Do you think its a bad mutual fund, because it is not doing well from last many years?

A lot of mutual funds investors lose their patience looking at their mutual fund’s returns after they invest for 2-3 yrs. Its commonly suggested that an equity mutual fund will perform very good over the long term and one can expect double-digit returns, however, if the fund does not return back good returns within 2-3 yrs itself, the investors get very nervous and start judging their mutual fund quality and wonder if they made a right choice or not!

Today I will tell you how to judge the returns of mutual funds using “Rolling Returns” analysis, which will help you to get more confidence in your mutual fund and will help you learn many aspects!

Let’s start!

You Returns will invest a lot depending on when you invested!

Before we go into rolling returns, let’s understand the issue!

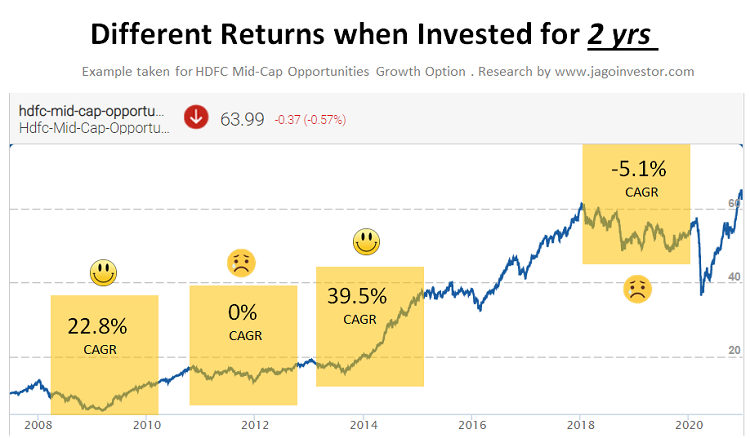

Take HDFC Midcap opportunities growth for example

10 yrs CAGR return: 14.96%

5 yrs CAGR return: 11.26%

At the time of writing this article, the returns from this fund are very good. But can this fund give bad returns in a 2 yr period. The truth is that this same “good fund” can give very different kind of returns in a 2/3 yr period depending on when you bought the fund.

Here is some data.

You can see that the 2 yrs return can be 22.8%, 0%, 39.5% or -5.1% depending on when a person entered the fund. So a lot depends on when you entered in the fund.

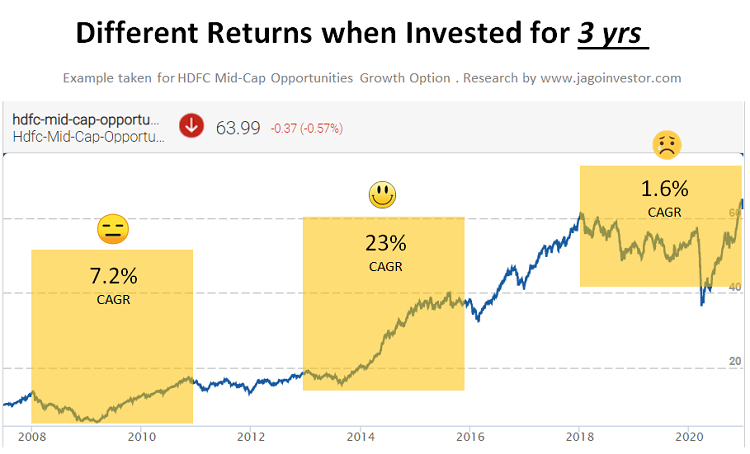

Now let’s see the same thing for 3 yr time frame.

Again, you can see that for a 3 yr period – the experience can be very very different. It’s not always possible to enter at the lowest point and many times, investors invest their money for the long term when the near term returns are going to be bad. However, they never get prepared for this.

Investor mind is also not designed to stay calm when returns go in negative and that’s when investors make a wrong choice of exiting the funds even if at the fundamental level, the fund has no issues and its just the volatility of the equity which is driving the fund into negative return zone!

You can see that this approach of just looking at the point to point return does not give you enough detailed information about the fund and its volatility.

Rolling Returns – What it is and How to look at it!

Rolling return means a series of returns data for each and everyday investment for a certain time frame.

So in our example of HDFC Midcap opportunities, lets assume a period of 14 yrs from 1st Jan 2007 to 30th Dec 2020. Thats approx 5110 days. If you do a 2 yr rolling return analysis, it means that a period if investing for 2 yrs and you are plotting the CAGR return for each day of investment from the start. (that’s 730 days of investment)

So you invest on

1st Jan 2020 and exit on 1st Jan 2022 (1st instance)

2nd Jan 2020 and exit on 2nd Jan 2022 (2nd Instance)

3rd Jan 2020 and exit on 3rd Jan 2022 (3rd Instance)

….

….

….

30th Dec 2018 and exit on 30th Dec 2020 (4380 instances: 5110 – 730)

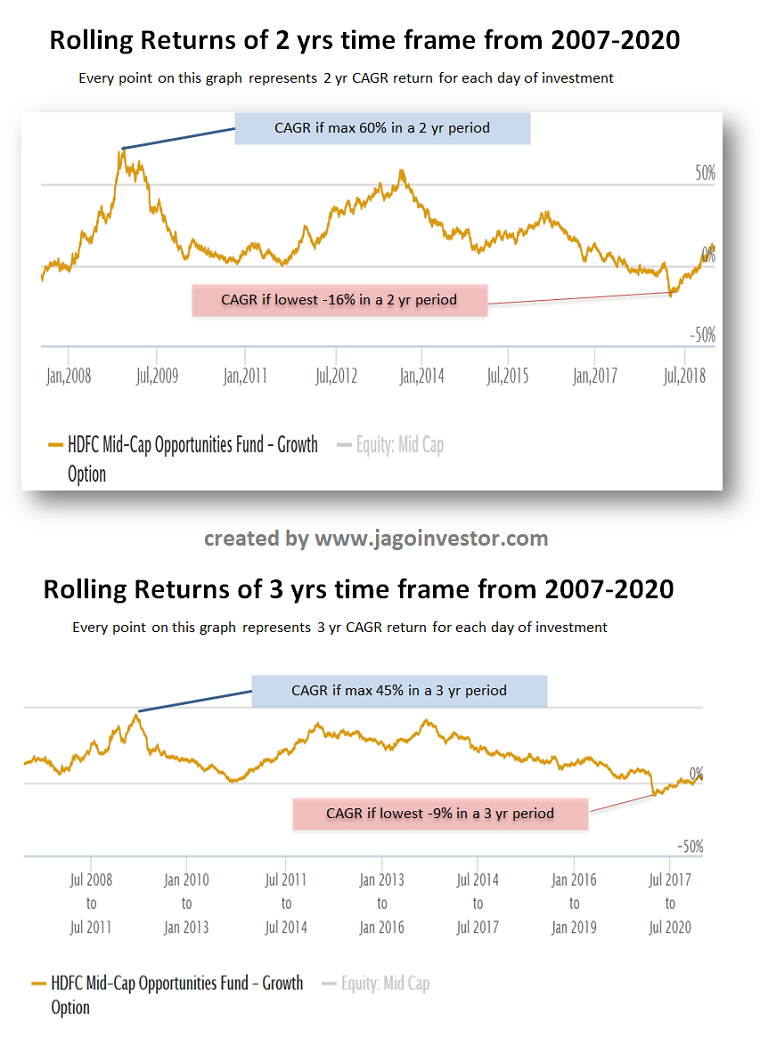

So you can plot these 4380 data points and that graph is called a rolling returns graph. In the same way, you can have a 3 yr, 5 yr or even 10 yr rolling return graph.

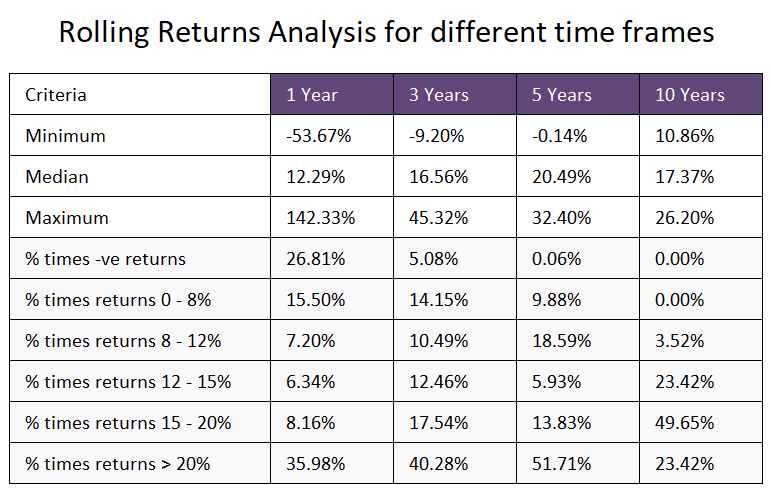

Check out the example of HDFC Midcap opportunities rolling return chart for 2 and 3 yrs period for last 14 yrs. You can see that in a 2 yr period, the highest CAGR has been around 60% and the lowest at -16% .. So it’s possible to see your investment go down by 16% in a 2yr period as per old data. The same kind of data is there for 3 yrs period too!

Rolling return graph will give you a deeper understanding of how volatile fund returns have been and even the probability of your return being in a certain range (only with past data). Note that its only historical data and the maximum and minimum returns can change depending on future performance.

If you look at the chart above, you can conclude that if you want to invest in this fund – then you can see a downside of up to 10% in a 3 yr period because it has happened in the past. Also, you can see flat returns even in 5 yrs period which has happened in the past.

This kind of analysis tells you that because of volatility even this kind of good funds can see a period of non-performance and flat returns.

I hope I was able to explain what is rolling return in a simple manner.

Conclusion

Remember that rolling returns exercise is a great tool for analyzing the mutual fund, but it’s not the final exercise in itself. There are many other kinds of analysis which is possible and this exercise alone does not give any final judgement.

If you are not happy with your fund performance, then I suggest going through this exercise!

Congrats! – Health Insurance just got a lot better

IRDA has recently come up with some major changes in health insurance guidelines which are extremely customer friendly. These changes will reduce a lot of confusion that customers used to face while buying health insurance and will also help in smooth claim experience.

These changes are really good and it’s suggested that you should be aware of all the changes if you have a health insurance policy. It will take some time to understand these changes, but please read this article fully.

In case you like to listen, rather than read – here is a 35 min video discussion I did with Mahavir Chopra of Beshak.org who is an expert on this subject and a good friend too. While there are many big and small changes in the guidelines, the video talks about the top 10 changes which matters to you.

Change #1 – Standard definition of 18 exclusion

There are various exclusions in a health insurance policy and wordings for them differ from policy to policy. This confuses the policyholders while their decision-making process. Now IRDA has standardized the definitions and wordings for all kind of exclusions

One of the examples of this is the wordings for a pre-existing illness, 30 day waiting period, maternity, obesity, and many more. In various policies, the definition is different for these terms and it leaves a grey area many times.

Now with the new rule, every policy will have the same wordings and definition of the exclusions along with a CODE for each exclusion.

Change #2 – No ambiguous wordings or definitions

Apart from this, IRDA has also said that there should not be any ambiguity in the wordings which can create confusion in the future. For example – “Obesity is not covered, and any other illness which is derived out of obesity is also not covered”.

If you look at the example above, how will an insurer and the policy come to an agreement is something was because of obesity or not? There may be a disagreement in the future and companies can deny the claim citing some unreasonable thing.

Now, this practice ends…

Change #3 – Many Exclusions are disallowed

Now many exclusions which were part of policies earlier are disallowed, which means that companies will have to cover them. Some of the examples are as follows.

Treatment of mental illness

Behavioral and Neurodevelopmental Disorders

Genetic diseases or disorders

Puberty and Menopause Related Disorders

Injury or illness associated with hazardous activities

So the coverage of the health insurance policy widens now and you will be able to get coverage for many more things. This is wonderful news because mental illness or psychological related hospitalization will now get covered which was a big requirement.

Check out our youtube video on these 10 changes if you want to listen to the whole conversation

Check out this video

Change #4 – The definition of “Pre-existing” diseases is standardized

This is one area that was quite confusing for customers.

Till now, it was not very clear what exactly is a pre-existing illness? So the onus was completely on the customer to remember his symptoms and go back in past to dig out all that had happened. If he had forgotten anything and it came up later in the future which was not disclosed in the policy, there was a good chance of rejection of claims.

Now, the IRDA has made it clear that a pre-existing illness is an illness for which,

A doctor has advised you a treatment

Or Doctor has diagnosed a disease

Only in these two cases, it will be treated as a pre-existing illness, else not. Hence, it has now become a much-focused definition now which will remove all the confusion.

So now just because you have some mild symptoms or an indication of an illness, does not automatically become a pre-existing illness going forward.

Another example is let’s say you are obese and have had bad eating habits and you are not sure if you are diabetic or not… In this case, a lot of people wonder if the insurer can reject the claims in the future because of hospitalization due to diabetes.. but with new rules, unless it was diagnosed by the doctor officially, it will not be treated just a pre-existing illness.

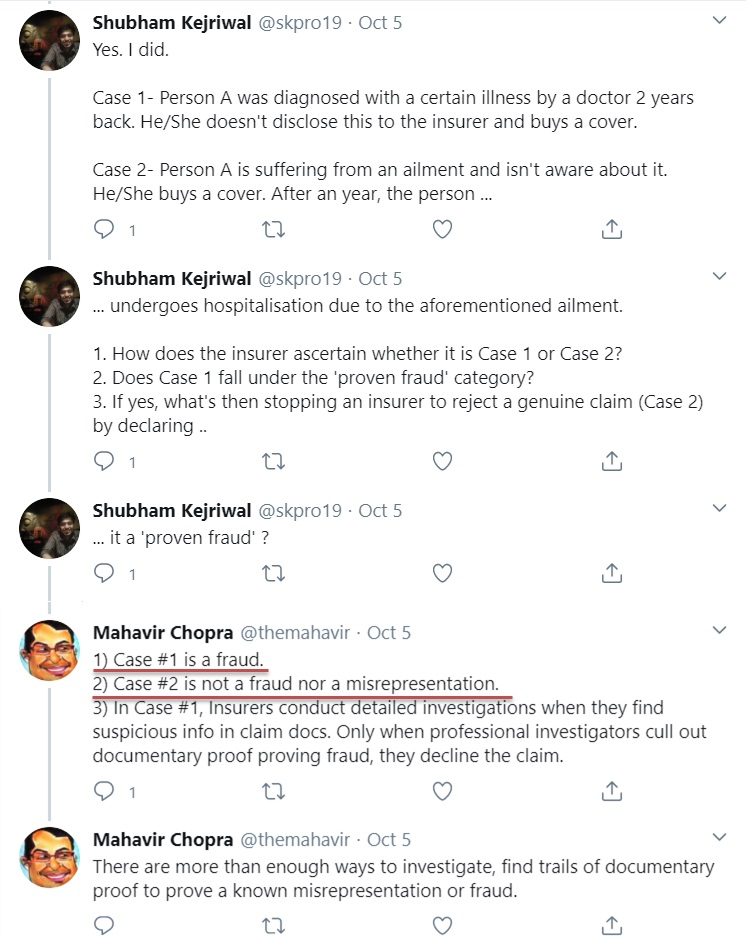

Change #5 – No claim rejection after 8 yrs. of premium payment

This is a big relief to policyholders.

Now health insurance companies will have to settle all the claims once a policy has been active for continuous 8 yrs. In case you increase your sum assured in the same policy, another 8 yrs. of moratorium period will be applicable on the increased limit. Apart from this, the permanent exclusions will always be excluded.

Only in case of a Proven fraud, the rejection can happen after 8 yrs. However, in case of a genuine claim, the policyholder doesn’t need to worry. Check out the reply by Mahavir Chopra on twitter timeline to one of the people who asked a question on what is a fraud and what is not.

Change #6 – People with serious illnesses to get cover with permanent exclusions

A lot of people who had some serious illnesses like cancer, epilepsy, Chronic Kidney disease, Alzheimer’s Disease were denied any kind of health insurance. They were not even provided cover for other things with these things put as permanent exclusions.

However, this has changed now.

IRDA has said that now people with these kinds of illnesses also have a right for getting health insurance for at least other illnesses. So health insurance companies will now have to give them health insurance for at least the other diseases with their pre-existing illnesses as permanent exclusions.

This is important because if someone had Chronic Kidney disease, they can still be hospitalized due to a completely different illness like a brain illness, mental illness, accident, or cancer .. You can’t just completely reject them and deprive them of health insurance.

This clause is not applicable to lifestyle diseases like diabetes, hypertension, etc. because insurers can’t put permanent exclusions on these things as they have almost become part of our life these days, and people like their whole life with these things. More on this in the next points.

Change #7 – Modern treatments to be covered in health insurance

Another welcoming change is that some advanced and modern treatments will now be compulsorily covered in health insurance policies. Here is a full list of modern treatments which IRDA has specified

Uterine Artery Embolization and HIFU

Balloon Sinuplast

Deep Brain stimulation

Oral chemotherapy

Immunotherapy- Monoclonal Antibody to be given as an injection

Intra vitreal injections

Robotic surgeries

Stereotactic radio surgeries

Bronchial Thermoplasty

Vaporisation of the prostrate (Green laser treatment or holmium laser treatment)

IONM – (Intra Operative Neuro Monitoring)

Stem cell therapy

A lot of times, these advanced treatments are advised by doctors but these were never covered by health insurance policies. However, with this, you get access to more advanced treatments going forward.

Change #8 – Waiting period for specified illnesses can’t be more than 4 yrs.

So earlier there was clarity on how much can be the waiting period for various illnesses like cataract, knee surgery, and many other kinds of illnesses. Most of the time it was in the range of 2-4 yrs. and some older policies may have higher than 4 yrs of waiting period.

But IRDA has now made it clear that in no case, it can be more than 4 yrs. of waiting period.

Change #9 – Waiting period for lifestyle diseases only up to 90 days

So the waiting period for lifestyle illnesses like diabetes, hypertension, and Cardiac conditions can be only up to 90 days and not beyond that. Till now the insurer used to keep waiting period for these lifestyle diseases up to 2-4 yrs. Nowadays these illnesses are very common and have become part of life in a way.

This is good from the customer’s point of view.

However, note that the waiting period of 90 days is only in case you don’t have these at the time of taking the policy. In case you already have them, then it’s classified as “pre-existing illness” in your case.

Also note that if you have recently taken a health insurance policy, then at the time of next renewal this 90 days waiting period will apply in your case and will get covered for you.

Change #10 – Pre and Post hospitalization expenses to be covered for domiciliary hospitalization

Another change is that now in case of domiciliary hospitalization (when you do the treatment at home because of unavailability of hospital beds) the pre and post-hospitalization expenses will also be covered which was not the case earlier.

When something improves by a big margin, it’s almost guaranteed that its price will also rise in the same fashion. The same is the case here. Because of all these new changes, the health insurance policies have got more superior and much better & provides more value now.

So you can surely expect that the premiums will rise in the future for these policies

If you already have the health insurance policy, you can expect the premiums to rise on your next renewal. However, you should take it positively and not feel bad about it.

These changes have happened for your benefit and it’s you who will benefit from it in the future. Health Insurance companies are also bound to incorporate these changes as an order from IRDA.

What is your view about these changes? Do you feel it will help customers?

The taxation becomes more complicated when you moved out of one country to another for earning. A lot of times, an NRI will be earning in India as well as abroad, and pay the income tax in India and abroad both at the same time, because of many country levy tax on global income. This leads to double taxation for NRI’s.

We will talk about Double Taxation Avoidance Agreement (DTAA) today and understand how NRI’s can take benefit from it while they are planning their investments

Many NRIs earn various types of income from India eg. rental income, interest on FD or NRE/NRO savings account or even capital gain on sale of asset, etc. However, due to DTAA (Double taxation avoidance act), An NRI can save himself from getting taxed twice.

What is DTAA?

DTAA is a tax treaty signed between India and various other countries because of which investors does not have to pay taxes twice in both the countries. Hence DTAA mainly have following benefits

Helps NRI’s in lowering their taxes

Helps NRI’s in avoiding paying dual taxation

Makes a country attractive for NRI’s because of such a treaty

Helps in curbing the tax evasion by NRI’s

The benefit of DTAA is extended every year to NRI. Which means that NRI’s who want to keep availing the DTAA benefits have to furnish the required documents at the start of every financial year to the tax authorities.

Here is an example

An NRI can avail tax benefits with the help of DTAA, as his earnings in India are taxed as per the rates decided in agreement. This prevents the NRI from paying 30.9% as TDS (Tax Deduction at Source), instead, he could pay tax at 10-25% rate depending upon the country he currently resides in.

Example of DTAA with USA

There is a DTAA between India and USA also, and the TDS rate is only 10%, which means that an NRI who has income in India and who falls in 30% tax bracket will only be paying a TDS of 10%, and not 30% if he does all the documentation. Note that there are different tax rates for various kinds of income like interest, dividends, royalty etc.

Following are the types of income’s which fall under DTAA

Salary that is received in India

Income from services that are provided in India

Fixed deposits & saving bank account held in India

House property situated in India

Capital gains arising out of transfer of assets in India

Below is a TDS rate list with all 89 countries (out of which some 85 are in force)

[su_table responsive=”yes”]

Sr. No

Country with whom India has TDAA treaty

TDS Rate

1

Albania

15.0%

2

Armenia

10.0%

3

Australia

10.0%

4

Austria

10.0%

5

Bangladesh

15.0%

6

Belarus

10.0%

7

Belgium

10.0%

8

Bhutan

15.0%

9

Botswana

15.0%

10

Brazil

15.0%

11

Bulgaria

10.0%

12

Canada

10.0%

13

China

10.0%

14

Columbia

10.0%

15

Croatia

10.0%

16

Cyprus

15.0%

17

Czech Republic

10.0%

18

Denmark

10.0%

19

Estonia

10.0%

20

Ethiopia

10.0%

21

Finland

10.0%

22

Fiji

10.0%

23

France

10.0%

24

Georgia

10.0%

25

Germany

10.0%

26

Hongkong

10.0%

27

Hungary

10.0%

28

Indonesia

10.0%

29

Iceland

10.0%

30

Ireland

15.0%

31

Israel

10.0%

32

Italy

10.0%

33

Japan

10.0%

34

Jordan

10.0%

35

Kazakhstan

10.0%

36

Kenya

10.0%

37

Korea

10.0%

38

Kuwait

10.0%

39

Kyrgyz Republic

10.0%

40

Latvia

10.0%

41

Lithuania

10.0%

42

Luxembourg

10.0%

43

Malaysia

15.0%

44

Malta

7.5%

45

Mongolia

10.0%

46

Mauritius

10.0%

47

Montenegro

10.0%

48

Myanmar

10.0%

49

Morocco

10.0%

50

Mozambique

10.0%

51

Macedonia

10.0%

52

Namibia

10.0%

53

Nepal

10.0%

54

Netherlands

10.0%

55

New Zealand

10.0%

56

Norway

15.0%

57

Oman

10.0%

58

Philippines

10.0%

59

Poland

10.0%

60

Portuguese Republic

10.0%

61

Qatar

10.0%

62

Romania

10.0%

63

Russian Federation

10.0%

64

Saudi Arabia

15.0%

65

Serbia

10.0%

66

Singapore

10.0%

67

Slovenia

15.0%

68

South Africa

10.0%

69

Spain

10.0%

70

Sri Lanka

10.0%

71

Sudan

10.0%

72

Sweden

10.0%

73

Swiss

10.0%

74

Syrian Arab Republic

10.0%

75

Tajikistan

10.0%

76

Tanzania

10.0%

77

Thailand

15.0%

78

Trinidad and Tobago

10.0%

79

Turkey

10.0%

80

Turkmenistan

12.5%

81

Uganda

10.0%

82

Ukraine

15.0%

83

United Mexican States

15.0%

84

United Kingdom

10.0%

85

United States (USA)

10.0%

86

Uruguay

10.0%

87

Uzbekistan

10.0%

88

Vietnam

10.0%

89

Zambia

10.0%

[/su_table]

What sections under IT Act provide relief from paying double tax?

Section 90, Section 90A and Section 91 of the Income Tax Act, 1961, provides for DTAA relief.

Section 90 – Reads as “Agreement with foreign countries or specified territories”. It applies to the cases where India has a bilateral agreement with another nation like Canada, UK, Singapore, etc.

Section 90A – When a specified association in India enters into an agreement with a specified association abroad, the Central Government, may by notification adopt such agreement and provide relief under section 90A of the Income Tax Act, 1961.

Section 91 – Applies to cases where India does not have any bilateral agreement, rather it has unilateral agreement. It states how tax relief can be availed in case of “Countries with which no agreement exists.”

How to claim DTAA benefits?

To benefits from the provisions laid under DTAA, an NRI individual will have to provide the following documents in a timely fashion to the concerned deductor eg. bank in case of tax on interest income earned.

Self-declaration cum indemnity format

Self-attested PAN card copy

Self-attested visa and passport copy

PIO proof copy (if applicable)

Tax Residency Certificate (TRC)

According to the Finance Act 2013, an individual will not be entitled to claim any benefit of relief under the Double Taxation Avoidance Agreement unless he or she provides a Tax Residency Certificate to the deductor.

To receive a Tax Residency Certificate, an application has to be made in Form 10FA (Application for Certificate of residence for the purposes of an agreement under section 90 and 90A of the Income-tax Act, 1961) to the income tax authorities of country of residence. Once the application is successfully processed, the certificate will be issued in Form 10FB.

DTAA methods

There are two ways NRI’s can claim the DTAA benefits, and let’s discuss it here

Tax Credit Method

This is the most popular method of taking DTAA benefits. Under tax credit method, the person first has to take into consideration all his income into consideration (foreign country + home country income) and calculate the taxes applicable. Then they will calculate the taxes as per home country and take that much credit while paying for taxes.

For example, if someone has a bank interest in India for 20 lacs and the tax rates applicable to them is 30%, and if in the foreign country they live right now taxes is at 40%, then the person will be able to take back the credit of 30% and only pay additional 10% taxes. This method makes sure that there are almost no way a person pays dual taxes.

Exemption Method

This is another way, in which you don’t have to consider your home country income at all and just have to pay the taxes on the income which you have earned in the foreign country. So it does not matter what are the tax rates in different countries. As per the DTAA treaty, you just skip the home country income altogether, so you just end up paying taxes in home country only.

Take Professional Help with it comes to DTAA

Once you have become an NRI, and you have multiple income sources in different countries and when you also have spent different times in India and abroad, it becomes quite complicated to take benefit of DTAA rules. You also have a chance of making a mistake and pay less tax (or to pay more) if you try to do it yourself.

Hence I strongly suggest that you hire a professional CA who has expertise in DTAA matters and pay the fees to them to do the calculations and tax filing.

I hope this article was able to help you understand various rules related to DTAA.

NPS is one of the most famous and talked about financial products today in our country and it’s quite a detailed and complex product. Today we are doing to talk about NPS in detail and I will try to teach you various aspects related to it.

National Pension Scheme is initiated by the government of India to make sure that in the coming future, more and more people have pensions to support their old age. The core focus of this scheme is to help investors save money for their retirement and also provide a regular income once they retire.

Since NPS was launched a few years back, there have been a number of changes and revisions to this scheme. So, this article will be the guide to NPS and answer to all your queries and confusions.

What is NPS?

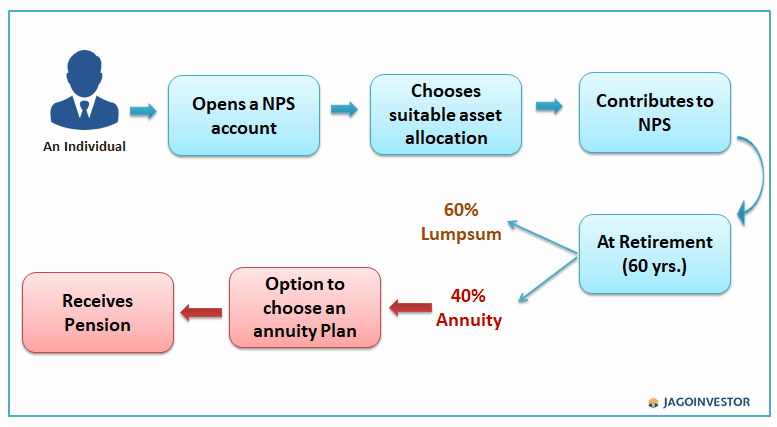

NPS is referred to as National Pension Scheme or New Pension Scheme. In this scheme, a subscriber can contribute to a pension fund that will be a mix of equity and debt investment. You have to invest in NPS till your retirement and the final corpus will depend on how the pension fund has performed over the years.

At retirement, you can withdraw part of the corpus as a lump sum and the balance will be used to provide you a regular pension till your death (and many other options are there).

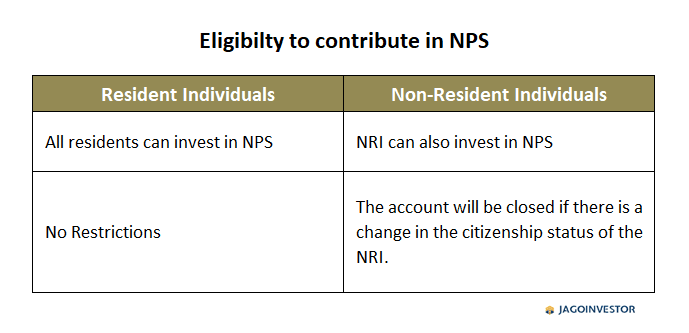

Who can invest in NPS?

Earlier only government employees were allowed to invest in NPS, but now anyone (including NRIs) can open the NPS account. The below chart will simplify it.

Important Point: Entry age for NPS is above 18 years and below 65 years.

Who regulates NPS and manages money invested?

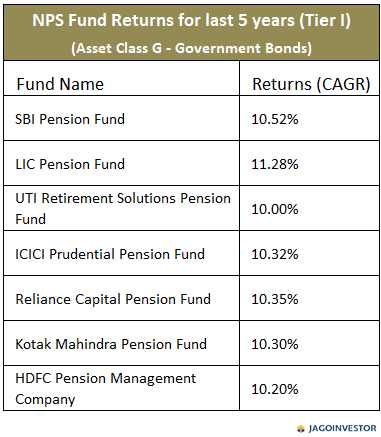

NPS is regulated by PFRDA – Pension Fund Regulatory & Development Authority. The money invested in NPS is managed by Pension Fund Managers (PFM). These are companies that are authorized and appointment by PFRDA to manage the wealth of investors. There are eight PFM right now.

ICICI Prudential Pension Fund

LIC Pension Fund

Kotak Mahindra Pension Fund

Reliance Capital Pension Fund

SBI Pension Fund

UTI Retirement Solutions Pension Fund

HDFC Pension Management Company

Birla Pension Fund

How can you invest in NPS?

The first step is to open an NPS account which can either be Physical or Online. First, let’s see the physical mode of the opening NPS account.

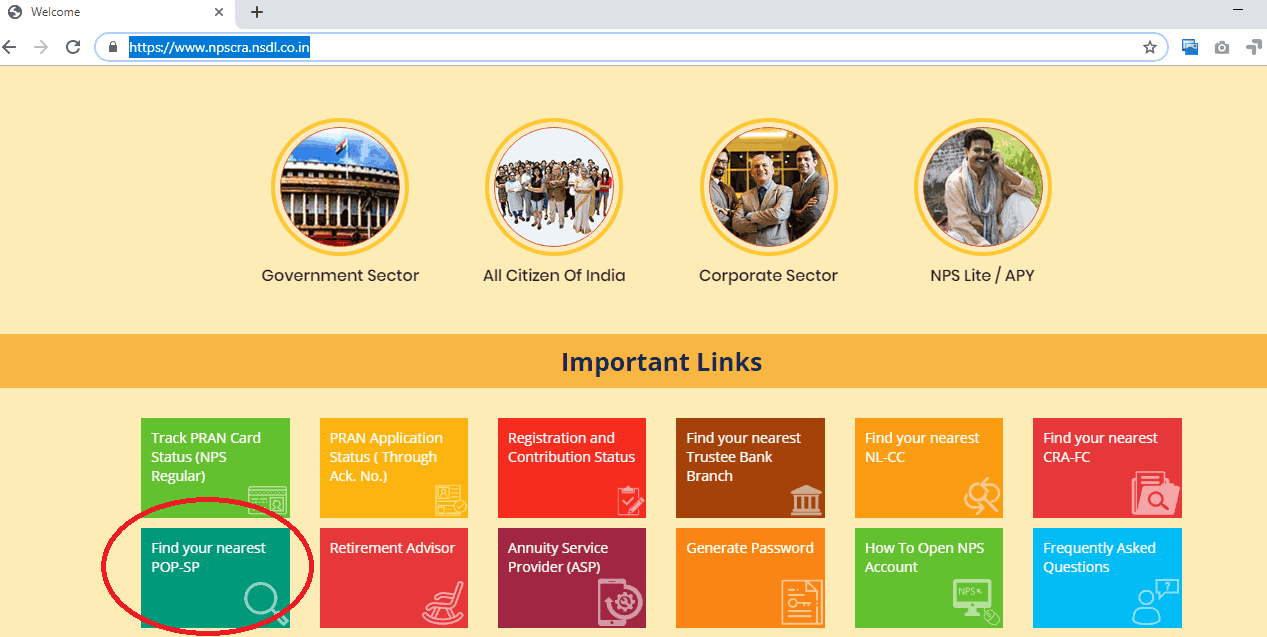

1. Physical Mode – For this, you have to open an NPS account with POP – Point of Presence service providers. POPs are the banks or post office or other non-financial institutions. You can find your POP through this link https://www.npscra.nsdl.co.in

There you need to enter your country and location and you will get the list of POP-SPs near you. Select the Point of Presence (POP) where you have an existing relationship – either a savings / current account (in case of Bank) or any other account such as Demat/Mutual Fund/Insurance etc. (in case of non-Bank POPs).

Once you have searched your POP, you need to submit KYC forms along with the NPS registration form to POP and after registration, you with getting a PRAN i.e. Permanent Retirement Account Number. This is a 12 digit unique and portable number issued to all the subscribers.

Important Point: For Government employees, there are NODAL offices where they can get PRAN for the NPS account. Mostly they get it at the time of joining.

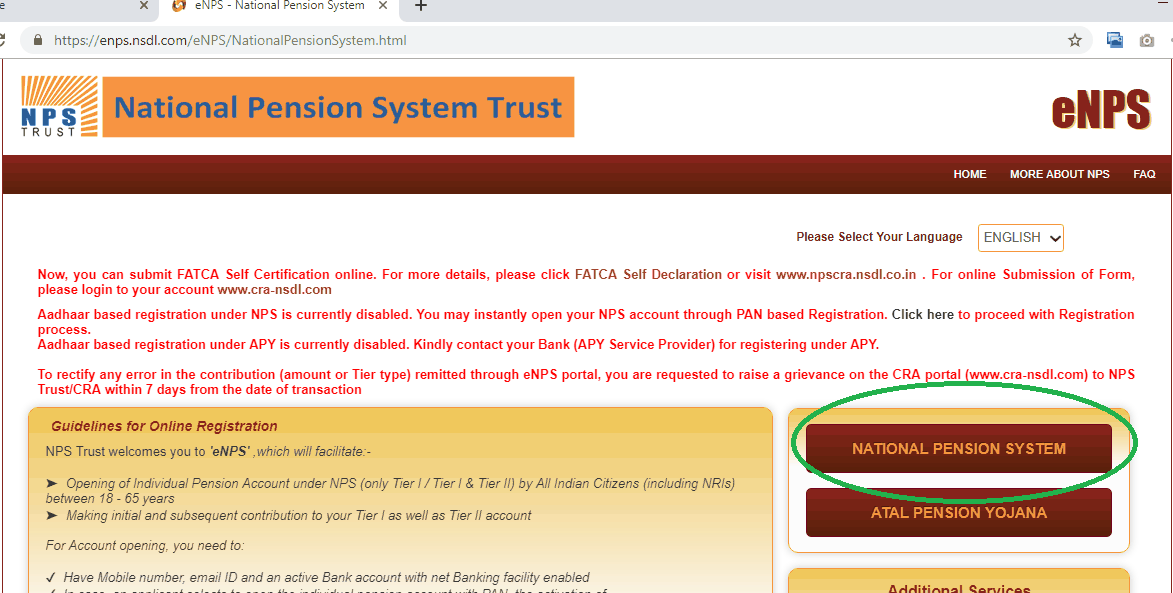

2. Online Mode – This mode is simpler than physical. You need to visit the e-NPS website and click on the National Pension Scheme. After clicking you will get 3 options i.e. registration, contribution, and tier-II activation. You need to select Registration.

There you need to select appropriate options, enter your PAN and select your bank/POP. After clicking, continue you will get a registration form, fill the form online, attach the required scanned documents like PAN, address proof and scanned signature. Once it is done your PRAN will be generated and you can start investing in NPS.

Important Point: For online registration, it is mandatory to have a net banking account

What are the investment options in NPS?

Your money in NPS will be invested in 4 asset classes. Which are referred to as ECGA?

C – Corporate Bonds (Moderate Risk – Moderate Returns)

G – Government Bonds (Low Risk – Low Returns)

A – Alternative assets like real estate investment trust (REITs) & infrastructural investment trusts (InvIT) (Very High Risk – Moderate Returns)

The choice of asset allocation among these options above will be defined by the subscriber himself (Active mode) or it will be auto defined depending on the age of the subscriber (the older you get, more stable will be your investments). In both options, 75% is the maximum limit for investing in equities and for alternative assets class maximum contribution can be 5%.

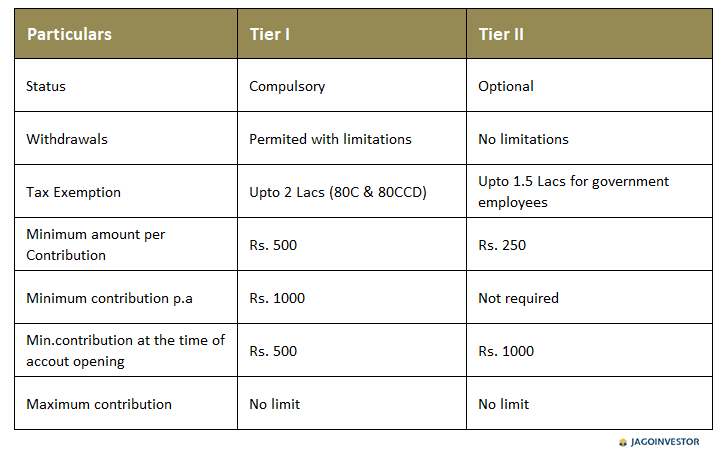

What is Tier I and Tier II in NPS?

These are two account types of NPS accounts. Tier I is primary compulsory account for NPS also referred to as “Pension account” whereas Tier II is an optional account commonly referred to as “Investment account”.

Following chart will elaborate the difference between Tier 1 and Tier 2 NPS accounts-

What are the tax benefits of NPS?

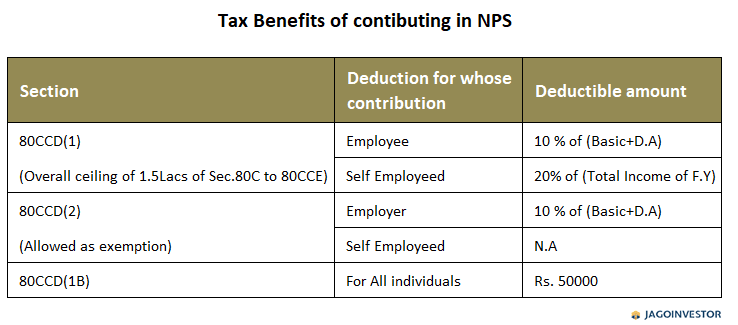

An employee’s own contribution in NPS will allow tax deduction under section 80CCD(1), up to 10% of salary plus dearness allowance and for self-employed individuals it is 20% of total income in a financial year, but this has to be within the overall ceiling of Rs. 1,50,000 of Section 80C to Section 80CCE of Income Tax Act.

An employer’s contribution up to 10% of salary plus dearness allowance is allowed as an exemption from tax under Sec. 80CCD(2)

Moreover, individuals can claim an additional deduction of up to Rs 50,000 under Section 80CCD (1B), which is in addition to Rs 1.5 lakh permitted under Section 80C.

The below-given table will simplify this to you –

What are NPS withdrawal rules (Tier I)?

Once an investor retires at 60 yrs., they will get 3 options

Option #1 – Exit from NPS at 60: If you want to exit from NPS at 60 years of age, you will get lump-sum 60% of your corpus and for remaining 40% an annuity will be generated with a PFRDA-registered insurance company(called as Annuity Service Providers) to provide monthly pension after your retirement. There are different annuity plans provided by a few insurance companies, you can choose any of them. And you also have the choice of increasing your annuity contribution (40% is mandatory). However, if the total corpus is 2 lakhs or less than it then the whole amount is given a lump sum.

Option #2 – Continue NPS with contribution till 70 yrs. : You can choose to continue contributing to NPS for more 10 years i.e. up till 70 years. This option is mostly chosen if you are earning after the age of 60. At the age of 70 withdrawal rules will be the same as the exit from NPS at 60.

Option #3 – Continue NPS with till 70 yrs., but without any further contribution: You can choose to not contribute to NPS and wait for your corpus to grow more by 10 years. This option is chosen mostly when you have monthly income flow from somewhere. Thereafter at the age of 70 withdrawal rules will be the same as an exit from NPS at 60. This option has to be exercised 15 days before the default date of withdrawal.

Important Point: Subscriber has to exercise continuation or deferment options 15 days before the date of retirement. Lump-sum withdrawal from NPS is tax-free. Whereas monthly pension will be taxable as per the tax slab of the subscriber.

Withdrawals in Tier II?

There is no limit on tier II withdrawals and all the withdrawals are taxable as per the slab rate of subscriber. It means Tier II works in the same way as Mutual Funds – Investing into Equity/Debt funds and has high Liquidity.

What is the NPS withdrawal procedure?

The withdrawal process starts 6 months before retirement so that pension will be started immediately after retirement. A subscriber can withdraw online or offline.

1. Online Process of pension withdrawal –

A claim ID is generated by a central record-keeping agency, six months before retirement, for which you will be notified via mail or letter. With the help of this ID, the subscriber can check and change his account details like address proof or bank account. Once the withdrawal claim is initiated, no details can be changed. Following is the process of initiating withdrawal –

Step#1 – Login to NPS using PRAN and Password

Step#2 – Go to Exit Withdrawal request and select initiate withdrawal

Step#3 – Select withdrawal type i.e. Exit at 60

Step#4 – Select ratio of Lump sum & Pension

Step#5 – Select One Annuity Service Provider

Step#6 – Verify all details and submit request form

Step#7 – Download request form

Step#8 – Sign and submit the request form to POP or Nodal Office

After 4 working days, lump sum amount will be credited to registered account. For pension all the details will be sent to ASP, once ASP processes all the details, you will start getting pension as per your selected annuity plan.

2. Offline Process of pension withdrawal –

In offline process withdrawal application is to be submitted at POP or NODAL office along with required documents. They will forward them to Central Record Keeping Agency (CRA) and NSDL. CRA will then register your request and issue an application form for withdrawal. Fill in all the details and describe the percentage of lump sum & annuity and select an annuity plan as per your needs. Once your request is processed you will receive the lump sum and pension as per plan selected.

What if I want to early withdraw i.e. before 60 years of age?

As NPS is a purely retirement solution product you should not exit before your age of 60. However, in some special circumstances, you can withdraw 25% in total of your own contribution in NPS. This you can do only after 3 years of investment and just 3 times in the entire tenure of NPS. The special circumstances are –

Children’s wedding or higher studies

Building/buying a house

Critical illness of self/family

Important Point: Partial withdrawal from NPS is tax-free.

What if I want to exit from NPS before 60 years of age?

After 3 years of NPS investment, you can opt for a premature exit from NPS and don’t want to contribute anymore, then you will receive 20% of your corpus as a lump sum and balance 80% will be mandatorily used for annuity fund. You can choose pension payment mode like monthly, half-yearly or yearly.

Important Point: In this case, the lump sum and pension you receive both will be taxable as per income tax slap.

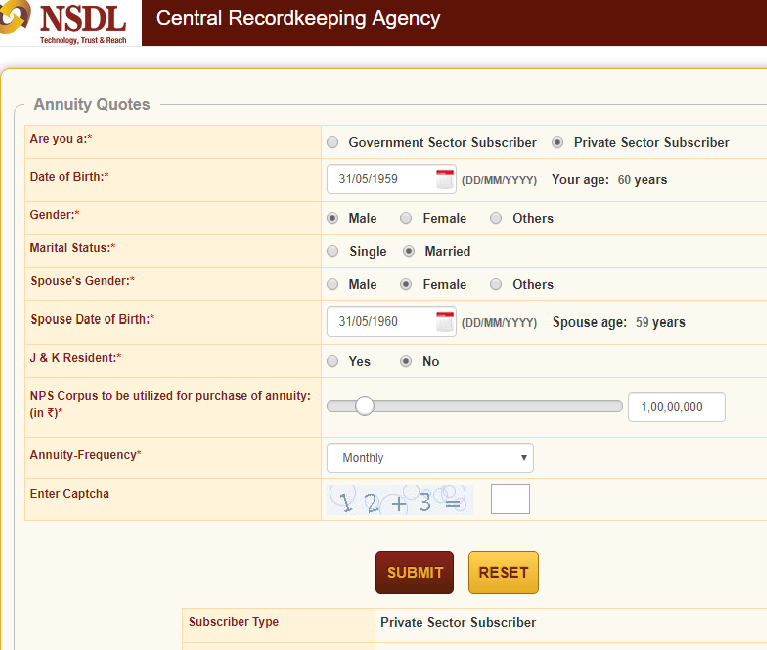

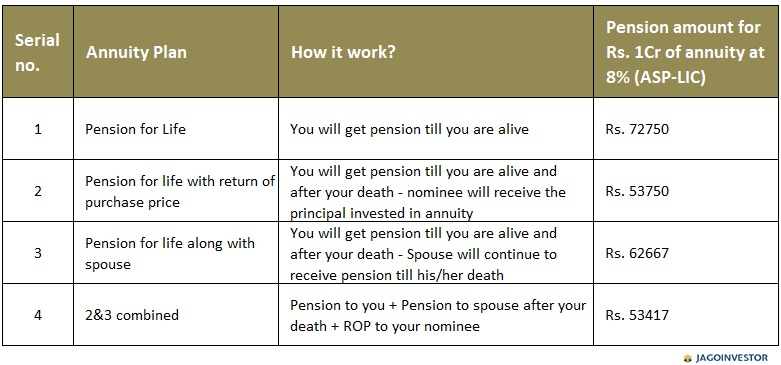

What amount of Pension or annuity I will get?

An annuity is a fixed payment like pension that we get every month, half-yearly or yearly depending upon the chosen model. In NPS 40% of the corpus is invested as an annuity with annuity service providers i.e. PFRDA registered insurance companies.

NPS corpus amount that you utilize for buying an annuity plan

Annuity Frequency

So, on filling all the details as mentioned above you will get the list of annuity plans along with the amount of pension that you will receive.

Other than this, the amount of pension also depends upon followings –

A prevailing interest rate of the annuity: The Interest rate on annuity will be the same as government securities, ranging from 6% to 8%.

Annuity Plan that you choose: There are different annuity plans provided by ASP. Here are some generic annuity options offered by ASPs. Remember, some ASPs may offer a slightly different or combination of these options:

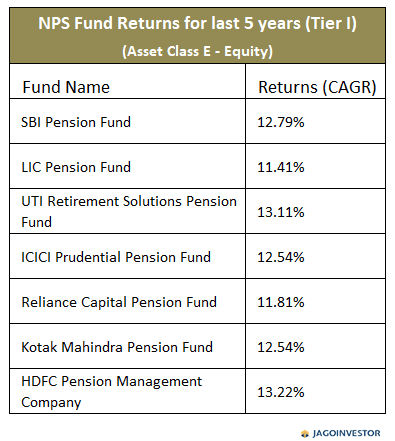

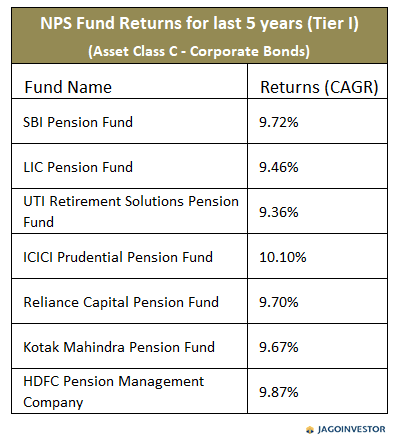

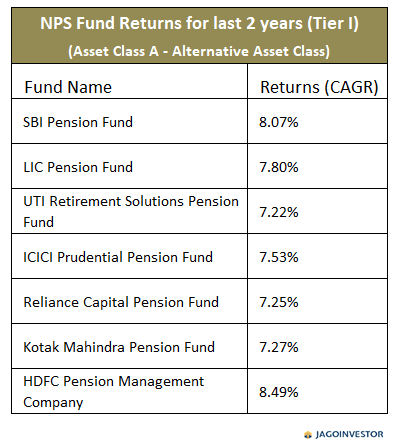

What is the result of NPS fund performance till now?

Following tables will show a return of pension funds in the last 5 years –

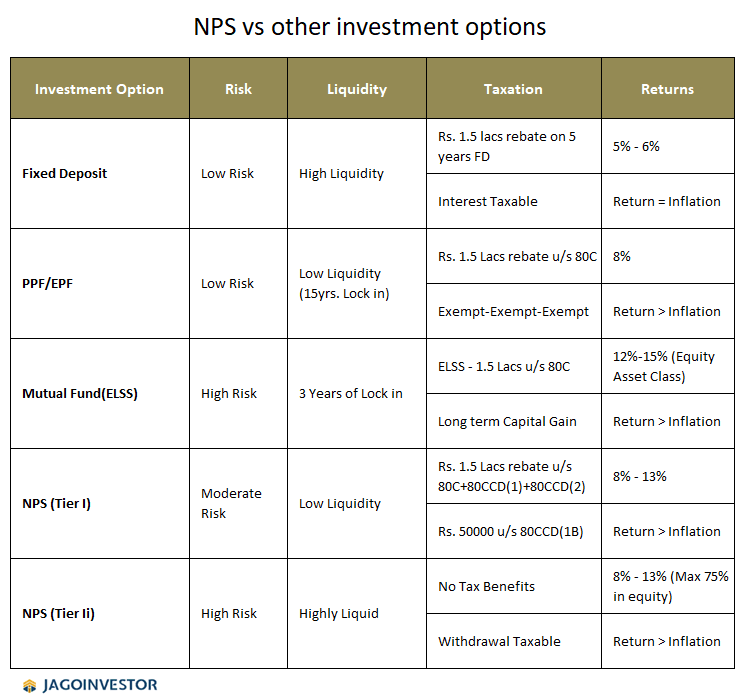

NPS vs Mutual Funds (ELSS) and Fixed Deposits / PPF/ EPF

Here is a small comparison between NPS with other investment options like ELSS mutual funds, FD, EPF, and PPF. The below-given table will show the difference between NPS and other Tax Saving investment options –

There is also an app for NPS to provide more convenience to its subscribers. Do let us know if you have any queries regarding NPS. It was quite an exhaustive article, hence there might be something we might have missed.

In the world of mutual funds, there are various kinds of categories for different requirements and risk appetite. One of the categories I want to talk about today is the “Balanced Advantage” Category.

What are Balanced Advantage Mutual funds?

In one line, a balanced advantage fund dynamically shifts between equity and debt depending on the market valuations. What it means is that when the markets are over heated and high, the fund decreases its exposure to equity and move the money into debt, so that if the markets fall, the down side is protected.

This strategy significantly reduces the volatility of the fund compared to an equity fund and at the same time, the returns potential also comes down.

A lot of funds in this category also name their funds as “Dynamic Asset Allocation Fund” rather than “Balanced Advantage”

Some of the examples of the funds in this category are

ICICI Prudential Balanced Advantage Fund

Motilal Oswal Most Focused Dynamic Equity Fund

Aditya Birla Balanced Advanced Fund

Kotak Balanced Advantage Fund

Reliance Balanced Advantage Fund

HDFC Balanced Advantage Fund

How does a Balanced Advantage Mutual fund work?

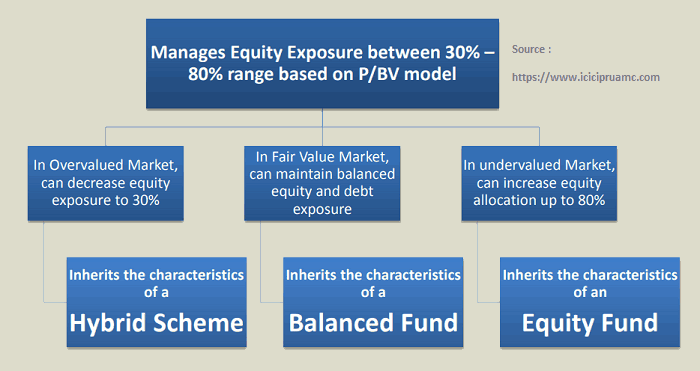

A balanced advantage fund uses a predefined algorithm and based on Market PE or P/BV or some other internal indicator to determine if markets are on the higher side or lower side and then based on that they keep increasing or decreasing the equity exposure.

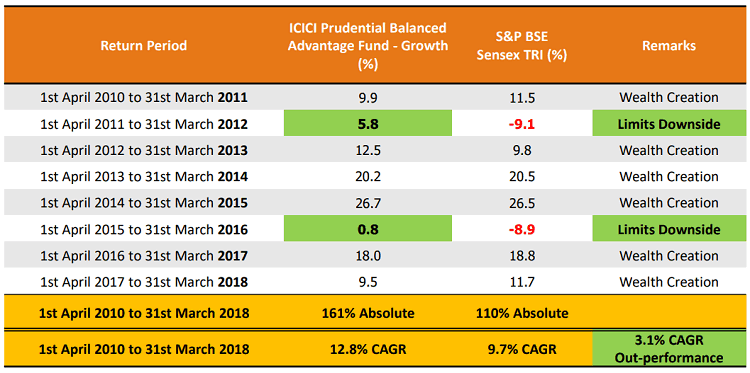

To explain you more about this, I will take an example of how the ICICI Prudential Balanced Advantage fund which was the first fund of this type in the mutual fund Industry and very successful in that category.

Disclaimer : I am taking the example of ICICI balanced mutual fund only because it’s the biggest in the category and quite old one in Industry and we have some data to show. It’s not a recommendation to buy. We have some equally good funds from other AMC’s also.

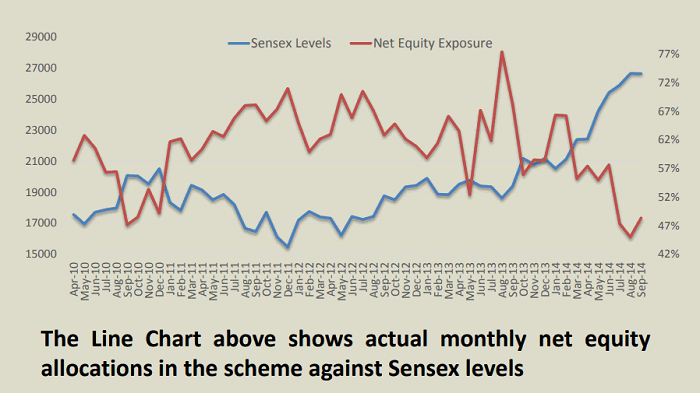

Below you can see how the equity exposure has changed over time from Apr 2010 – Sept 2014. You can see that equity exposure increases when Sensex levels go down and vice versa.

Limits downside and upside

The main benefit of Balanced Advantage funds is that it controls and extreme upside or downside. So you will not see very deep losses, but at the same time, you will also not see very high profits.

However, the balanced advantage funds will provide decent market returns (but not comparable to pure equity funds)

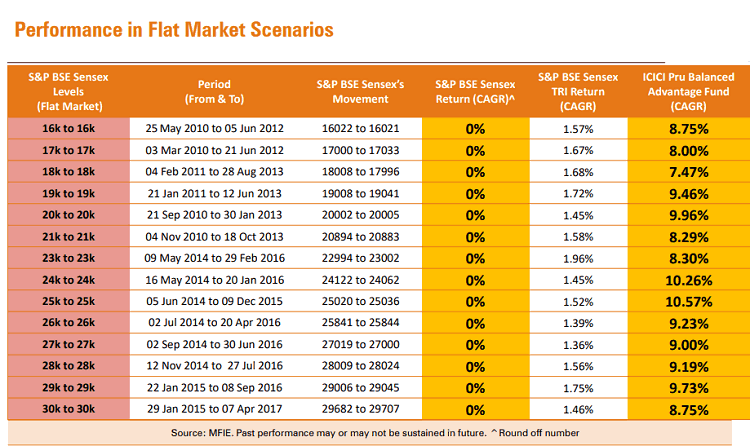

Even in the flat markets, you can see that the balanced advantage category has generated positive returns by taking advantage of the volatility.

Who should invest in Balanced Advantage (or Dynamic Asset Allocation) funds?

Now the big question is – Which kind of investors should invest in Balanced Advantage fund and When?

Who should invest?

It’s mainly for those investors whose focus is on reducing the risk, but at the same time enjoying better returns than Fixed Deposits. The fund value will still be volatile, but the intensity will not be as high as a pure equity fund. From Returns point, it will give decent return of 2-3% above FD returns, but that is all you should expect over a long term.

When to Invest?

As you have seen that the equity exposure is already controlled by the fund itself, you can actually invest anytime you want. There is no need to time the market, because the fund itself times the market internally. There are no issues if you want to put lump sum or SIP.

Who should not invest?

An investor who wants higher return potential and can take the higher volatility, should not be ideally investing in these funds. However, if you are unsure of the markets levels and want to play safe, you can invest lump sum in balanced advantage fund and then setup a STP (Systematic transfer plan) to an equity fund. This will reduce the risk to some extent.

Important: Don’t confuse this category of funds with “Balanced Funds”. Balanced Funds are those mutual funds that have a mix of equity and debt in their portfolio with equity exposure of around 65-70% and rest Debt.

A good choice for Retired Investors

I think these kinds of mutual funds are a very good choice for retired investors who want returns better than the fixed instruments and at the same time, can’t handle too much volatility in their portfolio. So some part of their portfolio can surely be invested in balanced advantage or dynamic asset allocation funds (same thing, but different name)

If you want to invest in balanced advantage mutual funds, you can contact the Jagoinvestor team to know the process and get a well-designed portfolio.

Let me know if you have any questions regarding this fund of a mutual fund? Was it clear enough?

Do you think corporate fixed deposits are as safe as bank Fixed Deposits? Has come agent convinced you that you will get 2-3% higher returns from corporate fixed deposits without any risk?

If that’s the case, you need to be educated a little more about corporate fixed deposits. I will talk about 5 major things every investor should know before they put their hard-earned money in corporate fixed deposits.

What are Corporate Fixed Deposits?

Corporate Fixed Deposits are deposits that are issued by private and public companies, which work very much like bank fixed deposits. There is an interest rate offered and there is a maturity duration for the company deposit. You can either opt for a cumulative option (where your interest is added in deposits) or you can opt for a non-cumulative option, where you are paid the interest after every fixed duration.

A lot of agents get a good commission for selling these corporate fixed deposits to their clients. Nothing bad in that as such, but you need to be clear about some important and critical points related to company fixed deposits.

Let’s start…

Higher the return, higher the chances of Default

In almost all cases, the corporate fixed deposits offer quite higher returns compared to a bank deposit. If bank deposits rates are 7 %, you will see that company deposits floating in markets are providing your returns in the range of 8-14%.

Always ask the basic question – “Why is a company providing higher returns?”

The logic is very simple, a company needs money for expansion or for some project and to fund that project, they can either take a loan from a bank or raise money from other measures and for that they will have to pay very high interest.

So they float corporate fixed deposits where normal investors like you and me can invest in their deposits and earn higher returns.

But, because you get higher returns, there is also high risk involved in corporate deposits. You never know how the company will do in the next few months or years. You never know how the project of a company turns out and if it’s going to make a profit or loss.

In short, after a few years, when its time for maturity – what will happen if the company’s financial health is not good? Will they repay the money on time? Will they repay the money at all?

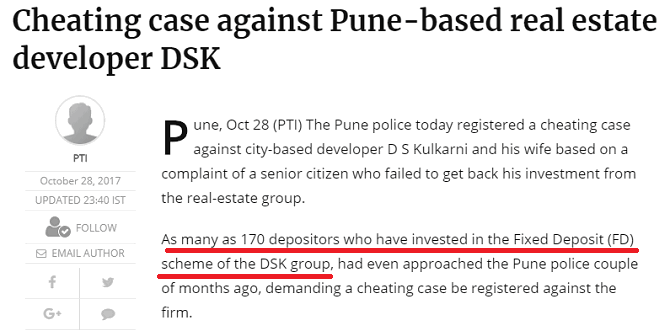

In one of the recent examples, a lot of investors had put their money in DSK group fixed deposits

A lot of senior citizens are lured into parking their hard-earned money into many shady fixed deposits offered by small or medium-sized company fixed deposits by showing them high returns.

Below is a heart breaking case study of a 78 yr old person who had put all his gratuity and PF money into DSK Kulkarni FD (a very big real estate group in Maharashtra). When his FD maturity came, he was told that he should renew it for another 6 months as its tough to repay right now. The video below is in Marathi, but you will understand some words and will be able to make out what is being said!

So please understand that when you are investing in corporate fixed deposits, there are good chances that if it’s offering very high returns, there is a lot of risks involved in that. You cant get higher return just like that.

Many big companies also offer corporate fixed deposits, but then the interest offered is quite lower and looks reasonable. However the risk is still there unlike a bank FD.

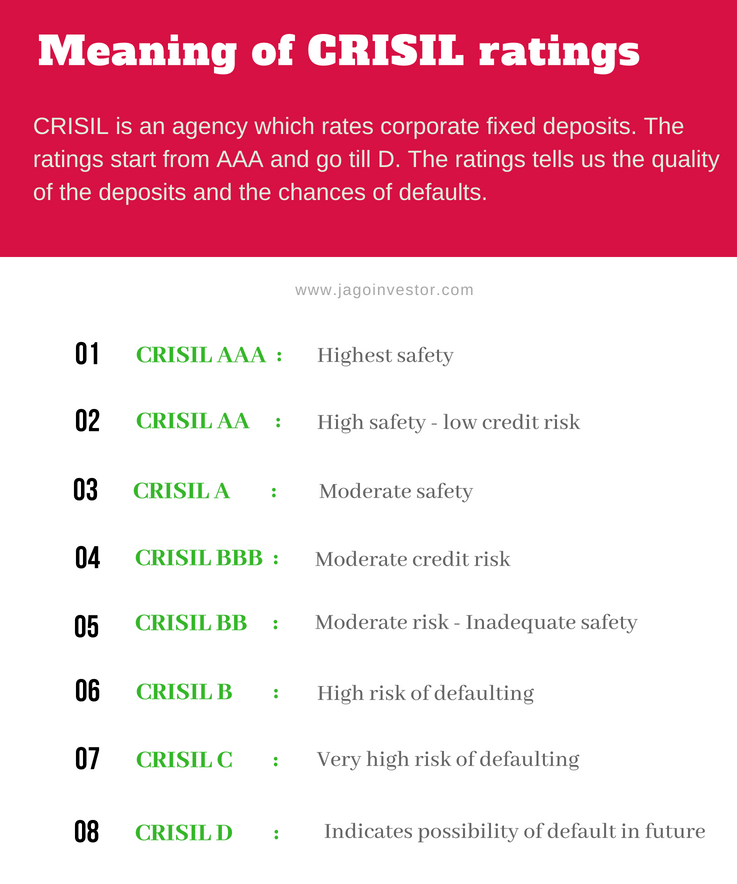

Every company fixed deposits are rated by agencies like ICRA, Crisil, CARE etc and they give a rating to the FD. These ratings are a measure of the company’s ability to pay the interest as well as principal to its investors. A high rating means no or very low probability of default.

Corporate FD’s are not regulated by banking rules

Note that unlike bank fixed deposits, corporate fixed deposits are not regulated directly by RBI regulations. All the deposits under corporate deposits are governed by provisions of 73 to 76A of the Companies Act 2013 (erstwhile section 58-A of The Companies Act 1956).

If the company is not paying you on time, you cant do much in that other than following up with the company. However, Fixed Deposits of Corporates are secured borrowing, so in case of winding up of business, secured borrowings are given preference over equity shareholders in terms of repayment.

Some important points related to Corporate Fixed Deposits

TDS is deducted @10% if the yearly interest is more than Rs 5,000

Premature closure of company FD is not possible for 3-6 months

Pre-closure of company FD is not a straight forward process, it’s cumbersome and involves too many documents

Still, want to invest in Corporate Fixed Deposit?

If you still want to go ahead and invest in a company fixed deposits, please take care of the following points.

Make sure that the company is paying regular dividends to its share holders

The balance sheet of companies is showing profits at least for 3 yrs in a row

Make sure its an at least a 5 yr of company

Make sure they are offering realistic returns (2-3% more than a bank FD). Do not fall for those companies which are offering very very high returns

Make sure these companies are listed on the stock exchange

Make sure that they have got a high rating from CRISIL like (AAA or AA or A at least)

Do you avoid various actions in financial life which are often suggested as the “right decisions”?

There are countless articles and videos these days which tell you that it’s important to have sufficient life insurance and health insurance. One should start investing very early in life so that they can create some good wealth to take care of their future.

Like these, there are various things that are mostly the building blocks of a good financial life. But often investors avoid taking those decisions. The biggest reason why it happens is that we are all lazy investors who focus on NOW rather than FUTURE.

If it’s not creating trouble for us right now at this moment, we keep postponing it and underestimate the trouble it can give us in the long future. In short, the future trouble or problems we will face is imaginary at this moment.

So today I thought I will talk about the impact of these decisions and how it can trouble you in the future. Let’s start

Mistake #1 – Not buying a health Insurance

Today I will not talk about what will happen if you buy health insurance, but I will talk about what CAN happen if you do not buy health insurance.

At one point in our life, when we start our career, we have ZERO wealth. There is no money in the bank account and we struggle too much to start saving. Our salaries are less and we have just started our career.

Our salaries are not much when we start our jobs, but our expenses start building up. Rent, groceries, Petrol, eating out and whatnot.

After a few years, suddenly we realize that we are just living paycheck to paycheck and we are not saving any money. Years pass by, but you have nothing worth calling “Portfolio”.

In fact, it might happen that you are in credit card debt now and you are wondering if you will ever be able to retire RICH!

Then comes, a point in life when you realize that it’s enough and now you need to start saving money for the future no matter what. Enough is enough.

You start your first investments

Somehow you start your first Recurring deposit or SIP in mutual funds. You start with a basic Rs 2,000 per month. A few months pass and you are happy to see that you have some savings now at your end.

You are excited and want to make sure you do not break this newborn habit. A few years pass by and you have done it! .. Congrats, you managed Rs 5 lacs in your portfolio. It took some years and lots of commitment to reach there.

You feel like a winner and you now truly understand the joy of having a big amount lying in your bank account. What a relief and feeling of safety it provides.

You are even more committed to save now you plan to reach the target of Rs 10 lacs with the next 2 yrs.

You are happy and life is all good.

Then the bad day happens

Then one day, while going to the office, some Rowdy Rathore in a Bolero who is trying to race his car with some unknown person hits your bike while you were on your way to the office. It’s a major accident. You can imagine some other medical emergency in a family if you do not like this example.

The hospital bill comes to Rs 6.3 lacs. There was a surgery done to make sure you survive and you were in a good hospital for 12 days.

You had to take out all your money from the bank or mutual funds and additionally, you have borrowed from your relatives/friends or swiped your credit card to complete the bill payment.

After a few months, you are back to life. But your financial life is back to square one. Your wealth is eroded. You did not protect your wealth from medical emergencies.

You did not take health insurance

We do not think like this about health insurance. We never see health insurance as a financial product that helps us to protect wealth. Buying health insurance is all about transferring the risk of paying the hospital bills to someone else. Health insurance does not protect your health. It can’t.

Remember, starting your savings and investments is easy (not that easy), and consistently doing it for many years it very tough.

Those investors who do not take health insurance over-focus on what is NOT GOING TO HAPPEN. They say things like

What if I never get hospitalized?

What is I drive carefully and never get into an accident

I exercise and eat healthily, why do I need any health insurance?

My company provides health insurance, so why do I need additional health insurance

I will waste my premium if I don’t get hospitalized for next 30 yrs

Sorry, but you need to focus on WHAT IF IT HAPPENS, rather than what if it does not happen.

Note that a health insurance product gives you a protection cover of a big amount every year. So if you buy health insurance with cover of Rs 10 lacs sum assured.

Click here to buy health insurance from our Trusted Partner (special collaboration with Jagoinvestor)

What you are accepting by not buying health insurance?

So finally, as a conclusion – When you do not buy health insurance, you are saying that I am ready to pay the entire hospital bill out of my wealth, every time it happens. I will take the risk of getting my wealth eroded by medical issues.

Mistake #2 – Not saving enough money for future

The next thing I want to talk about is not saving enough money for the future.

You have a nice car, you eat out often and you are able to take care of all your house hold expenses right now. You also take short vacations often. This is all well and fine if you are saving enough for the future. But if your expenses are almost equal to your expenses, remember that one day will come when your income is going to stop permanently.

That will happen when you reach around 60 yrs. And you will probably live for another 30 -40 yrs (wish a long life to you)

But if you do not have enough wealth created by that time, the journey ahead will not be filled with fun. Imagine you retire with just 5 yrs worth of expenses in your bank account.

How cool is that?

How will you feel to find yourself in a situation where you know that you require 100 units of money each money to live a comfortable life which you desired, but your wealth is only capable of providing your with just 40 units of money each month? Or 8 units?

You will have to choose between a vacation and food on the table. Forget food on the table, you will have to choose between “cheaper” vs. “what you like” each time you think of what to cook for dinner.

You will have to decide each time if you want to travel by air or sleeper class on a train (I love both options)

You might have to make excuses each time your friend circle plan a holiday trip

You might have to constantly worry if a restaurant bill will be too much?

It might sound very dramatic right now hearing all this, but the truth is that the future is imaginary and it’s tough to plan for it. I am not saying that you should create enormous wealth by compromising today, but all I am saying that you should be well aware of how your decision of not saving enough today will impact your future.

A little financial planning helps

Most of the people who come to us for financial planning are already late in investing. We can’t fix it fully, nor do we give them false promises that they will retire as a millionaire. But we make sure that they make the best of the years ahead.

We make sure that whatever suggestions we make to them for their wealth creation aligns with what they want in life ahead. We plan for their goals and create a decent strategy to reaching those goals.

Saving money right now does not give you any joy or benefit right now. Saving for the future also means cutting down on something today hence we don’t do it. Saving for future means.

Cutting some part of your shopping today

Cutting down on your eating out today

Compromising a bit on your entertainment today

Buying fewer gadgets today

Buying fewer clothes today (please raise hands, if your closet has something which is not used since last year)

What you are accepting by not saving enough for the future?

So finally, as a conclusion – When you do not save enough for your future, you are saying that I am ready to be dependent partially or fully on others for money and my day to day expenses. I am ready for a lifestyle which might be very different from today. I am ready to live a life which will come with daily struggle and stress about money.

Mistake #3 – Not having a term plan

Accidents are called accidents because they are not planned nor they are expected to happen.

Why are we so over confident that nothing can happen to us and bad things happen only to others?

We all have recently heard about the Kamala mills fire news. Almost a dozen people lost their lives in that fire. One couple who lost their lives were actually sleeping when their friends asked them to join the birthday celebration of some other friends. They woke up and went there, but never to return.

Life is LONG

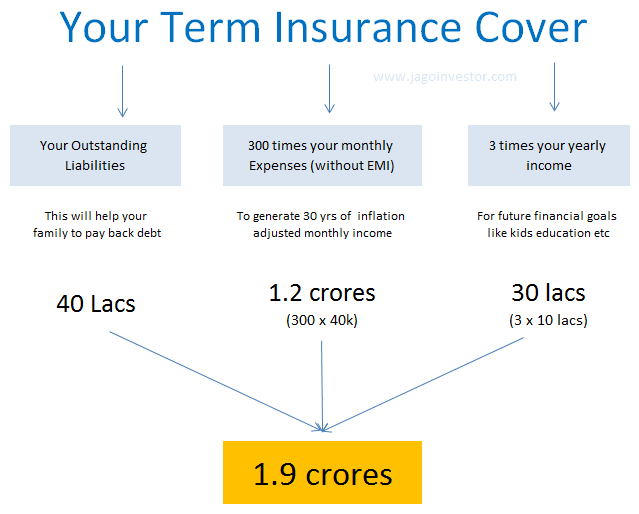

Life is very long and your loved one needs a lot of money to live comfortably. We need to make sure that we cover this risk by taking a sufficient term plan for which we need to pay a very small premium.

A family whose expenses is around 50-60k per month needs close to 2 crores of life insurance.

If you leave behind a family who is weak financially, you are leaving them with the risk of being dependent on others for their survival. While you can’t prevent the emotional loss, neither you can minimize it. You can surely take action today to minimize the financial impact.

If you have enough wealth and assets which will help them financially in the future, then it’s totally fine to not buy a term plan. But if you are someone who has no assets or wealth, you need to make an arrangement for the worst case. There is a famous saying – “You don’t buy a term plan because you will due, but because your family will live”

Answer this: In your absence (and the money you bring on the table)

How will the next 30 yrs of household expenses come from?

Who will fund for your kids education

Who will repay your debt?

Who will pay for all the desires your family has?

Where will they turn up to when they need money in cases of emergencies?

What you are accepting by not buying sufficient life insurance (assuming you don’t have enough wealth)?

So finally, as a conclusion – When you do buy sufficient life insurance for your family, you are saying that you are ready to let your family face lifelong financial suffering. Your kids and spouse + parents might be suddenly forced to live below the standard of living they are used to. Your kids might not get the same quality of education which would have been possible if you were there.

Mistake #4 – Over investing in Fixed Deposits/PPF

For some people, fixed deposits are the only way to invest their money. It’s a safe and secure way of investing. Our parents did it and there is a visible problem when you invest all your money in fixed deposits or saving bank account (or PPF or Post office schemes)

After all, you park your money in FD/Saving bank and it grows in value over time. What’s the issue in that?

The biggest problem is that your investments do not beat and outgrow inflation over the long term. You get a feeling that your investments are increasing, but your purchasing power does not increase. Its goes hand in hand with inflation.

So if you were able to buy 1 loaf of bread earlier, even today you will be able to buy the same 1 loaf of bread with the money you had invested in FD.

Your life style will remain the same over the years because your money is just growing as per inflation. To counter this, you need to invest your money in something which counters inflation, like equity. It can be stocks or equity mutual funds.

Here is an example

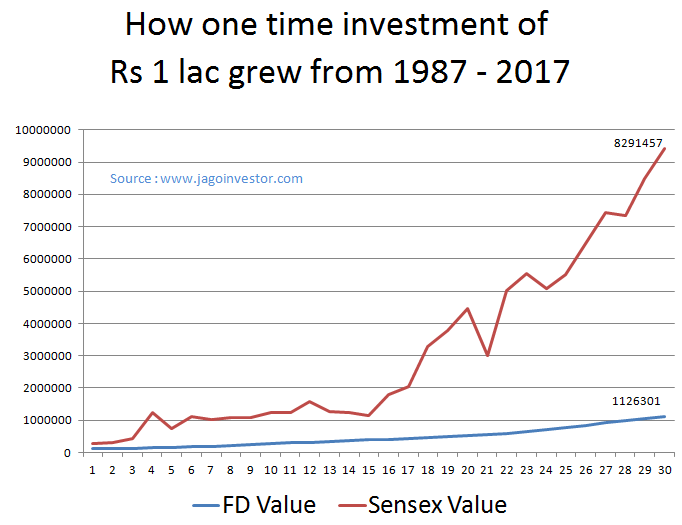

Imagine this, Rs 1 lac invested in Fixed deposits 30 yrs (year 1987) back is worth Rs 11.3 lacs today (the year 2018). Don’t jump out of excitement. 11.3 lacs today is worth Rs 1 lac 30 yrs back in real terms.

Whereas, if one had invested the same Rs 1 lac into Sensex 30 yrs back, it would be worth 83 lacs today, that’s close to 7-8 times than FD

Consider two friends who were 30 yrs old in 1987. They were fresh into jobs and started their career. One invested 1 0 lac into FD for his retirement and other one invested 10 lacs one time in Sensex.

One retires with 1.1 crores in hand and other one with 8.3 crores. One of them will get a monthly pension of 7-8 times compared to the other one. Just image the difference between them and how they will feel about it.

What you are accepting by investing only in Fixed income asset class (like FD, PPF, Post Office)

So finally, as a conclusion – When you only put your money in fixed income instruments all your life, and refrain from equity asset class, you are accepting that you will take the safe and secure path which has no growth element in it. You are ready to retire the middle class itself. You are consciously accepting that instead of 8X money, you are ok with 1X money because you are not ready to take the risk.

Mistake #5 – Taking too much debt in your life

There are two kinds of investors – One who buy things in life mostly with their saved money, and other one buys most of the things with their future income – i.e. LOAN

When we start our career, we have no idea what a devil is this credit card or a personal loan. It’s as simple as BUY NOW and PAY LATER. How bad it can be after all?

We feel we are in control of ourselves self and we will take rational decisions when it will come to money. We think we are not going to make stupid decisions. But only after years, we realize that the game is not so simple.

Once you depend too much on loans and credit cards, it becomes your way of life. You keep shopping and buying things you desire on debt, thinking that you will pay it later.

It’s all about falling for instant gratification and there are millions of people in India who are deep into debt. There are people who have bought cars which does not justify their pay package, and many people have home loans which are much bigger that what they can truly afford.

You will be the slave of MONEY

The biggest problem with this approach is that you become a slave of money. You have promised to pay all your future income, which is uncertain and which is not even earned.

You will be now going to your job to earn money, not by choice but a compulsion. Also, you are going to take less risk in life because you can’t afford to take much risk anyways now. If you do not like your boss, you need to keep quite because there is a sword of EMI hanging. What if you do not get an appraisal? What if you lose your job?

Also, you will be compromising with your wealth creation, because you have already consumed most of your future income through loans. Whatever you earn has to go in servicing your EMI’s and current expenses. There will always be less money for future goals, and this thought will keep on haunting you.

Here is a small 6 min short film on the debt trap which happens by use of credit card. It’s quite a simple short film but gives the message

Do not spend the money you don’t have

We all take a few loans in life and that has become the way of life, which is ok. I am not the person who advocates the concept of “Never take any loan” . But surely you need to control it and define the boundaries. If you get into the debt trap, it will be very tough to get out of it.

There are few signals which will tell you that you are too much dependent on debt, they are

More than 50% of your income per month goes into EMI

Your loan outstanding is more than 4 times your yearly income

You have more than 2 credit cards

You have a revolving credit card from last many years

You have too small savings even though you have worked for many years

What you are accepting by taking too much debt

So finally, as a conclusion – When you start depending too much on debt and overdo it, you are accepting that you will be working for money out of compulsion to repay it back. You agree to be constantly living under pressure and feeling frustrated about your debt. You agree to be living a life where you will not be able to take much risk and do what you wish for because you have EMI’s to take care about.

Do let us know how many mistakes are you committing right now in your life? Was this article useful for you?

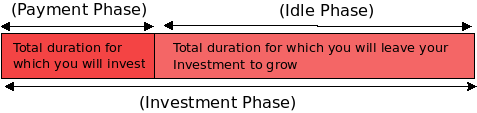

Lets say you want to invest Rs 2,000 per month for 10 yrs and then want to leave it for next 20 yrs to grow . How will you calculate it ? Do you know ?

Today we will see this basic calculation and learn how to find out the amount you can generate .

We have to understand that there are two phases to this calculation. First is Payment Phase, which is total time when you will pay money from your pocket , example 10 yrs .

Next phase is Investment Phase, This is total time frame you are invested in something product. Example 30 yrs, So in this case Phase 2 – Phase 1 = 20 yrs , which is the time when you let your money grow .

What it means is that your money will grow in two phases, First is the payment phase when you are investing money from your pocket, at the end of the payment phase , you will build a corpus which you can call as “Payment phase Corpus”, Now after this you stop payment any amount from your pocket and just let this “Payment phase coupus” grow year by year in some product till your target date.

So as per our earlier example, You may want to pay for 10 yrs (payment phase) and then let it grow for next 20 yrs and at the end of 30 yrs (Total Investment phase) you will build the “Investment Corpus” .

We will see an example calculation below . Assumptions are

Ajay wants to invest Rs 4,000 per month for 10 yrs and expects a return of 12% yearly (Payment Tenure) . After 10 yrs of investing from his pocket he then wants to leave that investment to grow in Equity (see suggestions for equity funds) and expects it to grow by same 12% return.

Payment Phase : Our first task here is to calculate the Corpus generated after Payment tenure first . So as per example, Ajay wants to invest Rs 4,000 per month for 10 yrs (120 payments) @12% return expectation . The forumla you have to apply is called Future Value forumla or annuity due (payment in the start of the period) . The forumla is :

FV = A x (1+R) x (((1+R) ^ n) – 1)/R

where

A = Investment per month : This is the amount invested per month , In our example its 4,000 per month

R = Rate of Interest per month (yearly interest/12) . This is monthly return you expect , If you expect the return to be 12% per year , then per month return will be 1% (compounded monthly) , hence R = 1% or 0.01

n = This is total number of payments , so multiply 12 by the number of years , so if your duration is 10 yrs ,then n = 12X10 = 120

As per the formula

FV = 4000 x (1+.01) x (((1+.01) ^ 120) – 1)/.01

= 9,29,356

So we have found that the total corpus generated after 10 yrs of payment tenure is Rs 9,29,356 . First step is completed .

Investment Phase : Here , we are going to calculate the final value of the corpus at the end of Investment phase , so as per step 1 , we have Rs 9,29,356 at the end of 10 yrs , which we will call as Payment phase Corpus (PPC) . Now this amount will be lying in the investment for growth . We just have to apply compound interest formula now which is:

Final Corpus = PPC x (1+R) ^ n

where

PPC = Payment Phase Corpus , we have calculated it above and its value is 9,29,356

R = Rate of return expected for the rest of the period , we have expected it to be 12% or 0.12

n = this is the number of years we are letting the money grow after Payment phase . In our example it was 20 yrs, because total investment tenure was 30 yrs, out of which first 10 yrs was payment tenure .

Applying the formula we get

Final Corpus = 9,29,356 x (1+ 0.12) ^ 20

= 89,64,840

So the final amount you can generate by investing 4,000 per month for 10 yrs and then leaving it to grow for next 20 yrs @12% is 89.64 lacs.

Mohit, one of our readers has agreed to share his rags to riches story which will help a lot of you to build the mindset to become rich and do what it takes. Over to Mohit.

—

My story is going to be about two generations and how each view, treats and values money differently. Some background first…

Imagine sitting under a lamp-post or under the stair-case of your palatial home (shared) for your studies, way back in the 1970s? Sounds like a scene from a Bollywood potboiler? Well, this was exactly how my father scrapped through his school and college education.

He was born to a joint-family that had a huge house but no income. A vain father, no mother and zero income; my father’s money story is a true rags-to-riches one in the sense that he had absolutely no support and progressed on scholarships by his college to complete his degree.

Also in true Hindi-film style; the love of his life (then) rejected him for lack of money.

How my father got his first job

In the 1970s, a generation waking up to the post-independence yet pre-liberalized era of working; he got his first job in the then Hindustan Computers (HCL) under its founder, Shiv Nadar. He still remembers fondly that his employee code was 0002, i.e, he was HCL’s second recruit.

My father faced such money hardships in his childhood that the only objective in his life was to acquire wealth. But there were no equity markets or organized financial planning back then. One invested in real-estate of whatever surplus they had, and he was no different.

My father started his own business

After a brief stint with HCL, my father decided to venture out on his own and set up a small logistics company (for the uninitiated, logistics is responsible for import of goods in India from a foreign-country and vice-versa), and again as my father fondly recalls now, the first month’s profit he made in 1980 was fifty thousand rupees!

That was more than what he earned in his five years in his job! Therefore he immediately recognized that business is the way to be if one wants to make more money.

From the early-1980s to the early 2000s, i.e. in a span of 20years, he made the tables turn in his favor and even though he did not make an Ambani out of himself; he acquired a 9-digit net-worth starting from absolute scratch. As much as I am proud of his achievement, I objectively analyze his money journey and mistakes in following bullet points –

My analysis on my father’s money journey – “Achievements and Mistakes”

He was never a big risk-taker. So his entrepreneurship success is a bit surprising (no risk = no gain) to everyone. Yet as a close observant and first-hand beneficiary; I attribute it to immense HARD WORK! Really he amplifies the cliche that there is no substitute to hard work. I have seen him work weekdays and then Sundays too.

He made some mistakes in businesses like a factory went wrong, but he knew what his A-game was and stuck to his guns. Often people over-diversify (even in investments) but he invested his majority time to the business he knew best.

He had absolutely no knowledge of shares. But he did make some IPO investments on advises etc but they never yielded any returns. It happened with endowment plans from LIC etc.

At the “right” time, he made some real estate investments, which paid off big-time and are the real reason behind his swelling net-worth.

The best part was – he was never a miser. I don’t recall a single day during my childhood when we felt we were missing anything for lack of money. He spent on cars, jewelry, travel, and the typical good things of a lavish life.

Typical old-school style, he kept his entire money either in property or in spending; which I often remind him as a mistake.

Cut to 2004 – This is where my own money story begins.

Having seen his business success story (which as a child, I often took lightly. I didn’t quite acknowledge that making money is this difficult), I had a few things clear to me –

Born to such a successful person, the benchmark was quite high.

My mother kept reminding me the importance of money during my growing up years, and so, making huge money was always a priority.

I was eager to get out of the world of business and take our net-worth to the next level, i.e, 10-digits!

Just like my father, I knew business was the way to be and set-up my venture in December 2004 (although I had a kickstart – firstly space was provided by him, secondly I didn’t have to be the breadwinner).

Again the first few months were so profitable that my self-belief was sky-high. In fact, I became over-confident, or maybe a better word would be snotty. Yes, today I can admit it; even though back then I didn’t realize it. So I set-up another business. And then another.

I wanted to become super-rich and in super quick time that I started losing sight of value-addition by my business. I learned 2 important lessons.

Lesson # 1: Never take things for granted

A couple of years later, my businesses started going downhill. I had to shut down a couple of them and like my father before me, I focused on the A-game. Thankfully a new trade-lane emerged in India and my business and money-journey started improving brightly.

As it became more consistent, I again ventured out in a couple of new fields. Whatever surplus I had, I either put in my businesses OR in bank FDs. Looking back, I am shameful to admit but I didn’t utilize India’s maturing equity markets especially between 2008-2010 period.

In late-2013, I had my first brush with mutual funds. Through a banker (I still credit him for bringing me to equity), I made my first SIP and my first lump sum mutual fund investment. Because the markets grew rapidly since Modiji came to power, my investments swelled handsomely.

And that’s when I made another mistake – I shifted all my FD money into equity. My 7-digit portfolio was 100% equity, full of mutual funds, NFOs, direct stocks, you name it!

Lesson # 2: Take financial planners seriously

Thankfully, better sense has prevailed since then and I have deliberately re-designed my portfolio with a 50:50 equity: debt allocation in late 2017.

As things stand today, I am doing two businesses and while the first one is doing great, second is still in nascent stages. My money is invested in these two, with no investments in real estate or FDs. A third stream is markets (as shared above, 50% equity and 50% debt) with running SIPs.

As of March 2018, I am proud to share that my own net-worth (not counting father) is nine-digit itself and the aim is to attain 10-digits by 40 (I am 34 now). That’s when I shall hang-up my boots and stop working for money.

Am I happier today because of my high net worth?

Personal happiness is a state of mind. When one is feeling rich (not only money-wise but overall), then one is bound to feel happy too. In that sense, I do attribute a lot of my happiness to my growing net worth.

I have never been too much into ‘brands’ or ‘consumption’ per se, yet it is mentally comforting and moral-booster to see your net worth grow. So yes, I will agree that happiness levels have increased definitely with growing money in the bank.

However, there is a very thin line to be identified here. One tends to cross that line unknowingly (as I did at the little success at the beginning of my career). If one gets obsessed with their money-success, then it captures your mind.

You start expecting more out of yourself every day, and in the process – keep pressurizing yourself. So the trick is to find the “right balance” and acknowledge that you are separate from your “material success”. Appreciate the money success, yet keep reminding yourself that it can all go wrong tomorrow – so don’t bet your life on it.

Rich have their own set of problems

A lot of people tend to feel that their problems will vanish once they get rich. This is largely true as well, however, once you settle into “the rich” life, a different set of pressures and problems will take over. Your lack of resources for foreign travel or a Volkswagen car; will be taken over by problems of beating your neighbor’s car or foreign travel with a business-class flight etc.

My point is – money problems will disappear temporarily but new ones will soon take their place. To counter it – always try and live a lifestyle one-level below the one you could afford. If say (in the Indian context) there could be five levels of income, and you are on the fourth level, then try to deliberately follow a lifestyle you deem fit for third-level income.

Those ways, your ‘money problems’ shall always be 1-step behind you.

10X money definitely can bring 10 times comfort or even 10-times security; but definitely not 10 times happiness. Unless again, your life is one-dimensional (i.e. only about money) which is definitely not the case with anyone.

Some money lessons out of my own experiences

Don’t become a philosopher, before you become rich. Nobody listens to a poor philosopher. This implies that one needs to get rich (whatever an individual’s definition of rich maybe) in life, to be taken seriously. You can reject the notion of “money is not important” only after you have conquered it.

Beyond your line of work (business, job, professional – whatever it may be), you need to develop a passive income. It can be through equity markets, interest income, rental or combination of all. One must aim that such passive income can match their monthly-expenses at some point in their life (earlier the better).

Do not consider your ancestral wealth as your own. At best it should be your fallback option. I speak this not only from my own experience, but n number of observations out of families around me. By the time you inherit it, you have lived past your prime life (i.e. past your 20s and 30s, even 40s). Also, you have to carve your own identity and make your own money for improving your self-worth.

Living on debt or on a monthly paycheck-to-paycheck can be mentally demoralizing. One must have a decent amount of savings tucked-up somewhere, to live with dignity and a sense of security.

And finally, DO NOT think of money as the only thing in life. One must value the balance of life very highly. It is of no use to have a high net-worth when you are occupied with it 24*7 or are living an unhealthy lifestyle plagued with physical problems. Always try to create equilibrium between money/income, health, close-ones and entertainment (travel, a hobby or something etc). I especially emphasize the last one as I have known people who are so much into their careers that they do not know how to spend their spare time, or what to do on their weekends except watching tv. That is quite sad.

Let me know what did you learn from this money story?

What is your money story?

I hope everyone has learned a lot from his story.

If you want to write your money story, Leave your details here and Jagoinvestor team will get in touch with you with the next actions.

Today we are sharing a very different money story, where one of our readers is going to share his life journey of becoming a middle class from being RICH years back. Yes – you heard it right.

As per his request, we are not revealing his name and identity. I thank him to share his story with a bigger audience.

Here it goes…

My story starts with an assumption that most of the jagoinvestor readers belong to a middle-class background or from a humble background. Most of the readers have either already moved to a level higher or are trying to move to a level of lifestyle better than what was available to them in their childhood.

My story is a complete reversal

Yes, I moved from affluent background to a mid-income kind of family (from a big city perspective and not on pan India basis)

My story is a lesson on why financial planning and diversification are important. I was born in a rich business family of a small town (population of 1 lac), my father was a well known and socially connected/respected person in society.