We will learn about creating a WILL in India today, but before that you need to answer this question – “Do you want to leave your wealth and let your loved one’s fight with each other to get their shares (a la the Ambanis!)?” –

I guess not! . If you nominated some one in all the financial products you bought and thought that it will be passed to them legally without any issues, you are living in the world of fantasies (kind of :). It’s a common misconception). You need to create a WILL to distribute your wealth in the manner you want to, and having nominated someone ain’t the answer!

Lets fine out in this article, how to make a will in India ?

What is a Will ?

A will can be made by anyone above 21 years of age in India. You can make the will on plain paper in India. It’s not legally necessary to make the will on stamp paper. It is advisable to write your will in your own hand writing, as the same can be verified later in case of any doubts raised by relatives.

It might happen that according to your family structure and your preferences, you want to divide your wealth unequally or make a provision for a close friend or a faithful servant. This isn’t possible if you die without a will.

A lot of us feel that talking about “Making a Will” is pretty morbid, and hence, we don’t look at it with right attitude.

“A will is a sensitive topic to open up to. People are not comfortable discussing a will in India. There is a misconception that if someone tells you to make a will, the person thinks that indirectly you are telling him that his end is near or that you are eyeing his property. However, all apprehensions disappear when I tell them the consequences of not making a will.”

– Says Shankar Pai, who has done some commendable work in area of spreading awareness on making wills.

How to make a WILL in India and its importance ?

A will is so important, that it should be your first step in your financial life. If your family structure is diverse, and you want to leave your wealth to different members of family like you want to, you should prepare your WILL today, not tomorrow, not later.

To wit, if you die without preparing a WILL in India, your wealth will then be distributed as per ‘Hindu Succession Law’ (Government rules, on how wealth should be divided among family members). A common misconception, is to believe that all the estate is automatically passed on to the spouse, because children and sometimes even relatives can stake a claim to the property.

Laws of inheritance and succession, are complicated and diverse in nature, and are different in case of Hindus and Muslims.

Inconvenience for the family members:

Another point you should consider, is the inconvenience caused to your family members because of your laziness, in not making a will for them. In case of a dispute, your family members have to produce the proof about their relationship with and also have to go helter-skelter to lawyers and spent money and energy.

Much better then, to gift them some time of yours, and creating a will! This will save them a lot of headache.

Watch this video to know why it is necessary to get a registered will:

How do you make a Will in India?

A will has several parts, which duly completed, make up a complete Will. Though there is no legal or defined format, there is a template, which has been generally used for ages. It’s simple, it’s very logical and derives from common sense. Let’s look the whole format and some important points while creating a will.

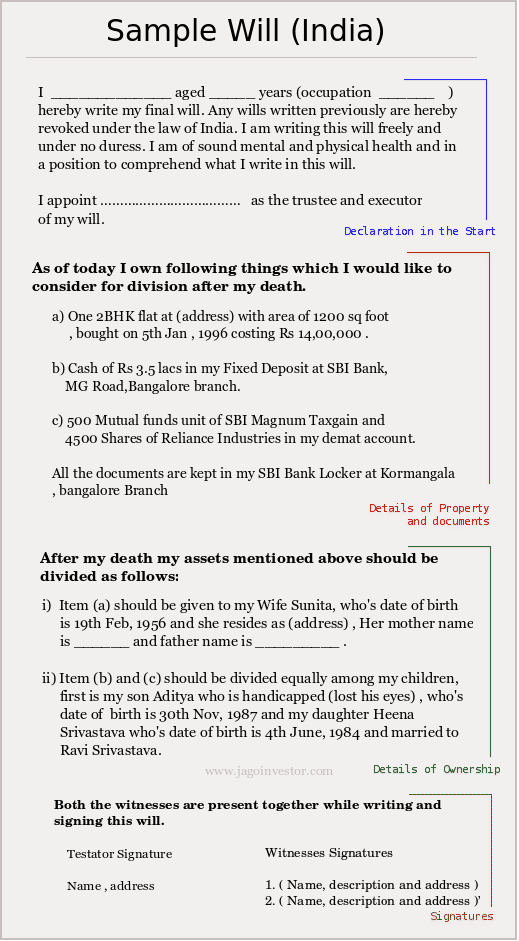

Step 1 : Declaration in the beginning :

In the first paragraph, you have to declare that you are making this will in your full senses and free from any kind of pressure. You have to mention your name, address, age, etc at the time of writing the will so that it confirms that you really are, in your senses 🙂

Step 2 : Details of Property and Documents :

The next step is to provide list of items and their current values, like house, land, bank fixed deposits, postal investments, mutual funds, share certificates owned by you. You must also indicate, where all these documents are stored by you. In all probability, these are in your bank safe deposit box.

Even the will should be stored in there! Make sure, you take the details from the bank manager, about the procedure and rules of releasing your will from the safe deposit after your death. Make sure you communicate it to the executor of the Will or your family members.

I am sure, they’ll be pretty interested in this 🙂

Step 3: Details of ownership :

At the end of the will, you should mention who should own your assets items and in what proportion, after you have gone. If you are giving your assets to a minor, make sure you appoint a custodian of your assets till the individual you have selected, reaches an adult age. This custodian obviously, has to be a trustworthy person.

Step 4 : Signing the Will :

At the end, once you complete writing your will, you must sign the will very carefully in presence of at least two independent witnesses, who have to sign after your signature, certifying that you have signed the will in their presence. The date and place, also must be indicated clearly at the bottom of the will.

Make sure you and the witnesses sign all the pages of the will. One important point while choosing witness, is that they should be your friends, neighbors, or your colleagues and not the direct beneficiaries in the Will. They only certify, that you yourself have signed the will in their presence and are not a party in making the will in India.

The envelope has to be sealed after completing all the formalities and the seal must bear your signature and the date of sealing. The witnesses need not sign on the seal of the envelope.

See another Template from Department of Stamp and Registration, Karnataka here, thanks to Babu .

Execution of Will in Court ?

When you are dead, there is someone called an “Executor” who will be responsible for dividing your wealth amongst the beneficiaries and he will make sure the whole process is smooth (You must have seen this in Hindi movies). It is not legally required to get the will executed in a court of law in presence of a judicial Magistrate in India.

However, if you wish, the will can be executed in the presence of Magistrate or the public notary, nominated by the government authorities and sealed in their presence.

Changing the WILL in India ?

You can change your will any time you want to. However, make sure that when you make a new will, you mention that this will is the latest and supersedes all earlier wills. If you don’t, it can complicate the situation, cause major confusion, make such matters go to the court of law and take several years before arriving at any final verdict.

Making a Will through Lawyer

“Do-it-yourself” wills often do not contain all the necessary components as required by law and many times ruled as invalid by courts (for example no signatures from witness or no witness at all). Many a time, it can happen that while creating the will, you use such ambiguous language that it results in lengthy legal battles (“My House should go to Sunita.”

Now if both mother and wife are called Sunita, which Sunita ought to get it?. Anyone who might benefit from the ambiguity of the will can jump in to claim a share! And if the courts decide in his/her favour, you wont like that situation 🙂 (not that, you’ll be around!)

What is a Probate and it’s importance?

A probate is nothing but a copy of will, certified under the seal of court. The executor (someone who is responsible to execute the will) has to file a probate petition in the court of law and if all goes well, the probate takes six months to a year. No right as executor or legatee can be established unless a court has granted the probate of the Will.

Probate can be granted only to the executor appointed by the Will. The cost of getting a probate includes legal fees as well as stamp duty on the value of the property being willed. The stamp duty varies from state to state. Probate is very important in case of Real Estate.

As per Sundar, a reader of this blog…

Legal heirs to get possession of the property from the nominees have to go through a legal process called probate. In Maharashtra this means, the will have to be submitted to Registrar and one will have to obtain a probate. The Registrar may ask the claimants to put an advertisement in newspaper to ensure that they will not be contested.

They may even ask the witnesses who have signed the will to come to their office and sign documents. After all this, and some court affidavits, the claimants have to pay the necessary tax to the state govt. which is hefty and based on property value. After Goverments takes its cut, then finally the probate order is given. Only then will the legal heirs get their property.

Note that, probate requirements differ from state to state. Hence even when making a will a Lawyer should be consulted. I know of fights between Nominees and Legal Heirs. Roadblocks put up by Goverment ( some times they ask for Registered Will etc.).

So just writing a will is not the end of the story. Better consult a lawyer before drawing a will.

Further please note especially in case of land or house property, the society will not transfer the flat without a probate and tax paid certificate. Many times, a prospective buyer will not buy a flat or land, if the holding is not clear and if the property had not been cleanly transferred and if there are disputes between nominees and legal heirs.

Flat may still stay in the dead person’s name till their heirs and nominees settle their disputes. Till then, the flat may be used by Nominees or any other person. But Society will not transfer the flat to prospective buyer till the process of probate is settled first. Hence such property cannot be sold easily.

Please proceed with great care in this matter.

Important points while making a Will

- If possible, have the two witnesses be a doctor and a lawyer. A doctor signing a will, won’t raise any question of you, being of unsound mind. The lawyer, will vet the will and make sure you dont make stupid mistakes at the time of writing and signing it. 🙂

- The attesting witness and his or her spouse should not be a beneficiary under the terms of your Will. This might create vested interests and some times make your will invalid. Also, make sure the witnesses are younger than you and not very old as your will might be in effect for several years! And you want them to be present in this world 🙂

- Write your will on good quality thick white paper so it doesn’t get spoiled over a period of time. It should be stored in a plastic envelope in full size, without folds.

- Note that you should keep just one more copy of will and stored separately from the original will. The will must be stored very safely in your bank, in safe deposit box. You must also inform your next of kin, as to where you have stored your will. Do not make many copies of your will.

- In case of Hindus, it should be clearly stated if the property is inherited or not, because it makes a huge difference, as no ancestral property can be assigned to any person through a will. All rights on inherited property are acquired by birth. So if you inherited a property from your Father, you cannot say in a will, that you want to assign it to person X only! It will go to all your legal heirs as it is “Inherited”

- A will must always be dated and if more than one will is made, the one with the latest date will nullify all the previous ones. In fact, there should be a statement in your will, nullifying all other previous wills. The pages should be numbered to avoid fraud.

- The value of assets often fluctuates, so it is better to mention how much each beneficiary will receive, in percentage terms rather than absolute numbers. Unless it is pure cash.

So what appeals to you more ? Writing a will your self or hiring a lawyer for this and pay to him ? I hope you are clear about the rules and procedure for writing a WILL in India ?