A Rose can be of more value than a Dress to your Wife or Girlfriend on Valentines Day. Even though that Rose was very less in Price compared to a Dress.

Today we will discuss things about investment products from a different perspective – Value and Price.

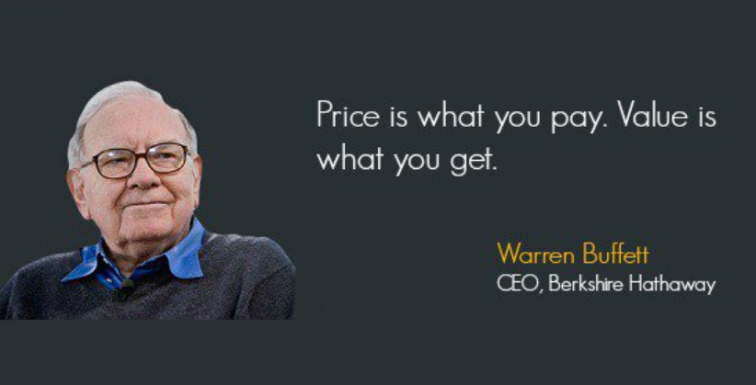

What is Price and Value?

Price : Price is the amount of money needed to purchase something.

Value : Value is the worth or Importance of something.

An Example

We pay Rs.8/Kg (20 cents/Kg) for Salt as part of our Groceries, Will we stop using it if its price rises to Rs.100/Kg or even Rs.400/Kg. May be not !!! Why ? Because the Value of Salt even then will be Very high, compared to the price we pay for it. Considering that, its a very cheap product.

As a personal Example, I recently bought a second hand mobile (Nokia 6610) to keep at my home as a land line just for Rs.800 (worth 8,500 at time of buying, excellent condition). The price i paid for it was much much less than the value it would provide to me. So i consider it as one of the best investments made till date.

By cheap I mean its Price vs Value is very high.

Cheapness (P) = Value provided by P / Price we pay for P.

The same way there can be things for which we pay high amount, they don’t have high value for us.

Please understand that it depends on individual where something is of great value or not. For example for me, an expensive Mobile set with 134 different things costing Rs.10,000 is low in value and high in price. I don’t buy things like that, but a digital Camera worth 12K a value buy for me (because of my interest in Photography)

So, in short we can say “Price is What we pay actually, and Value is what are ready to Pay”

We understand this in our daily Life, but we forget this simple rule when it comes to money and investing. Most of the time we invest in things which we should not because of this basic rule, but we are carried away by emotions or simple stupidity.

Watch this video to learn more about the difference between Price and Value:

Let us now see Some of the products which are really High Value, Low price

Term Insurance :

Term Insurance is one of the best example for this.

“How much are you ready to pay as yearly premium for Rs.50,00,000 Cover for 25 yrs tenure?”.

This is a question I ask a lot of my friends in there 20-30’s. And I am amazed to see that even with a miser mind they tell me at least twice the amount what it really costs. Everyone said 2k/month or min Rs.20,000/year. The actual cost is not more than 13-14k, in fact the best price is 10,112 for 30 yrs tenure from AEGON RELIGARE Life Insurance (Click Here to read more on this).

This clearly shows that it cost way less than the expectations of people and what people are ready to pay for it. The value offered by Term Insurance is more than what it costs.

Endowment Policies :

I am not sure if its my hatred for Endowment Policies or they really deserve my criticism every time, Or may be there are both the reasons. We pay so heavy price for Endowment polices and the value provided by them is almost nothing. Its a product designed for Wealth Creation, but wait … not for investor but for the Insurance company. (Click here to read more on Badness of Endowment Policies)

The other products I would rate in category of Cheap and Expensive are :

Cheap financial products:

- Term Insurance

- SIP investments in Equity Mutual Funds

- PPF

- Good Stocks in low markets (Like current markets, Buy Reliance, Infosys and Jaiprakash Associates for Rs. 1,00,000 each today and your retirement planning is probably Done !! If you are around 25 and retiring at 60)

- An interest free loan given to a close or a very good friend. (even if you don’t get any interest, you get some emotional satisfaction or valuable relationship which is more important).

Expensive financial products:

- Endowment Policies

- Bank FD (at the time of High inflation)

- NSC

- Most of the stocks in High Markets ( not true for all stocks but most of them) – A high interest loan given to someone whom you don’t trust much. (Even if you get good interest, there is risk of loosing money)

Every time you invest your money its important to understand the price of it and value of it. If you find that its cost is less than what you are ready to pay, consider it cheap and go for it and not in the other case. Price and Value depends on Situation, time, age and other factor, don’t forget it.

Stock Market Investments

Most of the successful investors become one because they invest in stocks which are trading at price lower than they deserve, which market eventually finds out later. Currently In this markets Reliance is trading at 1400 (Oct 11, 2008), the it was trading at 2300 before a month, and has lost almost 40-50% in a month.

Considering it is going to start its OIL exploration and other things, its a good stock to own and at an excellent price. Its price is less and its value. Which makes it a good investment regardless of what is going to happen next month or next quarter. Sooner or Later it will turn out to be a good investment and reward its investors.

Same is with Jaiprakash Associates, ICICI Bank, DLF, Ranbaxy and other similar blue chip stocks.

Summary

When you analyse some product, stock, mutual fund, Home (Real estate) or anything for investment matter or even for general shopping, always consider value and price for it.

Disclaimer : Any stock discussed on this article is not a recommendation. Please analyse it yourself and then invest. It can also result in losses.

What do you think about this article? Do you like it?

If you have any query related to this topic you can leave your reply in the comment section.