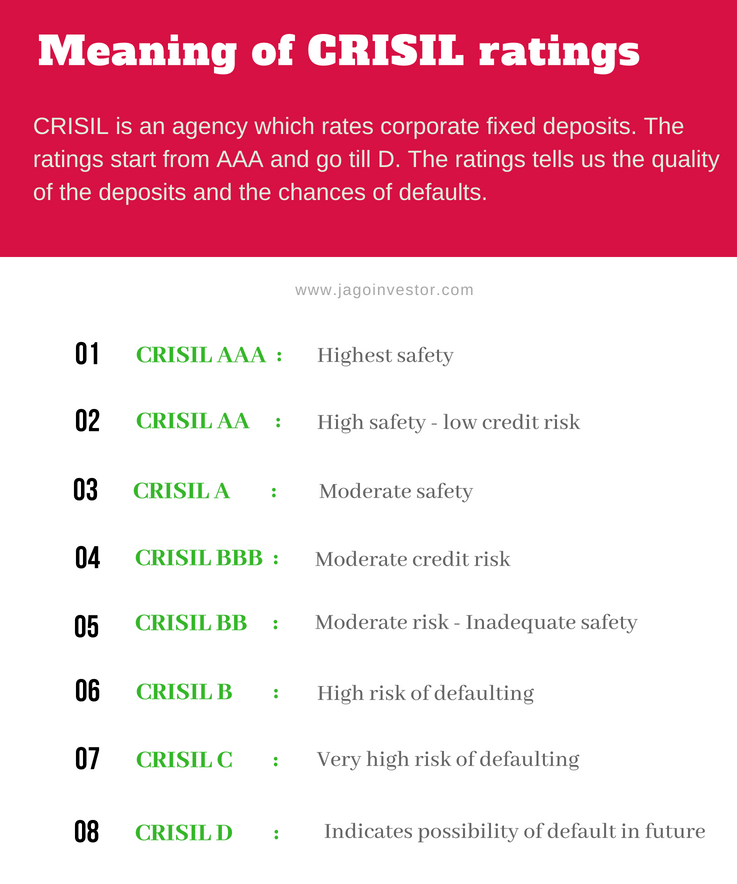

Every company fixed deposits are rated by agencies like ICRA, Crisil, CARE etc and they give a rating to the FD. These ratings are a measure of the company’s ability to pay the interest as well as principal to its investors. A high rating means no or very low probability of default.

Corporate FD’s are not regulated by banking rules

Note that unlike bank fixed deposits, corporate fixed deposits are not regulated directly by RBI regulations. All the deposits under corporate deposits are governed by provisions of 73 to 76A of the Companies Act 2013 (erstwhile section 58-A of The Companies Act 1956).

If the company is not paying you on time, you cant do much in that other than following up with the company. However, Fixed Deposits of Corporates are secured borrowing, so in case of winding up of business, secured borrowings are given preference over equity shareholders in terms of repayment.

Some important points related to Corporate Fixed Deposits

TDS is deducted @10% if the yearly interest is more than Rs 5,000

Premature closure of company FD is not possible for 3-6 months

Pre-closure of company FD is not a straight forward process, it’s cumbersome and involves too many documents

Still, want to invest in Corporate Fixed Deposit?

If you still want to go ahead and invest in a company fixed deposits, please take care of the following points.

Make sure that the company is paying regular dividends to its share holders

The balance sheet of companies is showing profits at least for 3 yrs in a row

Make sure its an at least a 5 yr of company

Make sure they are offering realistic returns (2-3% more than a bank FD). Do not fall for those companies which are offering very very high returns

Make sure these companies are listed on the stock exchange

Make sure that they have got a high rating from CRISIL like (AAA or AA or A at least)

What happens to the orphan bank account once the account holder dies?

Have you ever thought how your family members will be able to access and claim the money in the bank if something happens to you? Today we will discuss this aspect and see what exactly happens once a bank account holder dies and what are the steps to be taken by the family members.

Whenever there is a sudden demise in someone’s family, there is a panic attack. There is mourning of losing loved ones and chaos in the family for few weeks, but ultimately life comes back to normal later.

A few months later, family member start collecting all the financial data like life insurance policies, locker keys, investment details, loan details etc. etc. But the most important thing is the bank account. Bank account is the key to someone’s financial life and getting access to it is critical.

Here are the steps to claim the money in bank account.

Withdrawal from ATM Card

Before one moves to the actual process, we should first look at the obvious thing. Find out if you have the access to the ATM/Debit card and if you know the PIN. Just go and withdraw the money from the ATM if possible over next few days.

If for some reason you are not able to access the ATM/Card, then it’s time to follow the process.

Step#1 – Approach the bank & Meet the bank officials

You should approach the bank and meet the bank manager and share about the account holder death. Ask him/her the procedure to claim all the asset from the bank. If possible, show them the proof that the account holder has passed away (like death certificate)

Then the bank with immediate effect will make the deceased account in a dormant state (a state in which the there is no withdrawal possible). However, the deposits are still possible, because it may happen that few payments / dividends are going to be credited in coming days

Step #2 – Submit the documents

Case #1 – Single account holder

If the bank account was in single name, then the nominee approaches the bank with the death certificate of the account holder including his own authenticity proof. Then the procedure of transferring money to the nominee starts and the account remains in the dormant state for 6 months to 12 months (differs from bank to bank).

Here are the Required documents:

Application, stating that the account holder has passed away,

Notarized death certificate

FIR copy (if the deceased has passed in the accident and body is missing for some time )

Authentic photo id proof (such as adhaar card, pan card, driving license etc…)

Relationship with the deceased with proof,

Nominee KYC documents (photo, pan card, and adhaar card)

Some additional documents if there is no nominee in bank account

Incase nominee is not mentioned, then the bank needs clarity on who is the rightful owner of the money. For that, they might need a written WILL, which will mention clearly about the owner of the bank account money.

If WILL is missing, in that case, the bank can ask you to bring succession certificate from court, which will be the legal document certifying who is the actual owner of the money.

Case #2 – Joint account holder – If the 1st account holder has passed away then the 2nd account holder can inform the bank with the application stating the 1st account holder has passed away and also to make the 2nd holder the 1st holder so that he/she can have access to the money

Required documents –

Application stating the death of the 1st holder

Notarized death certificate of the 1st holder

FIR copy (if the 1st holder has passed in the accident and body is missing for some time)

Authentic photo id proof of the 2nd holder (such as Adhaar card, pan card, driving license, etc…)

What if there is a dispute among family members?

It may happen that there are many people in family, who claim to be the legal heir of the deceased. Even if nominee is mentioned in the account, still the legal heirs may be different from nominee.

In this case, one has to move to court and apply for succession certificate which we talked about before. It’s a document which will certify the legal heirs.

Make sure your family does not face any issues

How do you make sure that your family members do not have to go through the problems while claiming back the bank account? Here are few things you can do

Make sure your family knows the ATM PIN and net banking details

Convert the bank account in joint name, so that anyone can access the account

Make sure you mention a nominee among one of the legal heirs

Write a WILL and mention about the beneficiaries very clearly

Let us know if you liked the article? Leave your questions if any, in the comment section and I will try to reply to all the comments and doubts.

Everyone wants to check bank balance and keep a track on their bank accounts. Smartphone’s, internet and banking system together has made this process easier by providing the facility to check your bank account details online.

But what in case of those people who don’t have a smartphone or internet connection?

Now you can check your bank balance and a few other details of your bank account without internet also.

Let’s see 2 methods of checking your bank balance when you do not have internet and also you want the information quick fast.

Method #1: Missed call feature to know your bank balance

This is a very simple process by which you can check bank balance easily without having an internet connection.

How does this process work?

As I said earlier, it is a very simple process which will be completed in just 2 simple steps.

Dial the 10 digit mobile number which is allotted to your bank (Select from the list given below.)

After 2-3 rings your call will be disconnected and you will receive a message which will show you your bank balance and mini-statement of last 5 transactions.

OR

If your number is not registered to the bank, you will get an SMS which will show that your number is not registered with the bank and it will also include details of how to register your mobile number.

Given below is the list of banks and the 10 digit contact numbers which you can use to know your bank balance and mini-statements. You can simply save the related number of your bank in your contacts list and you can easily check your balance anytime.

Public sector banks and their contacts for missed call service:

Private sector banks and their contacts for missed call service:

Bank Name

The contact number for missed call facility

Axis Bank

09225892258

Dhanalaxmi Bank

08067747700

Kotak Mahindra Bank

18002740110

HDFC Bank

18002703333

ICICI Bank

02230256767

Karnataka Bank

18004251445

Yes bank

09840909000

Some salient features of this facility are given below:

This facility is completely free for everyone.

To get the benefit of this facility your mobile number should be registered with your bank account.

If you have more than one account, then your latest opened account will be considered as a default account and you will get the details of that account in this facility. However, the default account can be changed.

These features are the same for all banks. However, the process might be different in some of the banks.

Method #2: Know your bank account balance using *99#:

The code *99# is also called as USSD code which is not related to any particular mobile network service providers or any bank. This facility is introduced by NPCI to provide the facility to common people to have an easy access to their bank account.

Below given are the steps to check bank balance using USSD *99#:

Dial *99# from your mobile.

Select the option of bank balance from the list which will be opened on your screen (which is most probably 3 for all users).

Then enter the 3 letter name of your bank or first 4 letters of your IFSC code.

OR

It might ask your UPI pin if you are already registered for that.

Enter 3 letters of your bank name (for e.g. SBN is the 3 latter name for State bank of India) or first 4 letters of your IFSC code (OR UPI pin).

Your account balance will be shown on your screen.

Basic features of *99# service

This facility is a relief for those people who can’t have access to the internet all the time. This unique code has some basic features which you should know if you are going to use it.

The feature of this USSD code is as follows:

This code works without internet.

No hidden charges or roaming charges are applicable on use of this code.

It works across all the GSM service providers on all kinds of mobile handsets.

You can use this code 24/7 including holidays.

No need to download an app or activate any service on your mobile phone.

What kind of services you will get under *99#?

*99# is a USSD based mobile banking facility introduced by NPCI which brings together the two diverse ecosystem partners i.e. Banks and Telecom service providers.

Apart from the balance inquiry this banking system also provides some other facilities which are listed below. Let’s have a look at those facilities.

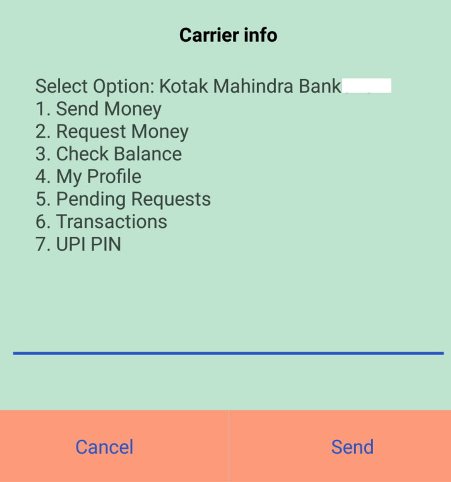

Send Money Using IFSC code and bank account number of the beneficiary.

Balance Enquiry

Mini Statement

Generate or change MPIN or Mobile PIN.

Send Money Using Aadhaar number of the beneficiary which must be linked to his bank account.

Know your MMID

Send Money Using MMID and mobile number of the beneficiary.

The only difference between these two methods of mobile banking is that by using missed call service you can know your bank balance and mini-statement only.

On the other hand, if you go for USSD code service, you can also transfer money from your account to any other account by using his mobile number and MMID OR account number and IFSC code or even Aadhaar number.

Isn’t a very easy way to know your bank balance without any internet connection?

I hope you enjoyed the article. What do you think, is this facility helpful or not? Leave your opinions in the comment section.

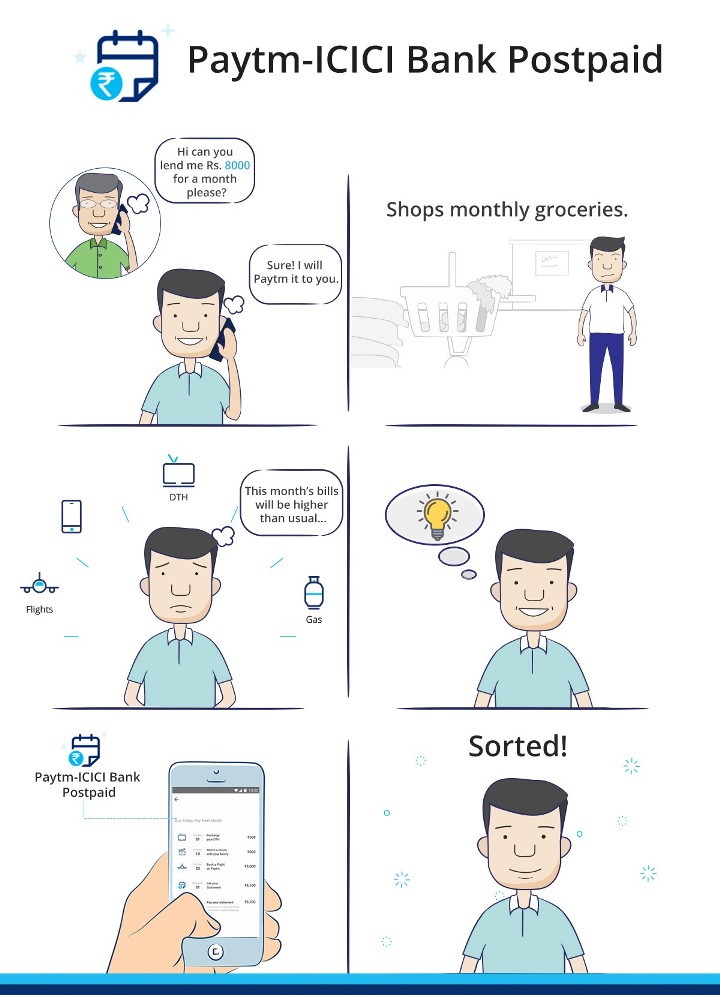

Paytm, India’s largest mobile payment network has partnered with ICICI bank to provide short term small loans to its users. This is India’s first scheduled commercial bank tie-up with a mobile payment platform, and it is named as Paytm-ICICI bank postpaid.

The main motive behind this partnership is to provide 24/7 digital money support to millions of Paytm and ICICI banks common customers across all over India.

This feature is introduced to ease the daily expenses of all ICICI bank customers who are using Paytm, by providing them Digital credit. The below image shows you how it works

As per this tie-up, you can take digital credit in your Paytm account from ICICI bank, which you can use for your daily expenses like paying bills, booking flight or bus or even buying a movie ticket. You can use this credit anywhere where Paytm payment is accepted.

Please watch below video to know the details.

Type of loan and interest rate

This credit will be interest free for first 45 days. If you repay it within 45 days, then you will have to to pay only the principle amount and no interest will be charged. But if you delay the payment for more than 45 days, then you will have to pay a late fee of Rs.50 and 3% interest.

How much maximum credit can you take?

This credit limit ranges from Rs.3000 to Rs 10000. It means you can take digital credit of minimum Rs.3000 and maximum of Rs.10,000. And if you have a good repayment history which means you payed all your credit loan in time, then the limit can be extended for you upto Rs.20,000.

Which means that this is going to be useful mostly to students and those people who are left with no money by the end of the month or have severe cash crunch.

Right now this facility is available for the customers of ICICI bank who are using Paytm, but soon all the Paytm users also can get benefit of this newly introduced postpaid digital currency.

Who should use this?

If you are using Paytm heavily and if you are the type of person who has severe cash crunch and want to take short term credits, then this facility if for you.

We do not recommend this facility to be used unless you really need the money. Its better to always maintain liquidity in your bank account and not fall for this kind of service.

I hope this information is useful for you. If you have any query, leave your reply in the comment section.

Have you heard about RUPAY cards? Today we will talk to them in detail and how they are different from Visa or MasterCard and if you should choose them or not. But before that, let’s understand the background first.

What is Visa or MasterCard?

You must be already having a debit card or credit card which must be having either VISA or MASTERCARD written on it. Visa and MasterCard are credit card networks with their own systems, rules, and processes for payments, benefits, etc.

However, Visa and MasterCard are both American companies globally accepted and widely used card networks across the world. There are some other card networks also like American Express, Amex, Citi etc, but you got the point. These are global card companies.

Now, these companies do not directly issue a debit or credit card, but various banks across the world offer their cards with payment network operators which can be VISA, MASTERCARD or others.

What is Rupay?

Rupay is just another payment network solution like VISA or MASTERCARD, but it’s our own desi version. It’s an Indian company and purely an indigenous product creates by us. Here is what Rupay website says

RuPay is India’s indigenous card scheme created by the National Payments Corporation of India. It was conceived to fulfill RBI’s vision to offer a domestic, open-loop, multilateral system which will allow all Indian banks and financial institutions in India to participate in electronic payments. It is made in India, for every Indian to take them towards a “less cash” society.

RuPay is the first-of-its-kind domestic Debit and Credit Card payment network of India, with wide acceptance at ATMs, POS devices and e-commerce websites across India. It is a highly secure network that protects against anti-phishing. The name, derived from the words ‘Rupee and ‘Payment’, emphasizes that it is India’s very own initiative for Debit and Credit Card payments. It is our answer to international payment networks, expressing pride over our nationality.

RuPay fulfils RBI’s vision of initiating a ‘less cash’ economy. This could be achieved only by encouraging every Indian bank and financial institution to become tech-savvy and engage in offering electronic payments.

Issuing Banks

Presently, RuPay has collaborated with almost 600 international, regional and local banks across the country. Its ten core promoter banks are State Bank of India, Punjab National Bank, Canara Bank, Bank of Baroda, Union Bank of India, Bank of India, ICICI Bank, HDFC Bank, Citibank N. A. and HSBC. It expanded its shareholding in 2016 to 56 banks to bring more banks across sectors under its umbrella.

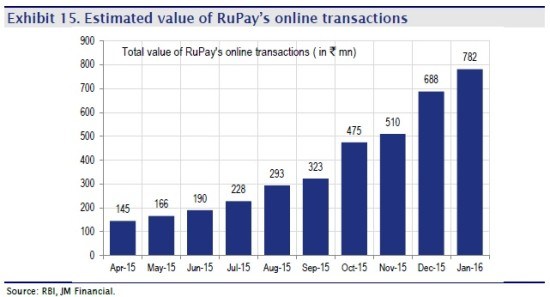

Rupay cards usage is increasing

Online transactions are increasing day by day in India as we are moving towards a cashless economy and the usage of Rupay cards is also increasing. Here is some data on Rupay online transactions.

Why Rupay was launched?

As we are moving towards becoming one of the major economies of the world, it was very important that we own our own payment solutions like Visa and MasterCard and hence govt started working on Rupay!.

Two more benefits of the Rupay card network are that.

The transaction history will not go out of the country if the transaction is within India.

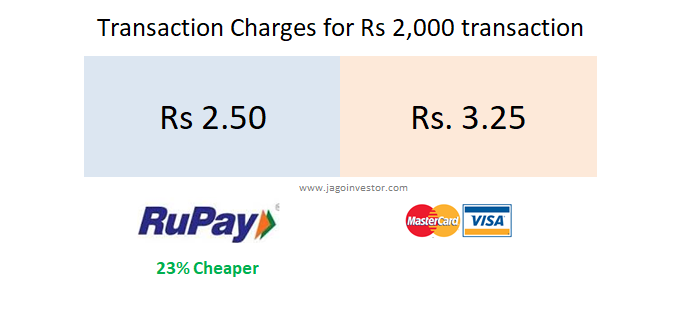

The charges that banks have to pay quarterly or monthly to the related companies to enter into the network is very low or NIL.

The image below shows you how a Rs 2,000 transaction charges will be lower in Rupay cards compared to a visa or MasterCard.

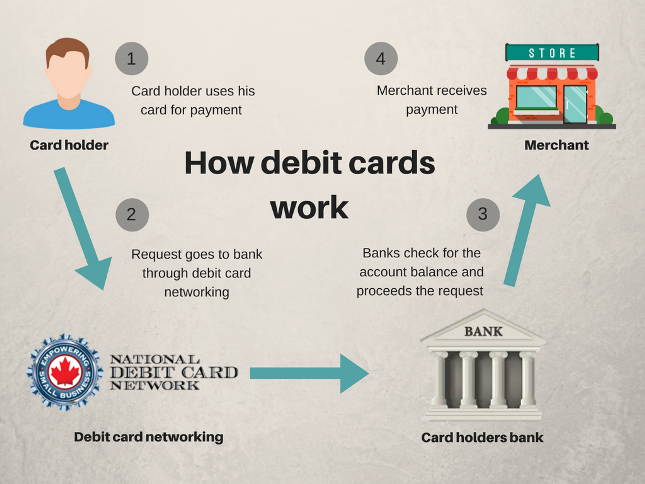

How does any card processing happens?

When you swipe your debit card or make an online payment, your request first goes to the debit card networking and then from there it goes to your bank. After that bank confirms your account balance and then completes the further procedure or transferring payment money to the merchant’s account.

See the image given below to know the procedure of your card.

Difference between Rupay card and Visa/Master card

Now let’s talk about some differences between Rupay and visa/MasterCard companies. This will give you a fair idea of how they are different from each other on various points.

[su_table]

Rupay

Visa/MasterCard

Rupay is 100% Indian system

Visa/MasterCard are international systems

Lower transaction charges compared to Visa/MasterCard

It has higher transaction charges than Rupay Debit Card.

Banks don’t have to pay any fees to enter into the network

Banks have to pay fees to join the network

Transaction history remains within the country.

Transaction data is shared outside the country as it is an international card

All processing is done within the country so it has a high speed of transactions

Here the processing happens at an international level so sometimes it has low transaction speed or errors in server

Some banks shows Rupay credit card on their website but it is not launched officially yet by NPCI.

Visa/Master credit cards are available and have a strong network

The usage is very low and not widely accepted as of now

Widely Accepted and Used

Can’t be used outside India as of now

No restrictions like this

[/su_table]

Transactions limits of Rupay debit card

Rupay cards like any other cards also have transaction limits and ATM withdrawal limits. Here is a quick list if you want to refer them.

[su_table]

Bank Name

Limits (ATM transactions)

Central bank of India

Rs 40,000 and Rs 1,00,000

Bank of India

Rs 25,000 each

Bank of Baroda

Rs 25,000 and Rs 50,000

Vijaya bank

Rs.30,000 and Rs.25,000

Punjab national bank

Ra.25,000 and Rs.60,000

Oriental bank of commerce

Rs.25,000 each

Dena bank

Rs.20,000 and RS.25,000

UCO bank

Rs.25,000 each

[/su_table]

How to Apply for Rupay card?

If you want to apply for a Rupay debit card, then you must first check with your bank if they have them or not? All the bank accounts under Jan Dhan Yojana already provide you the Rupay card, you don’t need to mention separately in your debit card application if you open an account under this scheme.

Let us know if you need any more information about the Rupay card and we will be happy to answer them in the comments section.

Today we will discuss why you need to stop investing in bank fixed deposits.

I know you are a bit shocked by this statement, but my only attempt is to give you some understanding of why banks fixed deposits are not the best financial products in these times for your long term wealth creation. There are other better alternatives today if your focus is assurity of returns, near inflation returns and convenience of investing

You can either read the article or just watch this 10 min video below where I have share why you should avoid investing in fixed deposits.

Why we create Fixed Deposits?

Since our childhood, I think most of us have only heard about Fixed deposits and PPF as investment products. We saw our parents talking about fixed deposits all the time. They broke “FD” when they needed sudden money.

And FD’s become were like the default financial product for most of us and when we started earning, we just created fixed deposits because that’s all we knew about.

On top of it, the fixed deposits come with assured returns of 7-8% (though the FD rates are going down and down these days). Also, almost all the banks offer the online fixed deposits creation (not breaking it) and that fact also adds to our love to creating fixed deposits whenever we need to park our money for some months/years

But, now there is a great alternative for fixed deposits called Debt Mutual Funds. This article will focus more on fixed deposits disadvantage and we will touch upon debt mutual funds to some level, but this is not a deep tutorial on debt funds

a) High Tax on FD – Fixed Deposits do not have any special taxation benefits. If you are into a 30% tax bracket, you will have to pay the tax on the interest you earn in a year as per your tax slab.

So if you create a Rs 10 lacs FD and you earn Rs 80,000 in interest (@8%) then you pay Rs 24,000 as the tax if you fall in the highest tax bracket. That’s not the case with Debt mutual funds. While debt mutual funds are not tax-free, their taxation is much better compared to a fixed deposit.

The video below explains how fixed deposits taxation is different compared to debt mutual funds.

b) No real returns – While you get an 8% return on fixed deposits, it’s just artificial .. because, after inflation and taxes, you are just left with a negative real return of 1-2%. So while you Rs 100 become Rs 108 after a year, you are not able to purchase the same thing after a year because it would not cost Rs 100, but Rs 110 by now (On an average)

Now, let’s look at debt funds and what they are and how they compare with fixed deposits

What are Debt Mutual Funds?

There is a big myth among investors community that mutual funds always mean risky investments because they are linked with the stock market, however, it’s far from the truth.

Debt mutual funds are a good alternative to fixed deposits. Debt mutual funds are financial products offered by AMC’s which pool the money from investors and invest in highly secured instruments like govt bonds, certificate of deposits, and other highly secured bonds in which a single investor cant invest on its own.

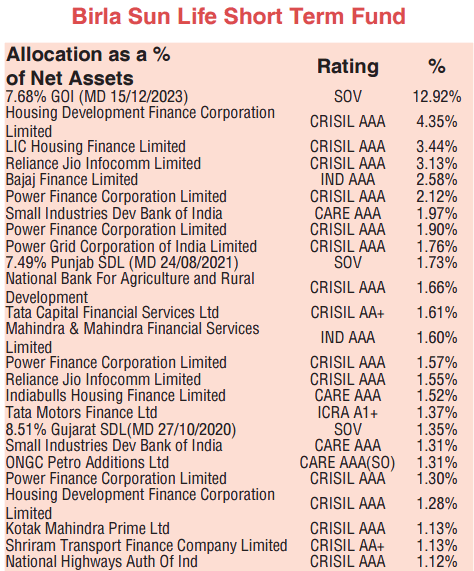

As an example, here is a sample top holding of a “Birla Short term fund” as per their factsheet

If you have done your mutual funds KYC, then investing and redeeming from debt mutual funds is online and very easy.

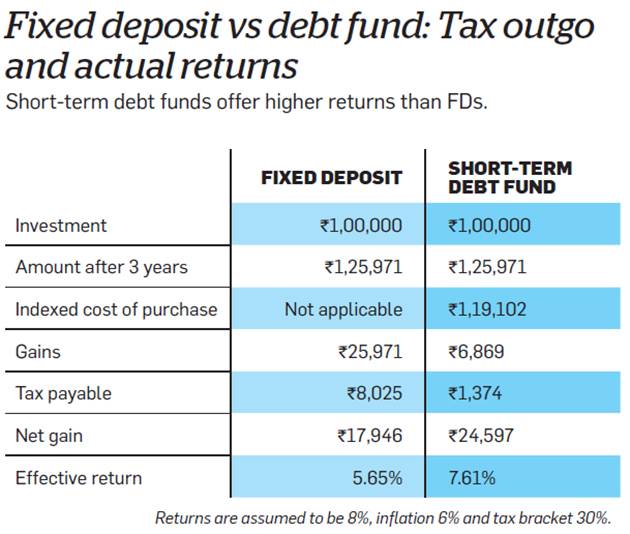

Debt funds also offer indexation benefits which means that you only pay tax when you redeem them unlike fixed deposits and you also pay tax on a lower rate (generally 20% after indexation). Below is a comparison by Economic times article on the taxation aspect of fixed deposits vs. a debt fund

When do Fixed Deposits make sense?

Fixed deposits can still be considered when you want to park your money for a short term period like 1 yr or 6 months and don’t want to go with mutual funds and also dont care about that extra 1-2% return. I think those investors who are trying to save money for the first time can look at fixed deposits or recurring deposits as open to start with.

SIP in Debt funds

If you are looking for an alternative of a recurring deposit, then SIP in debt mutual funds are the best option. The best part is that you can also top up your additional investments whenever you want unlike an RD in the bank.

Don’t use fixed deposits for long term wealth creation

While investing in a fixed deposit for a short term period is still ok, it’s strictly a no-no if you are investing for long term financial goals like retirement or children’s education or something. The positives of fixed deposits over long term are just a few compared to the negatives. Fixed deposits or recurring deposits are tools to just “save the money” and not wealth creation.

At best they can preserve your money purchasing power, but cant create big wealth for you (after adjusting for inflation and taxes)

So try learn more about debt funds, they are not at all that scary and much more easier to invest and maintain then you imagine. If you are looking to try out your debt mutual funds investments, our team can talk to you and help you save your money in debt mutual funds, Just fill up this form and we will call you

Let us know if you want to know anything about this topic ? Please post your comments and thoughts if any..

I got a fraud call recently and I was able to record it.

The person at the other end was posing as RBI officer and said that because I have not linked my Adhaar card with my bank account, they are getting closed and if I want to save them from not getting blocked, I will to do some verification on the phone call.

Watch the video below which as my recording!

Never reveal your critical information on a phone call

Never share the following things ever on a phone call with anyone

If you listen to the audio, you will realize that the person on the other side many times told me that the CVV number and account number is my personal information should not be shared with anyone. They do this to give a feeling that we can trust them and they are really some official people.

However, these people do not realize that their way of speaking and the language is such that it’s hard to believe that they are really some authorized person.