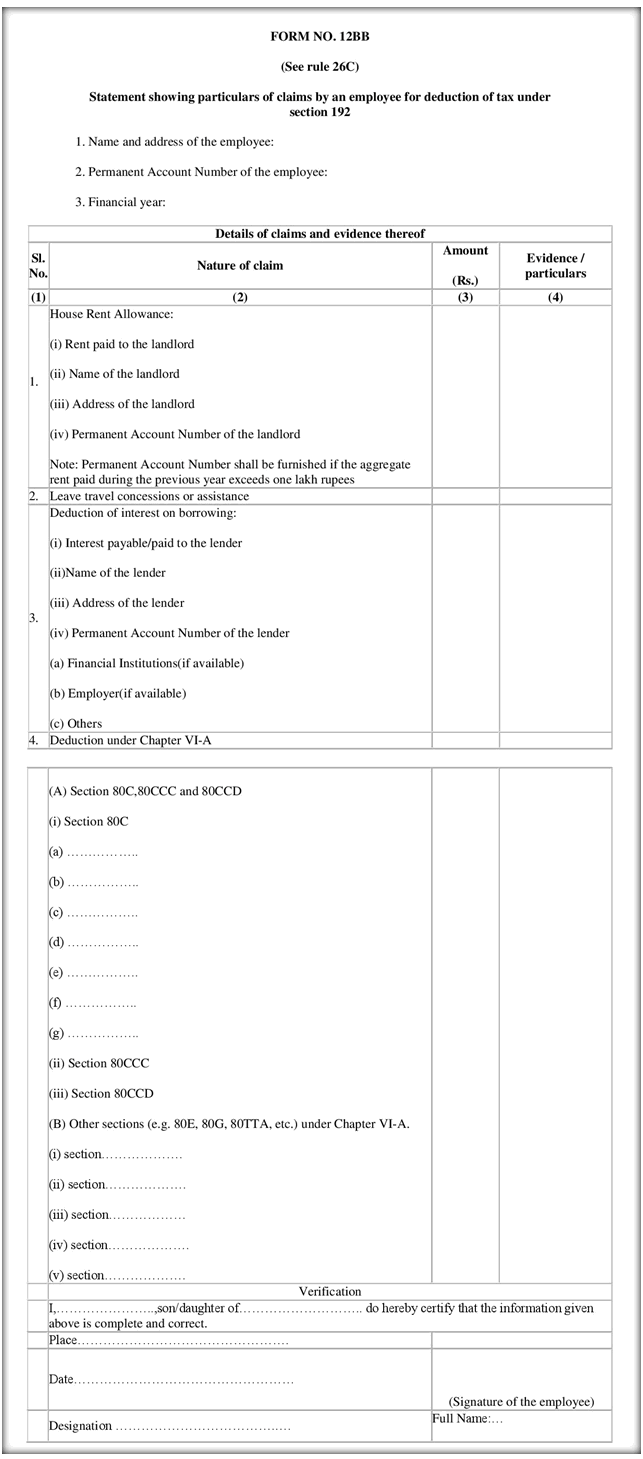

In a recent notification, income tax department has come up with a new form 12BB, which from now onwards has to be submitted if you want to claim your LTA, HRA and Interest on Home loan interest.

It’s a single form, which you need to fill and attach all proofs and furnish all information related to these exemptions. This form will be applicable from June 1, 2016.

What all information is asked in Form 12BB?

Following is the list of various things you need to arrange before you fill up this form 12BB form

LTA (Leave Travel Allowance) – One has to provide all the proofs of travel like tickets, invoices, boarding pass (in case of flight). More info here

HRA (House Rent Allowance) – For claiming HRA, If the rent paid is above Rs 1 lacs a year, one has to provide Name, Address and PAN of the landlord and Rent receipts.

Interest on Home Loan – To claim this, one has to furnish the name, address and the PAN of the lender organization

Deductions under 80C & Others – You will also have to furnish the details and proofs of the actual investments done under Sec 80C and others

You can download form 12BB here, It’s a PDF version (We don’t have excel format). Below I have provided a snapshot of the form 12BB format, so that you can have a look at it and see what all fields you have to fill up.

Main reason to introduce this form 12BB?

The primary reason why this new form is being introduced is that till now there was no standard process to collect all the proofs and information regarding the various deductions.

IT department thinks that with this new change, fraud will go down. Here is what Financial Express says on this point

You may no longer be able to provide fake bills to claim income tax deductions for leave travel allowance (LTA) and house rent allowance (HRA).

Changes announced on Tuesday in reporting format for individuals claiming tax deduction on leave travel allowance (LTA), leave travel concessions (LTC), house rent allowance and interest paid on home loans is aimed at plugging leakages on account of fake bills, experts say.

So with this form, all the information will be captured in one place and even the employers will be made accountable for checking all documents and if the proofs are genuine or not.

Please share what do you think about this new form? Do you think that this will add more work and headaches for salaried employees?

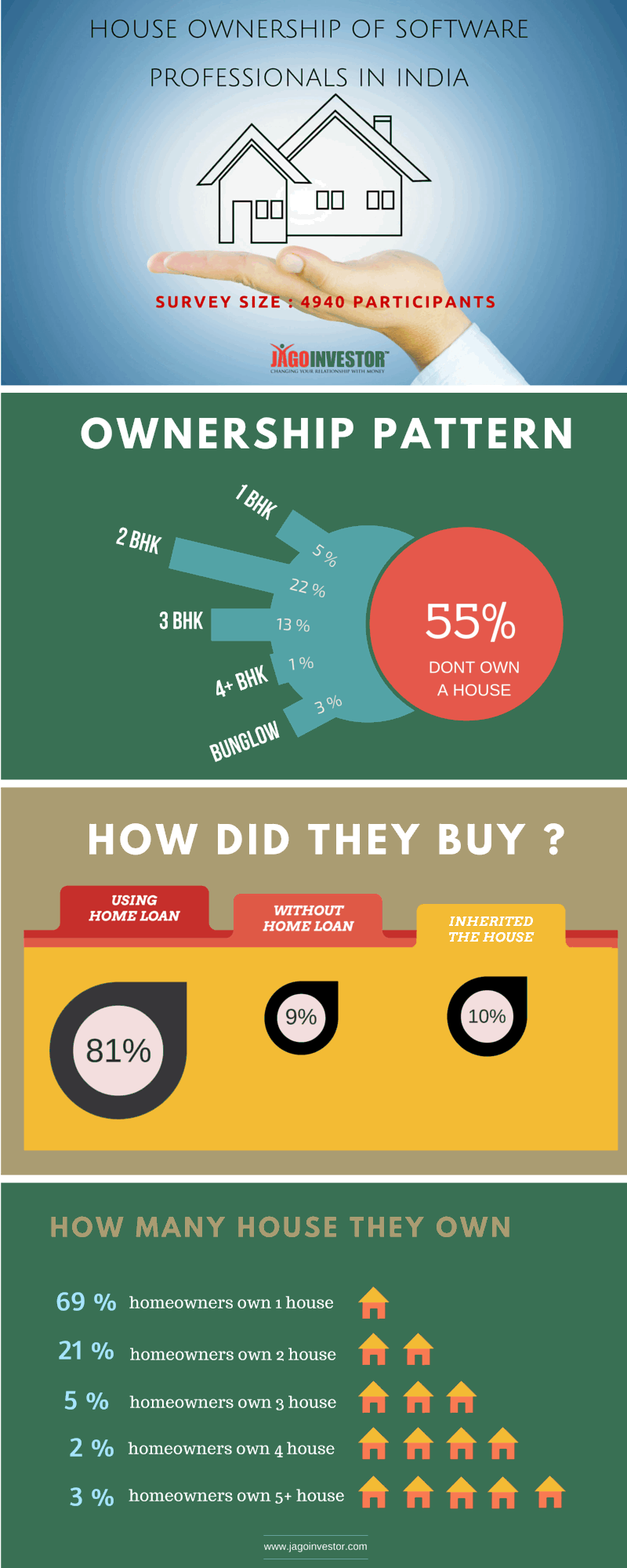

Today I am going to share with you some data related to software engineers and their home ownership pattern. But before you move ahead, I want to share with you that approx 55% of the software engineers who took our survey did not own a house.

Survey with 10,917 participants

Recently I ran a very large survey which was taken by around 10,917 participants. Out of those 4,940 people were from the IT Industry. I had asked many questions related to real estate ownership like how big houses they own If its bought with a home loan or not and if they don’t have a house, what kind of rents are they paying apart from many other questions.

As a big portion of this blog visitors is software professionals, hence I thought let’s do an article only for software professionals in India as of now. I will publish a detailed report later on the overall data, but as of now, you can look at 3 big and important information.

[su_animate type=”flipInY” delay=”0″] [su_button icon=”icon: facebook” url=”https://www.facebook.com/sharer/sharer.php?u=http%3A//www.jagoinvestor.com/2016/05/software-industry-real-estate.html” icon_size=”48″ size=”6″] Click Here to Share this on your Facebook profile[/su_button][/su_animate]

So what did I find in this survey? I found out that out of 4940 software professionals who took the survey, 2706 of them said that they don’t own any house or real estate property. That around 55%.

Majority of software professionals in India bought house with home loan

I know this is not a finding. Almost everyone buys a house on loan only because very few people can pay the full amount on their own and this gets confirmed by this survey. Around 81% IT professionals said that they took home loan for buying the house, however 10% people got the house in inheritance and only 9% people paid the full money out of their pocket, which I think is a good number.

90% of the house owners (IT professionals only) own either 1 house or maximum two house. Only 10% house-owners have more than 2 properties.

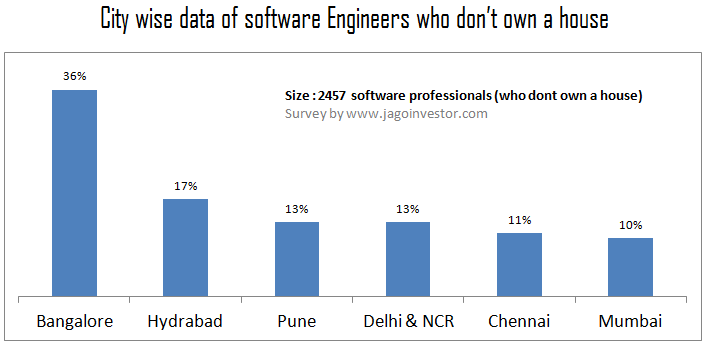

Out of 100 software engineers who dont own a house, 36 work in Bangalore

If we look at the top 6 cities which are into software jobs creation, we found out that the higher the cities reputation into IT Industry, higher is the number of non-home owners % wise.

I mean out of 4940 software engineers, 1533 work in Bangalore and out of those 886 said that they dont own a house, which is 36% of the total IT population which took the survey. So 36% of software engineers who dont own a house, live in Bangalore, compared to only 10% in Mumbai or 11% in Chennai. Here is the full data

Who is responsible for the high real estate prices in big cities?

In this article, I want to understand what you all think about high real estate prices? What is the reason behind it? Can we say that to some extent (if not fully), the IT professionals contribute to the real estate prices increase?

I know not all software professional earn very high salaries, but in all the big cities, there is a section of IT class which earns a very handsome salary and they suddenly use it to take home loan and buy a house either for consumption or for investment purpose.

This is true for many other Industries as well, but do you think IT sector contributes much more than other industries? I do not want to make any judgment here, but I want to hear from IT professionals who read this blog about what they think about this?

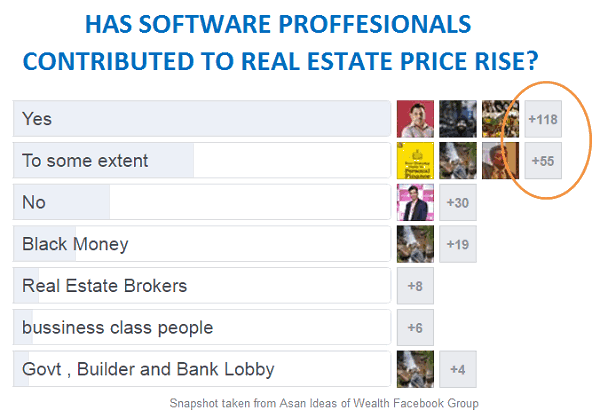

Some people told me that we can’t blame software professionals for high prices in real estate, which I agree. No one can blame anyone, but I wanted to know what thousands of people from IT background and non-IT background think? What is the perception?

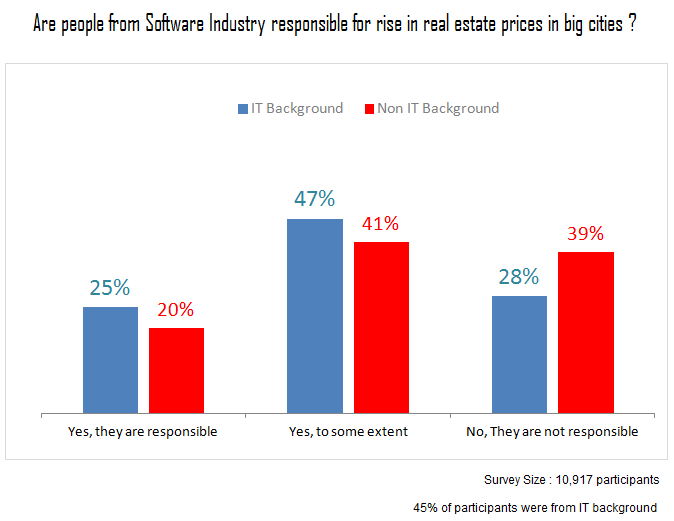

So I separated non-IT and IT people from the survey and I asked them the same question and looks like people from IT industry are of stronger opinion that real estate prices are high because of IT industry. While 39% people from non-IT background said clear “NO”, only 28% people from IT background denied that IT industry has contributed to rise in property prices. Below are the results of survey by around 10,917 participants out of which 45% are IT professionals themselves.

What people have to say about this?

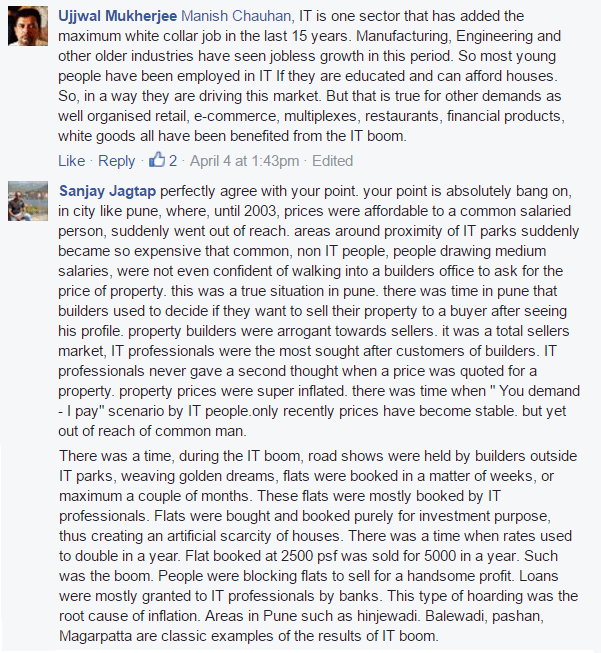

Let’s hear some people who have shared their views about this topic and how they feel that IT industry is somewhat responsible for high real estate prices.

But 55% of Software professionals still don’t own a home

At the same time, we have a big number of software professionals who cannot afford a house because they don’t belong to that very high earning class. Software industry like every other Industry has its own issues. A big percentage does not earn very high salaries and that is confirmed by the survey also.

Salaries in IT industry is highly skewed

Only 12% of IT professionals who were surveyed, are earning more than 20 lacs per annum where as 57% of the participants are earning below 10 lacs. Now that’s just 80,000 per month and I am sure, if one is living in a city like Bangalore, Pune or Hyderabad, it will not be considered as a very high income because given the expenses these days, people at that salaries would hardly be saving anything significant.

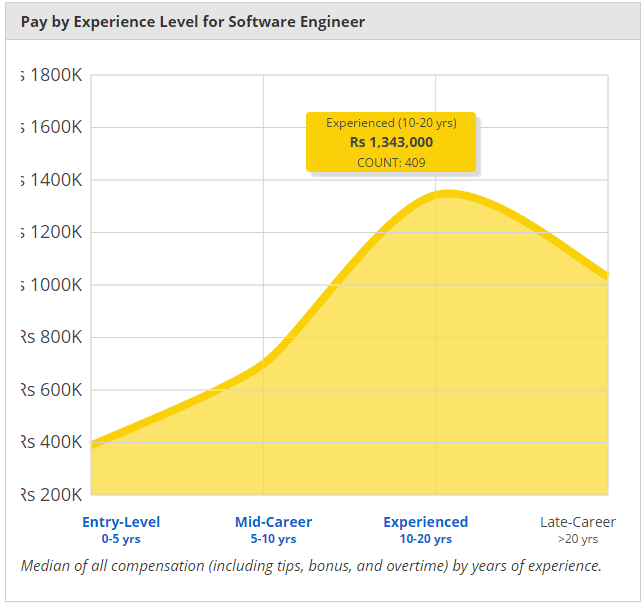

As per a website payscale, which has an extensive database of various jobs related information like the skills needed, salaries etc. The average Salary of an experienced Software Engineer in India is close to 13 lacs (with experience of more than 10 yrs) . Note that this is an average number

Hence, while there are many IT engineers who earn big amount (many a times double income family), and who can afford to buy a house easily. At the same thing, there are many software engineers who do not earn a big amount and are struggling to manage their expenses. Here is one perspective

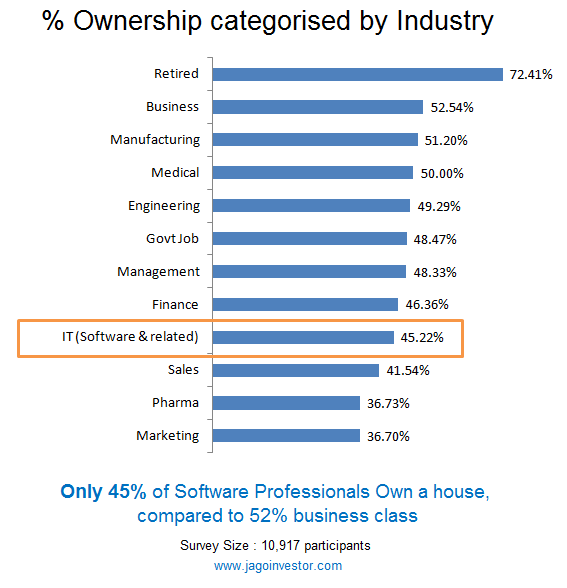

I analyzed the results of 10,917 people who took the survey and found out that if you look at the percentage home ownership industry wise, then software industry is not at all at the top. Infact, it’s quite below average. But then we are talking of only big cities (top 10 cities of India). On top of it, IT Industry has somewhat slowed down in last 5 yrs and its not at its peak now. You can read this long thread on IndianRealEstateForum where people discuss about the impact of IT slowdown on the real estate market.

So basically we are trying to see that out of 100 people who belong to XYZ Domain, what percentage of them owns a house. Domain here means Software, Medical, Govt Job, Business, Marketing, Sales, Engineering * Finance. There are many other domains, but we are not considering them, because there was not enough data. For each of the above domains, we had at least 200 data points each and at times more than 500 or 1000. Here are the results.

I had kept Retired also as one of the categories, because that would be a big number. So we found that the those who are retired have the highest home ownership which is kind of obvious, but after that business class has the highest home ownership ratio of 52% , followed by Manufacturing and Medical, but they are not having very big margin.

IT Industry ownership stands at 45% and we can be kind of very assured of that because that comes form 4940 people data, which is quite huge.

Also, note that the lowest home ownership is among Sales and Marketing Professionals & Even Pharma, I don’t have much interpretation for that, but may be it’s because they might have a big variable component in their salary and that might be a deterrent in their home buying. If you have insight on this, please put them in comments section.

Question for you ?

We want to know from you, what is your views on increasing real estate prices in most of the Indian cities and do you see IT industry contribution to it? Please share what you think in comments section.

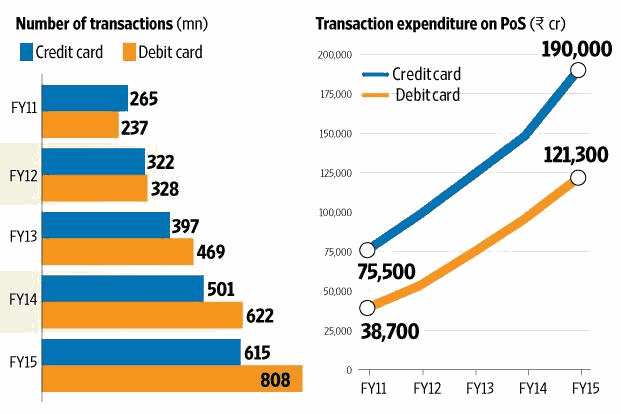

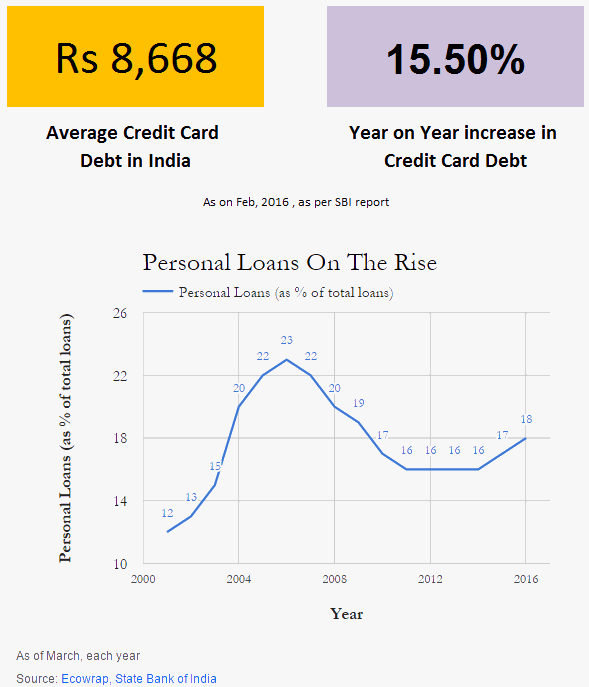

1,90,000 crore was spent using credit cards in India in the year 2015. Over the last decade, the usage of cards has increased many folds and while that’s great for the economy, it also means more and more people getting into credit card debt as many people are now dealing with credit cards.

In the graph below which was published by Livemint, it shows the growth in the card usage in our country

How investors get into Credit Card Debt Trap?

Credit cards if not used properly can get you into debt trap very easily. We get several emails and comments regarding how to handle credit card debt. Below is one of the comments

“I have a SBI card in which I have an outstanding balance of Rs 100000 so I went for settlement and they offered me a settlement amount of Rs.78000. Can it get it still reduced? Because I am not in a position to pay this amount”.

A lot of investors who do not use credit card in a wise manner end with a large outstanding on their cards and finally have to go for credit card debt settlement which lowers their credit score and puts a black mark on their credit report and this inturns hampers their chances of getting loans in future.

In this article, I am going to share some of the options which one can explore. If you want to quickly look over those 6 points, you can just watch the video below

Note that these points to be looked in order. I mean first, you see if option 1 is applicable to you or not. If not, then you move to option 2, if it still does not help you then you move to another option.

[su_table responsive=”yes” alternate=”no”]

Option #1

Break your investments and pay the bill

Option #2

Pay off the credit card debt in 5-6 payments

Option #3

Take a loan from friends/family and pay off the credit card outstanding amount

Option #4

Take a personal loan to pay off credit card debt

Option #5

Convert your credit card loan to EMI

Option #6

Use a Credit Card Balance transfer facility

[/su_table]

So here you go

Option #1 – Break your investments and pay the bill

There are many people who keep rolling their credit card debt, and at the same time have money in their bank account or a fixed deposit. It does not just strike them that they can just pay off the full outstanding by breaking their FD or cash into the account.

This happens out of ignorance most of the time.

So if you can restructure your money here and there and can pay off the credit card debt, it’s the best option.

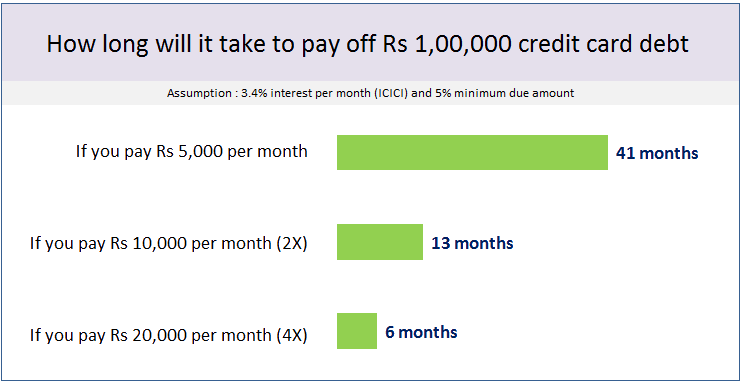

Option #2 – Pay off the credit card debt in 5-6 payments

If option #1 is not feasible for you, then the next best option is to pay off the debt in 5-6 parts. Most of the people get too attached to the minimum balance amount and then they just stick to it because that’s the minimum required to be paid to save the penalty.

But then the interest is anyways to be paid, which makes sure you never get out of the debt.

So go beyond the minimum balance amount and pay 3-4X of the minimum balance each month. For example, if your credit card debt is Rs 2 lacs and the minimum due amount which can be paid is Rs 10,000.

Then try to pay 2-3X of that amount, which is Rs 30,000 or Rs 40,000 per month. If not that much, then at least 20,000. That way at least you will pay off the entire debt in next 1 yr if you are disciplined enough.

Option #3 – Take a loan from friends/family and pay off the credit card outstanding amount

The 3rd option is to try to get some loan from friends or family members and pay off the credit card debt in one go and then pay back the person later as per what you agreed with him/her. One can often get free loans without any interest from a close friend or a sibling if you communicate your problem well.

Make sure you pay them back exactly within the time frame mentioned.

Most of the people have burned their fingers by giving money to their friends and relatives because it gets very tough to ask back the money and it can bring sourness in the relations due to money matters.

So you can also choose to pay some interest because the person can anyways earn some money from FD, so better offer to pay 10% interest per year. It’s a win-win situation if it works out!

Option #4 – Take personal loan to pay off credit card debt

If you don’t get loan from someone close in family/friends, then you can go for a personal loan and use that money to pay off the card outstanding. Interest will be in the range of 14-18%, but still, it’s better than paying 40% on a yearly basis.

This does not clear your debt, but just shifts your debt from credit card to a personal loan. Much better option. For those who already have a home loan going on, they can also look at the top-up loan facility which will be much cheaper to a personal loan.

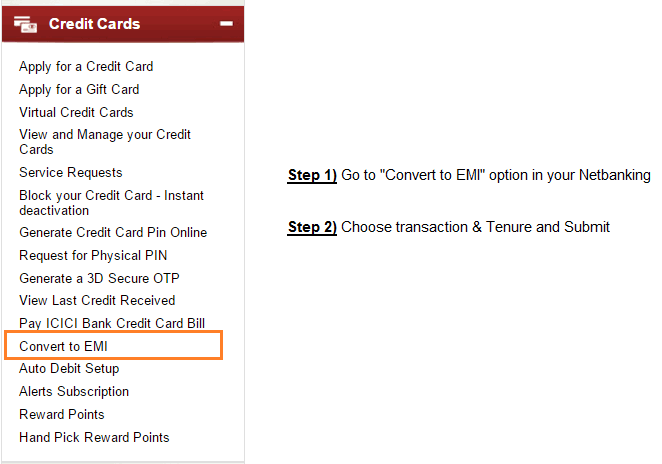

Option #5 – Convert your credit card loan to EMI

If you are not getting a personal loan, then you can convert your debt to an EMI option from the same lender. Almost all the big banks give an option to convert the credit card debt to EMI for tenures like 3/6/9/12/24 months. The interest can range between 13-18% depending on the lender.

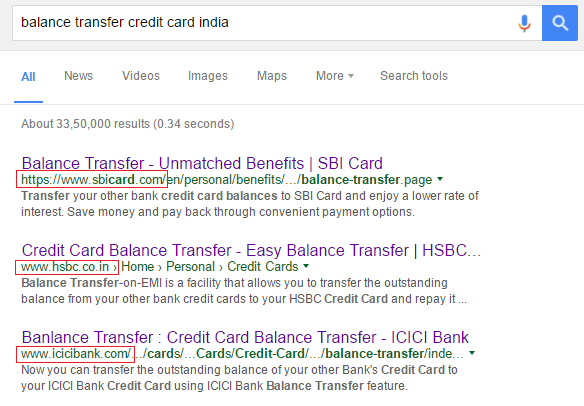

Option #6 – Use a Credit Card Balance transfer facility

There is a facility called Balance Transfer provided by many credit card companies, where you can switch your current credit card outstanding to a totally new credit card. In this case, the new credit card will pay off your old credit card and will also offer you some benefits like an interest-free period of 3 months or low interest for the first few months.

Almost all the major credit card companies like SBI credit card, ICICI credit card, and HSBC have this credit card balance transfer facility service with them. SBI credit cards even provide 0% interest for the next 60 days.

However, before opting for this option, please check if there is any processing charge or not? It might happen that the lender is providing free interest period, but then high processing fees will nullify the advantage 🙂

However, note that this is a temporary solution for the next 2-3 months and by that time you should look for further solutions.

Use your credit card wisely

Below are some high-level points which will save you from getting to credit card debt

Pay your Credit Card 3 days before the due date, keep a reminder on the phone if it helps

Don’t spend much more than you can afford.

Carry debit card instead of credit card, You will pay only what you have

Don’t keep very high credit limit, if you can’t control yourself when it comes to spending

Today I am going to talk about some mistakes which young investors make in their early life. Many experienced investors would be able to relate to it, because often we make these mistakes because there was no one to guide us when we started our journey of wealth creation.

“Young investor” here means any person who has just started their careers. Most of them would be below 30 yrs of age. I will share 7 mistakes in this article. You can consider these 7 points as the words of wisdom from experienced investors.

Mistake #1 – Not Focusing on increasing the income

Nobody became rich by only controlling their expenses!

“Low income” is probably #1 reason, why most of investors are unhappy in their financial lives. Low income means low/no savings, restricted life style and constant worry about future. A small financial mistake can turn very costly if one has small income.

Imagine a guy living in Mumbai & earning just Rs 35,000 a month (or even Rs 80,000 now a days) and have to support a family of 4 people? Can you imagine how “tight” his situation is?

For most of the people, salary increment “happens” naturally and never worked on consciously. Most of the people take whatever comes their way for many years, only to realize that rather they should have come out of their comfort zone and worked “actively” on increasing their income.

They could have relocated to a new place with better opportunities, changes their jobs, asked for a salary raise, or could have worked on an alternative income, but most of the people don’t do that. They just go with the flow thinking – “I will get, what I deserve”

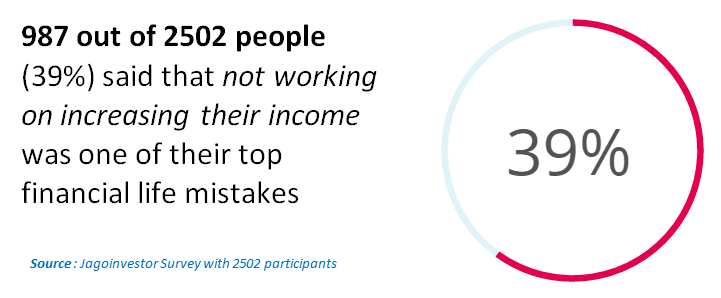

In one of the survey’s I have done recently, I asked participants to choose the top most mistake of their financial life. I gave them 8 different options to choose from and 39% of the people chose – “Never worked on increasing my income seriously”.

As a young investor, the best investment you can make it not some mutual fund, or a policy, but you yourself. Invest in yourself and develop skills which makes you “valuable”. Make yourself so employable that people run after you.

Remember, if you earn a big income, you can still make a lot of mistakes, spend like hell and choose not to control your expenses.

Mistake #2 – Getting into Debt Trap Early in Life

Don’t get me wrong!

I am not against taking debt.

But, a large number of young kids who start their career have bad relationship with money and credit facilities.

They start using credit cards as if it’s a money toy. It all starts with a small outstanding credit card bill, and soon it starts rolling up every month and soon they find themselves paying minimum due amount and finally when things go out of control, they take a personal loan to close off the loan or convert the outstanding amount to EMI’s and starts how their debt trap starts!

Then follows car loan, home loan, another personal loan, another credit card and this way a person gets into deep debt cycle. I am sure if you look back, you will realize that the debt trap started very small.

Let me share some data with you on this. As per this report, personal loans as % of loans stands around 18% as in the year 2016 (Out of every 100 loans, 18 are personal loan).

As a young investor, you can still do mindless spending, but that should happen with cash money and not credit. Because getting into debt is easy, but coming out of it is not that simple. So as a young investor try to take debt only if you don’t have any choice. As far as possible, take responsible credit which helps you in life (education loan or home loan).

Mistake #3 – Not taking risks in start of your career

I am not saying that everyone should go and start taking some risk without planning. All I am trying to convey is that its more easy to take risk when you start your career, rather than middle of your career or when you turn 40, because in your early days you have less responsibility and enough time to fix your mistakes if any.

Think of these options below!

Want to move out of your industry and try something else?

Want to try a start up?

Want to try that online business idea?

Want to change your career path because you don’t feel you belong to current job?

Want to ask for a salary hike, but too afraid to lose the job

The above 5 things can be tried at any point of career, but practically you have more appetite to try out these things in the start of your life, when you have less responsibilities and enough time in hand to correct the mistake if any.

If you are still confused about this, you should listen to this YouTube video about best practices in Career Risk-Taking. It will help you

Once you have already spent significant number of years in your job, you will get married, have kids, get into the cycle of “life” and it will become very difficult to come out of the comfort zone. I get many mails which starts with “Had I tried it 10 yrs back … ” and I can see how people feel so stuck into their jobs and now they can’t take much risk at this point of life.

Mistake #4 – Buying policies from your relatives/friends

There are millions of investors in India, who have lost a lot of money in bad products which were sold to them by someone close to them. It was often an uncle, aunty, father’s friend, distant relatives or even your siblings at times.

A lot of products are bought in India based on trust and goodwill. Often relatives pressurize you to take a policy.

This is particularly true for Endowments policies, ULIP’s and other insurance products. You will often find someone in your close circle who is an agent and your parents trust them like anything and force you to buy a policy from them.

Years later you realize that you have burnt your fingers and can’t express your dissatisfaction openly. So what is the way out? Either research on things on your own or directly buy form the companies or if you need external help, better hire an advisor or an external agent, but not a relative

Mistake #5 – Investing in a product you don’t understand yourself

On an average, 90% of the investors can’t explain what exactly they have bought. I was once talking to an investor in our workshops (the upcoming one is in Pune on 22nd May, 2016) and the guy said he has few policies. When I asked how many? He had no idea

When I asked what are the names of the policy, he didn’t even know that.

He said that he had bought them few year back for tax saving and does not exactly know what they are !

The problem is that investing in products, which you don’t understand blocks your financial energy. Your money is stuck in a rotten product and takes away a lot of time.

So if you are buying a financial product, please learn how it works and how it’s going to benefit you at the end of the day . Find out everything about return, risk, liquidity and taxation. If possible, better know which financial goal it’s going to fund.

Mistake #6 – Not saving early in life

After spending many years in your job, you will realize as an investor that “I will save when I will have more money” is an illusion.

When you start earning money, your income is less and you are not able to save money at all because you are hardly left with anything at the end of the month.

However note that this is going to be true always. While your income will rise in future, so will your expenses. You will get married, have kids, your lifestyle will improve. You will get a car, buy a house and what not. You will enough feel that you have enough to save.

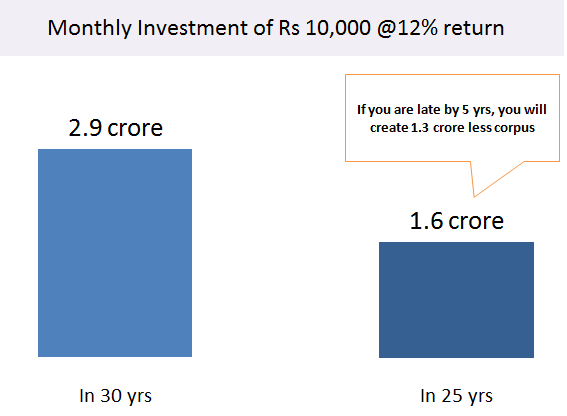

The graph for expenses is set to rise and this feeling of “I will save in future, when I earn more money” will be intact. This is the reason a lot of investor never save enough money which they deserve.

The graph below shows you if a person starts investing Rs 10,000 a month, they can accumulate around 2.9 crores in 30 yrs. However if they delay it for 5 yrs, and then start the same thing. They will accumulate only 1.6 crore by the same time. That’s a big difference because of the delay.

As a young investor, you need to understand that habit of “saving money” is more important than how much do you save. If you can’t save anything, start with Rs 100 per month.

I know it sounds like a joke. But once you do it for 5-6 months, you at east know that you can save Rs 100.

Then upgrade the number!

Upgrade to Rs 500 or Rs 1000 a month. Continue for another 6 month.

Soon, you will realize that you have reached Rs 5,000 or Rs 10,000 because you are just increasing the number, the “habit” was already in background.

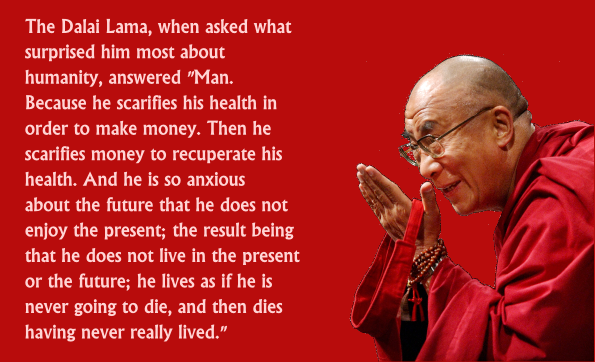

Mistake #7 – They neglect their health

If you do not have good health, it will not matter how much money you have earned, because you won’t be able to enjoy that money at all. It does not make sense to lie down on a bed made of gold in your retirement.

While earning money is important and required, make sure you also pay attention to your physical and mental health. These days, the jobs are too demanding and there are many money matters which will take the peace out of your life. You might get lost in the rat race and forget that you have a body to take care for years.

Only years later you will realize that it would have been better to earn a bit less and have a healthy body, rather than having bad health with money.

The quote from Dalai Lama is worth reading

Learn from others mistake

At this point of time, internet is flooded with the mistakes other investors have done. It’s a wise thing to learn from those mistakes and not repeat them.

A good and healthy start of one’s financial life helps a lot and if you are a starter, I strongly suggest you take a note of the points above and implement them.

Please share your views on the points above. Were they helpful to you as a new investor?

Our full day workshop is BACK in PUNE on 22nd May 2016 (Sunday).

We invite you to block 22nd May (just one Sunday) so that you can participate in our one day workshop. We are inviting you because our workshop will add a lot of value to your existing financial life. So far we have seen and observed that our workshop helps investors to add new and different dimensions to their financial world. In the whole process they learn to slow down so that they can examine what’s going on in their financial world. With our help and support they also define and adopt new set of actions and strategies to create an amazing financial life.

Our last workshop was done in the city of Hyderabad and it went very well. So now we are back in Pune this time.

Why we conduct these workshops?

We do offline workshops so that we can connect with some of our readers at a deeper level, round the year we write articles, reply to thousands of comments and work with a few hundred investors one on one and in that process we learn, grow and expand as professionals. Our Workshop gives us an opportunity to share outrageously all the knowledge and experiences that we acquire round the year. The program is an opportunity to get our readers more and more action oriented.

Why you should come for this workshop?

You will learn how to improve your financial life with your current set of resources and income.

You will learn how to plan for your financial life goals

You will interact and learn from other’s people’s financial life

You will dedicate one full day to get better with money management

You will learn to add new dimensions to your financial life

To understand that personal finance can also be fun

To give a whole new direction to your financial life

It’s time at add jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and the experience has been amazing. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation. We do not teach tricks and tips to build wealth in fact we help you to discover your own personal process of creating wealth.

This time we want more and more couples to participate so that they can get on same page when it comes to personal finance. It is extremely important that husband and wife both take equal interest when it comes to money management. We are offering special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct are highly interactive, it has lots of activities and fun exercises which helps you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short there is something for everyone in this workshop.

Listen to workshop Participants who attended in Past

Register for Pune workshop on 22nd May, 2016 (SUNDAY)

8:30 am - 6:00 pm , 22nd May (Sunday) , 2016

Ramee Grand Hotel, Apte Road

Shivaji Nagar, Pune

The hotel is very near to Santosh Bakery, on the main Apte Road

Lunch and Breakfast is included in the program fees

What you get as a participant?

You get a FREE Financial Health check-up Report worth Rs 499

One day workshop with some personal finance tools like budget sheet, Mutual fund tracker etc

Invitation to join our inner circle

Invitation to join and participate

From the bottom of our heart, we invite you to join and participate in pune workshop. Come alone or with your spouse or parents, siblings or friends but see that you do not miss this opportunity. Do not let time and money to get in your way and book your seat at the earliest because we will be taking only 35 participants this time and registration will close after some days.

This workshop is strictly for investors and not for advisors or finance professionals. This workshop is strictly for investors and not for advisors or finance professionals. Incase we find some financial advisor/planner or anyone from personal finance background registering for the program, we will refund the fees. We hold the right to admission to this program

If you have never participated in any personal finance workshop let this be your first workshop. If you have any questions you can write in the comments section.

Last year we got around 15695 emails from investors asking for help in buying different financial products. In all mails one thing remained common; people wanted jagoinvestor’s green signal before taking any major decision in their financial life.

We have observed that majority of people land on jagoinvestor out for searching for some product on google and then they subscribe to the blog for on-going education. Buying right financial product is extremely important step, because it can make or break anyone financial life.

Hence we thought of making a network of various partners whom we trust ourself. We are happy to now announce Jagoinvestor Solutions, which will help you in taking different personal finance decisions with the help of our network of trusted partners

[su_button radius=”auto” size=”8″ background=”#08B724″ url=”https://www.jagoinvestor.com/solutions”] Go to Solutions Page [/su_button]

To make buying products easy and safe for investors

To help investors in making right choices with quality advice

To protect investors from mis-selling

To help investors get best available options

Who is a trusted partner?

The personal finance choices you make today will determine your financial future and so it is extremely important to make right personal finance choices. In a nutshell, trusted partners will help you in making right personal finance choices. Our Trusted partner will help our readers in buying financial products that suits their requirement. Each Trusted partner has collaborated with jagoinvestor to serve readers of jagoinvestor in the most authentic way. They will understand the exact requirement of an investor and will craft a solution for each individual.

Internal Screening Process before choosing trusted partner

We have done background check and checked credibility of our trusted partners

We have studied and verified our trusted partners business model

We have seen their style of working

We make sure that we pick one of the best and high brand value in each category

We make sure that our trusted partners go an extra mile to serve investors community

They are the best in the industry when it comes to advice, basket of products and service

How does the Jagoinvestor Solutions work?

Step 1 – Choose a solution and leave your basic details

Step 2 – Trusted partner will get in touch with you

Step 3 – You decide if you want to move ahead and complete the action or not

Products/Services right now added to Jagoinvestor Solutions

We have various services and products under solutions right now which are

[su_button icon=”icon: heart-o” size=”6″ url=”https://www.jagoinvestor.com/solutions/buy-life-insurance-plan” onClick=”Testing”] Buy Life Insurance [/su_button]

[su_button icon=”icon: medkit” size=”6″ url=”https://www.coverfox.com/jagoinvestor/health-insurance/” onClick=”Testing”] Buy Health Insurance [/su_button]

[su_button icon=”icon: heartbeat” size=”6″ url=”http://goo.gl/6OOrFl” onClick=”Testing”] Cancer Care (Critical Illness) [/su_button]

[su_button icon=”icon: exchange” size=”6″ url=”https://www.jagoinvestor.com/solutions/apply-home-loan-transfer” onClick=”Testing”] Home Loan Transfer [/su_button]

[su_button icon=”icon: random” size=”6″ url=”https://www.jagoinvestor.com/solutions/apply-loan-against-property” onClick=”Testing”] Loan Against Property [/su_button]

[su_button icon=”icon: university” size=”6″ url=”https://www.jagoinvestor.com/solutions/open-saving-bank-account” onClick=”Testing”] Saving Bank Account [/su_button]

We are confident you will surely get benefited by our new initiative. See that you bookmark solutions page and also share the same with your friends and loved one’s. We will continue to create more trusted partners in near future to serve investors community more strongly.

There are many different kinds of tax paid by us in India; however, we don’t have a lot of clarity on each kind of tax and what it means. Hence I thought I will give a brief overview of the overall India taxation system. So in this post I will explain various kind of taxes one by one and their categories.

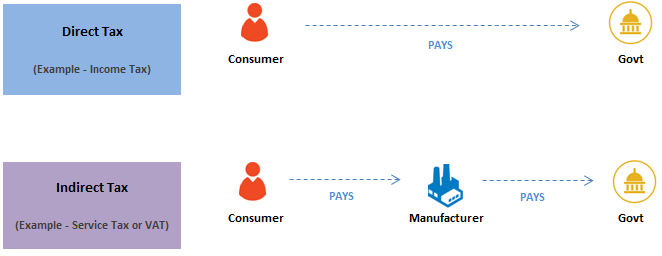

Direct Tax vs. Indirect Tax

Before explaining each kind of taxes, first understand that there are two categories of taxes, which are called direct tax and indirect tax.

Direct Tax – As the name suggests, Direct taxes are those taxes that are directly paid by the person/entity to the government. The best example for this is – Income Tax, where we have to pay the income tax on our earned income to the govt directly at the end of the financial year.

The direct taxes are the one that pinches the investor’s maximum because they clearly see it going out of their pocket.

Indirect Tax – Indirect taxes are those kinds of taxes, which are collected by govt from the intermediary or manufacturer, but eventually which is passed to the users only. So we pay these taxes also from our pocket, however, it’s taken from us in a very indirect way by including it in the price of the product itself. So we always hear the final price (price + tax) and it does not pinch us a lot because most of the time we don’t even realize that we are paying that tax.

A good example of this is “Service tax”. So when you go to a restaurant, you can see that the service tax is added to the bill and you make the payment for it. The hotel then pays this service tax to the govt only.

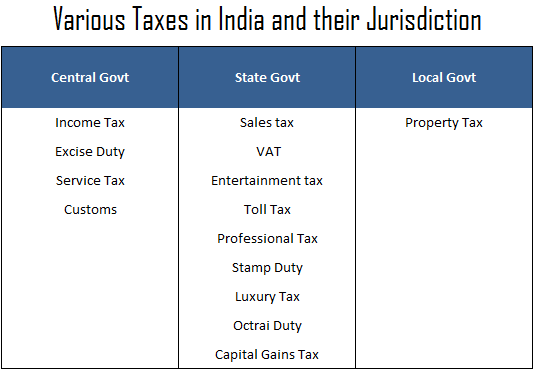

Jurisdiction of Taxes – Central, State and Local

You already know that India has federal structure and there are governments at center and different states and they have to arrange for their own income from various sources. So taxes fall under 3 jurisdictions, which is

Central Govt

State Govt

Local Govt

So some taxes go to the central govt and some go to state govt and few goes to the local city municipality. The below chart gives you a crisp idea about it.

10 types of Taxes we pay in India

We will now see various kinds of taxes we pay in India. I will explain each of them. We will first see the major taxes which impact us in a big way and which are the major taxes from which govt gets the revenue, then we will see the other taxes in brief

1. Income Tax

The tax which everybody is aware of is Income tax. This is levied on the income earned in a year by an individual or a business body. The 12 month period considered for the taxation is from Apr 1st to Mar 31. The incomes is categorized under 5 heads namely

Salaries

House property

Business Income

Capital Gains

Others

A person has to hence, find out all their income and see which heads they are falling into. For most of the people who are salaried class, it’s only one head “Salary” and a bit on the “Others” section like interest income from FD, saving bank account or dividend incomes.

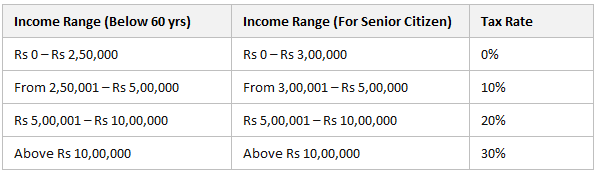

The income tax for Individuals is calculated based on the different slabs, which are as follows

So if a person salary is 8 lacs per year, there will be no tax on the first 2.5 lacs, Then 10% tax will be applicable on the income from 2.5 lacs to 5 lacs, which will be 25,000 and 20% on the income from 5 lacs to 8 lacs, which is Rs 60,000, totaling his income tax to Rs 85,000 for the year.

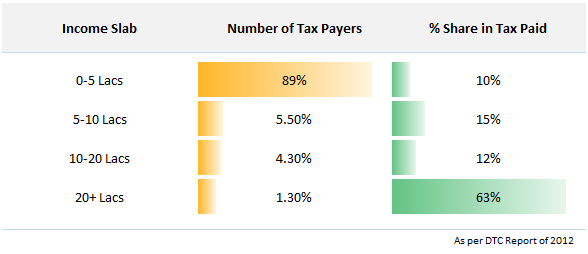

Below is a snapshot of income categories and number of people who fall under them along with the % share of their income tax as of 2012

Income tax is something that almost everyone is aware of because one has to deal with it directly.

2. VAT (Value Added Tax)

The VAT is an indirect tax levied by a state when some good is sold within the state. So if some goods are sold within Karnataka (Bangalore -> Mysore), the Karnataka Govt will levy VAT on the goods sold.

The VAT is a tax that is not very visible to a common man in their day to day life, but it’s presence in almost every sector and goods. Each small thing which we consume today has gone through multiple stages of production and VAT is paid at each stage by the manufacturer and eventually, the final consumer pays for it (Bundled within MRP)

For example, when you buy a mobile phone, you also pay the VAT, which goes to the govt but paid by the seller. The seller actually gets a lesser amount. For example in the below example, you can see the invoice of an Asus Zenfone mobile bought online by my wife. You can see that out of Rs 10790 which was paid, Rs 1325 (14%) was the VAT which went to the govt.

Note that VAT rates are subject to states, hence the rates change from one state to another. This is the reason why some goods are cheaper in one state and expensive in another.

CST (Central Sales Tax)

Note that VAT is a state-level tax, however when a good is sold from one state to another, then the tax is called CST or Central Sales Tax which goes to the central govt.

So when a seller in Maharashtra sells some goods to a consumer in any other state (like Tamil Nadu), then it’s not the VAT, but CST which applies and it goes to the central govt wallet 🙂

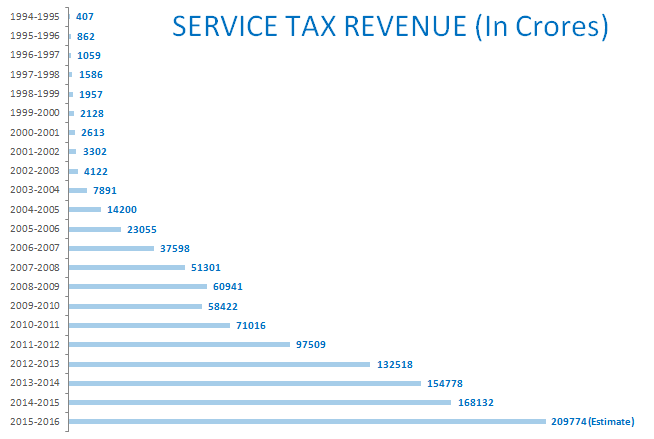

3. Service Tax

Service tax is another very important tax which was introduced in the year 1994. It’s a tax charge for providing services. Like in the case of restaurants, when they serve us for food, they are providing us a service, hence we are charged service tax on a certain portion of bill amount.

In the same way, when you hire the services of a consultant, they will charge you a service tax and pay it to govt. It depends if they have charged you the service tax on top of the fees or they have included the service tax in the price itself and tell you the final amount. In any case, the service tax is to be paid to govt if the revenue of the service provider is more than 10 lacs in a financial year.

Increase in service tax revenue in India

Over the last decade, service tax has become of the major tax collected by govt and it has been increasing year on year. It’s mainly because the number of services on which service tax is applicable has been increasing year on year in the last decade and even the rate has increased. At this point in time, the service tax applicable is 15% (including the Swachh Bharat cess of 0.5% and Krishi Kalyan cess of 0.5%).

Below you can see how the service tax revenue has increased in the last 20 yrs.

Negative List concept in Service tax

A few years back, there was a list of services that were issued by govt, on which service tax was applicable, and if a service is not on that list, it was not applicable. However a few years back, it’s changed and now a “negative list” concept in introduced, which means that service tax is now applicable to every service which exists.

Only on a few services which are part of the negative list will be exempted from service tax.

Service tax is now part of our day to day life. We eat in restaurants, stay in hotels, and take various kinds of services every month/year and if you calculate the total amount of service tax you pay, you will be amazed to see the number.

4. Excise Duty

A few years back, when I used to see the budget speech, I eagerly waited for the income tax-related announcements and wanted to know is 80C limits have been raised or if tax limits are changed. I happily ignored “excise duty” related announcements because frankly speaking, it made no sense to me.

How does it matter if to me if the excise duty on mobile handsets was increased? I never understood what all that means. However now I know how important excise duty is for the govt and what is it related to common man.

Excise duty (also called CENVAT) is the tax which is levied by govt at the time of manufacturing of the goods. It’s as simple as that. It does not matter if you hire someone to manufacture the goods or you do it yourself, but if you manufacture some goods, you will have to pay the excise duty if your turnover exceeds Rs 1.5 crore.

Now obviously, the excise duty is a cost for the manufacturer and it’s eventually passed on to the consumer. If excise duty didn’t exist, the prices of the goods would come down by that much margin.

So assume you start manufacturing some goods at mass scale, and if it’s in the list of the “excisable goods”, which means goods on which excise duty applies, one has to pay the excise duty to the govt. So if we take an example of cars, as it’s a big-ticket item, even a slight change in excise duty means the prices go up by a big amount.

See the example below

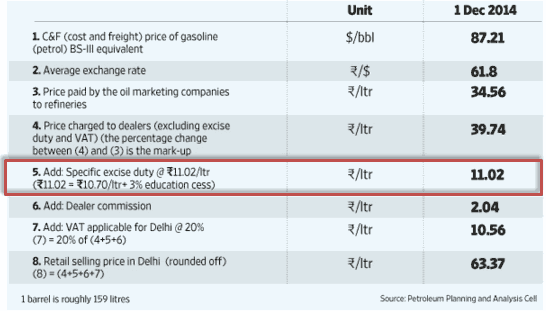

Excise Duty on Petrol & diesel

Let’s understand this better with petrol & diesel prices. The raw petroleum which is bought by the oil companies is the base price. After that when they refine it and convert it to the usable petrol and diesel, VAT and Excise duty is applied which increase the final price of the petrol, add to that the dealer commissions and we get the final price which we pay.

The chart below shows the breakup of petrol prices (for the year 2014).

Excise duty is one of the biggest revenue generators for the govt because the amount of manufacturing which takes place all over the country is huge.

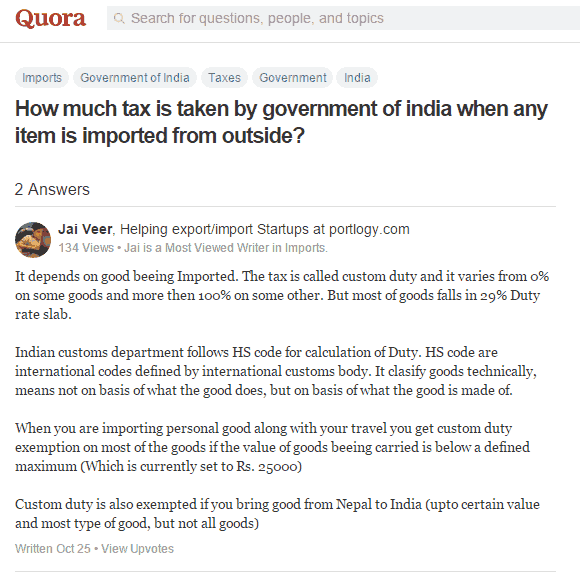

5. Customs Duty

Customs duty is the tax levied on the items imported from other countries to India or exported out of India. So when you buy something from Amazon US and want it to be shipped to India, you are actually importing it, and hence a custom duty will be charged separately.

Below is a duty rate for various products categories which is taken from this website

Category / Product to Import

Total Duty Rate

Laptops, Notebooks, Computers

14.712%

Tablets, iPad

28.852%

Laptop Battery

23.852%

iPod, Music Players

28.852%

Software CDs and DVDs

10.300%

Computer Printers

14.712%

Electronics

28.852%

Hard Disk (internal)

6.300%

Hard Disk (external)

14.712%

Web Cameras

28.852%

Computer Processor

6.300%

Internet Modem

14.712%

Other Computer Peripherals

14.712%

Cables and Wires

23.852%

Television Sets (TV)

28.852%

Movie CDs, DVDs, and Blue Ray

28.852%

Video Games and Game Consoles

28.852%

Mobile Phones

~18%

Phone Accessories

28.852%

Digital Cameras and Video Camcorder

28.852%

Camera Lens (Photography)

28.852%

Sports Equipment

14.712%

Books (Educational)

Free (No duty)

Car Parts

28.852%

Toys and Games

28.852%

Stationery Items

28.852%

Cosmetic Goods

28.852%

Hand Watches (Wrist Watches)

28.852%

Sun Glasses

28.852%

Apparel (Clothes)

28.852%

Fashion Accessories

28.852%

Artificial Jewellery

28.852%

Shoes (Retail Price < 1k INR)

21.782%

Shoes (Retail Price > 1k INR)

28.852%

Kitchen and Dining

28.852%

Food Supplements, Body Building

28.852%

Medicine

28.852%

No Custom duty up to Rs 25,000 while travelling back to India

Note that if you are coming back to India, then up to Rs 25,000 worth of goods can be brought back without any customs duty, but beyond that, you will have to pay the duty. This is applicable to most of the items. You can read more about this below in an answer given by Jai Veer on Quora

We have now covered major 5 taxes which needed more detailing and explanation, now we are going to see other taxes, but we will now see them in a crisp manner and not go too much into detail

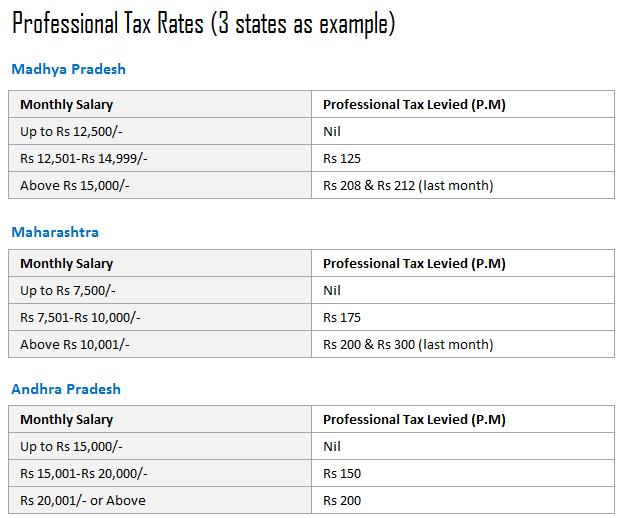

6. Professional Tax

Professional tax is levied by the state govt for all the salaried employees and some professionals like CA, Lawyers, etc. If you see your salary slip, you can see the amount of professional tax deducted. Note that the tax slab depends on the state in which you are working and the amount of salary you have per month.

Every state has different slab rates. Below is an example of a few states.

Many states do not have professional tax, for example – Punjab, Uttar Pradesh, Rajasthan, Haryana and many more.

7. Capital Gains tax

Capital gains tax is the tax which is levied on the gains which are raised by the sale of a capital asset like property, vehicle, jewellery, bonds, land or machinery.

This tax is not applicable each year, but only in the year when the capital asset is sold or transferred to some other party. The gains are categorized as either short term capital gains or long term capital gains depending on the duration you hold the property.

Here is a very good video on this topic which explains capital gains.

The calculation for this tax is not very straightforward and involves a bit of work, hence we are not covering it here. As of now, just understand that if you purchase a property at cost C , and sell if after some years at sale price S. Then your capital gains will be calculated and you will have to pay tax on that.

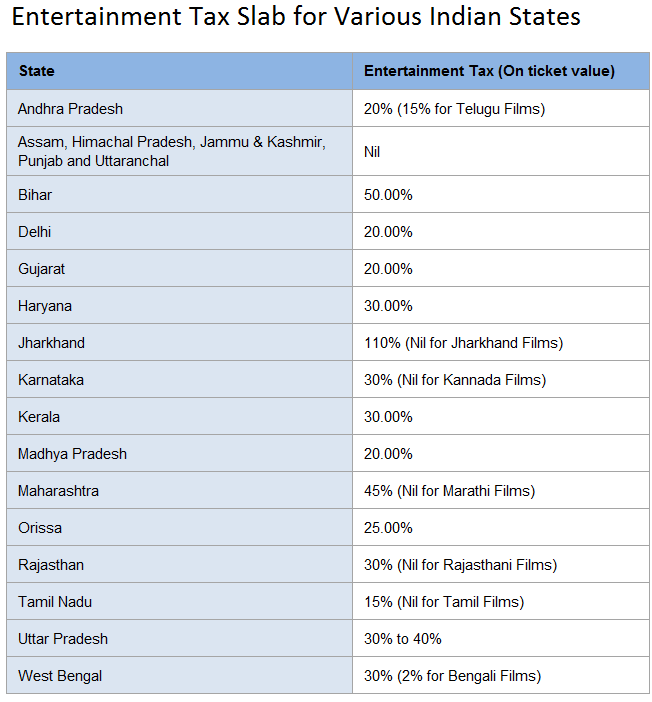

Entertainment tax is the state-level tax levied on the tickets for the cinema and other entertainment shows. It’s also levied on the stage shows, amusement parks, and many sports activities. Most of us can relate the entertainment tax with the movie tickets. If you see your movie ticket closely, you will see that a good chunk of the cost goes into the entertainment tax.

Maharashtra charges one of the highest entertainment tax at 45% and I am not very happy with that because I am a movie buff. However, some relief for me, because I see a lot of Marathi movies too (which are exceptionally well most of the time) and which does have entertainment tax (regional movies generally don’t have entertainment tax in the home state).

Below you can see the slab rates for all the states in India for entertainment tax.

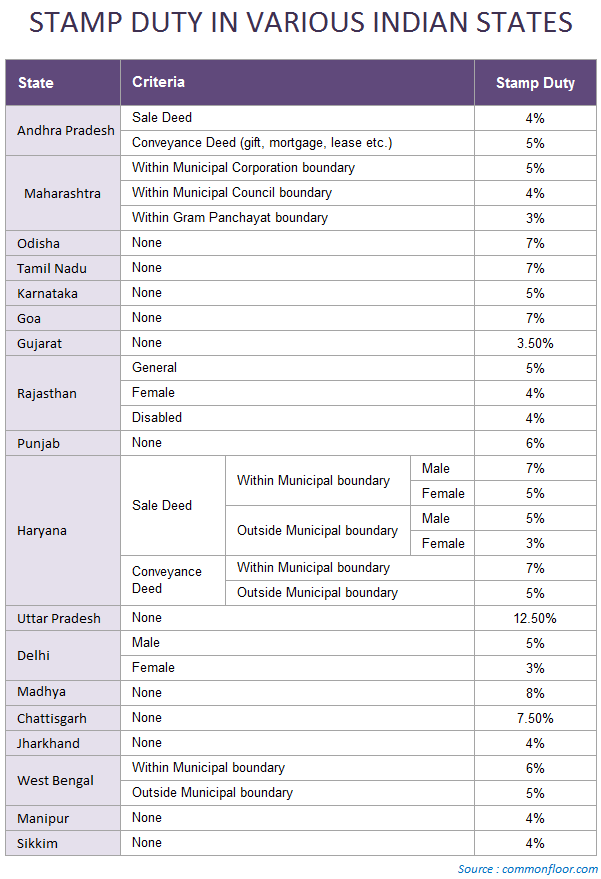

9. Stamp Duty

Stamp duty is a kind of tax which is levied when a legal document is executed. Most of us can understand it in real estate terms. So when we buy a property and we execute the agreement to sale, the stamp duty is charged as a percentage of the property value which is mentioned in the agreement or the govt ready reckoner rates whichever is higher.

Most of the time this stamp duty is in range of 4-6% depending on the state. This stamp duty is paid every time a sale is made in property, which means if the same property exchanges hand 5 times in 10 yrs period, the govt will get the stamp duty 5 times. Below is the slab rate for stamp duty in various Indian states.

Note that this data is a bit old and there might be slight changes at present, so please consider the chart below only as a reference point.

Hence, this way stamp duty becomes a revenue source for the state government.

10. Property Tax

Property tax is the tax paid by property owner every year. This tax is a local municipal level tax and the rate is decided by the local municipality. The amount of tax depends on various factors like the size of the property, kind of property (residential or commercial), age of the property and many more.

Just for reference, in a city like Pune, I know that the property tax for a 2 BHK flat comes around Rs 8,000 to Rs 15,000 approx.

Conclusion

Apart from the taxes above, there are various other small taxes that are paid from time to time like toll tax, dividend distribution tax, securities transaction tax, luxury tax, and Octroi. We have not covered them in this article, but you can read about them separately

Let us know what do you think about the tax system in India and if you feel you are over burdened with taxes?

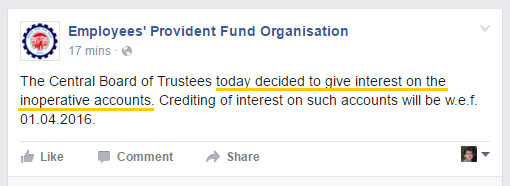

Good news, the inactive EPF accounts will now get interest from next month, i.e. Apr 1, 2016. Around 5 yrs back, under UPA rule, EPFO came up with the rule that any inoperative EPF account will stop getting interest after 3 yrs of inactivity.

So if a person left the job and never withdrew the money, he would stop getting the interest after 36 months. Inactive accounts are those accounts where there is no addition from employer or employee side. Now that old decision is reversed. There was a meeting of Central Board of Trustees at EPFO and this decision was taken.

A lot of employees will be happy due to this change because at a lot of people do not want to withdraw their EPF and still want to earn the interest. Also the withdrawal/transfer process is a bit cumbersome and many investors do not want to take the pain and let their accounts be there.

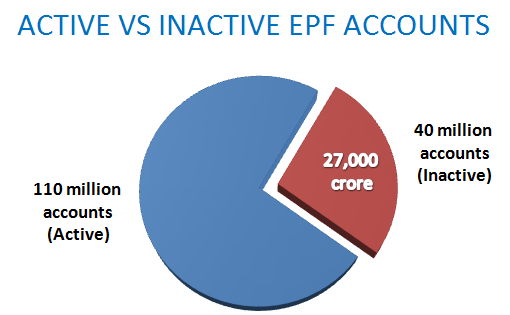

Inactive vs. Active EPF Account

As per a report, around 27,000 crore is lying in 40 million inactive EPF accounts (total accounts = 150 million), This money will now start earning interest.

That time many people were confused if the interest will be given to them or not if the accounts become inactive? Now that confusion is also cleared.

65% investment in G-Sec

As per this report, there is one more change in the way money will be invested by EPF in G-Secs

When asked about a proposal on enhancing proportion of incremental investments of the EPFO in government securities (G-Sec) from 50 per cent to 65 per cent, Labour Secretary Shankar Aggarwal said, “It has already been decided by the Ministry of Finance.”

The Secretary said that the limit of 50 percent was enhanced as they were getting good offers but unable to invest in such instruments as the limit had been exhausted.

“If we get higher returns in G-Secs then we should be allowed to invest more in these instruments,” he said further.

Yes, you heard it right!. I want to just explore the role of money in our life and how it changes our thought process. I want to know how we think about money. I will share some really interesting insights I got by surveying 2440 people on some creative questions related to money.

I am sure you are going to enjoy this article and also get some takeaways at the end on how others feel about money. Our financial lives are very private to us. Our income, our struggle with money, our desires in financial life. All this is very secret to us. You do not know how hundreds and thousands of other people like you think when its related to money.

Do they share the same feelings as you? Do they also feel scared about the future? Do they also have stress like you in their financial life?

I will show you 8 amazing insights I got from this survey

Role of Money is our life

Money has a very important role to play in our lives. In a way, it’s one of the most important ingredients you can say. We need money for almost everything today. What we will ear, how others will perceive us, how famous we might be in our friend’s circle and if a father will be interested to give us his daughter or not?

Money has a big role to play in all these points which I mentioned above.

Money has in a way controlled our lives these days. We start our day going to work for money, a lot of people are into jobs they don’t like, but the EMI’s are to be paid anyways, so we continue.

There are many examples in life, where a person is amazing at X, but they are doing a job in the Y domain. The reason being MONEY. Money turns wonderful people into a monster. Money is a wonderful thing, but at the same thing a very dangerous thing too.

Our interaction with money

When we were kids, we had very little interaction with money. We got it from our parents and used it, we didn’t earn it and our notion about money was different. But once we get into the role of a breadwinner, only then we realize the game and how money turns us into a completely different person.

One of the best quotes to understand the effect of money in our lives is the below quote by Dalai Lama

Survey with 2440 people – Results

Let me not bore you too much with my views on money and rather look at how people think about money and what impact it has created at their thinking level. I will now take various things I asked in the survey and share the results with you

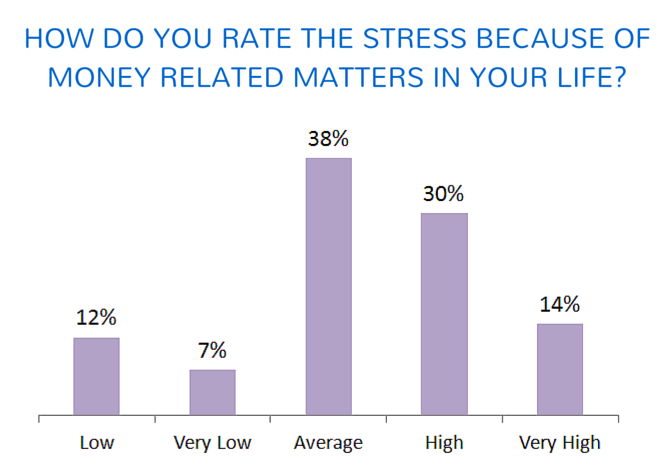

Insight #1 – How do you rate the stress level because of Money Issues?

One of the biggest problems in today’s times is STRESS. Stress at the office, the stress at the home and everywhere and a lot of times, you will realize that money has a big role to play there.

Oh my god, How will I pay my EMI’s if I lose the job?

Will I ever be able to buy a home with this salary?

I am already 38 and have not saved a penny, How will my retirement look like?

Many such kinds of thoughts occupy the minds of today’s generation. When I asked this question – “How do you rate the stress because of money related matters in your life?” Here are the survey results

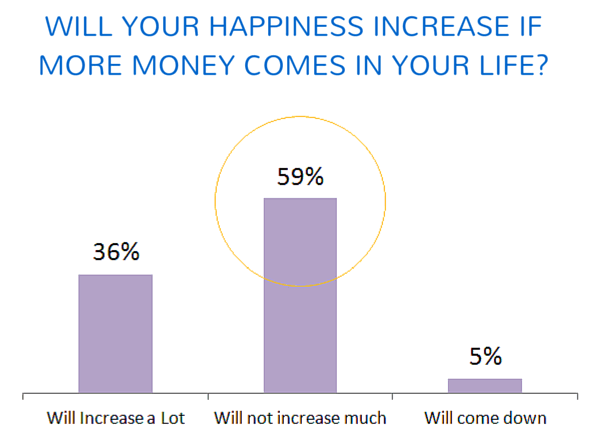

Insight #2 – Does more money means more happiness in life?

So we all are running after money day and night, thinking that money will solve all our worries and problems. However, those who have earned a good amount of money know that it’s true only to some extent. A rather correct statement would be “Absence of money leads to unhappiness”.

Yes, money is very very important and damn!, I also need tons of money and sure it can buy you all those things which can give you lot of happiness and make you feel like the king, but then beyond a point your happiness graph will start to appear flat even if more money comes into your life.

And this is confirmed by the survey results. 59% of people have said that more money will only lead to only a partial increase in their happiness and not beyond a point.

And trust me, if you have not earned a lot of money till now in your life, this statement will look like an idiotic one right now. If you are earning Rs 20,000 a month, surely Rs 2 lacs a month will mean 10X happiness, but will 20 lacs a month mean 10X more happiness from that point? I don’t think so? What about 2 crores a month? Salman also earns that !, Vijay Mallya also earns that as well. I am sure they have many issues in life!

This topic alone is worth a full book in itself, but we will keep it short as of now.

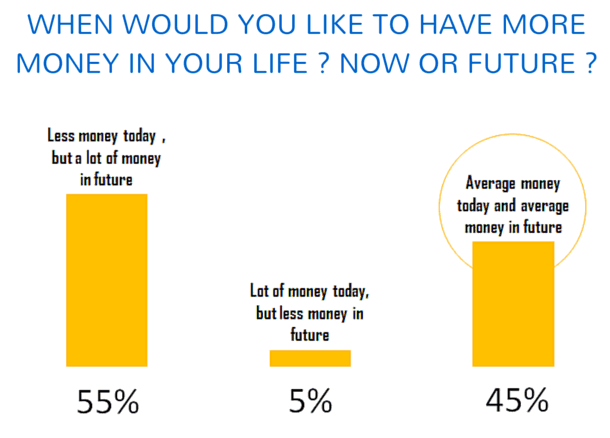

Insight #3 – Which option will you choose, More money Today or in the Future?

Most of us want a lot of money in our life. Surely more than what we have today. But we all know that it’s not going to happen suddenly? You either have to sacrifice your today to build wealth in the future, or you can enjoy all your money and retire poorer. Or there is a 3rd choice that you keep a balance between today and tomorrow. So given a choice between these 3 options, which one will you chose?

This was no brainer question in away. Around 55% of people chose that have a better future and are ready to compromise today, may be because they know that in the future they will have fewer means of earning and it looks natural. We all want an assured future.

However, 45% of people said that they just don’t want their future with lots of money but even their present. So they want average money today and average money in the future also, making sure that there is a good balance today and in the future.

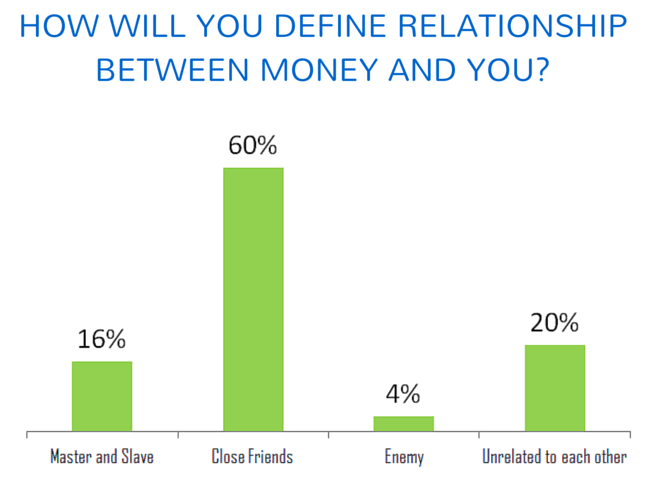

Insight #4 – What is your relationship with money?

Have you ever wondered what your relationship with money is? I first came across the term “Relationship with money” from my partner Nandish Desai, and I am thankful to him to share it with me. I added a new dimension to my thinking. He has also contributed a full chapter on this topic in my first book – “16 personal finance principles every investor should know”

Money or wealth is a non-living thing, but still, we have a certain kind of mindset towards it. We have some kind of “relation” with money. Imagine money as a human standing in front of you, do you see a friend or an enemy? Do you see it as a master and you as slave or you don’t feel any relation with each other.

I was happy and a bit surprised to find that around 60% of people who took the survey identified their relationship with money as “Close friends” . It’s a great thing that most people see a positive relationship with money. However, a lot of people who have messy financial lives don’t share very good relationship with money.

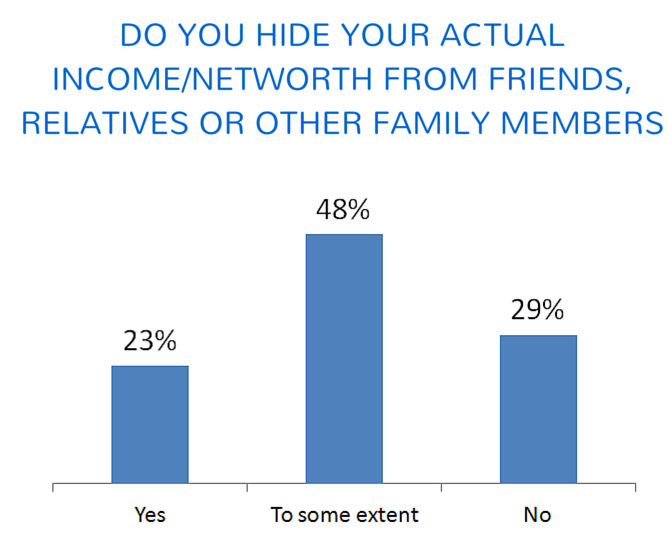

Insight #5 – Do you hide your wealth from others?

How many people know your exact salary? How many people know the exact net worth you have? How much you have in your bank account, or your mutual funds or other assets? Do you under-report it to your friends, relatives or even some close family members like your siblings and even parents? Spouse?

Seems like most of the people do. Only 29% of people said that they don’t hide it from others, but rest others hide it. while 23% said coldly YES to this question, around 48% said that they do it to some extent.

No wonder that this happens. There may be many issues which can happen if the world knows that you have a lot of money. Some might just expect “help” from you, some might ask it directly and unnecessary attention and expectations come across which most of the people want to avoid.

No wonder, most of the people want to keep a low profile when it comes to showcasing their wealth.

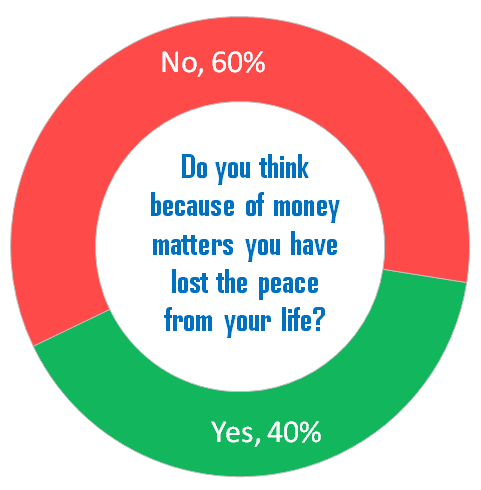

Insight #6 – Have you lost peace in life due to money issues?

A lot of people are very stressed because of money matters. Someone from low income and high expenses, while someone might be due to medical expenses while is costing them all their income each month. Someone might be under debt which was passed to them from their parents and they are paying for it. Someone might have lost money in some scam and someone might not be able to fulfill their loved one’s wishes due to money constraints.

Like I said earlier, lack of money might make the life hell in this competitive world. Around 40% of people say that they don’t find peace in their life due to money issues. They felt they have lost it. Think about it. It’s quite a big number, so every 4 out of 10 people is stressed out and does not feel relaxed.

Let me know what do you think about that?

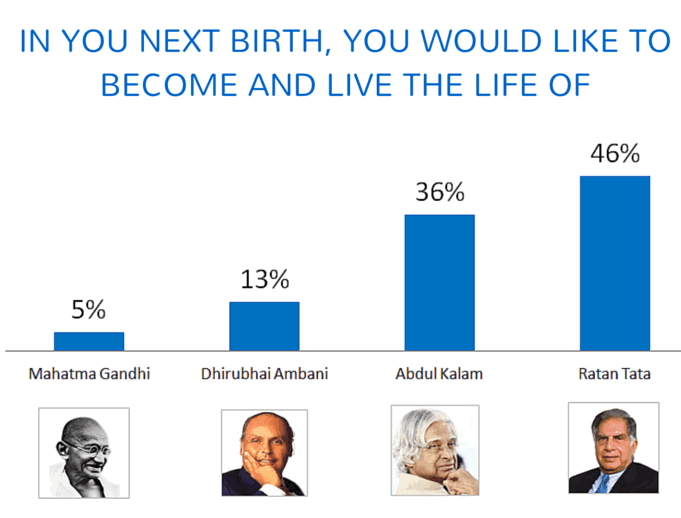

Insight #7 – In the next birth, who would you like to become?

I wanted to know what people aspire to be and what kind of life they want to live in reality. So I asked a very different kind of question, that if they got a chance, then in their next birth whose life they would like to live? I gave 4 options as below who are all very famous for whatever they have done in their life, some are respected because of what they have done for our country and some are known for wealth or both.

The options were

Mahatma Gandhi

Dhirubhai Ambani

Abdul Kalam

Ratan Tata

For a second, without looking at the results below, think for a moment about yourself. If you got a chance, whose life would you like to live in your next birth?

Here are the results and they might surprise a few of you.

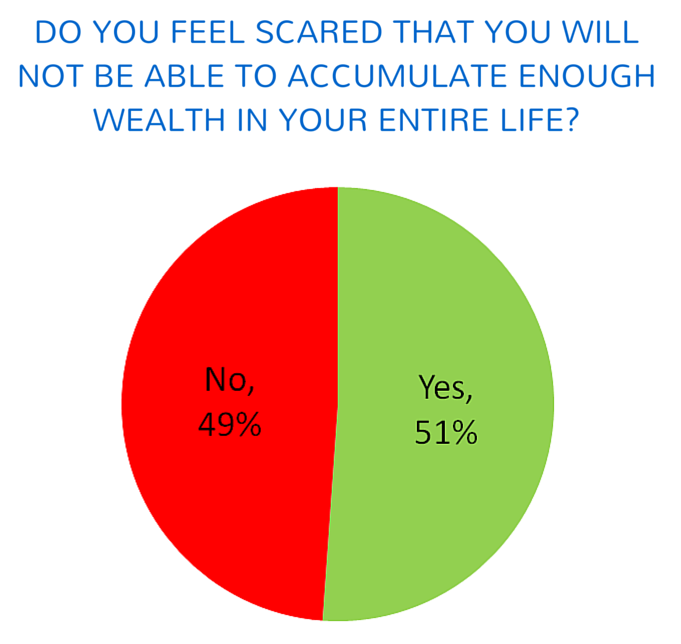

Insight #8 – Are you scared that you won’t be able to accumulate enough wealth in the future?

No matter how good your career is going or if you are earning decent enough right now, there is always a bit of anxiety about the future. We have no idea how things will turn out in the next 10/20 yrs. Because of rising inflation, and multiple expenses people do not save the amount which they deserve and they are always scared if things will continue this way ever?

So I wanted to know how many people are scared of future and they think that there are chances that they might not accumulate enough wealth in their lifetime which is required for leading a great life they desire. Here is what people say.

Around 51% of people said that they are scared of this.

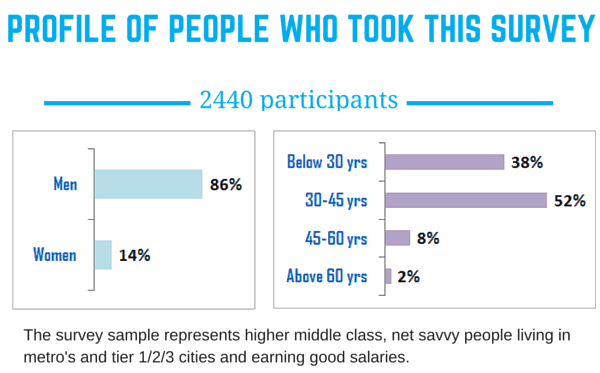

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.

With this, I would like to end this survey here. I would like to know what you feel about this survey and if you got any insights on how other people think in this country. I would like to mention very clearly that the survey size was 2440, which is surely not the representation of the entire country, but it’s a good enough sample size for the net-savvy higher middle-class people who live in big cities earning decent salaries.

The government has cut the interest rate on Public Provident Fund from 8.7%to 8.1% effective April.

This was part of the interest rate cuts in the small saving schemes and apart from PPF, other very famous instruments like Kisan Vikas Patra, Senior Citizen Scheme & NSC interest rates have also come down by a good margin.

These new rates will be applicable from Apr 1st. Please note that this is one of the biggest rate cuts in the small saving schemes in a long time.

Here is a summary of all the rate cuts

Kisan Vikas Patra interest rates down from 8.7% to 7.8%

NSC interest rates down from 8.5% to 8.1%

Senior Citizen Saving Scheme interest down from 9.3% to 8.6%

5 yr NSC (National Saving Scheme) interest down from 8.5% to 8.1%

1 yr time post office deposits has been cut from 8.4% to 7.1%

2 yr time post office deposits has been cut from 8.4% to 7.2%

3 yr time post office deposits has been cut from 8.4% to 7.4%

5 yr time post office deposits has been cut from 8.5% to 7.9%

Postal saving deposits remain unchanged at 4%

Interest rates aligned with market rates

On Feb 16, 2016 (before the budget) itself the govt had announced that they are working towards bring the small saving interest rates closed to the market rates, but that time no changes were done in these schemes.

The government had on February 16 announced moving small saving interest rates closer to market rates. On that day, rates on short-term post office deposits was cut by 0.25 per cent but long-term instruments such as MIS, PPF, senior citizen and girl child schemes were left untouched.

Now the interest on these schemes is closer to the interest rates given by the banks.

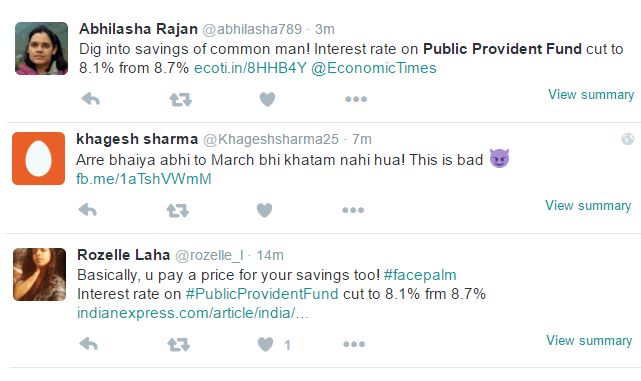

I will leave the decision to conclude if this was a good or bad move by govt on you, however the common man is not very happy with this. Messages against this move are are all over the twitter.

What is your reaction to this?

Majority of investors in India invest in Public Providend Fund (PPF) scheme and it’s very close to their heart. However this move will make many people think if PPF is the best thing they can do with their money or not (learn how PPF interest rate is calculated).

Will they move to equity markets because of this move? Will it make them interested in other kind of financial products?

What do you think? Do you think of this big interest rate cut in PPF and other schemes? Please share your views in comments section.

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.

Below you can find the profile of the people who took the survey. Around 90% of survey takers were below the age of 45 and only 2% were senior citizens. Around 14% of survey takers were women, which is low in a way and should improve.