Child Education is one of the biggest goals of parents these days because of the tough environment and high expenses involved.

Most of the parents start saving for Child Education right from the birth of Child, which is a great! In this post we learn how you should evaluate the target cost of Children Education and how you can achieve the targets within expected deadline. We are mainly talking about Higher education in this article.

Many Companies come up with Child plans and other products which are nothing more than ULIP’s bundled with special features like Wavier of Premium option and some other features. However Planning for Child Education is not a big task and you can do it yourself, given you have some interest and eagerness to do it.

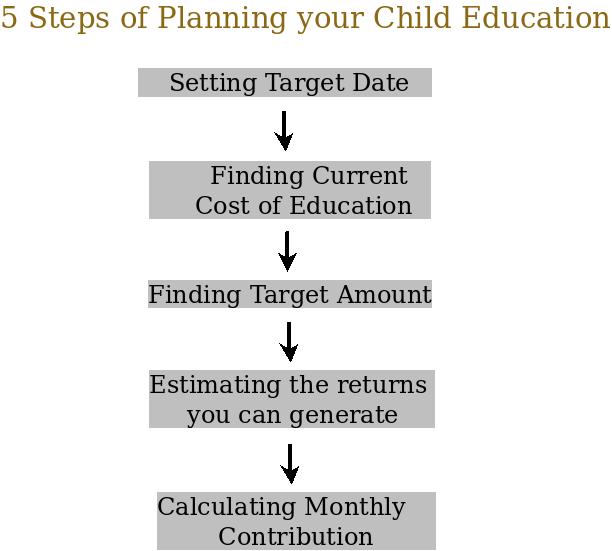

So following are the 5 steps you can do yourself to plan for your Child Education:

Step 1: Set a Target Date

The first step is to find out the target date for the child education goal. I feel the that average age when a child goes for Higher education can be taken as 21 or 22. You can take your own target tenure depending on your expectations and situation.

If you are not yet married then find out the estimated time left for your marriage and when you want to start your family (i mean children) and add target years to that number. For me personally it would be 4 + 21 = 25 yrs. what about you?

Step 2: Set a target amount in today’s term

The next step is to determine how much does it cost in today’s value for giving education to your child. All of us have different aspirations when it comes to our child education, courses like MBA, Engineering, MBBS, Software related courses are on our minds.

So let’s say for example you determine that Rs 10 lacs is good enough to provide a good education to your child in today’s value. Now you can jump to next step, but before that make sure you understand the effect of inflation on our Money. Here is another good article on Inflation

Step 3: Find out the amount you need on target date

Next step is to find out how much amount you actually need in the end. For this you first need to determine the rise in education cost per year. As per the recent year numbers, Education costs are increasing at 10% per annum.

A decade ago you could have done an MBA at 1.25 or 1.5 lacs, but today it costs more than 4 lacs. That’s more than the average inflation. Education cost in our country has been increasing at higher speed than other things. so you need to consider some figure. I would like to take this as 10%.

Now, you can just inflate the today’s cost using simple compound interest formula. Understand Compound Interest and other important Formulas.

Target Amount = Amount today X (1 + rate) ^ Tenure

Example: Considering myself, the amount I would require today is around 8 lacs. My tenure is 25 yrs and rise in education cost I would like to take as 10%. So

Target Amount I need after 25 yrs = 8,00,000 X ( 1 + .10) ^25 = 86 lacs (approx)

So, I can see that I need to make around 86 lacs in 25 yrs. Please note that this figure is based on your assumptions. The actual Figure you might need may be more or less to this amount. But still this is good enough, as we have a plan at least and we are near the goal.

Step 4: Estimated the return which you can generate over your investments

This is an important step where each investor has a different level of risk appetite and knowledge. Depending on those factors one can choose different products for investments and can generate some return through it.

One who is not much interested in finances and has lesser risk appetite can choose Balanced Funds or Debt Funds and can generate around 10-11% returns. On the other hand a person who can take more risk and have more interest in finances can invest in products like Equity Mutual funds, ETF’s, Direct Equities etc and can target close to 14-15% returns.

Getting more or less return is fine. All it matters is, does it suit your risk appetite?

There is no point in investing in risky products if you are not a risk taker. As a rule of thumb, a person who is investing for long-term like 10+ yrs should take Equity route because over that kind of time frame Equity has performed the best with maximum returns and with small risk.

So for long-term, Equity is what you should invest in and for short-term prefer equity only if you are great risk taker. Your range of return expectation should be from 8% – 15%. Anything above that is a bonus but getting more than 15% is tough for general investors like us.

Anything like 20-25% should be the target of more professional investors who have advanced knowledge and who are full-time into stock market and related fields. So better be satisfied with suitable returns which will be able to achieve your goals.

Understand Equity and Debt here

Step 5: Calculate per month contribution

The next step is to find out what is the monthly contribution you need to do. For this you have to use this scary formula.

C = [FV * r] / [(1+r) * { (1+r) ^ t – 1 }]

Where

- C = contribution per month

- r =Rate of return you expect to generate on your returns .

- t = tenure (It would be multiplied by 12 if payments are monthly)

- FV = Future value of your goal (this is calculated in step 3 .

You can Use this Calculator to calculate these figures. Just fill in your details and get the output. Now you can invest this money in product you have chosen.

Important Points to Remember

- Apart from these 5 points, there are other points you have to consider which will make your Child Education planning more strong and successful.

- Make sure you are Insured Properly because in between if you die prematurely the amount of insurance your dependents get should be good enough to achieve your Child Education. Make sure you buy a good term insurance plan to cover this risk.

- When you are near the end of the goal, when still 4-5 yrs are left then you should better start withdrawing your money from riskier products to more safer products, so that you do not get surprise drop in your Corpus. If another subprime crisis happens at the same time when your kid is ready to go to college, it will be a tough situation. So better start withdrawing your money every month from Riskier products to safer products.

- Make sure you review the performance of your Child Education plan every year and make sure that things are going as expected. If not, find out why? See if you need to change your numbers, if you do it’s fine. No one can plan for things in advance with accuracy and it’s totally find if things go little off track. Just be ready to adopt the changes.

- At the end, sticking to this plan is the deciding factor of whether you are successful or not. The consistency in Investing for this goal is the main thing. Returns will follow when you follow the plan.

- Make sure the Asset Allocation is right and make sure you stick to same asset Allocation.

- Make sure you do not force your Child to adapt as per your Plan. Make sure you don’t have anything rigid for Child. Let him/her decide what they want to do, You are mainly a motivational parent who are paying for cost of what your child wants to do in their life. A successful Child Education plan won’t make any sense if he/she is not able to pursue what they are passionate of and love doing.

Conclusion

You have several products in market which claim to be Child Plans. They are costly and complicated for most of the general investors. The simple funda for successful financial planning is “Dont buy if you dont understand it”. Planning for Child Education can be a step by step designed simple plan which we can do ourselves.

Please leave your Comments to let me know how did you like the article? Which one of these steps is the most challenging part? What do you suggest is the rough estimate of Child Education expenses today?

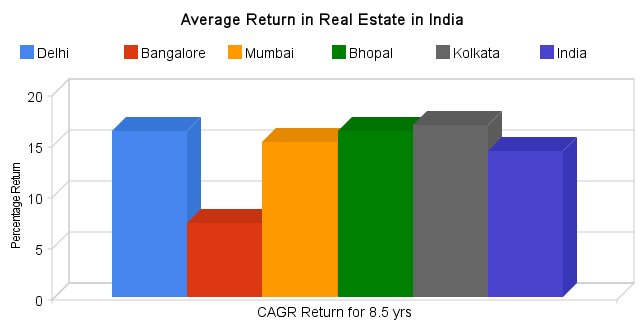

Note : I have assigned Index value for “India” by assigning weights of 25% , 25% , 25% , 10% and 15% to all five cities in same order .

Note : I have assigned Index value for “India” by assigning weights of 25% , 25% , 25% , 10% and 15% to all five cities in same order .