Are you clear about the tax-saving which you can do when you pay health insurance premiums every year? You will be glad to hear that it’s over and above sec 80C.

Yes, it comes under a separate section called section 80D!

What is section 80D?

Health Insurance policies have become very famous in the last 10 yrs and to encourage it, the govt gives tax benefit when you pay the premium for yourself, your family or your parents

Section 80D defines all the rules and limits related to health insurance premium payment and tax saving.

How much can you claim under section 80D?

One can claim a deduction of premium amount on health insurance of self + family (spouse + dependent children below 18 yrs.) and parents. If one pays a health insurance premium of his brother or sister then he/she will not be able to claim a tax deduction. To make it more clear, I have mentioned the list of people who will come under this benefit –

Self

Spouse

Dependent Children (below 18 yrs.)

Parents

How much you can claim Tax benefit u/s 80D?

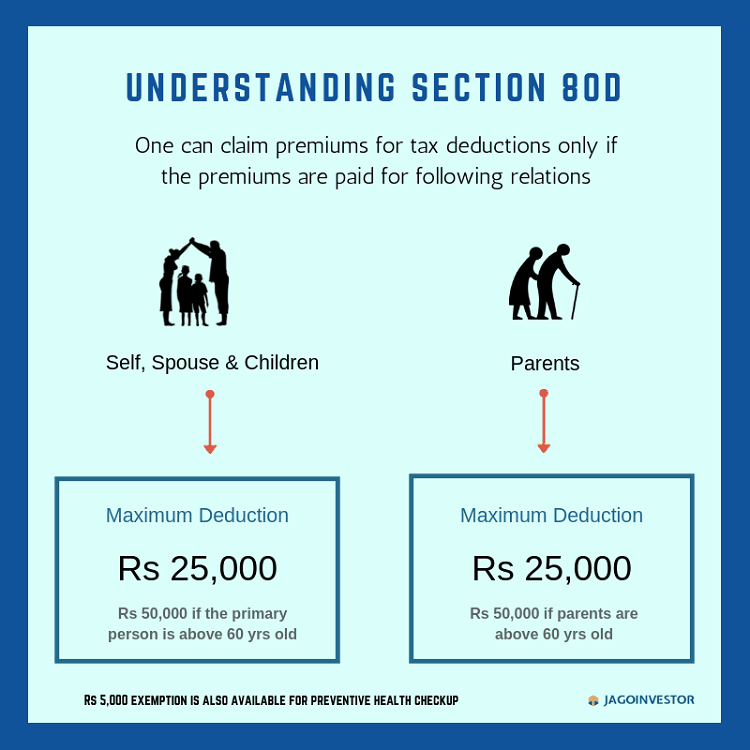

You can claim a maximum Rs. 25000 of the deduction for premium paid on health insurance of you, your spouse and children (under the age of 18 yrs.), if you are below 60 years

The same amount of Rs. 25000 you can claim for deduction of premium that you pay for your parents (father+mother).

And if the age of you or your parents is above 60 years then the limit will increase to Rs. 50,000/- in each case. In the above limits, exemption of Rs. 5000 for yearly health check is included.

For getting a clear understanding of the calculation part you can refer the info-graphic given below.

Let us now understand this through some examples –

Case 1 – Ram (35 yrs.) with a spouse and 1 kid + parents (mother 55 yrs. and father 57 yrs.)

In case 1, Ram pays a yearly premium of Rs 15000 (for self+spouse+1 kid) and Rs 34000 (both parents). So now let us see how much exemption Ram can claim u/s 8oD.

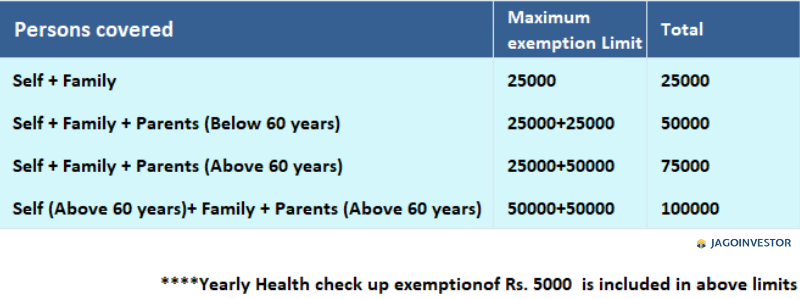

As self + family exemption limit is Rs 25000 and Parents exemption limit is Rs 25000. Then Ram can claim exemption of Rs 40,000 (15000 + 25000) u/s 80D.

Case 2 – Rakesh (48 yrs.) with a spouse and 2 kids + parents ( father 75 yrs.)

In case 2, Rakesh pays a yearly premium of Rs 32000 (for a self+spouse+2 kids), Rs 63000 (for father) and Rs 8000 (preventive medical check-up). So now let us see how much exemption Rakesh can claim u/s 80D.

As self + family exemption limit is Rs 25000 and parent (senior citizen) exemption limit is Rs 50,000. So, Rakesh can claim exemption of Rs 75,000 (25000 self + 50,000 parent). As Rakesh has already exhausted his self exemption limit so he won’t be able to claim his preventive medical check because preventive medical check is already included in the self exemption limit.

2 Benefits into 1

I think getting tax deductions on health insurance is a wonderful thing. Health Insurance in itself is a very important financial product most people should buy and you are also getting some tax benefits on it. So, do buy health insurance for yourself, your family and parents to protect your wealth and save tax.

Let us know your views in the comment section about this article.

I along with my teammate Sagar, recorded a 28 min video discussion related to this topic – “Should you buy 2nd house as an investment?” yesterday. We talked about various pros and cons which are often missed by those investors who are thinking of buying the second house for investment. Watch the video below

What we discussed in this video?

When does it makes sense to buy a 2nd house?

How does it impact your cashflows and stress level?

Why are investors so attached and attracted to buying “Real Estate”?

What are the real-life issues which investors face after buying the 2nd house?

Is it an emotional decision or a financial decision?

Why buying just 1 hour is enough for 95% of investors?

Why illiquidity is a big issue with buying a 2nd house?

How 2nd house can create a good second income, and in which cases?

Do let us know if you have any comments after watching the video!

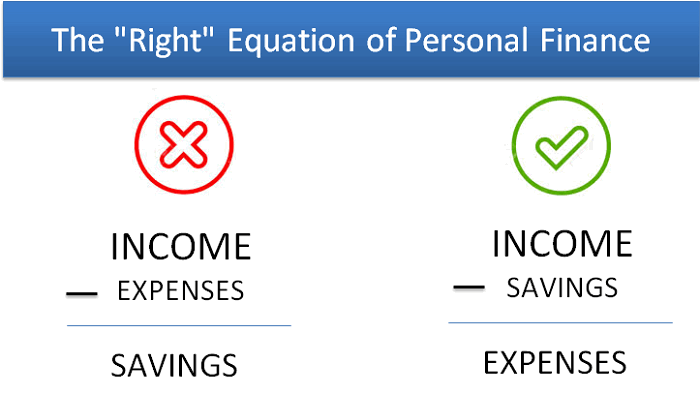

Today I want to talk about a mistake which we are all guilty of at some point of our life – “Keeping too much money in saving bank account”

I can understand how confident and great we feel when we know that we have a big amount in our savings bank account and if required we can just walk to the ATM and get the money within minutes. Nothing can beat that feeling !, however, there are some downsides to it too.

I want to talk about 2 problems (one small and one big) associated with keeping too much money in your bank account today.

You must be thinking, how can keeping money in my account be a problem? After all, more money into account is a good thing – RIGHT?

Let’s see

Problem #1 (small problem) – Negative Real Return

Let’s talk about the small issue first.

The money in your savings bank account earns a small interest of just 3.5% per year (in most of cases). Inflation is around 7-8% on average and if you consider that, you are actually earning a negative real return (real return = return – taxes – inflation).

So your purchasing power is only diminishing over time. What you can buy in the future is less than what you can buy today!. If the excess amount you keep in your saving account is very small, then you can dismiss what I said because the excess money in a way serves as your emergency fund, but when you keep big amounts, its an issue.

We recently saw the data of one of our client, and he was having 90 Lacs in his saving bank account from the last 4 yrs. He had sold his house because he wanted to purchase a new house, but then he did not finalize the new house for a long time and never invested that money for better returns. It just did not hit his mind! (not taking any action is so EASY)

So he earned just 3.5% on that 90 lacs for 4 yrs, which is around 13.2 lacs of interest (without considering taxes). If only he had put that in a liquid mutual fund or a fixed deposit, he would have earned 26.2 lacs as interest (without considering taxes again).

Which means that he said NO, to that potential extra 13 lacs by just leaving that big amount in his saving bank account.

Now in your case, the quantum of potential loss will be only to the extent of the money you have in your account.

A lot of us, don’t keep 90 lacs in saving bank account (do we even have that much networth?), but its not very uncommon, to see large amount like 3 lacs, or 8 lacs lying in saving bank for many months just because the investors does not calculate the potential loss, or is just lethargic of breaking the status quo (I think, this is the real issue)

What you can do to solve this issue?

The simple approach you can take is, that apart from 4-6 months of your monthly expenses, you can park rest of the money at least in short term debt mutual funds (earns around 8% per annum, with better taxation than a FD) and deploy the rest amount as per your financial goals in other avenues and let it go out of your bank account and your sight.

The 6 months’ worth of emergency fund can be broken into 2 parts, where you can keep one part in saving account and other parts into a liquid fund (earns 6.5-7% and available in 24 hours notice). This is a far better arrangement compared to just leaving all the money in saving bank account.

Problem #2 (Big problem) – That excess money gets SPENT unconsciously

I don’t see many people talking about this 2nd point often and its related to behavioral finance. This is a very big topic, which deserves a whole book, but I will try to cover it quickly here.

Money is like water, it finds its own direction, if you don’t give it one!

Our mind works in a very different manner when we have money lying in front of us. Supply creates its own demand is one of the principles of economics and very much applicable to money. If you have money in a savings account, you can be sure that your mind will come up with every possible reason to spend it.

So if money is lying around in your saving bank account, which can be easily accessed then,

Your TV will look old enough to you and your mind would like to upgrade it for a bigger one

That Amazon Cart will automatically have those unwanted items which you really don’t need (but you feel you need it)

You will feel that you can easily afford to give a bigger and fancier gift when you are invited to a marriage

Those swiggy / uber eats orders will never stop

The next vacation will feel within the reach somehow

The eating out will often happen

In short, your spendings will increase sub-consciously

The human mind is very interesting. You always feel that you are in control of your spendings, but research on this topic has shown that we humans are our own enemy. It’s extremely tough to be in control and think rationally about spending’s especially when you have the excess supply of money.

Your environment and which kind of situation you are in, mostly decides how you will behave and think, not rationally! (you need to exercise right? Did you wake up in the morning and go for the jog if that’s the rational thing to do?)

Let money go out of your bank account automatically each month

The beautiful thing about a recurring deposit or SIP is that it takes away a part of your money out of your sight and makes it tough for you to access it. It creates wealth for you because your manual intervention is not involved in it. You are not taking manual decision each month if you want to save it or not. I don’t claim that manual investing is superior or not, but it looks great on paper, but not in reality.

If you are struggling to save each month, I think 90% of the reason is that you might be trying to do it manually, thinking – “I will save something for sure if I am left with it at the end of the month” . Trust me it will not happen.

We have had clients, who tell us that they are surprised after 2-3 yrs when they accumulate so much wealth, which happened only because they started a SIP and nothing else changed in their life. It’s a structure that automatically helped them in their wealth creation. Its the battle half won when you want to create long term wealth for meeting your financial goals.

Paytm, Amazon Pay and Cashbacks!

Have you observed that the money you add in your paytm wallet, Amazon Pay or similar wallets gets spent without guilt and so fast. The moment you add it in Paytm or other wallets, you look at that money in a very different way. It’s now “available” for spending (that’s called mental accounting). Well, this is a topic in itself, but I wanted to just make a point that when money is not visible, you think about it totally differently.

Listen to the below podcast to learn more about behavioral finance (its an audio uploaded on youtube) which I did along with Siddhartha K Garg.

You become a bit careless with money and don’t think too much when you have Rs 2,34,965 in your bank account compared to say when you have Rs 12,500.

What you can do to solve this issue?

Here are a few things you can do.

Start your SIP / Recurring deposit 2-3 days after your salary date for your financial goals.

Keep minimal amount in your saving bank account (unless is needed in next few days).

Open a Liquid mutual fund folio, just to transfer the extra cash, and whenever you need it, you can redeem it and get the money in 24 hours

Don’t keep more than 6 months of expenses in your liquid mutual fund.

Try to use cash, if possible and add only small amounts in online wallets.

Artificially create the “Low account balance” especially, when your spouse or you yourself are a shopaholic

Do your financial goals planning and be aware of the future targets to achieve, it will help to know if you are lagging behind in reaching your financial goals

Try to forcefully lock your money in financial products just to win over your ‘lack of self-control’

These were two common problems with having too much money in saving bank account or by any other means. It’s always a great thing to let money get locked somewhere (only that part which is not needed for long term).

What are your views about his topic? Do you agree with what I said?

The Supreme Court has ruled that citizens of India do not have to link their aadhar number to a range of services such as bank account, mobile sim, digital wallet (paytm), passport, etc. However, the Supreme Court has said that biometric ID is mandatory for accessing social welfare schemes and subsidies such as, LPG subsidy, Jan Dhan Yojana, etc.

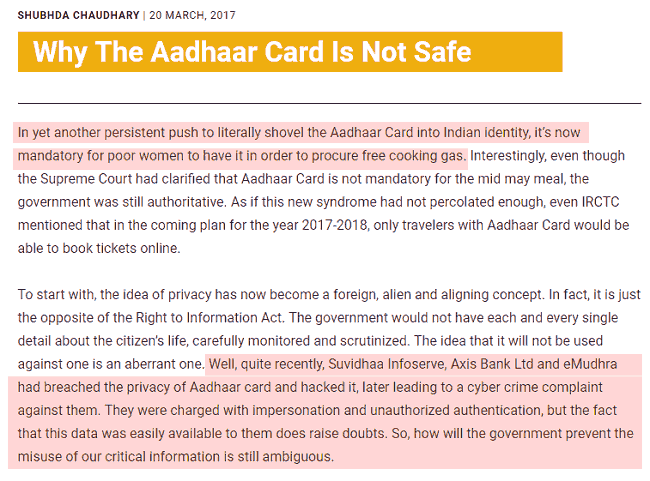

Last year a lot of stress was there for having an Aadhar card and urgently linking the aadhar to avail public and private sector services. That panic state in the country made us link our aadhar with a bank account, sim card, investments (KYC updation) and whatnot.

After all, there so many questions were raised on the basis of the Right to Privacy and Right to avail the basic services which should not be stopped on the question of not having aadhar card number.

There were so many news such as,

After all these, the verdict of Aadhar not mandatory has been passed.

So, now it is a good news for those you never had an aadhar and never got it linked with anything. However, for those who have linked the aadhar with their private accounts and are concern about their private information getting hacked, may delink the aadhar.

Process of Un-linking

Now, the question arises is it so easy to delink? Do I again need to stand in the queues at post office and banks for hours for delinking my aadhar? The answer is NO. Because, Aadhar delinking is optional and not mandatory. If you feel insure that your private information may get leaked than you should delink your aadhar number.

Below given are the processes of delinking aadhar from Post Offices, Bank, Digital Wallet, and Mobile operator.

1. How to unlink aadhar from Bank Account

Before proceeding to unlink Aadhaar from Bank, first, make sure that your Bank Account is not linked for any DBT (Direct Benefit Transfer). If you unlink the Aadhaar with the bank which is linked for DBT (like Gas subsidy), then you may not receive the DBT money in your account. Hence, try to unlink Aadhaar from bank cautiously. Following are the steps for delinking aadhar from bank.

Visit your branch

Ask customer service to give you Aadhaar De-Link Form.

Submit the de-link form

Within 48 hours your Aadhaar details will be de-linked from your bank account.

Cross-check after 48 hours whether it has been de-linked or not.

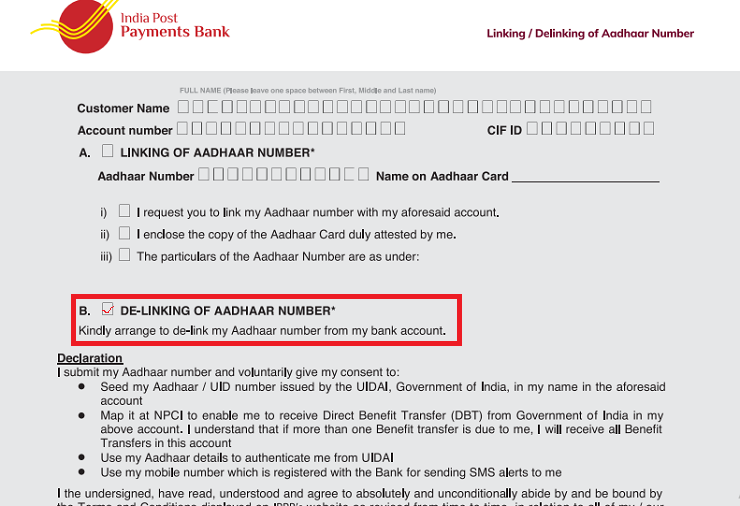

2. How to unlink aadhar from Post Office Account

For delinking aadhar card number from post office accounts, you just need to submit a form of delinking of Aadhar Number. This is how Indian post office payment bank de-link form looks like.

3. How to unlink aadhar from digital wallets such as Paytm, Mobikwik, Freecharge

Call the customer care and ask for the procedure to de-link.

You will receive an e-mail to attach a soft copy of your Aadhaar.

After sending the e-mail, you will receive a reply stating that within 72 hours (depends from company to company) your Aadhaar will be de-linked.

Cross check again after 72 hours with the customer care.

4.How to unlink aadhar from sim card companies such as jio, Vodafone, idea, etc.

Call the customer care and request for unlinking aadhar.

You may be asked to send an e-mail with a request to de-link your Aadhaar details.

Once you send it, then they will send you the confirmed message of unlinking Aadhaar.

There might be some difference in the process of delinking for every service provider. Because as of now there are no standard rules set up for delinking. So, you may directly contact the customer care of the service provider and they will guide you on the exact process.

Please feel free to comment on how fruitful this article was.

Buying a house isn’t easy today if you are living in a metro city like Mumbai, Pune, or Delhi. It’s nearly impossible to pay the full price of a house unless you have massive savings or an existing real estate that you can resell. This is the reason why most people take home loans, or rather joint home loans.

What is a Joint Home Loan?

As the name implies, a joint home loan is a home loan that you take with another person, who is usually your spouse or a sibling. There are many reasons why people avail of joint home loans instead of standard home loans, one of which is bad credit.

Let’s understand why.

No matter what kind of loan you apply for, the lenders always check your credit report to assess your creditworthiness. This a standard practice to reduce the risk of non-performing assets. So, if your credit report looks fine which means that you don’t have a history of late payments, loan defaults, etc. and your credit score is high, then you can avail a loan easily.

However, if that’s not the case, not all hope is lost as an alternative option exists! That’s when you can get a co-borrower to take a home loan with you. If their credit score is good, then it can balance yours and make it easier to get your loan approved.

People also take joint home loans when they aren’t capable of repaying the full amount on their own. By dividing the loan’s burden with their spouse or a family member through a joint home loan, the debt can be repaid easily. Now that you know what a joint home loan is, let’s take a look at some of the major pros and cons of the same.

Pros of Joint Home Loan

The chances of getting a home loan at attractive interest rates are much higher in a joint home loan compared to the regular home loan.

As per the income tax regulations, joint home loans allow both co-borrowers to claim tax benefits under Section 80C. They each can deduct up to 2 lakh INR from the interest amount and 1.5 lakh INR from the principal amount from their taxable incomes.

If you are unable to get a home loan due to poor credit score, then a joint home loan can be your best bet.

Cons of Joint Home Loan

If your co-borrower in unable or simply refuses to pay the EMIs, then your credit report apart from theirs is affected.

Joint home loans can raise all kinds of legal problems if the co-borrowers are married to each other and get separated by divorce even as home loan remains to be repaid. If the property is registered in the name of one co-borrower, then after the loan has been fully repaid, he/she will become the rightful owner even if the other co-borrower has also paid their share of the EMIs.

Common Myths About Joint Home Loans

A joint home loan is a massive financial obligation. Apart from the huge EMIs that are particular to these loans, the tenures are not lesser than 15 to 20 years which means you pay the EMIs for a large portion of your life. Thus, it’s a good idea to do extensive research before you finally start submitting applications for a joint loan.

It would help if you also were wary of some of the most common myths about joint home loans that mislead borrowers:

Myth #1: A Co-Applicant is Required Just for “Formality.”

A co-applicant is as much responsible for a loan’s repayment as the primary borrower. In other words, signing on the dotted line imposes legal and financial obligations which is why it’s strongly recommended that both co-applicants read the fine print and ask as many questions as they need until they have a good understanding of the agreement they are about to enter into.

Myth #2: Only One Co-Borrower Can Receive Tax Benefits

People think that in joint loans, only one of the co-borrowers can receive tax benefits. However, this is further from the truth as both co-borrowers are equally entitled to these benefits. This means that you and your co-borrower both get to enjoy lower individual taxable incomes. That said, you must know about Section 24 of the Income Tax Act which sheds light on taxation in joint loans.

As per Income Tax guidelines, a co-borrower can claim tax benefits only if he/she is also a joint owner of the property. This clarification is important because many times, people take joint loans to increase the loan amount and make the process easier. However, merely being a co-borrower doesn’t make you eligible for the tax benefits. You must have ownership rights over the property as well.

Myth #3: Roping in a Co-Applicant is a Sure Shot Way of Getting a Home Loan

It’s true that it’s easier to get a home loan with a co-applicant compared to when you apply just by yourself. However, there is no guarantee that you will get approved for a loan. This is because home loans are highly risky for the lenders, even if they are secured against the homes they are availed for.

So, a co-applicant can’t help with the application if they don’t contribute to your “creditworthiness”. In other words, a co-applicant can make it easier to get a home loan only if their credit score is high and their income big enough to cover the EMIs.

Failing to Prepare is Preparing to Fail!

Joint home loans have their pros and cons as explained above. However, there are many other factors that you must consider including the interest rates, income, financial projections for the future, and buying a new home vs. an old home. After all, once you borrow money from a bank, there is no turning back. So, take your time and pick the right loan at the right time. Good luck!

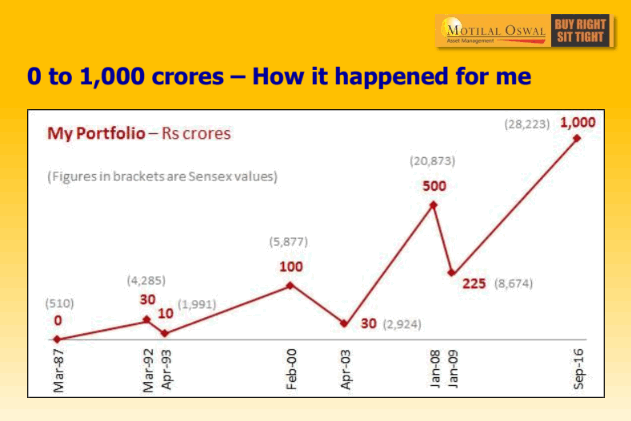

In the article, there are no tips and tricks on how to make 1,000 crores overnight. The article is about engaging with some powerful questions and not trying to find an immediate answer to create wealth.

The article is not about creating crores, it is about shifting your focus from markets to learning from the master investors- All I want is a shift in your mindset. Markets will continue to rock, your only job is to work on your mindset to create massive wealth.

How Investors should think when markets correct?

Right now a lot of investors, advisors and mutual fund companies are focusing only on the market volatility, Fall in NAV, portfolio return, some think markets are like a bloodbath, some are in the mood of stopping their SIP, some are in the mood of redeeming money, sharp corrections, on the other side mutual fund companies and advisors are asking investors to stay patient with their investments and encouraging them to invest more.

In short, some are positive and some are extremely negative about the situation we are into.

But……

There is very little focus on how master investors think when markets correct. There is very little focus on inspiring the wealth creation journey of master investors. There is very little focus on how successful or master investors behave and act during market turbulence. We all start from zero and it is important to think and observe winning or master investors as we continue to walk on our journey of wealth creation.

Wealth Creation Journey of Mr. Ramdeo Agarwal

In the personal finance world, I have many teachers, there are many master investors from whom I continue to learn and get inspiration from. I am always like Eklavya, who keeps learning from different teachers from a distance and I will always continue to learn and absorb the maximum I can.

Mr. Ramdeo Agarwal is the Co-founder of Motilal Oswal group of companies, his journey of wealth creation transformed after meeting his mentor Warren Buffet. I never miss to read his wealth creation studies and there is not a single YouTube video I have missed in which he has featured.

I got an opportunity to be in the same room with Mr. Ramdeo Agarwal Ji in the US, my friends took a picture with him but I did not. I was having thoughts like, let me first do something amazing in life, let me create immense wealth using equity as a vehicle, let me help others to get wealthy by educating them on equity investments.

I should perform as a student first and earn the privilege of sharing a photo with him.

The POWER Questions I engage with about my teacher ( Mr. Ramdeo Agarwal Ji) are?

How does he (Mr. Ramdeo Agarwal) create wealth?

How does he maintain his conviction in the equity market?

How he stays on the court, no matter where the markets are?

How does he build his business empire around equities?

How does he stay so consistent with his investments?

How does he deal with losses in his portfolio?

How does he feel when he makes huge profits?

How does he stay committed to the process of wealth creation?

How does he practice the power of compounding in his day to day life?

Initially, I was busy to get answers to the above questions but after hearing and reading about Mr. Ramdeo Agarwal and his style of investing I came to know that the real secret is not in getting the answers, the real secret is in staying engaged with the questions, it is about staying engaged with the journey of wealth creation. It is about having your own investment philosophy, it is about allowing the power of compounding to do its work.

It is about finding your own process of wealth creation and keep refining it. It is about doing something over and over and over and over again and if something does not work for you, you make changes in your process and continue to move forward in your journey of wealth creation.

Most newbie investors feel and think that master investors have something SPECIAL in them, they do something special to create wealth, they have some special knowledge or special skills. In reality, the only thing special about them is they do not look for ANYTHING special. They master consistency, repetition and stay focused on their path. They won’t allow any kind of outside noise to deviate them from their journey of wealth creation.

I invite you to read the pdf if you have read it before I invite you to read it once again. The PDF is old by now his personal net worth must have crossed a few more thousand crores. While you read to keep the above questions in front of you, do not look for special qualities or some special information from the pdf. From time to time we will continue to share other master investors from whom we can learn and inspire from.

Teacher and His Meditation Student:

Lastly, I want to leave you with a conversation, a student had with his meditation teacher.

A student went to his meditation teacher and said, “My meditation is horrible! I feel so distracted, or my legs ache, or I’m constantly falling asleep. It’s just horrible!”

“It will pass,” the teacher said matter-of-factly.

A week later, the student came back to his teacher. “My meditation is wonderful! I feel so aware, so peaceful, and so alive! It’s just wonderful!’

“It will pass,” the teacher replied matter-of-factly.

The market correction will pass away!

You have the power to create massive wealth

You really have the power to create massive wealth, almost everyone starts from zero or from a scratch and on one fine day they become an inspiration for others. Choose to be an inspiration to others, the article is not about Mr. Ramdeo Agarwal Ji, or how much money he has made.

It is about learning from the master investors and taking your financial journey to the next level. Create your financial journey more meaningful, stick to your mission of wealth creation and if that’s the game you will never bother where the markets are going. You will see every situation as an opportunity to create wealth.

(Check if you are capable to build Rs.1000 crore net-worth or not?)

Invitation to Check your Financial Health Score: During Diwali everyone gets HIT by the euphoria of shopping and buying new stuff, we invite you to check your financial Health score this Diwali, all you need to do is leave your details in the below link and my team will help you to check your financial Health score out of 100. After checking the score you will gain clarity on areas which are not working and areas which call for your immediate attention.

In the world of mutual funds, there are various kinds of categories for different requirements and risk appetite. One of the categories I want to talk about today is the “Balanced Advantage” Category.

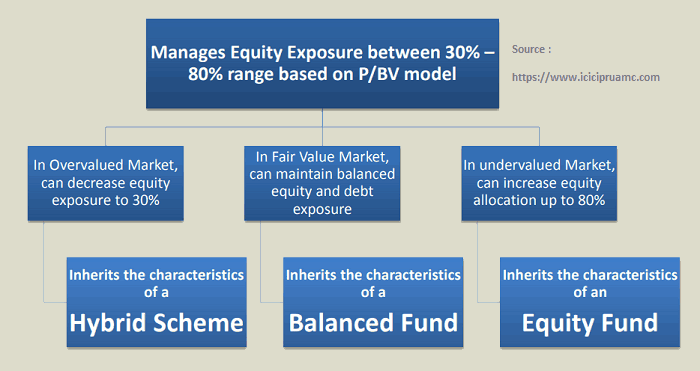

What are Balanced Advantage Mutual funds?

In one line, a balanced advantage fund dynamically shifts between equity and debt depending on the market valuations. What it means is that when the markets are over heated and high, the fund decreases its exposure to equity and move the money into debt, so that if the markets fall, the down side is protected.

This strategy significantly reduces the volatility of the fund compared to an equity fund and at the same time, the returns potential also comes down.

A lot of funds in this category also name their funds as “Dynamic Asset Allocation Fund” rather than “Balanced Advantage”

Some of the examples of the funds in this category are

ICICI Prudential Balanced Advantage Fund

Motilal Oswal Most Focused Dynamic Equity Fund

Aditya Birla Balanced Advanced Fund

Kotak Balanced Advantage Fund

Reliance Balanced Advantage Fund

HDFC Balanced Advantage Fund

How does a Balanced Advantage Mutual fund work?

A balanced advantage fund uses a predefined algorithm and based on Market PE or P/BV or some other internal indicator to determine if markets are on the higher side or lower side and then based on that they keep increasing or decreasing the equity exposure.

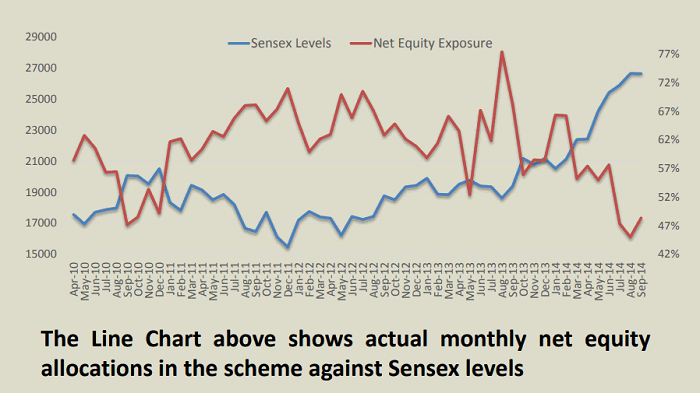

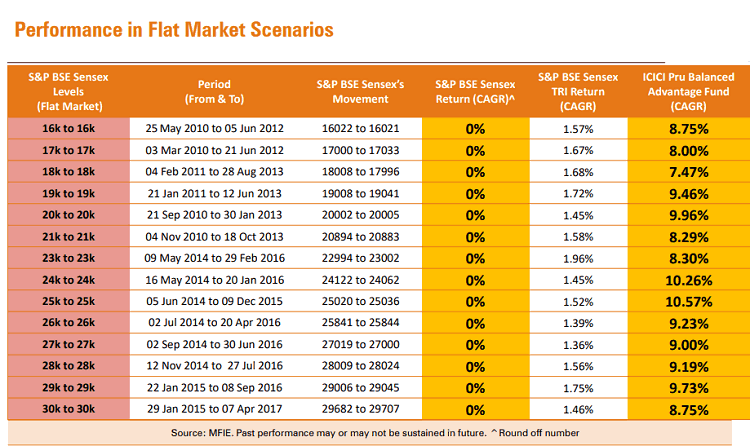

To explain you more about this, I will take an example of how the ICICI Prudential Balanced Advantage fund which was the first fund of this type in the mutual fund Industry and very successful in that category.

Disclaimer : I am taking the example of ICICI balanced mutual fund only because it’s the biggest in the category and quite old one in Industry and we have some data to show. It’s not a recommendation to buy. We have some equally good funds from other AMC’s also.

Below you can see how the equity exposure has changed over time from Apr 2010 – Sept 2014. You can see that equity exposure increases when Sensex levels go down and vice versa.

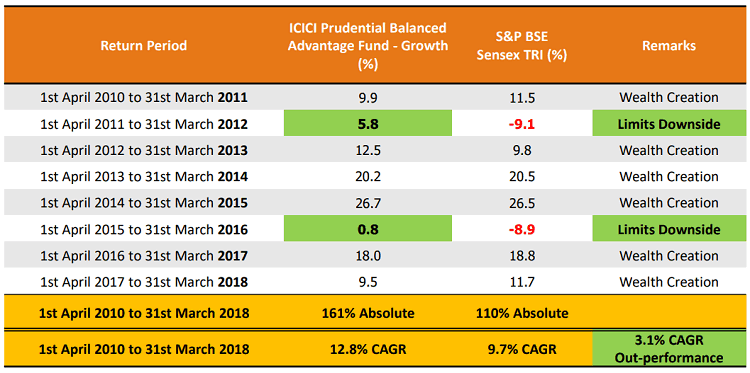

Limits downside and upside

The main benefit of Balanced Advantage funds is that it controls and extreme upside or downside. So you will not see very deep losses, but at the same time, you will also not see very high profits.

However, the balanced advantage funds will provide decent market returns (but not comparable to pure equity funds)

Even in the flat markets, you can see that the balanced advantage category has generated positive returns by taking advantage of the volatility.

Who should invest in Balanced Advantage (or Dynamic Asset Allocation) funds?

Now the big question is – Which kind of investors should invest in Balanced Advantage fund and When?

Who should invest?

It’s mainly for those investors whose focus is on reducing the risk, but at the same time enjoying better returns than Fixed Deposits. The fund value will still be volatile, but the intensity will not be as high as a pure equity fund. From Returns point, it will give decent return of 2-3% above FD returns, but that is all you should expect over a long term.

When to Invest?

As you have seen that the equity exposure is already controlled by the fund itself, you can actually invest anytime you want. There is no need to time the market, because the fund itself times the market internally. There are no issues if you want to put lump sum or SIP.

Who should not invest?

An investor who wants higher return potential and can take the higher volatility, should not be ideally investing in these funds. However, if you are unsure of the markets levels and want to play safe, you can invest lump sum in balanced advantage fund and then setup a STP (Systematic transfer plan) to an equity fund. This will reduce the risk to some extent.

Important: Don’t confuse this category of funds with “Balanced Funds”. Balanced Funds are those mutual funds that have a mix of equity and debt in their portfolio with equity exposure of around 65-70% and rest Debt.

A good choice for Retired Investors

I think these kinds of mutual funds are a very good choice for retired investors who want returns better than the fixed instruments and at the same time, can’t handle too much volatility in their portfolio. So some part of their portfolio can surely be invested in balanced advantage or dynamic asset allocation funds (same thing, but different name)

If you want to invest in balanced advantage mutual funds, you can contact the Jagoinvestor team to know the process and get a well-designed portfolio.

Let me know if you have any questions regarding this fund of a mutual fund? Was it clear enough?

We are happy to announce, that our next full-day workshop in Bangalore is scheduled for 16th Sept 2018 (Sunday).

We invite you to come and participate with your friends and family. It is an opportunity for you to block one full day for your financial life where you get a chance to work on your financial life. We do not teach tricks and tips to build wealth, but in fact we help you to discover your own personal process of creating wealth.

Why we do these kinds of offline event/workshops?

We do these events because they make a positive difference in people’s financial life. The conversations we do, create an impact on people’s thinking and they are able to re-invent themselves as an investor. The event is not about financial products and numbers, it is about learning and mastering the principles of wealth creation. It is about learning realizing your past mistakes and about creating a powerful future for yourself.

Register for Bangalore workshop on 16th Sept 2018 (SUNDAY)

Ticket Type

Pricing

Ticket Link

Single Ticket (Early Bird)

(First 10 tickets only)

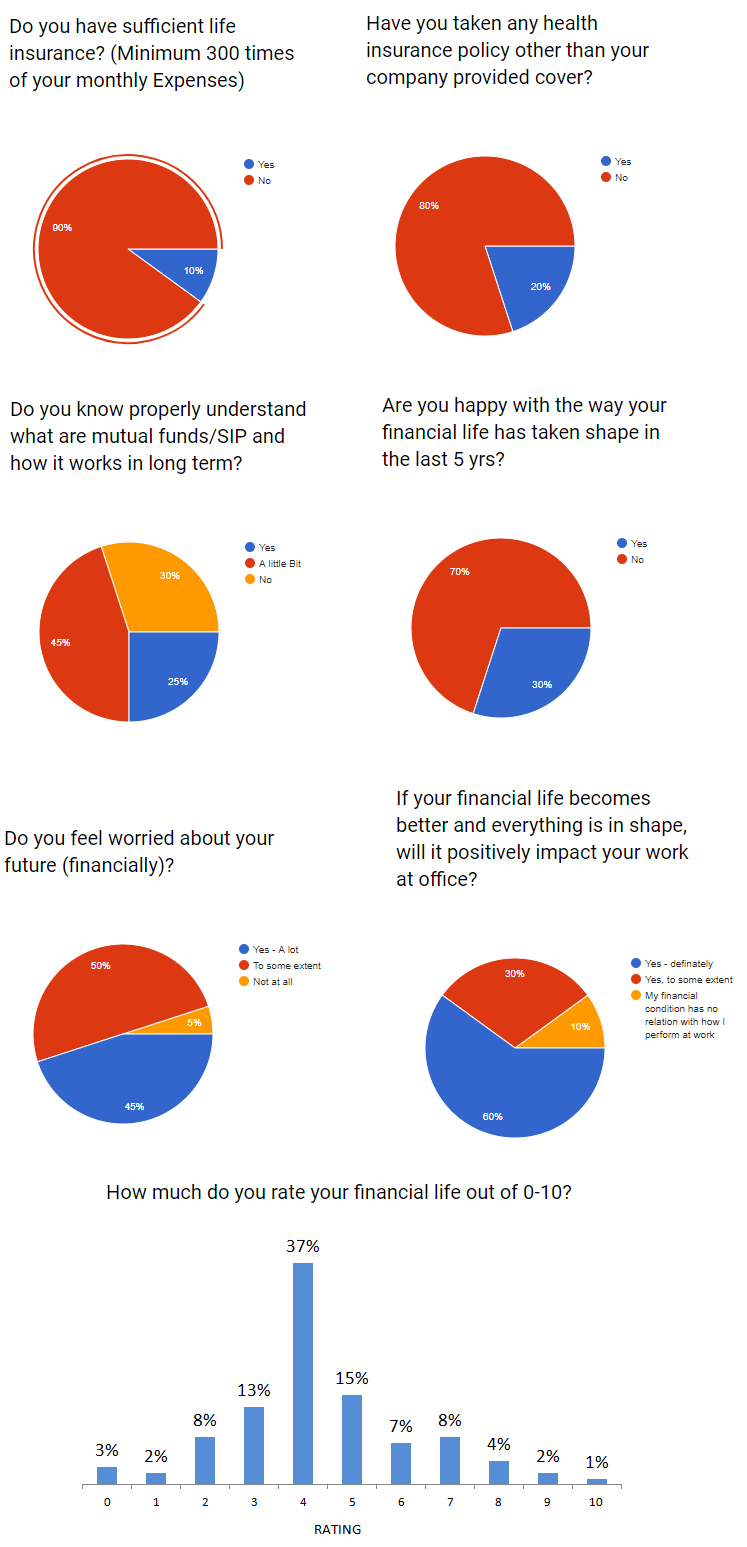

Let us share our survey findings (Survey was done on 10000+ Investors)

We did a survey with more than 10,000 investors some time back and here are the results of the survey.

The survey is LOUD and CLEAR – It’s time to re-invent

The theme of our workshop is going to be re-invention, you will get a chance to examine your financial life and will explore ways to re-invent your financial future.

The results from survey seem alarming and the best gift we can to the investor’s community is our workshop Your real wealth is your clear mind as once the mind is clear all the good decisions will happen on its own, the workshop will leave you with a clear mind and with new openings of action.

Our Vision to do Workshop in different cities and organizations

This year we intend to do the workshop in maximum cities and in more and more organizations. The content and design of workshop are powerful and we want the workshop conversation to touch more lives. If you want to do a workshop in your city or in your organization you can share your details in the below Google form, we will get in touch with you at the earliest.

It’s time to add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and each time it has been a very fulfilling experience for us. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation.

This time we want more and more couples to participate so that they can get on the same page when it comes to personal finance. It is extremely important that the husband and wife both take an equal interest when it comes to money management. We are offering a special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct is highly interactive, it has lots of activities and fun exercises which help you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short, there is something for everyone in this workshop.

If you have never participated in any personal finance workshop let this one be your first experience. If you have any questions you can write in the comments section or you can email on [email protected]

When you go for fill up petrol or diesel in your car/bike, you have an option to fill the normal fuel or high-performance fuel often termed as Speed, Power, Xtra mile, Turbojet or Hi-speed etc in the Indian Petrol pumps.

Today, I will share with you a kind of fraud/scam which is going on in petrol pumps on the name of these high-performance fuels and you will also learn if it’s really useful to use this high-cost version of petrol/diesel in your vehicle or not!

Because I educate you on the topic, I want to start with the cheating part first, which happens on the petrol pump!. The reason I am calling it a scam is because it is done with the intention of cheating the customer to make higher profits.

Petrol pumps give you “High-performance fuel” without asking you

Some days back I went to a petrol pump to fill petrol in my car. I kept my eyes wide open and made sure that the meter shows ZERO (read about zero meter scam on petrol pumps here), and no distraction is there and no one scams me.

As I was about to leave, I realized that the nozzle used to fill petrol was kept in the section which said “Speed”. When I enquired if they have filled the high-performance fuel in my car, the answer was YES.

When did I ask WHY? , they said that I should have mentioned that I wanted normal petrol.

So now you know the scam here..

Its common sense that by default petrol pumps should be giving us normal petrol and only if the customer wants/agrees, they should fill high performance/cost fuel. But here, they had made the costly fuel as the default choice and without even telling you they fill costly petrol/diesel in your car/bike.

A customer never pays much attention to which fuel was given to them and assumes that its normal/cheapest version of fuel.

There are many other scams which happen at petrol pumps, but I think is a much bigger scam, because this is so subtle, that almost everyone falls for it (without even knowing about it). Just think about it, even if 5% of people are scammed into buying high-performance fuels, it’s millions of litres and millions of extra revenue/profits for petrol pumps/companies.

What is High-performance fuel?

It’s very important to understand what exactly is high-performance petrol or diesel, to understand the whole game.

Branded high-performance fuels like SPEED and POWER are normal petrol with an extra additive/detergents added into it. These additives enhance theoOctane ratings for petrol.

The Octane rating is the petrol’s capacity to burn at higher compression ratios without knocking. Every engine has a unique compression rating and hence based on the compression rating, the manufacturers suggest the exact type of fuel to be used for the car.

99.99% cars/bikes in India have engines which only and only require normal petrol/diesel because its octane value is the same which is required by the engine of these cars.

In fact, you will be surprised to know that car manufacturer such as Maruti, Hyundai, Tata, Toyota, Ford, Skoda, Mercedes, BMW etc. strongly discourage the use of premium fuels in their cars and in fact its also written clearly in the car manual book too. This thread discusses everything about high octane and fuel performance if you want to learn about the topic.

If you also talk to qualified service engineers at the service stations, they also recommend using the normal fuel instead of these high performance versions.

Problems of using high performance fuel in normal car

Can you believe that use of high octane petrol (the costly high performance fuel) actually cause problems in the engine, instead of helping the engine?

If you use petrol which is having a higher octane level than what is recommended, then because of extra additives in the petrol, it is only going to cause unwanted settlement of these additives in the engine – no added benefits in terms of mileage/performance.

If you use petrol having lesser octane than recommended, the petrol will knock and cause damage to engine. Further, the anti-knock sensor will cause the engine to slow-down and the timing of the engine will be wrong causing decreased mileage.

The normal petrol which is available in the market is actually fit for the engines in most of the cars sold in India.

Some car owners have reported excessive exhaust smoke after using premium diesel. A few others have complained of damage to components in the fuel delivery system, including the fuel injection pump and fuel injectors. Modern common-rail diesel engines operate within fine tolerances.

Your motor was engineered to consume regular diesel only. In the worst case scenario, you might end up with damaged mechanicals due to premium diesel. In the best case, you won’t gain anything. With premium diesel, you have a lot to lose, and nothing to gain.

Video about High-Performance Fuel vs Normal fuel

I want to especially see this video by Mr Amit Khare of fame Ask Carguru Channel, which is an excellent source of all kind of information and knowledge about automobiles in India. A few months back, when I was watching this video, it was new learning for me and I decided that I will write an article about this soon on this blog.

The video is in Hindi and I am a fan of Mr Amit because of his simple language and engaging style of talking. Do listen to the following video for sure.

Why do petrol pumps sell high-performance fuel?

In one word – “High Profits”

Remember, that Petroleum companies and Petrol pumps both are “for-profit” businesses. They are there to make money and they will do all the things which increase their profitability. The petrol and diesel prices are regulated in India and no petroleum companies can decide the price of fuel on its own.

However, they can always decide the price of enhanced fuel because it’s their own formula and they are free to price it. Petrol pumps also get better margins when they sell high-performance fuels.

High-performance fuels can cost anywhere from 3-4% higher than normal fuels. In some cases, very high-performance fuels can be even 20% costly.

At the time of writing this article, the price of petrol/ltr in Mumbai was like this

Normal Petrol: ₹ 84.67

: ₹ 87.48

: ₹ 105.01

Which means that by selling high-performance fuels, the profits which these companies profit margins can literally shoot up by a big percentage. No wonder why they never share the secret.

When should you fill high-performance fuels in your car?

Very simple, if you have a car/bike which has a high-performance high-compression engine such as BMW / AUDI and superbike’s, then you can use those costly fuels and they will actually perform better also, but otherwise you should just stick to normal fuel only.

Do let us know if you liked this article and if it helped you to break your myth about high-performance fuels. Also if you have anything to add into this article, do let us know in the comments section.

A few days back, I was sitting with financial planning in our Pune Office and we did a very detailed discussion on his financial life. We looked at various parameters and did basic number-crunching which gave a deeper understanding to this client about financial status.

The first step was to record all his financial details in one place and that exercise alone took more than 40 min because it’s a task in itself to just bring all the financial details in one place.

For the next 2 hours, the husband and wife were totally into discussing some of the aspects of their financial life which they had never thought of or never dealt in detail. It was a wonderful experience in itself.

2000+ Families have gone through the process

My team has done this same exercise with more than 2,000 families to date across the world (Indian residents and NRI’s). Most of these discussions have happened online and few of them have happened face to face. But overall, what matters is the interest and dedication of the client and not the medium of communication.

While we were doing this exercise with the client, I thought that there are many things which are so common among the clients we deal with. I can see a lot of things which get repeated all the time and there is a pattern with the majority of the cases.

So I thought why not share some of common observations and I made a list of 10 points which is true for almost 80-90% of the clients we have dealt till now.

These 10 points will give you a good idea of how a typical financial planning case looks like and you can also check if these points are true for you or not.

Let me put these points now one by one.

1. No idea of their exact expenses

One thing which is most common is that most of the people do not have much idea of their own expenses and how much they are spending in different categories. Now you will feel – “How is it possible, that a person does not know their own expenses?”

The point is that most of the people have a very vague idea of how much they are spending on various categories because most of the people do not note down and follow a stringent budget. People have a high-level idea for everything, but once they put down all the numbers – They get surprised on their own expenses and feel like – “Ohh .. I spend so much!!, Never realized that”

2. The legacy of LIC policies

Almost everyone who comes to us for financial planning always has 2-3 LIC policies which were taken long back for tax saving purpose. If not for tax saving purposes, it was bought by their parents and they are now continuing it and paying the premium.

They have a high-level idea of the Sum Assured and when it’s maturing and hardly a few people recall the exact policy name.

3. People are Surprised

When we do the detailed analysis and show where they stand in their financial life (backed by data and proper reasoning), most of the people are surprised on how bad or how good they are doing.

Mostly we all are so consumed in our life that we never realize the status of our finances. We have a very fuzzy understanding if things are going bad or good.

Some of the people realize that they are worrying too much, where as they are well placed and are on right track (very few people are like that) and majority of people realize after meeting us that they have underestimated how bad they are in their financial life and its HIGH time they need to quickly take action.

4. Confused on how much they would need to retire today

When we discuss their retirement planning, almost everyone fails to reach a number which will be enough for them to retire today.

Just think about it.

If I ask you today that assume you retire today and you have to spend another 30-40 yrs of your life without any debt or EMI burden and no commitment like children related expenses. Assume you are 60 yr old today, and now need a big amount to live your life till you die, how much money would you need?

Just think about this for yourself and you will realize that it’s a tough question to answer. Will it be Rs 2 crore? 5 crore? 10 crore?

5. No clear Financial Goals in life

Most of the investors we see are mostly living in present and dealing with financial goals as and when they arrive. They know they would need “lots of money” in the future. But almost no one has properly planned for their financial goals.

One of the couples we met recently wanted to plan for their kid’s related goals. The wife was clear that the education was the biggest goal, but the husband was confused if they should also plan for the Marriage goal or not.

6. Decisions are taken based on “Instant Gratification”

We see that almost everyone has taken lots of decision-based on “instant gratification” or “the short term benefit” . Someone called from the bank and said they will save tax on a product, and they buy it.

The gold prices were rising and it “felt” right decision at that moment, so they bought lots of gold and not from the last 4 yrs gold has given a 0% return.

Like this, we see that decision is not carefully thought of with all pros and cons, but rather a very narrow approach.

7. “I could have done much much better” – The feeling of Regret

Every 1 out of 2 people we dealt with told us that they regret what they have done with their finances in the past and they wish if they could have done things differently.

More than doing “right things” , these people have done many “wrong things” and that has a higher impact (in a negative sense) in their financial lives.

8. The biggest part of Net worth is the House on loan

Almost always the house was the biggest part of the net worth, not the mutual funds, or stocks or fixed deposits .. I think it’s because we mostly deal with middle class or upper-middle-class salaried investors and the house is generally there in the portfolio.

Almost everyone had a big home loan.

9. Too many financial products

Another common issue which we see in most of the cases is that they have too many financial products. Many Fixed Deposits, many LIC policies, too many mutual funds (if any), various policies.

These people are more of product collectors who have added something new in their financial life each year when the tax season comes or whenever they had surplus money.

This is one reason that their financial lives get very complex.

10. Unable to meet Financial goals with current resources

When we check if these investors will be able to achieve their financial goals or not. We find that most of the people are not going to reach their goals easily .. and in some cases, they are seriously short of money and are in very bad shape.

It’s like a disaster waiting to happen. Investors are already in the age range of 40-45 yrs. They have some portfolio, but looking at their financial goals, it feels like they will be able to reach just 30-40% of it ..

: ₹ 87.48

: ₹ 87.48 : ₹ 105.01

: ₹ 105.01