Have you ever faced this situation, when you were making payment through your debit card or credit card?

“Sir How are you making payment ?

Debit Card or Cash ?”

“Card”

“Sir, There will be 2% extra charges if you pay by Debit Card ? ”

“Why extra charges ? I use it at every place and no one charges any thing extra ? ”

“Sorry Sir, this is our Policy. You can take out the CASH from the nearby ATM if you want to save that extra charges”

“Huh ! .. &^#$^&*J#^&&#%$&*N”

You often face the above situation, when you buy things like jewelry, Laptops, Mobile phones etc. I faced this 2-3 times myself, but could argue well with the shopkeeper, because I knew this is just a tactic used by shopkeepers to save on the charges they need to pay from their own pocket. Hence I never paid that extra 2% or just left the shop.

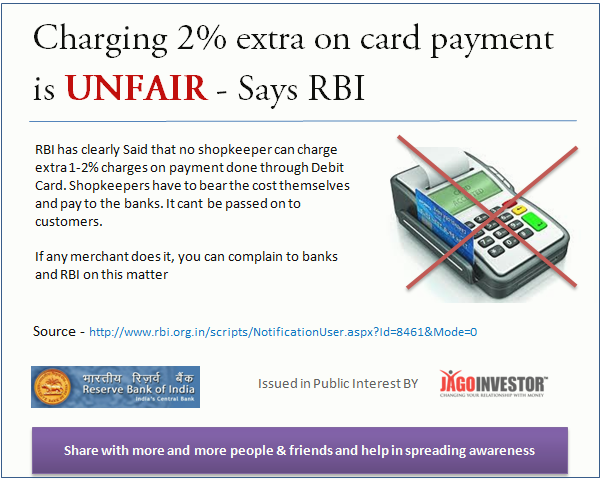

Merchants cant charge any extra charges on Debit Card Payment – say RBI

Now yesterday, RBI has openly cracked down on this unfair trade practice and issued a notification saying that Shop Merchants can not charge any extra charges from customers, if payment is done through Debit Card. Below is the exact wordings from RBI Notification

4. Levying fees on debit card transactions by merchants – There are instances where merchant establishments levy fee as a percentage of the transaction value as charges on customers who are making payments for purchase of goods and services through debit cards. Such fee are not justifiable and are not permissible as per the bilateral agreement between the acquiring bank and the merchants and therefore calls for termination of the relationship of the bank with such establishments.

Why Shopkeepers Charge extra 2% on Debit Card payments ?

When you swipe your debit/credit card for purchasing some item, the merchant has to pay some fees (1%-2%) to the Bank or the rental fees for the swipe machine. The charges goes out of their own pocket, as the cost of running the business and convenience of taking the payments (more customers will come, if card payment is there). If its a small payment like Rs 500 or Rs 1000, then its a charge of Rs 10 or Rs 20, which is fine. But when it becomes a payment of lets say Rs 30,000 (imagine buying laptop or iPad), then its around Rs 300-600 and to save that big charges, they discourage debit/credit card payment.

They often ask customers to pay by CASH and point them to nearby ATM. Almost always, customers could not refuse, because they have already made the buying decision, and dont want to argue for the small charge, and a lot of times, they finally believe that may be its not illegal, and finally give the CASH even if they do not want, or just allow the merchants to charge additional 2% charges.

But, as per RBI, its not a fair practice, because merchants already have agreed in the agreement with the card swiping machine bank that they will not charge anything extra from the customers. Here is one example of asking for 2% extra fees by some Geeta Ramani on rediff website

My worst experience was when I intended to purchase a Tata Sky card worth Rs 1000. The shopkeeper said 2.5% = 25 rupees extra. I told him — you give 10, I will give 15 rupees. He spoke quite roughly — hum kyon den? I told him it was because he was supposed to pay the bank, not I, and that I was doing him a favour and not the other way round. He said he did not earn anything from the transaction. Anyway, I did not give in. I didn’t purchase from him and purchased the same from Indiaplaza instead online without any transaction fee

What you should do, if Shopkeeper does not agree ?

RBI has clearly asked all the banks to break their relationship with those merchants who are practicing this. So, when any merchant asks you for extra 2% charges and even after the debate they do not agree, you can complain to the RBI about this and also complain to the bank. Each Bank has a “Merchant Services” section on their website and when you mail them or complain in personal to their branch, mention that you want to complain about Merchant Services. Example for ICICI bank is here and Axis Bank is here. But

When you take this step, at-least some merchants might fear the consequences and oblige!, but now the problem is how many people will go to this extra mile . It would require some time and effort from your end.

So next time you are asked to pay extra 2% on debit card payment, you can clearly tell them about this RBI notification. If required better take the print out of the notification and keep it with you in your wallet or as an image in your smartphone.

Have you ever faced a situation where you were asked to pay extra 2% charges on debit card payments and were pointed to a near by ATM, and what did you do in that situation, please share !

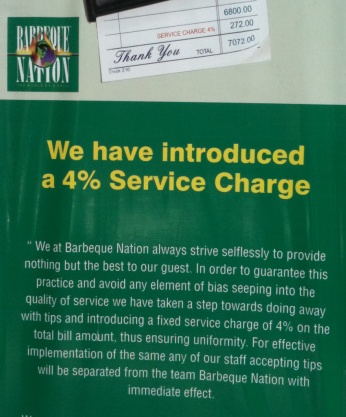

Actually service charges are to be distributed among waiters and staff and its kind of compulsory “tip” to be paid. So if there is service charge on the bill, you are not suppose to tip officially to any one. So don’t feel awkward not paying the tip, because you have already paid it in form of service charge, however most of the hotels and restaurants never tell you this explicitly. However one of the exceptions I know is restaurant called “Barbeque Nation”, I could clearly see it was written in their menu that “We will levy 4% service charge on the final bill, and you are not suppose to tip any one (strictly prohibited), because service charge will be shared among the staff” . The ethics quality was as high as their food quality 🙂

Actually service charges are to be distributed among waiters and staff and its kind of compulsory “tip” to be paid. So if there is service charge on the bill, you are not suppose to tip officially to any one. So don’t feel awkward not paying the tip, because you have already paid it in form of service charge, however most of the hotels and restaurants never tell you this explicitly. However one of the exceptions I know is restaurant called “Barbeque Nation”, I could clearly see it was written in their menu that “We will levy 4% service charge on the final bill, and you are not suppose to tip any one (strictly prohibited), because service charge will be shared among the staff” . The ethics quality was as high as their food quality 🙂