Jagoinvestor

Jagoinvestor

December 6, 2015

December 6, 2015

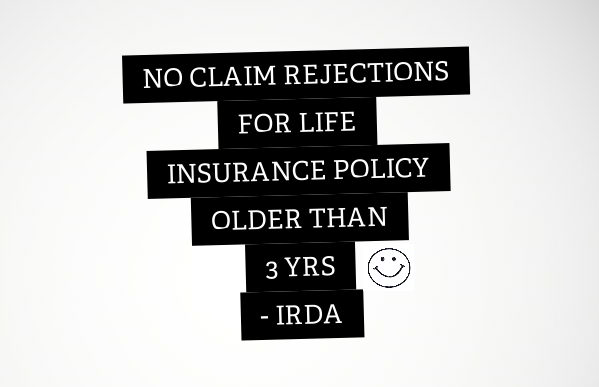

No claim rejection for life insurance policies older than 3 yrs – IRDA

There is very good news for those who have bought life insurance policies (especially term plans). From now on, life insurance companies will not be able to reject claims for any policy which is 3 yrs old.

Yes, you read it correctly.

No Claim rejection after 3 yrs

If your policy is 3 yrs old, no matter what happens, the life insurance company will not be able to deny the claims. There was an amendment in the sec 45 of the Insurance Act 1938, and due to that now onwards a policy can’t be denied a claim because the policy-holder gave some wrong information.

As per IRDA, the company has 3 yrs in hand to detect any misrepresentation or misstatement from the customer side and reject the policy. However, once this period is over, the insurer will have to settle the claims.

What this means is that those investors who were highly suspicious of insurer’s intention and always kept looking at the claim settlement ratio numbers don’t need to worry now.

While this seems to be great news, one should think of what kind of implications will arise out of this change. I can think of a few of them

1. It will not be easy to buy life insurance

The major impact of this change will be that now the medical tests might get more details checking a lot of things. Till now insurers were bearing all the costs, and I think it will happen in future also, however, I think this will result in higher premium amount, which I think investors will not mind because now there is a guarantee of claim settlement

2. Chances of Fraud in the life insurance space

Already, there are many frauds that happen in life insurance space from the customer’s side. I remember an episode of Crime Petrol, where a man planned his death so that his family can get the life insurance money, however, he didn’t get the money because he was not able to execute the plan.

However, with this new change – the chances of fraud and misrepresentation can increase. Imagine a smoker or a person involved in risky activities. A lot of people like these to not disclose these facts because their application might get rejected or the premium might rise. So a lot of people suppress disclosing this fact and it’s going to be a hard time for companies to figure out these things. There will always be few cases which will not come under their radar.

What do you think about this latest development? If you hold a life insurance policy already, how do you see this new change?

What about this news?

https://timesofindia.indiatimes.com/city/ahmedabad/man-lies-about-previous-life-policy-widow-loses-rs-6-6l-insurance-money/articleshow/80127231.cms

Its not been 3 yrs … Insurance company is right in rejection of claim

Manish

I could not find in the article when he took the policy…

It was written that the person died after 1 month of taking the policy!

Dear Manish . having taken a policy of HDFC life Uday one year back, the policy holder dies of an heart attack. He also had an angioplasty three years ago.will he be given his claim with out a problem. Thanks

s satish

The policy has not been 3 yrs old . So we cant say

If the policyholder had not disclosed all facts, then it will not be paid

Hi Manish,

I just to go through your website accidentally & I am impressed with your valuable comments for the queries being raised. I am 33 yrs old & now planning to buy a term insurance for 32 yrs ( upto age of 65 yrs) with 1 Cr coverage. While analyzing in various insurance companies variants, found Aegon to be the lowest premium including the riders. In comparison with other giants such as LIC, HDFC, ICICI & SBI for 1 Cr, the difference in Aegon premium is 60% lesser than the rest. But considering the claim settlement ratio & company recognition , I am confused to proceed. Hence would request your kind advice on this policy. Also, please suggest other suitable policies if there are any.

Thanks in advance !!!

Hi Ajay

I can see that you are thinking of buying a term plan. ALl you need to do is leave your details at http://jagoinvestor.dev.diginnovators.site/solutions/buy-life-insurance-plan

Our team will get in touch with you

Manish

Hi Manish,

I am a regular reader of your website. Recently while browsing through few other blog site, I came across an article on mintwise.com stating that claims settlement ratio is not fully reliable. Here is the link for that article.

http://www.mintwise.com/blog/claims-ratio-insurance-companies-india/

Currently I am looking to buy a term plan from Future Generali but its claim settlement ratio is lower than 85%. What should be the benchmark for this ratio? Can i consider Future Generali for term plans?

Thanks,

Mahesh Nayak

It does not matter now . Now after 3 yrs of policy being in force the claim has to be settled anyways . New rule from IRDA

Even if the policy is taken in 2012 and continuing ?

Its applicable for all the policies – Old and New both !

Dear Manish ji

I purchased a term insurance plan of 50 lac from Max life in April 2016 but my LIC agent says that you purchased term insurance from a private company and all private companies will not give money to your family in case of your death as all private companies aim is earn money only. so please take term insurance from LIC only. please give me your valuable suggestions.

Thats not true. He is misguiding you totally. I also have a term plan from a pvt company only. He wants to sell you only LIC because he gets commission. Dont trust him and change him 🙂

Manish

Thank you very much sir

This is great news for sure and everyone will benefit from it. I would personally suggest TATA AIA life’s Smart growth plus plan which is a very good plan and, it offers flexibility in choosing policy term, has good policy returns and tax benefits u/s 80C & 10(10D).https://www.youtube.com/watch?v=p6taJlYgVgY

Hi Manish,

The above things have been given in exclusions in policy brochure of hdfc, lic n icici pru. Currenyly i have term plan with hdfc n lic. Will it be still applicable because it is in exclusion clause in brochure.

Regards,

Praveen kumar S

Yes, whatever is there in brochure will be applicable

Sir, I have some queries regarding Pure Term Insurance:

1- In term plan which type of death is covered…actually i am confused about which type of death is really covered under pure term insurance, as death is occur mostly due to (critical or by normal) illness, or by accident but for them insurance companies are providing external riders….like critical illness cover and accidental cover etc separately for covering them….

then which death cover they are providing under pure term plan…

2– If one take Pure Term Insurance Plan, then does his/her family will get any money if policy owner decease due to accident/illness after 3 years ?

and what about if death occur before 3 year of policy issued…

3–If claim settles, then does claim paid amount to family equals to sum assured amount in policy(when it issued)?

Regards,

Prateek Varshney

Hi Prateek

I think you have many questions regarding that, if you can pass on your contact number to us , I will connect you to my teammate who will call you and help you in resolving your queries.

Just fill up this form – http://jagoinvestor.dev.diginnovators.site/solutions/buy-life-insurance-plan

Sir can I go cheapest online term plan being making myself sure that after three year all will be settled easily if nothing happens within three first months???

Yes, you can go that.

Let me know if you are interested in term plan , in that case we can connect you to HDFC team with whom we have a tie up for our readers.

Hi Manish,

I have taken a term plan for Rs.1 Cr in Jun 2015 from Edelwiess. I was about to change the insurer this year while due for renewal because they have a bad claim settlement ratio (~55%) . With the above good news I need not have to go for this is what i think now. Could you please advise me?

Sanjay

Hi Manish,

Could you please reply to the above? Thanks.

Yes, you dont need to change it now !

Thank you very much for your reply.

Hi Manish, I started reading your blogs few months ago and these are very useful. Thanks for the good job that you are doing. Requesting your help to clear below doubts on life & personal accidents:

1. It seems that the maximum death benefit coverage that one can get under Life Insurance is 20 times the annual income of the person. Does this death benefit coverage cap also include or exlcude the benefits that can be received under the employer group life insurance policy? Say a person with Rs.10 lakh annual income buys two life insurance policies from HDFC Life & ICICI pru for 1 CR each and also has a cover of 1 CR under the employer group life insurance policy. Upon death will he get 2 CR or 3 CR? Lets assume that he has made all disclosures.

2. It seems that the maximum death benefit coverage that one can get under personal accident Insurance is 10 times the annual income of the person. Does this death benefit coverage cap also include or exclude the benefits that can be received under the employer PA policy? Say a person with Rs.10 lakh annual income buys two PA insurance policies from HDFC Life & ICICI pru for 50 each and also has a cover of 50 Lakh under the employer Health insurance that has a rider for PA insurance as well. Upon death, his max benefits under PA insurance will be 1.5 CR or 1 CR only? Lets assume that he has made all disclosures.

3. Say above person dies due to accident, maximum death benefit coverage that one can get under life + personal accident Insurance is 30 times of the annual income of the person (20 times from Life and 10 times from PA). Is this correct?

Its not like that. this 20 times and 10 times is just a high level guideline. You can also get it more than that if the company is ok with it. But once you have got it, you will get the money later at the time of claims !

Hi Manish,

From when is this rule applicable? Is it from 28/10/2015.

Thanks in advance.

Reagrds,

Veeresh

Its already applicable now . Even for all older policies

Thanks for the info Manish.

Regards,

Veeresh

Hi Manish, Today I have completed medical examination for LIC’s eTerm policy. I have already made the payment. In policy, I have mentioned that,

1) I was admitted in hospital for Typhoid 5 years back.

2) My father is expired due to heart attack.

3) My mother is having Thyroid and BP.

4) My sisters health is not well.

What are the chances of rejection of my policy depending on above points. What LIC can do in such situation? Did I do correct by mentioned all the above truth?

Hi Raj

We cant answer that, It would depend on the underwriting process of the company

Hi Manish,

3 years back, I purchased HDFC Click 2 Protect plan (Online) for my spouse and me of 50 Lakh each.

I didnot get any intimation about medical test requirement on phone, email or through any other medium. Recently I met a sales person of HDFC Life who told me that it is strange that I haven’t gone though any medical test. My policy is still inforce and I am going to continue it.

I want to know absence of medical tests will affect policy claim in any case?

Regards,

Rahul

There is no issue as such if medicals are not done. Medicals are done only beyond a sum assured and age. If you are young, its not required

Manish

Thank you Manish.

I was 29 when policy is issued. No drinking and No smoking profile. May be that is reason.

Should I seek for a letter from HDFC Life that lack of medical test will not affect claim, just to be on safe side.

No there is no need for that..

Thank you Manish!

Well, a good move by IRDA. Insurance companies will now need some kind of detectives as well :))

Thanks for your comment Shravan

Hi Manish,

Thanks for the great info as always.

I am an NRI based in UAE. I checked out the HDFC website to purchase policy online. However i cannot enter anywhere that I am based out of India.

Also, what is your opinion on which riders I should go for?

I was thinking of the waiver of premium rider and disability rider.

Please adivse.

Hi Kevin

Riders are based on your personal choice, What I like might not be right for you, So better you choose which riders are better for you

Hi Manish !!

Suppose I Purchase Term Plan Today. Say after 2 Years I go for some Higher Studies. I will be definitely paying premiums but If something happens during my Post Graduation years, will company pay my nominee the entire amount ? Is there any chance that they can reject my claim since I will be non working that time ?

No atul

There is no reason as such why company will decline the claim. There is no requirement that you need to be working !

Manish

Thank U Manish !!!

Dear Mr.Manish

I have taken one Plan from Max Life and Paid 4 years and after that It was about to mature on Dec-2014.

Before that ,Company sent me mail & SMS to revive the policy for the complete benefit and contacted to company and they replied that they would revert back.

After that they refused to pay me money back and other benefits.

I lodged a consumer case on Nov-2014 and it was judged on 17th Dec-2015,against my request for that mail & SMS .

Now How to file this case with State Consumer forum now.

Guide me.

You need to check this on internet .. Its not a one line guidance ! .

Hi Manish,

I am a software engineer of age 25 . I want to take a term insurance plan , I compared between many companies , I found out that the private players are providing lower premium (Ex : Religare , Reliance etc..,) . But I personally have a doubt , Will the private players still be in market after , say 30 years ?? What is the assurance that they will prevail even then ??

THere is no assurance like that !

Hi Manish,

Since every insurance company is regulated by IRDA and if an insurance company goes out of business after 30 years, I heard that IRDA ensures the customers will not be affected by that. If this is not true, then what is the use of IRDA in customer’s perspective?

Regards

Asha

When you say “ensure” it means that IRDA takes care of all the regulatory things and make sure that a company cant engage in fraud and all . Generally when a company goes down, its taken over by another .. However there is no obligation from IRDA side like this.

Hi Manish

I had taken one term plan in 2012 , and due to the fear of policy rejection , I did not mention the correct details about the reason of death of my father. I stopped paying the premium of that policy , and thought that I will take one new policy.

What you suggest now ? Should I pay the premium of the old lapsed policy ? or shud I tell them the correct reason now ??

Please suggest.

Manish , can you provide any suggestion ?

You can revive the policy now . NO need to take a new one !