Spend enough time on social media and you may start believing that everyone is becoming financially free.

-

Someone retired at 40.

-

Someone left their corporate job at 45.

-

Someone is travelling the world with a ₹12 crore portfolio.

Slowly, it begins to feel as if Financial Freedom is now a normal milestone and if you are still working at 50, you have somehow failed in life.

You imagine everyone else happily vacationing in the Maldives while you are still attending Monday morning meetings.

But that is not reality.

After working closely with more than 1,200 families and interacting with thousands of investors through our workshops, articles and conversations, I can tell you this honestly:

Achieving Financial Freedom early is one of the hardest financial goals you can pursue.

It is possible. But it is not easy, common or guaranteed.

And we should stop talking about it as if it is merely the result of following a simple checklist.

Social Media Shows You the Winners

Social media naturally shows us successful outcomes. We see the person who retired at 42, but we do not see the thousands of people who started with the same goal and could not sustain the journey.

We see the entrepreneur whose business created crores of wealth. We do not see the businesses that struggled for years or eventually shut down.

We see the investor who built a ₹10 crore portfolio, but rarely see the income, family support, favourable circumstances, career growth and luck that may have helped along the way.

There is nothing wrong with celebrating these success stories.

They can inspire us.

The problem begins when exceptional outcomes are presented as normal outcomes. A person who has already achieved Financial Freedom may genuinely feel that the path was simple:

-

Earn well

-

Save aggressively

-

Invest regularly

-

Let compounding do its work.

All of this is correct. But success creates hindsight bias.

Once we reach the destination, every decision starts looking obvious.

Every struggle appears manageable. Every setback feels like a small and necessary part of the journey. We also forget how many things went right for us—a stable career, good health, a supportive spouse, no major financial disaster, the right opportunities at the right time, a favourable period in the markets and perhaps a little bit of luck.

The formula may look simple after the result has arrived. Living that formula for 20 or 25 years is a completely different matter.

Financial Freedom Is Not One Challenge

At a basic level, Financial Freedom means creating enough wealth to support your lifestyle for the rest of your life without depending on active income.

If you achieve it significantly before the traditional retirement age, you may call it FIRE.

For practical purposes, let us assume someone wants to become financially free by 48 or 50 not 35, so that we don’t give everyone a heart attack! Even then, it remains extremely difficult.

Because Financial Freedom is not one challenge.

It is many difficult battles happening together.

-

You must earn enough in the first place.

-

You must also grow your income over time

-

You must resist upgrading your lifestyle at the same speed.

-

Then you must spend less than you earn and have good surplus left each month for years, not months

-

You must invest that money sensibly instead of chasing whatever looks exciting that year.

-

You must remain patient while someone around you seems to be getting rich faster.

-

You must also enjoy your life today at the same time

Each of the above points is a battle in itself.

Consistently doing all the above points, year after year, again and again is not an easy thing in today’s world where AI is threatening jobs and social media constantly invites comparison

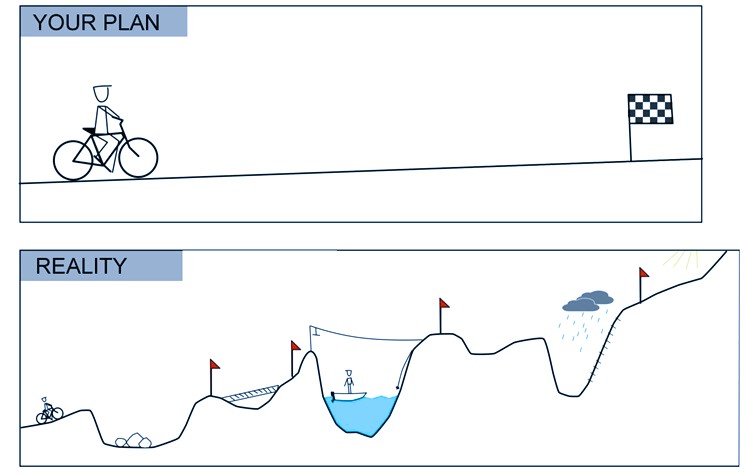

And then there is life itself—job losses, career stagnation, children’s needs, ageing parents, health problems, unexpected responsibilities and relationship dynamics. Our lives can become so consumed by these issues that finding time to relax becomes difficult, forget working consistently towards Financial Freedom.

That is why I find it difficult when someone says:

“Anyone can achieve FIRE if they simply follow these steps.”

No, Sir.

The steps may be available to everyone. The ability to execute them consistently for 20–25 years is not.

Why do I say this with confidence?

Because we work with more than 1,200 Indian families whose lives include regular jobs, family responsibilities, loans, health concerns and everyday struggles. Our understanding does not come only from a few extraordinary success stories on YouTube or social media. It comes from observing how difficult this journey is for ordinary families in the real world.

Financial Freedom Requires Three Things

In my view, Financial Freedom requires an unusual combination of three things:

Situation + Effort + Structure.

Miss any one of them, and the journey becomes much harder.

1. Situation

Your starting point and life circumstances matter.

Someone earning ₹5 lakh a year and supporting five family members is playing a very different game from someone earning ₹50 lakh with no major financial responsibilities.

Someone who begins investing at 25 has a different advantage from someone who starts at 32 with outstanding family loans and responsibilities.

Someone with good health, stable employment and strong family support has a different journey from someone facing repeated medical expenses or career interruptions.

Two people may have equal intelligence, intent and discipline, yet produce completely different results because life gave them different situations.

This does not mean your circumstances will permanently decide your future. It simply means we should not pretend that circumstances do not matter.

Financial Freedom needs a meaningful financial surplus, sufficient time and a reasonably supportive environment. Without these, the probability falls even if the desire is very strong.

That’s not pessimism. That’s probability.

2. Effort

A favourable situation alone is not enough.

A person may earn very well and still build very little wealth. Another may receive every possible opportunity but waste years through careless spending, repeated financial mistakes or simply a lack of action.

Financial Freedom requires continuous effort. It needs hunger to be financially free.

You must grow your income, control your expenses, save consistently and invest sensibly.

You must learn, make decisions, correct your mistakes and continue even when progress feels painfully slow. And this effort is not required for a few months. It may be required for two or three decades. You need to treat Financial Freedom as a serious project—not merely as something you wish will happen someday.

That is where most journeys become difficult.

Short bursts of motivation are common. Sustained effort is rare.

Anyone can feel motivated after watching a powerful video or reading an inspiring success story. But what happens six months later when markets are falling, expenses are rising, family conflicts are consuming your energy and the goal still appears 15 years away?

That is when the real journey begins.

3. Structure

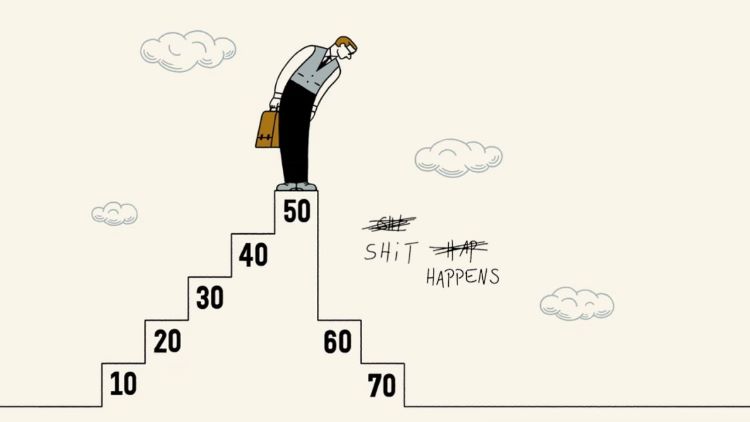

This is perhaps the most ignored part of the Financial Freedom journey.

Hard work and discipline are valuable, but discipline alone is unreliable. You cannot expect yourself to make the right financial decision every month for the next 20–25 years.

There will be stressful periods, temptations, fear, greed and competing priorities. Some years you will feel extremely motivated. In other years, you may not even want to look at your portfolio.

And then there is the simple reality of life: we get busy.

We know that the SIP needs to be increased, insurance needs to be reviewed or some important financial decision needs to be taken. But we keep postponing it. One month becomes six months, and six months quietly becomes three years.

Many financial goals do not fail because people make terrible decisions. They fail because people do not take the necessary actions at the right time.

This is why you need a structure.

By structure, I do not merely mean having SIPs, insurance and a few investments in place. I mean having a system that regularly checks where you are, what needs to be done and whether you are still moving towards your Financial Freedom goal.

Think about our health. Almost everyone knows that they should exercise, eat properly and sleep well. Yet many people achieve better results when they work with a good trainer.

A trainer does not exercise on your behalf. You still have to lift the weights and follow the diet. But the trainer creates a schedule, tracks your progress, corrects your mistakes and pushes you on the days when you would have otherwise skipped your workout.

That external check makes a difference.

The same principle applies to Financial Freedom.

A financial professional, mentor or experienced person cannot build wealth on your behalf. You still have to earn, save, invest and control your lifestyle. But that person can review your progress, follow up on pending actions, offer a second opinion and point out when you are drifting.

A good advisor can help accelerate your progress not by generating magical returns, but by reducing delays, bringing clarity, preventing avoidable mistakes and ensuring that important actions do not remain pending for years.

Yes, some people can manage everything themselves.

They have the knowledge, interest, time, temperament and discipline to create their own system and follow it consistently. Such people may not need external support, and that should be acknowledged.

But many others overestimate their ability to remain consistent for decades. Some understand money but keep postponing decisions. Some begin with discipline but lose direction after a few years. Others constantly doubt their own decisions.

Needing support does not mean that you are incapable. It simply means that you recognise how difficult it is to remain objective, disciplined and action-oriented over such a long journey.

A good structure may therefore include a clear saving rate, automatic investments, a defined asset allocation, proper insurance and emergency reserves, and regular reviews.

But for many people, it should also include external accountability—someone checking in every six or twelve months, tracking pending actions and helping them make course corrections.

Without this structure, every few months becomes a fresh negotiation:

-

Should I increase my investments now or next year?

-

Should I stop my SIP because the market is falling?

-

Should I review everything now or wait until life becomes less busy?

And life rarely becomes less busy.

A proper structure converts good intentions into regular action. Over a 20–25-year journey, that difference can completely change the final outcome.

Think Like an Athlete

Consider an athlete preparing for the Olympics.

-

The athlete needs the physical ability and life circumstances to compete at that level. That is the situation.

-

They need to train for years, tolerate discomfort and continue despite failures and setbacks. That is the effort.

-

And they need a coach, training schedule, nutrition plan, recovery routine and performance tracking. That is the structure.

Talent and effort alone are not enough.

A proper system carries the athlete even on days when motivation disappears. Financial Freedom works in a similar way.

You need a situation that makes the goal reasonably possible, sustained effort to move towards it and a structure that keeps you on the path when life becomes messy.

Early Financial Freedom Is a Statistical Outlier

A very small percentage of people will become financially free by 48 or 50. Not because people are lazy or lack intelligence, but because the goal demands an uncommon combination of circumstances, income, time, behaviour, health, family alignment, patience, structure, effort—and some luck.

Extraordinary outcomes are extraordinary precisely because few people achieve them. If half the working population retired at 48, we would not call it early retirement. We would simply call it retirement.

That is why early Financial Freedom should not be presented as the expected result of following five steps from an Instagram reel. It deserves far more respect than that.

Treat Financial Freedom as a Project

None of this is meant to discourage you.

It is meant to help you see the goal honestly.

Once you appreciate how difficult Financial Freedom is, you stop treating it casually. You understand that inspiration and motivation are not enough. You start building the right structure around your money and your life.

You save with more intention. You invest with greater clarity. You protect yourself against major setbacks.

You involve your family. You review your progress regularly. Most importantly, you create systems that continue working even when your motivation does not.

Here is what our client dashboard looks like. It compares the corpus required for Financial Freedom with the wealth already accumulated towards it. We track and update this progress every year

Financial Freedom should never be presented as a casual milestone.

It requires the right situation, sustained effort and, above everything else, the right structure. Those who achieve it have not merely accumulated a large corpus. They have successfully managed one of the longest and most demanding journeys of their financial life.

It should be recognised for what it truly is: an extraordinary achievement.

Ready to Begin Your Financial Freedom Journey?

If Financial Freedom is an important goal for you and you would like some guidance, support and accountability along the way, you can explore our #missionFIRE project.

Next Steps

-

Read stories from our clients as they share their Financial Freedom journeys and important milestones.

-

Take our 25 questions Financial Health Checkup

-

Contact our team to learn more about the program and how it works.