Do you exactly understand what the Claim Settlement Ratio in Insurance is?

A lot of people just look at the claim settlement ratio and make an opinion about an insurance company. In this article, let me break some myths and help you understand more about the claim settlement ratio.

What is Claim Settlement Ratio?

In simple words, the claim settlement ratio is the percentage of claims paid in a financial year.

Claim Settlement Ratio = (No of Claim Paid / No of Claims Received)

So if a company gets 1000 claims in a year and pays 985 of them, then its claim settlement ratio for that year will be 98.5%. An important point to note here is that it’s about the number of claims and not the number of claims.

What type of Claims is considered in the Claim Settlement Ratio?

Generally, most of the people willing to buy a term plan look for this ratio as they are concerned about the claim getting paid in case of their early death. But claim settlement ratio is not the same as the “death claim settlement ratio”

In the calculation of the claim settlement ratio (in the case of life insurers), all types of claims are considered like.

Death Claim: The claims once the policyholder dies

Maturity Claims: Policies that are maturing and needs to be settled

Surrender Claims: Policies that are closed prematurely and surrendered

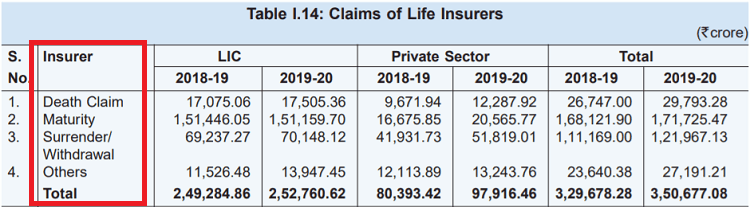

Here is the breakup from the IRDA report of 2019-2020, where you can see the number of claims for LIC and private insurers

Is Claim Settlement Ratio a probability?

One of the biggest myths about CSR (Claim settlement ratio) is that it’s a probability of claim settlement. This is not true and often leads to misjudgment of an insurance company.

CSR is simply a way of representing the data and nothing else. It does not tell you about the intention of the company. Let me share this with an analogy

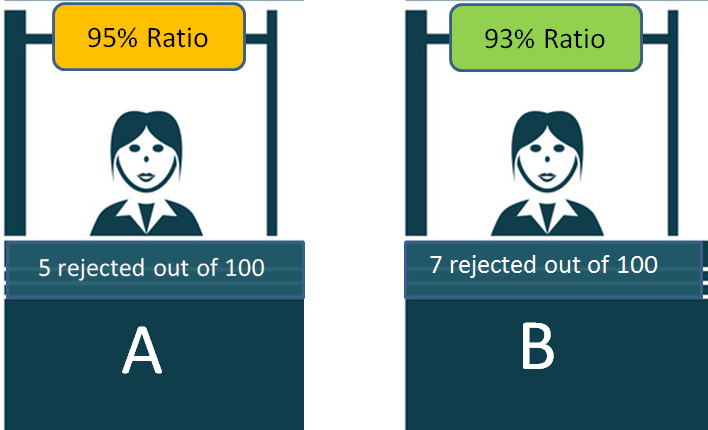

Imagine there are two VISA processing counters which are looking at documents of people and giving the VISA or rejecting it.

Now if the Visa will be approved or rejected depends mainly on how proper are the documents and the person and not depend on the person who is processing the Visa. If the documents and case fall into the rules set, then it will be approved, else it will not.

So imagine there are two counters A and B . Counter A rejects 5 people out of 100 and Counter B rejects 7 people out of 100.

Now, this simply means that counter A got 5 people who did not fit into the set rules or their documents had issues. In the same way counter, B got 7 people who had incomplete documents.

One cannot mistake these 93% (A) and 95% (B) as the probability of their visa getting rejected.

Hence, in the same way, the claim settlement ratio just tells you about what kind of claims did the insurance company received and how many of those claims were rejected. It’s not a probability.

Investors mostly have a very bad view of companies and attribute these rejections to their intentions, which is not a correct way to look at this ratio.

Does Claim Settlement Ratio depend on the policyholder?

Yes

A claim that will be rejected or accepted depends mostly on the policyholder itself. There are many people who file a claim which is bound to get rejected as it’s not valid as per the terms and conditions of the policy document.

Many policyholders also have a very vague and wrong impression of what is covered and what is not. They file claims based on flimsy assumptions and for things that are out of the scope of rules.

Let me give you an example.

Imagine a person who lied to the company while taking a term/health insurance, that he is a smoker and also went through some surgery in past. He lied to the company.

After some years the claim was filed (person died or got hospitalized) and now the company finds out the information provided by the insured person was false and hence the claim should not be paid in this case and it’s totally valid rejection.

So here it’s not the company who had the wrong intention but the customer who created a situation that led to claim rejection. Most of the policies which are rejected fall into this category.

From your end, you have to understand one thing. If you have bought your policy properly and revealed all the information properly, your claim will not be rejected. However, if you give reasons for the company to reject your claims, it will surely be rejected and there is nothing wrong with that.

What is Claim Intimation Ratio?

Claim Settlement Ratio tells you about “number of policies”, whereas Claim Intimation Ratio tells you about the “AMOUNT”

It tells you what percentage of the claim amount was paid out of the total claim amount which was claimed in a year.

Claim Intimation Ratio = (Amount Paid / Total Claim Amount)

Most people are not aware of this ratio, and this gives you better clarity about the claims paid by a company. It may happen that a company has a high claim settlement ratio, but its claim intimation ratio is lower than the other company.

Here is an example of how the Claim settlement ratio can be high despite a low intimation ratio

Company A and B receives 10 claims in a year as follows

9 claims of Rs 10 lacs each

1 claim of 1.1 crore

[su_table responsive=”yes”]

Company A

Company B

Claim Rejected

1 claim of 1.1 crores is rejected

2 claims of 10 lacs are rejected

Claim Settlement Ratio

9/10 = 90%

8/10 = 80%

Claim Intimation Ratio

90 lacs / 2 crores = 45%

1.8 crore / 2 crore = 90%

Comment

Claim settlement ratio is high, but not the amount paid

Claim settlement ratio is low, but the higher amount paid

[/su_table]

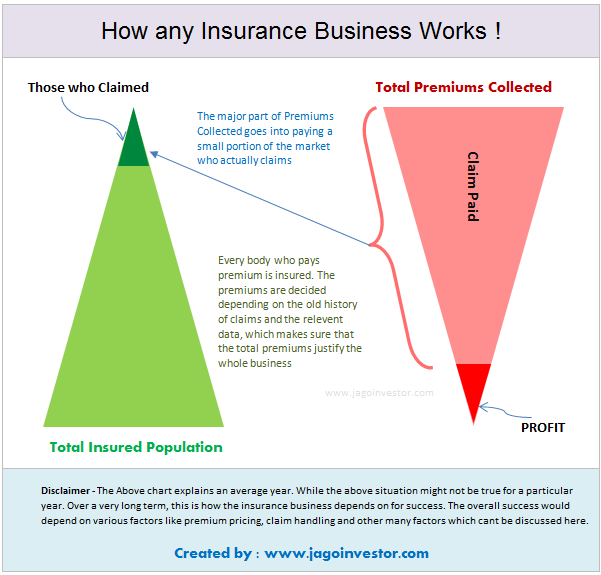

Business Model of an insurance company

As a customer, you should be very clear about the business model of an insurance company. An insurance company is a for-profit organization whose intention is to stay profitable and work for its profitability and also serve its customers as well.

The insurance company collects a small premium from a large number of people, but that money eventually goes only to a handful number of people who file for a claim. So in a way, it’s a shared resource which is given to those who are valid claimants.

In order to stay in business and be profitable, an insurance company has to reject all the claims which are not valid. If they start paying each and every claim without proper verification, they just won’t survive and it’s not in the customer’s interest.

This simply means that a company with not the best claim settlement ratio, in reality, is a good company because knows how to protect itself and not let a fraudster make a wrong claim.

A very important point to note is that a new insurance company will mostly be getting death claims in the starting 8-10 yrs and not any maturity claims which means their claim settlement ratio may look on the lower side.

How to buy an insurance policy?

Basically here is a high-level step by step process

Look at a company whose name you trust

Choose a company which has been few years old (this depends on you)

Choose a company whose product you like (features etc)

Check out the experience of other investors online about the company

Buy a policy with full honesty and by disclosing all information

Don’t lose your sleep over Claim Settlement Ratio

In the end, I just want to say that the claim settlement ratio is not a useful metric for any purpose and you should not lose your sleep over it. Don’t worry too much.

Do you want to get rid of your old money back insurance plans, but are confused if you should “surrender” or make it “paid up”?

Today I will explain which one is the best option amongst the two.

Surrender vs Paid-up option in Insurance policies

All those assured insurance plans which your parents made you buy from your friendly neighbourhood uncle is nothing less than a high premium low return policies with not more than 1-5% CAGR return.

These policies don’t provide enough life insurance cover neither they create enough wealth for you for your long term goals like children education, child marriage or retirement and on top of that, these policies have pathetic returns value if you want to close them before maturity and take back your money.

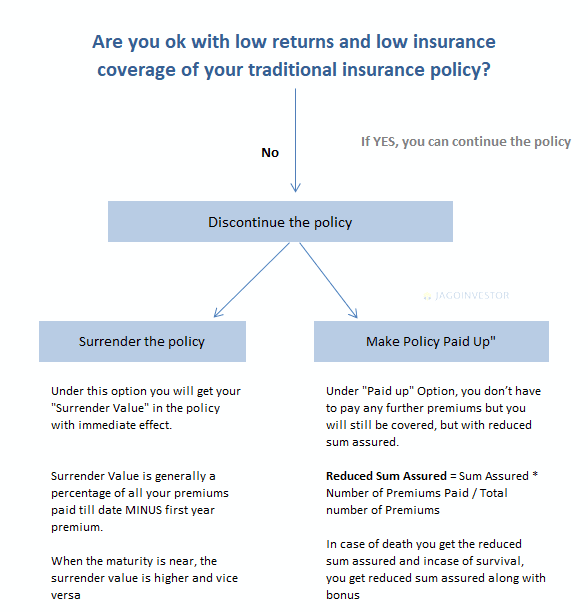

Mainly there are two ways to discontinue these insurance policies which are –

Paid-up Policy

Surrender Policy

What is “paid up” option?

Under this option, if a policy holder does not close the policy, but stops paying any further premium. However, note that this option is generally applicable only after one has paid for at least 3 yrs. (however, check your policy wordings for exact years)

The amount which you will receive at maturity will be reduced, in proportion to the premiums paid. This sum assured is called the paid up value. It is calculated using the following formula:

Paid up value = Original sum assured x (No. of premiums paid / No. of premiums payable)

Example – A traditional insurance policy with sum assured of Rs. 10 Lakhs for 20 years with a premium of Rs. 30,000 p.a. paid for 8 years. Let’s find out what will be its paid up value if one wants to stop paying further premiums.

Paid up value = 10,00,000 * 8/20 = 4,00,000

At a high level, the numbers don’t look back. You will get 4 lacs, but you paid just 2.8 lacs overall, however, remember that you will get this 4 lacs after so many years and you will lose the purchasing power because of inflation.

You can simply say that real worth of Rs. 4 lac received after 12 years is Rs. 1,58,000 today, taking inflation at 8%.

Therefore, if you are choosing policy paid up option, keep in mind that converting the policy into a paid-up policy will lock your money for the remaining term of the policy and also, actual worth of the amount, which you will receive in later years will be very less if the maturity of the policy is very far from now.

What is “surrender policy” option?

Under this option, you close the policy completely and take back your money. The money you get will be some percentage of your premiums paid minus the first year premium. And this percentage increases depending on how many years the policy premium has been paid.

A policy generally acquires any surrender value only after 3 yrs of premium payment, which means that if you choose to surrender your insurance policy before 3 yrs, you lose all your money and don’t get back anything.

Note that the surrender value starts with 30% and goes up depending on the number of years you have paid the premium.

Following is an indicative table which shows the surrender value as a percentage of premiums paid

[su_table responsive=”yes” alternate=”no”]

Time of Surrender

% of premium paid – first year premium

After 3 years

30% of premium paid

After 5 years up to 8 years

50% of premium paid

After 8 years

65% of premium paid

Last 2 years to policy maturity

90% of premium paid

[/su_table]

This percentage can change from company to company and depends on factors such as the type of policy. Every policy brochure mentions details about surrender value but, it is not compulsory that all the companies mention this percentage which is also called the surrender value factor in their brochures.

Example of surrender policy

Mr Pratik has bought a traditional insurance plan of 20 years with a sum assured of 6 Lakhs premium amount is Rs. 20,000 per year. After paying the premium of 6 years, he wants to surrender the policy.

Surrender Value = 50% of (premium paid – first year premium)

= 50% of (120000 – 20000)

= 50% of 1,00,000

= Rs. 50,000

You can see that he will just get Rs 40,000 from surrendering the policy even if he paid Rs 1,20,000

When to choose “Surrender” and “Paid up” option?

Surrendering a policy is suggested when

You are not able to pay the premiums

You need money for some reason

When remaining number of years in policy is more than 8-10 yrs

This option is suggested because you still have many years left and you can pay the same premium amount in a better product which will do wealth creation for you.

Making a policy paid up is suggested when

You don’t need money but don’t want to pay further premiums

When you don’t want to pay premiums, but still want the policy to run

When your policy maturity is very near (2-4 yrs)

Making a policy paid up is generally not suggested, but a lot of times, investors are not able to take the pain of getting the reduced amount from their policy and feel like “they will get something in future”, however considering “time value of money“, it’s not a great option.

How to deal with the emotional part “I am facing so much loss”?

In both the options, there will be a loss for sure. Money back insurance plans are designed to give low yields and penalize you if you quit in between.

I think dealing with closure of insurance policies is more of a psychological battle You know you have got a wrong product and its bad for your future, but people can’t deal with the fact that they are facing so much of loss – “I paid 8 lacs, and I will get back only 4 lacs, I will lose 4 lacs”

Note that if you consider TIME VALUE, things will be easier to decide.

If your friend borrows Rs 100 from you and returns you Rs 110 after 10 yrs, you are not in profit, you are actually in LOSS. Because you could have created Rs 250 with an alternate investment and now you just have Rs 110, that’s Rs 140 loss.

Just looking at it from absolute numbers point does not make sense.

For example, imagine a sum assured of Rs 10 lacs with a yearly premium of approx. Rs 53000 per year. Now if a person has already paid 5 premiums and wants to surrender the policy, they will just get back around Rs 85000 (assuming 40% of 4 premiums, as one premium is deducted). The immediate loss of mind is for Rs 1.8 lacs (paid 2.65 lacs and getting back 85,000)

This is a tough situation for the mind and very tough to handle. A person feels why to take a loss when one is not recovering the amount paid also and just continues the policy till the end. The person will get back anything between 15-18 lacs, depending on the bonus amount declared.

This translates to only 5.69% and this the best case (it will get better if you die early after taking the policy, but I am sure you would not like it)

Now if the same person reinvests the same 85,000 along with Rs 53,000 premiums yearly into some equity-based products like equity mutual funds or index funds, even if assume a modest 12% returns which have happened in past, the wealth one will have will be 24.5 lacs and the IRR will be approx. 7.4% of the whole scenario. This second option also gives you better liquidity and exit option whenever you wish to get money.

It is very easy to buy life insurance. You just pay the premium, attach some documents, get your health check-up done and you will become a policyholder. Even nowadays it has become more convenient to buy, as most of them can be bought online.

So, at the time of buying it’s really the fast process but, have you thought that how will your family get the claim settled after your demise? What all will be the steps that they need to take to receive the claim amount? It is important to have life insurance for your family’s financial security against the risk of your death but what’s more important is, that eventually its benefits must reach the beneficiary.

In this article, we will guide you on what all steps your family members will need to take to get your life insurance sum assured amount so that you can inform them about all the procedures and documents required to get assured life insurance sum.

What is Life Insurance?

Lets first see what does life insurance means by definition. So, “Life insurance is a contract between an insurance policyholder and an insurer (insurance company), where the insurer promises to pay a designated beneficiary a sum of money in exchange for a premium, upon the death of an insured person.” It means the main purpose is to provide a sum of money to the designated beneficiary (a nominee or legal heirs). So, now let’s see what does your beneficiary need to do to get the claim settled.

Claim settlement Form:

Firstly your family member has to get a claim settlement form from the insurance company and fill all the details. Along with the form he/she needs to attach all the documents along with the form. The list of all the documents required is given below:

Original Policy document

In the form, it is asked whether a claimant is a nominee or not? If not then the claimant needs to prove that he is a legal heir of the deceased by submitting the “Will” or if there is no will then it has to be proven by Succession laws.

If the claimant is a Nominee then Nominee ID proof establishing the relationship between nominee and person who died has to be provided.

Notarized death certificate of the policyholder (deceased)

In case the death happened in the hospital, document of hospital

Copy of claimant’s current address proof

In case of Accidental Death along with the above documents following are to be attached:

Hospital certificate

Post-mortem Report

FIR copy

Final report of police

Newspaper cutting if any

Driving license of the person if the death happened while driving due to the accident

In case of death outside India, was the deceased buried or cremated abroad? If yes, enclose a copy of the burial/ cremation permit.

It is very important to keep the acknowledgment slip mentioning all the documents which were submitted because it may be required for compliance of claim settlement.

Settlement of claim

As you now know how to claim, the next question will be how much time will it take to get the money? So, for this read the provisions on claim settlement provided by IRDAI.

As per the regulation 8 of the IRDAI (Policy holder’s Interest) Regulations, 2002, the insurer(company) is obligated to settle a claim within 30 days of receipt of all necessary documents including extra documents sought by the insurer. If the claim requires further investigation, the insurer needs to complete its procedures within 6 months from receiving the written intimation of the claim.

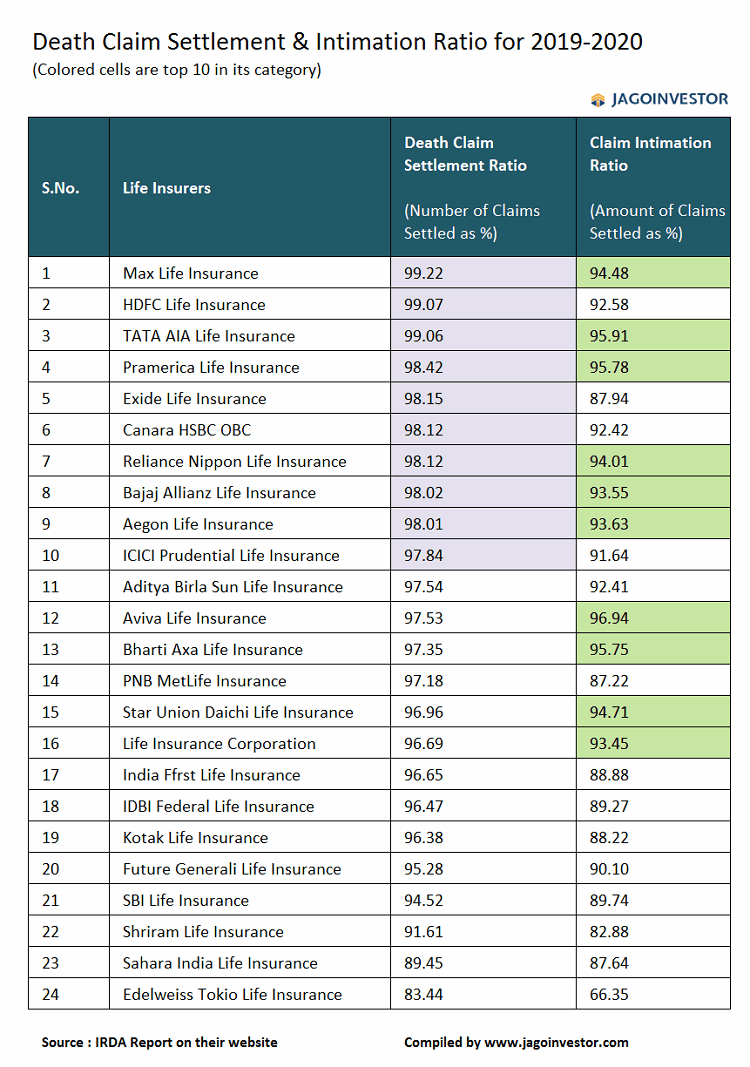

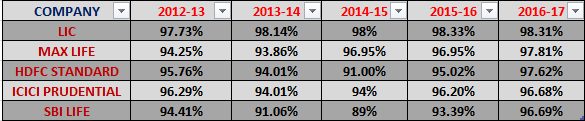

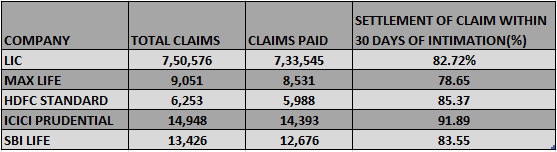

List of top 5 insurance company with death claim settlement ratio for the last 5 years – Below given table shows the claim settlement ratio of insurance companies. It is based on the individual death claim number published every year by IRDAI in its Annual Report. LIC tops the list of death claim settlement ratio for the last 5 years.

To give you a clearer picture, I have attached the screenshot of top 5 insurance companies during individual death claim settlement within 30 days of intimation.

Where to go if there is a dispute between the claimant and the insurer?

In many cases, life insurance claims have been delayed or denied due to a lack of proper documentation. So, make sure that your claim should not be denied due to this. And even after this claim settlement is delayed then there is a special court called Ombudsman of IRDAI (is a special court) where all claim-related disputes are solved. So if the claimant feels that they are being cheated or the claim is rejected despite submitting all the required documents then the claimant can approach the Ombudsman of IRDAI.

I hope now you are clear with the procedure to claim your settlement. Please feel free to comment about how fruitful this article was.

As per IRDAI, the insurance regulator – it is now mandatory to link your Aadhaar and PAN number with your insurance policies. Though this linking process does not have a deadline right now, its advised to act fast and complete this action asap to avoid any last minute rush and issues which you might face at the time of renewal or claims.

Note, that those investors who still don’t have PAN , have an option to submit form 60.

How to link Aadhaar & PAN in your LIC policy?

If you have any existing life or health insurance policies, you should link your Aadhaar and PAN soon.

As most of the investors have LIC policies, I am covering the online and offline process for LIC policies right now in this article and will give the links to update the Aadhaar for some other companies as well.

Online Process for updating Adhaar in LIC policies

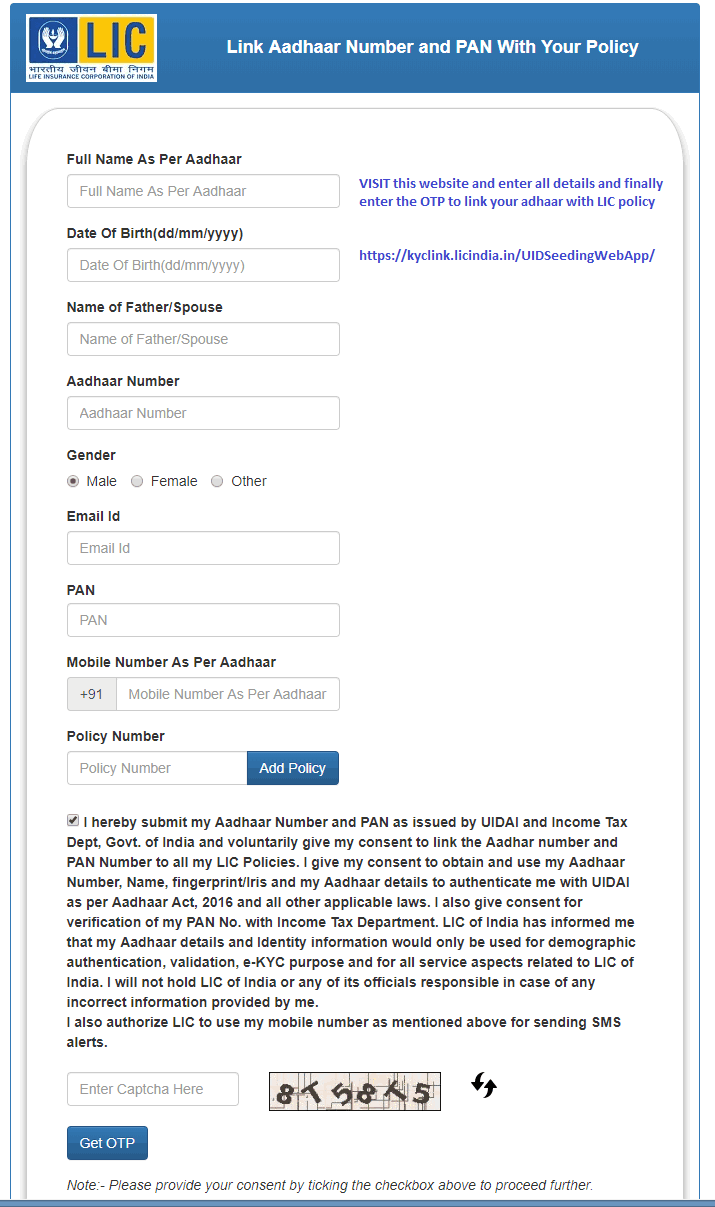

If you want to update your Aadhaar in your LIC or any insurance policy, the first criteria is that your active mobile number should be linked to your Aadhaar number, so that you can generate OTP which is necessary for the registration process.

and then click on generate OTP. Here is how it looks like.

Step #3: You will get an OTP on your mobile, which you need to enter on the site and click on submit. You will see the massage of successful registration for Aadhaar linking with LIC.

It might take few days to link your Aadhaar number with your Policy. Once this linking process is completed after verifying your details from UIDAI, you will be informed via SMS/e-mail on your registered mobile number or mail-ID. You can also watch this video to know the process.

Online Process for updating Aadhaar in LIC policies

You can also have an option to visit your LIC branch and fill up the offline form to link your adhaar and PAN with your policy. Make sure to take an acknowledgement letter once you complete the process.

How to link your Aadhaar and PAN with non-LIC policies?

Each and every insurance company has implemented the solution of linking Aadhaar with policies and you will find a dedicated page on their website. Just search for “Aadhaar + PAN + Linking + <<enter Insurance company>>” in google and you will surely get the link for completing the Aadhaar linking process.

However we are putting up a small list of some insurance companies and their respective links to make it easy for you.

Note that this takes just 1-2 minutes of your time, but its an important thing to complete. If you still have any doubt regarding this linking process you can leave your query in the comment section.

If you are planning to buy a term insurance plan in coming weeks, then you are at the right place, because today I will share dozens of points which any term plan buyer should know before they buy the cover.

So, if you have no idea of how does term insurance work, and if you have asked yourself – “Which term plan should I buy?”, then you are at the right place today.

Most of the buyers who are new to term insurance plans do not understand various critical facts and points which they should consider while they are buying the policy and because of that, I came up with this checklist which will help you.

Let look at each point in detail.

1. Earlier you buy a term insurance plan, better it is

There is no minimum or maximum age for term insurance. Earlier you purchase the policy better it is.

Do not be very late because as time passes, your premium amount will also increase depending on your age and also if you develop any illness or disease, it will get tougher to get the policy later. So once you are clear that you require a certain amount of life cover, go ahead and complete the action within a few months.

2. Buy the term insurance policy only till your retirement age

Till what age should you buy a term plan? Should a 30 yrs old guy buy a term plan up to 80 yrs? The answer is NO.

You should not buy it for the longest tenure possible because you only need life insurance policy till your retirement and not beyond that. This is because not many family members will be financially dependent on you beyond your retirement age.

When we are young, we have more financial responsibilities, and hence it makes sense to take a big cover. But as our age increases, our assets will grow and at the same time, we will be moving towards the retirement age, at which point we no longer remain provider for our families.

3. Don’t get mislead by “per day premium” marketing gimmick

A lot of insurance companies have started to advertise their term insurance plans by sharing the cost per day basis, like for example – “Buy 1 crore term plan just for Rs 25/day”. However, note that these numbers might be applicable only for a certain age group and tenure of the policy.

Like it might happen that the advertised premium per day is only for the clients around 25 yrs and for a policy of 40 yrs.

Your case will be different and the premiums might differ for you, so don’t get trapped by the lure of cheaper premiums.

4. Don’t buy single premium policies

At times, you have to choose between single premiums vs. regular premium while purchasing a life insurance policy. A lot of people think that just because they can afford to pay a onetime premium, it makes sense, but it’s not true.

Other than some cases, it does not make much sense to pay a one-time premium (single premium) while buying a term plan. The best option which will work for most people is the yearly premium. So if your agent is trying to explain to you how a one-time payment will help you save the cost, run away and don’t fall for it.

5. Take an increase in premiums in a positive manner

This is a big one which is critical to understand.

When you buy a term plan (or even health insurance), sometimes your premiums can increase after your medicals are done and you may be asked to pay an extra premium. This increase in premium is due to health issues and it’s very valid to ask you to pay this extra premium.

Most of the buyers are very critical of the premium increase and choose to not move ahead or postpone their decision of buying the plan.

However you should understand that the premiums increase is a natural thing to happen if you are of the high-risk category (like a smoker, alcoholic or if some past illness). It’s actually a good thing that the company is beforehand checking the facts and still offering you the plan, though at a little high premium which is very fair from their point of view.

At that point, rather than postponing the decision, the best thing is to go ahead and buy the policy.

6. Don’t get over-excited by term insurance riders

“Riders” are great add on with a term insurance plan, but only if you really require them or if they are specific to your case. Don’t add them just because it’s available and gives you a sense of more security. I mean if you do a lot of travel and are most of the time in your case, the risk of dying in an accident is higher for you, so in that case, you can add an accidental rider. Here are various types of term plan riders

Accidental Death Rider

Permanent & Partial Disability

Critical Illness

Waiver of Premium

Income Benefit Rider

In the same way, if you feel that you want to cover the risk of some critical illness in the future and don’t want to buy a separate policy, then you can add critical cover. But don’t add any term insurance riders for the sake of it.

7. Buy the basic version of the term insurance plan

A term plan comes into various flavors nowadays. The most basic one is the one which pays you a lump sum on death. However, there are other variations now which also gives you income for 10/20 yrs along with the main cover, or pays only the income for the next 10/20 yrs and a small lump sum at the time of claim.

I think one should just choose the base policy in most of the cases. Most of the other options are designed for very specific situations and they are not “better” or “bad” compared to the base policy. To check this, you can go to any term insurance premium calculator and find out the premium with rider and without a rider.

8. Tell them if you are smoker/alcoholic

One of the worst things you can do while purchasing any life insurance plan is to hide the fact that you are a smoker or consume alcohol. Please don’t hide it. There is nothing like a best term insurance plan for smokers in India at the moment.

Your premium calculation happens based on this critical information and if you hide these facts, then you are actually breaching the contract with the company and almost always your claim will be rejected at the end. Also, don’t think that just because you smoke just once in a while does not make you a non-smoker.

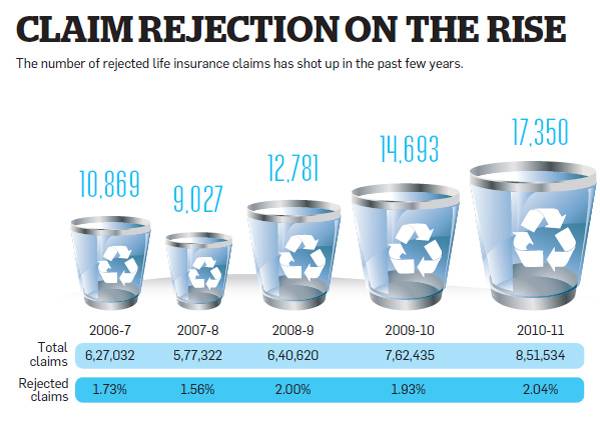

Below is some data from economic times on the rising number of claim rejections because of the hiding of information.

If you smoke (even though every fewer number of times), you are a smoker in the eyes of the life insurance company. Same is the case with those who take alcohol.

Make sure you fill your own form because there have been cases when an agent just mentions the policyholder as non-smoker or non-alcoholic to make sure the policy is easily issued.

9. Don’t hide your health information

Another grave mistake done by policy buyers is to hide any critical health information while purchasing the policy. If you have any health issues or have gone through any major operations/surgeries then you should clearly communicate that to the insurance company. One of the reasons for term insurance claim rejection is hiding important facts while purchasing the policy.

Please don’t wait for the insurance form to ask you the exact details.

An insurance policy is actually a proposal from your end in the eyes of law where you have to disclose all the facts and the company will accept your case or reject it. So the bonus of providing all the information is on you.

10. Don’t hide your family health history

Even your family health history matters. If your parents or siblings have some illness, then even that should be shared by you. Please don’t hide it because even that information impacts your premium.

Many people think that just because their parents had diabetes, it does not matter at all. That’s not true.

11. Don’t take small insurance cover (like 10-20 lacs)

Do you know that the average sum assured per India is in the range of Rs 90,000 to 1 lac only? Indians on average are highly uninsured, however, that’s mostly true for those who do not have term plans. But even those who have term plan try to cut the corners and eventually take less term insurance cover.

The most favorite number nowadays is Rs 1 crore. I see most of the people just taking a 1 crore term insurance plan thinking that it’s the right number. No, it’s not the case.

With the rising costs and lots of aspirations, Rs 1 crore might not be enough for most of the families all their life. I suggest you should take a good enough cover which gives you enough peace of mind.

Make sure you add up all your liabilities, 300 times of your monthly expenses and some more amount which can help your family reach your other financial goals and take at least that much cover.

If your life insurance requirement is Rs 1.3 crore, better than a 1.5 crore and not 1 crore.

12. Don’t overanalyze and delay your decision

Do you see that ad these days on TV where a lady shouts on her dead husband for forgetting to buy the life insurance even though they had decided to take it

“Kya, tum term insurance Lena bhul gaye, ab Ghar ka kharcha Kaise chalega”?

One of the biggest issues with most of the potential policy buyers is that they want to buy the best term insurance policy and don’t want to make any mistake. They are aware that they need a life cover, they also start searching for the policy, do the term insurance comparison, but then start to over-analyze the policy, its features, the premium comparison and what no.

Finally, they just don’t take any decision because of the analysis paralysis. They postpone the decision and think that they will “soon” buy it.

Don’t do this

But a decent term plan asap. Do some study, but don’t get into that zone where you are just stuck because of small points. It’s better to have a good term cover with any company, rather than having no cover trying to search for the best company.

13. Don’t forget adding nominee name

While filling the insurance form, make sure you carefully put the nominee name. But who can be a nominee in insurance? Ideally, it should be wife, children or someone whom you want to pass the term plan money. But try to avoid very old people as the nominee (in general).

Also make sure you mention this fact in your WILL too, or if you are not going to create a WILL right now, you can take the life insurance policy under MWP Act, so that your nominee will be the final person (it can only be wife and kids if you add MWP) who gets the money.

If you have bought the term plan long back and now your preference has changed, it’s better to change the nominee name.

14. Don’t take more than 1-2 policy

You should ideally have 1 term plan policy in your life insurance portfolio, the max can be 2 policies. But nothing more than that.

I have seen some people dividing their 2 crores of the cover into 4 policies of 50 lacs each with 4 different companies and it’s a little bit of stretch. In almost all cases, 1 single policy of a big amount is good enough.

However, if you still feel that you want to break it into two policies, that’s the maximum you should do. Also, some people who are buying another term plan after a couple of years should not note this point that they should eventually not have more than 2 policies.

15. Disclose the old insurance policy

When you buy any life insurance policy, it’s mandatory as per their rules to disclose the old insurance policy you already have. In most the cases, when people buy a term plan for the first time, they already have a couple of traditional insurance plans, but they fail to declare that.

I suggest you don’t do that because as per life insurance policies, a company should know how much coverage you already have and only based on that they will offer you additional cover.

If you have already bought a term plan without mentioning your old policies, you should reach the customer care of your term plan company and share with them about your old policies.

16. Be open to try online brokers

There are various online brokers which are building a long term business in the insurance space and provide various extra benefits to their customers like fast service, claim settlement assistance without you (customer) incurring extra cost, because they get compensated by the insurer (without putting any additional cost on your pocket).

The premium for you is the same if you buy it from the company directly only or through these brokers. These brokers give you various options to choose from and help you buy the policy which you want.

You can approach these brokers if you really feel they will add value to your transaction. I am not saying that online brokers are the only way to buy. If you are very critical of them or are old fashioned, then you can directly reach to company or your neighborhood broker.

17. Check the policy papers once you get it

One of the things which you should immediately do after receiving the policy is to check all the fine points and a copy of your medical examination. Nowadays, the policy papers have your medical records.

Kindly go through each point and make sure things like your age, name, blood group, address and other important things are mentioned correctly.

There have been cases, where the information has been wrong. If things are wrong, you can reach out to their company customer care to get it corrected.

18. Don’t fall for “10 times of Income” marketing

Almost all the call center marketing people try to sell you the cover equal to 10 times your yearly income. This often is a very simplified way of finding your life insurance coverage.

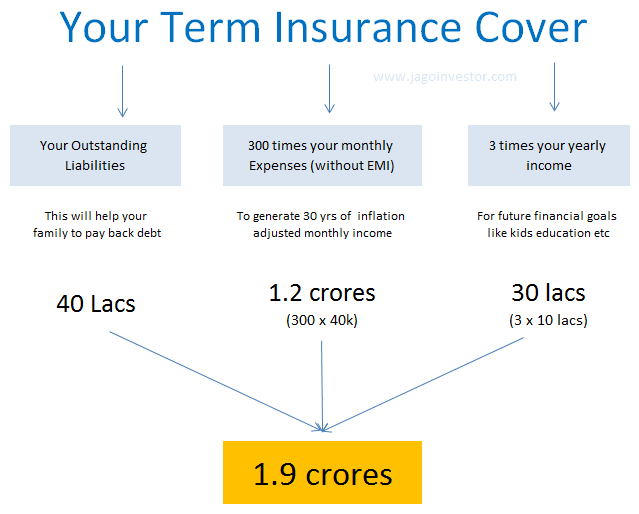

A better way to find out your coverage is to find out 300 times your monthly expenses and add up your outstanding liabilities to it. In the end, you can include 30-40 lacs more into the final number to take care of your other financial goals in future like kid’s education, etc.

For example, a guy with monthly expenses of Rs 50,000 per month and with 60 lacs of the outstanding loan will need 300 x 50,000 + 60 lacs = 2.1 crores at the minimum. So he can take a 2.5 crore term plan for himself.

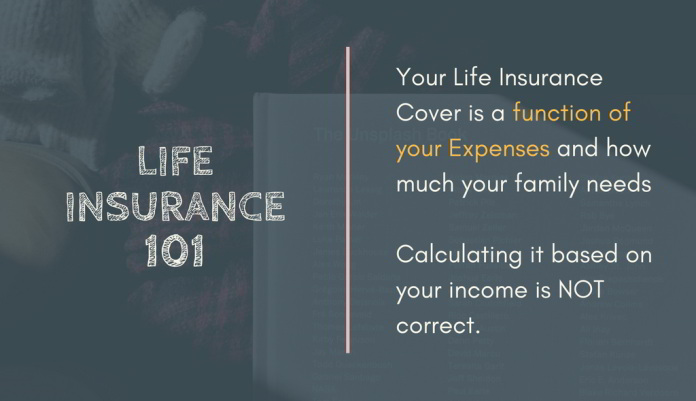

However much life insurance you should take is a function of your expenses and liabilities and not your income. What if a person earns 6 lacs a month, but a modest Rs 50,000 month expenses with no liability?’

The “10 times of your income” marketing will say that he should buy a 6 crore term plan, whereas his right number would be in the range of 1.5 to 2 crore only.

19. Choose a strong and good brand while choosing Insurer

There are 24 life insurance companies in India (the year 2017) right now. Do you think each of them are equal in terms of surviving, claim settlement experience (not ratio), dealing with clients, depth of medical examinations, integrity in conducting business and what not?

Here are the list of all the life insurance companies in India as of 2017.

AEGON Life Insurance

Aviva Life Insurance

Bajaj Allianz Life Insurance

Bharti AXA Life Insurance

Birla Sun Life Insurance

Canara HSBC OBC Life Insurance

DHFL Pramerica Life Insurance

Edelweiss Tokio Life Insurance

Exide Life Insurance

Future Generali India Life Insurance

HDFC Standard Life Insurance

ICICI Prudential Life Insurance

IDBI Federal Life Insurance

IndiaFirst Life Insurance Company Ltd – India First

Kotak Life Insurance

Life Insurance Corporation of India (LIC)

Max Newyork Life Insurance

PNB MetLife Insurance

Reliance Life Insurance

Sahara Life Insurance

SBI Life Insurance

Shriram Life Insurance

Star Union Dai-ichi Life Insurance

Tata AIA Life Insurance

When you choose a life insurance company, you should make sure you choose the one which has a strong presence, along with a good brand (not the biggest). Read reviews online and check their data and read about them.

20. Communicate to your family that you bought a term plan

You should share about buying the term plan with your family immediately along with the policy papers and the contact number of the insurer.

You can also write down the claim process on paper and keep that at a safe location and share it with family. I know it’s not an easy conversation to do even though it’s a logical thing to do. But at least communicate with your family about the important things they should be aware about.

20 things to know before buying a term plan

Steps to follow while buying the term insurance plan online

Understand your requirement first, find out how much insurance cover you are looking for

Go to various term insurance premium calculators on the web, and see what is the premium amount

If the premium is within your budget, then apply for the term plan

Make the initial premium payment and start the documentation

Medicals will be arranged for you by the term plan company which you should complete on time

Once everything is fine, your policy will be issued.

Do you have any life insurance? And are you really very sure that it will protect your family?

Majority of people who buy life insurance in India, buy it for the sole reason of protecting their family’s future. But is taking the life insurance a sure shot way to protect your family (I mean your immediate family here, which is spouse + kids)?.

If the primary breadwinner dies because of any reason, the family will have to suffer in absence of a regular income. The spouse will suddenly not get any income and might have to start earning. Your family and kid’s future is also at risk.

Let’s see some risk your family has

What if you are businessmen and you owe money to someone? After you are dead, the creditors will approach the court and they will get the money out of your life insurance proceeds

Consider you have a big home loan which you have not accounted for while taking a term plan. If you die, the first right will be of the home loan lender because the loan is on your name. The right of the family comes only when your loans are paid off.

What if you have not created your will and there are family members who claim their right in your life insurance proceeds?

What if you yourself change your mind later and don’t want to give the insurance proceeds to your own family?

Are you prepared for this situation? If not then think about it. There is a way which will help you at some points if this such situations appears in-front of your family in your absence and the solution is MWP Act.

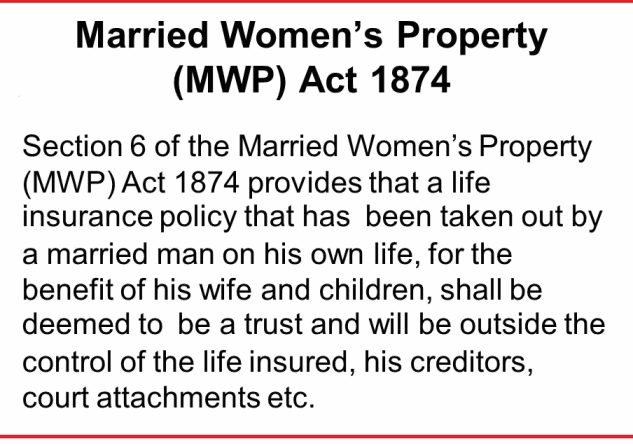

MWP means Married Women’s Property Act. This act is prepared by taking into consideration the rights of a married woman on her property. According to MWP Act . the earning of a married woman in India is considered as her own property and this Act Protects the property owned by a woman from Creditors, relatives and even from their husbands.

Buying Life Insurance Policy under MWP Act

MWP Act 1874 under which Section 6 deals with life insurance. If you buy a life insurance under MWP Act, then it will protect the women’s right on the life insurance proceeds money in all the cases. Even the husband can’t do anything about it once the buying is bought under MWP act. This applies to all kind of insurance policies be it a term plan or an endowment/money back plan.

Who can be the Beneficiary and Trustee?

When a policy is bought under MWP Act, the policy is treated as a TRUST and its guarantees that the proceeds from life insurance policy are free from any creditors or court attachments.

The first right is of the family only (women and kids). Imagine if you buy an endowment plan which matures in 20 years and you bought it under MWP Act. Once the policy matures, then even the person who started it will not be able to claim anything. The first right will be of the beneficiaries mentioned in the policy.

Beneficiaries can be:

The wife alone

The child/ children alone (both natural and adopted)

Wife and children together or any of them

Trustee can be:

Unlike beneficiaries, having trustee is not mandatory for this MWP Act. The policy holder can mention one or more trusties. Having a Trustee is not compulsory but if the beneficiary is minor then in that case it is compulsory to have a Trustee. The Trustee should not be minor. The Trustee can be change whenever the policy holder wanted. The Trusties can be –

A person

A bank

An institute

Beneficiary herself/himself

How will the beneficiaries get benefit ?

When something wrong happens with the policy holder and the insurance is claimed by the family, the creditors can claim for the insurance benefits. In this case the family members will get less benefit of the policy. Or sometimes the other family members can also claim for the part in that policy if the policy holder does not have will.

But if the policy is covered under MWP Act then the whole benefit will go to the wife or kids (whoever the beneficiary is) of the policy holder.

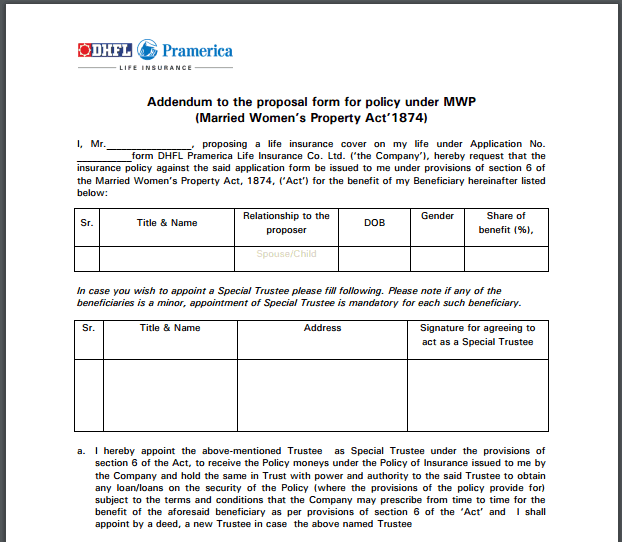

Procedure to buy life insurance under MWP Act

The process is very simple. All you have to do is fill up a MWP addendum form separately at the time of buying the policy. Your agent can help you with that form or talk to the company in case you are directly buying it from the insurer.

However note that it can’t be added separately once you have completed the process of buying the life insurance (means you can’t add the MWP act later)

Who can take a Life insurance policy under MWP act ?

Any married man can take a life insurance policy under MWP Act. This includes divorced persons and widowers. The policy can be taken only on one’s own name, i.e., the life assured has to be the proposer himself. Any type of plan can be endorsed to be covered under MWP Act.

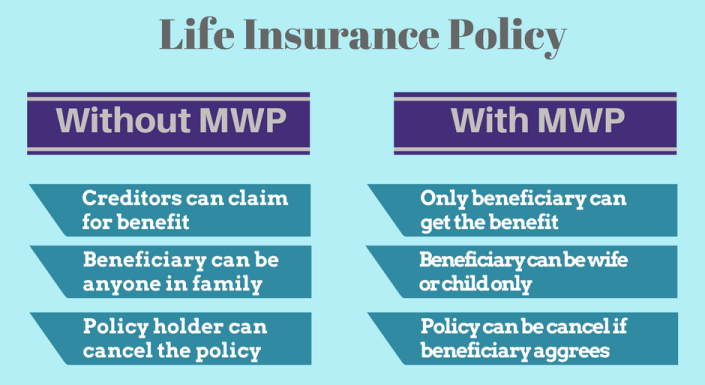

Difference – Insurance With MWP and Without MWP

There is not a lot of difference in taking a life insurance under MWP Act or without MWP Act but we can see some points which shows the difference. See the following picture.

Are there any disadvantages of buying policy under MWP Act?

Yes, There are disadvantages to signing the MWP addendum as well

The Beneficiaries cannot be changed. In case at some point you decide to change the beneficiaries . It won’t be possible if you sign a MWP addendum.

Loan cannot be taken on the basis of the policy. The policy could not be used as a security against loan.

That makes it also necessary for loan providers on Life Insurance policies to check before taking it as a mortgage for lending whether the policy does not contain any MWP addendum, as they will not get the benefits from its proceeds.

Starting 1st Oct 2016, all the insurance policies are going to be issued in electronic form.

Yes, you heard it right

Few years back IRDA had come up with the concept of 13 digit e-Insurance Account (EIA), where an investor had the option to convert their existing physical policies into demat form, but till now it was not mandatory. However now things have changed and starting 1st Oct,2016 it has become compulsory.

Now, every insurance company has to issue all kinds of insurance policies in an online format. So if you are buying any kind of insurance policies (life, health, motor, pension policies and all kind of general insurance policies too) you need to have an e-Insurance Account (EIA) and the policies will be issued in Demat form only in that account.

This will be true even for renewal policies. So even if you are not buying any fresh new policy, at the time of your policy renewal this will apply to you

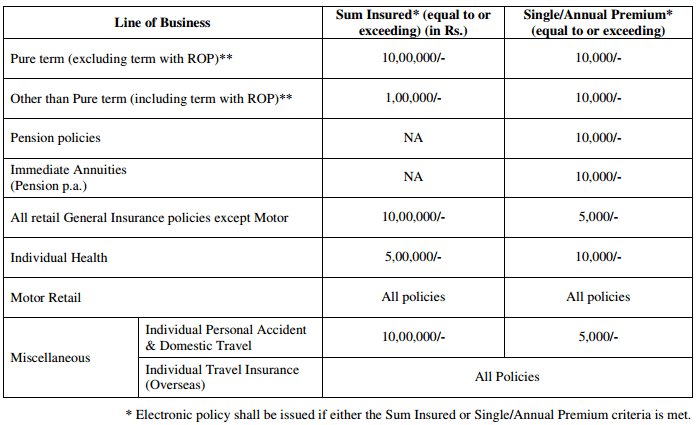

Under which cases, is this e-insurance account mandatory?

This e-account is required only if the annual premium crosses Rs 10,000 for most of the policies like term plan and health insurance or if the sum assured is above 5-10 lacs. The exact requirement is as follows for various kind of policies (source link)

How to open E-Insurance Account?

Step 1: Choose the Insurance Repository

There are 5 registered insurance repositories in the country, licensed by IRDA, out of which you need to choose one. These are …

CAMS Repository Services

SHCIL Projects Limited

Central Insurance Repository

Karvy Insurance Repository

NSDL Database Management

Note that you can choose any one of them, and there won’t be any difference, other than level of service. At the backend, everything will be the same. Also if you are not satisfied with your insurance repository provider service, you can switch to another one later.

Step 2: Fill up the form and submit the documents

The process now is very simple, once you have decided the repository company, all you need to do is fill-up the form and attach your KYC documents and submit it to their office in your city.

CAMSrepository also has an option where you can first fill-up the form online and then download the filled form. I think it will work for most people and save time. If you want to fill the form offline, you can download e-insurance account opening form here

Following are the documents you need to submit

e-Insurance Account form (fill by hand OR filled online one)

Date of Birth Proof (PAN , Passport, Voter Id etc)

Photocopy of ID proof (PAN or Aadhaar Card)

Photocopy of Address proof (Aadhaar, Passport, Electricity or Telephone Bill etc)

Canceled cheque

Passport size photograph

Note that the canceled cheque is required so that the information of the bank account is captured beforehand, Any maturity proceeds or claim amount will be paid in this same account. Ideally, this should be the same one from where the insurance premium is paid, but not mandatory.

All the major insurance companies like LIC, ICICI, HDFC, and others have already joined hands with this facility.

Check out this short video created by CAMS team

Once you submit the documents, it will just take a few days to open the account.

If you need the detailed list of the documents required, you can view this PDF document (2nd page)

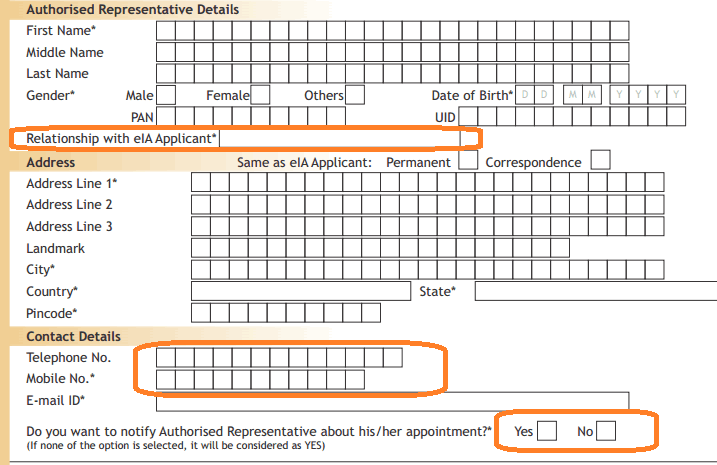

The concept of Authorized Representative

A special feature called “Authorized Representative” is introduced in this e-insurance account where an investor can assign someone trustworthy or close to being AI (authorized representative) who will be able to access the details of the account in case of death of the policyholder. This is different than the nominee.

For example, I can give my close friend name and details in the AI section ask him to have a look at all my details in case I am dead and ask him to communicate things to my family as per my plan.

Features and Benefits of e-Insurance Account (EIA)

Let me know to share some benefits and key points of this e-insurance account and how it will benefit the overall insurance industry as well as the investor, even though it may look like another hassle to you right now

FREE account – This account will be 100% FREE account for investors, there are no charges or maintenance fees to be paid by anyone. One person will have only a single account (like PAN)

All policies at one place – This will be the single point of contact for investors to view, download and manage their insurance policies, be it life, health, motor or any travel insurance policy.

No KYC repetition while buying new policies – After doing the KYC first time, you won’t have to do it again and again when you buy new policies. All you would need to do is mention your EIA number and buy the policy.

Get reminders – You will get reminders for your policy maturity, payment reminders and any other important updates.

Single place to update your KYC – IF you want to update your mobile, address or other details, you will just have to update it in e-insurance account and not in each policy individually.

Understand that with this initiative, the insurance companies will simplify their process and a good amount will be saved as there won’t be a lot of paperwork involved (printing of documents, courier etc) and that’s why insurance companies will fund this initiative and will keep it FREE for investors.

Converting your existing physical Policy in Electronic form

I know you must be thinking about what will happen to my existing policies which I have bought till date? So, there is a simple process to convert them online.

Once you open the e-insurance account, you can apply for conversion of your existing policies into the online form (its good that you do it beforehand, because at the time of renewal it’s going to happen anyways going forward)

As per Cam’s repository FAQ point 18, you can just mention your policy number and it will be converted into an online format

18. How do I convert my existing paper policy into electronic form?

If you already have eInsurance account, log in to your eInsurance account, click on “ePolicy conversion” and enter your policy number, name of Insurance company that needs to be converted into ePolicy. In the next few days, your policy will be converted into ePolicy.

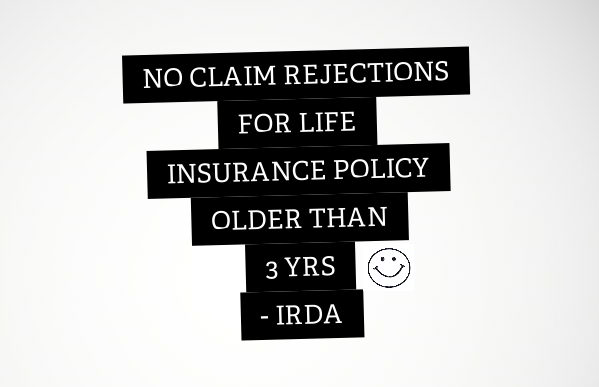

There is very good news for those who have bought life insurance policies (especially term plans). From now on, life insurance companies will not be able to reject claims for any policy which is 3 yrs old.

Yes, you read it correctly.

No Claim rejection after 3 yrs

If your policy is 3 yrs old, no matter what happens, the life insurance company will not be able to deny the claims. There was an amendment in the sec 45 of the Insurance Act 1938, and due to that now onwards a policy can’t be denied a claim because the policy-holder gave some wrong information.

As per IRDA, the company has 3 yrs in hand to detect any misrepresentation or misstatement from the customer side and reject the policy. However, once this period is over, the insurer will have to settle the claims.

What this means is that those investors who were highly suspicious of insurer’s intention and always kept looking at the claim settlement ratio numbers don’t need to worry now.

While this seems to be great news, one should think of what kind of implications will arise out of this change. I can think of a few of them

1. It will not be easy to buy life insurance

The major impact of this change will be that now the medical tests might get more details checking a lot of things. Till now insurers were bearing all the costs, and I think it will happen in future also, however, I think this will result in higher premium amount, which I think investors will not mind because now there is a guarantee of claim settlement

2. Chances of Fraud in the life insurance space

Already, there are many frauds that happen in life insurance space from the customer’s side. I remember an episode of Crime Petrol, where a man planned his death so that his family can get the life insurance money, however, he didn’t get the money because he was not able to execute the plan.

However, with this new change – the chances of fraud and misrepresentation can increase. Imagine a smoker or a person involved in risky activities. A lot of people like these to not disclose these facts because their application might get rejected or the premium might rise. So a lot of people suppress disclosing this fact and it’s going to be a hard time for companies to figure out these things. There will always be few cases which will not come under their radar.

What do you think about this latest development? If you hold a life insurance policy already, how do you see this new change?

A lot of you on Jagoinvestor must have bought term plan or other insurance plans, so that in your absence your dependents do not face any kind of financial crunch. It is good to buy life cover, but may be buying life cover is just half job done.

From last few days, I have been carrying a few thoughts in my mind which today, I would like to share with all of you. Whenever I look at the face of my little one, I feel I should do something special for him along with buying life cover for securing his future.

If something happens to me, my son will get enough financial support from the insurance money, but I will lose out on the opportunity to share my wisdom (my life learning’s) with him. There are a few things, which I would like my son to learn or know from me and my life experiences.

I feel that Life insurance policy is very strong support a parent can give their kids, but it lacks emotions, feelings and love in it. To add my feelings and emotions in it – I have started capturing a few of my experiences in a short journal which I call “Notes from Daddy”.

3 things which I captured in my “Notes from Daddy” Journal

1. List of Books that had deep impact on my life

Since my college days, I have been a voracious reader and there have been many life changing books that had deep impact on my life and it has major contribution on my overall learning and development process. I would like to share my reading list with my son when he grows up.

Now, it is possible that he may or may not choose to read books from my reading list but at least I would like to share or communicate my reading experiences and my book list with him. I have started building my reading list which I would like to share with my son. My “Notes from Daddy” journal has a section called “Hidden Treasure- Personal Reading list”.

2. List of Movies that inspired me

There have been many movies and short documentaries which changed my complete outlook towards life. I am sure you also must have encountered and seen such inspiring movies. I have a section called “Movies that will move YOU” in my “Notes from daddy” journal. If you want you can also make list of inspiring movies which you want your son or daughter to watch in their growing years.

3. Teachers who changed my WORLD

It is said that – “when the student is ready, teacher appears”.

I have been fortunate to have right mentors and teachers at different junctions of my life. I am sure my son and your kids will also have many teachers in their life. Sharing from my life my teachers taught me some very important distinctions of life which helped me to look at the world with new pair of eyes.

I am sure you also must have had some “wow learning moments” while you were with your teacher. Why not capture them at one place so that it gets communicated to your next generation in your absence.

Some final words

Our body is a place to observe the world from, it is a physical representation of you, be clear that your body is not you. Life is beautiful and at the same time highly unpredictable and uncertain. Having life cover is important but I feel it is still half job done. In my absence, I would not just like to pass on insurance amount to my son, I would also like to pass on my wisdom and selective life experiences to him as well.

If you already have life cover and would like to create your little “experience journal” you can start working on it. If you do not have adequate life cover leave your details here and we will guide with the buying process. In the comments section do share some more ideas that you can implement to do something special for kids along with buying insurance.

Lastly, we are all set to announce about our next workshop which will be held in Bangalore. It will be conducted in the month of July and the registrations will open soon.

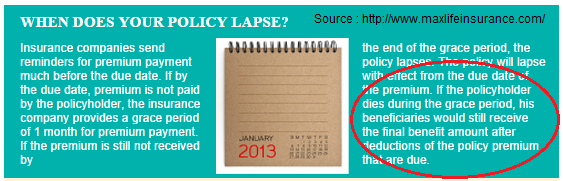

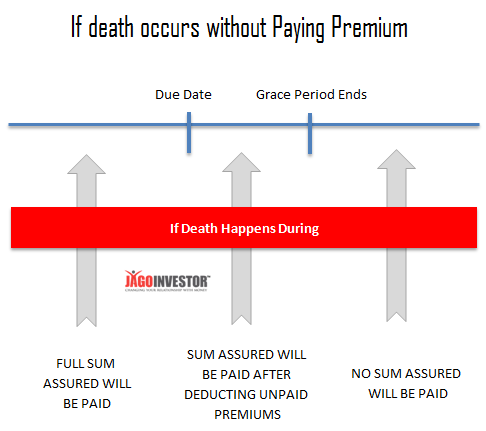

Do you know what happens when the policyholder dies within the grace period provided after the due date of paying the premium. The answer might surprise you because there is a big myth around this topic.

Every life insurance company provide a grace period of 30 days for paying the premium after the due date is over. Companies send reminders on SMS and emails to make sure the customer pays their premiums on or before the due date. But if they forget to pay the premiums on time, still they get 30 days of grace period.

If premium are not yet paid after the grace period, then the policy is considered to be LAPSED and no death benefits will be given if the death happens after the grace period.

Do you get sum assured if death happens during grace period ?

And the answer is YES. As per the rules, if the death of the policy holder occurs on the due date of the premium payment or during the grace period, still the policy is valid and the beneficiaries will get the sum assured. But after deducting the the unpaid premium for the current year.

As a proof I am putting up a proof of what the website of Max New York Life Insurance says below. You can see the exact wordings below.

So if a person has taken a 1 crore term plan for a 30 yrs period with premium Rs 10,000 per year on 20th dec 2010 and imagine the policy has run for 3 yrs , and now its the 4th premium is to be paid on 20th dec 2014 . The grace period will be upto 20th Jan 2015 .

Now if the premium was not paid and the death happens on 25th Dec 2014 , then its during the grace period. How much will be the sum assured paid to the customer family ?

It would be Sum Assured – all unpaid premiums for the current year

= 1 crore – 10,090

= 99.9 Lacs

There have been a lot of cases, where a person just discontinued his policy for some reason and they faced an accident and died. Internet is full of these kind of cases.

A lot of times death happens during the grace period and because the family is not well educated on this aspect, they don’t know that they are still liable for a claim (we provide our clients family claim assistance service).

Conclusion

So make sure you do not forget to pay your premiums and make sure you do not wait for the reminders from the insurance company. You can set up your own reminders and be more alert and proactive on this.

Let us know if you knew about this information or not ?