Some times back I gave my Interview to Ranjan Varma, where I discussed My views on Financial Planning. I also read his views on Why Personal Finance Articles and Advice is Useless?

Personal finance web has increased to a big size in last some years and most of them give useless information. I decided to Find out what do Readers think about this themselves and here are the results.

Results Of Poll

This is the result of the Poll I conducted some time back at this blog with question “Are Personal Finance Articles and Advice Useless”? The results are based on just 74 votes but its quite an ok sample and the results suggest that only 21% people thinks that its of no use but majority (54%) thinks that’s its useful and rest of all thinks that it depends on the person.

I agree with Ranjan Varma on the fact that Personal Finance articles can give you sense of Direction, but its you who have to take Action at the end. This is totally true. Here at Jagoinvestor that’s the reason why I talk on two things HOW and WHY?

HOW

These are the articles which tell you how you do something, How to judge something etc etc . These are Process oriented articles which are important to know but they are not the Key !! . You can get this information from many places . Examples are

See List of other “How to” Articles on Archives Page

Why

There are other Categories of articles which are Psychology oriented articles which make you think which actually answer your question of Why Financial Planning is important .

These are thought provoking articles which will open your mind and make you feel what you are missing from so many years… I hope I am doing it successfully on this blog. These are the type of articles which you can use to do your Free Financial planning but remember that it needs a lot of efforts and time.

My take on the subject is that Personal Finance articles will be useful to someone only when he thinks about his Finance with a Responsible Attitude. You need to ask lots of “Why” questions, you need to know a few “How’s” and a fraction of “Interest” to take care of your Financial Planning.

Lots of Readers have mailed me and told me how they are changing there views about Financial Planning by reading this blog and how there Finances have taken a better shape now… I feel good hearing this.

Please comment on wheather articles on Financial planning helps you and if yes in which manner, which was teh recent action you took, or which changed your mindset about something? I thank all the people who participated in the Poll… 🙂

“Secret of Happiness is low expectations” In this article we will discuss why it is so hard for us to make financial decisions and what factors play role in delaying our decisions?

When we have to make a decision, there are lot of choices offered to us, which makes our life difficult and hence it results in delayed decision. We will see how can we change our thinking and help ourselves to make our decision making a smoother and better process.

We will also have a look at some examples which will make reading this article better for you.

What makes Decision Making Hard?

The top most reason why we are unable to answer decision making questions is having Lots of Choices. As per Barry Schwartz in his excellent talk

When we want to choose a particular product from a group of products, it’s hard to decide because of more choices that we are exposed to. More choices means more data to process and more data to process means less chances of finding the best product that is suitable for our needs.

What is the reason Behind it?

As per Decision Theory: We want to make the best and accurate decision given a lot of choices, because we don’t want to be guilty later when we find that we missed out on the best choice. This is called “Opportunity Cost”. We don’t want to blame ourselves for not picking up the best choice. We often try to avoid that regret which can arise later because of the outcome.

The point to note here is that many a times, just because of the comparison we make, the satisfaction level goes down even though the results are good. Haven’t you felt bad when you saw giving 15% return and others gave an average of 23-24%. But you didn’t ever appreciate the fact that 15% in a year is a good return and you should be happy about it.

Next time while choosing the fund to invest in, you make sure that you buy something which is among the top performers. Watch this Video on how to choose a good mutual fund

He wanted the “best” fund and now compares the list with what he has currently. He should appreciate that what he has is a good fund and can fulfill his requirement… One should try to get the best fund and maximize his returns but if you give your mind and soul for it .. its just not worth it.

Now with so many choices and lucrative offers, it’s too hard for us to choose the best one. Even in my list of Best Equity Funds, you will find it very difficult to choose 1 or 2 funds to invest in. But I gave you just 2 funds and asked you to choose 1 fund. It would be so easy for you because less the choices higher the chances that your choice will be a good one.

Just Imagine a world where there were 2 Term Insurance products, 3 ULIPS, 5 type of Mutual funds and 3 Banks providing Home Loans. What a wonderful world it would have been! I am sure everybody would have a desire of that kind of Environment.

Then we will have very less information to process and there will be less changes of Regret and high chances of Satisfaction.

Do we delay our decisions?

Ask yourself…

Are you not delaying your Investments just because you are not able to figure out which is the best Mututal funds or ULIP?

Are you not trying to find the least rate of interest for your Home loan so that you don’t regret later that you didn’t get the best deal?

Don’t you want to stop your existing mutual funds because now there are other funds who are top ranked and more talked about on television and magazines, even though your Fund returns are very good and it has potential to achieve your goals?

Are you not confused on which stock will move higher and may be don’t invest at all?

There are so many websites, newspapers, blogs out there giving reviews, recommendations about products that a common person’s mindset is now totally confused because of all this. In case you really think you want take your decisions, you should consider Hiring a financial planner?

Is common person really confused or Am I talking Nonsense?

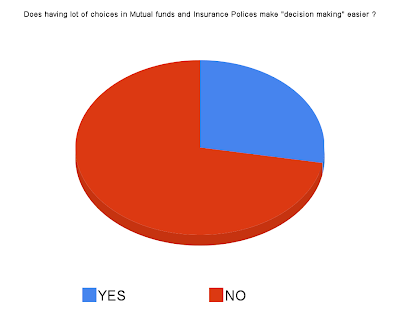

At the time of writing this post at 1:30 in morning… Here are the poll results with 97 votes which I conducted over last 3-4 days and here are the results. 72% people think that “Having lot of Choices in Mutual funds and Insurance Policies does not make “decision making” easier?

In case you are one of the person who voted for YES or NO please leave your comment and let every one know what was the reason for your Vote.

What is the Solution for this Problem?

How to made a decision making process an easy process? It can be to some extent solved using these ideas.

Change your Focus

By this I mean that we are here for achieving our financial goals comfortably, without compromising our family future and smoothly without much tension. That’s the real goal of Financial planning. Once your mindset is set like this, you will automatically not run behind the “best” funds.

What you will try to do is to find out a good product which suits you, just stick to it.

Filter out the Bad policies

Choosing the best product is not an easy task and not worth too. The easy thing would be to filter out the bad products which is easy to do! So in mutual funds you already get rankings and lists of top 10 or top 5 funds or Best policies from ULIPs or good Home loan from a Bank.

I would say they are worth a look and finally you should decide soon enough on one of them but for this you must have shifted your focus from choosing “best” product to “a suitable” product. People who want to Buy good mutual funds for long term can Choose any one of mutual funds listed in my article on Best Equity funds for year 2009.

Think Less and concentrate more on Fundamentals

There are more Important things than Best timing and Best product which you have to concentrate on. One of them is Consistency in your Investing and your Plan, your Asset allocation, your Diversification. Once you concentrate on this and forget all other materialistic things, it would be a more peaceful activity to manage your Finances.

Conclusion

So we can say finally that it was never like this before. Now a days we have too many things to choose for which has made like worse than even. Hundreds of products do exactly same thing but they all claims to be better than another. We have to narrow down our choices and choose any one of them and not try to hunt for that exactly best product for our self.

Readers, please share your experience of being in a situation where you had to think a lot before making a decision or had to delay your decision. What are your suggestions on this problem? Please post comment.

We will discuss about LIC’s Jeevan Tarang Policy today, One of the readers asked me my review about Jeevan Tarang in “Ask a Question” Section.

I thought it would be a good idea to discuss it with every one here. So lets see Whats the policy and lets evaluate and answer the question “Is Jeevan Tarang worth consideration or Not”? Also see How can we beat this Policy by huge margin.

Jeevan Tarang Policy Highlights

Jeevan Tarang is a Whole Life Plan from LIC, Whole life plan means that you are insured for whole life (max age 100) The plan offers three Accumulation periods – 10, 15 and 20 years. A proposer may choose any of them. This is the Tenure by when your Policy Matures.

Whenever you die, you will ge the Sum assured and then the Policy Expires. This policy will expire if you are at age 100.

If you Die before the Maturity, you will get the Sum Assured + All the Bonus Accumulated till date.

The yearly Premimum will depends on two things, your Tenure and your Age. It can range from 11% (Policy for 10 yrs), 7-8% (Policy for 15 yrs) or 5-5.5% (policy for 20 yrs).

For exact numbers see here. The percentages are with respect to your Sum Assured, 5.5% premium means 5.5% of your Sum assured. so Rs 10,00,000 of Sum assured means 55,000 of Premium each Year .

Incase you surviuve till your Policy Tenure, then at the end of your Tenure, you will get Bonus accumulated (not the Sum assured) and an annuity of exact 5.5% each year after the Policy Matures. One will get 5.5% of the Sum Assured each year till his death or upto age 100 whichever is earliar.

If you can not pay the Premiums and want to stop the policy (only after 3 yrs), you have two choices, either make it a Paidup policy or take back the Surrender Value. This is explained in detail later, so move on.

These are the main basic and approximate points of the Policy, for exact detials see the policy page at LIC website.

Let us now see an example with different Scenario. This will help you understand it better. Read Important of Life Insurance

Now let take Scenario’s

Ajay’s age is 30 and he takes Jeevan Tarang Policy for a tenure for 15 yrs with Sum Assured of Rs.10,00,000 (10 Lacs). His Yearly Premiums will be 71.40 for every 1000 sum assured, which is 7.14%. Which comes to 71,400 per year.

If Ajay dies before 15 yrs

In this case he will get Sum Assured + Bonus Accumulated till date. The Bonus amount is not fixed and we can not tell how much it will be now , But on LIC webpage its mentioned in range of Rs 20-88 .

Lets take a good figure of Rs 30 . In that case Per year it would be 30,000 more . So If he dies in 8th year , it would be 10 lacs (Sum Assured) + 2.4 lacs (bonus for 8 yrs) = 12.4 Lacs and the policy Expires .

If Ajay survives the Policy and does not die at all

In this case, Ajay will pay his premium upto 15 yrs and then in 15th yr, he will get back the Bonus accumulated (not sum assured), so may be it would be 4.5-5 lacs assuming Rs 30 as Bonus for every 1000 SA. Also he will get 55,000 per year(remeber 5.5% of Sum Assured) as annuity till he dies or upto age 100 .

He will also get Loyality additions , this will again be a very small amount just like Bonus , but this is not assured at all. Read this for same concept : Term Insurance with Return of Premium

If Ajay survives the Policy and Dies Later.

Its almost the same case as above, in this, Ajay will get Bonus at the end of 15 yrs and then He will start recieving 55,000 ever year. And suppose he dies before age 100, he will receive the Sum Assured of Rs.10 lacs and thats it .. The game is over and then LIC doesnt recognise him there after.

Ajay is not able to pay premiums because of some problem and wants to stop.

This is possible only after 3 yrs of taking the Policy, If he wants to stop it before 3 yrs, then sorry buddy, just forget your Money and go home cry. If its after 3 yrs, then He has two choices

Make the Policy Paid up : In this case, you stop the Premium payments and you will get your Premiums and Bonus Accumulated will date at the end of the Maturity. You Sum assured will also reduce in Proportion to Premiums Paid, so if you stop the policy in 6th year, your Sum assured will reduce from 10 lacs to 4 lacs (40%), as you have paid the premium only for 40% of the tenure (15 yrs), thats 6 yrs.

Take your Money Back : After 3 yrs of completion, the Policy acquires a Surrender value, generally its the Net Present Value of money in todays term what you are going to get at the end. See this post on Net Asset Value. So if you are going to get 5 lacs at the end of 15 yrs and todays worth of that money is 2 lacs, you will get 2 lacs today.

Watch this video to know about other features of this policy:

What is the Return of Jeevan Tarang Policy overall ?

Even if you receive all the annuity upto your age of 100 , the CAGR return for this policy using IRR Analysis comes to mere 4.72% .

I have taken the above example and assumed 5 lacs of Bonus and no loyality additions , even if we consider 7-8 lacs of Bonus and Some loyality additions, the CAGR return Does not cross 6% CAGR .

Why this Policy excites people and general people get fooled?

These kind of Endowment policies make sure that you concentrate too much on numbers and it traps your mindset in the present moment , One who is able to forsee beyond “now” can understand the real value of these Policies .

We concentrate on numbers, If we get something for a long time and we pay for less time, it appeals to us, and hence this policy takes care of that very beautifully, You pay for 10, 15 or 20 yrs and you get back till you are Age 100, Sounds great !!0

Psychologically our mind is programmed by nature to think about the best case for ourself, but how many of us will survive upto 100 yrs to get annuity back, The average person thinks emotionally , Insurance Companies work on Data, Statistics, probability Theory and complex calculations, which tell them that average person will die at 60-70, and only 1-2 will survive till 100 years of their age.

Most of the people see Numbers and Present, The policy will demonstrate how much You will get at the end of the Maturity but it never tells you how much will it be worth then and how much will it help you in your Financial goals. We never think that Rs.100 today can buy much more than Rs.100 after 15 or 30 yrs.

We know this somewhere inside us, but out mind just doesn’t feel everytime the same way, that’s the reason you need to calculate things by hand, on paper or computer and do some small analysis like I did on this article. Then you get the clarity

Trust and Blind Faith, We trust companies because they have been in existence from long time and our parents were made to believe that these are the best friends in our life, they will protect our Future. Love and “Taking Endowment Policies” in India has similarity.

I grew up hearing Love is Blind and experienced it too, and I feel that its same with Taking Endowment Polices. People just take it blindly, some new Policy comes up and bang !! It has to be great, no matter what, because it comes from the GOD company !!

Why age 100? How many people are going to live upto age 100 , why putting that number at 100, why not increase it to 500, even though life expectancy is just 60-70. Not more than 1-2 in 100 live upto 100.

In case of Ajay, if his monthly expeses is 30,000 (considering married, even though I doubt he will ever get any one), after the accumulation period of 15 yrs, he will start receiving yearly pension of 55,000 per year, read it again, 55,000 per year, but now after 15 yrs, even with 6% of inflation his monthly expenses has gone upto 72,000 . And his policy pays him 55,000 which cannot even take care of his 1 month of expenses . Now i can see him pulling all his hairs .

If he is dead at age 70 , His family would get back the Sum assured of 10 lacs and at that time , it can only pay for his family’s 3-4 months of expenses and his Funeral cost , thats it .. Aha .. atleast something , so one this is confirmed , There will be no financial burden , pun intended .

This is the question which we should always ask in every situation of our life, not just Financial planning. Lets take care of Ajay’s situation in Jagoinvestor’s way and plan him something better than Jeevan Tarang.

With Rs.71,600 per year to pay for 15 yrs, lets see what can we do.

First thing First, Lets cover his Family first from the Mis-happenings of life an secure his dependents, Lets take a Term Insurance of 50 lacs for maximum tenure of 30 yrs, Premium would be close to 13k or 14k approx, lets assume 14k. So out of 71,600, 14k is gone and we are left with 57,600.

Now lets put 21,600 each year in PPF for 15 yrs. We are now left with 36,000 to invest, we will start Rs.3,000 SIP per month (Rs 1000 each in 3 different Equity funds) for 15 yrs . See list of some good Equity Mutual funds for 2009 .

PPF will accumulate to 6.3 lacs in 15 yrs and Mutual funds will accumulate to 15 lacs in 15 yrs assuming a pessimistic return of just 12% (Historical return has been more than 17% and last 5 yrs return are more than 25%). Lets assume just 12% and not 18-20% even though its possible because our aim is to do better than Jeevan Tarang and achieve our goals and not compete with some one.

So total amount will be around 21.3 lacs at the end of 15 yrs. Now lets visit and see our Scenario’s again and hows does it compare now.

If Ajay dies before 15 yrs :

Gets 50 lacs from Term Insurance and also the money from PPF and mutual funds, which will be more than 50 lacs 🙂 . We beat Jeevan Tarang by huge margin in this case.

If Ajay survives and Does not Die at all :

In this case he already has 21.3 lacs accumulated and now he can use this amount to buy an Annuity which will pay him more than 1.6 lacs Per year, much more than what he was getting in LIC policy.

As a toppings, he also has a 50 lac cover for another 15 years. We can generate 3 times more annuity than Jeevan Astha here, again beat by huge margin.

If Ajay survives the Policy and Dies Later :

In this case if he dies in next 15 yrs , his family would get 50 lacs from Insurance (10 lacs in LIC), apart from this he will have his 21.3 lacs growing every year.

If he dies after 15 more year, There will be no Insurance money, but his money would have grown a lot by now .. If he dies after 15 yrs (total 30 yrs from starting), his money would have grown to 1.17 crores assuming 12% return per year (no annuity every year). and if he dies after 25 years (total 40 yrs from starting , means at age 70), his money would have grown to 6 crores.

Now incase you don’t want to faint, don’t ask me how much would have he had if he lived till age 100 and left his money to grow, Its 13 crores 🙂 . I have not assumed any annual annuity here, we can do that but the result would remain almost same. We beat Jeevan Tarang by hugest margin in this case. See how we can create Wealth using Equity in Long term.

Ajay is not able to pay premiums because of some problem and wants to stop.

His money will still be in PPF and Mutual funds and keep growing, there is no liquiditity issue with Mutual funds, he can withdraw from mutual funds anytime, even from PPF he can withdraw partially.

If he has limited money, he can at least pay his Insurance premiums and still get covered for 50 lacs, no big deal there. In every aspect it beats Jeevan Tarang

Note : For doing better than Jeevan tarang we have invested in Mutual funds which are risky instruments , but anyways we are not in great position with Jeevan Tarang .. so taking risk is worth it . If one is too concerned about risk , then even plain PPF will be better .

Conclusion :

Think Logical , Think mathematical , Think smartly and at last THINK !! .

Note : The figures have not considered the rebate provided by LIC, and hence the actual figures can deviate a bit from the actual numbers used here, but it wont be significant and the review still holds . ahh .. tired now !!

Sometime back, I had a Financial Planning Survey on “Where do you place your self on understanding and knowledge of Personal finance and Financial Planning”.

In total 96 people participated in the poll. Let’s see how the result compares overall. What were the results and what is the reality and what reasons are connected for this behaviour.

Comparison of Data

Let us first look at the results. In the above two pie charts you can see that Most of the people placed themselves in “Much above the average” and “Above Average” Category. That is 60% of total participants and only 40% people placed themselves “Below average” or “No Knowledge at all”.

From my experience, understanding and logic, majority of people are Below average in Financial Planning Advice. I think it’s around 80% and only 20% will be above average with a handful really way above the average. A huge chunk has to be below average but most of them have put themselves about as ‘Average’.

What is the Reason for this?

overconfidence and overestimation of their knowledge. For example they will argue about why not to take Term Insurance but they dont know that they are wrong

There can be other reasons as well but these are the top reasons.

To get SMS Alerts from Jagoinvestor, Click Here

What is the Effect or Result of this Thinking?

Most of the people live in the belief that Financial Planning is something they can do themselves without any profession help and hence mess it up at the end. They do not understand the Goal of Financial Planning

It causes delay in there Financial Planning and hence the situation becomes worse. They don’t get better “financial planning advice” because of this. They don’t understand how to figure out if a Financial Product suits them or not

Basically its a comparison between “Thinking” Vs “Reality”. I must admit that this blog is getting a lot of readers who still need to learn a lot to manage their Personal finance in a better way. Read “Do you need a Financial Planner ?”

Question: What do you think about this post, why do you think most of the people ahead of others? Is it Reality or just a sense of disagreement that you are not ahead of others.

BankBazaar.com is an excellent one stop destination for all your loans and insurance products Needs . BankBazaar is partner’s with India’s leading financial institutions and insurance firms, and provide all information at one single place in a very user friendly manner .

Lets see in detail what all it has to provide a retail investor like you and me in India .

If you are a Fan of Jagoinvestor , Fill the Fan book to tell how much you like it

What can you compare at BankBazaar.com

Home Loans

Personal Loans

Home Loan Transfers

Loan Against Property

Credit Cards

Home loans section is my favorite and I am really amazed by the level of detail they ask and based on that they suggest you the best Bank suitable for you .

Anyone going to take a home loan should first go thorugh this to get an idea about it . The best part I like in BankBazaar is cool Scale type Amount and Duration Selector .Also check out there amazing EMI Calcualtor . Read an article explaining how to choose best Fixed Deposit for you .

Personal Loan is another section I like , You can find same kind of comparision calculator at many sites , but bankBazaar really goes in detail and takes care of all the details which your Bank will ask anyways at the time of Application .

Loan Against Property This Calculator will take all your inputs and let you know how much amount are you eligible for taking Loan and for how much tenure . It will give the list of Banks which will provide the least interest to you .

Credit Cards This is for getting the best Credit card offer for you.

Are you on Facebook ? Join Jagoinvestor Community on Facebook

Overall I think its the best place at the moment to get information on best products available on Home Loans. I hope to see many other things on Bankbazaar over time .

We talk about Financial planning on this Blog. Today let’s see in this article what is the goal of Financial Planning? More importantly what Financial planning is not!!

Most of the people think that Financial Planning is about getting great returns and about Finding the best Insurance for yourself and about having better than average knowledge about Finance and Investments. But in reality they are small components of Financial planning and the core of it is something else.

Why do we come to this World?

Let us answer some basic questions in life. Why are we in this world and what is our life’s Objective ? Why are we working hard with the jobs we have , For a moment just ask yourself , why are you here on this blog?

Is your sole objective or goal in life is to Make a lot of Money?

Is your purpose in Life is to choose the “best” mutual fund , so that you don’t miss that 30% return next year , and you don’t want to compromise with just 26-27% return which other mutual fund can also give?

Is your Purpose in life is to save 10,000 (not more than 3-4% of your Annual salary) by not buying Term Insurance to cover the risk of your Family?

Why do people ask me which Stock will go high in next week and they should but it.

At the end, Ask your self what is the top fundamental requirement in your Life, What do you want from your life, I will answer it for you if you are confused.

We are here to be lead a Happy and Healthy Life .

We are here to be with our loved ones and share little moments of life with them

We are here to fulfill our Basic dreams in Life first

We are here to fulfill out desires in life after our Basic Requirements are met

We are here to make sure that our children get Good Education and we are able to provide them whatever they want comfortably

If that is the case, the right Question to ask our self is “How should I make the most of my situation and Plan for things which will help me achieve my Financial goals easily and comfortably, without risking too much ”

What is Financial Planning?

So this is how I will define Financial planning

Financial Planning is deciding a road map for you self and deciding in advance how will you invest your money which helps you achieve your Financial Goals in life comfortably.

Financial Planing will give you a Path on which you just have to walk overtime because you have decided and planned everything in advance . Financial Planning is about Consistency. It’s about having a vision. It’s about promise to yourself that you will follow the plan with discipline.

Its not about getting 30% or 40%, its about getting X% which will help you achieve your goals easy enough without compromising and exposing you to unnecessary risk.

This this case , you have to do just follow the plan , Just invest 2k every month consistently and review your Fund performance every year once [See this calculator to calculate it for your goals]. If they start getting bad , shift to some other good fund.

Just imagine how easy and comfortable this situation is! If you can little more risk you can do that but not too much.

Choice 2: You are ready to invest 2k per month but here you want the best mutual fund- one which gives 25% or may be 30% return. Now the point is, may be this Mutual fund returns you a lot of money, may be more than what you wanted BUT, it also may go up and down too much in short term or long term because of the risk it exposes you to.

Are u ready to take that risk of not meeting your financial goal? I would also agree that the chances of that case it too small but why to take even that risk when you have the other way where you can achieve it without any risk?

If you are a Fan of Jagoinvestor, Fill the Fan book to tell how much you like it

Short term goals

People concentrate too much on Buying the Excellent Mutual Fund? May be people do not understand meaning of “Best Mutual Fund”.

So let me declare what is meant by best Mutual fund: the best mutual fund for you is the Fund which suits your requirement and has ability to help you achieve your Financial Goals without risking your money! Some days ago I posted about “Best Mutual Fund for 2009”, now does it mean, that you go and buy it just because their returns are too high? NOT at all!!

All these mutual funds gave negative 40-50% return in 2007-2008. What if you had 1 lakh today and wanted to save that money for your Child Education which is payable in next 1 yr , suppose you need to pay 1 lakh only after 1 yr or may be 1.05 lacs.

In this case your “requirement” is Safety and not growth of your money. Will you go and invest in those mutual fund for the reason that they are excellent funds.

Will you not take into consideration that if they go down your 1 lakh will go down to 50-60k and in that case it does not suit your requirement. You have to understand that they are linked to Markets and may not suit your requirement.

Long Term Goals

If you are planning for your Retirement and saving a decent amount of money every month then all you need is return that is close to 12-15% CAGR [Learn What is CAGR], which is achievable in long term if you just invest in mutual funds through SIPs.

In that case how does it matter if you invest in “Rank 1” Mutual fund or “Rank 5” mutual fund? I am not saying that you should not try to find good Mutual funds but shift your Focus from “buying the best mutual fund” to “Buying a Mutual fund which will help me achieve my goals”.

Conclusion

I would conclude this article by repeating the same point that Financial Planning is not at all about getting great returns or beating your friend’s portfolio performance or doing better than average.

It’s a personal thing and totally relevant to you and to your needs and your Financial Goals. Its about having a predetermined plan or strategy to make use of whatever money you have in a hassle free way.

Getting great returns or doing just better than average is not a very significant part of Financial Planning.

I hope all your doubts must have cleared by now. If you still have any then leave your query in our comment section.

I am 25, single and my parents are my only dependants. My Dad is aged 65 and mother is aged 55. I have a Group Health Insurance Plan from my company which is given as a part of my compensation package. The insurance cover is for 4 lakhs (2 lakhs for self, one lakh each for my mother and father).

Given the features of the plan and my current need, the coverage of 4 lakhs is sufficient. But, I don’t have any other health insurance plan. Should I go for an additional plan, personally? I also assume that I would be given similar health policies in all my future jobs.

Answer

This is often a question in people mind , you say 4 lacs cover is sufficient , what if you had 10 dependents ?

Then each one would have 1-2 lacs cover and would you say 10-20 lacs is sufficient , what you must see is how much is “each person” cover, For you , its 2 laks , and for your parents its 1 lakh , now this logically , what is chances of you getting any health issue than your parents who are old (55+)

So the real situation nails down to this . Parents has 1 lakh of cover each and they are Old (probability of health issue drastically high compared to you) .

Now there is another issue , which is psychological , people think that chances of bad things happening to them is low than others , which is totally baseless . God forbid , but suppose there is some surgery or any health issue , you can imagine how much does it cost these days .. Lakhs of rupees .

Conclusion :

U should seriously consider covering your parents, Because of old age your will face some issue getting health cover now, also the premiums will be high (good enough), now its you who have to decide if you want to save those premiums (which can go waste, as some logical people declare) or pay the high cost of Hospitalization or Surgery or whatever when it comes, but save those premium . your call 🙂

Question 2 # by Taranprit Singh

I am beginner in this stock world and doing trading just for earn money, money and only money. I can say I am doing good in intraday trading of equities. Now I want to enter in future and options but the problem is I have ZERO knowledge about them, so please it’s my humble request to give proper guide for the same by which I can understand FNO easily.

Answer

I want to congratulate if you are making money in markets with intraday, Keep it up. But !! if its just 1 week or 1 month that you have made money then wait, It can be because of luck or market may not have shown its real face to you.

I would suggest you to keep trading for 1 yr and see all the faces of markets, believe me, 1 yr is minimum time you should trade to see if you can do it consistently 🙂 . Take the greed out of your mind to make lakhs and crores using F&O. I am experienced enough to say that it would kill you badly if you jump into it.

I would suggest you this.

Keep trading the way you are doing and see if you can do it consistenely for 6 months

Once you succeed in that, then keep trading and slowly learn F&O, buy books and read on Net, practice a lot.

Paper trade F&O trades , don’t jump into it with money

Once you succeed, then do some real money trades with small money, Grow slowly 🙂

If you are a Fan of Jagoinvestor , Fill the Fan book to tell how much you like it

Question 3 # by (Name not allowed to Disclose)

Have taken a new Aviva Lifeline,whole life plan(its still in free look period),i want your opinion abt it… details, Annual premium: Rs.25,000 Premium Policy Term:20years Policy term 72years (i m 28 years – 100 years policy max years) Invested Amt(for 20 years) Rs.5,00,000 Expected Return at 6% is Rs.8,00,000(at the end of 20 years) is this plan good from normal middle class person(of salary of Rs.15,000 per month) point of view?

Answer

Lets not ask a question “Is it good or Bad”, let us ask a question, Can we do better than this ourselves with simple things.

Equity Returns over long term have been more than 17%. Good Mutual funds over 10 yr of history have returned somewhere around 20%. If we think about future and assume even 12% return over long term, Your investment of 25k per year will become 20 lacs after 20 yrs.

>>> 25000 * (1.12)*(1.12 ** 20 -1)/.12

2017468.

If you think aggressively and assume 15%, it would be 29 lacs after 20 yrs

>>> 25000 * (1.15)*(1.15 ** 20 -1)/.15

2945253

At 6% , it comes out to be 9.7 lacs

>>> 25000 * (1.06)*(1.06 ** 20 -1)/.06

974818.

The reason why you were told 8 lacs is because of the charges and may be some mortality charges for penny insurance you might get there. Check it yourself.

Even if you take a term insurance of 30 lacs yourself now, it will not be more than 10k per year, remaining 15k you can invest in 2-3 good mutual funds for long term. at the end of 20 yrs, you will have at least 12 lacs assuming 12% return. Apply logic and maths and that’s it, you are your own financial planner 🙂

So my suggestion : Break this policy before the free look up period, and take what you get back, the amount spent on medical exam if any will be deducted.

Question 4 # by Vikas

I am 35 and haven’t had much opportunity to invest till 33 yrs. Now I have invested some funds in MFs (DSP Equity, Magnum Contra, DSP TIGER, HDFC Prudence and Sundarm Tax Saver).

I don’t have an established career and have taken any suitable opportunity that came along my way. Off late, I am jobless but have strong desire to start something independently of my own. However that “something” is what I am searching for.

I have to start small with no doubt due my financial restraints, but I know I have special liking for computer related jobs, exports, something creative like handicrafts etc.

Could you please suggest some books or articles or links or your own opinion how to translate this ” virtual something” in my mind to “real something”. I am absolutely sure if i strike the right chord, nobody can stop me, I have worked so hard for others in my regular job so I don’t see why I cant put my “everything” to get that elusive “something” 🙂

Answer

Great .. All the mutual funds u have are nice ones and keep continuing in them . Regarding converting your “virtual something” into “real something”, I have this to say confidence in yourself is amazing and worth appreciation.

To find out what you want to do, you may have to try out various things which may fail in start, but you need to have enough reserve of confidence to tell yourself that you will get it someday. “Making mistakes is a privilege which Unsuccessful people don’t get in life”, I said this one day to my friend and realized what a nice quote I made 🙂 .

“Believe in it.”

Most of the people are doing jobs which they hate or cant excel at, just because they don’t have that guts to start some thing on their own or change their jobs, you are much ahead of them, congrats on that.

Meet new people , try some ideas and make a list things “which you don’t want to for sure”. Prune out the things you don’t like. That would be a better way for finding what you want to do.

“One important thing” –

We many times think that just because we have lot of confidence and desire to do something on our own will make u succeed, but there are something which have no substitute like Hardwork, spending time reading about what we like, Jagoinvestor was not build in a day, or a month, It needs work and patience and confidence that it will succeed.

There have been instances when I wrote 20 posts in a row after doing so much reading and hardwork, writing in night, but there was no comment which said “Nice job”, that is kind of heart breaking sometimes and makes you feel that “You are going no where”.

But what you need is the “belief” that things will turn out well at the end, just do your karma and results will come, and when they don’t come, just get out and accept it and be ready to move one just like it happens in Trading or Relationship. Its all the same thing at the end.

I did Trading in Markets (options) and failed like anything.

I am still learning and my confidence and belief in myself does not allow me to quit. Best of luck to you in trying to find your way. Don’t get underestimated by the failures . Failures will come and they will teach you more than your success .

Its only the times when you feel like quiting is the time when you really need to keep up yourself. “Difference between Coal and Diamond is that Diamond takes a little extra pressure”, So don’t let that extra pressure make you quit 🙂

Which is the best Equity Diversified Mutual Fund ? . I am going to list down some of the best Mutual funds which I have figured out from Valueresearchonline.com . I am listing down 6 Equity Diversified Mutual Funds and 3 Tax-saving Mutual funds . I will highlight the main points of Mutual funds like its History , its performance and its Portfolio Allocation.

Best Equity Diversified Funds

These funds are suitable for people who are looking for long term investments and are ready to take the risk of mutual funds .

4.5 year old fund , Return Since Launch is 22.5% even with the bad markets.

Good 3 yrs return at 16.5% beating its benchmark by 7% .

With close of 75% Portfolio in Midcaps and Small cap makes its Fund with heart of real Risk takers . Don’t get into this if you don’t like messy markets . It can take your heart our of your body and play hide and seek with it .

These are tax saving Funds , used for saving the tax under Sec 80C upto Rs 1 lac . Suitable for investors who want to invest for long term and also require tax saving .

This one is the quite genius who does not shout much about its achievement . Not much appreciated among its peers but has one of the best long term track record which has ability to put all the tax saving funds in shame .

One of the oldest Tax saving Funds with 13.5 yrs of excellent track record.

Return Since Launch is 34% which is an unmatched achievement in itself .

Close to 29.5% returns in last 5 yrs beating its benchmark by 6% .

It is now becoming more aggressive by increasing its allocation in Midcap funds .

Note : This is not an exhaustive list of Good funds . There are many good funds which are not here . Its just a Compilation of funds which I personally feel are good ones and have ability to perform in Future . All the funds have high Equity Allocation and can be very risky . You should invest in these only after understanding your Asset Allocation and Risk-appetite to handle the ups and downs of its performance .

I will come up with the compilation of some good Sectoral Funds , Debt Funds and Balanced Funds later . Watch for it 🙂

Comments Please and let me know which fund is your favorite and why . If I had to choose 1 fund , it would be Sundaram Tax Saver because I did a detailed Analysis of it myself and It went ahead of SBI magnum which had number 1 position from long time .

ICICIDirect has revised its brokerage charges for Mutual funds Investments . Some time back SEBI abolished mutual funds entry load , In this post we will see the new charges by ICICIDirect and analyse if its good or bad . The new revised charges look good to me . In case you don’t know what is SIP , Read here

So ICICI Direct came up with this Rule . If your Mutual Funds portfolio with them is

Your Mutual Funds Portfolio Above 8 Lacs with ICICI

So , it means you can just invest through ICICI Direct website and your brokerage would be Nil and you wont pay any thing in charges .

Your Mutual Funds Portfolio is Below 8 Lacs with ICICI

You will have to pay lower of Rs 30 or 1.5% of the amount each time if you go for SIP . On a lump sum investment , you will pay Rs 100 .

Is it Good or Bad ?

If your SIP payment is High

This revised charge structure will be very good for you if you are making Higher SIP payments like 10,000 . In that case your charges would be Rs 30 each time , which is 0.3% , which is 87% cheaper than earlier cost (2.25% entry load) . Even with 5,000 SIP , your charges would be .6% , which is much better than what you were paying earliar and this all with the convenience of doing everything online yourself .

If your SIP payments are less than 1,500 , then your charges would be 1.5% , which is near 2.25% , what you earlier paid, you are still benefiting , but not to great extent . Now its you who have to decide

if you would like to go with direct Mutual funds investing yourself (without any charge at all)

You can find some other agent who charges less than 1.5%

You are ok with 1.5% charges and comfort is more important to you .

Suggestion to people who have lot of Mutual funds in your portfolio

In case you have too much mutual funds in your portfolio and your SIP payment in each of them is small , the better thing would be to prune out most of them and consolidate your mutual fund portfolio to maximum 5 funds and better to more payment in each , for example if you have 15 mutual funds of Rs 1,000 each , change it to 4 mutual funds with 4k payment to each or Something like that . It will help in management of funds also and also help you reduce the charges .

There may be some other agent or web portal who are not charging at all for mutual fund investments through them . For people who are yet to open a Demat account and also looking for Mutual fund investments , Opening a ICICI Direct Demat account may be worth looking into .

What is most Important

Don’t try to put too much thinking in this , less charges are good , but its not the main thing , you must concentrate on your Asset Allocation and Portfolio Rebalancing and choosing a good mutual fund for you . So if you getting a good advice , its worth to pay good fees for that , don’t try to save that small amount just for saving it .

Please comment what do you think about this ? Do you know of some other alternative route through which the commission will be better than this .

There is going to be some really big changes in Taxation laws if “Direct Tax Code” comes into existence year 2011. There are some big changes proposed in the Draft which if implemented will be the biggest ever change in Tax laws and will impact people in a big way.

Let us see what are the changes Proposed and How they will affect you?

What is Direct Tax code ?

The Finance Ministry has released a new draft direct tax code, which is a document containing changes in Exemptions, Tax slab. This will be a big change to four-decades old Income Tax Act . As per the proposal, the new tax slab would be

0% : Less than 1.6 lacs

10% : 1.6 – 10 Lacs

20% : 10 – 25 Lacs

30% : 25+ Lacs

This sounds really amazing that almost 90% of Indian (tax payers) will then pay 10% tax because majority of the income earned will be below 10 lacs (that’s very obvious). We will a comparison at the end. Don’t Worry 🙂

If you are a Fan of Jagoinvestor or Manish , you might want to fill up the Fan book

Other Major Changes which can affect a Common person

1. Tax Exemptions upto 3 Lacs

At present we get exemptions upto 1 lac under section 80C . This may be raised to 3 lacs . This will encourage people to invest and help.

2. Proposes tax on Maturity amount from Insurance Policies, PPF, EPF and GPF

This is a big turnoff. So as per the new draft, the amount you get on maturity from your PPF, EPF or Insurance policies will be taxable, just like NPS right now. As per the proposal, the amount accrued till 2011 will be non-taxable, this will be applicable to all the proceedings after 2011. So some relief here.

3. Interest you pay for housing loans cannot be exempted and your tax burden increases.

4. Recommends Long term capital gains tax to be reintroduced and Short Term Capital gain tax to be added in Income

Enough is Enough- is what you may be thinking. 🙂 But tax on long term capital gains may be introduced which means that you will have to pay some tax on that profit from Mutual funds or Shares which was tax-free after 1 yrs. Short term capital gains will be added in Income and taxed at applicable rate.

Also Short Term capital gains would be before 3 yrs and Long Term capital gain after 3 yrs. Long term Capital Gains will be less than regular tax slab, I think around 10% or 15%.

5. Suggested abolishing the Securities Transaction Tax (STT)

So the STT which was paid while buying shares will be abolished. Currently when you buy shares you pay a small tax called STT which is included in share cost by your Share broker, this will be no longer there 🙂

6. Perks now will be included as a part of the income for purpose of tax calculation, so tax burden may be sightly more.

All the perks you were getting from your employer like interest free loan, free lunch etc will get added to your income and be taxed.

7. Lowering Corporate tax to 25% from 30%

This will cheer up companies as their tax burden would reduce. I am not sure about its impact on common person.

Watch this video to know more about direct tax code:

Comparison of New Vs Old Tax Code

Lets see an Example

Name : Ajay Patel

Salary : 8 lacs per year

Investments : Investment of 30k in Mutual funds, 30k in EPF, 20k in PPF and 20k in Insurance Policy.

Home Loan : Taken a Home loan and pays 80k as Principle and 1.4 lacs as Interest.

Tax as per Current System

Amount Exempted = 1.4 lacs as home loan interest + 1 lac in 80C = 2.4 Lacs

Taxable Income = 5.6 lacs

Tax = 14k (10% from 1.6 to 3 lacs) + 40k (20% from 3 – 5 lacs) + 18k (30% on 5 – 5.6 lacs) = Rs.72,000

Tax as per New Tax Code

Amount Exempted = 1 lac from (mutual funds , PPF , EPF , Insurance) + 80k as Home loan principle = 1.8 lacs

Taxable Income = 6.2 lacs

Tax = Rs 44,000 (10% on 1.6 lacs – 6.2 lacs)

Note: Your Tax Liability will be totally different and can vary a lot depending on the your condition and financial commitments. Don’t take this one example personally as its just for demonstration purpose.

Is New Tax Code Good or Bad

This is an important and good question. I will classify this tax code as a good one the biggest thing to note in this is that the tax slab is just 10% for income from 1.6 lacs to 10 lacs. There are many changes in the new tax code which may look bad and hurting but at the end you will gain from it because the tax charged will be just 10%.

So your taxable salary will go up because of some changes but your tax liability will actually reduce. It will not reduce too much though but surely it will be a reason to cheer up.

The biggest doubt is that over long term if my Maturity amount from Mutual Funds, Insurance policies and PPF will become taxable?

Then YES! But now you will save more to invest. So, even if we assume 20% tax charged at the end, we need to invest 25% more than we usually do to gain that will happen I believe… Anyways, this is now a debate topic and can be argued upon.

Download the Full Direct Tax Code Bill 2009, Click Here

Conclusion

This was just an analysis of the proposed DTC and how the changes can impact if it is approved. But for now, its just a proposal so don’t panic. Lot of debates and discussion will happen on this and this can take totally new direction or may be it does not happen at all and we continue with current tax system.

Comments Please as I would like to hear your views on New Tax code and how can it impact you. Do you think its a right thing to do and what are the issues involved with it? Did you like it?