Do you want to get rid of your old money back insurance plans, but are confused if you should “surrender” or make it “paid up”?

Today I will explain which one is the best option amongst the two.

Surrender vs Paid-up option in Insurance policies

All those assured insurance plans which your parents made you buy from your friendly neighbourhood uncle is nothing less than a high premium low return policies with not more than 1-5% CAGR return.

These policies don’t provide enough life insurance cover neither they create enough wealth for you for your long term goals like children education, child marriage or retirement and on top of that, these policies have pathetic returns value if you want to close them before maturity and take back your money.

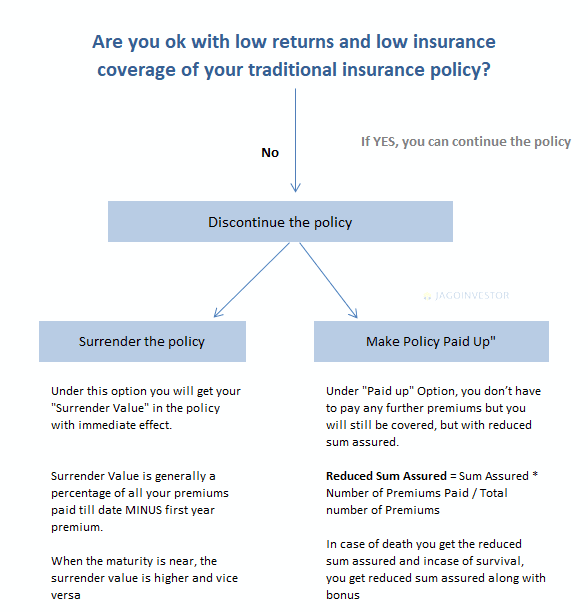

Mainly there are two ways to discontinue these insurance policies which are –

- Paid-up Policy

- Surrender Policy

What is “paid up” option?

Under this option, if a policy holder does not close the policy, but stops paying any further premium. However, note that this option is generally applicable only after one has paid for at least 3 yrs. (however, check your policy wordings for exact years)

The amount which you will receive at maturity will be reduced, in proportion to the premiums paid. This sum assured is called the paid up value. It is calculated using the following formula:

Paid up value = Original sum assured x (No. of premiums paid / No. of premiums payable)

Example – A traditional insurance policy with sum assured of Rs. 10 Lakhs for 20 years with a premium of Rs. 30,000 p.a. paid for 8 years. Let’s find out what will be its paid up value if one wants to stop paying further premiums.

Paid up value = 10,00,000 * 8/20 = 4,00,000

At a high level, the numbers don’t look back. You will get 4 lacs, but you paid just 2.8 lacs overall, however, remember that you will get this 4 lacs after so many years and you will lose the purchasing power because of inflation.

You can simply say that real worth of Rs. 4 lac received after 12 years is Rs. 1,58,000 today, taking inflation at 8%.

Therefore, if you are choosing policy paid up option, keep in mind that converting the policy into a paid-up policy will lock your money for the remaining term of the policy and also, actual worth of the amount, which you will receive in later years will be very less if the maturity of the policy is very far from now.

What is “surrender policy” option?

Under this option, you close the policy completely and take back your money. The money you get will be some percentage of your premiums paid minus the first year premium. And this percentage increases depending on how many years the policy premium has been paid.

A policy generally acquires any surrender value only after 3 yrs of premium payment, which means that if you choose to surrender your insurance policy before 3 yrs, you lose all your money and don’t get back anything.

Note that the surrender value starts with 30% and goes up depending on the number of years you have paid the premium.

Following is an indicative table which shows the surrender value as a percentage of premiums paid

[su_table responsive=”yes” alternate=”no”]

| Time of Surrender | % of premium paid – first year premium |

| After 3 years | 30% of premium paid |

| After 5 years up to 8 years | 50% of premium paid |

| After 8 years | 65% of premium paid |

| Last 2 years to policy maturity | 90% of premium paid |

[/su_table]

This percentage can change from company to company and depends on factors such as the type of policy. Every policy brochure mentions details about surrender value but, it is not compulsory that all the companies mention this percentage which is also called the surrender value factor in their brochures.

Example of surrender policy

Mr Pratik has bought a traditional insurance plan of 20 years with a sum assured of 6 Lakhs premium amount is Rs. 20,000 per year. After paying the premium of 6 years, he wants to surrender the policy.

Surrender Value = 50% of (premium paid – first year premium)

= 50% of (120000 – 20000)

= 50% of 1,00,000

= Rs. 50,000

You can see that he will just get Rs 40,000 from surrendering the policy even if he paid Rs 1,20,000

When to choose “Surrender” and “Paid up” option?

Surrendering a policy is suggested when

- You are not able to pay the premiums

- You need money for some reason

- When remaining number of years in policy is more than 8-10 yrs

This option is suggested because you still have many years left and you can pay the same premium amount in a better product which will do wealth creation for you.

Making a policy paid up is suggested when

- You don’t need money but don’t want to pay further premiums

- When you don’t want to pay premiums, but still want the policy to run

- When your policy maturity is very near (2-4 yrs)

Making a policy paid up is generally not suggested, but a lot of times, investors are not able to take the pain of getting the reduced amount from their policy and feel like “they will get something in future”, however considering “time value of money“, it’s not a great option.

How to deal with the emotional part “I am facing so much loss”?

In both the options, there will be a loss for sure. Money back insurance plans are designed to give low yields and penalize you if you quit in between.

I think dealing with closure of insurance policies is more of a psychological battle You know you have got a wrong product and its bad for your future, but people can’t deal with the fact that they are facing so much of loss – “I paid 8 lacs, and I will get back only 4 lacs, I will lose 4 lacs”

Note that if you consider TIME VALUE, things will be easier to decide.

If your friend borrows Rs 100 from you and returns you Rs 110 after 10 yrs, you are not in profit, you are actually in LOSS. Because you could have created Rs 250 with an alternate investment and now you just have Rs 110, that’s Rs 140 loss.

Just looking at it from absolute numbers point does not make sense.

For example, imagine a sum assured of Rs 10 lacs with a yearly premium of approx. Rs 53000 per year. Now if a person has already paid 5 premiums and wants to surrender the policy, they will just get back around Rs 85000 (assuming 40% of 4 premiums, as one premium is deducted). The immediate loss of mind is for Rs 1.8 lacs (paid 2.65 lacs and getting back 85,000)

This is a tough situation for the mind and very tough to handle. A person feels why to take a loss when one is not recovering the amount paid also and just continues the policy till the end. The person will get back anything between 15-18 lacs, depending on the bonus amount declared.

This translates to only 5.69% and this the best case (it will get better if you die early after taking the policy, but I am sure you would not like it)

Now if the same person reinvests the same 85,000 along with Rs 53,000 premiums yearly into some equity-based products like equity mutual funds or index funds, even if assume a modest 12% returns which have happened in past, the wealth one will have will be 24.5 lacs and the IRR will be approx. 7.4% of the whole scenario. This second option also gives you better liquidity and exit option whenever you wish to get money.