Let me take one by one each line and do some analysis and raise some questions.

A)Death Benefit:

On death during the first policy year: Basic Sum Assured with Guaranteed Addition.

On death during the policy term after the first policy year, excluding last policy year: 1/3rd of Basic Sum Assured with Guaranteed Addition.

On death during last policy year: 1/3rd of Basic Sum Assured with Guaranteed Addition along with loyalty addition, if any

Some points here to consider:- Your risk cover will be 6 times your investment and just 2 times for the rest of the duration + some loyalty addition if any. So, in a nutshell, it as good as saying your Cover is just 2 times your premium …

– What does it mean? you will get double our initial investments if you die after the first year.

This is the case when you die …

B)Maturity Benefit:

On maturity, the Maturity Sum Assured along with Guaranteed Addition and Loyalty Addition, if any, shall be payable.

Maturity Sum Assured shall be 1/6th of Basic Sum Assured.

– Means, if your premium is Rs 1,00,000, then Basic Sum assured is Rs 6,00,000 and hence, Maturity Sum Assured is Rs 1,00,000

C)Guaranteed Addition:

The policy provides for Guaranteed Addition at the following rates:

Rs. 100 per thousand Maturity Sum Assured per year for a policy of 10 years term.

Rs. 90 per thousand Maturity Sum Assured per year for a policy of 5 years term.

– Means, if your premium is 1,00,000, then your Guaranteed Addition is Rs 10000 (10 yrs) … Means, You will get Rs 1,00,000 as Guaranteed Addition in 10 yrs .. and along with your original capital, you will get back Rs 2,00,000 back after 10 yrs.

D)Loyalty Addition: Depending upon the Corporation’s experience the policy will be eligible for Loyalty Addition on death during the last policy year or on the Life Assured surviving the stipulated date of maturity at such rate and on such terms as may be declared by the Corporation

This may or may not be there.

Now, let’s take a real like example.

Ajay takes a 6 lacs policy over a 10-year term.

Jeevan Aastha Premium = 96,960

The amount he would get if he dies in the first year: 6,00,000

Amount on Maturity : 97000 + (10*10000) = 197000 (loyalty bonus is not assured , so not adding it)

from what angle do you think this policy makes sense. You are maximum doubling your money in 10 yrs and nothing else. And the best time to die after taking the policy is the first year itself .. then you can get a little benefit (but still at a big cost).

I don’t understand why people complicate things .. LIC plans to collect Rs 25,000 Crores from this policy, and I am sure they will succeed. Because there are many people in our country, who don’t understand the effects of Inflation, compounding and get confused with all those confusing statements.

Now if you are a regular reader of this blog .. then you should be able to utilize Rs 97,000 to generate better returns than Jeevan Astha.

Let us do this …

1. Insurance for the cover of 6 lacs, not just for the first year but for all 10 years .. Simple: Take a term Insurance of Rs 6 lacs for 10 yrs, it’s around Rs 9840 (single premium, SBI life insurance for a 26 yr old ) …

2. After this, you are left with around 88,000, which you should invest in Equity Diversified mutual funds either one time or through SIP for 10 yrs … Even if we take a 10% return. It would be 2,28,000.

When it comes to Investing, just Keep it Simple, Stupid (K.I.S.S) … 🙂 UPDATE (28 AN 2009 ): Shyam Pattabi (writes for HINDU) also shares his similar thoughts on this product at http://www.shyamscolumn.com/2009/01/guaranteed-return-schemeanyone.html ( i am glad I made correct analysis) Update (Jan 19, 2008): On NDTV Profit, Monika Halan has given comments that “Jeevan Astha” should be the last product you should look for and only if you have cash to put nowhere, They have given “Don’t Buy” rating to this product and they also said that this product has lots of hype got created. Monika Halan is Editor of “Outlook Money” and One of the most mature and best personal Finance advisor I can think of.

Disclaimer: The above analysis is based on my study and should not be taken as investment advice or discouragement from advice, use your own analysis to take your decisions. I will not be responsible for your investment decisions.

Planning your financial life does not mean planning for your long term financial needs only, It will be incomplete unless you keep an emergency fund for the unexpected emergency situations.

In this article i will tell you why it is important to keep emergency fund and how much of this fund you should keep aside.

What is Emergency fund?

Emergency fund is the money that you should keep aside, so that you can use it in case you meet up with some sudden financial surprises, for example –

Emergency funds are not to satisfy the daily expenses and basic needs, it is a support that you will have when you really need it in your hard time.

Why is is essential to have an emergency fund?

Having an emergency corpus must be the priority for everyone while planning for a great financial life. Let’s see some of the impacts of having emergency fund on your personal and financial life.

1. Helps you to keep your stress level low

When your know that you have an emergency fund, you can live a stress-free and relaxed life. Because you know that you have a backup plan and so if any emergency pop-ups you are already ready to face it.

2. No need to take an emergency loan

Taking a loan or asking for money in your hard time can sometime hurts your pride. Having an Emergency fund will be helpful not only to solve the problem but it also protects your self-esteem.

3. Don’t have to redeem from your future savings

Your savings are related to some very important future goals of yours. Contingency fund will help you to protect those dreams of yours by satisfying your today’s emergency need.

4. No need to cut your essential expenses –

It happens with most of the people, they have to sacrifice their expenses though they are important, to collect money for their unplanned or emergency expenses. Having an emergency will be a helpful hand in those difficult times of yours.

Why it makes sense to have an Emergency fund?

With the global slowdown, there are many cases of unexpected job losses in the field of Finance, IT, Manufacturing and many others. You never know when you will be without job.

Lets take two scenario when you loose your job and you either had Contingency funds and you did not, Let us see what happens in these two cases.

Case 1: You do not have contingency Funds: Put yourself in this Situation, Close your eyes and try to think about this situation, How do you feel?

Your Family depends on you, all your family expenses are met with you salary, now you loose your job!! What if you don’t find another job soon? In this situation you have a heavy pressure on you to anyhow find a new job as soon as possible, You need a JOB !! and not a “good” or “appropriate” or “Dream” JOB.

If you find a job, but you don’t like it or wanted to do it .. still you will have to take it because of the pressure of “finding a JOB because of others depending on you” …

You compromise on Salary, Company and your wishes. Why does this happen? This happens because you cant wait, because you don’t have the to survive of another 1-2-3 months. You know that you can wait a little more and find a good job suitable for you, but you cant wait.

Case 2: You have Sufficient Contingency Funds: This case is just the opposite of what we discussed above. When you have sufficient CF, you have a relief in mind that you have sufficient time to find a good job without compromising your family needs.

You don’t feel the pressure to get the job ASAP. Though you have to find a good job soon, its not necessary that you take any shitty job which comes your way …

See this Video too …

How to start saving for Emergency fund?

1. Pre-decide your monthly expenses –

Plan your monthly expenses. Try to control your expenses as much as possible, so that you can save money to invest in your emergency fund. Today’s unnecessary expenses can have a bad impact on your savings for your contingency fund.

2. Set an auto deduction towards emergency fund –

When you set an auto-deduction for your emergency fund at the start of the month, you will not have any regret at the end of the month for not saving anything for your unexpected emergencies.

3. Don’t touch the emergency fund for quick needs or smaller crisis –

Lot of people do this mistake, they use their emergency corpus for the some very small emergencies which they can handle with their routine expenses also. You should criticize the situation and

4. Save for emergency before investing in long term goals –

You long term investments are related to your specific goals. So it is obvious that you have as emotional attachment with those investment and you don’t want to touch that money for any other purpose. If you have an emergency fund, then you don’t need to use the money you have invested for your future dreams.

Besides, some long term investment have lock-in period, so if you want to redeem your money before completing the maturity time period, you will have to pay some penalty charge.

Where to have Contingency funds?

As per the name, it can be seen that this amount is required at the time of unforeseen situation which can happen anytime,so it must be parked at some liquid avenue like Bank account or Liquid funds.

If you are keeping 4 months of funds as CF, then you can keep 1 month money in Cash and rest 3 months money in Liquid funds.

Summary: Contingency Funds are the part of Risk management. And risk management is something no one should avoid. People realize its importance only when they plan for it and get trapped in a situation which demands Contingency funds. ..

So now its your turn. Plan for it, be ready for unplanned emergency, and secure your future.

What do you feel after reading this article? Do you agree with this?

do let us know what do you think about the concept of emergency fund and also your view on this article in our comment section.

This is a time when long term investing should be done. If you have spare cash for long term, Equity is for you. But how do you do it? How do you choose them? What are the important things you should look at while buying shares for long term?

There are some key things we will have a look at today, these are the key ratios discussed in book Profitable Investment in Shares, by S.S Grewal and Navjot Grewal.

But, before reading them understand that they are ratios which good indication of share prospects and are not guarantee about share price rise in long term, Share markets always run on Emotions and perspective which can change anytime…

Also periodic review is necessary, just buying today and looking after 10 years is not the idea… Buying is always the first step, Periodic review is the next.

8 Ratios to look before buying a share

1. Ploughback and reserves

After deduction of all expenses, including taxes, the net profits of a company are split into two parts — dividends and ploughback.

Dividend is that portion of a company’s profits which is distributed to its shareholders, whereas ploughback is the portion that the company retains and gets added to its reserves.

The figures for ploughback and reserves of any company can be obtained by a cursory glance at its balance sheet and profit and loss account.

Ploughback is important because it not only increases the reserves of a company but also provides the company with funds required for its growth and expansion. All growth companies maintain a high level of ploughback. So if you are looking for a growth company to invest in, you should examine its ploughback figures.

Companies that have no intention of expanding are unlikely to plough back a large portion of their profits.

Reserves constitute the accumulated retained profits of a company. It is important to compare the size of a company’s reserves with the size of its equity capital. This will indicate whether the company is in a position to issue bonus shares.

As a rule-of-thumb, a company whose reserves are double that of its equity capital should be in a position to make a liberal bonus issue.

Retained profits also belong to the shareholders. This is why reserves are often referred to as shareholders’ funds. Therefore, any addition to the reserves of a company will normally lead to a corresponding an increase in the price of your shares.

The higher the reserves, the greater will be the value of your shareholding. Retained profits (ploughback) may not come to you in the form of cash, but they benefit you by pushing up the price of your shares.

2. Book value per share

You will come across this term very often in investment discussions. Book value per share indicates what each share of a company is worth according to the company’s books of accounts.

The company’s books of account maintain a record of what the company owns (assets), and what it owes to its creditors (liabilities). If you subtract the total liabilities of a company from its total assets, then what is left belongs to the shareholders, called the shareholders’ funds.

If you divide shareholders’ funds by the total number of equity shares issued by the company, the figure that you get will be the book value per share.

Book Value per share = Shareholders’ funds / Total number of equity shares issued

The figure for shareholders’ funds can also be obtained by adding the equity capital and reserves of the company.

Book value is a historical record based on the original prices at which assets of the company were originally purchased. It doesn’t reflect the current market value of the company’s assets.

Therefore, book value per share has limited usage as a tool for evaluating the market value or price of a company’s shares. It can, at best, give you a rough idea of what a company’s shares should at least be worth.

The market prices of shares are generally much higher than what their book values indicate. Therefore, if you come across a share whose market price is around its book value, the chances are that it is under-priced. This is one way in which the book value per share ratio can prove useful to you while assessing whether a particular share is over- or under-priced.

3. Earnings per share (EPS)

EPS is a well-known and widely used investment ratio. It is calculated as:

Earnings Per Share (EPS) = Profit After Tax / Total number of equity shares issued

This ratio gives the earnings of a company on a per share basis. In order to get a clear idea of what this ratio signifies, let us assume that you possess 100 shares with a face value of Rs.10 each in XYZ Ltd. Suppose the earnings per share of XYZ Ltd. is Rs.6 per share and the dividend declared by it is 20 per cent, or Rs 2 per share.

This means that each share of XYZ Ltd. earns Rs 6 every year, even though you receive only Rs 2 out of it as dividend.

The remaining amount, Rs 4 per share, constitutes the ploughback or retained earnings. If you had bought these shares at par, it would mean a 60 per cent return on your investment, out of which you would receive 20 per cent as dividend and 40 per cent would be the ploughback.

This ploughback of 40 per cent would benefit you by pushing up the market price of your shares. Ideally speaking, your shares should appreciate by 40 per cent from Rs 10 to Rs 14 per share.

This illustration serves to drive home a basic investment lesson. You should evaluate your investment returns not on the basis of the dividend you receive, but on the basis of the earnings per share. Earnings per share is the true indicator of the returns on your share investments.

Suppose you had bought shares in XYZ Ltd at double their face value, i.e. at Rs 20 per share. Then an EPS of Rs 6 per share would mean a 30 per cent return on your investment, of which 10 per cent (Rs 2 per share) is dividend and 20 per cent (Rs 4 per share), the ploughback.

Under ideal conditions, ploughback should push up the price of your shares by 20 per cent, i.e. from Rs 20 to 24 per share. Therefore, irrespective of what price you buy a particular company’s shares at its EPS will provide you with an invaluable tool for calculating the returns on your investment.

4. Price earnings ratio (P/E)

The price earnings ratio (P/E) expresses the relationship between the market price of a company’s share and its earnings per share:

Price/Earnings Ratio (P/E) = Price of the share / Earnings per share

This ratio indicates the extent to which earnings of a share are covered by its price. If P/E is 5, it means that the price of a share is 5 times its earnings. In other words, the company’s EPS remaining constant, it will take you approximately five years through dividends plus capital appreciation to recover the cost of buying the share. The lower the P/E, lesser the time it will take for you to recover your investment.

P/E ratio is a reflection of the market’s opinion of the earnings capacity and future business prospects of a company. Companies which enjoy the confidence of investors and have a higher market standing usually command high P/E ratios.

For example, blue chip companies often have P/E ratios that are as high as 20 to 60. However, most other companies in India have P/E ratios ranging between 5 and 20.

On the face of it, it would seem that companies with low P/E ratios would offer the most attractive investment opportunities. This is not always true. Companies with high current earnings but dim future prospects often have low P/E ratios.

Obviously such companies are not good investments, notwithstanding their P/E ratios. As an investor your primary concern is with the future prospects of a company and not so much with its present performance. This is the main reason why companies with low current earnings but bright future prospects usually command high P/E ratios.

To a great extent, the present price of a share, discounts, i.e. anticipates its future earnings.

All this may seem very perplexing to you because it leaves the basic question unanswered: How does one use the P/E ratio for making sound investment decisions?

The answer lies in utilizing the P/E ratio in conjunction with your assessment of the future earnings and growth prospects of a company. You have to judge the extent to which its P/E ratio reflects the company’s future prospects.

If it is low compared to the future prospects of a company, then the company’s shares are good for investment. Therefore, even if you come across a company with a high P/E ratio of 25 or 30 doesn’t summarily reject it because even this level of P/E ratio may actually be low if the company is poised for meteoric future growth.

On the other hand, a low P/E ratio of 4 or 5 may actually be high if your assessment of the company’s future indicates sharply declining sales and large losses.

5. Dividend and yield

There are many investors who buy shares with the objective of earning a regular income from their investment. Their primary concern is with the amount that a company gives as dividends — capital appreciation being only a secondary consideration. For such investors, dividends obviously play a crucial role in their investment calculations.

It is illogical to draw a distinction between capital appreciation and dividends. Money is money — it doesn’t really matter whether it comes from capital appreciation or from dividends.

A wise investor is primarily concerned with the total returns on his investment — he doesn’t really care whether these returns come from capital appreciation or dividends, or through varying combinations of both. In fact, investors in high tax brackets prefer to get most of their returns through long-term capital appreciation because of tax considerations.

Companies that give high dividends not only have a poor growth record but often also poor future growth prospects. If a company distributes the bulk of its earnings in the form of dividends, there will not be enough ploughback for financing future growth.

On the other hand, high growth companies generally have a poor dividend record. This is because such companies use only a relatively small proportion of their earnings to pay dividends. In the long run, however, high growth companies not only offer steep capital appreciation but also end up paying higher dividends.

On the whole, therefore, you are likely to get much higher total returns on your investment if you invest for capital appreciation rather than for dividends.

Watch this video to know more detailed information about dividend and yield :

In short, it all boils down to whether you are prepared to sacrifice a part of your immediate dividend income in the expectation of greater capital appreciation and higher dividends in the years to come and the whole issue is basically a trade-off between capital appreciation and income.

Investors are not really interested in dividends but in the relationship that dividends bear to the market price of the company’s shares. This relationship is best expressed by the ratio called yield or dividend yield:

Yield = (Dividend per share / market price per share) x 100

Yield indicates the percentage of return that you can expect by way of dividends on your investment made at the prevailing market price. The concept of yield is best clarified by the following illustration.

Let us suppose you have invested Rs 2,000 in buying 100 shares of XYZ Ltd at Rs 20 per share with a face value of Rs 10 each.

If XYZ announces a dividend of 20 per cent (Rs.2 per share), then you stand to get a total dividend of Rs 200. Since you bought these shares at Rs 20 per share, the yield on your investment is 10 per cent (Yield = 2/20 x 100). Thus, while the dividend was 20 per cent; but your yield is actually 10 per cent.

The concept of yield is of far greater practical utility than dividends. It gives you an idea of what you are earning through dividends on the current market price of your shares.

Average yield figures in India usually vary around 2 per cent of the market value of the shares. If you have a share portfolio consisting of shares belonging to a large number of both high-growth and high-dividend companies, then on an average your dividend in-come is likely to be around 2 per cent of the total market value of your portfolio.

6. Return on Capital Employed (ROCE), and

7. Return on Net Worth (RONW)

While analyzing a company, the most important thing you would like to know is whether the company is efficiently using the capital (shareholders’ funds plus borrowed funds) entrusted to it.

While valuing the efficiency and worth of companies, we need to know the return that a company is able to earn on its capital, namely its equity plus debt. A company that earns a higher return on the capital it employs is more valuable than one which earns a lower return on its capital. The tools for measuring these returns are:

1. Return on Capital Employed (ROCE), and

2. Return on Net Worth (RONW).

Return on Capital Employed and Return on Net Worth (shareholders’ funds) are valuable financial ratios for evaluating a company’s efficiency and the quality of its management. The figures for these ratios are commonly available in business magazines, annual reports and economic newspapers and financial Web sites.

Return on capital employed

Return on capital employed (ROCE) is best defined as operating profit divided by capital employed (net worth plus debt).

The figure for operating profit is arrived at after adding back taxes paid, depreciation, extraordinary one-time expenses, and deducting extraordinary one-time income and other income (income not earned through mainline operations), to the net profit figure.

The operating profit of a company is a better indicator of the profits earned by it than is the net profit.

ROCE thus reflects the overall earnings performance and operational efficiency of a company’s business. It is an important basic ratio that permits an investor to make inter-company comparisons.

Return on net worth

Return on net worth (RONW) is defined as net profit divided by net worth. It is a basic ratio that tells a shareholder what he is getting out of his investment in the company.

ROCE is a better measure to get an idea of the overall profitability of the company’s operations, while RONW is a better measure for judging the returns that a shareholder gets on his investment.

The use of both these ratios will give you a broad picture of a company’s efficiency, financial viability and its ability to earn returns on shareholders’ funds and capital employed.

8. PEG ratio

PEG is an important and widely used ratio for forming an estimate of the intrinsic value of a share. It tells you whether the share that you are interested in buying or selling is under-priced, fully priced or over-priced.

For this you need to link the P/E ratio discussed earlier to the future growth rate of the company. This is based on the assumption that the higher the expected growth rate of the company, the higher will be the P/E ratio that the company’s share commands in the market.

The reverse is equally true. The P/E ratio cannot be viewed in isolation. It has to be viewed in the context of the company’s future growth rate. The PEG is calculated by dividing the P/E by the forecasted growth rate in the EPS (earnings per share) of the company.

As a broad rule of the thumb, a PEG value below 0.5 indicates a very attractive buying opportunity, whereas a selling opportunity emerges when the PEG crosses 1.5, or even 2 for that matter.

The catch here is to accurately calculate the future growth rate of earnings (EPS) of the company. Wide and intensive reading of investment and business news and analysis, combined with experience will certainly help you to make more accurate forecasts of company earnings.

Trading and investing are two different things which confuses lot of beginner investors. In this article I’m going to tell you what is trading and investing and how they are different from each other.

What is an Index?

NIFTY and SENSEX are the Index, they are the indicator of how Markets are performing. An Index is created for measuring a particular section of stocks. When the Index goes up or down, they represent the group of Stocks they comprise of.

So if an Index is up you can say with high probability that most of the stocks under them have done well.

What is Nifty and Sensex?

There are many Stock Exchanges in INDIA, BSE (Bombay Stock Exchange) and NSE (National Stock Exchange) are most famous and biggest of all and with maximum business happening there .

Nifty : Nifty is the Index of NSE. Nifty has 50 biggest companies of India representing the companies from almost all of the sectors, Each stock has there own weightages. Like Reliance, Infosys have High Weightage and Ranbaxy has less.

Sensex : Sensex is a Index of BSE, It is comprised of 30 shares.

What are different Indices on Exchanges?

There are different kind of Indices on Stock Exchanges like for NIFTY.

NIFTY : Basket of all the sectors, Represents all the whole Economy CNX IT : For IT stocks CNX 100 : Top 100 Stocks CNX MIDCAP : For Midcap Stocks BANK NIFTY : For Banks

Each Index represents a sector or a group, if you track a Index you can understand how the sector is performing overall.

What is difference between a Trader and Investor?

Trader : A Trader is a person who tries to earn profit from small movements in price, there time horizon is very small like 1 day or a week or some weeks. For example, A trader will buy something @100 and will sell it at 105 and make a profit of 5. He will try to take advantage of volatility.

His main tools will be Charts, News, sector outlook for short term etc. He will not concentrate much on Company fundamentals, Long term sector outlook.

Investor : A Investor is someone who tries to invest money for long term. Long term can be anything from 1 year to 10-15-20 years.

Investor is more concerned about the fundamentals for the companies, its growth and factors like those which are going to drive the share price in long term not short term … Investor is not concerned about the short term volatility. There focus is long term.

How to Begin Trading?

Trading is one of the toughest things to master. Its a better idea to first learn and read about Trading for some months, Watch the markets for some months and try to paper-trade first. paper trade means just trading on paper and seeing how you perform.

Read about Technical Analysis also. Try to gather more and more info on Trading. Read good Books and Learn as much as you can.

Knowledge and your intelligence has very less contribution in your success as Trader. The main things are Money Management, Discipline, Control over GREED And FEAR, and Risk Management.

Once you are very confident you can start, Start with very small Cash and take big bets only when you have made some progress to cheer about.

Have a plan and targets for your Trading. Take Trading seriously as your business and not as hobby, else with high probability you will Fail.

Watch this video to learn about stock trading at beginners level:

How to Begin Investing?

Read How to analyse stocks and Read books. Have a long term horizon and don’t be afraid of your share coming down …

Should you be a trader or an Investor or nothing?

It depends on your personality, the time you want to give in this and your goals. If you find fun with dealing in markets in short term basis, Be a trader.

If you can devote time to markets in daily or weekly basis, then you can be an Investor.

If you are not interested in Either, just don’t be anything .. Do what you are doing right now 🙂

It was a fast written post, I hope thing are clear.

If there is anything in world which can make you instant rich, it’s Options Trading !!! What is instant Rich here !! Instant can indicate anytime from 10 days to 5-10 yrs. It depends on you how much risk you want to take. Options can deliver returns which you can never imagine.

You can get returns in a day equivalent to what you get in 8 years in Fixed Deposit !! 10% return in a week is what I call a realistic average return in long term after risk management.

Just to give an example, if you start with 15,000 and take 10% profit each week, you can generate 1 Crore in 1 year (compounded basis).

How to Trade options?

To just like people trade in Stocks, shares, they can trade in Options .. Buy them at a cost and selling it later at some profit or Loss. The main difference in options trading and Stock trading is that Options trading also has time limit attached to it. That’s makes them more dangerous.

There are some selected shares which have options for them. Almost all the well known stocks have their options. Nifty index also has an option for it.

Almost 85-90% options trading happen in NIFTY options … Each stock option have lot size, like NIFTY lot size are 50. So if the price for NIFTY 2600 CA is 90, 1 lot will cost you 4500. And suppose the price reaches to 200, you can sell it and get 10000, 5500 of profit – brokerage charges.

Some other very good stocks for options trading are RELIANCE, ICICIBANK, CHAMBAL FERTILIZER, JAIPRAKASH ASSOCIATES and many more.

Watch this video to learn more about Options trading:

Some Experiences I can remember

I have often seen an option rise anywhere from 2 times – 50 times.

Just 2 days before NIFTY made the lowest of 2250 in OCT, NIFTY was at 3000, and I bought NIFTY 3000 PA at 60 (NIFTY was at 3000 and 3 days left to expiry). Within 5 min, it went up to 90 and started coming back down .. I sold it at 88 and took good profit of 40% …

Just after I sold it market starting going down and it went up to 200.

Next day market tanked heavily and the price was now 500.

Next to Next day market again tanked heavily and option price was now 750.

Something I bought at 60 was at 750 after 2 days and I sold it at 88. Anyways .. I made good profit and I was happy (It’s a white lie, you know that)

This is a little extreme case, but in general options can give close to 50% – 200% return in short duration. Scenario is very different at the starting of month and at the end of month because of Options expiry. At the time of options expiry, the change in price is significant because of the time value and uncertainty.

How Risky Options Are?

If you don’t fear anything in World, better you fear Options .. It can wipe you out within days … It’s a Money eating machine. You can lose all your money if you are not focused or don’t have knowledge or good money management.

If you are trying hard to lose money and you are not successful, try options ..Warren Buffet calls Derivatives as “Weapons of mass destruction”, I agree with him, but I also differ on the fact that options have the power to make you super rich if you can use it effectively and with intelligence and without GREED.

Advice

If you want to try options trading, first learn about it heavily .. Read books, read stuff .. Watch it for 1-2 months .. See the behavior and once you are confident that you can make some money .. enter with small money (because you are going to lose) …

Don’t feel back after losing money, think of it like “Guru-Dakshina” … everyone has to give it in the start, you are no exception. Now go back .. Again read some more books, Do some virtual trading, and once you are confident again start with small money (which you can afford to lose) .. And start doing the trading slowly step by step … Don’t put all your money in one go .. Else you will cry later.

Disclosure

I have been trading options from last 6 months and still I am in loss and way far than break even .. Please don’t take it as my advice to trade option; it’s just for informational and sharing purpose .. You are yourself responsible for your losses.

“I thought Women are complicated and tough to handle, then I met Options” 🙂

what kind of markets have these been .. a slight news of hope is causing stocks to rally to so much amount which they used to rally in a year .

As i write this Citigroup Corp shares have risen 68% in just 1.5 hrs of trading . 68% in a day !!

That’s a kind of return which mutual funds are really jealous of . Last month when there was some bad news about UNITECH , it plunged by 50% in a day only to recover back 40% the next day ..

Last quarter DLF lost 33% in 2 days on the news of US FDA banning its drugs in US . and then it again came back to its normal levels .

When DLF lost for 2 days , I had seen DLF PUT options went up 50 times in 36 hrs …and on the third day when it was up again by 20% , then its CALL options went up by another 5 times . means if you got everything correct and bought call and put options at right time , you could have made 5 Crores ($1 million) with 4 lacs of money ($8000) . that’s 25000% return in 60 hrs . there is an assumption that you bought things at right time which is almost impossible … but with little luck and study at least 1000% was possible for sure …

I thought of buying DLF puts after it fell for 1st day , but because of fear , i didn’t buy it .. and it went up by 800% next day ( i remember it correct , it went up from Rs 4-5 to Rs 40) , that’s 800-900% return in 2 hrs .

I am sure Citigroup option traders would either have made a killing or killed themselves . 🙂

Anyways , options are extremely dangerous products , its not advisable to get into them unless you are sure what you are doing ..

Read the basics of what are options

We will talk about Equity, Debt and Liquid Funds. We will also discuss dividend distribution tax is treated for all these funds.

First understand what is DDT (dividend distribution tax)

Dividend received from a mutual fund is tax free, but only at receivers hand. But mutual funds have to pay a tax on that dividend to Govt before giving it to us. So actually the tax is paid by mutual fund on behalf of us. This tax is called DDT.

They are the funds that invest more than 65% of their corpus in equity shares of companies. The dividend distributed by such funds is exempt from the dividend distribution tax. So all the dividend which is declared comes to the unit holders, you get 100% of dividends.

But don’t think that this is some extra income .. it is just a part of your own money, after you get the dividend, NAV comes down by that much. This is difference between growth and dividend funds. You actually got some money back, nothing else.

Dividends are are totally tax free and not even DDT is applied to it.

Why to invest : You should invest in Equity mutual funds when you want to invest for long term and when you can take risk. Understand that these funds invest primarily in Equity, so there is more risk, but if you are investing for long term and want capital appreciation to happen, these are the funds for you.

Debt Funds

These funds invest in medium-to-long term debt securities like government bonds and corporate bonds/debentures. The dividend from these Funds are subject to 12.5% Dividend distribution tax. The fund is also liable to pay a surcharge and a cess of 10% and 3%, respectively, on the tax. The effective tax rate comes to 14.16%.

Why to invest : They are debt products and offer good liquidity also. If you want to invest some money for safe returns and for short term goal, then Debt funds are something you can look at.

Liquid Funds

These invest in short-term debt securities (which have a duration of less than a year) like commercial papers, certificates of deposit and call money. The income distributed by such funds is subject to an income distribution tax of 25%. The fund is also liable to pay a surcharge and cess of 10% and 3%, respectively, on the tax.

The effective tax rate for liquid and money market funds is 28.32%.

Why to invest : The main reason for investing in Liquid funds should be Liquidity factor, these funds are most liquid and least volatile .. So if you need to have liquidity in your portfolio, always invest some money in Liquid funds, any extra money lying in your Saving Account above your 1 month requirement should be in Liquid fund.

Conclusion :

There are different type of funds and they all have different purpose, you should see which one suits you and accordingly invest in that. Dividend received from mutual funds are not any extra money like Stock dividend. It is your own money.

Today we will see what is CRR and Repo rate and how they help in combating Inflation and other monitory issues of Economy. CRR and Repo rate are nothing but the tools available in the hands of RBI to maintain the liquidity and growth.

You might know what is CRR and Repo Rate, but may not know what is there significance and how they help. Read whole article to understand.

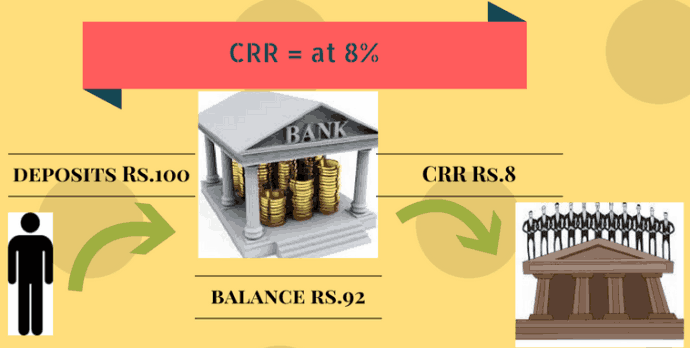

What is CRR Rate ?

Each Commercial Bank has to keep certain percentage from their deposit amount in the current account with the Central Bank of India i.e. RBI. This amount is called as CRR i.e. Cash Reserve Ratio. It is the ratio of deposits which banks have to keep with RBI.

Banks do not have access over this amount for any economic or commercial activity. It means Bank can’t invest the whole deposit and they can’t use the CRR money for any lending or investing purpose.

Let’s see an example – When you deposit Rs.100 to your bank, bank gets Rs.100 and now can use this money to lend others, but they have to put some part of it with RBI, if CRR is 8%, they will have to deposit 8 with RBI and they are left with Rs.92.

So when CRR is decreased, Banks are left with more money to lend and when its increased they are left with less, even though 1% decrease in CRR leaves bank with 93 instead of 92, this Rs.1 is big enough thing.

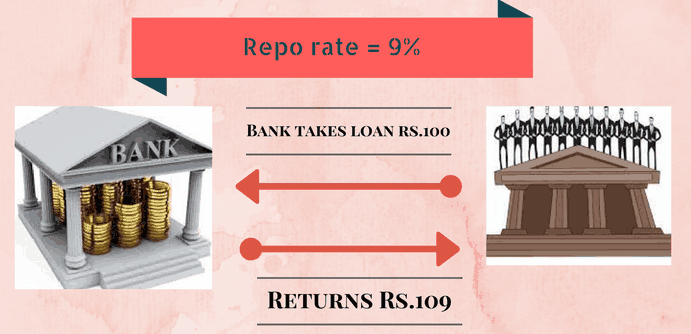

What is Repo Rate?

When we need money, what do we do? We take loan from particular bank. And when we pay back that loan bank charges some interest on principle amount. This is called cost of credit.

Similarly, when banks need money they borrow it from RBI and the rate of interest which RBI charges on that loan on Banks is called Repo Rate or Repurchase Rate.

So if repo rate is 9%, and some bank takes loan of Rs.100 from RBI, they will pay interest of Rs.9 to RBI. This is a short term loan i.e. upto 1 to 2 weeks.

Higher the Repo Rate higher the cost of short-term money, Lower the Repo rate lower the cost of short-term money. This means at higher Repo Rate the economic growth will slow down and at lower Repo Rate economic growth will enhance.

How is Repo Rate linked to the interest we pay for loans from Bank ?

Simple, Banks need to charge more interest than they are paying, so if repo rate is 8%, they will charge more than 8% for loans which they give, If Repo rate comes down, banks’ may also consider the interest rate they charge us.

That’s the reason why with this latest Repo rate cut, people are talking about home loans rates coming down, so what will happen is that Bank need to pay less interest for the loan they take from RBI, now because they are paying less, they may think of charging us less on the interest for the loans which we have taken from them.

What is Money Creation ?

How does money get created? When A gives 100 to B, Rs.100 is created for B , then when he gives this to C, 100 is again created for C, this way money creation happens for different people from that same 100.

How does CRR help ?

Suppose CRR is 8% you had 100, which you deposit to bank, now bank will Deposit 8 to RBI and lend this 92 to some one, This 92 will be another money which is created for someone, now this 92 will exchange hands and then come back to bank somehow, out of this 92 again bank will deposit 7.36 to RBI and then lend the rest of it to someone … and it goes on like this.

It means that this 100 actually generates 1250 in the economy indirectly. What will happen if CRR is increased by 1%, from 8% to 9%. though it may looks like that this is a small change and it would affect a lot.

Lets see what happens now . . .

How much money will 100 create now?

Ans = 100/.09 = 1111 (approx)

So the same money is now generating 1111 instead of 1250, that’s 139 less or 11.12% less money in the market.

How does Repo Rate and CRR help to ease Inflation?

Repo Rate:

When Repo Rate increases, the banks have to pay higher interest to the RBI and thus Banks also charge higher rate of interest to the common public who borrows loan from bank. Due to this people gets discouraged to take more credit from banks, because of which there is less supply of money in system and there is less Liquidity.

So on one hand Inflation is under control as there is less money to spend and on other hand growth will slow down as companies or people avoids taking loans at such a higher interest rate.

CRR:

It’s easy, if CRR is increased, banks have to deposit more money with RBI and banks will have less money to invest. So now bank will increase the interest rate on the loans which they will lend to other people.

People will avoid taking loan because of higher interest rate and it results in less money creation in economy, and hence people have less money to buy things and they will think twice before paying higher price for something. Due to this prizes will fall because of low demand.

What makes an Healthy financial Portfolio? There are some good traits of portfolio which makes it better than others. A good and strong portfolio has some strong elements or parameters which it must meet. These are the Pillars for a strong Portfolio or Investments.

This is one of the biggest reason to invest. Isn’t it very obvious? Yes, it is. But the main point is not just its growth in numbers but its real worth. We are talking about Post-tax and post inflation returns.

The real return of Plain Fixed Deposits in these high inflation days are negligible when you factor out Inflation and tax. The best investment must be robust and good enough to provide appreciation in real worth over long period of time. Real Estate and Equity (Long term) can generate good returns.

Liquidity

Another important aspect of a good financial portfolio is that its provide enough liquidity, so that in case of need, you can get the money.

What is Liquidity? Liquidity is how fast and easily asset can be sold and you can get cash. For example Mutual funds and Shares are highly Liquid, If you have them and want to sell, you can get the money soon. Where as Real estate is not a Liquid asset. So if you need urgent cash, you might not find right price and or buyer.

Every portfolio must have some element of Liquidity, as per the requirement of the investor.

What do we mean by this? A good investor is one who sees beyond what an average investor cant see. Average investors concentrate very well on Profits, How good an investment can be, High returns etc.

An exceptional investor goes beyond that and takes care of Worst case Scenarios and situations which may cause damage. He is the real investor.

Some of the steps to be taken are :

Adequate Insurance to be taken .

Proper monitoring of performance of investment.

Getting out early in a bad investment and accepting that you made a wrong decisions.

Keep your self updated with news, laws, things which can affect you investments.

Risk management is not buying some product for managing risk but being aware of things and taking right and logical decisions.

Goal Oriented

“A good investment is one which has a purpose”

Each and every investment should be done because of a strong reason. I see people who take Insurance policies to save tax at the last rush hour of the year !!! Better loose the tax benefit and don’t take that policy.

That kind of investment is nothing more than a waste or burden. On the top of it these people don’t even need insurance !!!

When someone asks you the reason for making a investment, you should know why you did it?

Some of the bad or idiotic reasons for doing investments are :

I can save tax by that

My friend did it and recommended me

Everyone is doing it .. why shouldn’t I?

Every time you take a decision ask yourself some questions like :

Do i really need it at this point of time?

Can i afford it?

Do i understand it well? Can i protect myself if people make me fool?

What is the purpose or goal of this investment?

If you get satisfactory answers go for it else take an expert advice.

watch this video to learn more about investment analysis and portfolio management :

Sample Portfolio Analysis.

Sample Portfolio 1

Robert is a married person earning 40,000 per month. He is the sole Earner of the family and and has 2 kids. He is not a risk taker and his portfolio looks like.

50,000 invested in NSC (opened before 3 years)

An endowment policy with 10 lacs cover and 40,000 premium for 30 yrs, with maturity benefits.

1,40,000 in a Tax saving mutual funds (investment 70k for 2 years for tax saving)

Home (Rs.30,00,000)

Cash : 20,000

Car : worth 5,00,000

Jewelry worth 80,000

Lets rate his financial portfolio on all the parameters on the scale of 5 stars

Capital Appreciation : A small portion in Equity, and that too for a wrong reason of just tax saving, Saving through Endowment policy is another wrong decision, the returns are too less.

Liquidity : None of the assets are Liquid and Cash available is not enough to meet emergency requirement.

Risk Management : No Risk management, What if he dies after 10 days, What if he meets an accident, What if suddenly he requires 1,00,000, what if he looses his Job.

Goal Oriented : * (The reasons for investment in most of the things looks like they are for Tax saving, or some one suggested )

Sample Portfolio 2

Ajay is married and has 2 kids and parents who are all dependent on him, He earns 40,000 per month.

Long term investments in Tax saving Mutual Funds (Rs.4,000 per month)

Term Insurance of Rs.80,00,000 (80 Lacs)

Health Insurance of each member up to 3,00,000 – 4,00,000 (Family Floater Policy)

Yearly Contribution to PPF (Rs.50,000)

Invested 1,00,000 in Liquid Funds

Home loan taken by him and his Wife Jointly (Along with Home Loan Insurance)

30,000 invested in Gold ETF and some good shares.

Rs.25,000 Cash

Lets rate his financial portfolio on all the parameters on the scale of 5 stars

Capital Appreciation : Appropriate investment in Equity with long term view, and some money in Debt.

Liquidity : Has good amount of money in Liquid funds, Cash and Gold ETF, which have good liquidity and can provide him Money quickly in case of requirement.

Risk Management : In case of any type of Eventuality, He is properly covered. He is protected well against Death, Health Issues, Home related issue, Emergency issues.

Goal Oriented : Most of the investments have strong and valid reasons.

Like Term Insurance is required for Financial Cover, Mutual funds investment was for Long term Wealth Creation, PPF investment for Wealth Creation with Debt Route and safe investment, Joint Home Loan with wife for Tax benefits, Health Cover for Tax benefits and cover against Health Issues, Gold Investment in ETF because of Diversification and Liquidity, Cash for instant requirement, Liquid funds investment for Liquidity along with some returns.

Note : Both the financial portfolio’s are created just for the illustration.

Summary

Each and every person portfolio should be strong on all the areas, it should pass all the criteria to some extent. A portfolio should pass all the parameters for different requirements. If you have a financial portfolio ask yourself all these questions :

Is it good enough to provide stable and good returns over long term. Is capital appreciation happening in Value or just numbers are growing, but post-tax and post-inflation returns are negligible.

If i require instant money within 2 hrs, 2 days or 5 days, Is my portfolio smart enough to provide me.

Is my portfolio good enough to provide protection to me and my family against calamities or any unexpected events . Do i review my Portfolio in regular basis to cut out the losers.

Is my portfolio a result of my Needs and requirements or Greed, Ignorance and Hearsay and emotional Buying? If that’s the case, take action !!!

This page contains all the “Term of the Day” posted on this blog earliar .

1. Short Selling

Short Selling : Short Selling refers selling of shares without owning them . If you short sell a stock , you first sell them at higher price and later you buy them (cover them) back at lower price .Lot of times you feel that markets will go down , at that time you short sell a stock . People who deal in Derivatives can either Sell the Futures or Buy PUT options . Short Selling can offer tremendous returns in short frame , because bear markets are markets fall with much speed and momentum compared to rising market . Read more

2. Derivatives

Derivatives : Derivatives are contracts whose value depend on value of some other thing. Examples are Futures and Options . Value of Stock is independent , But value of Futures or Options depend on the movement of Stock . Derivatives are dangerous Instrument and not recommended for Starters . In India People are attracted towards Derivatives because of its Return potential , but they underestimate its Risk potential and its ability to paralyse investor or trader financially , Better to learn first and then enter in Derivatives. Read more

3. P/E Ratio

P/E Ratio : P/E ratio is a reflection of the market’s opinion of the earnings capacity and future business prospects of a company. Companies which enjoy the confidence of investors and have a higher market standing usually command high P/E ratios. This ratio indicates the extent to which earnings of a share are covered by its price. If P/E is 5, it means that the price of a share is 5 times its earnings. In other words, the company’s EPSremaining constant, it will take you approximately five years through dividends plus capital appreciation to recover the cost of buying the share. The lower the P/E, lesser the time it will take for you to recover your investment. Its one of the most imortant Ratios you can look at .

Price/Earnings Ratio (P/E) = Price of the share / Earnings per share

4. ETF

ETF : ETFs are a basket of securities which tracks an underlying and are traded on a recognised stock exchange. Examples are Nifty Beas (this tracks Nifty) and Gold ETF’s (this tracks Gold prices) . Read More

Soon there will be Silver ETF’s in India .

5. FMP

FMP : FMP’s are close ended mutual funds , similar to FD’s but much more tax efficient and with marginally superior returns , but they have there own risks . The returns offered by FMP’s is indicative and not guaranteed. They come from 1 month maturity to 1 yrs maturity . In year 2008 , FMP have done very badly because of defaults . Read here for more

6. Technical Analysis

Technical Analysis : A method of evaluating securities by analyzing statistics generated by market activity, such as past prices and volume. Technical analysts do not attempt to measure a security’s intrinsic value, but instead use charts and other tools to identify patterns that can suggest future activity. It is generally used by people who want to take advantage of short term price movement. Technical Analysis can make you a better than average Investor

7 . Demat Account

Demat Account : Demat account is an account where shares are stored electronically . Just like Bank account deposits money , Demat account deposits your shares . Now a days , you cant hold shares in physical form , every share has to be in physical form . A person can only hold a single Demat account (trading account is different) .

8. Trading Account

Trading Account: Trading Account is an account through which you can buy and sell things on stock market . Dont confuse it with Demat account , Demat account is just a place of storage . Trading account is a platform which provides you a service of buying and selling things . You can have multiple trading accounts , which will all be connected with your single demat account .

9. Futures

Futures: Futures are the contract which gives you a right to buy or sell a specified commodity of standardized quality at a certain date in the future, at a market determined price . For Example, If you buy Reliance Futures for June series, you will get a right to buy specific number of Reliance shares at a fixed price on last Thursday of June . The future date is called the delivery date or final settlement date . Read more

10. NAV

NAV: NAV is a price of a mutual fund unit . You can see it just like a share price of company . Mutual funds invest the money in market and its tracked by NAV , if investments goes up , NAV goes up and vice versa . Generally NAV value starts with Rs 10 .

There is a myth among investors that low NAV mutual funds are better than high NAV mutual funds, which is totally wrong .