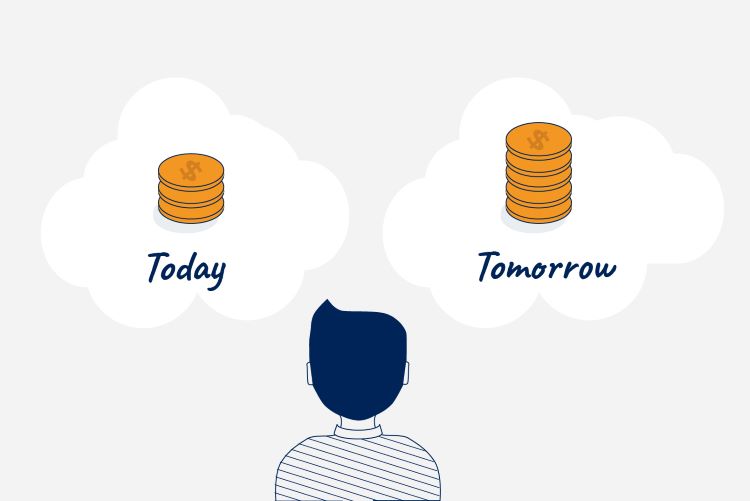

One realization I’ve had over the years is that the purpose of wealth is not to make your life bigger.

It’s to make your life lighter

For a long time, I thought wealth was mainly about acquiring more.

a better house,

a better car,

more travel,

more experiences,

and the ability to buy things without worrying too much.

And to be fair, it does provide all of those things. But over time, I’ve come to appreciate a very different benefit of wealth:

Wealth removes friction from everyday life.

Of course, for someone struggling to meet basic needs, money does far more than that. It provides security, dignity, opportunity, and peace of mind. But once those needs are met, something interesting begins to happen.

You start noticing how much of life is consumed by small problems.

Not life-changing problems.

Just endless little irritations.

Waiting in queues.

Delaying a repair because it feels expensive.

Spending hours comparing prices to save a small amount.

Taking a longer, more tiring option because it’s cheaper.

Postponing a decision because cash flow is tight.

Fighting with customer support over a billing error.

Travelling overnight to save money and then spending the next day exhausted.

None of these are major problems on their own. But together, they quietly consume time, energy, attention, and emotional bandwidth.

When money is limited, every decision carries a calculation behind it.

Can I afford this?

Should I wait?

Is there a cheaper option?

Can I manage without it for now?

A surprising amount of mental energy gets spent answering these questions.

As your financial situation improves, many of these calculations begin to disappear.

You don’t have to engage with every problem.

You can choose convenience when it matters.

You can pay for speed.

You can outsource repetitive tasks.

You can replace something instead of repairing it three times.

You can take the flight instead of the train.

You can solve a problem in ten minutes instead of letting it occupy your mind for ten days.

The change is subtle, but profound. Life doesn’t necessarily become more luxurious.

It becomes less cluttered. Less draining. Less noisy.

And that’s a benefit I never fully appreciated when I was younger. In fact, I suspect this is one of those lessons that is difficult to understand until you experience it yourself.

Real Value of Wealth

The real value of wealth isn’t always in what it allows you to buy.

It’s in what it allows you to stop worrying about. Perhaps this is one of the most underrated reasons to build wealth.

Not so that life becomes bigger, but so that life becomes lighter.

Not so that you can impress others, but so that you can protect your time, energy, attention, and peace of mind.

And once you experience that freedom, you may discover that it is worth far more than many of the things money can buy.

And perhaps that’s what financial freedom is really about.

Not just having enough money. But reaching a point where your life is no longer dominated by small financial calculations, unnecessary compromises, and problems that money can easily solve.

A life where your attention is free to focus on the people, experiences, work, and pursuits that matter most to you.

I sometimes wonder why people can’t foresee how their financial future will look?

Don’t people know that there will be a day when the paycheck will stop?

Don’t they realize that one day they might become obsolete, physically or professionally?

That their health will decline? That emergencies will arise?

Cant they see that they need to have wealth at age 60 to survive the rest of their life?

And don’t they see that inflation is real — silently eroding their purchasing power year after year?

Don’t they see?

But the answer, sadly, is NO.

People can’t see far enough.

After years of working with thousands of clients, observing their behavior and decision-making patterns, I’ve come to a stark realization:

Most people operate with a short-term mindset.

The reality is that most people don’t operate with a long term mindset!

They live year-to-year.

Salary-to-salary.

Milestone-to-milestone.

Yes, deep down they have a vague idea of what the future holds, but their actions rarely reflect that understanding

And it’s this inability to think beyond the immediate that is slowly creating a retirement time bomb in India.

Millions of people will hit age 60 without a meaningful corpus. No financial cushion. No peace of mind. Just dependence — either on their children, or on a broken government system, or on hope.

Today, I want to talk on 4 mistakes which people need to correct in their life to move forward and create a better financial future.

Mistake #1 : Instant gratification

The desire to feel good now, even at the cost of the future is called Instant Gratification. This is the root cause of why most people have bad financial lives.

Their focus is so much on making their NOW better and amazing that they fail to see if its impacting their future badly.

Have you seen people blindly buy useless insurance policies just to “save tax” for the current year — without even understanding how that product helps them in the long run

Swiping your credit card for things you desire but can’t afford, then paying just the minimum due to “survive the month in peace” — it feels like a quick fix today, but all you’re doing is piling up interest and penalties, silently pushing yourself deeper into a future debt trap.

Or those who register property at a lower value (by paying part of it in cash) to reduce registration charges now, only to realize years later that they’ll face huge capital gains tax — because on paper, their profit appears much higher?

Then there are those who postpone buying health insurance in their 30s thinking they’re fit, only to be denied coverage later or hit with a massive hospital bill they have to pay out of pocket.

And perhaps the most common — people who don’t save enough in their early years, thinking they’ll “start later,” and then find themselves in their mid-40s or 50s, stressed and anxious, wondering how will I ever retire?

Instant gratification is tempting. But the cost is silent, invisible, and irreversible.

If you want to build wealth, you need to master the art of delayed gratification — the skill of saying no today so that you can say yes to something far bigger, later.

Mistake #2: Blindly Extrapolating the Present

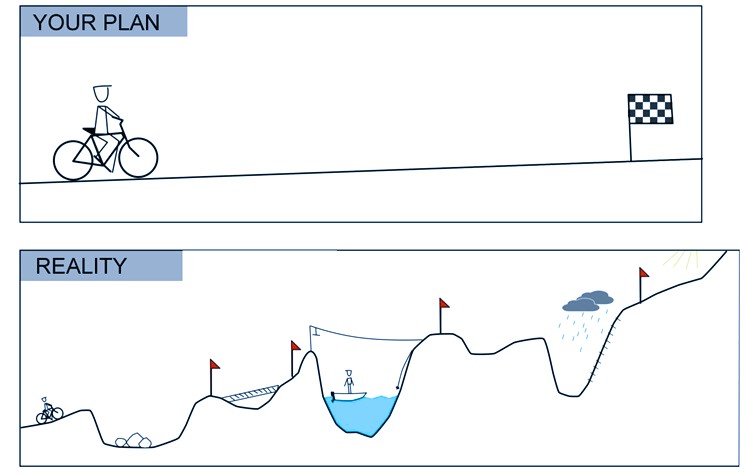

One of the most dangerous financial habits is assuming that the current good times will simply continue forever — as if life follows a straight line upward.

People confuse a short-term win with a long-term pattern. They anchor their future on recent success without factoring in uncertainty, volatility, or change. And this isn’t optimism — it’s delusion dressed up as confidence.

Your brain is wired to prioritize the present—what’s working now feels like what will always work

I often hear things like:

“I’ve never had a health emergency — I don’t think I need health insurance yet.”

“I just got a big salary hike — I’ll buy a luxury car on EMI”, assuming that the income will keep growing like this forever.

“My crypto investments doubled in the last two years, so I’m going to pull all my money out of mutual funds and put everything into crypto”

But here’s the truth: just because something worked this year doesn’t mean it will work next year. Growth is never linear, and neither are careers, stock markets, or life itself.

That said, taking risks based on careful analysis and a clear understanding of potential outcomes is a different story. Calculated risks can pay off and are part of smart wealth-building.

The problem is blind extrapolation — making big moves based only on short-term results or hope, without contingency plans or room for error.

When you assume that today’s highs are tomorrow’s norms, you stop planning for risk, stop saving conservatively, and stop preparing for the possibility that things might slow down, plateau — or even reverse.

Good phases are not guarantees — they’re opportunities. Use them to build buffers, not fantasies.

Mistake #3 : Overconfidence of Future Income

One of the most subtle — yet dangerous mistakes people make is over-relying on their future income. They assume that salaries will always rise, bonuses will keep coming, and promotions will be predictable. This assumption gives them hope — a comforting illusion that even if they’re not saving enough today, their future self will somehow fix it all.

“I’ll start saving more once I hit the income of 25 lakhs per annum.”

“My next bonus will take care of my credit card outstanding debt.”

“I’ll buy that house now, and manage the EMI easily when my salary increases.”

I won’t say you shouldn’t be optimistic, but if you’ve had a history of financial struggles, these aren’t plans — they’re financial fantasies

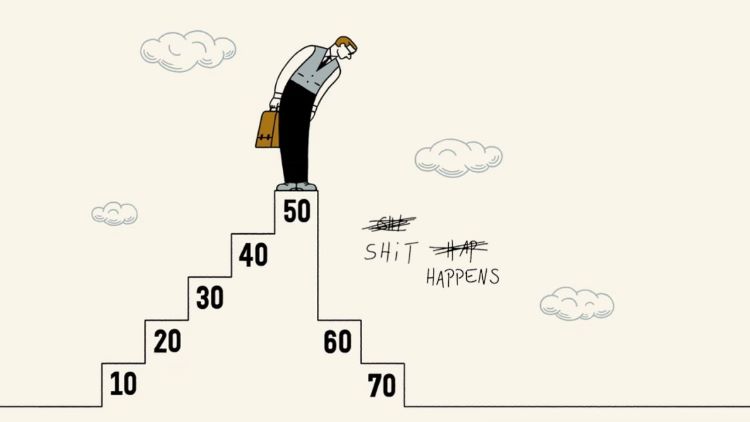

The problem? Life doesn’t always go as expected.

Career growth is not guaranteed. Industries evolve, companies downsize, and roles become obsolete. The high performer of today can become irrelevant tomorrow if they stop learning or the economy shifts. A promising startup job may vanish. A high-flying role may suddenly come with burnout or health issues.

Health issues can derail careers. Accidents, mental health struggles, or chronic conditions can force people to slow down — or stop altogether.

You must learn to expect ugly surprises in life. Shit happens!

Based on thousands of client experiences, I can confidently say I’ve seen several cases… where mid-career professionals had to take long breaks or even quit because of personal or family health crises. After a point, a great career can stagnate and there may be less to no growth in salaries. There may be constant medical expenses which can eat out all the bonuses and salary rise.

Family responsibilities grow. Elderly parents may need support, children’s education costs may skyrocket, or a single income may suddenly have to support two generations.

In real life, your expenses rise faster than your income. But most people build their lifestyle on optimistic assumptions about raises, appraisals, and windfalls. They increase spending the moment income rises — and plan long-term liabilities like loans based on best-case salary scenarios.

This mindset creates a dangerous feedback loop:

You don’t save enough now because you believe the future will take care of itself.

But when the future arrives, it’s messier, costlier, and more uncertain than expected.

And because you didn’t prepare, your future self is left scrambling — without buffers, without options.

Overconfidence in future income is a form of financial procrastination. It gives you a false sense of control, while quietly eroding your real control over your future.

The solution?

Plan for your future based on realistic assumptions — not wishful thinking. Build your lifestyle based on your current income, not projected growth. And treat any income jump or bonus as an opportunity to accelerate your goals, not inflate your lifestyle.

True financial freedom comes not from earning more — but from using what you earn wisely, intentionally, and with foresight.

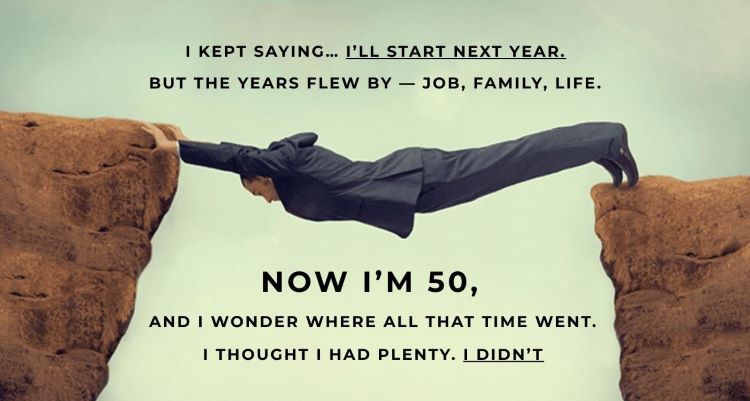

Mistake #4 : Myth of “Plenty of Time”

When we’re young — say, 25 years old and just starting our careers — retirement feels like a distant, almost imaginary event. Bursting with energy and optimism, you feel like time stretches endlessly before you.

There are so many more exciting priorities: romance, adventure, spontaneous trips with friends, and all the first tastes of true independence. You’re finally free—earning your own money, making your own choices, living life on your terms.

Why worry about some far-off future when there’s so much to experience right now?

We tell ourselves, “I have so much time ahead to plan, save, and do what’s necessary.”

But if you ask most people in their 40s, they’ll laugh at that 25-year-old’s confidence. By then, they’ve experienced how fast time really flies, and how life throws challenges and complexities that demand constant attention. Managing a career, family, health, and unforeseen events eats up years quickly.

The biggest regret many people in their 50s share is that they started “late.” They always thought they’d get to important financial and personal goals “later.” Without setting firm deadlines, the future keeps moving away: at 25 you say later, at 28 later, at 30 maybe at 35, at 35 you’re busy with kids and work, and at 40 you realize you’re only halfway — but the clock keeps ticking. By the time you hit your 50s, you realize you’re already behind.

This myth of having “plenty of time” is another trap of present bias. It leads to procrastination and underestimating the power of compounding—whether in investments, health, or relationships. It’s easy to defer important actions when you believe you have infinite tomorrows, but time waits for no one.

Understanding that time is limited—and acting early and deliberately—is one of the most critical steps toward building lasting wealth and a fulfilling life.

What’s the way out?

When you are young, you just have to make a small start — and then build on it.

Even saving 5–10% of your income is enough to begin with. If you earn ₹50,000, start a SIP of ₹5,000. Then slowly increase it to ₹7,500 and ₹10,000 over the next 2–3 years. What matters most is not how much you start with, but that you start early and stay consistent. That’s how wealth — and peace of mind — is built.

Final Thoughts: Build Meaningful Wealth, Not Just a Number

If you’ve read this far, take a moment to reflect on the four mistakes we discussed above.

Each of them — instant gratification, blind extrapolation, overconfidence in future income, and the myth of plenty of time — quietly eats away at your potential to build lasting wealth.

These aren’t just financial missteps. They are mental frameworks that stop people from creating the life they truly want.

But the goal is not just to get rich.

The goal is not to win some imaginary race and wake up one day with money in the bank — but bad health, broken relationships, and a deep sense of emptiness.

Create your Wealth with Jagoinvestor Team

If you’re serious about transforming your financial life and avoiding these costly mistakes, the Jagoinvestor Team is here to guide you. We’ve helped thousands build meaningful wealth with clarity, discipline, and a proven roadmap. If you’re ready for real progress — not just information — join hands with us. Fill up this form and let’s start your wealth journey the right way, with the right support

Wealth is not the end. It’s the enabler. It’s the tool that gives you freedom, options and security.

It’s what allows you to take care of your loved ones, enjoy life on your terms, and age with dignity — not dependence.

So yes, fix your mistakes. Start taking your financial future seriously. Create systems that help you grow your money with discipline and clarity. But don’t lose your soul in the process.

Meet Rahul: 35 years old, ₹1.2 lakh monthly salary, ₹3 lakh in credit card debt, ₹16 lakh personal loan, and zero assets. From the outside, he’s the picture of middle-class success – nice apartment, latest smartphone, weekend brunches. But peel back the Instagram filter, and you’ll find a financial time bomb ticking. I am sure if you’re honest with yourself, maybe a part of Rahul’s story sounds familiar to you or someone you know personally.

This isn’t an exception – it’s the dangerous norm for millions of urban Indians today. The scariest part? They don’t even realize they’re drowning.

Most people blame external factors—low income, bad luck, or family pressures—for not building wealth. But more often, the real reason is silent and dangerous: a casual, indifferent attitude toward money.

I call it the Casualness Trap.

It took me nearly ten years to realize this after working with thousands of clients and hundreds of our workshop participants

People who are casual about their finances usually show the same attitude in other areas of life. They often run late, make promises they don’t keep, and carry a certain “chalta hai” mindset—the belief that things will somehow sort themselves out.

How Delaying Decisions Can Derail Your Wealth

This isn’t about people being reckless or intentionally careless. It’s about the small ways we let important things slide, the way we avoid looking at the uncomfortable truths, and how we push big decisions to the future because they feel overwhelming today.

When it comes to money, this casualness shows up in phrases we’ve all heard—or even said ourselves.

“I’ll start saving once my salary goes up.”

“I don’t need to track my spending; I have a rough idea.”

“I’m still young; I’ll think about investing later.”

“Life is for living—I’ll enjoy now and figure things out down the road.”

These don’t sound like financial sins. They sound…normal. Relatable. Even harmless.

But that’s exactly what makes this trap so dangerous. It’s not rooted in bad intentions—it’s rooted in delay, in inertia, in living on autopilot. And wealth doesn’t get built on autopilot. It’s built when you act with intention. And when that intention is missing, every year that goes by becomes a missed opportunity.

Often, this mindset isn’t entirely your fault—it’s inherited. Many of us grow up in households where money isn’t discussed openly, planning isn’t prioritized, and financial decisions are driven by emotion or urgency, not strategy. If your parents lived paycheck to paycheck, avoided risk, or treated money as a taboo topic, it’s likely you absorbed some of that thinking. Without even realizing it, their casual approach becomes your default setting—until you choose to break the pattern.

Why the Casualness Trap Destroys Your Future

Casualness feels safe in the moment. You avoid tough conversations with yourself. You don’t have to confront how little you’re saving or how unstructured your finances really are. But life, as we all know, has a way of shaking you up when you least expect it.

Maybe you lose your job.

Maybe someone in your family needs sudden medical care.

Maybe an unexpected bill lands on your lap.

And that’s when the cracks show.

There’s no emergency fund to dip into. No investments to fall back on. No plan to help you through.

So what happens?

You swipe the credit card, take a personal loan, maybe even borrow from friends and family. And just like that, stress multiplies, pressure builds, and financial anxiety becomes part of your daily life.

What makes this worse is that these situations aren’t rare. They happen all the time—to millions of people. And if you’re caught off guard, it’s not just your money that suffers—it’s your confidence, your peace of mind, and sometimes even your relationships.

But the biggest loss? Time.

Time that could have been used to build. To grow. To compound.

Because once compounding is off the table, catching up becomes 10X times harder.

You Start to Feel Lost, Behind, and Defeated

This trap doesn’t just affect your wallet—it affects your identity. Deep down, people stuck in this loop begin to feel like they’re failing at life. Like they’re the only ones not getting ahead. That creeping feeling of being left behind by your peers—despite working just as hard—starts to take root. And soon, you start losing faith in your ability to change your situation.

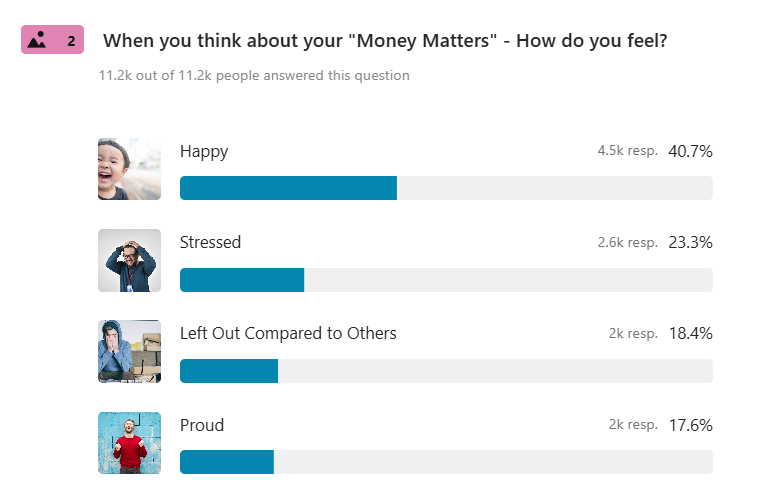

In our 25 questions financial health checkup, we ask people how do they feel about their money matters and around 1 out of 5 people said they feel “Left Out Compared to Others” .. That’s such a heavy feeling!.

But here’s the truth: it’s not too late. Not if you choose to act.

The first step is recognizing this pattern. The second is having the courage to break it.

Why Good-Income Alone is not enough

A lot of educated, urban professionals fall into the trap of thinking they’re “doing fine” just because their salary is increasing. But wealth isn’t about how much you earn—it’s about how much you keep, how wisely you invest, and how patiently you let it grow.

Without budgeting, without protection (like insurance), without long-term planning, you’re just burning fuel without direction. Income rises, but so do expenses. And you remain financially vulnerable, just at a higher lifestyle level.

The Emotional Cost of Casualness

Many people think of finance as a cold, logical area of life. But let me tell you—it’s deeply emotional. Living paycheck to paycheck, dreading the 1st of the month, avoiding bank statements, worrying about every expense—these experiences leave scars.

The regret of not starting earlier, the shame of not knowing where your money went, the fear of financial instability—they’re real. And they’re painful.

The Casualness Trap may feel harmless at first, but its consequences are far-reaching and long-lasting. It’s easy to ignore today’s financial decisions, thinking they can wait for tomorrow, but tomorrow is never promised. The good news is, it’s never too late to break free from this pattern. By becoming intentional about your money—starting today—you can turn the tide.

It’s not about earning more, but about doing more with what you have. The key is making conscious, proactive choices that build the foundation for a secure, prosperous future. So, stop letting “later” dictate your life and take charge of your financial future now. Your time—and your wealth—are far too precious to waste.

Wealth isn’t built by grand gestures—but by killing the ‘Chalta hai’ voice in your head, one intentional choice at a time.

If this piece struck a chord, maybe it’s time to stop delaying and start deciding. For some, DIY works. For others, expert guidance brings clarity and speed. If you’re in the second group, we’ve helped thousands like you build systems that stick. Do fill up this form and lets Talk!

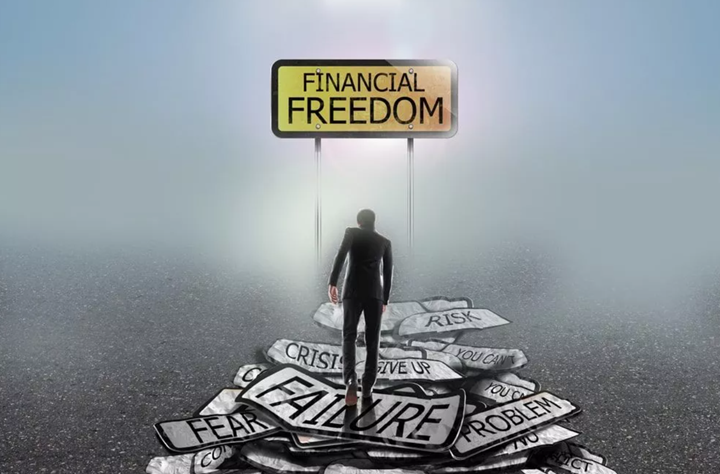

Financial stress is at an all-time high in India, and this is evident from the increasing popularity of terms like FIRE (Financial Independence, Retire Early). People are worried about their financial security and are struggling to save as much as they should.

Retirement used to be the big goal that everyone aimed for, but today that has shifted. The focus is now on achieving financial freedom, or FIRE, as it’s commonly known.

7 Key Reasons to Achieve Financial Freedom by 45

In this article, I want to explain why achieving financial freedom as early as possible should be your top priority, especially if you’re just starting your career. It’s not just a nice-to-have goal; it’s a necessity in today’s world. Here are 7 powerful reasons why FIRE is something you need to work towards right now.

Reason #1 : Job Security is a Myth After 45

One of the main reasons to aim for financial independence by the age of 45 is the fast-changing job market. The idea of “job security” is becoming outdated, especially with the rise of artificial intelligence (AI), automation, and companies leaning towards younger, tech-savvy workers. By the time you reach your mid-40s, your career path can start to feel unpredictable—this is already happening in sectors like IT and BPO/KPO.

I just came back from a two-day session in Delhi, where a researcher from Gavekal Research shared some startling insights. He mentioned that one of the key figures he spoke to predicted that in the next 5-6 years, there would be no jobs left in the BPO/KPO sector in India. While this may sound extreme, it’s a strong reminder that major changes are on the horizon.

Companies today are increasingly looking for employees who are flexible and skilled in new technologies. As AI continues to disrupt industries worldwide, older workers who haven’t kept pace with these changes might find themselves displaced or forced into uncertain career transitions. Job security, especially after 45, is no longer something you can rely on—this is why financial independence is more important than ever.

With AI making huge strides, it’s clear that repetitive jobs with no creative input are at risk of being replaced in the coming years.

Reason #2 : Family Responsibilities Peak After 40

As you hit your 40s, family responsibilities often become more demanding. Between your children’s education, the rising cost of living in major cities, and the increasing desire for luxuries, it can feel like your entire life revolves around finances. If you live in a metropolitan area, school fees and daily expenses can pile up so quickly that you might start feeling like an ATM machine rather than a person.

On top of that, parental responsibilities grow as your parents age and require more healthcare. Many families find it tough to balance the financial needs of both children and aging parents. Without preparation, these dual pressures can quickly overwhelm your finances. This is where achieving financial independence by 45 or 50 can make a real difference. It provides the peace of mind that your family’s needs—both educational and healthcare-related—are covered without sacrificing your own financial stability.

Reason #3 : Midlife Crisis Becomes Easier to Navigate with Wealth

As you enter your 40s, it’s natural to reflect on your life—your choices, accomplishments, and what you still want to achieve. This is often the time many people experience a “midlife crisis.” While it can be emotionally and mentally challenging, having financial security can make a big difference in easing the process.

If you haven’t built a solid financial foundation by this point, the midlife crisis can feel even more overwhelming, and the stress can be three times heavier.

Speaking from personal experience, I’m currently 42, and I’m going through my own midlife crisis. But at least the wealth side of my life is strong and sorted, which helps me navigate this phase with greater confidence.

That’s why it’s crucial to have your finances in order by your 40s. With a solid financial base, you have the freedom to pause, reflect, explore new paths, or even change direction in life. Whether it’s pursuing a new career, diving into a passion, or taking a break to travel, wealth gives you the space to make those choices without the constant worry of financial strain.

Reason #4 : Health Focus Gets Better with Financial Independence

By the time many people reach 45, health issues tend to catch up with them. When you ask them how they rate their health, most people won’t score higher than 6/10. Years of stress, long work hours, and poor lifestyle choices begin to take a toll. At this stage, you realize that all the talk of financial freedom, owning multiple properties, and traveling the world means very little if your health isn’t in good shape.

However, it’s tough to focus on your health when you’re burdened with EMIs, financial worries, and constantly living paycheck to paycheck. I’ve always said, “Health is wealth.” Financial independence gives you the freedom to prioritize your health without the stress of financial constraints.

Achieving financial freedom by 45, allows you to invest in your well-being and I am personally experiencing this right now. Only at the age of 42, I become more aware of importance of health and in last 18 months, I have lost 19 KG and I am still on my health transformation journey. From the bulky 89.5 kg guy, I now feel amazing at 71 kg (a detailed article on this later)

While money isn’t a guarantee of good health, financial independence provides the space to focus on this critical aspect of life. It lowers stress levels, which is key to maintaining your health. Financial independence also lets you work on your terms, avoid toxic work environments, and live a more balanced, healthy life.

Reason #5 : Reclaiming Your Time to Do What You Love

One of the most enticing aspects of financial independence is the freedom to pursue your passions. Whether it’s traveling the world, picking up new hobbies, starting a business, or giving back to society, financial freedom allows you to focus on what you truly love, without financial constraints holding you back.

Let’s be real—many people dismiss FIRE (Financial Independence, Retire Early) as a “scam” or an “escape from hard work.” But the truth is, 8 out of 10 people are stuck in jobs they don’t enjoy. They have a deep desire to do something else with their lives but can’t, simply because finances don’t allow them to make that shift.

By the time you’re 45, many begin to question if they’re truly living the life they want. When your financial security is in place, you have the ability to make life choices based on desire, not necessity. You can decide what kind of work you want to do—or whether you want to work at all.

You can also pursue dreams that you may have put on hold earlier in life, like writing a book, learning a musical instrument, or starting a charitable organization. And if you genuinely love your job, you can approach it with more passion and energy. In a world that’s rapidly changing, having the ability to live authentically and without financial worry is the ultimate form of freedom.

Reason #6 : India (and the World) is Becoming Increasingly Consumeristic

We are living in a new India, and soon, it will be a version of India we could never have imagined. Desires are growing — and it’s only natural. Better homes, luxury travel, quality food, the latest gadgets — people today want to live well, and there’s nothing wrong with that.

But somewhere, many still cling to old sayings like “Live a simple life, don’t chase wealth.” While these words sound noble, the reality is different. Most people who preach this either never had the chance to build wealth or have accepted it won’t happen for them. In truth, it’s often not a genuine choice — it’s a compromise.

The harsh reality is: money is going to matter more than ever in the India of tomorrow. If you don’t plan and build wealth now, you’ll likely feel left out in a world that’s moving toward greater comfort, abundance, and financial independence.

It’s not about becoming greedy; it’s about being future-ready. Building financial strength today ensures you can live life on your terms tomorrow — without regret, without compromises.

Reason #7: Peace of Mind Comes from Early Financial Strength

In today’s unpredictable and increasingly materialistic world, the biggest luxury is peace of mind — a mind that is strong, calm, and secure. And this peace comes from financial independence.

A strong, powerful bank balance and a secured stream of future income bring a next-level confidence in a person. You not only have money in hand, but also enough time in life — a rare and priceless combination.

It makes you stand out as the special one among the large, messy crowd still running behind money, chasing deadlines, and worrying about bills.

Having strong financial reserves by the time you’re 45 means you can face life’s surprises calmly and confidently.

Without financial security, every decision carries stress — whether it’s about career moves, health emergencies, or family matters. But when money is no longer a daily worry, life transforms. You sleep better. You make choices based on dreams, not desperation. You enjoy family time without the constant background noise of anxiety.

Money may not solve all problems, but it shields you from countless unnecessary battles. The earlier you build your financial wall, the longer you get to live peacefully inside it — without fear, without compromise.

Speed Up Your Financial Freedom Journey with Jagoinvestor

Financial freedom isn’t just about numbers on a screen or a retirement corpus tucked away for the future. It’s about creating a life of choices, security, and fulfillment — well before society thinks you’re “allowed” to.

By aiming for financial independence by 45, you gift yourself the priceless ability to live deliberately, with strength and clarity, while you’re still full of energy and ambition. The world is changing fast, and the greatest advantage you can have is the freedom to adapt, grow, and enjoy life on your own terms.

At Jagoinvestor, financial independence isn’t just a service we offer — it’s a mission we live and breathe. Every client we work with shares a common goal: to achieve true financial freedom — and we specialize in making that vision a reality.

If you feel ready to have a strong support system by your side — a team that treats your financial journey like a serious 10–15 year project — we would love to work with you. We help manage your wealth, guide your strategy, and walk with you until you reach your Financial Freedom milestone.

If this resonates with you, you can apply for our program, and we’ll be happy to have a conversation and explore how we can help you achieve your mission.

Interest rates and inflation dont really matter much in long-term equity investing.

I am going to prove it to you with my personal experience of stock investing in last 16 yrs!

In the previous article, we discussed 2 key macroeconomic concepts such as interest rates and inflation.

Most investors tend to overemphasize on these 2 concepts and use them for investing into direct equity. One thing to consider is that the equity market is a completely different beast to conquer. And that’s what we discuss in this article, in the long run, macroeconomics becomes completely irrelevant for an equity investor. Sounds contradictory, read more to find out.

In my 16-year-long investment journey, I’ve found that macroeconomics has absolutely no connection to investment returns.

In the short term, yes.

Let me tell you my own story.

My first stock that I had bought in 2006. Right after my 10th Board exams, I was asked by my family to work in the family business. If you’re a Gujarati or Marwari reading this, it’s normal. For others, it’s child labour and yes, I’m with you guys despite being a Gujarati.

Jokes apart.

I was asked to work on the shop floor of our family business. 12 long hours every single day. No social life. I was just meeting my friends on Saturday nights or Sunday evenings. It was tough back then, but now it’s a habit.

After 3 months, I got into the HR College of Commerce and Economics. As a gift, I was rewarded with my first paycheck after 3 months of bone-cracking work for a 16-year-old. And naturally, this money was the most important thing in my life at that time.

It could have gone 2 ways. I would have partied long and hard. But I chose the second option, I invested that money because it was hard for me to waste it over a weekend.

I invested at the high of the 2006 markets

It’s 2006, and the stock market is soaring to new highs every other day. And everyone is talking about how much money is being made. Plus, my family didn’t appreciate my thought of investing in some shares. So the rebellious child in me got an opportunity.

Since I was wiped out of my 3-month vacation, this money should at least give them some stress. A guilty pleasure indeed.

So I decided to open a demat account. But I was a minor back then. So I turned to my mother who accepted my decision because I had fulfilled my promise of securing admission into the top 3 colleges of Mumbai.

After a few days, I had my demat account.

Now came the decision to invest my money. Since everyone in the family was against it. No one helped. So I started watching CNBC TV. After a few days, it confused the life out of me. Plus, my college had started and I was still working at my family business in the first half of the day.

My schedule was:

7 am to 9 am – Accounts and Maths classes

9:30 am to 1 pm – Shop floor of family business

2 pm to 6 pm – College (bunked most of the time and made some closest friends)

7 pm to 8 pm – Learning some new course

The reason I’m telling you this is because it was in Indian Merchant Chambers where I was learning about stock markets, where I had a lucky break for my investments. It was a chance to attend a lecture by Mr Deepak Parekh of HDFC Ltd and Mr Aditya Puri of HDFC Bank on Indian Banking Outlook.

I don’t recollect the speech that day.

But it had a profound impact on the way I looked at investing my hard-earned money. As a result, I called up my broker and asked him to buy HDFC Bank with the money I had. It just made sense to me.

Because I could see HDFC Bank’s service to customers was superior, they had a friendlier staff when compared to other PSU Banks and its standards were equal to a foreign bank. These days, it’s a normal thing. Back in 2006, it was revolutionary.

Fast forward to 2023.

That investment is up 30x.

And yes, I’ve stayed invested.

It wasn’t a smooth journey, to be honest. There were times when I felt that the Bank would be shut the next day. That’s where my hard work in the family business paid off. Whether it’s a boom or a recession, good employers never let their employees go away.

2008 was particularly tough to digest. Because my investments were down by 50%. And there was bad news everywhere. Banks in the US were failing. Sensex was going into red every single day. There was panic all around.

So I did some research. I asked my college professors about my investment into HDFC Bank. One of them was pleasantly surprised and told me his secret.

She said,

“Whenever you feel like selling a banking stock, just keep a check on their non-performing loans. If they are going up more than the industry average, then sell the stock even if you have made a loss. But if the bank is able to provide for those non-performing loans, then be rest assured that it will tide through.”

I made my attempt and discussed it with her. Later on, I decided to hold the stock.

I didn’t buy more because it was my first rodeo and I was just turning 18. I had CA exams to prepare for, it would be my perfect escape from the family business in the later years. Fortunately, I don’t get sleepless nights or anxiety when the stock corrects by 50%, sleep is my superpower.

The same scenario happened in 2013, when India was tagged as the fragile 5 economies of the world. I was in a similar situation of thinking of selling the stock. But again, it didn’t seem like the bank was unable to control the downside.

In the same way, I have taken this decision multiple times. And each time, I have decided to stay invested with the stock.

It’s never a buy-and-forget situation.

It’s a constant analysis.

As a result, I’ve realized how little interest rates and inflation really matter. As an investor, my job is to assess the company’s ability to tide over this crisis properly. Every single time, there’s a macroeconomic event, it’s best to go back to the roots and check the balance sheet of the company. If the business is happening as usual, then you shouldn’t worry so much about the stock price.

I will end my story here.

Leave the macroeconomics to the economists! We are investors!

Who is an investor?

An investor in simple terms is a person who commits capital with an intention to earn profit.

The key thing to understand here is that an investor is purely committing capital, not labour. There are 3 forms of commitments that a business requires, namely,

Capital (money)

Labour (human resource)

Land.

As a result, when we commit capital, our primary objective is to understand whether that business or company has the capacity to efficiently use land, labour and capital. When there are good times, the company doesn’t splurge money or get into unnecessary projects and when there are bad times, the company doesn’t take on unnecessary debt.

A good investor looks for a balance in these 3 aspects of the business. Because both good times and bad times are a part of the economic cycle. It’s the very nature. Cannot be changed.

The banking industry for example went through deep trouble in 2008 and 2013. After RBI Governor Raghuram Rajan asked all the banks to recognise their NPAs and monitor their health closely, the system was shocked to see so many bad loans coming out.

An investor who put his money in good banks survived and thrived. Those who put their money and even averaged while the stock price was down in bad banks have lost a lot of money.

Think about it.

Even in bad times, good banks survived and thrived. Times such as high inflation and interest rates, saw these good banks gain market share from the bad banks.

A smart investor will take a cue from here that timing the market is not important at all. Infact, in the long run, it results in portfolio destruction. We will cover this topic in our next blog.

How timing the stock market is completely irrelevant to build a long-term portfolio.

To conclude, here’s a story of Jagoinvestor’s founder, Mr. Manish Chauhan who has a unique way of building his long-term portfolio.

A couple of months ago, I was sitting in our Pune office with Manish. I was sharing my journey of wealth creation with him.

The one I’ve written above.

While he acknowledged the passion that I have for equities, he gave me a unique perspective, something I’ve never really seen or heard before.

Manish very gently said that he doesn’t track the IRR of his portfolio and does not look at his portfolio performance.

He has a simple way.

Invest your savings every month.

Redeem money when you really need it

Make sure you have chosen the right portfolio

Review it once in 2-3 yrs

That’s it.

Constantly looking at any particular metric of return such as annual return, compounded return or any other math number is beyond him. This comes only when you have belief in what you do. This happens when you have done your homework correctly. This happens when you really understand what “high risk high return” means.

The first thought in my head was disbelief.

To me, it sounded like a chocolate seller doesn’t eat the chocolate at all. But after pondering a lot of my thoughts over it, I realized that Manish is exactly doing what we preach to everyone.

Don’t obsess over the short-term returns. In the long term, when the selection of the investment strategy is correct, massive wealth creation will happen.

For an investor, this is the guru mantra. Don’t obsess over the short-term bit of money-making.

Leave it to the professionals. If you have selected your professional such as an investment advisor correctly and believe in the process of choosing a mutual fund manager or a portfolio manager correctly, then you will be able to create wealth.

Most of us forget this simple bit.

So what you should do as an investor in the long term?

You shall choose the right portfolio which suits your needs and temperament. Create a strong equity portfolio of mutual funds, PMS, and real estate and cover the basics like life and health insurance along with a good emergency fund. Work on your income and just be disciplined in investing.

If you do things correctly, the short-term underperformance or overperformance will not make any significant difference to your life.

So there’s no point in looking at interest rates, inflation or the short-term performance of the investments for a long-term investor. What shall matter to you is your health, family, and working on your craft.

Think about it.

“In the end, what matters most is how well you lived, how well you loved, and how well you learned to let go.” ― Ziad K. Abdelnour

The article is written by Jinay Savla, Equity Expert @Jagoinvestor.

This is a long, but intense and immensely high-value article. So please read it fully!

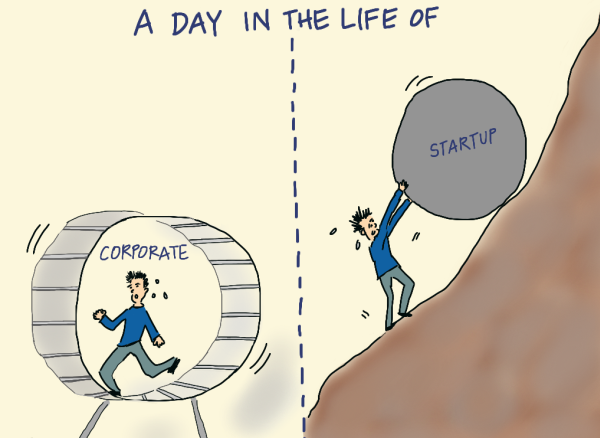

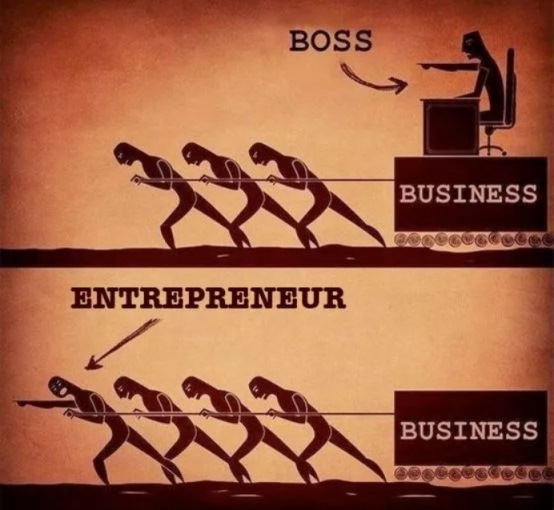

Today I want to talk about some of the advantages of “doing a job”, rather than running a business or being an entrepreneur.

If you are someone who thinks that having your own business is “always” better than “doing a job”, I want to break your myth and point out several things which people don’t appreciate about doing a job.

There are lots of articles, videos, and podcasts about “leaving your job to pursue passion” and in almost all of them, a “job” is projected as some kind of modern slavery. It projects “doing the job” as working for someone else success and giving your life for others’ benefit.

I think it’s a gross over-exaggeration and while the job has its own limitations and issues, being your own boss has its own share of very big problems. I have also seen many salaried people complaining about their life, work culture, pay limitation, lack of opportunities, and their declaration about how they want to leave their jobs one day and achieve nirvana and ultimate success and get out of the rat race.

Before I tell you some good things about being in a JOB. Let me first share the bright side of “business”

When you do some business or try a startup – you surely become your own boss, you feel more in control of your career path and there is huge huge income potential.

However only when you “become your own boss”, you start missing many things which you get in a job. Only then you are able to appreciate those subtle benefits of a job, which you never realized while being in the job. Today I want to talk about those good things about being in a job that is often not appreciated or realized.

So I am going to talk about 3 primary and major benefits and 7 secondary benefits which not major, but matters a lot.

Lets Start

#1 – Less Headache

When you are in a job, your work is very focused as you are accountable for one single thing. You don’t need to take the headache of other departments and other small things. The way you operate is simple and you can blame others for anything which is not your core-domain.

This means that you have less headache and you can be very productive and focused on your work as you are clear of what is expected out of you. I used to love my job in Yahoo years back when I had very defined tasks in hand and my to-do list was clear and precise.

Compare this to your own business!

For the initial few years, it’s nothing less than a horror movie.

While you are the “BOSS”, you are also a peon.

You are the person who does salaries, buys office furniture, pays electricity bill, works on the website, open the bank account, talk to customers, talk to vendors, run around to deal with CA, get GST calculations done, do hiring, do training and tons of other small and big things!

If you feel that this is doing to happen for just a few months of starting the business. It’s not true. Businesses take anywhere from 5-15 yrs of establishing. There are many people who are having a small company now with few team members, but there are tons of things on their plate which they need to handle and with the changing landscape of business, competition, regulator, customer experience, and business cycles, its a never-ending circus for many entrepreneurs.

Sometimes you start wondering why you are doing everything OTHER than the main task.

When you are in a job, there are lots of invisible systems that are around you and speed up your work. You become a HERO in your company, mainly because you had a lot of focus and time to excel in what is your core job. The invisible support system around you helps you in that.

So in a job, even if you feel there are lots of headaches, it’s often at a minuscule level compared to your own business. So if you are someone who doesn’t want to do be lost in too many things and doesn’t like to handle multiple things in hand, a job is a wonderful place to be in.

The job comes with fewer headaches

#2 – Clear Separation of Work-life and Personal Life

When I had started working 13 yrs back in Yahoo, Bangalore, I remember Friday evenings.

It used to give a feeling that I am starting a new life altogether – The “Weekend Life”

For the next 48 hrs, I was detached from my work life and there was nothing on my mind. It was not my headache what is going to my company. That conversation started only on Monday morning.

Unless you are at a very top position or at some senior level, there is a very very clear separation of work life and personal life.

This becomes very tough when you start your own business. No matter what you do, there will be some thoughts of business that will crop up in your mind. This is simply because now you are not working for someone else. You are working for yourself. Your company is part of you.

Sadique Neelgund who started his entrepreneur journey with networkfp.com 10 yrs back shares his comment on this point.

As an Employee, one of the biggest benefit I enjoyed was fixed work hours – 8 hours per day – 5 days a week. Forget about work and boss, enjoy life with friends and family after work and on weekends. Tomorrow, take it as it comes. Resign and move forward if things don’t work out.

As an Entrepreneur, it’s actually work right from the time you wake up to the time you go sleep. Once you become an entrepreneur, your mind is always thinking what next; sometimes for growth and other times for survival. It’s strange many of us want to become an entrepreneur because we want freedom of time. Although we can take leave whenever we want, go to office late etc… But that really does not translate into freedom from thinking about work & business.

According to me, freedom of time in real sense is much higher as an employee than as an entrepreneur.

One of my friends was sharing about his relative who has started a restaurant business in Dehradun. Because he is the “chef” himself, the weekends are non-existent for him now. His business is such that the shop has to be opened almost every day.

Either he has to wait for his business to become much bigger when he can hire a staff who is as good as him or wait for some extreme situations or get SICK in order to enjoy a day off.

Also, some businesses are seasonal and their peak business happens in the holiday season. So be ready to forget holidays or full off time during the holiday season. This depends on business to business also. Imagine that you start a business which is related to “Gift items”. In that case, you will be super busy in all holidays. For you Diwali, Holi, New Year and this kind of time do not mean holidays, but double shifts!

So if work-life balance matters too much for you, a job is a wonderful place.

Note that while you sacrifice the work life balance in the start of your business. Once its established and things are in place, you enjoy a great amount of work life balance. Then you can be very flexible in your office timings, you can take off whenever you feel like and work on days as it suits. It gives a lot of flexibility to you.

#3 – Steady and Stable Income

One of the things many salaried employees do not appreciate well enough is the steady and stable income that comes with a job. Each month, you know how much you will make by the end of the month. You know that till you have your job, your income is assured and it will come without fail.

The business risk which your company takes or any short-term problems which happen with the company do not impact your paycheck. This also means that you can plan your life in a more clear way. You know much EMI you can handle, you know how much expenses you can do, etc etc.

However, in business, it’s a roller coaster ride. It’s like an equity mutual fund chart, where you know deep down that while in long run, you will do well and things will be in place, in the short term you have to face a lot of volatility. A good month/year does not mean that the next month/year is also guaranteed.

Business uncertainties sometimes can be very painful and can put you in a situation where you start wondering why the hell you are into business. This is more true in the businesses where you also have to deploy too much investment and the income stream is very volatile.

Checkout out more on this, in this video by Ankur Warikoo, the cofounder of nearbuy who shares his real-life experience on this matter

No doubt that over the long run, the business can give you an amazing payoff. Your income from business can be huge and you will forget all the initial painful years, however this an important point to consider.

I asked Amit Singh, an entrepreneur who runs a WordPress design and development Agency since 2009 to share his comments, and here is what he says.

To me, there are two good things about the job

1. Assurity Cashflow, that is as long as you have a job, your salary is guaranteed. This allows people to plan and focus on the work at hand. Another major advantage of this is that you get to take loans from banks easily for big-ticket items like Home or Car.

2. Time for hobbies, while this may not always be true but while I was working I used to regularly write blogs to share my learning, and build interesting side projects for myself just for fun.

If you are someone who needs a very predictable income, the job will give you that.

#4 – Flexibility to move on and easy withdrawal

If you are not happy with your job and can’t stand the stress, it’s comparatively easier to move on to some other company, role, or location.

In the end, you are not married to the company you work for. You can take the decision to move on to something else because at the end of the day you are a resource. The way you are replaceable by the company, even the company is replaceable by you.

You need to start the job hunt, plan out things, pack your bags, and move on. I am not saying that it’s a cake-walk, but there is a good level of flexibility on this front.

However, when you start your entrepreneurial journey, there is a good amount of financial & emotional involvement from your end for your venture. You give you time, effort, mind, soul. It’s like raising a baby. You can’t just leave it in between and move on.

If things start going wrong or if you face challenges, you get to fix it and stay in the mess. You cant back out so easily. I don’t want to sound as if I am trying to say that job-switching does not have its own challenges. It surely does! , but in comparison, there is a huge advantage in the job.

So if you are someone who enjoys this “weak attachment” and appreciate the flexibility to move on to something easier, the job is for you!

But let me also point the bad thing here. Even if you are working well, doing decent – there is always a risk to get fired from your company for various reasons. In the end, it’s not YOURS.

That thing never happens in a business. Jaise Bhi ho, Apna hai!

#5 – Social Standing & Recognition

“Hi – I am AVP of XYZ corporation” draws much more attention in social circle, than a “Co-founder of an ABC Struggling startup”.

If you are holding a key position in some big company, people want to talk to you, be friends with you and invite you for various events. You are also recognized on social media and getting this attention often pampers you and acts as a motivation for you.

You get your identity due to your designation/brand. Also if you are handling a key position or managing a big team, you also get a chance to experience giving orders to others and command things. You handle people

In business, this social recognition will come very late or may not come every. When you leave your big position in a company and do a startup on your own, it’s like from a happy, glossy Karan Johar movie, you are in a dark, realistic Anurag Kashyap movie

Let me give one more shot at it!

From Varun Dhawan of Humpty Sharma Ki Dulhania, you suddenly become Manoj Bajpayee of Gangs of Wasseypur.

Here what Mahavir Chopra who recently started beshak.org after leaving his job at a very big company shares with us

Entrepreneurship is an extreme sport. It’s a mental shift. It’s a rollercoaster journey of finding yourself that is not for the faint-hearted. When you take up an entrepreneurial journey, you are changing who you are.

You are no more the senior guy working in that successful company, who called the shots in the system and things worked. You are unarmed, you are vulnerable, you are naked in front of the world. From you representing a large company, a tiny company now represents you.

The romanticization, glorification of an entrepreneur shown in movies, shouldn’t be the reason you want to become an entrepreneur – that way all of us should become gangsters or serial killers :D. You should become an entrepreneur if you are ready to unlearn, rebuild your self while building an organization that generates value from scratch – when you are ready to test your strengths in the real world, you are ready to face your weaknesses.

If this social standing or commanding position is something you enjoy a lot, the job will be a perfect place for you.

#6 – Move up the ladder and access certain kind of roles/work

When you are in a job, you mostly move ahead and up the ladder.

If you are extremely skilled in something and your domain knowledge is incredible. Then as you move up the ladder, you can get a chance to lead a big team in your area of expertise.

If you feel saturated in a particular domain, you can think of trying out another domain in the same company or the same domain in another company once you switch the job. You mostly experience “progress” in your career when you are in a job.

Also in Job, you can use someone else success and hard work to lead a role that you want. You can let the business uncertainties be handled by someone else and dedicate yourself to learn a new skill of your liking (obviously it has to be related to your work).

For example, let’s say you are a good software programmer and have designed great front end websites. Now if someone doing a new startup, and you want to give a shot at leading the planning and creating of the front end of the startup. You can join the startup and fully focus on that new thing you to add to your resume. You can let the business owner worry about the funding, company future, salaries, and other things.

However, when you start your own business, you often start from scratch the rebuild things. You first do down, then move up which is quite volatile.

Let me explain with few more examples (ahh.. its not an easy thing to explain)

If I want to explore “teaching” a bunch of students. It’s almost impossible to do if I open my own school. I will then be running around for things like hiring teachers, renting or buying land, construction work, managing staff, design of curriculum, making a marketing plan for the school, and whatnot. I can’t be a teacher then.

If you want to lead a team of 20-50 people. Then if you are an expert in your field, then there is a possibility that within a few years you can move to another job where there is an opportunity to lead a big team.

If you think of starting the business, you have to first deal with a lot of petty tasks before you can do that years and years later. You will mostly be busy with so many things that you will hire someone else to lead the team at the end of the day!

I hope you are getting what I am trying to say. In a job, there a nice chance of incrementally become bigger because of other efforts and setup.

Here is what my friend Ameya Dhani says, who worked for more than 15 yrs and now started his own business as an Industrial solution provider

When I was engineering student, I always fascinated about corporate culture and dreamt of working with MNC. I was fortunate to have my dream come true and had chance to serve in Corporate offices of MNCs at various levels in my job tenure.

Working in a company will give u readymade identity at the professional & social world. You will have the knowledge required for completing your assigned task and if required, company will upgrade/polish it through their internal team or consultants. This will help you to learn new skills to master the task.

As every employee is responsible for the task assigned to him, this reduces the burden which helps in having a better work-life balance. At MNCs, at younger age you can sometimes visit new countries, meet new people and gain better knowledge of world. Also with job, its possible to have a better lifestyle at younger age. Timely salary and perks are icing on cake.

#7 – S0cial Life & Atmosphere

If you are doing a job, it’s almost a given fact that you have some office friends, a happening office atmosphere, birthday parties of friends, monthly/quarterly eat-outs, and yearly outings once in a while (obviously not in this corona phase)

You are part of a buzzing environment and there are people all around you. Even though you spend the highest time at your desk, you don’t feel lonely. I remember every day in the office we friends used to meet in the cafeteria and engage in silly chit chats while gulping that juice and sandwich. I remember my office friends, colleagues, and the whole ecosystem which used to give me a nice feeling.

Welcome to Entrepreneurship, which is often a lonely world!

You start working out of home, or some shared office or a tiny office which is nowhere close to that swanky office, and on top of it, you are paying the rent. You miss that big-office culture and often that can be tough to handle if you are too used to that kind of life.

A lot of people do not think about this small aspect, but for some people, it can matter a lot.

It takes time to reclaim that level of social life in your own business unless obviously you are starting your business with funding money and get a big team and office from 1st year itself.

#8 – Corporate Perks

When you are in a job, you also get tons of perks

Apart from various small perks, I want to first talk about two major benefits which are health insurance and EPF

One of the biggest perks, when you work in a job, can be the free group health insurance which covers you and your parents from day 1 for all kinds of illnesses. You know how big a perk this is if you are not getting health insurance for your parents or yourself when applying separately.

Another big perk is the automatic investments which happen in form of EPF. For most of the employees, a forced EPF deduction is nothing less than a big boon. At least this way they have some investments happening every month and over years, it compounds to a very big amount.

Let’s see what my long time friend Animesh Gautam who started his own business around 2 yrs back (after 13 yrs in the job) says

For me the most important think I relished about the Job was the PF contribution that were made compulsorily, it helped me at finally arriving at the decision of quitting my job, as the contributions in PF after 13 yrs of work were considerable enough to give me some financial stability and I was then able to take calls independent of financial constraints.

Then there are many small perks and advantages like

Free/Discounted food

An unlimited doze of free tea/coffee/cookies.

Creche

Free office cabs

Free Life Insurance

Corporate tie-ups with restaurants and brands

Gym Memberships

Tie up to get easy credit cards

Tie-ups with various loan providers

Being in the job, people really never appreciate how fast they get a loan by just giving their form 16 and ITR for last 3 yrs for any kind of loan (for business people its a headache to prove that they can repay the loan, we have to give our company balance sheets, income computation with CA attestation and what not!)

In short, there is a good amount of pampering happening which often you don’t realize.

One of my friends who works in the IT sector also mentioned that she is missing the super comfortable office chair in this WFH period. She never realized it, but only now.

I don’t know how true it is, but my Delhi friend said that many people in the North also love the fact that their offices are fully AC which they miss when they are back home (if they don’t have AC at home)

When you start your own business, you often start from a lower base with all these benefits and amenities gone. But once you are established with a nice office and staff to take care of things, you get some of it (still not FREE)

#9 – Set back due to mistakes or external factors is lower

In a job, the impact on you, because making a mistake is much lesser compared to a business.

Any mistake on your end will mean a direct loss to your company and an indirect or a delayed loss to you. It’s not that your next paycheck is at stake.

Even when there is some big mess up from your end, the maximum you can lose is the job, but you still have your skills and years of experience with you. Even when you are too stressed due to some office issue or a mistake done by you, you have an option to leave the job and move to some other company and feel guilty for some limited period. The case is closed for you.

Compare this to your own business, where you have to deal with the mistake and fix it. You cant leave it!. Also, the direct impact is on you.

#10 – No financial Investment

Finally, a very small benefit of a job is that you can do a job without incurring any financial investment. You just need the skill and that’s all. The best example of this is the restaurant business.

Imagine someone took up the job of a restaurant manager in a new upcoming restaurant.

Due to the corona pandemic, the setback for the restaurant manager is only his job. But for the restaurant owner, it may be a loss of huge capital.

So a job gives you an opportunity to earn money without any financial investment.

But if you want to do business, you should be ready to invest money in most of the cases

Apart from the 10 points I mentioned above, I also want to talk about a few more things .. Let’s see those

Am I glorifying Jobs?

When I finished writing this article, I felt as if I am glorifying jobs and giving an impression that one should not attempt doing business and always be in jobs as they are so great. However, I am just trying to put a point that you should love and respect your jobs a lot as they are amazing in certain aspects.

People in jobs will surely have a limited upside on their salaries (apart from exceptions) compared to a business person. Almost all the rich people in India are business owners and not a salaried class. However, there is no written rule that everyone should aim to become a billionaire. You can lead a happy and content life even being a salaried person and that’s absolutely fine.

Businesses even though have their own limitation score on many points which is not the agenda of this article and I am not going into it for now.

“Entrepreneurship is always better than just a job”

This is surely not true.

When we hear about entrepreneur stories, we often hear about the big success stories which are worth billions. We will hear about Bansals who used to be in a normal job in Amazon and who are now worth billions of dollars. But we will not hear about other folks who also used to work for amazon and left their jobs to start businesses which never took off and they had to return back to jobs and no one knows their stories.

No doubt that entrepreneurship has the potential for a very big payoff if things go in the right direction. But it’s not for everyone and should not be attempted just for the sake of trying.

There are tons of struggles in starting your own work and most people fail at it. Also, small successes are often not celebrated enough. You will not hear about the guy who left his job to build a 4 cr company and a team of 8 people after 12 yrs of hard work. You will not hear about the 2 partners who are making 5 lacs a month each after going through the hardships. These all stories are not “success” as per the startup world even though 99.9% of people end with exactly that kind of results.

In the end, it’s a decision between what you want to be – a “Small-time entrepreneur” or a “Big-time employee!”

You can be an “entrepreneur” while being in a job

Think of it like this.

An entrepreneur exists only because of the people who do the job. No entrepreneur wants to work in isolation.

He wants to have a salaried team that will help him grow his work. Salaried people are the backbone of any company. What you need is the mindset of entrepreneurship to make tons of money and command lots of respect.

Do your work as if you are the owner. Think from a business angle and contribute. You will become a valuable part of the organization and your compensation will also grow and be linked with the business.

Aditya Puri of HDFC bank was an employee, but his attitude was of an “Entrepreneur”. He retired with 800 crores worth of company stocks.

Sundar Pichai is also a salaried employee of Google. But he acts and thinks like an “Entrepreneur”. Last year, Pichai was granted a $240 million stock package on top of a $2 million annual salary.

If you create value and work with a giving attitude, then you automatically become an “Entrepreneur”, you don’t always have to start your own business.

I hate my job, so I want to start my own business

“I hate my job” is the worst reason to start your own business.

Most of the people who succeed in their “business” are those who were quite happy in their jobs.

They didn’t leave the jobs because they hated it. They left it for a bigger reason. Maybe they wanted to be in a commanding position, maybe they wanted to experience the tough path, maybe they want to execute an idea which they were not able to do in the job. Maybe they wanted more flexibility in their life which job was not providing them. Maybe they wanted to earn a lot of money, which they didn’t see happening in their job.

If you don’t like your job or are unhappy. Check out what is the reason is and then fix that.

Maybe it’s your boss

Maybe its the company environment

Maybe it’s your salary

Maybe it’s the lack of freedom.

Fix that.

Leaving the job is not a solution.

Don’t devalue the money you earn for the sake of “passion”

Pursuing a passion is highly overrated and full of fizz.

Most of the people who seem to be following their passion are just lucky people who started something and it clicked and they don’t hate it now. It was not a planned path they took.

Often, the stories of “he/she left his job to pursue his dream” don’t look at life realities and the importance of money in life.

You cant pursue your passion with worries of paying the next rent and thinking from where your kid’s fees will come next year. If you have studied well and got your hands on a well paying job, do value it and the money you make from it.

There is no problem is pursuing your passion, but do it with some good planning and once you are financially stable. Else things can go in the wrong direction.

I once came across an NRI who wanted to come back to India to pursue teaching. He had a decent networth. I asked him if he can stretch a bit more and work for 5 more years? He said YES.

I asked him to do that and delay his entrepreneur stint a bit late. That way he would be around 1.5 crores richer because he was able to save close to 3 lacs a month while in the job. I asked him to not devalue that.

I want to end this article with this point that even though I tried to share many benefits of a job in this article. I definitely don’t want to portray that the business world is bad or should not be pursued. All that I have said above is keeping in mind a larger population. There are times in life where all the logic does not work and doing what your mind tells you is the right thing to do.

A job even though has many benefits often puts you in your comfort zone and you are not able to explore your full potential. But anyway, I just wanted to make sure that people love their jobs and respect what it provides them.

We often don’t appreciate what we have in hand and just feel that we are missing out on something which others have.

I hope you will start seeing your job with a new perspective and become more valuable going forward.

I got a call from one of my friends. He was feeling down in life and wanted some help on how to deal with the current negative scenario, he asked me some questions and requested for some coaching, he started with questions like

How can I make more money?

How can I have a blog like yours?

How can I build a successful business?

How can I increase the flow of money?

How can I increase my income and get more clients?

How can I have things which others already have?

In his words I could see, he was comparing himself with others and so I asked him to prepare his IDIOT LIST. I told him that even I was the same a few years back and how I connected with my flow of money.

I asked him to sit with a blank sheet of paper with a question written on the top – “Why that idiot is rich and I am not?”

He started writing about people who had more money, more resources, more clients, more cars, bigger bank balance, and more stuff than he was having (even my name and Manish’s name was in his list).

After he was done, I asked him to empty his mind. I asked him who he would be without his idiot list? (He minus his idiot list)

He said, he will have freedom.

An Empty mind will lead to wealth creation

I asked him to GIFT that very same freedom to himself, because only an empty mind, a free mind can lead to wealth creation, only an empty mind can get him peace with himself.

You can’t create things if you are having a war in your mind. I told him, first your mind has to get free if you want your mind to serve you. The process is simple, write your thoughts on paper, and question your thoughts till you experience freedom.

More money, more business, more income, and more clients were not his real business, his thinking was his real business and I asked him to focus only on his true business – “his thinking”.

I kept asking him to work on his thinking, to hold a clear mind, once the mind is clear all the good things will happen on its own. I asked him to get rid of his idiot list. We see the world, compare ourselves with others and that is where the problem starts if there was nothing to compare there would be no rich or no poor person on this planet.

Every single person who you meet on the street wants to make money, in fact, a lot of money. I think it is your right to be RICH but then why do people struggle in the area of money.

“Making money” is a myth

Consider that in reality there is no “making money” in life because the money is already out there. All the Money is out there and now you simply need to fill in your little bucket between the age of 25 to 52. (The range can be different for you)

Let me share some elements we covered in our coaching conversation, maybe the elements can help you to fill in your MONEY buckets.

Consider that money has a flow to it. It has a rhythm to it and no matter how hard you try to hold on, it will find its way and continue to flow.

If you are experiencing any kind of struggle in the area of money it means you have disturbed the flow of money in some way.

People think our job is to spread financial awareness, write articles, make financial plans, and coaching people. No, our core job is to help people to connect with their flow of money.

Here is something you can do to connect with your flow of money

1. Stop trying to have money and just be like Money

Really stop trying to make money and start to be like money. The money will flow from you to me and from me to you, it passes through the phone, it passes through the plastic cards, it passes through wires and it crosses countries, moves from one company to another. It sees no limitation it simply flows.

Everything around you right now someone has seen the opportunity and filled his or her bucket with the money earned. The more you get in touch with the flow of money the faster you move towards wealth.

When you are like money you will find that Opportunity is always knocking and you just need to open the door. The computer on which you are reading this article someone saw the flow of money in it, the software, the internet provider, the chair you are sitting on, the phone that you own, the food that you had today.

There are so many businesses to be started, so many services to be offered. If you can see money in everything you will see opportunity in everything. Wow, this is what happens when you start to be like money. You will feel the flow right now at this moment. Take some time and make some notes if some new thoughts came to you. The flow is touching base with you and I request you to respect it.

On hearing the above words my friend said, ” Oh my god, there are so many opportunities, so many things he can do to create wealth and he needs to get rid of his idiot list. I just need to be like money, I don’t need to have money”

2. Love, Serve and Create

You have already learned from Manish about term plans, investment ideas, how to save tax, etc. He is not good but great at what he does. One more thing you can learn from Manish apart from personal finance is these three words Love, serve, and create.

He has dedicated his life to creating Jago effect in people’s life be it personal finance or any other area. He simply loves to serve that’s all.

Earlier we use to work for 7 days a week and we use to hate holidays and Sundays as they take us away from our love, our work. Manish has replied to hundreds of people whom he does not even know and he will never ever meet most of them in his lifetime.

This is being of service to people from morning to night. Being of service should be your 24×7 job. It should be your full-time job or I would say the only job you have.

If who you are is good enough, give yourself to the world; give your talent to the world. Here is how the two world’s are different.

Operating from the Space of love, service, and create

Focus is on what others are having

Focus is on having a clear mind