Do you know how much money is there in this world?

It’s $36.8 trillion (or 2569 Lakh Crores)

What if you get all this money? Imagine you wake up one day and your bank balance shows 2569 Lakh Crores. However, you also find that you are the only person left on this earth while every other person is missing.

All the malls, all the shops, all the movie theaters, all the entertainment parks, all the jewelry shops, all the real estate, all the fruits and restaurants and everything you can imagine is intact. It’s all available there.

So what can you do with all that money with you?

The answer is NOTHING.

You can’t do anything, because you can only exchange money with something and if you already have everything available on earth lying there and already available to you, the money just loses its role completely. That 2569 Lakh Crores with you is nothing but trash.

Coming back to our life, at the start we do not have much and money is something which can help us get access to lots of things in life. However, we move from having “Nothing” to “Something” to “Good enough” to “A lot” and then slowly “Almost everything we wanted”

In this transition over years, the importance of money comes down in our life. We already have most of the things we can wish for. You already have a house, a car, nice furniture, a second home, great vacations, eating out, etc. etc.

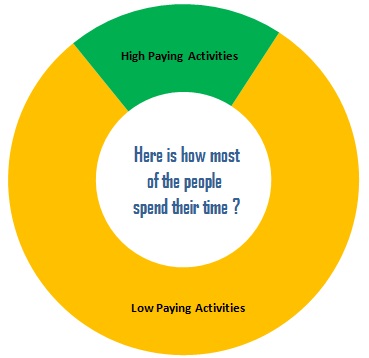

The Race of Earning Money

While money is very important in life, we are conditioned to think from our childhood that money is the solution to everything in life. We are subconsciously in this race of earning more and more money without setting a target. More is always better it seems.

Note that.

There is a limited amount of food you can eat in this world

There is a limited number of vacations you will take

There is a limited number of houses you can live in

There is a limited number of cars you can drive

There is a limited number of things you need to have a great life

How much money do you need?

5 crores, 10 crores, 50 crores?

I strongly suggest that you need to target a number or a range after careful thought and then let that number define your speed. There has to be a number which is ENOUGH for you.

You will be able to lead a very good, desired lifestyle in that much money.

Trust me you will eat the same thing and dress quite in the same manner if you have 10 crores or 50 crores. Rakesh Jhunjunwala or Mukesh Ambani eats the same thing as you do.

It should not happen that you keep acquiring wealth in life, and later it turns out to be nothing more than trash.

The Dalai Lama when asked, what surprised him most about humanity, he said:

“Man.

Because he sacrifices his health in order to make money.

Then he sacrifices money to recuperate his health.

And then he is so anxious about the future that he does not enjoy the present;

the result being that he does not live in the present or the future;

he lives as if he is never going to die, and then dies having never really lived.”

So what is the role of money in your life?

You need to define how much money you are targeting to acquire in your life. How much money is enough for you? Are you in a mindless race, acquiring all the money you can imagine and later, think where did my 60 yrs go? Or you are going to define the range which you want to acquire?

Something like “10 crores” is good enough for me once I retire. This is important because whatever time you give to earn money can potentially go somewhere else.

If you are working later hours for money, and coming home at 11:00 pm at night, then it means that you can’t wake up early and go for an exercise.

If you are working in some other city away from your family to earn a better income, it means you can’t spend that much time with your loved ones

If you are away from home during festivals so that you can earn/work extra, that means you are not going to spend that particular time with your family.

If you are not attending a wedding for your close friend, because you don’t want to lose those 6 days of a pay cut, that means that you will have that money, but then you will not have that memory of your friend’s wedding

If you are not taking your family to a nice vacation, then you will have that money in the bank, but you won’t have something to talk about years later when your kids grow.

Just like these examples above, there are multiple instances in life, where we have to decide between using our money and exchanging it with something.

Your Target = 1000 times your monthly Expenses

A simple calculation tells us that when a person accumulates around 400-500 times of their monthly expenses, they have enough to last for another 30 yrs.

This means that if you have monthly expenses of Rs 1 lacs per month, then 4-5 crores is a reasonable corpus for you. Let’s take 1000 times? So for a person, 10 crores if enough to last his lifetime (a very high-level calculation tells us that). In the same way, you should know what amount you are targeting for yourself.

So make sure you are clear about the importance of money in your life. While we have seen that a lot of people are not working hard enough to achieve all their financial goals targets, we see that a lot of people are putting too much emphasis on earning money and spending all their limited time into the race of earning money. While earning money is not bad in itself, make sure you know how much you need in life?

Question for you

I would like to know from you – “How far are you from your target?”. Do you think money has a bigger role to play in our happiness or a smaller role? Please comment below

Note: Note that I am not saying money is not important. I understand and acknowledge that money brings peace of mind, a sense of security and makes us powerful in away. I am only trying to give a perspective about the role of money in life. I am not saying that earning more money is bad or good. So in case you have hate comment, please read the article once again fully and point of the para or line which you want to debate on.

Here is a guest post from Zubin Ajmera from Progress & Win (detailed bio at the end) .. He would like to share his insights on creating extra income while you are at job.. Over to him.

–

If I have to tell you the latest trends and fantasies of Indians these days, it would be 4 things :-

Going on dating apps (“Forget Tinder, did you check out this new app?”)

Trying a new restaurant (“We should really go to this new cafe opened last month, they serve the most delicious desserts”)

Watching the latest movie (Robot 2.0?), or the new series on Netflix (“Did you watch Sacred Games, or Narcos?”). I mean, look at this craziness

Starting a business (“Sometimes, I feel my manager doesn’t understand it! I just want to quit my job and start something of my own!”)

Today, I want to talk about the 4th — starting a side business. And it’s funny because the moment I tell this, the instant choleric reaction is:-

“Uhh, I’m already occupied with so many things. I don’t have enough time”

“Business?? I don’t even know where to start from”

“Why will anyone pay me? I’m not an expert”

“I’ve an idea in mind, but not sure if it will work!”

I call these Mental Scripts, these are some of the barriers you have in your head when starting anything new.

I don’t necessarily blame anyone for this. The fact is, we live in this “startup ecosystem” where you’ll come across hundreds of sites talking about technology, ecommerce, and mostly hear words like — “funding, investors, seed round A, renting office space, hiring”, etc.

I want to tell you that all of that is possible, but you CAN take a different route. A different route might mean –

Starting a tiny business while still working at your day job (so eventually you’ve an option to quit your job)

Working on something you’re interested in or deeply care about. For eg: I love to research and spend on perfumes. My weird dream is to start a business on it someday. Not kidding, just look at my enrapturing expression when I buy a new one online –

The expression after you order your favorite thing on Amazon

Creating a second income stream

Finding your first paying customer (Apple sold its first iPhone on 29th June, 2007 Flipkart got its first customer in October 2007. Moral for you — It all starts with ONE)

In fact, imagine how life looks like if you have 2 paychecks deposited in your bank account every month. A second income rolling in.

For most of us, the bulk of our fixed income comes from our salary. What if you added one more stream to your income? That one stream might not be equivalent to your salary, but even an extra, say 25,000 — what do you think you can do with that?

Pay for petrol or other bills

Cover up for rent

Buy that extra pair of clothes or shoes

Take someone out for a lavish dinner

Maybe take a short weekend trip to some new place?

Here, I’ll show you what that second stream of income looks for me –

This was from November itself. Each customer worth $50

And let me show you what a business where you’re your own boss looks like for other ordinary people, who are just like you and me –

Deepak Kanakaraju teaches digital marketing through his online courses and workshops

Sandeep Singh sips a chocolate milkshake at a coffee shop, while he finds/reports online security loopholes for tech and ecommerce companies

Karan Batra is a finance expert who provides various tax and finance saving services

Ritika Tiwari is a writer, who provides content writing services for many websites and companies

Google all of them, and there are plenty of others who were working professionals and started as beginners. See more examples here.

Is this a dream “not possible”?

No! With a few simple steps, this is achievable. It’s not even a distant dream, you can start earning more in as little as 6 weeks and build a sustainable income — for life.

Let me show you how.

The simple framework to start a side business (in 6 weeks or less)

It boils down to 3 simple steps:-

Step 1: Find an idea

Step 2: Niche it down

Step 3: Get your first 1-3 paying clients

That’s it. I’m not going to throw 100 different things at you (“start a website, buy a domain, get the xyz discount”) to confuse you further.

I’m not even going to use complicated jargons you’ve never heard of, you really don’t need to when you start off.

It’s kind of like when you start working out at the gym. Your goal initially is not to lose 20 kgs, but maybe a tiny goal to lose 5 kgs first.

That’s the goal here as well. To find an idea, test it, and get your initial clients. Do these 3 steps, and boom — you’ve a functioning business.

And the interesting part is all of this is possible while sitting in your office desk….doing your work…on the laptop…..or on a weekend….or coming home after work….or after dinner….just by spending 5-7 hours per week

Let’s go through the details of each.

Step 1: Find an Idea

Tool required: A pen and a paper (do not ask “what fancy tool should I use?” There isn’t)

Time required: 15-20 minutes

You’d be surprised when I tell you this — 80% of my readers face this challenge, which is coming up with an idea.

“I don’t have any ideas”

“Where should I start from?”

“Zubin, I have an idea, but I am not sure if it will work”

It’s kind of like an “excuse” you make to cover up on not taking action. But you also make it sound “correct” in your head, so you think what you’re doing is right.

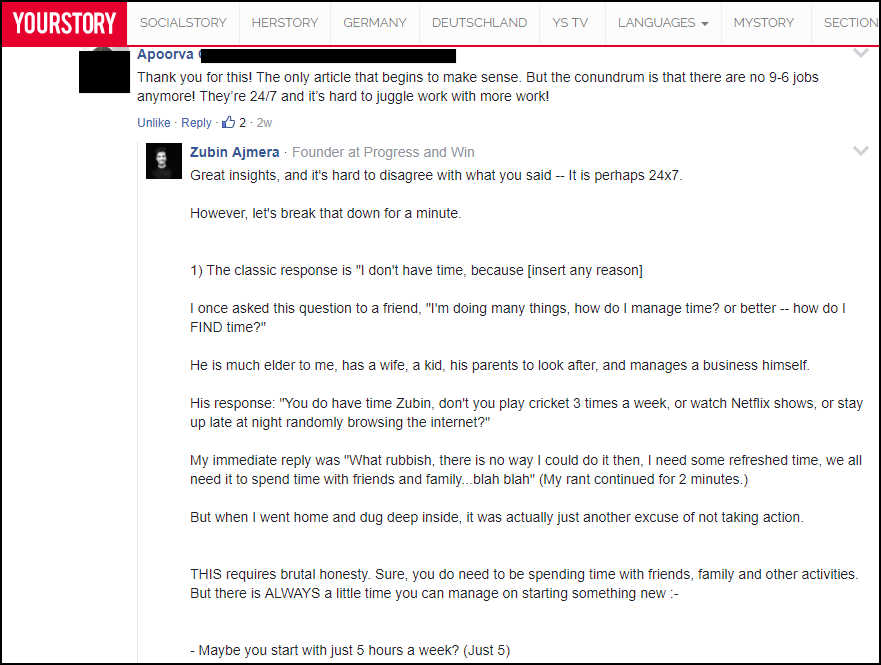

For eg: “I don’t have enough time” is the most common one you’ll find. Here’s an interesting comment on one of my articles for YourStory – (You can check my full response here btw.)

A big part of starting a side business is internalizing your inner psychology and mindset. (And it’s never about “which domain to pick”, or “what the name of your company should be”)

Let me show you 2 simple techniques to come up with atleast 10 different ideas in under 15 minutes. I’ve used them and I still do, many of my readers have, and it continues to work.

One quick caveat is to stop censoring yourself as you go through this process. No telling yourself “I can’t do this”, “I’ll do this some other day maybe”

Much of this is about creativity, testing, taking action, and eventually having fun with it.

Technique #1: The YUS Technique

I call it Your Unbeatable Superpowers (YUS). Each one of us is different. Our story is different — where we come from, experiences we’ve had, people we meet, places we travel, stories we know, food we eat, clothes we wear, etc. This is what makes you unique.

So, how can you monetize these experiences? How do you turn your unique experiences into profit viable ideas?

Answer the key elements below:-

Experiences you’ve gained — like learning algebra or studying architecture, finance or consulting, traveling by spending less, doing interior designing

Skills you’ve developed — like playing a guitar, working on excel, taking better photos, coding in java

Challenges you’ve faced and overcome — like treating foot pain, getting the perfect muscular body, losing weight, learnt to write better

Achievements you’ve been awarded for — maybe you got a promotion, or a high MBA score, or bought a car from your own pocket, or stood first in a swimming competition

Write down as many you can think of.

Technique #2: The Detective Hat Technique

I want you to answer these questions –

What would you do on a Sunday morning after your morning breakfast?

You wake up at 10 am (hey, it’s SUNDAY!), spend another 10 minutes on your bed. Brush your teeth. Take a bath. Have your breakfast.

Now after all this, what do you usually do?

Will you go to the gym? Read business websites? Watch cooking videos? Go to a networking event? Arrange your next travel trip?

Write it all down!

What do your friends/family struggle with and ask your help for?

Do they come to you for design advice? Or ask you about finances? Or they need help with planning an event? Learning how to create excel spreadsheets? Advise on what phone/laptop to buy?

Remember, no idea is a bad idea at this stage. I want you to list down EVERYTHING you can think of when using the techniques. You’re not allowed to

Chalk out any idea

Think “this idea isn’t possible” (How do you know?)

Critic yourself (“I am not an expert”)

We’ll remove some of these ideas, don’t worry. I’ll show you how to identify and eliminate the bad ones. But, we’ll address all of these concerns later.

Right now, just put everything on the page.

Great! With using just these 2 techniques, you now have a list of 10-15 potential ideas. (If you also want to see the Book Shelf and The Flight technique to come up with more ideas, check below here.)

Here’s how your list might look like –

This is from one of my readers. A simple exercise, and you already have so many ideas

Awesome! Pat yourself.

Now, I want you to pick one idea. Do not obsess over this. Pick one idea. Do inky-pinky, or something that interests you, or what idea catches your eye when you look at the list, or just ask your mom (she gives the best advice sometimes trust me) — that’s not the point.

The point is to pick 1 idea to test and validate, and move to the next step. A lot of people get stuck at this step alone. Treat this as a system. You simply follow the steps, trust the process — and you will see results.

Step 2: Niche it Down

Tool required: Just your creativity

So, you’ve an idea. Now, let’s determine who can be your potential customer/client.

In marketing, there is a golden rule penned by author Tim Ferris in his book, which goes — “if everyone is your market, then nobody is your market”

Once you have a rough idea, the next step is to identify the person who will pay you. Don’t go after each and every individual you can think of.

Ask yourself – Who is my ideal client?

Bad answer: My ideal client is 18-35 year-old men

Really? An 18-year old college “dude” has almost nothing in common with a 35-year old professional. They are at different stages in their lives, have different goals, their lifestyle is different, and they have completely different mindsets.

GET REALLY SPECIFIC! I cannot emphasize the power of getting super-specific.

Good answer: 30-35 year-old men who are working professionals

Amazing answer: 27-35 year-old men who are working professionals, in the IT industry, living in Mumbai. They typically work in IT, Banking, Finance companies. They are either middle or senior level professionals in their career. They work largely on these xyz softwares, excel spreadsheets, and emails. Most of them are married. They commute either by train or a bus. They spend most of their time on social media (Facebook and LinkedIn.)

I mean, look at that amazing answer above. I love you already!

The more specific you get, better your chances of early success. When thinking of your ideal client, you want to deeply understand :-

Age

Location

Demographics

Where do they hang out often?

What do they read, watch, listen?

Where do they go to solve their problems?

Type of industry they are in

etc.

Let me walk you through an actual example. Say our idea is — “content writing”

Who is my ideal client? Maybe we come up with –

Marketing agencies who require content writers on a part-time basis

Authors or bloggers who require for their website or a new book

Small scale companies who need for regularly putting out new content for their blog and social media channels

Say we pick the first one — marketing agencies, since the demand for content writers might be more there. Agencies need content writers everyday!

Again, the point I want to emphasize is do not obsess over and over again. Pick one and move to the next step. With a little testing and refinement, you will learn a lot more, than to simply sit and daydream on it.

So, where are we? You’ve an idea — you’ve narrowed it down for a specific market, you know EXACTLY who would be a good target audience for your idea.

Alright, great then, this is a good start!

Step 3: Getting Your First 1-3 Paying Clients

Back in the day, getting a client meant doing some grilling work — months and months of waiting, no response, following up repeatedly, all a dreadful process. Oh, and by the way, how can we forget there was less internet access and penetration!

Today, finding your first paying customers is pretty quick, cheap and easy. Let me show you the cheapest and a free way of getting a client.

Go Direct!

Yes, just go direct — send an email, or meet in-person, or do a direct cold call.

My recommendation: Start with 5-10 emails a week. Can you do that? Don’t answer that, since the answer to that question is “Yes, you can!” So, you better not give me the “I don’t have time excuse!”

With about 30 minutes per day, you should be able to send 10-12 emails (even while watching Netflix on your laptop, OK?).

Let me go one step further and show you an exact word-for-word script to send.

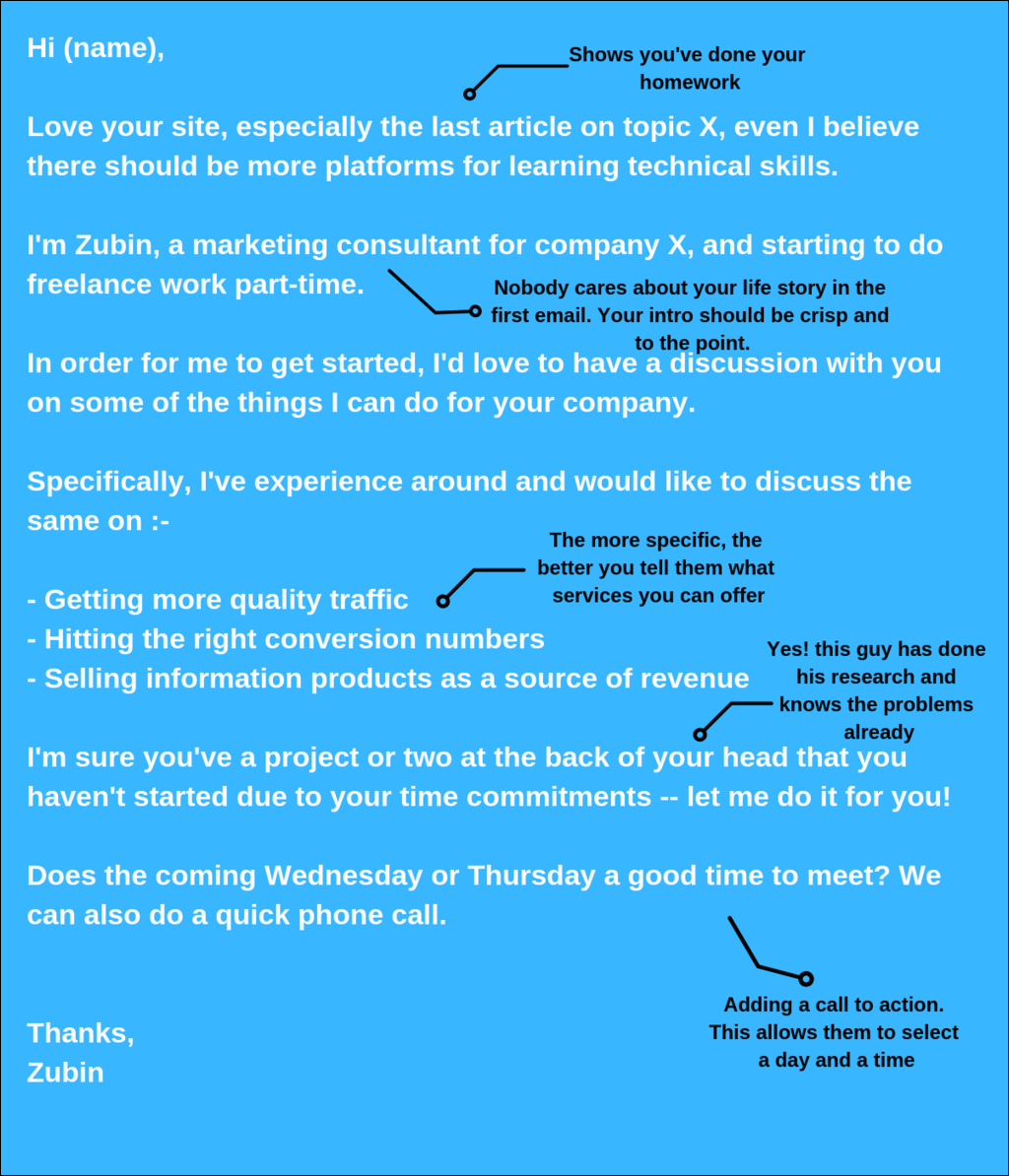

The 5-Point Formula Email Script to Get your First Paying Client

Few things which make this deceptively simple email work like magic –

It’s simple and casual (you feel you’re talking to this person friendly. No “sir”, nothing formal)

It’s not too short, and not too long, yet it covers all important points —

a quick intro

services you can offer

problems he has

benefits to him

a call to action

Not all of your recipients will respond, but a few will, and that is your road to turning those into paying customers

Once you set the foundation of getting your first client correct (i.e. you know your idea is validated, there is demand for it, you’re getting responses to your emails, etc.) — you can then scale. You can get your next 10 or even 100 clients pretty easily.

Conclusion, and Your Next Step

Unlike other “digital marketing” gurus, who preach overwhelming stuff –

“You NEED a website. Here is the 50% discount on the hosting provider”

“Just do affiliate marketing” (Blunt truth: you will not see any results for the first 6 months alteast!)

“You must have a Facebook page!”

These are the same advises I got, and which you will get too.

Instead, without setting up a website or a facebook page or any fancy bells and whistles, which is all for later, start with this simple 3-step system. I’ve used it, many have, and the best thing about it? IT WORKS!

Forget Black Friday, here’s my “give-me-a-slap-if-it-doesn’t-work” guarantee offer: Apply this proven system, and you WILL see results. If you don’t, I’m open to get slapped (just don’t hit me hard, please!)

About the Author: Zubin Ajmera

After his 5-year stint in USA, Zubin returned back to India. He’s a Content Marketer, Founder of 2 online businesses, and startedProgress and Win, a site where he helps working professionals and beginner bloggers start an online side business from scratch, using tested techniques and strategies.

He believes in a strict “no-B.S” approach, has been covered on Entrepreneur India, YourStory, directly worked with 2 authors, 4 CEOs, and featured on multiple other brands.

Do you want to read the story of an investor who has tripled his net worth in just 8 yrs and learn about his great skills in financial planning?

We bring you the money story of one of our readers from Pune, who agreed to share about his life journey and his achievements. Over to him …

—

Hi Manish

First, let me start by thanking you and Jagoinvestor team for running this great learning portal (Jagoinvestor) and giving me an opportunity to tell my money story which may help some of the readers.

A little bit about my family

To give you some quick background on myself, I live in Pune and I am an IT architect by profession working with Wipro. I come from an upper-middle-class background with my father (passed away last year) been a banker and mother being a housewife.

I also have a younger sister who has been married and well-settled. I have been married with a 4- year old kid now and my wife takes care of the home.

My childhood experience with money

My introduction to money management started at a very early age. My father and mother were always advising us both kids to spend it right and all genuine/reasonable demands were met. However, we didn’t get any pocket money any time as we had been asked to ask for our needs and no money was just given to spend as we like.

Even during my teens, we had a simple practice of giving complete account to mother/father for the money that was given to buy any items. So, I have always valued money to be spent and would continue to do that with my kid.

My father was also a good investor in his time even with no internet and mobile phones available. He had invested in some stocks, some land/flat, FDs and PPF during my growing up days. As a kid, when I used to see him receive cheques for shares dividends for paltry sums, I used to ask him what is this that you keep receiving. He used to tell me that you will understand more with time.

So, curiosity started very early.

I got a job in Bangalore

My hands-on work in personal finance and financial planning space began when I started working in Bangalore at a very low salary (~10K in hand) and was always trying to see the best I could make out of it in terms of savings. To me, money saved was always money earned.

So, I looked upon all possible legal ways of reducing income tax to start with and then investments in other avenues. It also gave me a great boost that all friends used to ask me on how best to save taxes. Later, I did the same even when I was outside India by understanding the IT laws of that country and ensuring I only paid required taxes.

Expanding the horizon

As my interest grew in financial planning, I started covering all bases including insurance policies, PPF investments. Interest in investments led to Stocks, MF, real estate and eventually Portfolio Management Services (PMS).

For fixed-income instruments, I keep some investments in Sukanya Samruddhi, NPS, Fixed Deposits and of course PF. I had created cash inflow/outflow projections for the next 20 years and my estimated expenses at various stages considering inflation.

This has led to investing as per goals at various stages like buying flat, child’s education expense at age of 15, 18, 21 and then marriage, retirement corpus, etc.

My Financial Achievements

From where I started (10K per month salary with zero bank balance) 15 years back to today with well-over 6 figures take-home salary, of course, the salary has grown many folds but then expenses have too. My net worth has tripled in the last 7-8 years (my salary went up by 50% in that time), Stocks/MF/PMS portfolio stands over 1 cr, 2 flats owned.

Money attracts money and so, more investments I made, more returns I got. I bought a flat with no home loan a few years back because of the investments made and that gave me great satisfaction.

My Equation with money

In one sentence, my equation with money is to maximize my potential. Be it earning through all legal means or maximizing returns on my investments. Money has and will always be important to me just like others. Having enough money to me means all needs (and not necessarily all wishes) at different stages are met with ease.

Spending money to me means that every rupee spent is worth the object to be bought. When I meet either of these, I am a happy and content man. If I fail on either one, it’s not losing money which troubles me but it’s the standard/process that I couldn’t follow which led to the loss of money.

How my perspective towards money changed

My primary experience with money is that you need to be diligent with money management. When I was not diligent enough with a couple of investments, I made bad calls and lost money. Similarly, informed decisions in investments have given me substantial returns. Like other aspects of life, Wealth creation takes time and knowledge.

You have to be alert and keep reading to understand views from experts. Blogs like Jagoinvestor help a lot when you start on this journey.

Money is not everything as they say but not having enough money brings everyday problems, I believe.

People crib about not earning enough but they don’t know how to manage and invest what they are earning which leads to higher dissatisfaction. Then come compromises on various needs that have a butterfly effect on other aspects of life.

I have seen someone in my family who has retired from a very high post in Income Tax department, still doesn’t even own a single house and not enough retirement kitty which shows not being diligent enough with money management. He lost money in bad investments with no tracking and his family simply loved spending on shopping time and again.

Then came excuses and defensive attitude. That’s the worst case of lack of money management that I have seen around.

Summary of learning

While I am still learning, there are some experiences/habits/ which have helped me and would like to share –

Cover your bases – Before you invest, make sure you insure yourself/family with the right policies for Life, Medical, Critical diseases, House and Car (in that order).

Start Early – It’s been said multiple times that when you start early, the magic of compounding works big time. Make sure you start the habit of saving and investments early even for small amounts. Remember it is a habit and with time, you can increase investments. I started at the age of 23 with saving not more than Rs 1000 in taxes but the habit was developed.

Ask/Look for help – Solid financial planning is not everyone’s cup of tea. Leave it to experts (check with Jagoinvestor team) where required and don’t hesitate in paying small fees for that work. You also get paid for the job that you do because of your skillsets.

Track your net worth – It is critical to track your net worth i.e. difference of assets and liabilities. Similarly, track your cash (FD/Savings Acc, Liquid Funds), fixed (real estate, PF/PPF, NPS) and variable assets (Stocks/MF/PMS/Gold). I try to maintain a healthy cash balance too.

Return on Investments – Your investments should grow when you sleep. Make sure there are no dead investments. A lot of bank balance in savings account looks good but it is detrimental to wealth creation and leads to “money erosion”. Ideally, Your investments should take care of at least your regular payouts i.e. Loan EMI, Credit Cards, Policies premium.

Track your monthly expenses – I have created a simple excel sheet to track all expenses in a month. I then bucket them in real expenses, Liabilities payout (Loan EMI/Insurance premiums etc) and investments (SIP, Endowment Policies, NPS, Sukanya Samruddhi etc). The idea is to capture % of your income from getting allocated to these sections and avoid unnecessary expenses. Typically, I average 35% in expenses, 35% in liabilities, 25-26% in investments and remaining as just savings.

Share with spouse – Share with spouse details of your bank accounts with passwords, complete details of assets and liabilities. You never know when would they need it suddenly and you may not be around. Trust me, it becomes impossible for someone new to find all your investments. I have created simple excel sheets, keep updating them and share them with my wife. I store all physical documents in one place.

Diligence in money management – As there are no shortcuts, make sure you read enough and then make informed decisions. Respect your hard-earned money.

Wealth Creation – The key is to create wealth over a period and increase your net worth. We are not born millionaires.

Aspire, not greed– When you see someone successful/failure in money matters, try to learn. Aspire to be successful but don’t envy or have greed. Don’t lose night’s sleep because everyone makes mistakes. There’s always a chance to make a comeback but with patience and again, no short cuts. I learned this from my father who made all right investments but was still very detached emotionally from those investments.

Follow the right processes and money will follow – Wealth creation is a result or even a by-product (if you may). Following right processes of money management will lead you on the right path.

So, that’s it, folks. I hope my story helps some of you and you can benefit from learnings/best practices I shared. I would like your views on areas that you think I might be able to do better in money management.

Mohit, one of our readers has agreed to share his rags to riches story which will help a lot of you to build the mindset to become rich and do what it takes. Over to Mohit.

—

My story is going to be about two generations and how each view, treats and values money differently. Some background first…

Imagine sitting under a lamp-post or under the stair-case of your palatial home (shared) for your studies, way back in the 1970s? Sounds like a scene from a Bollywood potboiler? Well, this was exactly how my father scrapped through his school and college education.

He was born to a joint-family that had a huge house but no income. A vain father, no mother and zero income; my father’s money story is a true rags-to-riches one in the sense that he had absolutely no support and progressed on scholarships by his college to complete his degree.

Also in true Hindi-film style; the love of his life (then) rejected him for lack of money.

How my father got his first job

In the 1970s, a generation waking up to the post-independence yet pre-liberalized era of working; he got his first job in the then Hindustan Computers (HCL) under its founder, Shiv Nadar. He still remembers fondly that his employee code was 0002, i.e, he was HCL’s second recruit.

My father faced such money hardships in his childhood that the only objective in his life was to acquire wealth. But there were no equity markets or organized financial planning back then. One invested in real-estate of whatever surplus they had, and he was no different.

My father started his own business

After a brief stint with HCL, my father decided to venture out on his own and set up a small logistics company (for the uninitiated, logistics is responsible for import of goods in India from a foreign-country and vice-versa), and again as my father fondly recalls now, the first month’s profit he made in 1980 was fifty thousand rupees!

That was more than what he earned in his five years in his job! Therefore he immediately recognized that business is the way to be if one wants to make more money.

From the early-1980s to the early 2000s, i.e. in a span of 20years, he made the tables turn in his favor and even though he did not make an Ambani out of himself; he acquired a 9-digit net-worth starting from absolute scratch. As much as I am proud of his achievement, I objectively analyze his money journey and mistakes in following bullet points –

My analysis on my father’s money journey – “Achievements and Mistakes”

He was never a big risk-taker. So his entrepreneurship success is a bit surprising (no risk = no gain) to everyone. Yet as a close observant and first-hand beneficiary; I attribute it to immense HARD WORK! Really he amplifies the cliche that there is no substitute to hard work. I have seen him work weekdays and then Sundays too.

He made some mistakes in businesses like a factory went wrong, but he knew what his A-game was and stuck to his guns. Often people over-diversify (even in investments) but he invested his majority time to the business he knew best.

He had absolutely no knowledge of shares. But he did make some IPO investments on advises etc but they never yielded any returns. It happened with endowment plans from LIC etc.

At the “right” time, he made some real estate investments, which paid off big-time and are the real reason behind his swelling net-worth.

The best part was – he was never a miser. I don’t recall a single day during my childhood when we felt we were missing anything for lack of money. He spent on cars, jewelry, travel, and the typical good things of a lavish life.

Typical old-school style, he kept his entire money either in property or in spending; which I often remind him as a mistake.

Cut to 2004 – This is where my own money story begins.

Having seen his business success story (which as a child, I often took lightly. I didn’t quite acknowledge that making money is this difficult), I had a few things clear to me –

Born to such a successful person, the benchmark was quite high.

My mother kept reminding me the importance of money during my growing up years, and so, making huge money was always a priority.

I was eager to get out of the world of business and take our net-worth to the next level, i.e, 10-digits!

Just like my father, I knew business was the way to be and set-up my venture in December 2004 (although I had a kickstart – firstly space was provided by him, secondly I didn’t have to be the breadwinner).

Again the first few months were so profitable that my self-belief was sky-high. In fact, I became over-confident, or maybe a better word would be snotty. Yes, today I can admit it; even though back then I didn’t realize it. So I set-up another business. And then another.

I wanted to become super-rich and in super quick time that I started losing sight of value-addition by my business. I learned 2 important lessons.

Lesson # 1: Never take things for granted

A couple of years later, my businesses started going downhill. I had to shut down a couple of them and like my father before me, I focused on the A-game. Thankfully a new trade-lane emerged in India and my business and money-journey started improving brightly.

As it became more consistent, I again ventured out in a couple of new fields. Whatever surplus I had, I either put in my businesses OR in bank FDs. Looking back, I am shameful to admit but I didn’t utilize India’s maturing equity markets especially between 2008-2010 period.

In late-2013, I had my first brush with mutual funds. Through a banker (I still credit him for bringing me to equity), I made my first SIP and my first lump sum mutual fund investment. Because the markets grew rapidly since Modiji came to power, my investments swelled handsomely.

And that’s when I made another mistake – I shifted all my FD money into equity. My 7-digit portfolio was 100% equity, full of mutual funds, NFOs, direct stocks, you name it!

Lesson # 2: Take financial planners seriously

Thankfully, better sense has prevailed since then and I have deliberately re-designed my portfolio with a 50:50 equity: debt allocation in late 2017.

As things stand today, I am doing two businesses and while the first one is doing great, second is still in nascent stages. My money is invested in these two, with no investments in real estate or FDs. A third stream is markets (as shared above, 50% equity and 50% debt) with running SIPs.

As of March 2018, I am proud to share that my own net-worth (not counting father) is nine-digit itself and the aim is to attain 10-digits by 40 (I am 34 now). That’s when I shall hang-up my boots and stop working for money.

Am I happier today because of my high net worth?

Personal happiness is a state of mind. When one is feeling rich (not only money-wise but overall), then one is bound to feel happy too. In that sense, I do attribute a lot of my happiness to my growing net worth.

I have never been too much into ‘brands’ or ‘consumption’ per se, yet it is mentally comforting and moral-booster to see your net worth grow. So yes, I will agree that happiness levels have increased definitely with growing money in the bank.

However, there is a very thin line to be identified here. One tends to cross that line unknowingly (as I did at the little success at the beginning of my career). If one gets obsessed with their money-success, then it captures your mind.

You start expecting more out of yourself every day, and in the process – keep pressurizing yourself. So the trick is to find the “right balance” and acknowledge that you are separate from your “material success”. Appreciate the money success, yet keep reminding yourself that it can all go wrong tomorrow – so don’t bet your life on it.

Rich have their own set of problems

A lot of people tend to feel that their problems will vanish once they get rich. This is largely true as well, however, once you settle into “the rich” life, a different set of pressures and problems will take over. Your lack of resources for foreign travel or a Volkswagen car; will be taken over by problems of beating your neighbor’s car or foreign travel with a business-class flight etc.

My point is – money problems will disappear temporarily but new ones will soon take their place. To counter it – always try and live a lifestyle one-level below the one you could afford. If say (in the Indian context) there could be five levels of income, and you are on the fourth level, then try to deliberately follow a lifestyle you deem fit for third-level income.

Those ways, your ‘money problems’ shall always be 1-step behind you.

10X money definitely can bring 10 times comfort or even 10-times security; but definitely not 10 times happiness. Unless again, your life is one-dimensional (i.e. only about money) which is definitely not the case with anyone.

Some money lessons out of my own experiences

Don’t become a philosopher, before you become rich. Nobody listens to a poor philosopher. This implies that one needs to get rich (whatever an individual’s definition of rich maybe) in life, to be taken seriously. You can reject the notion of “money is not important” only after you have conquered it.

Beyond your line of work (business, job, professional – whatever it may be), you need to develop a passive income. It can be through equity markets, interest income, rental or combination of all. One must aim that such passive income can match their monthly-expenses at some point in their life (earlier the better).

Do not consider your ancestral wealth as your own. At best it should be your fallback option. I speak this not only from my own experience, but n number of observations out of families around me. By the time you inherit it, you have lived past your prime life (i.e. past your 20s and 30s, even 40s). Also, you have to carve your own identity and make your own money for improving your self-worth.

Living on debt or on a monthly paycheck-to-paycheck can be mentally demoralizing. One must have a decent amount of savings tucked-up somewhere, to live with dignity and a sense of security.

And finally, DO NOT think of money as the only thing in life. One must value the balance of life very highly. It is of no use to have a high net-worth when you are occupied with it 24*7 or are living an unhealthy lifestyle plagued with physical problems. Always try to create equilibrium between money/income, health, close-ones and entertainment (travel, a hobby or something etc). I especially emphasize the last one as I have known people who are so much into their careers that they do not know how to spend their spare time, or what to do on their weekends except watching tv. That is quite sad.

Let me know what did you learn from this money story?

What is your money story?

I hope everyone has learned a lot from his story.

If you want to write your money story, Leave your details here and Jagoinvestor team will get in touch with you with the next actions.

Are you looking for selling your old used car? Are you wondering how to get the best deal for your 2nd hand car?

Today I will share with you 4 different ways you can sell your second-hand car and also share the pros and cons of each option.

But before we move ahead, it’s important to point out that when you sell an old car, there are few things which matter and should be taken into consideration. It’s not always the money you get by selling the old car which is to be maximized. It’s not the top priority of all the people.

Yes, price matters. But then a few more things matter.

Sale Price

Convenience

Documentation and RC transfer

Safety and Security

How fast you can get money in your account

Speed of Transaction

So these are 6 things which you look at when you sell your old car. Sometimes you need money fast, sometimes your preference is the convenience it takes to sell the car.

Sometimes you are not in hurry and can run around and you want to maximize your sale price and for some people, it matters that the whole transaction should be safe and they should not get into any trouble.

There is no “best way to sell your old car”

One important point to note is that there is no single best way to sell your car. In some situations, you can get a great deal when you sell your car directly to the end-user. But in situation, it can be the dealer who can offer you the best price. Sometimes, it can be online and some times it can be in the exchange offer.

If you want to watch a video on this topic, below is a detailed step by step process I have created.

Let’s start our discussion.

Option # 1: Selling a car in Exchange Offer

When you buy a new car, you can sell your old car in an exchange offer. They buy your old car for a price and deduct that amount from your new car price. You have to just pay the balance.

However, this is not so simple. Let’s dive deeper into this

There is something called “Exchange Bonus” which most of the showrooms give you which makes the whole thing very interesting.

So apart from the old car price, you also get an exchange bonus which increases your net price of the old car. However, the exchange is not always available and depends on the new car which you are buying.

So to sum it up,

Total discount you get = Old Car Valuation + Exchange Bonus

Here is how it works

When you want to buy a new car, the car showroom will do your old car valuation first. They will screen it various parameters and then tell you how much they can offer you for your used car.

On top of this, they may have an exchange bonus also in offer. It’s mostly available for cars which are already established as brands or towards the year-end when its time to clear the old stock (the old year model) or when some new version of the existing car is going to be launched (like New Swift)

But there is a problem, the thing is that the valuation you get in exchange is generally the lowest you can get. You can get much better pricing generally if you try to sell an old car in the open market. But let’s talk about it later.

Also, know that a discount is usually available most of the time, so even if you do not sell your old car, some discount you can get just by negotiating, hence the “Exchange bonus” is not something extra you get. It’s more of a marketing gimmick or a trick to give you a special feeling.

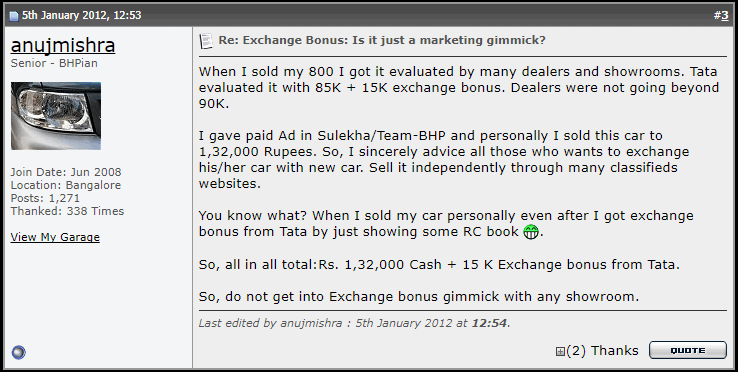

Here is a snapshot of a car seller confirming this point on Team-BHP thread (one of the best places to discuss and learn about cars)

When you sell your car in n exchange, you get high convenience and it saves you a lot of time, and that’s the reason you get lower valuation almost all the time. But if there is a good exchange bonus available, then the final deal might be ok (if not the best)

However when an exchange bonus is not available, its almost the worst pricing you get in exchange.

For example, suppose you want to buy a new car which is worth Rs 7 lacs and you want to exchange your old car. The showroom person tells you that your used car will fetch Rs 2 lacs and there is also a Rs 20,000 exchange bonus. So your total discount is Rs 2.2 lacs and you need to pay just Rs 4.8 lacs (7 – 2.2)

Pros of selling car in Exchange offer

It’s an extremely convenient way to get rid of your used car. All the formalities are taken care of by the showroom

You need less money to buy a new car. The amount you get in exchange is automatically deducted from your final price

It’s a safe way to sell your car, no worries of getting it misused or RC transfer

You get discard old car as soon as you get the delivery of your new car

It’s a good choice if your car is very old and not very famous

If good exchange bonus is available, then it can give you a very good deal overall

Cons of selling car in Exchange Offer

You get the lowest price for your second-hand car when you sell it in the exchange offer, especially when there is no exchange bonus

Not a great option if your car is not very old and is quite popular (swift, i10, Alto)

You can get manipulated in buying a bad option (some car which is going to get discontinued soon) by offering you a good exchange bonus which might look great.

Things to Remember

If your car is not very old (below 5 yrs) and it’s a popular brand, then do not sell it in the exchange offer, because you will not get a very good deal

You will not get any exchange bonus for newly launched cars or some car which has heavy waiting list. Do not try much

Do visit more than one showrooms of the same car brand to check what is the price they are offering for your old car along with the exchange bonus.

Do also visit a few other brands showroom just to check what valuation they are providing for your car.

While using this option, always make sure you are clear about the new car which you want to buy. Do not get influenced by the salesman talks about other cars and awesome deals you can get on them

Option # 2: Selling used car to local Dealers

The next option is to sell your old car to local dealers in your city. Dealer is someone who buys your old car, makes all the minor repairs, cleans it properly and sells it to another potential buyer who is looking to buy a second-hand car.

So instead of selling your car to the end person, you sell it to an intermediary who makes some money out of the whole process. Its a business and the intention is to maximize the cut from the deal.

There are two kinds of dealerships. First is the organized dealers which are quite big brands like Maruti True value and Mahindra First Choice and second is the unorganized dealers which are small local setups.

Just watch carefully and you will be able to see tons of cars lined up in a ground with a board which might say .. XYZ car dealer.

You can sell your car to any dealer, the price you get from a dealer is generally much better compared to the exchange offer, but you do not get any exchange bonus here. However, still, you can get a decent price.

My personal example

I recently sold my old car (I was the second owner) for Rs 91,000 to a local dealer. I had tried selling it to showroom in the exchange offer, but I was getting the valuation of only Rs 65,000 along with the exchange bonus of Rs 10,000. So in total they were offering Rs 75,000 only (this was TATA showroom)

It looks me close to 1 hour in selling the car and the local dealer went with me to his bank and did the NEFT transaction and I got the money in my account in the next 15 min only. So overall I sold my car in 90 min and got the money in my account. I got the proof of sale, and the RC transfer to a new owner is in the process now (looks like they have sold the car to someone)

I also went to Cars24 but got the pricing of Rs 85,000 only, which I declined as I had the offer of 91,000 already with a local dealer.

When to sell your car to the dealer?

So coming back to the discussion, you can some times get a very good deal with the dealer itself. Yes, its a business for them and they will not give you the real worth of the car, but your time is also important and if you are looking for a speedy fast transaction, dealers can be a good option.

This also turns out to be a great option, especially if your old car is technically working great, but from outside it seems too bad. Like if there are too many dents, scratches, etc. If your car is making too much sound etc. In this case, dealers can paint it, service it well and make it look like a new car and then sell it off at a good price and make money.

Pros of selling the old car to Dealer

Better pricing than exchange offer (without considering exchange bonus)

Very Convenient – Just take your car to them, they will inspect it and give you the quote. If everything is fine, you can sell your cars to them within hours

Its a great option if your car is quite popular because it’s very easy for dealers to sell them to new buyers

Some big dealers give you option of both cash payment or direct bank transfer.

Some room for negotiation (make sure you quote your expected price 50% higher than what you really need)

Cons of selling used car to dealers

If the dealer is not professional, it can turn out to be a bad experience

Often the small dealers will offer you only cash and there is no proof of sale

Important points to note

Do not rush when dealing with the dealer. Take your time and enquire at 2-3 dealers.

Do mention to them that you are looking at other dealers

Always take the sale invoice and enquire with them about the RC transfer and when you will be informed about it.

Note that you can not fool the dealers. They are the masters of the game and they do this day in and out. It’s their full-time job. Don’t try to be smart with them. You can negotiate with them (you should), but don’t try to give them wrong information about cars and how great your car is. They can’t figure out things just by looking at the car.

Option # 3: Sell your car to CARS24 or SPINNY

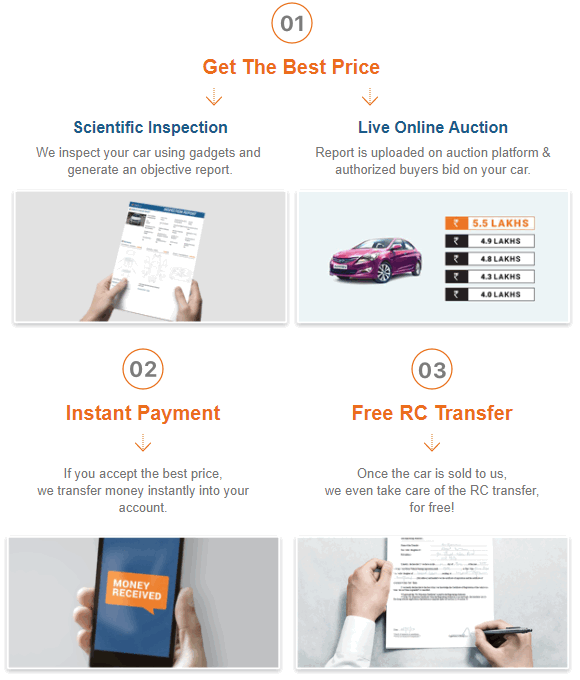

In the last few years, some startups (now full-grown business model) are bringing innovation in the used car buying and selling markets. The biggest player in this market is CARS24 and a new entrant is Spinny. I have strictly chosen these two options because these websites directly buy your car from you and give you the money, without you waiting for a third buyer.

Spinny is a website where you can choose to get your car evaluated. They will come to your doorstep, inspect your car and offer you a price. If you accept it, the payment will be made instantly and they can take away the car. They sell the car to the end buyers (people who are going to use it for their own purpose)

However Cars24 is a little different. with Cars24, you need to take your car to them. They will inspect your car (takes around 1 hour) and then they will make a report which will have all the details of the car, its issues, its good points etc and they will upload that report online.

They have a network of dealers who are registered with them. These dealers can bid for the price and the highest bidder gets the car. Then cars24 delivers the car to that dealer and after that dealer can sell the car to the end party. Many businesses are also registered with cars24 who use the car for taxi purposes for as cabs.

Best part about CARS24

The best part about CARS24 is that its a fast and safe way to sell your car. The payment is instant (within few minutes but Rs 1,000 less) or 2 days (NEFT , but full payment)

The prices you get from Cars24 can be a good price (but not always). As I said, I got a quote of Rs 85,000 from Cars24, but I sold it to a dealer for Rs 91,000 one the same day

However, I suggest you can go with Cars24 if you are looking for a speedy and hassle-free transaction with a “not so bad” price. There are lots of people who are ready to settle for 10% less money if it comes without any issues and risk. You need to decide for yourself.

Real-life experience with CARS24

Here is one real-life experience by Mr. Atul who sold his car in Pune branch. He had some RC transfer issue which you should know about before you want to go to CARS24

I recently sold my car via cars24 Pune Kharadi branch. Let me share my experience.

I booked the appointment, got the reminder message before the appointment. I reached cars24 office on time for inspection. They did the inspection & offered me 2.05 lack. He said is the final max price.I simply said NO to that price because I know my should be around 2.15L to 2.30L.

Then the negotiation started. He came to 2.10 then followed by 2.15 then finally 2.17 L. I still said NO & came back to home. Next day I got the call from the same person he offered me 2.25L. I said yes handed over the keys on the same day. I got amount next day.

Lesson learnt – Although Cars24 executive says its the final highest price but there is certainly scope for negotiation, In fact I would recommend all cars24 customer to negotiate. You can expect 5-10% more after negotiation. They pretend that it’s the final price but it’s not true.

I sold the car in Nov 17. It’s been more than 3 months now. I have been told that RC transfer would take max 90 days. but it’s not yet transferred. Everytime I call customer care they say car is with the inventory partner only it means car is not yet sold to the end user. This is simple pathetic. I keep on calling those guys(1800112233) & send mail to [email protected] but no concrete response. Everytime I get following generic response.

“Thank you for writing to Cars24

We would like to express our deepest regret for the inconvenience caused due to delay in response. We would require some more time in order to resolve your case.

We have also sent your concern/query to the concerned department. We hope this experience will not dilute our relationship and that you will allow us to rebuild your confidence in us.

Please contact us via phone at 1800 11 22 33 or write back to us for any further assistance.

Happy to help,

Team Cars24”

I already got the money, the only concern is RC transfer. Who would be liable till RC is not yet transferred? When I asked the same question to them they say cars24 would be liable but on paper & in govt records car is on my name. Please suggest how to solve this problem.

Overall I would not recommend cars24 to anybody because of RC transfer issue. There is no timeline when car would be actually sold to the user & RC transfer would be done. customer care is really bad. No SLA or escalation matrix defined which can help customer to resolve the issue.

Pros of selling your car to Cars24

Very professional attitude

Speedy transaction (expect 2X time, which is fair)

Instant Payment

FREE and Assured RC transfer .. it’s safe

A good way to inspect your car even if you just want to get a valuation

Cons of selling your car to Cars24

Not the best price (they need to make money too …), but still better than exchange offer

No time to time and wait (if you agree on price, you need to sell instantly .. or at best within 24 hours)

Important points to consider when selling your car to Cars24

Always go to cars24 with 1-2 more offers in hand, so that you know if you want to accept their offer or not

Its suggest to fix small issues in car before you go to them

Always carry various documents which can increase your car worth like extended warranty, servicing invoices for past few months, insurance documents, warranty cards, etc.

It’s better to have 2-3 hours in hand when you go to Cars24. Do not go expecting that process will compete in 1 hour (especially if you are going on weekends)

Always negotiate. They offered me a little higher pricing (only a little).

Option #4 – Directly to end buyer by listing on various website

Another option to sell your car is directly to the end-user – someone who is going to buy the car for their own use.

If you can get an end buyer directly through your network of friends and family circle, its a great option. You can trust the person and the transaction is smooth most of the time. But most of the times it does not work that way.

So the next best option is to list your second-hand car on various online portals. You will have to get your car details, pictures etc and then the prospective buyers will contact you and then you can negotiate with them and take the conversation forward.

While there are tons of portals for selling a used cars these days, and I will list all of them here. But I will mainly talk about OLX in this section, because I have used it personally.

The best part about this way of selling your car is you can get really good price if you come across a genuine and reasonable buyer. There is no intermediary and there is no cut for anyone. It’s good for you and its good for the buyer also. You get better pricing compared to what the dealer gives you and the buyer also gets better pricing than what he would have bought it for from the dealer.

The biggest disadvantage of selling directly to the buyer

The biggest issue with this approach is that you will get a lot of junk inquiries and broken promises and conversations which will frustrate you. Lots of people will contact you and offer you lower prices. Then lots of people will start conversation and look genuine, but they will never come back.

Then there will be people who will come and look at the car, but not move ahead. So the point is that selling directly to buyer is easy, but only when you come across a nice and genuine buyer. But if you through OLX/QUIKR route, be ready to get a lot of non-serious enquires

I got 50 enquires on OLX

I had listed my car on OLX and within 24 hours, I got around 50 enquires. People were offering prices which was 50% of what I quoted (1.4 lacs). Some people called to get more information. Some people offered to bring cash (50%) and take away my car instantly. Some of them were from nearby towns (as far as 200 km). One guy came to have a look (it was a genuine buyer), but we could not agree on the price.

I am just sharing my experience here and not declaring that you always get junk leads. I have sold some other things from OLX and overall the experience was great. But some category of items like automobiles is different because there is a big market for it and risks are involved.

Apart from OLX / QUICKR, there are many other famous options and let me give you the list of these portals along with their links

When you are selling to the end buyer, the biggest problem is the PRICE. Your price should be realistic and fair. It should be a price which makes you (seller) and buyer both happy.

Note that when you sell your car to dealer, he is going to make some profits (around 10-15%) on that and sell it to the end buyer. So you are also not getting the best price and the buyer is also not getting the best price.

If you quote your car at a price that is somewhere between what you are getting to the dealer and what the buyer is paying to dealer, then its a win-win situation and you both benefit.

So the best way to find the realistic price of your old car is as follows

Go to meet 2 dealers with your car and check the valuation of your car

Negotiate with them the best price they are ready to offer and take an average of that

Inflate the amount by 15%. This is roughly the price at which the dealer is going to sell your car to someone else

So if you get an average price of 4 lacs from the dealer, you can assume that he sell this car to another prospective buyer at 4.6 lacs (15% margin). He will quote the car at 4.8 lacs, and then sell it at 4.6 lacs finally

So now you know that the reasonable price at which you should sell the car is anywhere from 4.3 lacs – 4.5 lacs.

This way, you also get higher price and the buyer also gets it at cheaper price compared to a dealer.

You can also visit few dealers (without your car) and show interest to buy the car (your model, KM driven), you will get a rough idea of what is the selling price going on for a car similar to yours.

Bonus Tip : Always quote your expected car price 20% higher than your expected price (the price at which you will be ready to sell). On OLX, people always bargain, no matter what. So if you quote it your expected price, you will get mad looking at how people bargain.

Make sure you complete the documentation

One headache when you deal with the direct buyer is that you need to make sure that the car is transferred to the new owner. The RTO related works are to be completed. Never sell the car without making sure that the documentation is complete. Else in case of any accidents or criminal cases where a car is involved, you will be considered as the owner because the RC book has your name on it.

I think if you are getting a good price (not the highest) and you come across a genuine nice buyer, it’s better to close the deal rather than trying to maximize the deal and lose the good buyer in process.

It also makes sense to tell the buyer that you will help in RTO work. It helps in selling the car faster and also you can be convinced that the documentation work will happen properly.

Pros of selling your car directly to end buyer

Possibility of fetching the best value for your car

If your car is great and popular, you will close the deal faster

Minor issues with a car may go unnoticed as buyers don’t have full knowledge sometimes

Cons of selling your car directly to end buyer

Can take too much time as lots of junk inquiries come

Too many followups may be required

Takes too much time and effort

Important points to remember while selling the car to direct buyer

Always ask the buyer to carry their ID proofs like Adhaar card or PAN card with them.

Do not hand over your car (or 2 wheeler) for a test drive without taking their ID Proofs. Always accompany them when they do the test drive

It’s better to enquire on phone with the candidate if they are end buyer or a dealer. There are too many dealers on olx and quikr now a days

Do not handover the car unless the full payment is done and you see the amount credited by logging into your bank account (not by looking at the SMS .. there are frauds going on where you receive fake SMS of amount credited)

It’s better to take a small token from the potential buyer to lock the deal (even a small amount like Rs 500 is ok to test his genuineness)

Which is the best way to sell the used car?

By now, you must have understood that it depends from case to case and there is no single way that every car owner can follow. To summarize things, here is a table which will guide you on which option you should follow and how these options are different one various parameters

[su_table url=”” responsive=”no” class=””]

Criteria

Exchange Offer

To Dealer

Direct to Buyer

Cars24/Spinny

Sale Price

Convenience

Ease of RC transfer

Safety and Security

How quick you get money

Speed of Transaction

[/su_table]

Documents checklist for selling your car

Make sure you take extra care of the documentation part when selling your car to someone. While it’s not an exhaustive list, here are some most important documents required to sell the car

Mandatory Documents

RC (registration certificate)

PUC

Insurance Invoice

3 copies Form 28 (with 3 imprints of chassis)

2 copies of Form 29

2 copies of Form 30

Pan Card and Address Proof

2 Photographs

There may be many more documents required if its the case of interstate sale, and insurance transfer and things like that.

7 steps to follow when you want to sell your old car

We have discussed different ways to sell your car and what are the important points to consider. But now let’s look at some of the steps you can take and process you should follow to sell your car the best price and without any hassles

Do all the minor fixes – If your car has some minor issues like some dents, scratches, paints coming off, make sound, or things like these. It makes sense to get them fixed first. You can choose to get things fixed at a local service station if you do not want to spend a lot

Clean the car before selling – It strongly suggested that you clean the car properly and make it look very good. These things matter a lot. The first impression which the potential buyer gets by looking at the car changes the way they feel about the other aspects of the car. Always remember, a clean car makes less sound, and drives move smoothly. It’s totally worth to go for a professional clean up if your car is a little expensive one. However, if your car is too old and in bad shape, no amount of fixes and cleanup will help in increasing the price.

Post good photos online if you are listing it – If you are listing your car at some portal, make sure you click good pictures from all angles and give all the required information along with details

Have 3-4 offers in hand – Make sure you find out the valuation of your car in exchange offer (if you are planning to buy a new car), with dealers (one branded dealer like true value and 1-2 local dealer). It’s suggested that you take a day off for this. Start from the morning.. Go to a showroom and then dealers .. and finally go to Cars24 to find out their pricing

Give higher expected price – If you are ready to sell your car for 2 lacs, then start from 3 lacs expected price. Don’t worry about embarrassment. Its a game of maximizing the price, everyone plays it. Quote 3 lacs, show surprise if the other party offer 2.1 lacs, negotiate it for 2.4 lacs at least and then finally accept what you get (if it’s fair)

Carry your documents – Carry a copy of your PAN, Adhaar card or another address proof and photos (just in case)

Make sure the documentation is complete – Whatever channel you sell your car, always make sure that the documentation is complete in next 30-40 days. Prefer the payment to be done online so that the payment can be tracked back if required and always take SALE proof. If you are selling it to direct buyer, its worth to get it done on a Rs 100 stamp paper.

Some Real-Life Experience (and Tips)

This section is empty right now. When you add your experience in the comments section below, I will add your experience here in this section.

Do please contribute here in the comments section to enrich this article for others benefit

One of our readers, Anjan had shared his experience of leaving his salaried job last year to become self-employed. He wrote a detailed experience of his journey on one of the posts so I am reproducing his message in the form of the article here. (note that this was shared last year, but I am posting it now)

Over to Anjan experience sharing below…

I want to start off by saying that I was really inspired by that one article of yours (I am talking about Manish Article) where you wrote your experience about how you quit your job at Yahoo and finally decided to follow your dream against all odds and opposition.

I left my software job at 27

Ever since the day I read that, I knew I had to get started on my dream and drew up an action plan to free myself from this IT job which I considered as nothing more than slavery from Day 1.

So last month, I successfully quit my job at the age of 27.

How my frugal nature helped me

I was always very frugal by nature even from back in my college days when I used to do odd online jobs that didn’t pay much but I ensured I saved every penny I possibly could. I built up sizeable savings which netted me a few thousands of rupees as interest every month.

I guess that habit carried over to my professional life when I got a job. I started saving almost 95-98% of my monthly income and managed my expenses as much as possible from the interest income.

My salary was a meager 35k, so it wasn’t easy but where there is a will, there is a way.

I was fed up of boring work and Politics

So after working 5 years during which I cursed my company and boss every single day, I finally had enough of the BS and dropped the resignation notice on them out of the blue. I got the topmost rating in 4 out of 5 years of my stay there.

So they were surprised by my decision especially at a time when media is reporting massive job cuts in IT due to US Visa issues and automation.

Having to do 12 hours of boring donkey work everyday, having to work on weekends/holidays thanks to impossibly tight deadlines without any extra pay, having to beg for 5 days leave to go on a vacation once a year, having to tolerate their politics and favoritism which denied me opportunities I deserved was killing my soul from within and I was dying a little with every passing day.

Even on holidays/vacations, there was an expectation to be available on phone for support.

I started acquiring new skills and planned my exit

I just knew life couldn’t go like this forever. So I made plans to become self-employed late last year. I started acquiring new skillsets through sleepless nights and sheer hard work to switch over to freelancing with the aim to open a small business a few years later.

Once I felt ready and confident, I quit.

After being self-employed for just over a month, it feels amazing. It’s hard work without a doubt and there have been many sleepless nights to deliver projects on time but the sense of freedom is just indescribable.

There is truly something to be said for working for yourself. The best thing is my salary is not fixed anymore. The harder I work, the more I earn, so there is an incentive to work hard and increase income.

Why I planned it NOW and not in the future?

Age is an important factor. I have reached an age where I knew my parents would start badgering me for marriage within the next couple of years. So I knew it’s now or never. I had to act and I knew I had to stick to my plan no matter what may come or else it will be too late.

The fact that I love to travel was perhaps my biggest motivation to become self-employed as employers would never give you more than 5 days’ leave even if you beg. I am the kind of guy who loves to go on month-long tours.

My next plan?

Thanks to my frugal nature, I saved up enough money during my employment to last many years even if I stop working today. I plan to increase my savings to an amount that would last a lifetime by the time I reach 30.

So a few years of sheer hard work is ahead of me but for now, I am enjoying my new found freedom even though I am working super hard.

Conclusion

Congratulations to Anjan for this new journey in life and best of luck to him. I hope reading his experience would be helpful for those who need some motivation to leave their jobs to break the monotony and explore their full potential.

Let us know if you have any more ideas or points to share?

In the last article of “Increasing income” series you read Anupam’s real life sharing about how he created his second income (we thank him for sharing his experience with our readers). Today let’s go a little deeper and learn ways by which YOU can also create passive income stream, which means ways of income where you do not work actively and still the income is generated.

We can see that a lot of you are interested in creating passive income but you don’t know from where to start, so after reading today’s article take at least one committed step to create second source of income in your life. After you complete reading today’ article, in comments section share at least one new idea for creating passive income.

We are a community of 50k+ people at jagoinvestor, if we all share one good idea for creating passive income, imagine what kind of passive income idea bank we will be able to create.

The rich get richer. Not only because they have surpluses with which to invest, but because of the overriding emotional release they experience from having wealth

– Stuart Wilde

I really want you to take a day off from your routine life and name the day as “PI day” of your life. On this day, you won’t touch upon any other area of your life,you will only think about creating passive income and nothing else. As next step create a special kind of account in your life called “P I income account”, in this account you will accumulate passive income, it should not come from real work or from active job. Passive income is the kind of income where either your money works for you or your people work for you.

10 ways to create passive income

(Do not discard ideas instead start thinking how the ideas can get into your life)

1. Rental Income from Real Estate

You can create rental income with the help of real estate. If you have more than two properties, the rent you get from one can help you to pay the EMI of other property you own. You can give your office space on rent or your second house on rent. You can also create either boys or girls hostel, if you have more than 1 flat on the same floor. Some even create small office units in one big commercial space and they give it on rent to people who do not have frequent visitors.

Make sure that you are selecting right people and legal aspect is taken care of. If someone (only if you are the owner) has good office space in Pune, we would like to touch base with you. (In 2015 we would like to establish jagoinvestor office in the city of Pune).

2. Buying Space for ATM Centre

This is one of the best ways to create passive income. Generally in a building, the space which is below the stairs gets sold at lower rate as compared to other offices and it is ideal place for ATM Centre. Banks can even pay upto 25k-50k per month to ATM centre owners in big cities, but again it depends on the location and the area where you own your space. There is a detailed discussion on this topic here

3. Buy extra Parking lots and renting it later

Parking is one of the biggest problem that everyone is facing today. One of our clients created passive income from the parking space that he owns in his building. Also I know someone who owns open plot next to a multiplex; he gave his space on rent to multiplex for parking purpose. This may not be possible for all but as I said do not discard ideas from your life.

4. Create Websites & Blogs

The machine age is over and we now leave and breathe inside information age, where no one cares where your office is or how many people staff you have, with the help of internet from a remote place you can create a lot of money. Creating a blog or a website is almost free (or I can say it is not very expensive) and is one of the best ways to create passive income.

You can do this as a part time activity and start creating second income in your life. This may be a slow process and it calls for good content for you to attract people to your blog or website. Jagoinvestor as a blog started very small and with the love and trust of our readers it has now created a special space in investor’s community.

5. Advertisement hoarding on your building and terrace

If your building is on main road with proper visibility you can put some banners or hoarding on the terrace of your building or even in garden or open space of your building. If you own terrace rights the money will come to you otherwise, it goes to society kitty as passive income. Some permission & authorization is required to take this step.

6. Interest income from your investments

This is one of the simplest ways to create passive income, which is in everyone’s reach. You can either create interest income through Bank Deposit products or by offering loans to people at attractive interest rate. For this your need cash on hand or pool of money from which you intend to create interest income.

7. Dividends from Stocks and Mutual Funds

You can either receive dividends through Stocks or from different mutual fund schemes. This income depends on the performance of stock and mutual fund which is linked with market conditions. There are many people, I know who create good dividend income from stocks and mutual funds.

8. Royalty Income