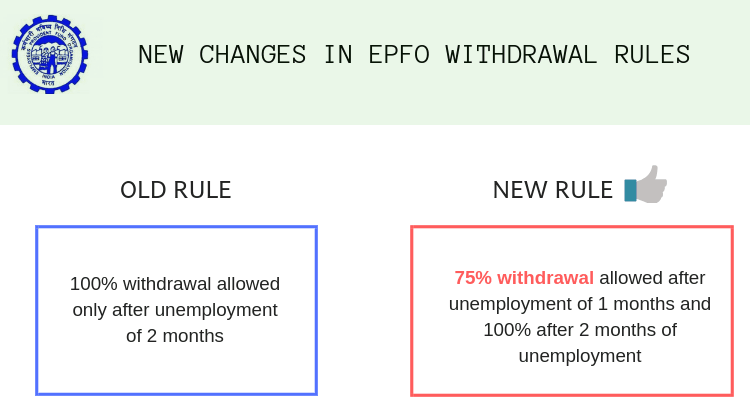

EPF is a long term retirement saving scheme. Therefore, it can be withdrawn fully(100%) only after retirement. And early retirement is not considered until the person reaches 55 years of age. However, if you get unemployed for a period of not less than 2 months, then as per the old rule of section 69(2) of the EPF act, you can withdraw 100% of EPF balance outstanding in your account.

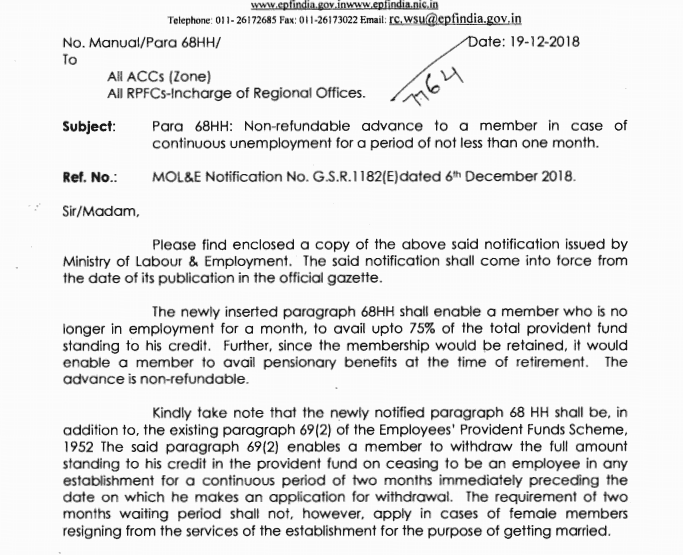

A new clause, 68HH has been inserted after para 68H in the 1952 EPF act

As per this, If a person has been unemployed for a period of not less 1 month can withdraw upto 75% of EPF balance outstanding in his account as on date. The section says that, even after such withdrawal is made, the person shall remain part of the EPF and eligible for pension benefits. However, the advance cannot be remitted back into the EPF i.e. it will be non-refundable.

In addition to this, the circular clearly states that para 69(2) (old rule) is still continuing. That means, after two months of continuous unemployment, 100% of EPF withdrawal is allowed. However, the waiting period of 2 months does not apply in cases of woman retiring from services for the purpose of getting married. The snapshot of circular is given below,

Do you think this small change in the rule of EFP withdrawal, would be beneficial on a larger scale?? Let us know your views in the comment section.

A lot of EPF accounts are lying unclaimed after the death of an employee. Families have no idea how to claim the EPF money and what is the process?

Today I will share with you how your family will be able to withdraw the EPF account money in case something happens to you.

How to claim EPF money after the death of an employee?

Once a person is dead, the beneficiaries of the dead employee can proceed with the process of withdrawing the EPF money. The first right is of the nominee who was mentioned in the EPF by the account holder. Mostly it’s a father or mother as most of the people are unmarried when they start their careers and they mention one of the parents as a nominee.

Here are the documents one need to submit

[su_table]

1

EPF Composite Form

The first form is called the Composite form for death cases, which is a single form to be filled to claim EPF, Insurance money and any pension amount.

2

Death Certificate

You need to provide the death certificate of the EPF account holder who had died.

3

Birth certificate of children claiming pension

If there are children of the deceased who are claiming the EPF, they need to provide the birth certificate for each of them

4

Joint photograph of claimants

One has to provide a joint photograph of all the claimants together. This is to make sure that there is no fraud in the name of claimants.

5

Copy of cancelled cheque or attested copy of the first page of Bank Pass Book

To make sure there is proof of the account where the money is is going, one has to provide a copy of the cancelled cheque or the first page of the bank passbook

6

EPS Scheme certificate (only if applicable)

This is a certificate which is a document that has all the details of who will get the pension etc after the death of a member. It’s issued by EPFO and this is applicable only when there is a pension part applicable.

[/su_table]

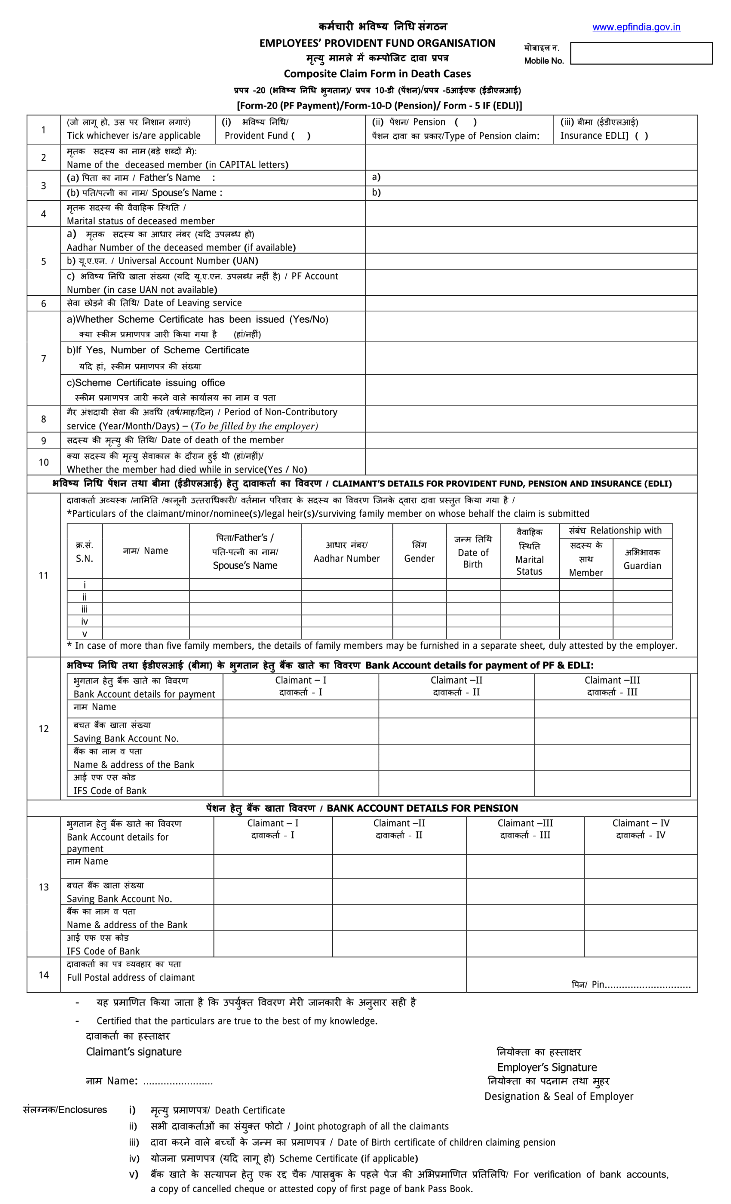

How does the EPF Composite form look like

Here is a snapshot of how the EPF composite form in death cases looks like. This is the main document that one has to fill if they want to claim the EPF amount.

As you can see, that the process of claiming EPF is lengthily and painful, you should make sure that you make it easy for your family members to claim back the EPF money. Hence please do the following things

Keeping all of your important information in one place which is safe and accessible to your family

Please update the nominee of your EPF to someone whom you really want it to go

If you have a WILL, mention the beneficiary who should get the EPF money

I hope you get a clear idea about the EPF claiming process now. If you have any query please reply in the comment section.

Now it has become much easier to transfer your EPF accounts while changing jobs. You no longer have to file separate EPF transfer claims using Form-13 after changing jobs. It will now be done automatically. EPFO has introduced a new composite form called Form 11 that will replace Form 13 in all cases of auto transfer.

In this article I will tell you the process of transferring your EPF account in case you are changing your job.

EPFO i.e. Employee’s Provident Fund Organization has introduced the online portal to transfer your EPF account from one employer to another employer.

How to transfer EPF online automatically in case you change your job?

Old Process –

Earlier, transferring EPF account from one employer to another employer was quite a hassle for an employee for which employees needed to wait for a prolonged time period. As per the old process, one had to complete the process only through offline mode which resulted in various problems like misplacing your documents, taking a long time to get the claim approved and a communication gap which had proved as a major problem.

New EPF composite form 11 –

Form 11 is a composite declaration form, which includes all the basic details of the employee such as Name, registered mobile number, bank account number, PAN number, date of birth, date of joining, etc.

From now on, employees have to fill only form 11 to his employer at the time of changing his job, and his EPF account will be transferred to his new employer automatically. But for this process employee’s UAN must be linked with his Aadhaar number, so that the employer can verify employee’s details and e-KYC.

The introduction of this new online portal has saved lots of effort from every employee and made this process a lot easier.

Let’s see the process of how to transfer EPF online.

Online mode of transferring EPF Account:

Here in this process, I have classified all the steps into 3 categories according to the work done by employee, employer, and EPFO. Now let’s see the steps –

What employee has to do –

Fill form 11 – providing all your details.

Provide all the details regarding your previous job.

Sign and submit this form to a new employer.

What employer has to do then –

Get the form filled by the employee and check the details entered.

First, enter all the details of the employee and then upload form 11.

Further process –

The employee will get an SMS on his registered mobile number to inform him that his auto-transfer request is in process.

Once the process of transferring the account is completed, the employee will be informed via SMS or e-mail ID register with UAN.

The process will be completed unless –

Employee stops it in between

The new employer deposits his 1st contribution

Watch this video to know how to merge EPF account from one company to another company:

Let us know if you understood the process? Have you tried doing this?

After the launch of the BHIM and TEZ app, the government of India has now launched a new multi-channel platform which is known as Umang App. This move has been taken by the GOI to unite all the government services and schemes in one place and make it more convenient for all the citizens to take the benefit of these services.

What is UMANG APP?

Umang (Unified Mobile Application for New-age Governance) is an all-in-one mobile app that has 1200 services including state and central government. It is a multi-channel platform that is absolutely free for everyone. This app will reduce your efforts of going to the regional government offices. It will also save you precious time and energy.

How to register for the Umang app?

Downloading and registering for the Umang app is as easy as downloading other apps from the Google Play Store and the iPhone app store. It can be completed with a few simple steps. Let me tell you how?

Download the Umang app from your mobiles Play store

Select preferred language and click on terms and conditions

Click on register (if you don’t have login id and password) and proceed by entering your mobile number (make sure that you have this number in front of you because you will receive an OTP)

Enter that OTP and proceed to set MPIN.

Now enter all the other details like your name and all and click on submit.

Once you save all the data then you get confirmation at your registered mobile number .It also says if you have not updated your details then you can give missed call at this number- “1800-11-5246.”

That’s it. With these simple steps, you will be registered with the Umang app. If you enter your Aadhaar number, it may use your Aadhaar number for E-KYC purpose and your data linked with your Aadhaar will be automatically linked with the Umang profile. You don’t need to provide any other details for the registration process.

Watch this video to know about all the features of Umang app :

Many of our investors, when we ask them about their accumulated balance in their Provident fund account or pension fund, they don’t have any idea about the same. So for all those investors, Umang app is very useful to get to know the balance of all their investments in EPF/PPF, or other government schemes, on just a few clicks. So, in this article, we have focused on how to check EPF balance. By following the same process you can get to know about other government schemes balance.

What is EPFO?

EPFO (Employee Provident Fund Organization) assists the Central Board in administering a compulsory contributory Provident Fund Scheme, a Pension Scheme and an Insurance Scheme for the workforce engaged in the organized sector in India.

How to check EPF balance and view passbook on the Umang app?

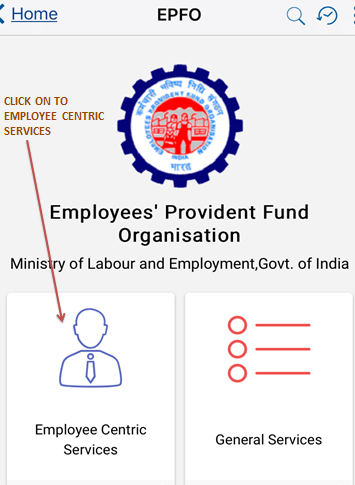

Step#1– Open the Umang app and click on to EPFO :

Once you click on the Umang app and click EFPO. After you click EFPO the below window opens. Then click on to employee-centric services to know your EPF balance.

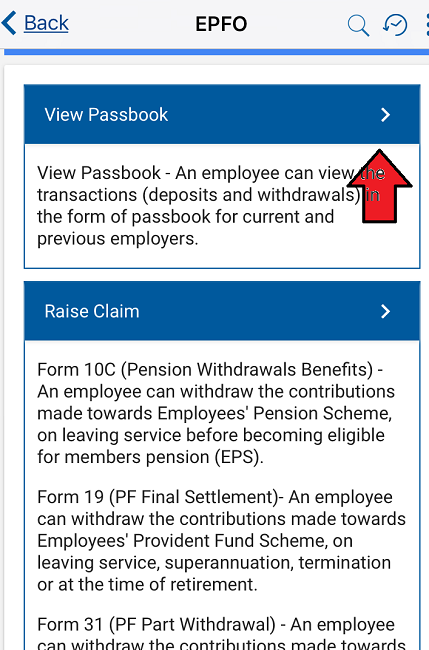

Step#2 – Click on to view passbook :

After clicking on to employee-centric services, below window appears. Now click on to view passbook and wait.

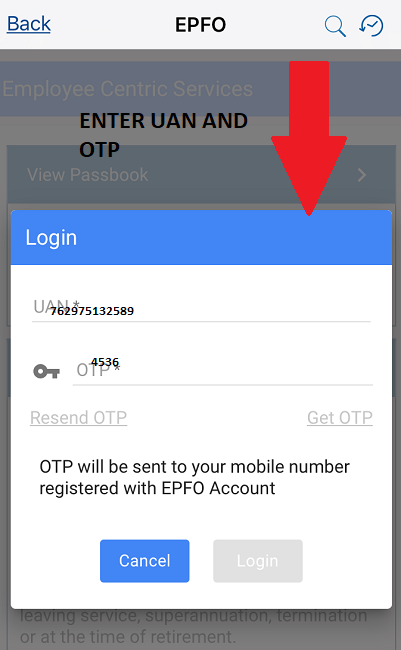

Step#3 – Login :

After you click on to view passbook now you will have to log in. For login, you need UAN (Universal Account Number) allotted by the EPFO to every employee that contributes to PF. You can ask your employer for your UAN number. Once you enter UAN number, you will have to click on get OTP. You will receive OTP on your registered mobile number. Put the OTP and log in.

Please note – If you leave your current job and move to another job then your UAN number will not change. This UAN number will be with you forever.

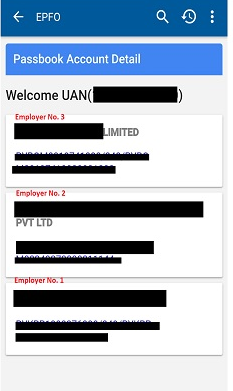

Step#4 – Again click on to view passbook :

After you log in the below window appears. You will have to click on view passbook and

Step#5 – Details of your EPF balance :

After you click on to view passbook the below window will appear which will show you the entire EPF balance created during your employment with various employers. You can open each of the links that are mentioned employee wise to see complete details of the deposit made towards PF.

List of other services available on UMANG APP:

Central Services :

AICTE ( All India Council for Technical Education)

Aadhaar Card

Bharat Bill Pay

Bharat Gas (BPCL)

Buyer Seller – mKisan (Sell product to Better Price)

CBSE (Central Board of Secondary Education)

CHILDLINE 1098 (Night and Day)

CISF (Ministry of Home Affairs, Govt.of India)

CPGRAMS (Centralized Public Grievance Redress and Monitoring System (My Grievance)

Crop Insurance (Department of Agriculture, Cooperation and Farmers Welfare)

CRPF (Central Reserve Police Force)

DAY – NULM (Deendayal Upadhyay Antyodaya Yojana National Urban livelihood Mission)

Digi Sevak (Digital India Volunteer Management System)

Directorate of Marketing & Inspection (Department of Agriculture, Cooperation and Farmers welfare)

e-RaktKosh (A Centralised Blood Bank Management System)

eMigrate (Ministry of External Welfare)

ePashuhaat (GPMS Transportal)

ePathshala (National Council of Educational Research and Training)

EPFO (Employees’ Provident Fund Organisation)

eRahi Sukhad Yatra (National Highways Authority of India)

ESIC – Chinta Se Mukti (Employees’ State Insurance Corporation)

Extensions Reforms Monitoring System (Ministry of Agriculture and Farmer Welfare)

Farm Mechanisation (Ministry of Agriculture and farmer Welfare)

Goods & Service Tax Network ( Ministry of Finance)

HP GAS

INDANE GAS (Indian Oil Corporation Limited)

Kendriya Vidyalaya Sangathan

Khoya Paya (Citizen’s Corner of Track Child)

Kisan Suvidha (Ministry of Agriculture and Farmer Welfare)

MADAD (Ministry of External Affairs, Government of India)

Ministry of Petroleum & Natural Gas

My Pan (Income Tax Department )

National Consumer Helpline (Department of Consumer Affairs)

National Scholarship Portal (Ministry of Electronics and Information Technology, Government of India)

NDL India (National Digital Library of India)

NPS (Retired Life ka Sahara, NPS hamara)

ORS (Online Registration System – Patient’s Portal for e-Hospital)

Parivahan Sewa – Sarathi (Ministry of Road Transport & Highways)

Parivahan Sewa – Vahan

Passport Seva

Pay Income Tax

Pensioner’s Portal (Department of Pension and Pensioner’s Welfare)

SARAL (Transforming Citizen service delivery in Haryana)

SSRD KYRC (Special Secretary Revenue Department – Government of Gujarat)

The welfare of Plain Tribes & Backward Classes Department (ASSAM)

As you now know that, with just a few clicks you can know your EPF balance. I have checked mine, what are you waiting for go and check yours. If u still have any doubt or query please ask in the comment section.

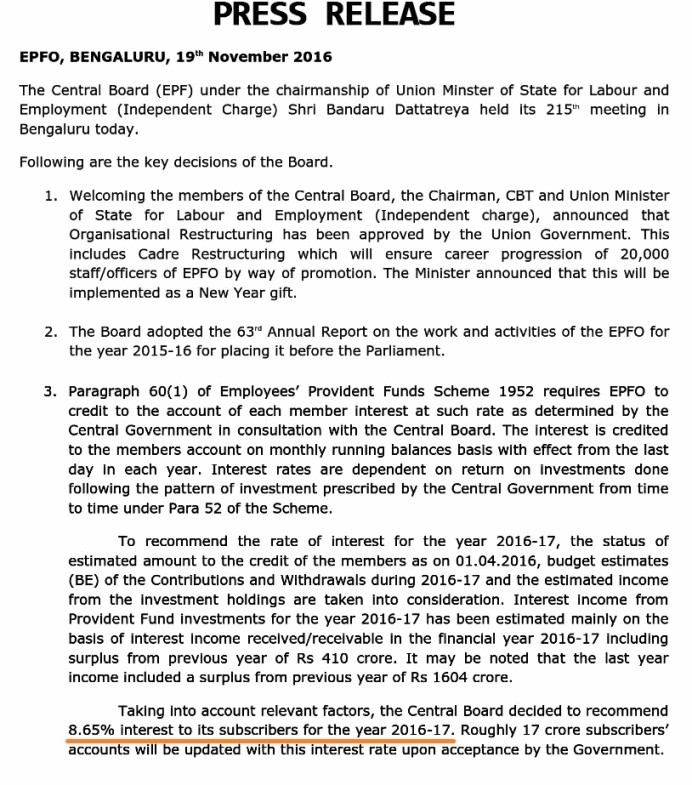

The EPFO department (Employees Provident Fund Organisation) reduced the EPF interest rate to 8.65% today. The old interest rate was 8.8%.

This interest will be applicable for the deposits made for financial year 2016-2017. Which means that all the deposits which were made after 1st Apr, 2016 by the employers will be earning the interest of 8.65% only, and not 8.8%.

While an interest rate of 8.62 per cent would allow the EPFO to keep a surplus of around Rs 22 crore, fixing the interest rate at the present rate of 8.8 per cent would have left it with a deficit of Rs 700 crore, EPFO’s income projections showed.

According to sources in EPFO, the lower interest rate is on account of poor rate of return on investments made by the EPFO on all fronts.

You will notice that the bank deposits interest rates were also reduced recently and this move might be in tune to that decision, as it’s tough to provide high interest as the money availability is high.

Today we will talk about the issue of duplicate UAN, which has confused a lot of employees. A lot of people have contacted us that 2 UAN were generated for them by their past employer and current employer and now they have no idea what is to be done in this case.

You can see following question which was posted by one of the reader of this blog.

Hello Manish,

I left my previous company on 1st April 2014 and joined new company on 7th April 2014. Now problem is I have been allotted UAN no. from both employer. I want to withdraw whole amount of EPF (Employees’ Provident Fund) of previous employer.

So kindly guide me what to do in this situation?

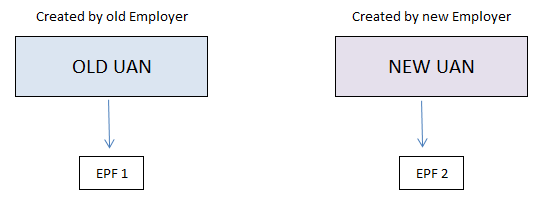

Why does multiple UAN get allotted?

UAN (Universal Account Number) as you all know, is a single unique number for each EPF member for all this EPF accounts under them. You can see the UAN as the folder (UAN) which has various files under it (EPF accounts)

Before we discuss how to solve the duplicate UAN problem, I want you to know how two UAN are generated and why does it happen?

Reason #1 – Not disclosing old UAN number

A lot of employees do not want to disclose about their past employment, hence they do not quote their old UAN number to new employer. In that case, the new employer will generate a fresh UAN for the employee. This is one of the reasons for having duplicate UAN number.

Reason #2 – Past employer did not furnish ‘the date of exit’ details in the ECR

ECR or Electronic Challan cum Return is an electronic return filed by employers to EPFO to submit your EPF payments and other things. In this, they mention “the date of exit” for those employees who have left the job. So incase due to some issue the employer does not mention this date of exit.

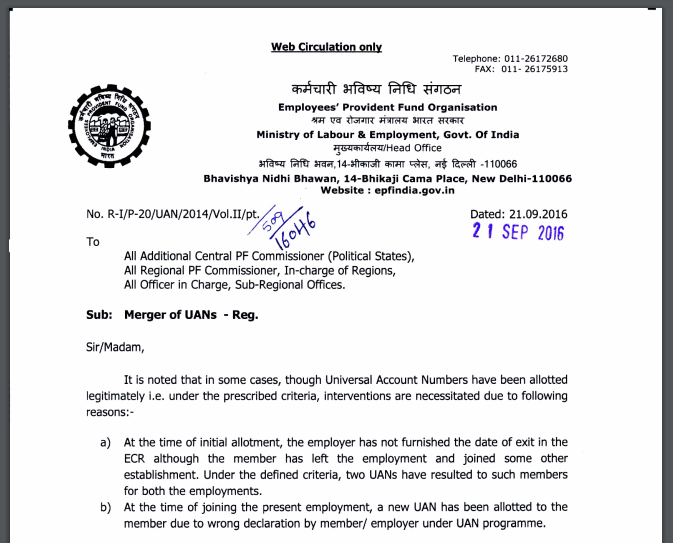

This is another reason why another UAN gets generated by new employer. I have no idea why that happens, but this is the reason which is mentioned by the EPFO in their recent circular which talks about the issue of multiple UAN allotment

How to solve the two UAN problem?

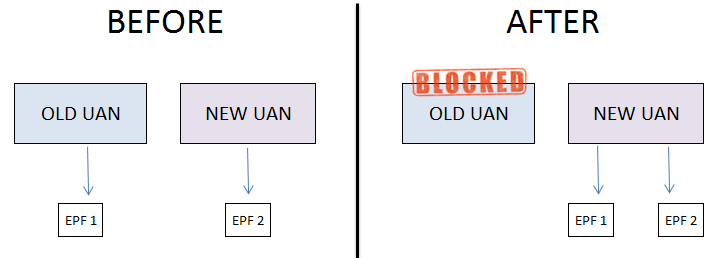

Note that each person should have only one UAN number (like PAN), hence if you have multiple UAN, it’s not allowed and creates problem in the EPF system, because is no proper track. Hence, as soon as you come to know that there are multiple UAN assigned to you, you should cancel one of the UAN (mostly the old UAN) or should try to deactivate one of them

Process to deactivate old UAN

Step #1 – The first step if that you should start the EPF transfer for all the EPF’s which are not under the latest UAN generated. This can be done using the OTCP portal of EPFO . I am not going in details here, but first you need to make sure all the old EPF’s are transferred and linked to the new UAN.

Step #2 – In the next step, the EPFO system will automatically identify those UAN for which the EPF transfers have happened and completed. Once they find the idle UAN, they will automatically deactivate that UAN. You don’t have to do anything here. This deactivation process will take place from time to time as per decision taken by EPFO. Once the deactivation happens, your old member id (your old EPF accounts) will be linked to new UAN.

If you are already sure that your past UAN does not have the EPF linked to them, then you can mail your old UAN number along with recent UAN to your employer and to [email protected] . They will verify your UAN’s status and deactivate the old UAN.

Let us know if you have more clarity on this subject or if you have already completed the process for the benefit of other readers.

Good news, the inactive EPF accounts will now start getting interest. Also the interest will be paid since Mar month of this year. This will start once the govt issues the notification regarding this. Since 2011, the EPF accounts which were not active for 3 yrs before inoperative EPF accounts and they stopped getting the interest.

Now Inoperative EPF accounts will earn interest

However now the rules are changed and if someone wants to keep the money in EPF account, they can do so. The EPF account will keep earning the interest decided by EPFO from time to time. This year itself the news was out that the inoperative accounts will get interest. However the notification news has come just now yesterday.

As per the EPF officials, Around 42,000 crore has been lying in inoperative EPF accounts and they will get interest @8.8% now.

“The inoperative EPF accounts are not being paid interest since 2011. As per the instructions given by Prime Minister Narendra Modi and Finance Minister Arun Jaitley, we decided to start paying interest on those accounts to make them operative,” Mr. Dattatreya said on Monday.

You can now leave your EPF accounts active even after leaving the job

As per this latest development, now after you leave your job, and do not join somewhere else, you can leave the EPF account to keep earning the interest. Given that the EPF interest is upwards of 8%, it’s a good place to park the money.

Good news, the inactive EPF accounts will now get interest from next month, i.e. Apr 1, 2016. Around 5 yrs back, under UPA rule, EPFO came up with the rule that any inoperative EPF account will stop getting interest after 3 yrs of inactivity.

So if a person left the job and never withdrew the money, he would stop getting the interest after 36 months. Inactive accounts are those accounts where there is no addition from employer or employee side. Now that old decision is reversed. There was a meeting of Central Board of Trustees at EPFO and this decision was taken.

A lot of employees will be happy due to this change because at a lot of people do not want to withdraw their EPF and still want to earn the interest. Also the withdrawal/transfer process is a bit cumbersome and many investors do not want to take the pain and let their accounts be there.

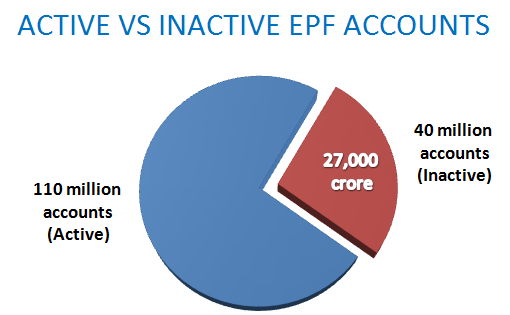

Inactive vs. Active EPF Account

As per a report, around 27,000 crore is lying in 40 million inactive EPF accounts (total accounts = 150 million), This money will now start earning interest.

That time many people were confused if the interest will be given to them or not if the accounts become inactive? Now that confusion is also cleared.

65% investment in G-Sec

As per this report, there is one more change in the way money will be invested by EPF in G-Secs

When asked about a proposal on enhancing proportion of incremental investments of the EPFO in government securities (G-Sec) from 50 per cent to 65 per cent, Labour Secretary Shankar Aggarwal said, “It has already been decided by the Ministry of Finance.”

The Secretary said that the limit of 50 percent was enhanced as they were getting good offers but unable to invest in such instruments as the limit had been exhausted.

“If we get higher returns in G-Secs then we should be allowed to invest more in these instruments,” he said further.

Before I even start this article, please watch the first 5-6 min of the following video which comes from Ravish Kumar of NDTV and you will get the hottest points of discussion in this budget, which is taxation on EPF withdrawal.

The video below discusses various viewpoints from govt representatives, economists and some other people on why this is a foolish decision from govt and at the same time, why it makes sense to tax the EPF withdrawal. You will listen to the full video if possible for you, or else at least listen to the first half.

So, I was watching Budget 2016 yesterday and desperately waiting for the personal taxation announcement because that’s the main thing I understand :). By the end of the budget speech, it became clear that there were no changes in income tax slabs nor 80C limits and all hell broke loose on the news that the EPF withdrawal will be taxed on the 60% corpus.

The whole twitter and facebook was full of angry people showing their disappointment on the budget and how it has betrayed the salaried class. The issue went really out of hand and a twitter trend #RollBackEPF started trending and every person from across the country wanted it to be taken back. It was really a crazy day. And today govt has clarified that the tax is only applicable on the interest component only (more on that later in the article)

This budget’s major focus was on the rural economy and farmers which are neglected for decades anyways. Only time will tell if the efforts were taken in this budget work or not and if things improve and get better for farmers and rural economy. Let’s wait for that.

While there were many things in this budget, on the taxation front and other announcements, nothing major was there in this budget for a common man on taxation front and that made the salaried class very very disappointed.

Let’s look at the budget highlights one by one. My focus is to share all the major points which concern or are related to a common man.

1. No Changes in Tax Slab rates or 80C

Let me again share it. There was no change in the income tax slabs or the 80C limit. Everything remains the same on this front. Everyone was expecting that the slab will be raised or 80C limits will be increased, but that didn’t happen. There were conversations like the basic exemption limits should be raised to at least Rs 5 lacs from the current 2.5 lacs, and this was, in fact, Arun Jaitley’s demand in 2014 that the limits should be raised. Not sure what’s coming in his way now when he himself is the decision-maker.

2. Up to 40%, NPS withdrawal maturity becomes tax-free

Now 40% of the NPS corpus will be tax-free at the time of maturity, rest 60% corpus will be taxed if you withdraw it fully. However, if you buy an annuity (pension) from the remaining 60% corpus you won’t have to pay the tax. However, note that the pension amount which you will get will be normally taxes as the income in your hands.

This means that if you have Rs 1 crore in NPS at the time of maturity, if you withdraw the full amount, then 40 lacs will be tax-free, but the rest 60 lacs will be taxed. Now if the applicable tax at that time is 20% (just an example), then 12 lacs will go in tax and you will get the remaining 48 lacs in our hand. So a total of 88 lacs you will get out of 1 crore. However, you can choose to just take 40 lacs in hand and leave the 60 lacs in a pension product to generate the monthly income (which I think many will choose anyways).

One good point is that if the NPS holder dies, then the full death claim will be tax-free in the hand of the receiver.

3. EPF Interest becomes taxable for 60% corpus

As I said earlier, the EPF was the center point of discussion after the budget speech and govt has clarified that only the interest component will be taxed at the time of withdrawal and that too only on the 60% corpus. The 40% part will be tax-free fully. Note that this is applicable only on the interest earned after 1st Apr, 2016. The interest earned before this date will be tax-free.

Also, an important point here is that there is a lot of debate and confusion around this point as of now. We should wait for more clarification on this from govt in the coming days.

4. PPF remains tax-free (its still EEE)

PPF is untouched and still remains full tax-free as of now. Yesterday there was this confusion, that NPS, EPF and PPF, all of them are brought at the same level and many worried people whose PPF was going to mature in the coming months/years panicked and started asking if their PPF corpus will also get taxed.

So at this point of time, PPF remains the only investment product which comes under EEE (Exempt, Exempt, Exempt)

5. Employer contribution in EPF restricted to 1.5 Lacs per year

Now an employer contribution is EPF is restricted to Rs 1.5 lacs per year or 12% of the basic salary whichever is lower. Till now there was no limit like that, but with this budget that is changed. Incase employer does contribute more than 1.5 lacs per year, then it will taxable in employees hand.

Also, note that the govt will now contribute the 8.33% EPS part for the employees from its own pocket for the first 3 yrs for the new EPFO members.

6. Health Insurance of Rs 1 lacs for Senior Citizens

There will be a health insurance scheme launched soon which will provide Rs 1 lac of health cover to poor families. Also, the senior citizens who belong to these families will also get an additional Rs 30,000 top-up cover on top of Rs 1 lac. The govt budget documents give the reasoning for this scheme.

Catastrophic health events are the single most important cause of unforeseen out-of-pocket expenditure which pushes lakhs of households below the poverty line every year. Serious illness of family members cause severe stress on the financial circumstances of poor and economically weak families, shaking the foundation of their economic security

7. HRA exemption under Sec 80GG raised from 24k to 60k per year

As per sec 80GG, those who do not get HRA in their CTC from their employer can now claim up to Rs 60,000 per year as a deduction under rent paid. Earlier this was only Rs 2,000 per month. This will help a lot to those people whose employers are not giving them HRA Component. Rs 5,000 though is a less amount, but still a respectable deduction at least.

In other word eligibility will be least amount of the following :-

1) Rent paid minus 10 percent the adjusted total income.

2) Rs 5,000 per month. (this was Rs 2,000 earlier)

3) 25 percent of the total income.

8. First time home buyers to get extra Rs 50k deduction in Interest

The first time home buyers will get an additional Rs 50,000 tax exemption in interest part apart from the current exemption, provided following points are true

The loan amount should not be more than 35 lacs, and the value of the house should not be more than 50 lacs

The loan should be sanctioned between 1st April 2016 – 31st Mar 2017

The home buyer should not have any other residential house on his name

9. Dividends above Rs 10 lakh to attract an additional 10% tax

Now if a person is earning more than Rs 10 lacs of dividend from stocks will have to pay the tax of 10% on it. Right now companies anyways pay DDT (Dividend distribution tax) on the dividends declared. I think this is anyways going to impact only those who have very high investments in stocks and they earn big dividends. A normal investor will mostly be out of this.

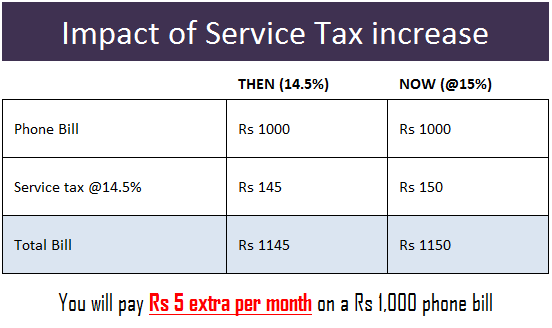

10. Service tax increased from 14.5% to 15% due to Krishi Kalyan cess

A new cess called Krishi Kalyan cess of 0.5% is added to service tax, which is applicable to all taxable services, which simply means that the service tax has now gone up from 14.5% to 15%. While this 0.5% does not look much, its actually going to be a decent amount for a common man in addition to what we pay.

That means an extra Rs 2 in the bill if you have food worth Rs 1,000 in a restaurant.

That means an extra Rs 5 in your phone bill of Rs 1,000

I think it will add a few hundred extras in your expenses if you count entire years of expenses. This will be applicable from 1st June, 2016 so you still have some time 🙂

11. TDS of 1% on buying cars above Rs 10 lacs

1% TDS is proposed on the purchase of luxury segment cars costing Rs 10 lacs or more. The same TDS is also there if one buys any goods or services exceeding Rs 2 lakh. On top of this, an infrastructure cess of 1% is on small petrol cars, CNG cars and 2.5% cess on diesel cars are there, which means that cars, in general, become a bit expensive.

Even the branded clothes and tobacco items will become costlier due to the excise duty increase

12. Possession period for property raised to 5 years for claiming tax benefit

Earlier, if one used to buy/construct a property, one had to get the possession in 3 yrs itself to claim the tax benefits on the interest paid under sec 24. Now it has been raised to 5 yrs. This will help those real estate investors who have not got the possession due to delays from builders.

13. Tax Rebate of Rs 5,000 for those with income less than 5 lacs

For small tax payers with an income of fewer than 5 lacs, the tax rebate is increased from Rs 2,000 to Rs 5,000. This means that if the income tax payable is upto Rs 5,000 for small tax payers, they don’t have to pay it. Rs 5,000 will get deducted from the tax payable. So if a person is earning Rs 4 lacs (taxable income), then as per slab his income tax is Rs 15,000 (10% of the income above 2.5 lacs), out of this Rs 15,000 tax payable, he will get the rebate of Rs 5,000 and he will pay only Rs 10,000. This was earlier set at Rs 2,000 only, but now changed to Rs 5,000

14. ATM’s in Post offices

Over the next 3 yrs, govt plans to roll out the ATM’s in post offices so that more people in rural areas can access the banking services. The department of Posts plans to bring around 25,000 post offices under this in the next few years.

There are many more things in the budget, but I am not going into each of those. The points above are the main highlights which I am discussing here. You can read all the points of budget in this PDF file

Please share how do you rate this budget and what do you think about the move on the EPF taxation?

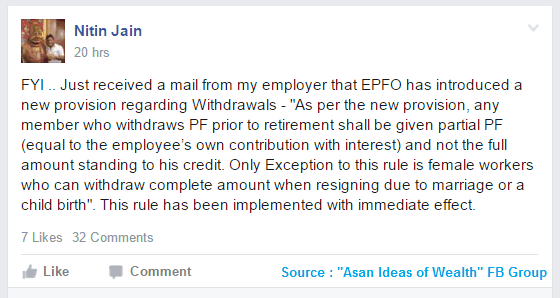

Indian Govt has brought a new amendment in the EPF rules, according to which the members will not be able to fully withdraw from their EPF before they reach the retirement age.

The maximum one will be able to take out is their own contribution and its interest (which was raised to 8.8% recently), and that can be done only after 2 months of ceasing employment.

The only exception shall be made for female members resigning for the purpose of marriage or pregnancy or child birth. I came across this news from Nitin Jain when we got an mail from his employer about this notification. Thanks for Nitin to send the notification PDF to me.

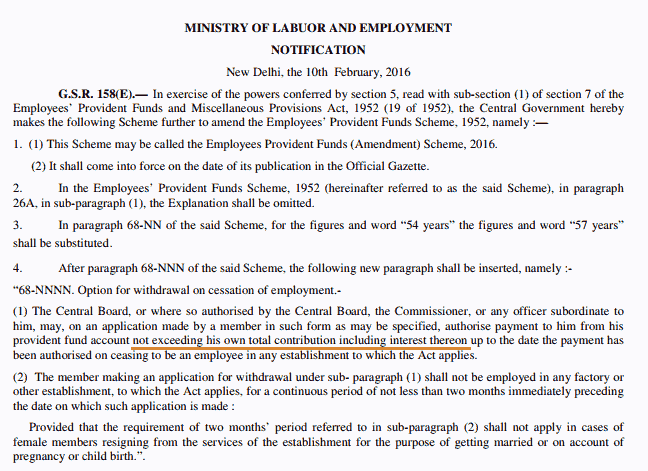

Below is the snapshot of the exact wordings taken from the notification which was released by the govt recently. please find out the PDF of the notification here

So whatever your employer is contributing to EPF and the interest on that part will be retained in EPF till the retirement age and you will be able to use it only at the end.

Many investors when they change jobs withdraw from their EPF’s and till now they used to get the full amount. But this is not going to happen from now onwards. What this means is that if you have an EPF account, your relationship with EPFO is lifelong now, because your account will be active till you retire (or die)

This is not a sudden decision taken. It was properly planned many months back itself and there was news about this restriction coming up in future, however that time, it was said to be the limit of around 75% of the total amount, but now it’s close to 50% only (employees share only).

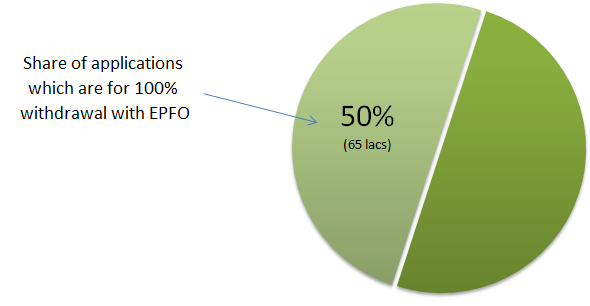

Also note that as per the stats from EPFO; out of the 13 million annual claims pending with the EPFO, over 6.5 million claims are for 100% withdrawal, that’s 50%. This means that out of every 2 claims which EPFO gets for withdrawal, 1 of them is for full withdrawal.

This means that a big portion of claim withdrawal applications was coming from people wanting to withdraw the full amount. Now with this new rule, the number of applications to EPFO will also reduce drastically.

Is this new change in EPF withdrawal rules Good or bad?

From an employee’s point of view, the flexibility to withdraw the full amount (the painful process) has gone and now you can’t just take out full money like you used to do earlier. EPF is a social security measure, and was designed keeping that in mind, but people used to apply for withdrawal the moment they changed the jobs most of the times, now with this new change, it will not be possible and in reality one will be forced to keep a part of their wealth in EPF till their retirement

No matter how much I try to think like an employee, my experience of working with thousands of investors tells me that it’s a good move. PDF is the only saving at the moment, which happens by default for a salaried person, and even though one does not touch it for years, eventually a big percentage of the population always thinks of withdrawing the money on job change and the money gets utilized somewhere.

Retirement Age increased from 55 to 58

Another change in the notification is that the retirement age is increased from 55 yrs to 58 yrs, which means that one can now only consider themselves to be retirement from the EPF point of view once they turn 58 yrs. One can also apply for a pension only at that point in time.

This is a good move if you think long term. Consider a person who is 28 yrs old, and his salary is Rs 30,000 per month. Assume that his basic salary is 40% of the gross amount, which here comes to 12,000 per month. Now on this, he will get 12% of salary deducted as for the EPF and another 12% will be added from the employer which would total Rs 2,880 per month.

Now if the salary increment happens @7% per year and the return on EPF continues to be 8% per year, the person will retire with 80-90 lacs of EPF corpus at the time of retirement, provided he does not withdraw anything in between. However now even if the person chooses to withdraw the money in between, with this new rule the employer contribution is going to the restricted and one will bound to have 40-50 lacs at a time to retirement (with the assumptions above). Below is the chart which shows how the numbers move.

Note that the above chart is only for illustration purpose, The only point I want to make it a decent amount of money will be there at the time of retirement because of this new forced rule.

Please share what you think of this new rule. Do you think it’s good or not? How do you react to this?