Jagoinvestor

Jagoinvestor

March 7, 2016

March 7, 2016

4 big reasons why you should avoid investing in a “wrong product” ?

Have you ever bought the wrong financial product? Or it was mis-sold to you out of pressure from family/relative? Or because you trusted the seller too much? If not these reasons, maybe you wanted to do last minute tax saving and you jumped into buying that policy and gave yourself a life sentence of paying premiums which will not help you much in long run?

We are today going to discuss all sort of issues which arise when you get into a wrong financial product and why you should avoid it at any cost.

Background

Let me first give you some background on how I got started with this article. Here is what happened.

A few days back, I was once watching a TV show and there was a story of a woman who married a guy out of the pressure of family who wanted to get married as such as possible. She fell for the short term tricks and didn’t pay much attention to those points which matter in the long term.

Soon after the marriage, she started realizing that she made the mistake. It’s not what she wanted in life and its not a match which can sustain. Life was a mess. She was stuck in this relationship.

Coming out of it was not easy. She was in depression and all the time was going into regretting the decision. Almost 5 yrs had passed and by this time, a lot of her energy and time had got wasted.

Finally, she came out of that bad marriage. Often she wondered why she took such an impulsive decision? What if she had never got into that bad relationship? How would have her life shaped up?

Investors do the same thing with financial products

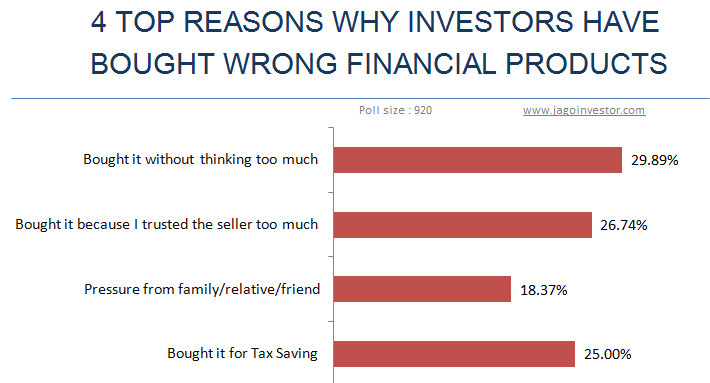

A lot of investors buy unsuitable or wrong financial products in their financial lives and it drains their money and valuable energy. It gives them unnecessary tension, which could have been avoided if they were a little more prudent in their financial life. Below are the top 4 reasons why most of the people have bad financial products in their life. I surveyed 920 people, the top most reason why because they were careless themselves and bought things without much thought. Where pressure from family/friends was not the major reason.

The careless attitude costs them too much trouble. I have worked with more than a thousand investor now, and I can tell you most of the good financial lives which we see are not because of making good decisions, but by avoiding bad decisions. Most of the people who have high net worth or powerful financial lives are those who have not wasted their valuable time and money in wrong financial products and concentrated on simple things.

One bad move can nullify 2-3 good decisions.

Today I want to talk about 4 core problems that arise out of buying the wrong financial product. Let’s look at them one by one.

[su_table responsive=”yes” alternate=”no”]

| Problem #1

Waste of money |

Problem #2

You feel “stuck” and waste your time and energy |

| Problem #3

The opportunity Cost |

Problem #4

You lose trust and everyone looks like a “cheater” |

[/su_table]

1. Waste of Money

Nothing hurts investors more than losing their hard earned money. When you buy a wrong financial product, most of the times, you lose money or do not get the returns your hard earned money deserves. A few years back ULIP’s were one of the most mis-sold financial products. Millions of investors have lost their hard-earned money in these products. The charges in the first year were huge at that time which ate away all the returns one got. On top of it, the returns of the ULIP were linked to the stock market and most of the investors never knew this.

Because of this, a lot of investors lost a big chunk of their money in these products.

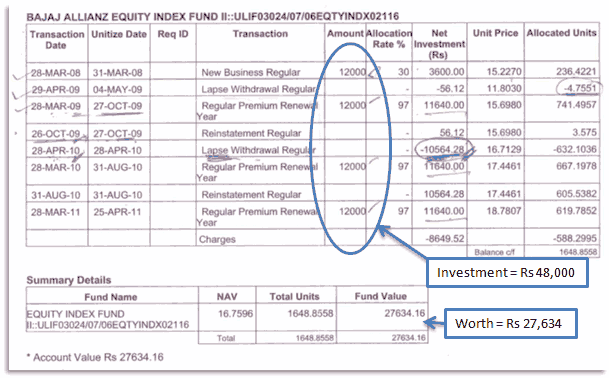

Below is a snapshot of one of our readers who bought a ULIP in 2008, and he paid a total of Rs 48,000 in the ULIP, however when he checked his statement after a year, his fund worth was just close to Rs 27,000.

The value of the fund had come down due to market movements and commissions structure, but the main point is that the investor never expected it. He didn’t know that it could happen because, at the time of selling, there was no communication of the risk part. This is what happens when one buys a financial product without understanding it.

Then there are other kinds of products like endowment insurance policies which does not pay you back your full money if you surrender them in between or very early. Its the product design. If you pay Rs 50,000 per year premium, then in 4 yrs you must have paid Rs 2 lacs in total. Do you know much would you get back, if you wanted to close the policy and take your money back? On average it would be just 40%-45 %, which means only Rs 1 lac you will get back.

Forget financial products, some time back I bought a sim card which was available on purchase of an internet connection and there were some attractive benefits associated. I fell for it and bought it without giving much thought. I spend a good amount of time and energy behind it, paid bills without using it and finally ran around to close the connection. I could have avoided a lot of pain, had I just ignored it. The same is true for various credit cards, unwanted memberships, etc.

2. You feel “stuck” and waste your time and energy

Forget money, what about the time and energy you waste? Once you are stuck with the wrong financial product, you will keep thinking about it. You will keep regretting your decision. The financial product will be part of your life and you will often wonder why you invested in it?

Most of the people anyways take a lot of time to take financial decisions and just imagine what happens if one of those decisions is wrong or bad for you? You will keep cursing the agent, your financial planner, yourself, the system, SEBI, IRDA and every other person (even yourself).

You feel STUCK …

Nothing is more frustrating than feeling stuck and not being able to do anything fruitful. There are millions of investors who are stuck with their endowment policies, ULIP’s, bad credit cards, wrong advisors, other products. They want to get rid of it, but they DON’T.

Also, the world is cruel, you as investors are taken for granted. See how one of the readers, when tried to surrender his LIC policy, was treated.

Hello – I approached the branch manager on cancellation – it’s not even 7 days – he is asking me to get the agent to the branch! is this correct ? I have a question : If I want to surrender the policy or retrieve the maturity amount , is the agent required , this is weird stuff , If this is not true, please help me how this can be escalated and resolved .

Over-analysis leads to more delay

Investors also over analyze what they need to do once they realize that they bought something bad? How to minimize their losses and how to come out clean. But in that process more and more time passes and the situation gets messier compared to the past. Most of the people keep delaying their policy surrendering for years and the damage keeps compounding.

It’s like you bought a bad stock and you didn’t sell it off when you had a 10% loss. You wanted to get out of it at the right time and then it will send down by another 10% and then another 20% and finally out of frustration you sell it at 50% loss wondering why you didn’t take 10% loss itself at the first place.

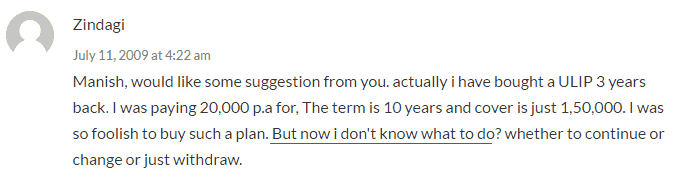

In the same way, most of the investors keep thinking about the loss they are going to make if they get out of the bad financial product and keep postponing their decision. Here is one comment from our blog where an investor shares his state of mind. You can see that he feels so stuck. This is a very common problem

Our lives are very busy these days and if one pending item gets added to our list, it takes months and years to complete it, even if it’s just a few hours of work!.

So the big problem which happens when you buy a wrong financial product is that you waste your valuable energy trying to fix the issue. That precious time should have gone into earning more money and managing it well.

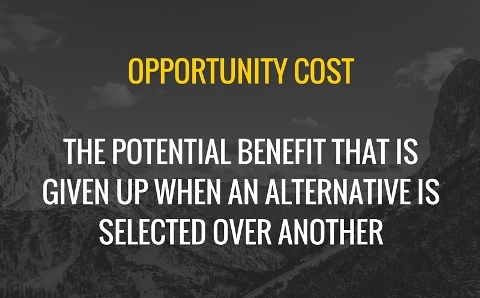

3. The opportunity Cost

Opportunity cost here means what is the other thing an investor could have done had he not got into a bad financial product. This is a very important thing to understand for financial success. Imagine a bad decision, where you invest Rs 5 lacs and after 2 yrs, your money worth is just Rs 4 lacs. You are in a loss of Rs 1 lac ?

NO, it’s not just Rs 1 lac.

Why?

Because you could have taken the right decision and could have made a profit which you lost in addition to the real loss. In that same example I gave above, you could have invested Rs 5 lacs in such a way that it would have become 6 lacs in 2 yrs. So your opportunity cost is Rs 1 lacs which you didn’t make here. Instead, you are sitting on a loss of Rs 1 lac.

Another example is of a young investor who wants to create a big corpus in the long term, but he/she is maximizing the PPF by investing Rs 1.5 lacs per year in that.

After 15 yrs, they will get a near inflation return only. I consider even that as a bad decision looking at the goal of wealth creation. The same 1.5 lacs can be invested in an equity product and a better inflation-adjusted return can be earned. The final wealth different in case of equity vs. PPF will be quite a big amount. The difference between 8.5% return compared to a 12% return is huge.

4. You lose trust and everyone looks like a “cheater”

Do you know how does it feel when you take some financial decision by trusting someone and you lose money? The tweet below was done by Kalpen Parekh, CEO Of IDFC Mutual funds.

When investors hear us say, it’s cheap so buy more, this is what Dharmendra will say! pic.twitter.com/UIHLdhpzAC

— Kalpen Parekh (@KalpenParekh) February 27, 2016

Money is a very private matter and most of people are very very attached to it. When an investor gets a bad experience once, they carry it with them for a very long term. Every other person starts looking like a cheater to them. Everyone seems to be behind their money and it’s tough to trust others.

It’s a very natural reaction, but the problem is that it also damages the investor’s chances to get into a good association too. There are many investors who contact us for their financial planning and many of those who have faced bad experiences in the past never move ahead because it’s difficult for them to trust someone now.

Imagine a guy who has had a bad experience with ULIP, someone who has lost his money due to market movements, will find it very tough to start his SIP’s in mutual funds for his long term wealth creation. This is a big loss for himself based on his past experience.

I know few investors who have vouched to never buy any other financial product other than a fixed deposit because they felt cheated in the past.

So what is the point I am making? If you take the wrong financial product, then it affects the way you think about financial products and advisors in the future.

How to buy financial products?

I am not going into detail here, but one thing is clear. You have to take out the emotions out of it. No greed, no fear, no pressure, no over trust on others. Make sure you understand what you are buying, why you are buying, for which goal are you buying, what are the risk factors, etc.

If you spend just 1 hour before you get into a financial product, I think 95% of the investor’s woes will be solved.

What do you feel about this article? Do you have more points to add?

ALL ULIPS ARE BASICALLY FOR CHEATING OTHERS MONEY BY THIS ULIP LOBBYS ONE OF THEM IS AVIVA . INVESTED 4 LACS IN 4 YEARS AND NO ANY BENEFIT ..SO I CLOSED IT AFTER 4 YEARS , AND JUST GOT MY PRINCIPLE AMOUNT . I REALLY DONT TRUST ANY KIND OF ULIP PRODUCTS . EVEN INSURANCE COMPANIES .

Thanks for your comment JAMES

Dear Danish,

I have purchased Icici smart kid Maxima 6 years back with 20000 premium PA. After 6 years the NAV seems to be not encouraging. What shall I do.

I suggest getting out of the scheme

Hi Manish , I purchased an ULIP product SBIlife Smart Performer , Fund Daily Protect Fund – III Paid 5 years premium 50,000 PA this product on Maturity it will consider the Highest Guaranteed NAV throughout investment period .So kindly suggest about this product should I close it or will hold for some period to get better return .

Close it

A very well explained article!

The other factor which I feel dominates is our GREED for the financial product or a stock. We most of the time buy a product out of greed without even caring about its fundamentals and the management efficiency because its price is rising continuously. I feel that greed should be kept aside while deciding our financial goals otherwise it may create a havoc on our investment portfolio.

You rightly said that we sometimes take decision without thinking much about the product thereby putting at stake the growth of our investment portfolio.

Thanks for sharing!

Yes Yashkumar

You are very right in pointing out that ! . .GREED is one major reason why most of the people get into mess 🙂

Manish

HI Manish,

I’ve invested 60K, in Feb ’13, 10K in Mar 14, in HDFC Long term advantage growth fund, another 50K in HDFC Tax saver growth in Mar ’15 and starts SIP for 4K from Apr ’15 till now, Also another SIP for 1500 in HDFC Infrastructure fund growth from Jun ’14.

My aim is for maintaining in long term basis like for another 10 years. My query is whether shall I continue the SIP in the same fund or to switch over to another, as i found both tax saver and infrastructure fund values are declining. If I need to switch over suggest me a good option.

Kindly suggest me

I think you can keep investing in same funds

Thanks Manish for your suggestion,

Kindly suggest me in which portfolio shall I go for another 4K SIP

You can look at ICICI Pru Discovery Fund

Thanks

Hi Manish,

Great Article. Thanks for educating us. I have a query and it is commonly asked and answered. but to make sure i am taking the right decision , let me post it here.. I have a money back LIC policy started on 28/04/2013 and investing 16175 quarterly in the same . policy is for 20 years and for 10L sum assured plus 10L accident cover. I have paid the premium for 3 years-1,94,100(16175*4*3) so far. I know it is not wise to continue with the policy, but i am unsure when to quit/make it paid up. first money back of 20% of sum assured(2 L) will be debited after completing 5 years, so next 2 years.

in 5 years i will be making a payment of 3,23,500 and will be getting 2 L money back.

My doubt is whether to surrender/paid up the policy now Or should i stay invested for 5 yrs so that i can get the money back and also avoid income tax reversal since i invested for only 3 years. Please help

Yea , I think continue for 5 yrs and then get out of it, thats the best solution!

HI MANISH

I buy a ulip plan of hdfc click to invest of 2000 Per month for 20 Years is it a good choice for long term please sugggest me

If its the online ULIP called Click2Invest, then its fine !

I surrendered all my LIC policies of almost 75k premium yearly started since 2005. Invested Money got LIC in HDFC HOMELOAN PREPAYMENT. Bought term plan of 50 lac. Started SIPs 20k/ month. Still loss in share market. I can wait for long term.

This is howI took measure decision on finance. Manish Your views pls .

Yes, better wait for long term !

This is a question to all the knowledgeable people out here, I need help. Please advice me so that I can plan better. I am a 35 year old male, married, no kids, live with parents and they are getting their own pension. I am not keeping well and I dont know how long I will be able to work, so I need guidance to manage my funds which can make me a bit stress free. I am worried about fixed income in future and highly worried about infaltion/hyper inflation so please advice accordingly. Currently I save 20K per month, I do not have health cover at the moment. Here is my total assets:

4 L in equities

2 L in gold ETF

23 L in FD

5 L in MF

A house worth 40 L

Please suggest the most intelligent way to manage these funds.

Regards.

Hi Sujit

Not much can be suggest like this. We suggest that you do your financial planning once and align your wealth for your goals in future.

I will surely think about that. Meanwhile what are your views on 23L in FD, I know it is a lot so how it should be distributed. Thanks.

I suggest moving it to atleast a FD to earn better interest. And at best, I think you should put it in equity funds …

Thank you Manish for a wonderful article

I have made same kind of mistake in ULIP, Paying since five years

and realize the thing. Last year purchased Term Plan with same premium and

20 times more Sum Assured. withdraw the ULIP which gave negative return.

I think you did the right thing 🙂

Hi Manish, thanks for your article. I myself directly experienced buying wrong product. I bought one ULIP product three years back and paid first two years premium. later only I realized that it was waste of money. I didn’t pay remaining premiums. I would have got some good returns even if I invested my money in FD or RD.

Thanks and Regards,

Dhinesh A.

Thanks for sharing that Dhinesh

Great.

Illiteracy in finance is huge weakness. Though it is very late, your articles are very useful for people like me.

Thanks

Thanks for your comment SureshUnnikrishnan

ok , so out of 10 or 100 or 1000 there are only 4 reasons not to take “wrong product” ?.

wrong product is wrong product. that’s it.

Thanks for your comment netizen

Hi manish ,

Its a mindblowing article . Hoping that it would change life of millions. Anyone should not take such bad financial experiance.

Thanks for your comment Sunil

Hi Manish,

I need an advice regarding an ULIP I was trapped into at the start of my career back in 2007. SBI ULIP Plus II Growth Fund was sold to me with an annual premium of 24000/- and 3 yrs lock-in period. As per agent, I understand my life insurance is active till the time fund value is at least equal to one year premium (24000). Currently am using this policy to save tax on paid premium and then partial withdraw similar amount when needed.

Please advise what should I do along with pros and cons of each option, if possible.

(a) Continue paying premium and keep policy in force n hope that it may fetch decent return in long term

(b) Maintain amount like 30000/- (more than one year premium) just to maintain life insurance and stop paying further premium

(c) Simply surrender the policy

Also, kindly guide how to decide upon appropriate switch option in case policy continues.

I am happy that I’ve stopped being trapped into such bad financial product and I advise the same to all my friends/relatives after coming across this portal and your eye opening articles. Thank you.

Hi Vicky

I strongly suggest just get out of it now and take whatever you are getting right now. BUy a term plan for life insurance and reinvest all money in equity mutual funds.

Hi Manish,

Thanks for response. I do have term insurance as well. Would you still suggest to surrender the policy? Does it make sense to keep life insurance active by simply maintaining 30k fund value as it is already 9 yr old policy as it has 20L sum assured? I am sorry to take your time but it would greatly help if you can help me understand pros and cons of available options.

From what I understand, I dont suggest continuing this for this small point . Better have a clear portfolio !

To add on to what Manish has written “Spend 1hour before getting into any financial product”, I would like to suggest the following pointers.

1. what are the charges?

2. what are your commissions?

3. what are the returns? show me the math of that.

4. what are the risks?

5. what is the lock in period of this investment?

6. Finally, what is the goal for which you are considering a specific financial product.

GOod points Rajesh

Thanks for the artical Manish !

Since last week i am into same dilemma. 3 years ago I had bought LIC Whole Life Policy Limited Payment policy (SA 5 Lacs, TT-5, Term 44 years Premium to be paid for 34 years only, Premium 16000 yearly). I think being endowment policy its costly & i am loosing on opportunity cost & i should surrender it.

At least i will get guaranteed Surrender Value (30% of all premiums paid – 1st year’ s premium) for 3 years. Vested bonus value is Rs.1 lac as of today.

Kindly request you or experts to comment.

Dear Manish,

I got my answer through your other artical “Why Endowment policy must be avoided”

Link : http://jagoinvestor.dev.diginnovators.site/2008/10/why-endowment-policy-are-never-best_08.html

Thanks for eye opening views.

Glad to know that SantoshJunnarkar ..

Yes, looks good. Better surrender it and use the money in something better

I was also missold an insurance policy that I surrendered after 5 years and loosing 5 thousand rilupees of my invested amount but if is consider if is had isunvested that 6 lacs some where else it would have given given me at least 9% return.

Thanks for sharing that himanshu

Yes, please make sure no pressure, emotion, fear, greed, push from others forcing you to you invest in any financial products.

I had a bad experience with ICICI Bank once, and from then I decided whenever I invest in any new products make sure where you are putting your money, what is expected return and risk etc.

I agree, when people loose money in unsuitable products some people come out very fast but for some people its very hard to come out so they think products likes MF is not suitable as well which is not the case most of the time.

Private banks like ICICI and HDFC prey upon customers like vultures to mis-sell useless insurance policies, ULIPs and of course platinum credit cards. Recently, my dad went to HDFC to request Internet Banking facility for his account. They made him sign in 6 different places in a bunch of forms stapled together. He was in and out of the bank in 5 minutes, What great service right? 4 days later, some HDFC guy came to deliver a parcel which he signed for. It was for a high end credit card with huge annual fees issued in his name. Where did that come from and where is the Internet Banking facility he signed up for?

So guys, never ever sign for anything without first taking the forms home and reading carefully what it’s all about.

“never ever sign for anything without first taking the forms home and reading carefully what it’s all about.” A very very very important point made by anjan . Now days these guys have become smart they have devised new tactics to somehow not allow the customer time to think and ponder . Now many schemes are being promoted over phone . I ask them to send email or brochure . The answer i get this “Sarr its not available with us but saar i can explain to you over call , also saar when can i send my person to your place or office “

Better to not talk to them in case they cant give you the PDF for that policy

Thanks for sharing that Anjan

Hi Renga

I think you should make it paid up or surrender the policy.

Manish

Thanks for sharing that Renga

Hello Sir,

I can also relate to this article.

I have also buy a LIC policy having term of 25 years and paying 8000 quarterly. Shall i discontinue this??

Though i am already investing in equity.Pls suggest.

I would suggest you to stop that LIC policy, provided you have not crossed half of the journey, I mean you have not reached the 12 year mark in your case.

There is a case for endowment plans in which atleast 3 year premium were paid (irrespective of whether it is continued or not) you will get the premiums paid sofar with bonus(any if applicable) will be paid at the time of maturity or demise whichever is earlier. Read about Paid-up poilcies

Hi Deena Thank you very much.

Its been only a year paying the premium, can you tell how much will I be getting the refund.

I bought an LIC ENDOWMENT PLAN in year 2008 for 16 year term with sum assured 5lac. I am paying premiums continuously till now . Would it be good decision to to invest this amount in diversified equity mutual funds for 10 year to compensate my loss in insurence plan.

Yes, its very much suggested ! . Incase you are new to mutual funds, we can help you in that – http://www.jagoinvestor.com/start-sip

Friends, Do not surrender LIC endowment policy before checking the amount you receive.

My recent experience is I had endowment policy with 30 yrs term premium 3063/yr with 1 lakh sum assured, i had finished 18 yrs already. My agent told me i will get approx 1.8 lakh(includes the vested bonus of 1 lakh). I surrendered the policy , but what i got was only 68000. Customer care said, we get only 50% of total amount and then some charges is deducted.

I think your agent lied to you !

Yes, better get out of it.

I can see that you are interested in investing in mutual funds. I want to share that now you can invest in mutual funds with Jagoinvestor as your advisor

We create a FREE online account for you, from where you can invest and redeem online.

Our team will be happy to explain you more on this.

Find more at http://jagoinvestor.dev.diginnovators.site/start-sip

Manish