Do you come across health insurance policies from Bank with surprisingly low premiums and with amazing features and benefits, which makes you feel you should not miss this offer? Today I will give you good enough ideas about those health insurance policies and will help you understand the limitations of those health insurance policies from the bank and why you should avoid them in most of the cases. Let’s start.

Background about Health Insurance policies offered by Banks?

All the health insurance policies offered by banks is mainly a group of health insurance provided to all their banking customers in association with some external general insurance company. What happens, in this case, is that a health insurance company approaches a bank and tells them that they can offer a specialized health cover to all their bank customers with lots of benefits with a small premium. The best part of these policies is that there are no medicals involved, there are fixed premiums for all age group customers, very low premium, etc. On the first look, you will not even believe that something of that kind can exist.

But there is always another side of the situation and now these policies despite looking amazing to have lots of problems and limitations which you should know and then take the decision. Let’s check them one by one

1. Depends on negotiations every year

Health insurance policies provided by banks are actually an outsourced thing. So if you buy it from bank A, then actually its a policy from Insurance company B, the bank is merely an intermediary. As this policy is a group cover, the policy premiums and all the featured are going to be negotiated on a regular interval like each year or twice a year. Now the problem is that if the health insurance company feels that the premiums should be revised (for whatever reason), then banks can’t do anything and the only customer will suffer here because he did his long term health insurance planning with this policy.

The premiums of the policy can rise like anything in the future because the pricing of the product is very flawed in most cases because banks do not have much experience in the health insurance domain.

In absence of the right expertize with most Banks, the pricing could be majorly flawed. Though there are no published figures available, our sources at some Insurance companies say that it is an incessantly “bleeding portfolio”. We believe, any contract, in any field, which is not win-win,does not work in the long term.

2. Chances of association breaking in future

What will a customer do if the association breaks between the bank and insurance company in the future? Health care costs are increasing and its always a good thing to get your self insurance as soon as possible, now if after 5 yrs of running a policy suppose the association breaks, a customer will be left into a situation where he has to again find a suitable policy and who knows if he has developed some illness in between these 4-5 yrs, who will cover that. Here is a real-life experience from Ketan shah on the forum, see how he suffered when something similar happened with him

Dena bank 5 Years back came out with Scheme in tie up with Oriental Insurance for providing mediclaim at highly attractive premium i.e. Rs. 7000 for 5 Lac cover.

We hold various accounts with dena bank and as per their tie up we got ourselves covered (5 Policies) after paying 2 years premium, when the 3 rd year renewal came we were informed that the tie up with Oriental is no more there and the same policy will be transferred to United India Insurance for same Premium..

Now we have paid 2 years premium with United India and the 3rd year Premium we are informed that Dena Bank has increased the Premium 2 -3 fold for policies…

Now trusting Dena bank and paying 5 years of Premium which comes to almost 2 Lacs we are stranded and forced to pay high Premium for my parents and now we are in a fix If we don’t pay and we cant even change the company since parents are 65 +

we were assured that the scheme shall continue since it is bank tie up and therefore we got our previous pvt policy cancelled which had a very High Premium for my Parents (20000 for 5 Lac)

Please advice if we can approach IRDA for the same…

3. Limits on renewable age

Health insurance is a long term financial product and should always be bought with very long term benefits in mind. Having a lifetime renewal option is not just a wish, but kind of must-have feature in your health insurance policy and that’s where these policies from banks fail. They all have a limitation on the renewal age in most of the cases.

Even if the premiums are lower, what will you do sometime in the future when you really need that policy and it shuts the door for you.

4. Pathetic “service” issues

The service provided at the time of claim settlement is really a big parameter. Now if you have bought it from the bank (here bank is the agent), there is no “person” or “company” to help or assist you at the time of claim settlement? Whom do you mail? Who do you talk to? Who will you catch? Who will you blame? The bank due to its size and nature will not entertain you in a proper manner.

Also being a group policy, it some times gets very complex to understand their limitation and many things will be a complete nightmare for you as a customer. So it’s really a big disadvantage here. I want you to go through the following conversation on service issues which was done by Mahavir Chopra of medimanage and Ritesh sometime back. It will give you some idea about this aspect.

Overall I would say any health insurance from banks which are pure group cover should be just an extra health cover in your life. It should NOT be the primary long term solution for your health insurance needs. Its very important to have a large health cover from a very strong company with great benefits and strong service levels.

Have you ever thought of applying for Priority Banking with your bank (also called as Preferred banking)? A lot of banks offer something called “Priority Banking Solutions” to their customers who qualify the eligibility criteria. A priority banking customer is treated in a more special way and is taken care of priority by the bank. Let us talk about it in detail and does it make any sense for you as a customer to apply for priority banking customer or not?

Why does a bank have a Priority Banking Model?

The first question to understand is why do banks have a Priority banking model at all? The reason is very simple, to treat different levels of customers differently. If you want to harshly put it, then its just a way of keep a separate list of High Net-worth Individuals and focus on them more and service them in a better manner, because one customer who is eligible for priority banking will give 100 times more business/profit to the bank compared to a normal customer. A preferred banking customer will have a few eligibility criteria to honor, which is generally linked to his bank amount balance.

You are eligible for the HDFC Bank Priority Programme ** if you:

Hold at least one Savings or Current account, sole or joint, with HDFC Bank.

Maintain a minimum Average Monthly balance of Rs. 15 Lakhs across all your accounts (Savings, Current and Fixed Deposits*)

OR

Maintain an Average Quarterly Balance of Rs. 2 Lakhs in your Savings account.

OR

Maintain an Average Quarterly Balance of Rs. 5 Lakhs in your Current account.

The requisite balance can be maintained over your accounts and over those of your immediate family members.

In the same way, other banks also keep criteria for maintaining a high balance in saving bank account. That simply means that the bank would get lots of cash to use for their own business and naturally they can treat these customers very well. Check out this survey on the best banks in India.

Facilities provided to Priority Banking Customer

A Priority banking customer has few advantages over normal customers and gets more features. Some of the most common one’s are

Separate queue for in the bank so that you don’t wait

No charges on NEFT and RTGS transactions through Net banking

Free “At Par” cheque book payable at any Bank branch across the country, so you do away with the need to ask for demand drafts

Charges waiver for DD cancellation, Cheque return, Duplicate statement charges, Demand Draft Charges, Discount in Locker Charges,

Cheque pick-up facility

No charges on balance inquiries and cash withdrawals if you transact on Other Bank ATMs in India.

Many other benefits

Premium Credit Cards

However, all this is not so real and true

While banks list down these facilities on their website, on the ground level – there are many real-life customers who say that at the end of the day, you never get what is promised from these banks. There are a lot of things just on paper. Most of the banks just use the Preferred banking route to attract high net worth customers and finally end up calling then for investment products. A relationship manager keeps in touch with you (the target), he has all the information on how much money you have and when money comes and goes out of your account.

Here are 2 real-life experiences related to Priority banking from our questions and answers forum. Hope you get some good ideas from it.

Case 1 – Yogesh Shares his experience

There are no major benefits for being Classic or even Priority customer except some savings in NEFT charges and cheque book requests. I was HDFC classic customer for last 10 years. Around 9 months back they changed my status as Priority customer without taking a consent from me (same reason..as I opened some FD the bank) I just received letter that I am now Priority customer.

I did not notice any big difference of status being Classic or Priority customer.

The facilities they have are actually only on paper. Despite of a lot of follow up locker facility when one new branch had recently started and lockers were available, I did not get it. I was told to take some Young star policy in case I want locker. I denied this condition and the result was they did not allocate locker to me. So 50% discount is on paper. In last 10+ years I even did not meet personal banker for more than 5 times. My experience is personal banker keeps on changing periodically (on an average 2 years for each PB) and sometimes you need to trace who is your PB !

Question one may ask why I am still continuing with HDFC bank as classic customer. The simple reason is the bank is closer to my residence and with very less crowd.

In the last month I broke my FDs because of some reason and immediately they put my account into ‘Others’ category and again without informing me ! I could know that after they started charging me for account statement, signature verification/wife’s name change for mutual funds, NEFT transactions etc. So now I have instructed them to update my account as to ‘Classic Customer’ status as I still meet those criteria. Important thing to note…my Personal Banker did not take action immediately this time. That person told me s/he will forward my request to relevant department. Also at the same time this Personal Banker asked me to send request to know new Personal Banker !

Case 2 – Ayush Shares his experience

In my opinion there is no harm in being a Priority or privilege customer and using benefits offered by the bank (if they are of any use to you and are saving you time and money)

The main drawback here is, your name will go into their database as a customer with more money than some (or say lot) of others. This may result in some unwanted call such as credit card / loans / insurance or other banking products. When it comes to the actual banking needs there is nothing big that you will get. The relationship manager may keep calling you with information on new products.

My personal experience being a classic customer with HDFC is not so encouraging when the genuine banking needs are there. For example, I requested that I need a safety locker in HDFC branch but just like other customers I am on waiting list. In case I am lucky enough to get a locker, I have to pay only half the annual fee but will I get a locker is the question, that remains. You can save a few Rs. by saving on DD charges (to a certain limit), NEFT charges etc. but nothing big.

I am continuing just because I have all my banking /investment etc through HDFC and do not want to change and this classic banking is an added thing on to that account.

Conclusion

Most of the people have very basic banking needs, especially after Internet banking and mobile banking has arrived, your dependence on cheque books, Demand Drafts, and any physical visits to banks has reduced. For most of the people, anyways banking is just a small part of their financial life and they get most of the facilities and what they need from their basic banking account only. For them, it does not make a lot of sense to apply for priority banking . However, there are many investors who are heavily into banking due to personal reasons or for their professional needs. For many of them, few features which come with Priority banking might mean a very big thing. If you are one of them, just see how much of it will be eventually used by you and then take a call.

What do you think about it? Would you like to become a Priority Banking customer or not ?

I don’t want to shock you, but there are tons of cases where employer happily deducts your EPF amount from your salary, but they do not deposit it with EPFO. This goes on for years and one day you come to know that you are stuck ! , because there is no EPF money for you. Your employer has severe cash crunch or is about to shut down and now you have to run pillar to post to claim your money. The whole situation gets ugly and you feel cheated, because your company never deposited the Employee Provident Fund amount. Now you go to Police and file a case against employer. But this all can be avoided if you are careful a bit, from starting itself.

How about making sure your employer is depositing your provided fund money into your EPF account ? Before I tell you, how you can do that, let me first share with you some REAL LIFE cases where employer failed to deposit EPF money and employees are suffering ! . These are some of the examples shared by readers of this same blog over comments section in various of EPF related articles.

Case 1 – How Abha’s company didnt deposit EPF money for 2 yrs

Dear Manish,

Thanks for such an informative post. At last i do see some hope. Here is my situation:

Worked for this company A for almost 4 years and left them in Nov 2011 as they were downsizing…yes it’s been more than a year and half of torture they have given me thus far. Company is kind of closed now as I don’t get any proper response from them, CEO is just not bothered. Company first asked us to wait for 2 months to file the claim as it is a rule, did that patiently. Later came the story of change of PF office from one (under which it was originally registered) to another and that went on for several months

They kept saying PF offices are not coordinating among themselves, the real reason was even shocking and more disappointing, PF guys were not updating because this company didn’t not deposit our PF amount for long time (2 yrs appx), they however kept deducting the same from our salaries (was surprised how come there was no annual audit by PF office and how this company could continue doing so for this long), anyways they cleared things in January this year and said we have applied again. When filed a grievance online, PF person says we haven’t received any claim whereas this X employer says they have already applied. Don’t know what the real truth is but on the basis on experiences I have… most certainly it is the X employer at fault.

Another strange thing is, when I checked by balance online in January this year it looked fine (updated up to 2012… I do have SMS proof) but from last 2 times it saying updated up to 2010, I am worried if this employer has dome some mischief here too, is it possible for a company to take back money from an employee’s PF account or it is the issue with PF website?

I don’t want to apply for my claim via options you suggested above unless I see the balance updated. Thank you so much for reading thru my query/concern. Appreciate your feedback.

Case 2 – Balaji Company asked him to Wait till they deposit the Employee Provident Fund money

Hi Manish,

I switched jobs in August this year. Before I quit the job, I had submitted form with my previous employer for withdrawing the amount in my PF account. I had not received the amount due till December. When I called my previous employer, they told that they have not yet deposited the money and I will have to wait till March 2013.

My question is, is what my employer did legal? How frequently should the employer deposit the PF money with the EPFO? I have been working with the organisation for little more than a year now.

Case 3 – Sarabjeet Kaur company not replying her because they did not deposit EPF amount

I worked in an organisation for 2 years. They have not deposited the PF amount which they used to deduct it from our account. Its been 1 year I am asking them to refund the PF. They have stopped replying to the emails and have stopped answering everybody’s call. Is there any ways I can withdraw the amount? The firm is based out in Mumbai and I used to work in Delhi Branch.

Employer can be Jailed if they do not deposit EPF money

An employer has no right to deduct the employee share from salary and not deposit it with EPF. There can be any excuse or justification for this, because its employee hard earned money. Once the employer deducts the Employee Provident Fund money from the employee salary, its their duty to deposit it with EPFO , and if they fail to do so for any reason, its a crime.

Whatever is the case, you can always complain about it with the EPFO department and the concerned officer has all the rights to proceed the legal complaint against the Employer and in the worst case, employer can also go to jail, because what they did is a criminal offence under section 405/406 of IPC .

1. Complain to CVO officer – You can also email your situation and case to the CVO (chief vigilence officer) at EPFO, who is appointed by Ministry of labour for EPFO to look after these kind of irregularities. You can email them at [email protected] . More at this link

2. File a Police Complaint – You can also file a criminal case, against the employer in police station which comes under the jurisdiction of your working office (not the registered one) . All you need to show them is the salary slip, which shows the EPF deducted, note that its always better to mail CVO about it anyways, so that the chances of local authorities influencing the matter will reduce.

3. Complain to Regional Provident Fund Commissioner (RPFC) – You should also complain about the matter to the RPFC officer if under the EPFO office, which will be investigated by him/her.

How Employers Deposit your EPF contribution to EPF account ?

How exactly your EPF money gets deposited in your EPF account ? Here is what I found on this website

Employees’ PF a/cs are maintained under these two different methods are –

1) All accounts are with O/o the RPFC

Every registered employer remits the Employee Provident Fund contribution by challans to the RPFC’s Bank a/cs. which in turn gets accounted in the respective A/c No.of every such employee. And the employer submits monthly returns to the RPFC showing the details, employee wise of contribution thus remitted.

Every such money is maintained by the RPFC who in turn disburses, thro’ the employer towards refundable loans, F & F settlements together with accrued interest to the respective employees. Once in a year a ledger sheet showing the transactions of any employee for one full year is issued to the concerned. Similarly from the PF contribution pension contribution is divided and remitted to the Pension a/c. of the employees thro’ a separate A/c. code. This method is the largest.

2) The other method is called “Exempted Establishments (PF Trust)”

An employer/company who employs more 100 employees on roll is eligible to apply to the RPFC for “exemption” from maintaining the EPF under the above said (1) method. RPFC grants the “exemption orders” under certain conditions after examining various aspects. After which the Employer sets up a EPF Trust to be run by Employer (employer’s nominees & Employees’ representative (Union nominees) which manages all the contributions of employees & employer (excepting Pension Fund which is never maintained by the Trust). A set of Bye laws, in the lines of EPF Act & Rules is prepared & duly approved by the RPFC for running the Trust.

This PF Trust money is invested in the Govt.approved securities for earning the assured interest from which accrued interest to the employees’ PF a/cs is credited. The Trust once in a year prints the Employees’ PF ledger a/cs and distribute to the concerned. The Trust accounts are audited by the CA and submitted to the RPFC. RPFC also periodically inspects the Trust a/cs and oversee. Monthly, annual returns in the Forms have to be submitted. The convenience under the Trust is quick disbursement of loans, withdrawals and F & F settlements to the employees. Surplus, if any never distributed but any shortfall is made good by the employer.

How to find out if your employer is depositing your EPF contribution or not ?

Let me share with you some steps you should follow, to find out if your company is depositing your EPF contribution properly or not.

1. First thing is the do not rely on hearsay’s here and there. It might happen that you come to know from some one that your company is not depositing your EPF money, but it might not always be true . Delays happens at times .

2. Every month on 25th , your employer is suppose to send few documents to EPFO department to intimate them on

Form – 2 (for new member during the month)

Form – 5 (detail of new joinees during the month)

Form – 10 (detail of left employees during the month)

Form – 12 – (Details of money deducted from employees salary)

3. The best thing is to first contact your employer and ask them for a copy of these forms for last 2-3 months, do double check if they deposited the money or not.

4. As per my opinion, the best way for a common man and most convenient option is to file a RTI against EPFO and ask them all these questions . Mention your EPF account number, your employer Code and simply ask if your employer has been depositing your contribution or not.

Conclusion

Mostly the big size employers might be depositing the Employee Provident Fund money properly on time, but some of the companies which are small sized or whose owners and management teams are unethical might be into these illegal activities of not depositing employees hard earned money. Its always a good idea to spend some time to be assured, in-case you feel your company is one of those who are not depositing EPF amount with EPFO 🙂

Do you know of any case like this ? Also Please share this article with more and more people

While I was working out in gym in morning, I has a strange feeling that I can connect every aspect of ‘staying healthy’ with ‘building wealth’. There are various things which can be used as an analogy to teach good things about ‘creating wealth’ , but the area of health is best as an analogy. I am sure a lot of you who take health seriously and exercise regularly will be able to connect well and appreciate this article, others who do not take care of their health might get the maximum value because they will appreciate both the things (health and wealth points) . Lets see those points .

1. Starting is Easy, Continuing is not

Its very easy to go for a jog/walk at 6:00 am for 2-3 days. A lot of people decide they will do it, and a lot actually achieve it . But what happens after a week/month ? We discontinue it and life is back at square one and we are just lost in our daily life exactly the same way we were earlier . You break your promise of “I will exercise in morning at 6:00 am” , and it all starts with a very small violation, which takes a big shape. Starting out something is damn easy, but the real question is how long you continue it ! and with what commitment. So don’t tell me you got up at 6:00 am . Tell me how long have you been doing it , that’s the real parameter.

In the same way, its too easy to start reading a new blog, starting your SIP , start writing your budget and even working on your financial life. A lot of people get some adrenaline rush, after I write some good article which makes them feel – “Its high time now. I should do something about my financial life” and they start doing something, but the real parameter to look at it is – “Are you consistently doing it ?” . Is your SIP running from many years, month after month without fail ? Are you writing the budget month after month and following it ? A Rs 5,000 SIP running for 10 yrs would always (well , in most the cases) beat a inconsistent SIP of Rs 12,000 . A consistent written and followed budget which was not that detailed, will be much better than a inconsistent budget which was very detailed. A simple strategy followed for years with consistency will just be better than a complex one which is not followed regularly.

2. Focus has to be on Long Term

Imagine you a trainer in gym and someone recently joined with 90kg weight, and complains to you that – “It has been 1 week, and my weight is still the same !” . What will be your reaction to that ?

You need to give sufficient time and patience to see results. You need to understand how things work in health and only when you understand the internal working , you will have faith in exercising , only then you will continue it. Over 6 months, you will see some results , over 1 yrs you will see good change, over 2-3 yrs , you will be a transformed person all together. Short term is just short term ,you can only build some artificial muscle in such a short time. But if you need some serious health, it can come in long term only.

In the same way, wealth can not be created in short term (I am talking about investments here) . Wealth multiples itself over long term and if you want to build 1 crore rupees in 3 yrs with your Rs 50,000 per month salary (god knows what is left at the end of the month) , you are probably from Venus , not Earth for sure. Just like long journey starts with a small step, you need to start your wealth journey with small steps and then built upon it . You need to understand some of the fundamental principles of personal finance (which I have shown in my book – “16 personal finance principles every investor should know“) . Unless you understand them, you will always doubt short term volatility in your portfolio, you will just get too much attached with security aspect of your money and will not allow your wealth to grow.

3. Diversification is Important

Imagine you are only and only working on your left hand when you exercise . Try to visualize it . You are concentrating only on your left hand and how to make it strong. What will happen in next 2-3 months ? I am sure you will not even last that long, but even if you do , your left hand will surely look artificial on your body and ache like anything because you just never cared about other parts of your body and other aspects of your health. A good health is function of good diet, good sleep , good exercise and your life style. Imagine you work out brilliantly , but then, all you eat is junk like Mc’D , KFC , Pizza’a , maggi etc etc .. Or imagine your diet is excellent , but you do not work out at all and sleep at 3 am and wake up at 11 am daily. This all is going to reflect in your health and you are not giving 100% to your health. You cant expect a lot !

In the same way, when it comes to wealth, you just cant be sitting on only and only Fixed Deposits or only and only ETF’s, or just 100% into real estate fully (unless you are a pro and understand what you are doing). You have to make sure you keep a balance and understand each component’s importance in your financial life. A good mix of real estate, equity, debt , cash , gold is desirable for most of the people (for a common man) . While Debt part will give you security and some peace of mind, real estate will make sure you do not feel left out in the race, the equity part makes sure, you are earning some real return at the end after tax and inflation, gold will keep you wife happy and cash will bring smile on your face and tears in your relationship managers face. The point is – don’t over-invest in one category without understanding its impact and accepting the outcome. Always keep balance and harmony among each other depending on your age and risk profile.

4. To get best quality, you need to invest your time/money/energy

I recently invested a huge annual fees in a well known gym. We get best equipment’s, best environment, best facility, dietitian to look after what we are eating and a good tracking of where we are in our health chart, regular track of our weight, measures and it helps me and my wife move in the direction we want to reach. You need to invest money to get the best most of the times. Apart from the money, you need to put a lot of times and energy from your side. This brings good health over long term. While you can also just go to a park in morning or jog on a road, you still need to invest your time and energy. You need to invest in good shoes, a comfortable work out dress. The point I want to convey is – while you can always look out for free things in life, which works , at-times you need to invest your money, time and energy to get the best. Do not look for money when it comes to your health, you can earn 10x times more if you have a better health.

Just like that, I see a lot of investors destroying their financial life, because they just do not want to invest money, time or energy in their financial life. You can get best, if you are open to invest money, time and effort from your side. The good things do not come cheap always. Hire a good advisor/planner who you think will be able to deliver what you want out of him. Invest in good programs, good books , invest your time to learn things, go to that extra mile to understand concepts and how things work. We have around 550 articles at this moment on this blog and 6,000 questions answered on our Q&A forum, ask yourself how much energy and time have you dedicated to learn things and find out new ideas. We have written 3 books, which we feel can really transform your financial life, all it takes is Rs 1,000 to buy them. Go ahead and just read all of them and you will at a new level. I recently paid Rs 3000 to attend a TIE session in Pune, just to hear Naranyan Murthy (for 1 hour) and Devdutt Patnaik (for 30 min) . What I got back was tons of their experience and whole new ideas which made my Rs 3,000 a tiny thing. Good things always comes when you make an investment , you just have to focus on value.

5. It keeps you energetic

When you exercise in gym or at park near by or at home, there is a point where you feel – “I cant do more exercise, Its paining now” . At that point if you stop, you do not get the best results. The best results are always on the other side of your comfort zone – Always in every area of your life. When you feel exhausted, gave your 100% , when you are wet with sweat, your whole day goes amazing. The kind of energy and excitement you feel inside you is awesome. You are more happier, you smile more, you are more kind and you feel more energetic, ideas inside your head are better. Just one activity leads to a great day. And when you do it every day, then each week and each month is great.

Just like you feel energetic when everything in your health area is good, you feel really blessed and good when thing are right in your financial life. When you have completed all your pending tasks in financial life (Join our massive action revolution called 100moneyactions), when you have achieved a sufficient milestone in accumulating wealth, when you have some respectable bank balance, when you have good emergency fund in place, term plan and health insurance already taken and completed. The kind of energy and excitement you have in your financial life is different . You look at your financial life and feel better. You can concentrate on other areas of your life.

6. Structure and Environment increases your dedication and consistency

Good health comes when you are into a nice structure and environment, which fuels your appetite to exercise and improve your health. You will not feel like working out when you are inside your office space, you will not feel like exercising when you are into a movie theater. But when you are inside a gym or a park in morning, you suddenly ‘feel’ from inside that you want to exercise. Thats the power of Environment. Just see anyone who has amazing health, its because they are part of some great environment and structure, it can be as simple as getting at 6:00 am and going for a walk. That’s also an environment.

In the same way, a proper environment helps a lot when you want to improve your financial life. When we did a 1 day full workshop in Mumbai recently, It was all about creating an environment, where you 100% focus on your financial life and discussing ideas which can take your financial life to next level. This blog is an environment, our 100moneyactions is a dedicated environment for taking actions in your financial life . I want you to look at the following video which will help you understand more about power of environment and structure in your financial life.

7. Starting early helps

While its never too late, its always a good idea to start early in life. Imagine two cases, one where you have had a healthy life all your life, and then second case is when you are extremely unhealthy till now and now trying to have a health life at 45 yrs ! . Most of the people around 40-50-60 yrs old today are facing so much issue getting a health plan and also dealing with life overall. They have medical issues and its affecting everything in their life, even people who are connected with them.

Imagine if they had taken care of their health long back, it would be a different situation today. If you are not joining the gym right now, just because it costs money or you have less time, you get very clear that you will pay both of them later with huge interest. In Nandish Book – “11 principles to achieve financial freedom”, In one of the chapters, he has put a quote by Dalai Lama , when asked what surprised him most about humanity ..

“Man. Because he sacrifices his health in order to make money. Then he sacrifices money to recuperate his health. And then he is so anxious about the future that he does not enjoy the present; the result being that he does not live in the present or the future; he lives as if he is never going to die, and then dies having never really lived.”

The same applies to your wealth and financial life. The mistakes you make today, will come back to you later and hit you hard very much. I cant say more on this, but just say you this – A lot of people are not able to lead their financial life properly when they are earning right now. Imagine what they are going to do when they will not earn and still be living on this planet for 30-40 more years. I am talking about retirement. You work for 30 yrs and earn, and you struggle a lot. Imagine retirement of another 30-40 yrs, when you are not earning. Its a life sentence followed by death if you do not start earning and do something about your financial life. A good start will always give a great support to your financial life. Here is an article showing you the power of starting early

8. Neglected, because it does affect you in short term

This is my favorite. This I think this is one of the biggest reasons for a bad health life and a bad financial life. A single action if not taken does not affect our health or wealth at that moment, but collectively they destroy our health and wealth in long term.

Coming to Health, When you eat a sweet (I used to eat a lot of them, when I worked in Yahoo) , skip your meal, skip your gym/exercise , that single act is not going to affect you at all (it looks like that) . You cant see its impact on your health in a long run. Each Pizza you put down your stomach instantly gives you taste, but instantly it does not give you a shock. You only see it months and years later. When you put on weight, you suddenly one day realize – that you have put on weight, it does not appear in parts. Suddenly one day you feel , your are too weak or do not feel energy in your body. It all starts small.

In the same way, I see a lot of messed up financial life which all started with one small mistake and then just grews SLOWLY ! . Every time you swipe your credit card, you feel like you will deal with the debt somehow, how troubling can one credit card swipe (which was really not needed) be anyways ! and then you create history !

Each month, when you blow up your money and do not save a single rupee, it does NOT affect you at that very moment. Every time you stop you SIP for something which is URGENT, it does not mess your financial life at that very moment. But all these things combined are just destroying your financial life. Each time you postpone taking some action in your financial life, it just messed up your financial life even more. So nothing hurts in short term, because its not visible – and its true in all the area like health, wealth, relationships, career or whatever it is ! . Stop looking for instant gratification, and suddenly you will have the half battle won !

9. There are shortcuts offered

You must be seeing a lot of shortcuts offered in the area of Health on TV and Newspapers. Some magic belt which will eat off all the fat, some majestic coffee, which has divine properties and can reduce your fat, health clubs offering packages which promise you things like – “Reduce 20 kg’s in 2 weeks” .. etc. A lot of people take these shorts cuts and end up paying huge costs, Money is lost, time is lost, health takes a hit and your trust reduces on anyone who comes to offer you any advice in future.

The same thing happens in the area of wealth too. We often get a lot of paid clients, who had a bitter taste with some other financial advisor in past, who sold them junk or didn’t provide any thing valuable to them even when they charged them good amount of advisory fees.

There are too many people offering you free advice, some good and some bad, there are too many short cuts which are offered to you and even you as investors are keen on taking short routes to build wealth, but eventually end up paying huge cost. There is no alternative of doing your homework and really spending your time and effort in building your financial life.

10. You act on it when you feel a sense of Urgency

Its a strange thing, but most of the people start to take any action in the area of health, when they see there is some ‘problem’ . When its URGENT to do something, when its too late and now its a matter of Do or Die. Didn’t those people who are very obese, knew from many years that some thing needs to be done ? Are you not aware right now, that you need to improve your health ? Yes you are , but you will take action only when you have a sense of urgency in that area, then you will suddenly have time, money and that effort required, which you do not have at the moment (this is what you believe).

The area of money is same. You do not work on it, until there is no option left. Most of the people who come to us for financial life come at the last moment. We always tell them, if only they would have come lot earlier, we could have served them in a better way. You go to a paid workshops, only when you are very sure now you need an external help, you go finding a solution, not to learn and explore new ideas . You are too needy in your financial life then and remember one thing – “Needy people do not have power in life”

I would suggest that you get my latest book – “How to be your own Financial Planner in 10 steps” and start planning your financial life in a better way. So do things not when they are urgent, but when you should do it. Dont take health insurance when you have a illness, you will not get it. Take it when you are in the best of your health. Don’t start SIP in mutual funds, when you can see your goals has almost arrived, do it when its very far and you have good time left for your money to work hard.

Wish you best of luck !

I hope you got some realization today, do let me know which area of your life did you get realization on ? Wealth or Health ! .. or BOTH !

Today we are going to talk about “Bank Lockers” and how banks use unfair tactics by forcing customers to open a fixed deposit for a very large amount and that too for a long duration. It’s not uncommon to hear bank officials asking for fixed deposits of Rs 5-10 lacs in case you want to get a locker. That is just not allowed as per RBI and we will see what exactly the RBI guidelines say about it.

What is a Bank Locker and How does it work ?

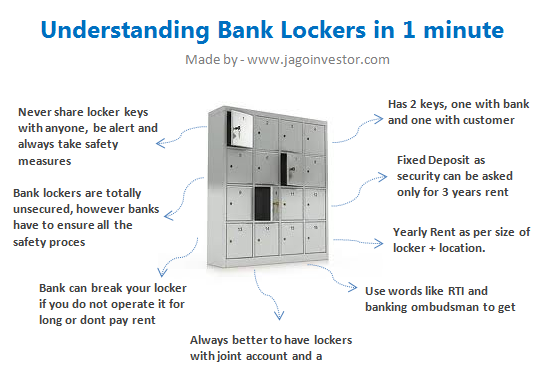

Just like we have a saving bank account and fixed deposits to keep our money safely, we have “Safe Bank Lockers” to store our physical belongings like jewelry and various kind of important documents like WILL, Property Papers and other valuable items which you feel should not be kept at home.

There are always 2 keys for the locker, one key is with Bank and the other with the locker holder. The locker can only be opened when both the keys are used at the same time. Generally bank official applies the key and then leaves the locker room and only after he/she leaves, you should open the locker door and do what you wanted to do. The banks use very high quality, strong lockers (generally Godrej). So overall, this all makes sure that your locker is very safe.

Lockers are to be allotted on first come, first serve basis (as per rules) and in-case the lockers are exhausted, the bank is suppose to keep a waiting list of customers who have applied for the lockers and have to inform them when the lockers are free in the same order of application. If bank says that they do not have any lockers left at the moment, you can ask them for the “Waiting Register.”

Annual Rent for Bank Lockers and Security Fixed Deposit

Bank lockers come in different shape and sizes, which can be taken by customers depending on their requirement. For using the facility of lockers, you have to pay an annual rent which will vary depending on the size of the locker, the city (metro, urban, or rural). For most banks, the locker rent starts from Rs 750-1,000 per year and can go up to 5,000-10,000 for PSU banks and even 40,000-50,000 in case of Private banks (see the locker rates for bank for Baroda here) .

Is opening a Fixed Deposit mandatory for getting a Locker ?

Now lets discuss the biggest pain point of customers. Almost all of you might have faced this. When you go to open a bank locker, you are asked to open a Fixed Deposit for a large sum like 2-5 lacs for a long duration or asked to buy some policy (ULIP or Traditional Plan) saying that this is the rule for assigning the locker. However it’s just a plain lie and an unfair practice followed by Banks. A common man has no idea if the bank is correct or not and where to get the right information? So, I looked at RBI regulations on Banking and found out the exact rules.

And this is what I found – YES ! , Banks can ask for Fixed Deposits as security !

But, here is the catch ! .

As per RBI regulations, the bank can ask for a fixed deposit only to cover 3 yrs of locker rent and the breaking charges, not a rupee more than that and that too only from the new locker applicants, not old one’s already having a locker. Here is the RBI wordings from their notification

1.2 Fixed Deposit as Security for Lockers

Banks may face situations where the locker-hirer neither operates the locker nor pays rent. To ensure prompt payment of locker rent, banks may at the time of allotment, obtain a Fixed Deposit which would cover 3 years rent and the charges for breaking open the locker in case of an eventuality. However, banks should not insist on such Fixed Deposit from the existing locker-hirers.

To give you the proof one of the PSU banks – Bank of Baroda clearly mentions this fact on its website here

At the time of hiring the locker, bank will obtain a minimum-security deposit in the form of FDR from the lessee for the amount which would cover 3 years rent and the charges for breaking open the locker in case of such eventualities.

So, suppose you want to get a locker whose yearly rent is Rs 1,200 and the breaking charges for locker is say, Rs 100, then they can only insist on a Fixed deposit of Rs 3,700 (3 years rent + breaking charges); nothing more than that. Ergo, 3 years locker rent is going to be a very small amount, which almost anyone can afford, but banks lie to you and trick you by telling you to invest in a really large Fixed Deposit .You oblige for your own reasons. Banks do it to make sure they reach their monthly and yearly targets of acquiring new fixed deposits and selling useless policies like ULIPs and traditional plans (Note that banks are one of the channels for many companies to sell their products)

So next time you go to the bank for enquiring about lockers and bank officials don’t give you proper information, you can tell them about the rules and the notification from RBI. That should give some shock to the employees there and they might treat you a bit fairly. If still they do not budge, use the threat of RTI and banking ombudsman (and then actually use it)

Use RTI to resolve the Issue and Find Information

RTI is a powerful tool for a common man. We will see now, how you can use RTI against PSU banks. Next time when you go to a bank (I am referring to PSU banks here), tell them you want to have a locker (assuming you are having a saving bank account there already) .

When the bank staff tells you that they do not have any lockers available at the moment or try to impose some rules, you can tell them that you will find out things by filing an RTI application to the branch manager and also would quote his name in the RTI (stare on his name plate at the desk , he/she might be in horror). If they do not budge, then really go file a RTI after the incident. I would say better file a RTI before and once you get the reply from RTI, reach the bank with RTI reply letter itself.

When you file RTI letter, ask following things

How many lockers are installed in the branch ?

What is the size and volume of lockers and how many types ?

Rental amount per year for the Lockers ?

How many lockers are Unoccupied and available for allotment

How many people have requested for it and are on “waiting list” ?

What is your serial number in that waiting list (in-case you have applied for it) ?

Is there any requirement to make a Fixed Deposit for getting the Locker (YES/NO) ?

What is the amount of fixed deposit to be opened and what are the rules for it ?

In how many days a bank locker is allotted ?

Who is responsible to allot the bank locker in bank ? What is the name of the officer or designation ?

A weak person is always exploited in society, that’s the nature of life . When you appear as uninformed and too needy, anyone can take advantage of you, but when you appear as informed investor, who will not allow anyone to take advantage of his/her and who appears to be committed to be treated fairly, its tough for the other side to exploit then. Here is an instance on how Nikhil got the Locker facility with any FD at ING Vyasa Bank

I experienced a similar forced selling sometime back at ING bank. I wanted a locker and the Relationship manager said I need to make an FD of Rs. 100000/-. when I said NO. they said its a rule. I said there is no Rule book which mentions this. Rules are same for all banks and branches. the Relationship Manager stubbornly said ‘This is the rule of this branch’.

I just went to their website, found the no. of Chief compliance officer and spoke to the officer who helped me on this. After 2 hrs, I got a call from the same Branch of ING and they requested me to come to the branch and gave me a locker without any kind of FD!

Locker with Joint Accounts and Nomination

Just like saving bank accounts and fixed deposits, you can open a locker as joint account and with nomination facility, so that in case the demise or unavailability of the main locker holder, the joint holder can access the locker and operate it. Also in case the locker holders die (both joint holders), at-least there would be a nominee, who can get access to the locker by producing death certificate and filing up claim form.

There are tons of cases where locker was just owned by a single holder and when he died ,the family had to move mountains to finally get access to the locker. Worst, many families are not even aware about the existence of the locker and banks don’t take much interest in tracing down the locker family for many years (provided they have got the rent or have the fixed deposit linked to it).

Can bank open the Locker without your permission ?

In the worst case YES ! You need to operate your locker from time to time (at least 6 months to an year ideally.) Recently there have been cases when explosives and illegal things were found in lockers, which shows how lockers can be misused. When you are allotted a locker, there is proper KYC done by bank to make sure they know everything about you. They would place you in particular risk category like low, medium or high. If you are a high risk category person, you need to operate your locker at least once a year to make sure everything is fine. If you fail to operate your account for very long (depending on your risk profile), the bank will first remind you about the locker and will ask you reasons for not operating your locker. If you still do not take actions, the bank has all the rights to break your locker and give it to some one else, even if you are paying the yearly rent on time.

In case there is a genuine reason for not operating your locker for a very long time, you need to give it in writing to the bank mentioning the reason (like if you are now an NRI or if you are out of the city for a long time.) Also, if you fail to pay the yearly rent, they can break off the locker and re-allot it to someone else. Fair enough 🙂

Are bank lockers really safe ? Who is responsible if something goes wrong ?

Now this can be news to many, and a shocker, but in truth, Banks are not responsible for your bank lockers for any unforeseen events which is beyond the control of banks, provided they have done every due diligence from their side to protect it. You have to understand what exactly a locker facility is. The bank just gives out the space they have, on rent and make sure that its safe and secured professionally. They are suppose to make sure they have all the safety and security measures in place, to ensure that the lockers are safe and secure. So its more of a proprietor and a tenant relationship. In case there is a robbery (not in control of bank), Earthquake, Tsunami, Fire (which is not in control of bank) then bank is NOT responsible, or liable to compensate you.

Let me give you an example – If there is a robbery in the bank and your locker is one of the unlucky ones to get robbed, you lose it completely and the bank is not liable to compensate you for the reason that it wasn’t in their control to stop it, especially when they have all the security measures in place like a security guard, powerful lockers, CCTV cameras installed, and emergency alarms in place. The act of robbery is more of a unlucky event for them and you. (However there are some policies in market which insures the jewelery in your bank locker like this policy from Axis Bank). If you think that robberies in bank (with locker looted) do not happen in reality, I must tell you that it happens and has happened in past. Here is one such example.

Robbers recently broke into the strong room of a Punjab and Sind Bank branch in Jalandhar and emptied out 36 lockers in an incident that stands out as a grim reminder of the abysmally poor security infrastructure at financial facilities in the country. The incident is a reminder of a burglary at the Chirgaon branch of the Central Bank of India in Jhansi, Uttar Pradesh. As many as 45 lockers had been robbed in the November 2010 episode. (Link)

When you put your valuables in bank locker, the bank does not know what did you put in there, there is no record of it in writing with bank. That’s one reason, they can’t compensate you in case something happens to it (It could happen that you never had anything in locker and you can suddenly say that jewellery worth 10 lacs is missing! What’s the proof ?) However it does not entirely mean that banks are not liable to pay back or compensate the locker holders in every case!

Bank has to make sure they have done their side of safety measures and security

Bank is not responsible for your lockers only in case of those events which are totally not in control of bank and unavoidable, but only when they have done their share of work and security like I explained above. If banks fail to do their duty and then a robbery or some unforeseen event occurs, which results in your loss, then a customer can always claim that the bank is liable to compensate, because then the incident might have not happened or could have been avoided if banks did their part.

In another case, of Bank of India vs Kanak Choudhary, the customer had kept currency notes in locker which was eaten up by termites. Here the bank didn’t do their job of ensuring that the place is clean and safe. The customer was awarded the compensation.

Bank of India vs Kanak Choudhary

Here, the customer filed a case stating that termites had destroyed currency notes and important papers kept in her locker. The commission said that the bank “was bound to ensure that the respondents’ locker remained safe in all respects”, and awarded compensation to the customer.

Even in the robbery case shown above, the bank was found to be irresponsible and didn’t not do a lot of security measures, and definitively there was a chance of the robbery being unsuccessful if only bank had done their share of work, which means the locker holders would get compensation from bank, but then issue now is, how much compensation bank has to give and why when ? The matter would have gone to court and delays and frustration must have happened in that case.

But how much you can claim back from Bank ?

Not 100%, because you can never define how much you lost with 100% certainty. Banks themselves insure the lockers to deal with the loss in an extreme eventuality, so bank themselves get some compensation from wherever they have insured the lockers. So you can get some compensation from bank out the amount they themselves get, but to get back the compensation, you will have to show the receipts of the things which you claim was kept in the locker. Even in that case, you will not get 100% back, it will be some percentage, which can’t be defined. Also you can’t get back any compensation for the documents kept (as you cant define it’s value) and the currency notes if any. You can look at the youtube video above to see these points on claims you can get back.

While the risk is always there with bank lockers, note that this is an extreme eventuality. This information should be seen more of an awareness point, rather than a decision making criteria to choose or discard taking a bank locker. You don’t stop driving a car, just because there is a small chance of accident, right? In the same way, just because lockers are not 100% secured, does not mean you say that – “I will not go with bank lockers, because its not 100% safe.” Truly speaking it’s much safer than you bank almirah at least.

Some safety measures you should take for Bank Locker

You can never get rid of the complete risk, but you can ensure that you follow some best practices and common sense tips to make sure your bank locker is safe. Here are some good practice.

Always open your locker after the bank employee who accompanies you to the vault leaves the place.

Make sure your bank has all the necessary security measures, such as alarm system, iron-gated rooms, electronic surveillance via CCTV, etc.

Visit your locker frequently and ensure your valuables are safe. The RBI and banks expect frequent locker visits from customers.

Also, ensure the locker is properly locked before you leave the vault.

If possible, better have 2 lockers to diversify the risk (like one locker for valuables, and another for Documents)

If possible, always go with the bank where you have huge trust and comfort and its near your place, so that you can visit them often

Keep laminated documents in the locker, so that they are not damaged if you keep them for a very long tenure.

Always keep a record of what all you have in locker, so that in-case of eventuality, you can alteast find out what was lost and what was the worth

Demand a copy of the hire-purchase agreement for the locker so that the bank cannot ask for a higher rent in future

If a bank says the locker request is in the waiting list, ask for the waiting number

Demand a copy of the bank’s internal guidelines regarding lockers (their guidelines never mention fixed deposit as a mandatory condition)

I hope this articles has helped you understand almost everything about the bank lockers and how they work and different rules and regulations. Do you also have a bank locker ? Generally what all you keep their and how much do you trust your bank for the locker safety ?

Guys – It has been 5 years now spreading personal finance education through writing blog articles, writing books on personal finance, leading workshop in different cities. We started very small and have reached so far only because of your trust and partnership. Every day we (I and Nandish) wake-up with one thought in our mind “How can we help people to live an awesome financial life?”

It’s time to look at what is exactly happening in your financial life?

I’ve always been fascinated by Socrates’ bold statement that “The unexamined life is not worth living.” The statement holds a lot of value and meaning in it, it has acted like a wake-up call to me. I examine my financial life every year very closely and my personal finance actions.I want you also to examine your financial life and your actions. Look at what is going on in your financial life, How many articles you marked as important but you never found time to read them, How many personal finance actions you have been procrastinating, how many times you told yourself it’s high time I need to get serious as an investor. Get honest with yourself as that is the first requirement to be a part of personal finance action revolution.

You are committed but then why you are not able to take actions?

It is not that you are not committed but as life is dynamic you are always surrounded by multiple responsibilities in life. You play different roles in life and one of the role you play is of an investor. One of the thing we have found to be missing is a STRUCTURE. Yes, to move from point A to Point B you need a structure without that you will not be able to become effective. We have created a wonderful personal finance structure for you that will help you, motivate you and empower you to take actions in your financial life. It will not help you to complete 10, 20 or 50 actions but it will help you to complete 100 money actions in your financial life.

In our experience Personal finance is NOT about knowing things, it is about getting things done !

A lot of people think they need to have a lot of knowledge to take actions in their financial life. Because of this they start to expand their knowledge domain, they start subscribing on different websites and blogs, start to buy different books but eventually due to lack of structure they are not able to take required actions in their financial life. 100 money actions program is about getting things done, it is about expanding your action domain and it is about breaking your habit of procrastination.

What Existing Users are Saying about 100moneyactions.com

100MoneyActions is a real boon for people like me who are charged up and convinced to improve their financial life and take it to next level. Thanks to Jagoinvestor’s prolific pioneers Manish Chauhan and Nandish Desai for launching such a beautiful concept that is filled of actions. I have started recently with this program and I can sense the positivity that it has started to bring in, in my financial life. 100MoneyActions provides an excellent structure that is built on top of one critical thing “ACTION” and not just actions but “CORRECT POWERFUL ACTIONS”.

I believe that if I take all those 100 actions (believe me it is not as easy as you can read it ) my financial life will move from where it is now towards positivity. I believe that 100MoneyActions will bring in structure and actions that is missing in my financial life. And I wish that it will do the same to many more like me! Big thanks to this concept and all the best to the program/concept. I am sure it will be a great success.

Prasad Kulkarni

IT Professional

Pune

100 money actions is one of the best thing that has happened to me. This is one program which I am following very religiously over the last 2 weeks. After reading so much on Jagoinvestor blog I used to think that my all fandas related to investment instruments, finance management etc are in place but still I was not sure if I am doing everything right or I am taking enough actions to put the plan on track. This program is helping me in structuring my thoughts, making me aware about the smallest of gaps, consolidating literally everything.

Today I am using the sheets of this program extensively to track the progress of my actions which I am supposed to do within the defined timelines. While your blog and its articles are very informative and in plain English for a layman, this program is a next step to identify, structure and follow the actions which you always want to take. I am so thankful that I came in contact with you guys. Thanks Manish & Nandish. Cheers!

Anuj Gupta

IT Professional, Microsoft

Delhi & NCR

What you get on JOINING this ACTION REVOLUTION ?

PLEDGE Sheet (Your commitment with yourself)

100 Investigative Questionnaire (GAP Analysis)

Well designed ACTION document that helps you to complete 100 actions

Ready Reckoner List of Financial Products

Simple Structure to complete 100 money actions

Supporting Audio Files

Personal Finance Tools and templates where required

Useful Ebooks, Study material and resources for support

What it takes to be a part of this ACTION REVOLUTION ?

It takes commitment to be a part of this ACTION Revolution. You will have to trust the structure of this program. If you can make a commitment you will complete all 100 actions you can be a part of this revolution. Anything free has no value so it calls for a small financial commitment to be a part of this program.

Visit 100 money actions website and get more idea on how you can be a part of this personal finance action revolution. From the bottom of our heart we invite you to be a part of this ACTION REVOLUTION. Once you complete these 100 actions in your financial life, your financial life will not be the same and THAT IS OUR PROMISE TO YOU.

Now, anything free has no value so we decided to keep a small fee to be a part of this action revolution which is Rs. 1999/- only.( This fee is to generate commitment in you). Don’t let your concerns get in your way, don’t let the conversation of money get in your way as your Financial life is Priceless. Paying Rs 1,999 will not make you bankrupt but not taking actions will surely lead you to bankruptcy

You must have heard the name of Parag Parikh, the veteran who has spend decades in the Indian stock markets. He runs PPFAS (Parag Parikh Financial advisory services) . They have been running PMS scheme for quite a while now, since 1996!. They have been practicing value investing from decades and now they have decided to enter the mutual fund space, not just as another also ran, but with a very clear focus. They want value investing to be the prime focus of investing in equities and have come up with “PPFAS Long Term Value Fund”. SEBI has cleared it and it will launch by next month!

So, I decided to directly catch Rajeev Thakkar , CEO & Fund Manager of PPFAS Mutual Fund to answer few questions for our readers. This should give us a clear idea of their vision. Those of you, who would really like to invest in equities for a very long term like 10-12 yrs, can place your bets if you find you are interested.

Here are few questions I asked Rajeev Thakkar (he has been managing the PMS for PPFAS since 2003).

1. A lot of investors still do not know about PPFAS . Would you like to share its history?

PPFAS Ltd. our Sponsor, was incorporated in 1992. Prior to that, our Chairman, Mr. Parag Parikh, ran a proprietary organisation from 1979. It was one of the earliest recipients of the Portfolio Management Service (PMS) licence, having secured it in 1995.

Over the years, it has transformed itself from being a stock and fixed income brokerage house to a reputed Portfolio Manager and currently manages over Rs. 300 crores in its flagship scheme. It has now embarked on the next step in asset management by sponsoring PPFAS Mutual Fund.

2. Why PPFAS entered Mutual funds when you already had a successful PMS ?

The main reasons behind this move are –

a) Over the years, the landscape for PMS has become progressively challenging for the investor. A hike in the minimum ticket size and increasingly tedious account opening procedures are two examples.

b) A PMS product is also perceived to be an opaque one – though we can proudly say that we defy this perception by disclosing various key data points on our sponsor’s website [www.ppfas.com].

c) Tax treatment of capital gains in a PMS product has also been a point of contention, subject to various interpretations based on the nature and frequency of the transactions .

On the other hand, a mutual fund is a far more regulated and transparent investment vehicle as compared to a Portfolio Management Scheme. Unlike PMS schemes, a mutual fund scheme’s performance, portfolio etc. is tracked by independent research agencies on a regular basis. This helps an investor in making comparisons and allocating capital accordingly. It scores on the operational front too. For instance, each time a client opts for a PMS scheme he/she has to undergo

tedious and time-consuming Know-Your-Client (KYC) related formalities.

This can be obviated in case of a mutual fund, where one KYC / KRA number is valid across all mutual funds. An investor is also able to deploy smaller amounts of capital in a mutual fund scheme. This is especially helpful when they are testing the waters. This latitude is all the more useful, now that the minimum initial corpus for a PMS account has been raised from Rs. 5 lakhs to Rs. 25 lakhs.

For fund managers too, a mutual fund is operationally easier to manage as it does not call for segregation of individual accounts, separate order placement etc. Unlike a PMS scheme, a mutual fund scheme is treated as a pass-through vehicle, thereby making it a more tax-efficient vehicle for investors.

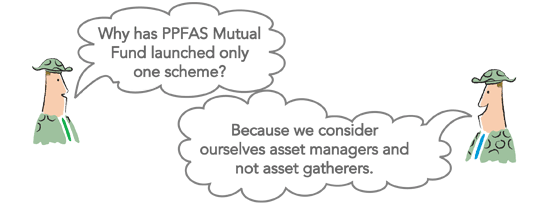

3. Can you share why you have come up with just a single equity fund? Won’t you come up with 5-10 funds ?

Yes. In an age of ‘the more the merrier’ we walk alone. Others may launch an array of equity schemes with narrowly focussed objectives, but we believe, this leads to needless duplication and confusion.

PPFAS Long Term Value Fund’s mandate permits it to invest in companies, unfettered by any self-imposed limitations with regard to market capitalisation or geography. We believe that if our investors’ objectives can be met through one scheme there is no need to launch a slew of them. Hence it will be our only offering in the equity segment.

4. What are the top 3 things which you feel will be different with PPFAS LTEF and other equity funds in market? What is the value proposition you are offering?

The top three differences between us and the others is –

We will be the first mutual fund to disclose the holdings of key employees of PPFAS Mutual Fund in the scheme.

As mentioned above, we will launch only one scheme in the equity segment.

On our website (amc.ppfas.com) we have explicitly mentioned the kind of investors, we do not want. I do not know of any other mutual fund which actively discourages the wrong kind of investors from investing in its schemes.

Apart from these, there are a few more differences which have been outlined on our website

5. As It is a new entry in mutual funds, a lot of investors might want to wait and watch for the performance of your NFO. What do you have to say about it?

Sure… We are cognizant of that.

That is why we are not hard-selling our scheme through the mainstream media at this juncture. Also, that is why we have not approached the national distributors / banks. Only a few distributors (currently 20) who believe in our approach have signed up with us.

Many key investors in the PMS scheme of our Sponsor, have agreed to migrate to ‘PPFAS Long Term Value Fund.’ They will form the nucleus of our scheme. Besides these, we have received over 300 expressions of interest from new investors through our website and other sources. Some of them may invest either at the New Fund Offer stage or soon thereafter.

We envisage greater interest among the distributor community after a couple of years, once we have built a track record and are actively tracked by reputed agencies such as Morningstar and Value Research.

6. I am sure a lot of investors might want to invest through DIRECT route now. How can some one invest easily with PPFAS, because right now I suppose you do not have a lot of offices across India or in various cities?

We are actively promoting the benefits of investing through the Direct Plan, positioning it as a cost-effective mode of investment. Investors can choose between

The online option – via our website

OR

The offline option – Investors can submit the duly filled forms either at our Corporate Office in Fort, Mumbai or at any of the offices of our registrar, CAMS, who will double up as Points of Collection. CAMS has a very good network of offices India-wide.

7. What is your outlook for next 10-20 yrs for equity markets? I am asking you this, because you have come up with a equity fund, saying that it’s a long term fund.

While our scheme stresses on the long-term it does not necessarily mean that we have any strong view on the state of the overall stock market. Our premise is that investment-worthy stocks will be available irrespective of index levels and we prefer to concentrate on that aspect, rather than crystal-gaze.

Having said that, we obviously believe that equities form an important constituent in the portfolios of most investors now and over the coming decades and as a corollary, you could infer that we are positive on the future prospects of equities in general.

8. Anything else you would like to tell our readers?

Just like the boilerplate which states ‘Read the offer document carefully before investing’ we urge investors to read the contents of our website carefully and then decide whether you would like to invest with us or not.

While we cannot guarantee you any returns owing to the volatility inherent in equities, we will manage your money prudently, based on the time-tested principles of value investing, and play a role in helping you achieve your long-term financial goals. We are here for the long-term and our journey is just beginning. You could join us if you believe in our method of money management.

Scheme Information Document – PPFAS Long Term Value Fund

While there are tons of AMCs in India, most of them focus on too many funds. PPFAS mutual funds seem to be very focused on what they believe in and seem to be on the path to evolve as a fund house that’ll be known for value investing. In a recent interview with firstport, Mr. Parag Parikh is sharing how they are themselves going to put their own money into the fund, so that there is inherent accountability and committment.

About 29 years ago, I started off as a broker and we were the first brokers to have a research department. That was the competitive edge which I wanted to get the institutional business, because that was cornered by about 12-13 brokers. As far as broking was concerned, we always believed money management is a profession rather than a business. When it is a profession, you do what is good for the client. But when it turns into a business, you do what the business demands.

Unfortunately, in mutual funds today you have this mad craze for getting assets under management. You have marketing teams, distributors. You pay them anything to get the money. From our MF’s point of view, we were professionals and we will keep it that way and run the MF as professionals. That’s the idea.

Ultimately, when you invest in our fund, what are you looking at? Returns. That is where we want to be game-changers. Secondly, what is your commitment to a fund? Today, me, Rajeev (Thakkar, CEO of PPFAS AMC) and all our senior people are going to make our own equity investments through the fund. We have to believe in what we’re doing. Whatever equity investments we have in the market, we’d rather put that in the fund.

Are you going to invest in PPFAS mutual funds ? Anyone !

We are extremely delighted to share the news about the launch of our 3rd book – “11 principles to achieve financial freedom”, which is written by Nandish Desai and published by CNBC18. I consider this book as a masterpiece work by Nandish, which presents a totally new dimension to investors on how to think about financial freedom and how to step by step improve their mindset and thinking beyond the traditional thinking and ideologies when it comes to money.

When Nandish started writing the book, we brainstormed many times as we wanted to make sure the book becomes a gem of the lifetime. I read the book at every stage and re-read it 3-4 times after it was completed (as part of proof reading and to check things are fine) and every time I personally got so much learning and value out of it. I think every investor who will not read this book will loose some thing amazing in his life.

What is the Book all about – “Forward” from me

The best way to give you an idea about what this book is all about, I am putting the “Forward” section which is written by me specially for the book. It will clearly give you the understanding of what this book is all about.

Right now, what you are holding in your hands is not just a book, but years of effort and creation. Nandish and I started our career making financial plans and somewhere we started to realize that many investors’ financial life was changing after having a financial plan in their life. After a lot of research, we concluded that a financial plan was just one part of the process and other elements were required to live an awesome financial life. This book is about those elements that we have discovered over time.

We challenged the traditional financial planning process a few years ago and that is how our financial coaching program came into existence. This book is based on our financial coaching program that we have conducted with over 100 people spread across the globe.

With this book, we invite each investor to look beyond financial products and returns, and look at wealth creation as a game. Most investors make investments out of compulsion and out of need; the core message of this book is to see wealth creation as a project and will teach you how to fall in love with the process of wealth creation.

There are books that follow the trend and there are some books that set the trend. This book falls in the latter category; it is here to set the trend in the personal finance world.

Discovering who you are as an investor

Most investors are in search of solutions and answers; this book is not about getting answers, but about discovering who you are as an investor and gaining insights on how you can connect with your true wealth.

Nandish has written this book after working with hundreds of people. I am sure this book has the power to change your financial life; to some it will act as a wake up call, to some it will help them discover who they are as an investor, to some it will help them add different dimensions to their financial life.

While I was going through the initial draft of this book, I was convinced that this book would be a game changer not only for investors but also for financial planners. This book is simple and yet powerful and it will leave a deep impact on you as an investor.

There is a lot of hype around the words “personal finance” and “money” out in the world. While you are reading, this book will teach you to fall in love with the process of wealth creation.

Working with a Financial Coach

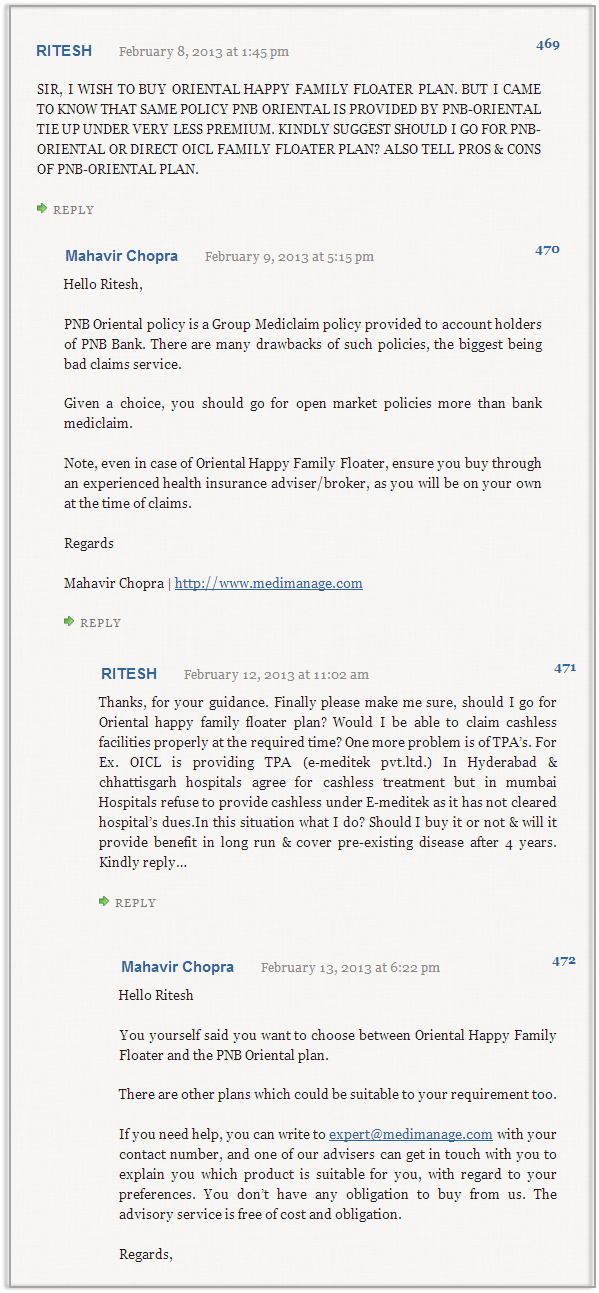

The narrator of this book is Sam, an IT professional based in Mumbai, who shares his experience of working with a financial coach. This book is not a story but it has conversations between Sam who is a lost, confused and directionless investor and his financial coach. They both meet and Sam participates in a program called the “90 Day Money Game.” The coach invites Sam to work with him for the next 90 days. The money game has 11 exciting levels that span the next 90 days.