Do you want to know how to save money to do what you love in life?

I recently did a 49 min audio podcast with Sanjay Khandelwal of The Break School. The podcast is mainly aimed at those who want to do something on their own by quitting their jobs, but they get stopped because of a lack of money & planning or fear of starting out. The podcast will also help those who want to know some of the best principles of savings and investing. Please listen to the podcast below

Here are the 11 things we discussed in the podcast?

Why did you start Jago Investor ( 02 min, 48 Sec)

Two biggest challenges in last 10 years in building Jago Investor ( 05 min, 43 Sec)

What have been your 3 biggest learning as a personal finance coach? ( 06 min, 54 Sec)

Have you come across people who wanted to quit their job and be freelancers or be on their own? What do you think holds them back?

Is it just money or something more? ( 10 min, 47 Sec)

What kind of habits makes people spend more and save less? ( 15 min, 11 Sec)

Do e-wallets increase our propensity to spend ( 21 min, 49 Sec)?

How can personal finance help? And how does it not help? ( 26 min, 11 Sec)

Can you share 3 to 4 financial concepts that layperson must be aware of? (30 min, 30 Sec)

How much money does one really need? (35 min, 33 Sec)Are there any misconceptions/Illusion that people have with respect to money? ( 39 min, 38 Sec)

Can you suggest a basic Financial Plan for someone who wants to quit her job in two years and start a blog? What are the things that the person must look at? ( 41 min, 05 Sec)

Please share what you think about the podcast after listening to it?

A total of 120 people voted on the question and I got the answer somewhere on the lines of what I have always believed in.

Are Happiness and Convenience the same?

A lot of people confuse “convenience” with “happiness” and hence believe that getting ultra-rich will make them very happy in life. They don’t realize that when they will get ultra-rich, they will be able to afford everything from nice house to amazing vacations, all the gadgets they want and fancy cars.

This all will make their life super easy and they will not be worrying about anything in life which can be bought with money.

But that’s not “happiness”, its “Convenience”

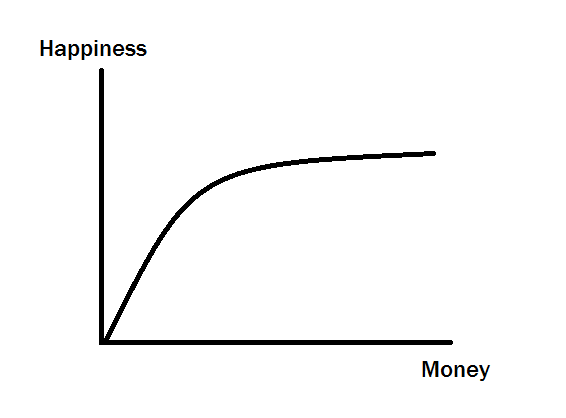

Money and Happiness

There are many books written on the topic of money and happiness and there is tons of research to conclude now that an increase in happiness you get out of having more and more money keeps diminishing over time.

So may be quite unhappy when you are poor because you are frustrated and have no idea where the next meal will come from.

Going from Rs 10,000 to Rs 1,00,000 (increase of 90,000) is very different than going from Rs 1,00,000 to 2,00,000.

Your life style will not drastically change if you earn 20 lacs a month instead of 6 lacs a month. But it surely is a big change from Rs 20,000 a month to 80,000 a month.

Out of 120 people who voted on my tweet, 76% people choose “more convenience” as their answer and only 12% choose “more happiness”. I am sure people who choose “more happiness” still need to see a good salary in life

I personally think that you surely need to aim to build great wealth and aim for huge income because more money will surely be better than less money in life. At least you have one less thing to worry in life and that is MONEY.

Around 12% people also voted for “more worries” as their answer. Money can also bring trouble in life at times, especially if you are not ready to share the fruits of wealth with others and if you have no idea how to extract happiness out of your money.

There are many examples on earth where people have done suicide and gone mad while their bank accounts had millions. Remember that unhappiness can come from various sources like relationships, health, how you feel about yourself, family issues and money.

What do you think about this topic?

Please share your thoughts about “What does more money give you in life?”.

Let me make it clear that above points are my personal thoughts about money and I accept that different people have a different experience in life which shapes their relationship with money. I would love to see how people think about this topic.

Jagoinvestor completed 10 yrs recently and it was a wonderful experience for these 10 yrs writing so many articles, working with thousands of investors.

While I was at my Ahmedabad office recently, I and my partner Nandish thought of an idea. We were discussing our kids (I have 1.5 yrs daughter and his son is 7 yrs old) and their future. We were wondering what kind of things we would like to teach our kids so that they can have a great financial life or life in general.

Here are those 10 lessons… Do listen to the whole talk

So we thought about why to keep things private and not share the 10 lessons we would like to pass on to our kids which can help them greatly when they start their own financial life many years in the future from now.

These 10 lessons are not those regular “start early” and “take your health insurance” kind of points. We are talking about some solid lessons which are going to impact your life overall. It’s more of a RICH mindset vs Average Mindset lessons.

Here are the topics we discussed in the video:

[su_table responsive=”yes” alternate=”no”]

1) Future is an Illusion

2) Target Financial Freedom in 10 yrs

3) Speak the language of NETWORTH

4) Focus on your Health

5) Be Coachable

6) Always think in terms of Milestones

7) Look at life in sum-total

8) Slow down to Speed up

9) Be a student of Life

10) Always tell the Truth

11) Don’t Listen to Your Inner Voice (Bonus lesson)

[/su_table]

Incase you have any thing to add to these 10 points, we would love to listen about your thoughts in the comments section.

We owe our success and whatever we have achieved to all our readers, our teams and our teachers.

Here is a 1-hour deep discussion on the topic of Retirement Planning and how India is set to have a massive problem in the coming times (and it’s still going on).

In this video, I talk with Mr. PV Subramanyam (also called as Subra) who is a retirement expert and has also authored a best selling book called “Retire Rich – Invest Rs 40 a day”

What is covered in this video talk?

Here are the discussions which are part of this 60 min talk.

What is Retirement (it’s not what you think)?

Investors attitude towards retirement

Retirement Time Bomb – The future of India

Job Opportunities which can be created if Govt address Retirement issue

Top mistakes investors do in their retirement planning

Where to invest for your Retirement?

Why retirement planning has become famous these days

How “bad retirement” puts the burden on children

A quick and simple way of estimating your retirement corpus

Early Retirement – What it means and is it possible?

Suggestions for someone who is already late for retirement!

It was a fun-filled talk I did in Pune, and I plan to do more of these talks with various other people in Industry. So keep a watch on it.

Do subscribe to our youtube channel, if you don’t want to miss out on the upcoming videos. Do let us know what you feel about the video and also share your views about retirement planning.

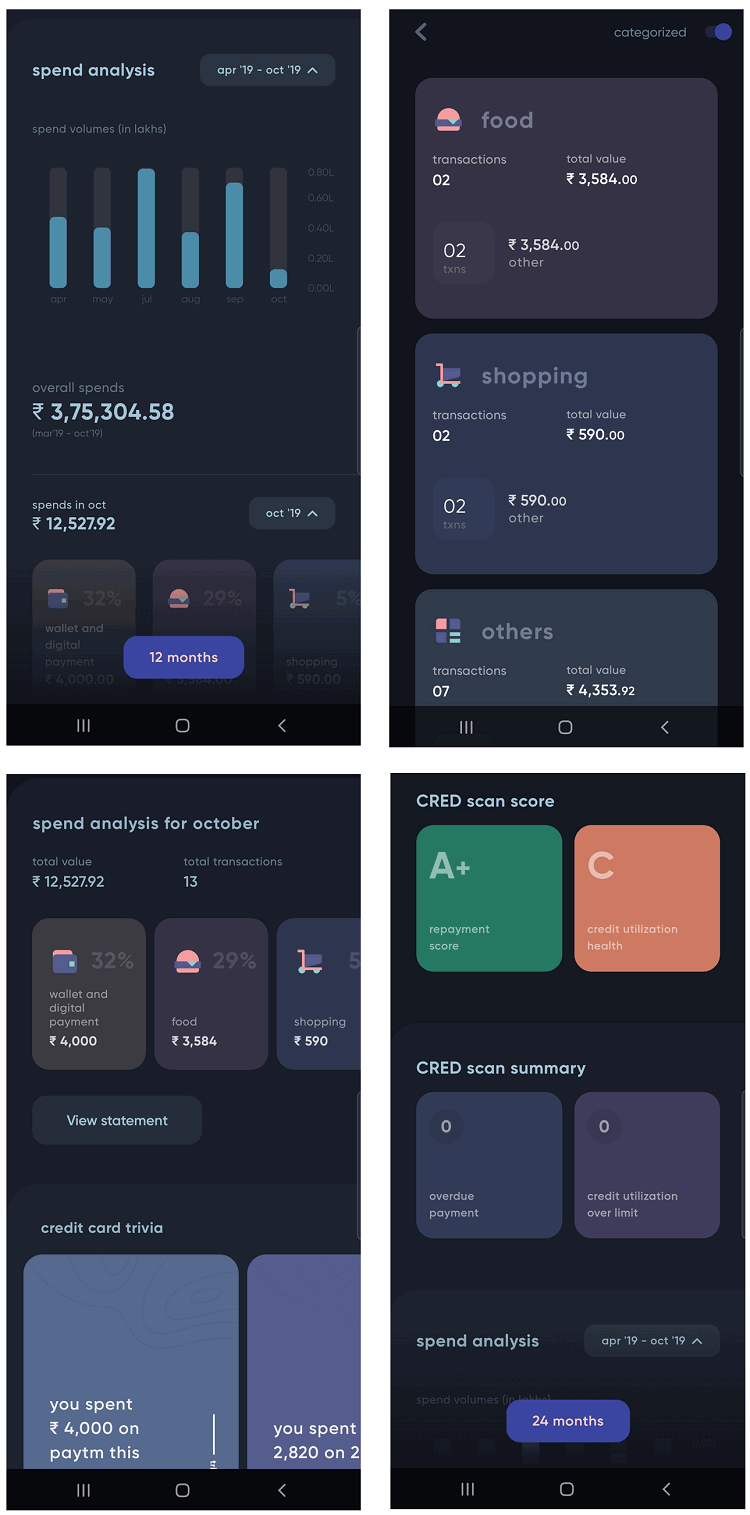

Today I want to do the review of the CRED app. I have been using it for the last 12 months already.

CRED is an app, which gives you rewards on timely payments of your credit card payment. If you are not using this app, you may be making credit card payments anyways by other online methods. All you have to do is to make payments using the CRED app, that’s all.

It’s that simple to use!

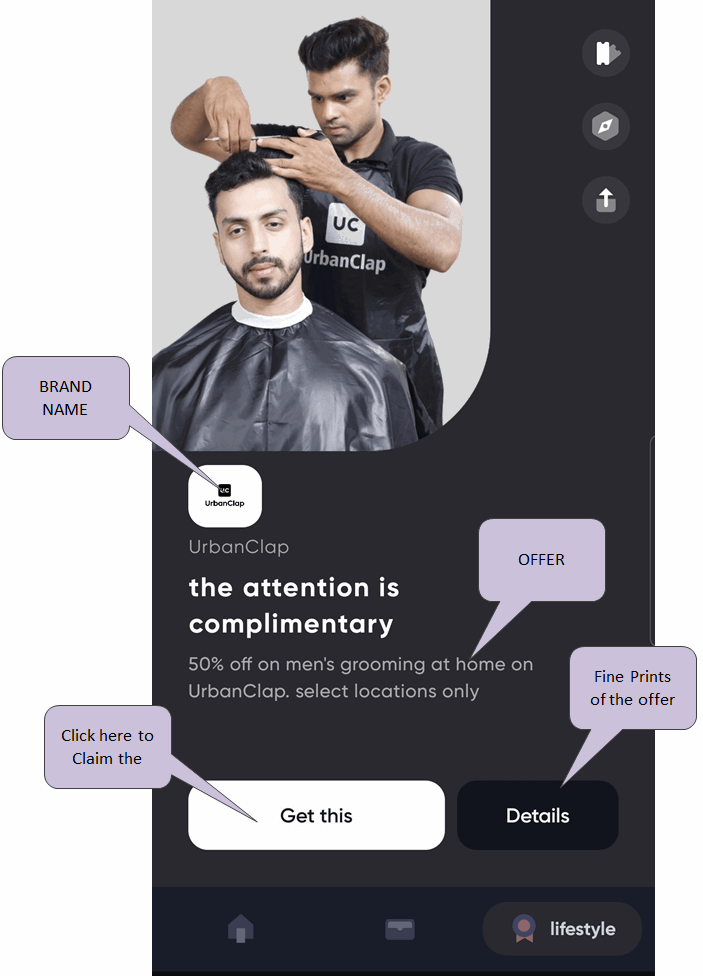

There are various brand offers and coupons from categories like dining out, food delivery apps, flight tickets, and even shopping? Here is one instance.

We get different kinds of rewards for using or raising the credit card bill amount. Like, in my case, I have a PVR credit card of Kotak bank, for every Rs. 15,000 credit card bill, I get points to redeem against 2 PVR tickets (max. Rs. 400 for 1 ticket). Because of this, I get influenced to pay my bills mostly by credit card to reach Rs.15,000 of a bill every month.

Here is how an offer looks like

This is how banks influence us to use a credit cards. But, when we pay bills of credit cards we never get any discount or reward on that amount?

However, now it is possible with the help of the CRED app. This app gives you rewards for paying your credit card dues via this app.

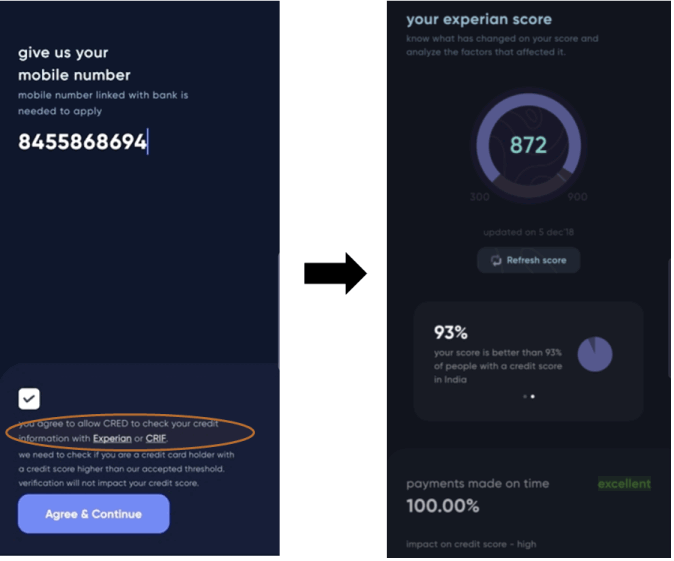

What is CRED App?

CRED is an app on which you add your multiple credit cards and make payments by the app itself, which gets credited to your bank in few hours. The app is exclusively for those people who have a good credit score (checked automatically from Experian or CRIF) and have some history of credit card payment. This is checked when you register for the app for the first time.

It is also equipped with the cred to protect feature which is an AI (Artificial Intelligence) backed system, that keeps track of every single nuance of a credit card payment journey – right from due date reminders, spending patterns and other card usage statistics.

There are two things you can earn on CRED App

Coins – You will earn coins equivalent to your credit card bill amount every time you pay the credit card bill. So if you pay the credit card bill of Rs 40,000, you will get 40,000 coins. The coins will keep accumulating month after month. So you can keep collecting coins and later redeem it in any manner. There are some offers and benefits which requires a very large amount of coins, so it’s beneficial to collect lots of coins. I currently have around 3,50,000+ coins in my own account.

Gems – You can also earn “gems” in the CRED app. These are different kinds of currency that are required by some offers. Right now one earns 10 gems on each referral. So if your referral signs up on the CRED app, then you will earn 10 gems. If you like Jagoinvestor, please help us earn some coins by registering on the CRED app using this link.

Here is a sample of some of the offers on the CRED app

iXigo flight bookings – Rs. 1000 off on using 5,000 coins

Flo Mattress – Rs. 5,000 off on using 20,000 coins

Swiggy – Free delivery for 3 months on using 5000 coins

UrbanClap – Flat 50% off on man grooming using 25000 coins

Flea Bazaar cafe – Flat 20% off on total bill using 5000 coins

Cashback – Get Rs 1,000 cashback for 30 gems

Flipkart – Rs 500 gift card for 20 gems

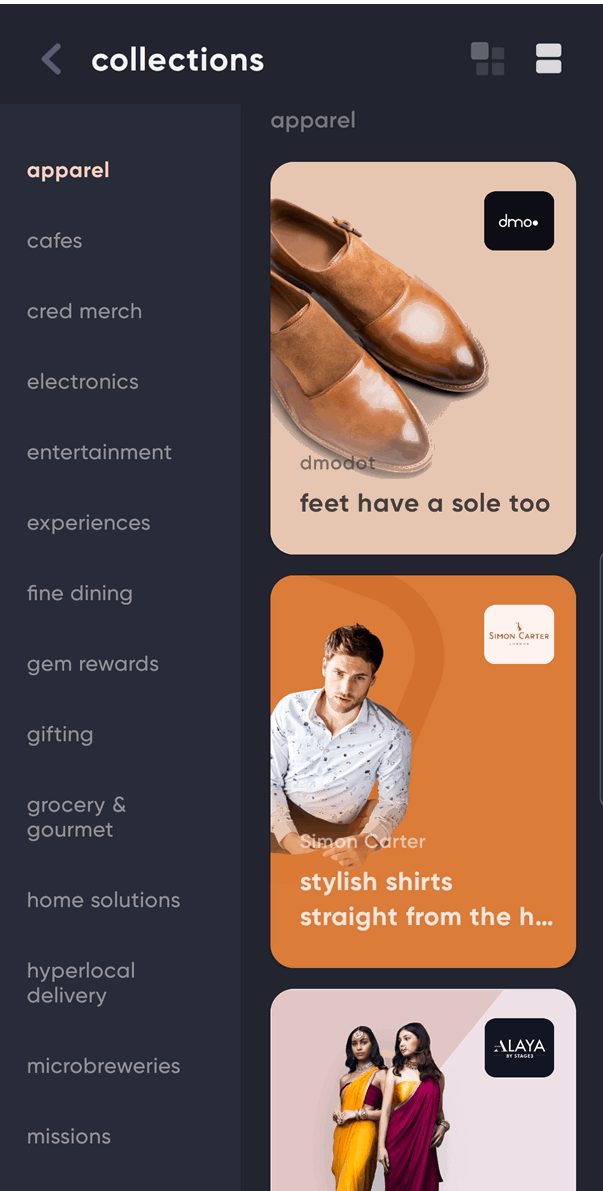

There are various kinds of coupons and offers available under the CRED app under different categories. Depending on what offer you want, you can go into that category and explore the offers available in your city.

3 steps to register for CRED App

You can avail of the benefits of this app only if you meet the eligibility criteria defined by the app. Which is – to have a good credit score. Following is the step-by-step process for this –

Login to cred using your name and phone number registered with a credit card.

The app will prompt you to grant permission for phone access to verify the number and SMS (which is needed to send a reminder on your due credit card bills), just grant the permissions.

Cred will process this data and check your eligibility, on the basis of your credit history. Cred has a tie-up with credit bureaus like Experian and CRIF.

If your credit score meets the standards of cred then you will receive an OTP to proceed further

If your membership is rejected, improve your credit score and apply after a few months again. It may also happen that you are using multiple mobile numbers for banking, so try again using another number. So, if you have just got your credit card some weeks back, please wait for a couple of months before you apply.

Step 3 –Add your credit cards

Once registration is successful on the CRED app home page all your Credit Cards would be displayed. You just need to verify these cards by entering the last 4 digits of the card. To ensure the active status of these cards, cred will instantly deposit Rs. 1 to each of the cards.

You will not be asked to enter an expiry date or CVV of your cards which ensures the safety of this app.

Once successfully getting your card verified, you can exclusively earn rewards and scratch cards on every bill payment. Master card, American Express, Diners Club, and VISA cards are presently being handled by the CRED app.

5 benefits you get in the CRED app

Coming to the main point of getting rewards and benefits from the CRED app, below are the following things

Cashbacks on paying bills

Discounts

Free gifts and offers

Spending Analysis

Credit Score tracking

Let’s look at each of them

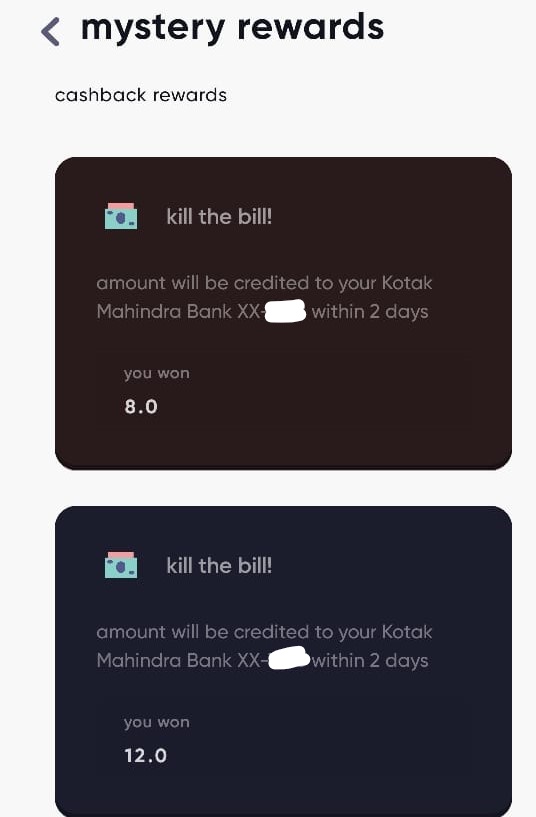

Benefit #1 – Cashback on paying bills

You may earn cash back (all called #killthebill) on every transaction. At the time of payment of more than Rs. 1000, you may be notified that you have won a scratch card and you might earn some amount which will be credited back to your credit card.

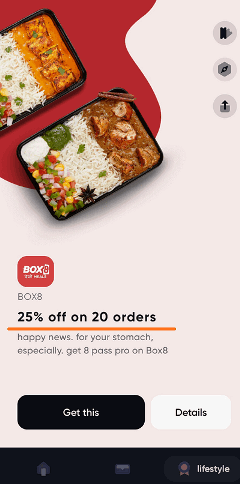

Benefit #2 – Discount Offers

Now, this is the major part of the benefits. CRED app has associated with various brands and it offers you some discount (cash discount or percentage discount) when spending a particular amount.

For example one of the offers is a “20% discount on the next 20 orders from BOX8”, so you can see that you will get 20% on the Box8 for a long time, but you still have to pay the rest amount. So even if you are getting a discount, you need to SPEND on it. So these discount offers are truly good only when you are anyways going to spend money on these brands.

Sometimes, it may happen that these offers also give you a chance to experience things which you might not have done without a discount, so technically it’s beneficial in that manner, but still, spending has to be done.

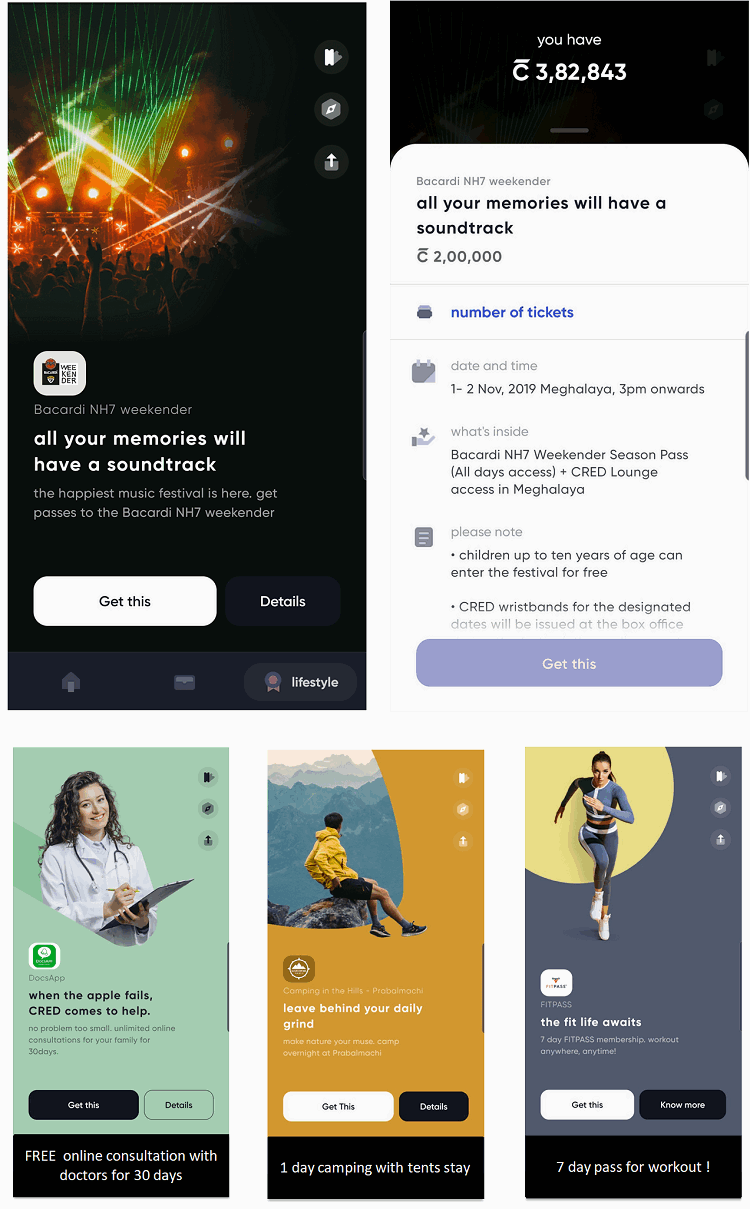

Benefit #3 – Free Gifts and benefits

There are some rewards that are truly free for you by burning some coins or gems. You don’t have to pay anything to get the benefits. These I personally think are the real benefits in a way, because you are not spending anything out of pocket, but just availing an offer.

Below you can see an example, where you can burn 2,00,000 coins and get a pass for 2 people Bacardi NH7 weekender event and even lounge access. Apart from that, I have shown 3 more offers for complimentary benefits without paying any extra from your own pocket.

So you can keep collecting the coins and wait for the right offer or reward to arrive which is useful for you.

Benefit #4 – Spending Analysis

One small benefit of the CRED app is that you get some insights into your spending pattern and the history of your credit card payments in one single place. This is good for those who have multiple credit cards and want some visibility on how their spending is happening.

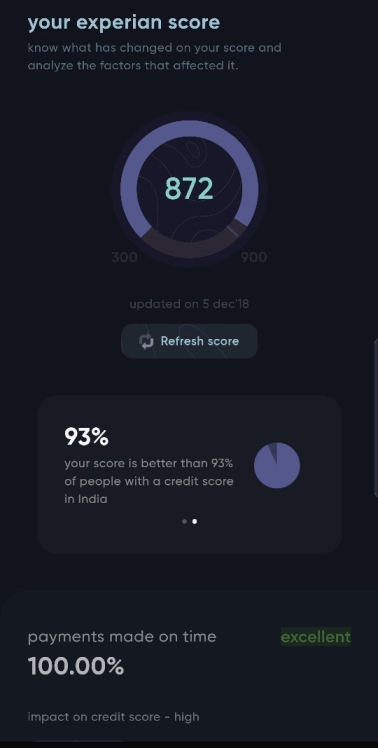

Benefit #5 – Credit Score Tracking

CRED app will keep showing your credit score from time to time, so this will help you to stay motivated to make timely credit card payments and you can also keep a track of how your credit score is moving over time. Right now CRED has done a tie-up with Experian and CRIF and pulls your credit score from both places.

How to make payment in the Cred app?

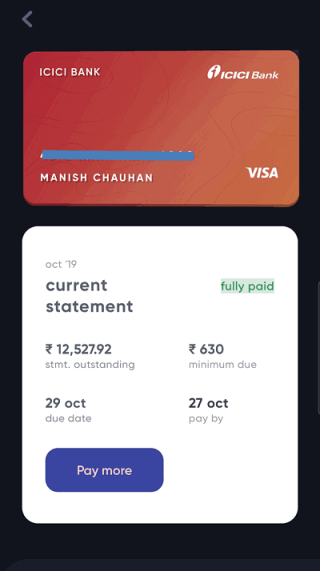

Paying credit card bills via the CRED app is very easy, just click on pay now, enter the amount and click proceed. Nowadays the bill amount along with the minimum due amount automatically gets pre-populated. You can make payment via debit card/net banking (NEFT/IMPS) or UPI. It may take some time to reflect on the money credited to your credit card account.

On Completion of Bill Payment of your Credit Card, you will be rewarded with CRED Coins and Kill Bill Scratch Card which you will have to redeem.

Is the CRED app safe?

I am sure that you must be having this question about the safety of this app because you are putting your credit card details and authorizing the app with all details.

First, this is this app is founded by Kunal Shah, the person who started Freecharge and the startup is heavily funded. The past record of the founder is intact so you can trust the company.

Next point is that the CRED app never asks you to provide the date of expiry or CVV on your credit cards, hence you are not giving any critical information to this app.

Then, you should know that when you install any other app, those apps also get various permissions like reading your SMS, making calls on your behalf, tracking your activity etc, and this app is nothing different from others.

If you want, you can deny access to emails and messages then you won’t be able to receive a notification on due dates and also you won’t get any expense analysis.

Nothing is FREE in this world

While it feels great to get great offers and benefits and freebies, remember that nothing is FREE in this world. Behind everything which looks amazing, there is a business model and the reason why you get those free rewards and offers.

You should be aware that CRED or any other coupon company does various tie-ups and associations with brands and companies and acts as a lead generation company. You are nothing but a lead to some other company and CRED is helping in growing sales for the other party.

They will mostly get something back in return and that’s the business model. Nothing wrong with it, but you as an investor should be aware of what you are getting into.

The discounts and awesome benefits you get from CRED or any other similar app are basically tempting you to spend on the pretext of a “great deal”. If you spend on something which you originally did not intend to buy then it’s an extra expense for you at the end of the day. The coupons are pure rewards only when you were anyways going to spend on something and if you get an additional discount on the deal.

So, we need to be conscious while spending and getting discounts by using CRED coins, it should not happen that you are spending on some unwanted stuff to just redeem Cred coins.

Let’s take my example, I attended two live concerts in Pune, VIP pass of Rs. 5,000 each. No doubt I just paid Rs. 4,000 (Rs. 2,000 each) instead of paying Rs. 10,000. But, if this reward would not be in the pictures so, I would have never gone to that concert and saved Rs. 4,000.

Are you one of the NRI’s who wants to know if you should invest your money in India and how to do it? Then this article is a good place to start with.

There are close to 3 crores NRI’s and PIO from India in different parts of the world, however, this post is mainly for those NRI investors who go out of India for 2-10 yrs and will mostly return back after few years of work.

Generally, there is a perception that NRI’s make a lot of money outside India as they are paid in Dollars and Dirhams! While this is true in general, one can’t deny that their expenses are also high and their life out of India is challenging as it’s a different city, culture, and environment overall.

NRI’s earn well, spend well and in most cases also “save” a decent amount of money every month. Even if one some is saving $2,000 in USA it’s close to 1.5 lacs a month after all. So the first challenge is to “save” money while you are NRI and the second one is to invest it properly and manage it well, especially if you are have limited time in your hands as an NRI.

What a person can save in India in 5 yrs, many NRIs can do that in just 1 yr – which means that if an NRI plans well – he/she can do financially very well in 8-10 yrs and come back to India semi-retired or fully retired.

In this article, we are just going to do some conversation regarding the various options available to NRI’s for investments and why they should choose India for their investment purpose. I will not cover too many technical rules or aspects related to investments in this article and will keep it quite too the point.

Which bank account to use – NRE or NRO?

A lot of NRI’s keep using their saving bank account for many years, without realizing that it’s illegal. The moment you become an NRI, one needs to convert their savings bank account to NRE or an NRO account. Or one can open a new NRE/NRO account if needed.

NRE account is a bank account where the money is full repatriable – which means that you will be able to take out all the money back from the NRE account and use it in a country where you are residing. It’s an account where you can deposit both your foreign and Indian income.

On the other hand, the NRO bank account is only partially repatriable and you can only deposit your Indian income in this account.

So depending on your situation and income type, you need to open these accounts. One can have any number of NRE/NRO accounts if required. There are too many aspects you need to consider between NRE / NRO account, which is explained in the table below

[su_table responsive=”yes”]

Comparison

NRE Account

NRO Account

Income can be Deposited

Foreign earnings and Indian Earnings

Only Indian Earnings

Meaning

Tax-Free

Taxable

Repatriability

Fully Repatriable

Partial (interest fully and principle within set limits)

Joint Account

Can be opened by 2 NRI’s

Can be opened by an NRI along with another resident or NRI’s

Deposits and Withdrawals

Can deposit in foreign currency, and withdraw in Indian currency

Can deposit in foreign as well as Indian currency, and withdraw in Indian currency

Should you be investing your money in the country where you are residing or in India? Does it make sense to earn and stay in the US or the Middle East, but invest all that money in India? Many NRIs are confused about this, so I will just give you 4 small points which you should be aware about.

Reason #1 – India is one the fastest growing and a stable Economy

Note that India is one of the fastest major economy and quite a stable country compared to many others where NRI’s live. It’s important to make sure that your money is invested in the country which is stable enough. On top of that, you also help in growing the foreign exchange of your country.

Reason #2 – High-Interest Rates

Compared to many developed economies, the interest rates or “returns” you can get in India is quite good. Japan has negative interest rates and the US has not more than 2-3%. Many NRI investors make the mistake of keeping too much money in the bank accounts outside India and earn very little interest rates.

Reason #3 – Because you understand the investments in India

There is a high probability that you already understand various Indian investments options and financial products. Also, you will never fear what happens to your money because there is a sense of familiarity with India’s markets and financial ecosystem.

Reason #4 – Mostly you will be back to India

A vast majority of NRIs return back to India after working for a few years outside and finally use all their investments back in India. That’s one strong reason why you should invest a major part of your money in India itself.

I don’t mean to say that no investment products outside India are better than Indian financial products. There will surely be options which can be looked at, please do that in case you feel you want to.

What options do NRI have for investments in India

Quickly, let’s see what various options are where NRI’s can put their money for short – long term. This is not a guide which will give you very detailed information, but a quick commentary of what the option is all about.

#1 – Bank NRE Deposits

Bank NRE deposits are one of the wonderful choices an NRI can make. The interest you earn on NRE deposits is tax-free and it’s a simple product that gives you decent risk-free returns. You can choose the NRE deposits for some part of your investments if you don’t want to complicate things and are investing for less than 5 yrs.

Many NRIs take a loan from the local banks at low-interest rates and invest in NRE deposits and earn the margin. See if this is a profitable thing to do in your case of not.

#2 – Real Estate

One the hot favorite for NRIs is real estate in India. Real estate investments require big-ticket investments and many NRI’s have that. Even if you are buying a flat or land on installments, it works well for NRI’s are they have a big disposable income per month. One of my close friends also invested in the Hiranandani project in Bangalore by making a down payment because they knew that the installments to be paid will be easy on the pocket with NRI income.

The only negative side is that many NRIs choose real estate just based on the limited information sitting outside India or in a hurried manner. So make sure you take your time in researching the property and take decisions slowly. As it’s a high ticket transaction, its highly recommended to hire a real estate lawyer, pay them fees and get all the work done like title search, property inquiry. If needed go with a real estate broker who can manage everything for you!.

One more thing NRI should know is that they are allowed to only buy residential or commercial real estate, but not agricultural properties.

#3 – Insurance Policies

There are many Insurance policies (which are actually investment polices) that are marketed well for NRIs. These, in my opinion, are to be carefully chosen as many traditional products can turn out to be dud investments and a very bad choice of long term investments. Some ULIP’s in the market have got reintroduced with lower charges and much better structure – so please choose them after a lot of studies and only for the long term.

I would strictly advise against traditional investment option which does not have exposure to equity in them because they are not better than normal NRE deposits.

NRI’s can and should buy the pure insurance policy (term insurance) if they require it.

#4 – Direct Equity

Direct equity is a good choice for NRI investors, provided they know the equity game and are able to pick the right stocks with proper research (either on their own or on someone’s advice). Make sure you do not over diversify your stock portfolio, because with too much money you may go on a shopping spree, which will make your portfolio very complex and with bad stocks.

If you want to do equity and want to take high risk, you can also look at PMS. If you want help in PMS, our team can help you out with that. Note that in order to invest in equity, an NRI needs a PIS permission (portfolio investment scheme). These are generally done by your broker or trading account provider and you don’t have to worry about it.

#5 – Mutual Funds

Mutual funds are quite hot these days among NRI’s and it surely is one of the best choices for investments, provided you have proper guidance about it.

In Mutual funds, you have two choices – Equity mutual funds and Debt Mutual funds.

Equity mutual funds are long term financial products that can deliver extremely good returns if managed well. Those who are ok with volatility in their portfolio and want very tax optimized inflation-beating returns for their long term goals, for those NRI’s mutual funds are a very good choice.

Even Debt mutual funds are a very good choice for those NRI’s who do not want to get into equity risk and want alternatives to bank deposits and bonds. Debt mutual funds are quite a good option even taxation wise if you are ready to invest for more than 3 yrs.

[su_table responsive=”yes” alternate=”no”]

Taxation

Equity Mutual funds

Debt Mutual funds

Short Term Capital Gain (STCG) (Before 1 yr)

Taxable @ 15%

Taxable as per Income tax slab rate

Long Term Capital Gain (LTCG) (After 1 yr)

Taxable @ 10% where LTCG>1 lakh (No indexation benefit)

Taxable @ 10% without indexation or 20% with indexation

[/su_table]

NRI’s from USA and Canada can also invest in mutual funds, but only with some limited mutual fund houses due to FATCA compliance. Here is a detailed guide on NRI’s investments in mutual funds

We at Jagoinvestor manage more than 140 NRI families’ investments in mutual funds. If you want to explore what we have to offer, please do let us know by clicking here and schedule a phone call with us.

#6 – Bonds and NCD

NRI’s can also invest in various bonds and NCD’s which are issued from time to time. These instruments have fixed interest which you can get every year credited in a bank account and you get your principle on maturity. The liquidity has to be compromised in these instruments as getting out of these before maturity becomes very tough even if these are tradable in the secondary market.

#7 – PPF

PPF is a choice for those NRI investors who already had it opened while they were in India because an NRI can’t open a fresh PPF account. Also, PPF is going to be a limited time product as one can’t be extended beyond 15 yrs.

#8 – NPS

NPS is another choice for your long term investments if one wants equity exposure in their portfolio, and pension benefits embedded into the product itself. Only NRI’s who are Indian citizens can invest in NPS. PIO and OCI are not eligible for opening the NPS account. In NPS, you get choices between equity investments, govt securities, and other fixed-income instruments.

Note that in NPS your savings get locked in till your retirement and only after that you get a part in a lump sum and rest is used for a pension. So choose NPS if you are very clear that your retirement is going to be in India.

KYC compliance and taxation For NRI’s

Note that once you become an NRI, there are lots of compliance which has to be followed by you. There are limits on where you can invest and where you can’t? Even the taxation for NRI’s is different and rules regarding TDS are different. We are not going into detail in this article regarding this as its out of scope.

How to avoid double taxation for NRI investments?

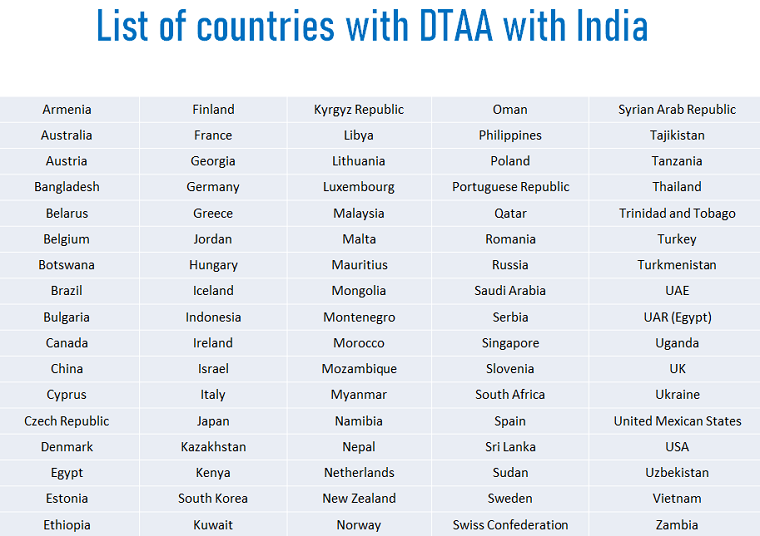

A lot of countries have DTAA agreements (double taxation avoidance agreement with India. In the case of NRIs – one can avoid paying double taxes in country of residence and India due to these agreements. You can get an equivalent deduction if DTAA exists between both countries.

Let me give you an example – In USA, a person has to pay the income tax on global income, so if an NRI has Rs 1 crore of FD in India they will pay the tax in India as well as in USA, but because of DTAA they will be avoiding it. There is paper work involved here, but you can surely save the double taxes.

When should an NRI invest outside India?

While India is a great place to invest for NRI’s overall, there may be certain life situations and some cases where investing in the country where you are working may be a good idea. There may be certain countries that might also be offering similar or better interest rates and returns compared to India. However, makes sure you consider the safety and return of your capital while you are investing along with tax to be paid.

Do let us know if you have any more questions related to NRI’s investments in India? Share your questions in the comments section.

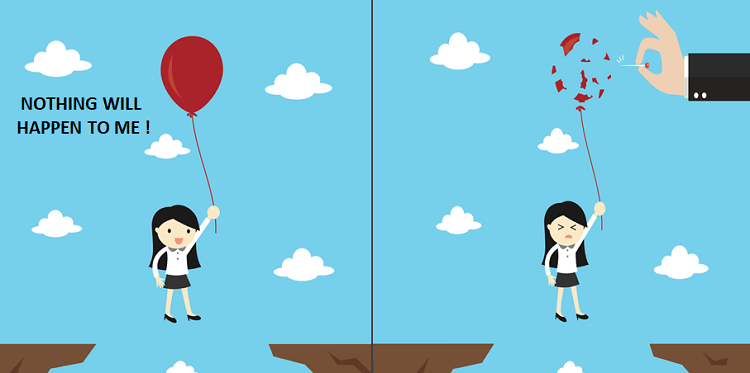

There are many investors who do not buy (or delay) term insurance plan, because they feel that nothing will happen to them.

Some feel they can’t die due to illness, because they take care of their health.

Some feel they will never die in an accident, because they drive their vehicles carefully.

Some feel they will never die, because they eat healthy.

Some feel they will not die because they keep an eye around them for all the risks.

I don’t know why people feel that they are “special” and bad things happen in only other’s life.

Do you think that those people who die suddenly because of some reason, were not confident that it will not happen to them in unexpected manner? “Accidents” are called accidents because they are unplanned and out of your control. So thinking that nothing will happen to you accidently itself is technically wrong thinking.

No one plans their death or any major accident. Life is so uncertain and external risks are so huge that statistically a certain percentage of people will die a sudden death due to various reasons.

That’s the sad truth of life.

Let me tell you two real life incidents where someone I knew personally died in an unexpected manner!

20 years back, we got a sad news one day that one of our relative died while taking bath. How? He suffered sudden brain hemorrhage and died. He was lying down on floor, when family broke the door. Do you think the guy in question ever thought that this can happen to him?

6 yrs back, someone I knew personally died because he got sucked into a daldal (mud puddle). He never realized that he is getting there as he was moving casually into that region and in no time he was stuck. He was there for taking a picture of his wife from distance & he got sucked in slowly while he was crying for help. Who can imagine or guess if something like that can ever happen?

At some point in our life, we all get casual and do things which have high risk. If we don’t do it, someone around us does not which can impact us. As humans, we have tendency to terribly under estimate the bad things which can happen to us. We feel that “accidents” and “unlucky incidents” happens in other lives.

If you really want to know how unexpected life can be, then I want you to watch out this following youtube video (just few seconds) before I start this article

https://www.youtube.com/watch?v=BxGBf6XsAio

Emotional and Financial Impact on Family

Death is not an issue for the person who dies because that person does not exist later to face the consequences. It’s the dependents, who face the heat – emotionally and financially.

Emotional suffering however huge, finally fades away over time slowly. Over years, life gets back on track. However financial impact is huge on the family, if a sufficient life insurance was not taken by the bread winner. Financial impact also completely changes the lives of family members and creates big issues.

It can leave the family with questions like

How will we pay back the home loan?

Will we have to sell the house?

How will we send children to school?

Who will give us money for many years?

Will we have to sell house belongings?

Will our children have to start working after their school?

How will we take care of old parents?

Who will earn now in family?

Think about this!

I have seen lots of investors not taking the decision of buying life insurance very seriously. They delay the decision, cut down on the sum assured feeling what’s the need to “waste” the premium and worst of all, close an existing term plan because now they feel “Nothing happened in last 6 yrs, I wasted so much of premium” ..

And then the most unexpected incidents happen ! … Sudden death due to a health issue or accident!

Rains in Pune in last 2 days

From last week, Pune is witnessing heavy rains and two days back there was an overflow in a lake within city which literally created havoc in one part of the city. One of the society wall fell and 5 people died because of that. I wonder if these 5 people ever wondered if they will die like this?

One guy was returning late in night in his car when this over flow happened and while he was going through a tunnel, the water from the other side came because of the overflow (like you must have seen in a scene from titanic). The car got washed away and after few hours, the guy death body was recovered. He did not even get time to react and do anything as his seat belt was on and he could not do much in response of that terrible accident.

Imagine this guy, and ask yourself if he had ever thought that this could have happened to him?

We need to accept that shit happens! . Many things are beyond our control. We can only minimize the impact or risk, but can never eliminate it.

7 real life incidents which will lower your over-confidence !

Here is a small compilation of few real life incidents, where people have died because of various unexpected reasons which was beyond their control almost all the time. Please imagine yourself and ask if by any chance, it’s possible that you could have been at their place?

Pune man saw wife disappear in flooded stream (Link)

We all were trying to get out of the house when suddenly the heavy flow of water came and in that Jyotsana was washed away right in front of my eyes. I could not get hold of her or save her; afterwards, we found her body nearby.”

7 school children die in Kenya as school building collapses (link)

“We were in class reading and we heard pupils and teachers screaming, and the class started collapsing and then a stone hit me on the mouth,” 10-year-old survivor Tracy Oduor told the AP. “When we got out of the gate, we heard that pupils were dead. I feel so sad.”

Spine surgeon & driver killed in accident on Mumbai-Pune Expressway (Link)

The car had stopped on the roadside to get a punctured tyre changed. When the driver was changing the tyre of the car a speeding private bus coming from Mumbai rammed into the driver and Dr Khurjekar, killing them on the spot.

A person died while taking selfie with elephant (Link)

A 30-year-old man was trampled to death by an elephant at the Bannerghatta Biological Park on Tuesday, after he and his friends sneaked into the park to take selfies with the elephant.

14 dead, several injured in massive fire at Mumbai’s Kamala Mills (Link)

The fire broke out shortly after midnight on the third floor of the four-storied building on Senapati Bapat Marg. The majority of those killed were women attending a birthday party at a rooftop restaurant.

Illegal banner claims another life, 23-year-old dies after hoarding falls on her (Link)

An illegal banner which was installed by an AIADMK functionary for a family function fell on Subhashree, making her fall to the road. Meanwhile, a lorry which right behind her on the road ran over her.

28-yr-old engineer dies after sharp kite string slits his throat in Delhi (Link)

A 28-year-old civil engineer was killed and at least half a dozen others, including a retired defence forces officer, were injured after being allegedly hit by sharp kite strings (manjha) in separate incidents during Independence Day and Raksha Bandhan celebrations on Thursday.

Please take Life Insurance

So the point is clear!

In case your family members are financially dependent on you, and you do not have sufficient assets with you, please buy sufficient life insurance (only a term plan) as soon as possible and secure their future. Do not over estimate your ability to avoid accidents. You have far less control over these things than you think.

If you are confused on which term plan to buy, I can help you along with my team. We will connect you to right platform to buy the term plan which will also give your family claim support in future. Just email us at [email protected] and we will get back to you!

Do share any incident or real life story related to this topic in comments section below.

“How much money would it take for you to feel “Rich”?”

I recently came across this interesting question on my Facebook timeline and the answers given by people were very interesting. I thought of sharing it with you all and discuss this insightful and interesting point with you all.

I want to become RICH and I am sure even you want to become one. We all have different definition of “being rich”.

Below are some of the unique and interesting answers which were given on the question – ““How much money would it take for you to feel “Rich”?

Read these answers carefully and it will tell you a lot on what is a person’s belief system about money and wealth. Here they are !

My dad gave me 200 rupees when I was going to work for the first time back in 2005, I’m rich till I have 200 bucks in my pocket

Once I have no loan

All the money my boss has

When I own my private jet..

Money can’t buy Richness… It has to be in your nature..

Fifty thousand a month

As long as it pays the Bill and afford my material needs and few luxury to some extent

10 crore per month

Answer depends upon ones needs or greed

Fill 10 x10 x10 room with 1000 doller note

1 crore per month

only my husband, He with me I feel rich

One roti with dal fry

Only mother and father nothing else no money required

1 Rs. more than Bill gates

At least 1 lakh to spend per month. No taxes either.

Modiji hain na… we all will be rich very soon!

Just a safe place giving shelter to me in any condition with a bowl of rice to eat with chickens from the farm and a cigarette to smoke before switching off to bed

So much money that I could feed all the people on earth who have no food n clothes n no shelter… I want that much money..

Had Fun?

I am sure you must have enjoyed reading various answers mentioned above. While they all look fun and crazy answers, deep down they are telling how these people see money and what is their relationship with money.

The answers tells us something about them as a person and how they see MONEY in their life. Based on the answers, I can see 3 ways people think about “Feeling Rich”

Category #1 – Attached to an absolute numbers

People who have given answers like “10 crore per month” and “Once I have no loan” are thinking purely from a absolute number in mind. They are currently having some particular income or net worth, and they feel that once they reach a new height called Y, it would be a great situation to be in. They will then feel “RICH”

This kind of belief system builds when one is looking at money as a tool to acquire things in life. You know you need some particular amount of money to buy a house, go on a vacation, buy a car and meet your day to day expenses, and you look at a number which is surely enough to buy those things. I feel this is a very natural definition of “RICH” and most of the people start this way!

Category #2 – Comparing with Others

There are investors who feel rich not at absolute level, but in comparison with others in society. So answers like 1 Rs. more than Bill gates” and “All the money my boss has” tells that the person mainly wants to have more than someone else. Its not about his requirement or desires, but how he/she feels in contrasts with others.

I think this is quite dangerous, because there will always be someone wealthier and happier than you and even if you have enough resources in life, you may feel miserable looking at others. Surely not something I would recommend.

Category #3 – Not giving money any importance

There are some answers like “Money can’t buy Richness… It has to be in your nature..” and “only my husband, He with me I feel rich” and even “Only mother and father nothing else no money required”

I personally have mixed reaction to these kind of answers. At one level, It feel great and really good that a person places more importance to relationships, values and memories. Money is a human created thing and there is really no limit to greed. Its good that a person givens answers which shows their detachment with money and shows that their happiness is not entirely dependent on money.

However, now at a different level, these answers also look to me a little unthoughtful. Money is surely a reality in life. I am not saying that you acquire obscene amount of money, but people around you (if not you) want to live a convenient and decent lifestyle. Just saying that “No money is required to feel rich” is not everyone’s cup of tea.

You might be a person who don’t need money to he happy and feel rich, but what about your spouse, your kids and your parents? Do they also feel that way?

A common man who has to pay rent, pay school fees of children, put ration in home and do all sort of real life expenses. One can’t deny the fact that money is required in life for most of the things.

So keep a balance between both the things. Every thing has a role in life. Money is not important, but important in life and its quite easy to make these statements when you have enough food at home and your future is sort of taken care.

Can there be a 4th Category?

I am not sure if there can be other categories or not. I was not able to think beyond 3 categories myself. Can you think of more?

Btw – Can you answer me (and to yourself) the same question – “How much money would it take for you to feel Rich?”

Can you share your answer in the comments section?

On 4th of May 2019, I (Nandish Desai) got an opportunity to attend the Annual General Meet of Berkshire Hathway, hosted by Warren Buffet and Charlie Munger (I also attended the AGM last year)

As a student of wealth, it was a great learning experience for me and I would like to share my learning and insights with all of you. I will not get into companies he named or into the numbers or statistics; I want to keep it simple so that you can pick a few insights for your personal growth.

Here are some of the pictures from the AGM meet.

Background of AGM

Every 4th of May in the city called Omaha warren buffet holds the Annual General meet of his company Berkshire Hathway. It is a global event where more than 30-40 k people travel from all over the world to attend the same. It is more like a celebration where people come to hear his view and to learn from his school of thought. Currently, one single stock of Berkshire Hathway is approximately around 3,00,000 USD ( or maybe more)

9 Lessons learned from the sharing of Warren Buffet

I am putting 9 points I learned from Warren Buffet which I made out of what he spoke in the AGM.

#1 – On Happiness: This one was an eye-opener for me. Most of us equate money with Happiness whereas Buffet made a point, happiness is not a place to reach rather it is a place to come from or operate from. If you are not happy with your current net-worth you won’t be happy by adding a few more lakh or crore to your net worth. He is asking us to focus on things that make us happy in the right now moment.

#2 – On Workability: The bold statement made for investors was very profound, “ All you need is to do is figure out what works and just do it”. Every investor has to discover his or her own process of investing. During the journey keep your eye on what is working for you. For example, in the area of health if going to the gym is working then go to the gym every day, and if yoga fits in your schedule then do yoga regularly. The focus is on bringing workability and staying engaged with the sport called wealth creation. There can be various ways to build wealth, you need to figure out what works for you.

#3 – On Building Competencies: Warren insisted on building and expanding one’s personal competencies. He insisted on investing in one’s own self more than anything else. The future belongs to masters and not to incompetent individuals. He also gave some examples of professionals you will never approach just because you doubt their competency level. You can do your own SWOT Analysis, find your strengths, weaknesses and it will help you to explore newer opportunities and will help you to eliminate weaknesses.

#4 – On Human Behavior: There are many books written on warren buffet and his investment style, however, he insists on reading people more than books. The real insights about human behavior can only be learned when you sit with someone and have a deeper conversation. Every human being is like a book filled with experiences and he invites everyone to spend more time with other beings.

#5 – On Investments: Price has the power to make or break any investment decision. When you buy expensive it can turn any deal into a bad deal. Maybe he was pointing towards buying when markets are low and having a hold strategy. Once a stock is bought, you can’t reverse or do anything if the price falls down.

#6 – On Making Investment Mistakes: Warren was generous enough to admit some of his mistakes on a public platform. In the world of investments, you are bound to make mistakes and going wrong is part of the game. Berkshire Hathway was a late entrant in the technology front and they admitted the same. They are slowly moving out of their old school of thought to match with the new shift happening out in the world.

#7 – On Succession plan: Some Questions in the AGM also came around his succession plan and asking to hand over the stage completely to his team of managers. As a person sitting in the audience I felt, it is a bit hard for Warren to leave the limelight but in next 1-2 years his managers will lead the AGM and will find space on the stage rather than sitting in the first few rows of the AGM

#8 – Big NO to IPO: He advised investors to stay away from hot IPO’s that float into the market. His logic is very clear, these companies may have huge growth potential but they have yet not shown or generated profits. There are few companies he named as well who show growth potential but the numbers they are generating are not sufficient for him to make any investment decision.

#9 – Focus on the BIG picture: He used a very interesting metaphor of owning a stock with owning a farm. By simply owning a farm and watching your farm every day won’t yield you any returns. One has to work hard on the farm to deliver the output. Similarly, by watching the stock price every day won’t serve you, the stock price will grow only when the company delivers performance over a period of time. He is again asking you to buy the right stock or equity or fund and hold for a longer time. Some people check the NAV very often, now it is not a good practice at all (stop watching your farm).

Off the stage, things learned from Mr. Ramdeo Agarwal

Ramdeo Agarwal the co-founder of Motilal Oswal has been attending the AGM from the last many years, he looks up Warren as his Guru and he makes a point every year to attend AGM without fail. In an informal set-up, we got a chance to hear his past AGM Experiences, I also met his first PMS client, some fund managers from the US and Singapore.

Signature on One Dollar Note

Mr. Ramdeo shared that at the start when the crowd was small warren use to sign on a dollar for his shareholders. The queue started to expand in the subsequent years and slowly the tradition of giving signature stopped. He still carries the one-dollar note with him when he met Warren for the first time.

He personally checks the arrangements: Even to date, Warren visits the AGM venue one day in advance to check the arrangements. It shows how committed he is to details and giving a pleasant experience to people attending the AGM.

What I learned personally from the event:

Operating from a vision: I and Manish Chauhan, we started jagoinvestor with a vision of spreading financial awareness. The event helped me to ground more powerfully with our life’s vision and mission.

Life Force: Both Warren and his partner are 87+ of Age and they are full of energy and enthusiasm. This is because they see age as a number, they hold their life force high and that keeps them going. Take good care of yourself, exercise regularly, eat well and keep the enthusiasm scale on a high note.

Statue of Compounding: If you look at the wealth graph of warren buffet it has compounded after he crossed the age of 55. Compounding really works, equity markets are sensitive by nature but when you hold good funds or stocks it compounds and helps you to produce wealth. I placed my net worth on paper and I created a game for the next 30 years.

Keep Re-inventing: Warren and his team are constantly re-inventing their approach and style. They are now stepping into companies that are more technology-based. It was an important lesson for me as well, the way we run jagoinvestor and its operations we will continue to re-invent every year. It will be a ritual for us to meet once in a year to introspect and to explore the unknown territories.

Investors meet in a stadium: Yes, it is a dream to fill the entire stadium with investors. It is a dream I saw while I was in the AGM, Questions that kept hitting me were, what can I and Manish do or be to attract people to a stadium. What kind of financial discipline we will have to cultivate to inspire the investor’s community? What kind of content we will have to produce to create space in people’s hearts? The AGM gave me a dream bigger than who we are.

Power of Partnership: I saw Warren and Charlie on stage, two people working on a common mission and both having a very different style. I would like to create the same Magic with my partner Manish Chauhan. We both have qualities distinct from each other, our styles are different and together it helps us to create magic. In the AGM I could learn that partnership creates magic. We need to partner at a deeper level with each other, with our team, business partners, clients, readers, and other interested parties.

My recommendation

The next financial year if you get a chance to listen to the AGM, they show the event live on yahoo finance or if you are in the US I highly recommend you attend the AGM. It is a great space to be in, people get together to celebrate wealth.

I was accompanied this time with some Big time investors, fund managers and the co-founder of Motilal Oswal Group and I see Mr. Ramdeo Agarwal as one of my mentors. He is amazing to be around, spending time with him was a great learning experience.

During the Trip, I made many friends, met many interesting personalities, overall it was a life-altering experience for me.

Our upcoming sessions in Hyderabad and Chennai

One more point – I am going to share some of my learning’s in our two upcoming sessions in Hyderabad (29th June) and Chennai (30th June), if you are in any of these cities, do book your seats for our 3-4 sessions.

Do you know how much money is there in this world?

It’s $36.8 trillion (or 2569 Lakh Crores)

What if you get all this money? Imagine you wake up one day and your bank balance shows 2569 Lakh Crores. However, you also find that you are the only person left on this earth while every other person is missing.

All the malls, all the shops, all the movie theaters, all the entertainment parks, all the jewelry shops, all the real estate, all the fruits and restaurants and everything you can imagine is intact. It’s all available there.

So what can you do with all that money with you?

The answer is NOTHING.

You can’t do anything, because you can only exchange money with something and if you already have everything available on earth lying there and already available to you, the money just loses its role completely. That 2569 Lakh Crores with you is nothing but trash.

Coming back to our life, at the start we do not have much and money is something which can help us get access to lots of things in life. However, we move from having “Nothing” to “Something” to “Good enough” to “A lot” and then slowly “Almost everything we wanted”

In this transition over years, the importance of money comes down in our life. We already have most of the things we can wish for. You already have a house, a car, nice furniture, a second home, great vacations, eating out, etc. etc.

The Race of Earning Money

While money is very important in life, we are conditioned to think from our childhood that money is the solution to everything in life. We are subconsciously in this race of earning more and more money without setting a target. More is always better it seems.

Note that.

There is a limited amount of food you can eat in this world

There is a limited number of vacations you will take

There is a limited number of houses you can live in

There is a limited number of cars you can drive

There is a limited number of things you need to have a great life

How much money do you need?

5 crores, 10 crores, 50 crores?

I strongly suggest that you need to target a number or a range after careful thought and then let that number define your speed. There has to be a number which is ENOUGH for you.

You will be able to lead a very good, desired lifestyle in that much money.

Trust me you will eat the same thing and dress quite in the same manner if you have 10 crores or 50 crores. Rakesh Jhunjunwala or Mukesh Ambani eats the same thing as you do.

It should not happen that you keep acquiring wealth in life, and later it turns out to be nothing more than trash.

The Dalai Lama when asked, what surprised him most about humanity, he said:

“Man.

Because he sacrifices his health in order to make money.

Then he sacrifices money to recuperate his health.

And then he is so anxious about the future that he does not enjoy the present;

the result being that he does not live in the present or the future;

he lives as if he is never going to die, and then dies having never really lived.”

So what is the role of money in your life?

You need to define how much money you are targeting to acquire in your life. How much money is enough for you? Are you in a mindless race, acquiring all the money you can imagine and later, think where did my 60 yrs go? Or you are going to define the range which you want to acquire?

Something like “10 crores” is good enough for me once I retire. This is important because whatever time you give to earn money can potentially go somewhere else.

If you are working later hours for money, and coming home at 11:00 pm at night, then it means that you can’t wake up early and go for an exercise.

If you are working in some other city away from your family to earn a better income, it means you can’t spend that much time with your loved ones

If you are away from home during festivals so that you can earn/work extra, that means you are not going to spend that particular time with your family.

If you are not attending a wedding for your close friend, because you don’t want to lose those 6 days of a pay cut, that means that you will have that money, but then you will not have that memory of your friend’s wedding

If you are not taking your family to a nice vacation, then you will have that money in the bank, but you won’t have something to talk about years later when your kids grow.

Just like these examples above, there are multiple instances in life, where we have to decide between using our money and exchanging it with something.

Your Target = 1000 times your monthly Expenses

A simple calculation tells us that when a person accumulates around 400-500 times of their monthly expenses, they have enough to last for another 30 yrs.

This means that if you have monthly expenses of Rs 1 lacs per month, then 4-5 crores is a reasonable corpus for you. Let’s take 1000 times? So for a person, 10 crores if enough to last his lifetime (a very high-level calculation tells us that). In the same way, you should know what amount you are targeting for yourself.

So make sure you are clear about the importance of money in your life. While we have seen that a lot of people are not working hard enough to achieve all their financial goals targets, we see that a lot of people are putting too much emphasis on earning money and spending all their limited time into the race of earning money. While earning money is not bad in itself, make sure you know how much you need in life?

Question for you

I would like to know from you – “How far are you from your target?”. Do you think money has a bigger role to play in our happiness or a smaller role? Please comment below

Note: Note that I am not saying money is not important. I understand and acknowledge that money brings peace of mind, a sense of security and makes us powerful in away. I am only trying to give a perspective about the role of money in life. I am not saying that earning more money is bad or good. So in case you have hate comment, please read the article once again fully and point of the para or line which you want to debate on.