Recently the govt has announced the pension scheme called “Atal Pension Yojana”, which is targeted at workers from lower class who work in unorganized sector which constitutes around 88% of the workforce.

An account needs to be opened under this scheme and monthly contributions needs to be made till the time of retirement after which a pension amount ranging from Rs 1,000 to Rs 5,000 per month would be paid to the account holder and on death of subscriber and spouse, the nominee will get the lump sum accumulated by the end of the period.

Any person below 40 years of age can open an account.

The retirement age will be set to 60 years, hence one will get at least 20 years of contribution. Any person below 40 years can open an account. The retirement age will be set to 60 years, hence one will get at least 20 years of contribution.

How to open Atal Pension Yojana Account?

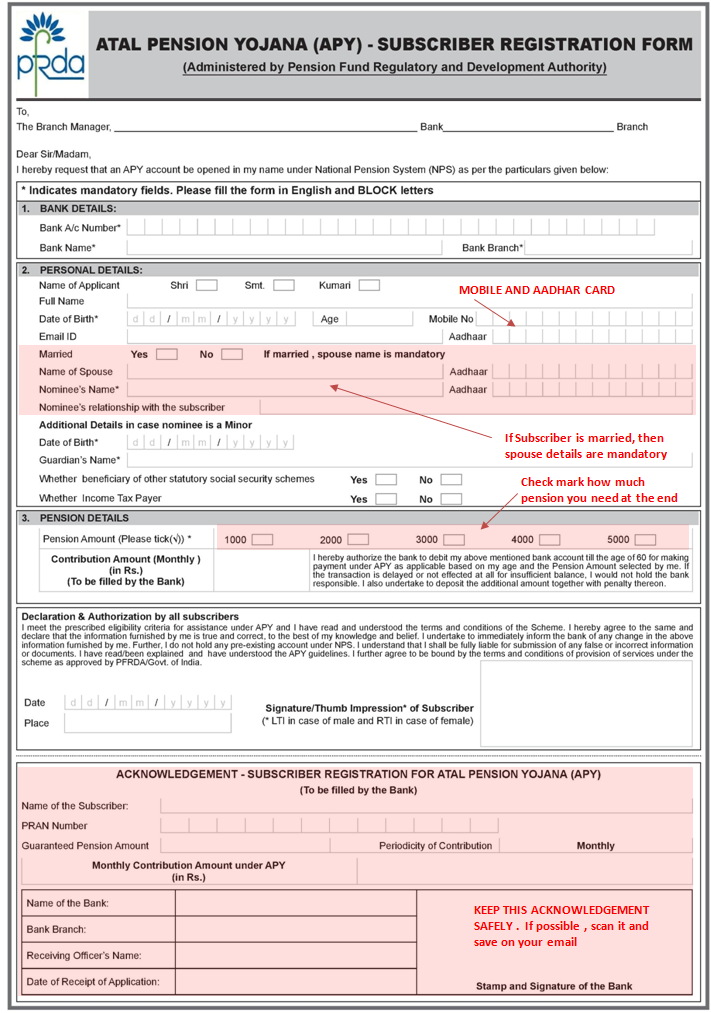

Go to the bank where you have your saving bank account like SBI, ICICI, HDFC or any other bank..

Mobile number is compulsory, hence that needs to be filled

If you have Aadhar card, provide the number in the form (but its not compulsory)

You also need to provide spouse details if applicable and nominee details, which is compulsory

You will select the pension amount you need in future and based on that the bank official will write the monthly contribution required on the form

Below is a sample form

Note that the form itself contains a section which mentions that you are authorizing the bank to deduct the monthly contribution from your account till the age of 60 yrs. So once the Atal Pension Yojana account is opened, your bank account will then get auto debited in future every month.

If one does not have a bank account, then one can give their KYC documents along with account opening form with the Atal pension Yojna account form.

Eligibility Criteria for Opening an account

The age of the subscriber should be between 18 – 40 years.

One should have a saving bank account or should open a new saving bank account

One should be having a mobile number, which needs to be furnished at the time of filling up the form

Governments co-contribution for 5 years

If one joins this scheme between 1st June, 2015 to 31st December, 2015 , the govt will co-contribute 50% of the total contribution or Rs. 1,000/- per annum, whichever is lower for the 5 yrs period from 2015-16 to 2019-20, But this govt contribution will be available only for those who are not covered by any Statutory Social Security Schemes and are not income tax payers.

What that means if that if you are an EPF subscriber, then you will not be eligible for govt co-contribution part.

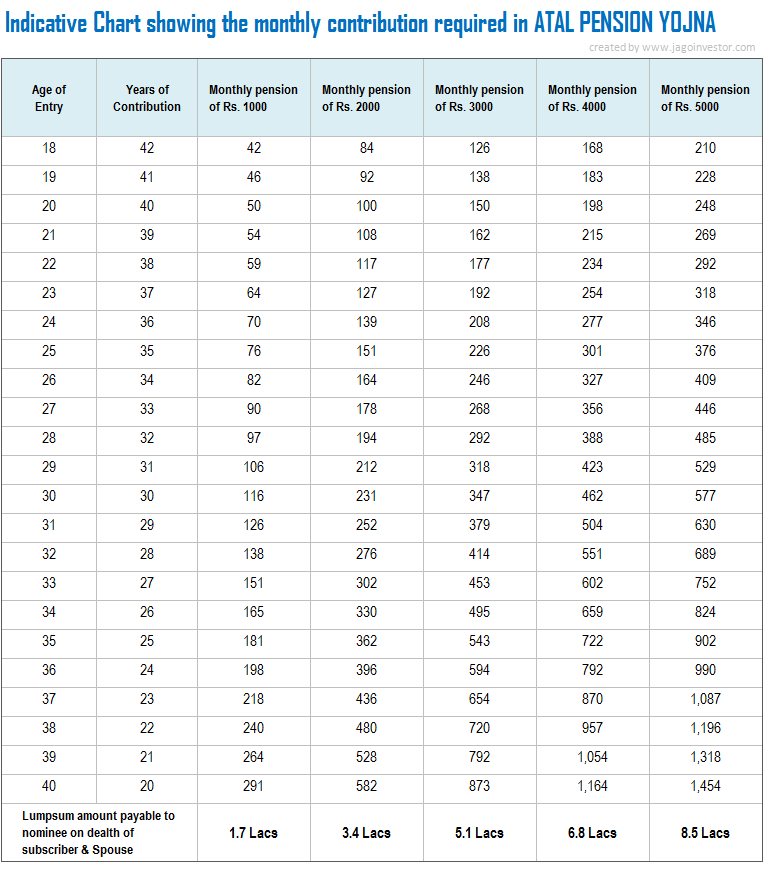

Below is the indicative monthly contribution required in this scheme at various age limits.

The subscriber can increase or decrease their contribution amount at some later stage if they want to do it

Will you get statements of transactions?

Yes, you will be getting regular intimations on your account information through SMS and even a physical statements each month. Note that you can move to any part of India without interrupting your contributions because the deductions will happen automatically from your bank account.

Can you exit or partially withdraw from the scheme ?

1. On attaining the age of 60 years – The first option is when you reach 60 yrs of age. At that time you will be able to use 100% of the money, but only in the pension form. You will only get the pension per month and not the lump-sum amount.

2. In case of death of the Subscriber (once they cross 60 yrs) – In case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

3. Exit Before the age of 60 Years – The Exit before age 60 yrs, would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease. As per Wikipedia, Terminal illness is a disease that cannot be cured or adequately treated and that is reasonably expected to result in the death of the patient within a short period of time. This term is more commonly used for progressive diseases such as cancer or advanced heart disease than for trauma.

What is your want to discontinue the payments or delay in payments ?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re 1 per month to Rs 10/- per month as shown below

i. Re. 1 per month for contribution upto Rs. 100 per month.

ii. Re. 2 per month for contribution upto Rs. 101 to 500/- per month.

iii. Re 5 per month for contribution between Rs 501/- to 1000/- per month.

iv. Rs 10 per month for contribution beyond Rs 1001/- per month.

Discontinuation of payments of contribution amount shall lead to following

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Are there any Tax benefits in Atal Pension Yojna scheme ?

No , there are no tax benefits available in this scheme. A lot of people might think that they will get any exemption under 80C or on maturity, but no benefits are available. The pension amount will be considered as the income for the person and will be added in the taxable amount.

What if someone is already a subscriber of Swavalamban Yojana under NPS ?

All the registered subscribers under Swavalamban Yojana aged between 18-40 yrs will be automatically migrated to APY with an option to opt out. However, the benefit of five years of Government Co-contribution under APY would be available only to the extent availed by the Swavalamban subscriber already.

This would imply that if, as a Swavalamban beneficiary, he has received the benefit of government Co-Contribution of 1 year, then the Government co-contribution under APY would be available only for 4 years and so on.

Existing Swavalamban beneficiaries opting out from the proposed APY will be given Government co-contribution till 2016-17, if eligible, and the NPS Swavalamban continued till such people attain the age of exit under that scheme.

Note that, the ultimately the money under this scheme will be managed through NPS only and thats the underlying thing. All the investments decision will happen as per the guidelines of PFRDA.

A good support system for Poor

As I mentioned, this scheme has the maximum pension of Rs 5,000 per month, that too when the person reaches 60 yrs of age, that too will happen only after a minimum of 20 yrs from now (only people below 40 yrs of age can open an account), so Rs 5,000 at that time would be a very miniscule amount.

However note that we are talking about the people in lower section’s who are really poor. At least this Rs 5,000 per month would be a great support in their old age when they won’t be working. A subscriber can open only one APY account.

With this scheme, people will be encouraged to save a small portion each month ranging from Rs 40 to Rs 210 per month. Below is the full chart showing how much money would be required to be deposited each month depending on the time of entry in the scheme and the pension amount chosen.

What is the returns of this scheme and should you invest?

So the question finally is, how good is this scheme and its returns if you consider the returns? I did a XIRR analysis of the scheme considering a 40 yrs old person is investing Rs 1,454 per month for 20 yrs , and then gets a pension of Rs 5,000 all this life (till age of 100 years). The returns I get is 7.74% through the excel sheet.

When I do the same thing for a 25 yrs old person invests Rs 376 per month for next 35 yrs (till age 60) and gets pension till he turns 100 yrs . The overall IIR is 7.9% . This includes the lump sum payment at the end to the nominee

So looking at the numbers, we can conclude that the returns from this scheme is in range of 7.5% to 8%. Considering that, Its a guaranteed return from govt of India, I will leave the judgement of its being good or bad to you only.

You should also read, Debasish Basu critical analysis of this scheme on this link to get more understanding about the issues of this scheme.

I would like to again reiterate the point that this scheme is more for the people of poor background who do not have access to any social security scheme already and will be somewhat beneficial for them, and not high-income earners because Rs 5,000 even after 20 yrs will be very very small amount.

If one wants to still open this account, one should find a good enough reason for themselves.

Are you investing in this scheme?

I would like to know what you think of this scheme and if you will be opening an account for yourself? You can also suggest this scheme to your maid, driver or any person who you think should get a minimum pension by the time they turn 60 .

At the end, I would like to share that we are doing our Bangalore workshop on 2nd Aug, please register asap for the event before its full

I got cheated at a Petrol Pump yesterday for ₹ 400.

Yesterday I went to a BPCL petrol pump to fill petrol in my car, where it all happened.

I asked the attendant for a “Full Tank”. I generally get out of my car and stand near the person filling it, but I was in a conversation with my friend and trusted the petrol pump as I have been there quite a number of times. However, this time I made a mistake.

The attendant asked me to see the ZERO on the meter and then started filling the petrol. Once the meter started and I thought that everything is fine, he stopped at ₹ 400 and started billing.

I knew this tactic where they say “Oh .. I thought you said ₹ 400”. So I told him to leave it at that point and bill it to me for ₹ 400 only. I paid the amount and went ahead.

However, my car indicator was still showing the same “51 km” which it was showing before I went to petrol pump and did not go past it. That’s when I realized that I was a victim of another Petrol Pump fraud, which I was unaware of. I already went too far from the petrol pump and had no proof of the incidence that happened. However, I was surely tricked.

I got back my Rs 400 and offer to terminate the employee

My immediate next was to lodge a complain on BPCL website with all details and I was quite surprised and happy to see that I got a call back from the petrol pump manager within 30 minutes.

He accepted the mistake and offered to pay back the fuel worth ₹ 400 and also terminate the employee if found guilty. I told the manager that I do not wish him to get terminated in this hard times. It will be enough if he can warn that person strictly and take measures to ensure this does not happen again.

Please listen to my 3 min audio recording with Petrol Pump Manager.

Update

Today I visited the petrol pump again as requested by the petrol pump main manager (he was not present that day when I got scammed). He was quite helpful and courteous in explaining all the things to me. He also got my car filled for Rs 400 petrol so that I am not in loss. Apart from that, he also showed me their automation system which records each and every entry with the time stamp.

I was able to see the entry of Rs 401.50 for the exact time and date. However as I said, the petrol did not reach my car at all. As I said I was not attentive enough that day. I guess the petrol was getting filled in some other vehicle or container (check Fraud #4 below) which I will leave the petrol pump to investigate using their CCTV. I was also offered by petrol pump to do 5 ltr fuel test incase I want to.

Please note that I am not holding BPCL or manager responsible for what happened. After I met the manager, and asked all the questions I had – I am convinced that it was purely employee mischief in this incident.

Also I want to acknowledge that BPCL was quite fast in resolving my case and the petrol pump manager was also quite prompt to investigate the case.

Is this a new kind of petrol pump scam which got invented?

This got me thinking about the quantum of these kinds of scams and frauds which happen almost every minute in our country in almost all the cities of India, where people get cheated of small amounts like ₹ 50, ₹ 20 or ₹ 500….

99% of the people who get scammed are not even aware of it. Others who are bit aware, they make a scene for 2 minutes, may get a refund and the matter is closed.

Massive “Small Scams” going on across the Petrol Pumps

There are close to 60,000 – 70,000 petrol pumps in our country. Imagine the amount which is looted together by all petrol pumps (leaving those who are clean) even if they do small frauds.

I feel it’s so rampant that it might amount to thousands of crores which is yet to be investigated in detail.

So to make everyone aware, I started digging internet, YouTube and various other platforms like Team-BHP, Quora, etc to check experiences of other people who got cheated and thought of compiling a list of different ways through which petrol pump attendants along with owners/managers in some cases defrauds customers.

So let’s see various frauds one by one ..

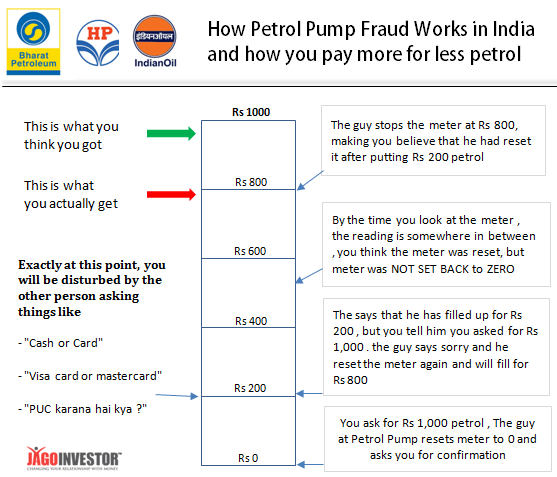

Fraud #1 – Short Fueling by distraction

This is most common and widely experienced fraud which can be done quite easily if you are not alert. Here is how it happens;

You ask for petrol worth ₹ 500, and the meter is already at ₹ 100 (the person before you filled it for ₹ 100) . The person tries to show that he is resetting the meter to ZERO, while you are distracted by another person. He does not reset the meter in reality, but starts from ₹ 100 itself and goes till ₹ 500.

You pay ₹ 500, but you get the fuel only worth ₹ 400 only.

If the meter is already set to ZERO, then they use another trick.

So you ask for petrol for ₹ 500, the attendant asks you to check the meter at ZERO and then stats filling the petrol and stops at ₹ 100. When you ask him why he stopped at ₹ 100, he tells you that he heard ₹ 100 only. Then he says that no issues, he will reset and fill another ₹ 400 (will give some crap technical reason why he can’t continue from that same point).

At this point someone from his team distracts you while the attendant starts filling from ₹ 100 onwards itself, when you think that he had reset the meter back to ZERO. Then he goes till ₹ 400 and charges you ₹ 500 (₹ 100 + ₹ 400). You get petrol worth ₹ 400 only, but pay ₹ 500.

In both these tricks, someone distracts you in the name of PUC, cleaning of vehicle, or will just ask you some silly thing and you turn your eyes away from meter.

Here is an image showing how it works

Unless you make a scene then and there itself, it becomes quite tough to catch them later because by that time the incident in old enough and you also loose the interest in fighting for few hundred rupees.

Fraud #2 – Tweaking fuel-dispensing machines using integrated chips

This is a clear cut fraud from the main owners of the petrol pumps or at manager level, because in this fraud – an integrated chip is installed in the machine itself. This chip makes sure that 3% less oil is filled every time while the meter shows the full amount. So if you ask for ₹ 1000 petrol, everything will look perfect but you will get petrol worth ₹ 970 only.

Even the receipt will be generated for the full amount. This is a small tweak which is done in the machine itself.

Imagine 10,000 customers coming to a petrol pump and everyone gets 3% less fuel. How big is that as a scam .. Now multiply that with hundreds of petrol pump who may be doing this.

To read more on this kind of fraud, you can read this article where it’s explained in detail about how the chip works and the methodology

Fraud #3 – Filling the costly version of Oil (Speed / Power) without asking

This is not exactly a fraud, but an unethical thing which most of the petrol pumps do.

They by default start filling the costlier version of the oil (Speed Petrol or Power Petrol) without customer asking for it. Most of the cars or bikes in India run totally fine with the unleaded version of oil which is the default thing. Then there are high octane fuels which can cost 5-10% more than the normal price.

A lot of petrol pumps guide their employees to NOT ASK which version to fill and directly start filling the high performance fuel. And if you catch them and question them, they inform you that it’s your responsibility to clear in start which one you wanted.

You may want to refer to this video from AskCarguru on this topic or read my article

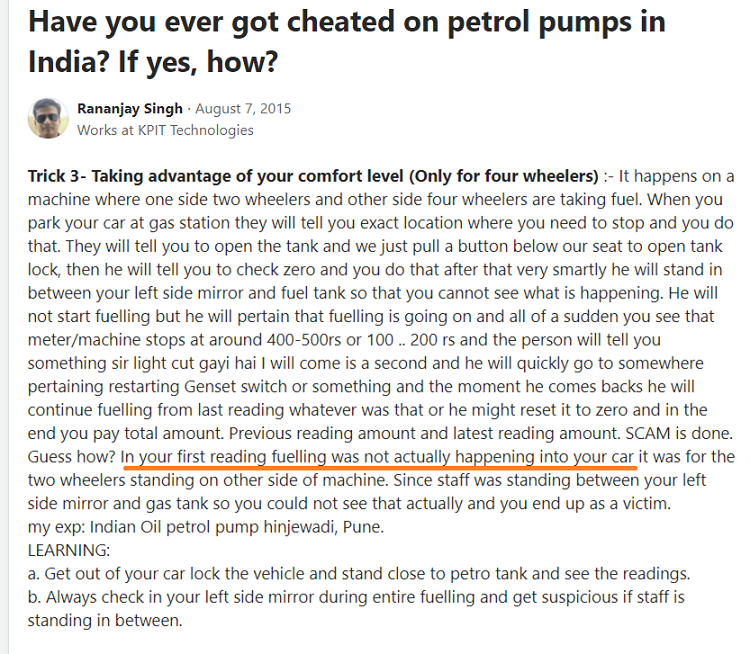

Fraud #4 : Blocking your Mirror and Filling Oil to another Vehicle

This is an advanced level of fraud done by some high risk taker employees of the petrol pumps. This is done to those who like to sit in the comfort of their cars and completely trust the petrol pumps.

In this case, the person filling the petrol pump will show you the meter and set it at ZERO and then come in between of your left mirror and fuel tank. While fueling, he will stop at ₹ 200, ₹ 300, ₹ 500 or some number like that and will give you various reasons for why he stopped, for example, he is coming in 2 min or he has to bring swipe machine or start generator, etc. Once he is back, he will start from the same point.

You will feel everything is normal; however, the trick is that before he left, he was actually filling the oil in some other vehicle (obviously another guy is involved). Your mirror was blocked from seeing what is happening and you were either on a phone call or were listening to music, etc.

I guess this is what happened with me recently as I was in a conversation with my friend and was bit careless (as I had used the same fuel station many times! poor me)

Fraud #5 – Start-Stop Trick to create an air lock (Long Nozzle)

A lot of times, the attendant while filling the oil, does not lock the dispenser nozzle into the tank neck and manually keeps pressing the start and stop button repeatedly. This makes sure that some quantity of oil is locked into the dispensing machine due to the air lock which is created.

As per the studies, 200 ml of oil is saved for every 10 liters of oil. Which means that if you are asking for FULL Tank, you are probably loosing close to 500-750 ml depending on your tank size.

Also if the dispenser nozzle is a long one, a decent amount of oil remains in the nozzle.

Considering thousands of liters of oil sold by a petrol pump every day, it probably saves them dozens of liters of oil, which I and you are paying for.

The solution for this is simple. Make sure the attendant locks the nozzle and does not interrupt till the auto-cutoff point is reached. Also the hosepipe should be raised as high as possible while taking it out of the tank.

Fraud #6 – Resetting the Meter to your final amount in between

This is a trick which shows how innovative people are.

In this trick, suppose you asked the attendant to fill petrol for ₹ 2,000. He shows you ZERO in the meter and starts filling the petrol.

Everything is going fine.. But towards the end when the meter shows around 1600-1700 and you get a feeling that now no one can scam you, some random guy will disturb you for various things like “Card or Cash” or “PUC” or “Lucky Draw” and things like that.

You are already relaxed now because you have been cautious enough from start thinking “what can go wrong now”.

The billing time comes, you check the meter and it shows your final amount of Rs 2,000. You pay the bill and leave.

Congratulations! You are scammed of few hundred rupees.

What happened?

So when the meter was at ₹ 1,700, and you got disturbed and diverted your attention to something else. The guy who was filling the petrol stopped filling the oil, did reset the meter to ₹ 2,000 (while the number of liters did not change).

We generally look at the amount only and not pay much attention to the quantity displayed. Some websites where I researched about this fraud also mentioned that in this kind of unauthorized meter reset, the meter amount blinks which is an indication that it was reset in a wrong manner.

Here’s another trick used by the pumps. This one in Pune. Mauli Petrol Pump (Baner Road) – HP dealership. You ask the attendant to fill Rs 1000. He asks you to check the Zero (reset) to gain your trust. Thereafter you don’t pay attention till it’s time to pay – that’s a mistake. You should pay attention throughout the process. Here’s why.

Attendant punches in Rs 1000 into the dispenser, asks you to see the Zero and continues filling. Then when it is close to being Rs 1000, say at Rs 800 or so, he pulls a switch to reset the counter – apparently there is a way to “round-off” or reset the amount, so that the amount on the screen is seen as Rs 1000. You feel that Rs 1000 has been filled when in actuality only Rs 800 is filled.

Modus operandi is this. After around half way of fuelling, someone at the pump will distract you for Cash/Card or Car Polish or PUC, etc. It is during this time that the attendant cheats you by pressing the reset switch. This particular pump does not have an electronic receipt system and gives handwritten receipts to hide this fraud – an electronic receipt would have indicated the exact volume of fuel dispensed.

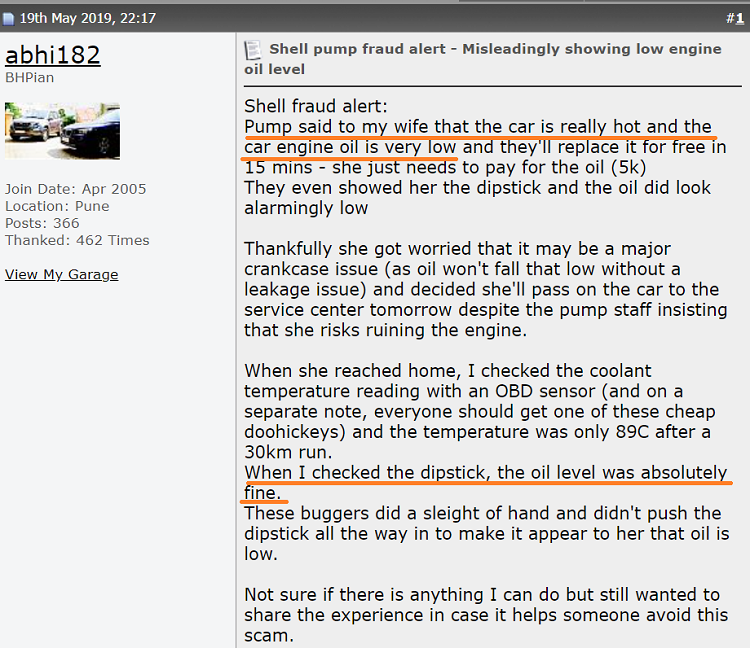

Fraud #7 – “Low Engine Oil or Coolant” Scare

Another fraud is not about the petrol or diesel, but scaring car or bike owners of low engine oil or low coolant and then selling their products. I have seen this multiple times happening at some petrol pumps where they offer to check the engine oil level and refill the water level. I don’t understand why my engine oil is always low only when I reach the petrol pump.

Once I realised that it was just to scare me in order to sell their products, I always tell them that my car is going for the servicing next day.

Here is an incident which was reported at Moneylife where they were cheated into believing that their engine oil was diluted and they were sold 5 packets of servo engine oil, which they got refund for later once they figured out the scam.

This even happens at Shell Petrol pumps which are generally quite famous for no scams (which I agree). Here is an incident which was reported at Team-BHP website by one of their members

Who is involved in these frauds? Employee or Owners?

Majority of the time, it is the attendant who is responsible for the small frauds and cheating which involves few hundred rupees.

They carry out some on their own and some with help of fellow attendants. However, in some cases even the petrol pump incharge/manager might be involved with the attendants in such frauds.

A lot of people say that manager/owner might be involved because the attendents take payments using the cards/paytm/google pay and not cash always. Even in this case the attendents might be able to benefit. This is because the payments happen by both cash and card and at the end of the day, they may adjust the amounts.

Having said that, some of you might think how exactly the entire process is carried out.

To understand this let’s look at a scenario.

At every petrol pump, meter reading on the petrol vending machine is taken at the start and end of the day. Sometimes it’s taken during shift changes. So, the point here to note is that the meter reading of start and end is taken.

Each transaction is not reported one by one. So at the end of the day only thing which is checked is the oil sold and amount collected through Cash and Card. If a fraud is done for Rs 500 and the payment happened by card, the attendant can take the Cash of Rs 500 out of all the cash collected. That’s all

Here is a simple example

Now suppose according to meter reading the sale made for that particular period is ₹ 900 just for understanding the system. There were two buyers who filled the oil, you and me.

You paid through card and I paid through cash. Now you asked for ₹ 500 fuel, but the attendant filled your tank only with ₹ 400 of fuel. Then I came and asked for ₹ 500 fuel and got fuel for entire amount and paid ₹ 500 in cash. Now, at the end of these two transactions. The amount that is with attendant is ₹ 1,000 (₹ 500 card payment slip + ₹ 500 in cash). However, the total fuel sold is only for ₹ 900 (₹ 400 to you + ₹ 500 to me). Hence, he conveniently takes out ₹ 100 cash from his collection and pays ₹ 900 to the petrol pump incharge/manager.

This ₹ 100 will then be distributed among the conspirators as per the agreed percentages.

Note that only in the big frauds which are manipulation of machine it self, the owner or manager might be involved.

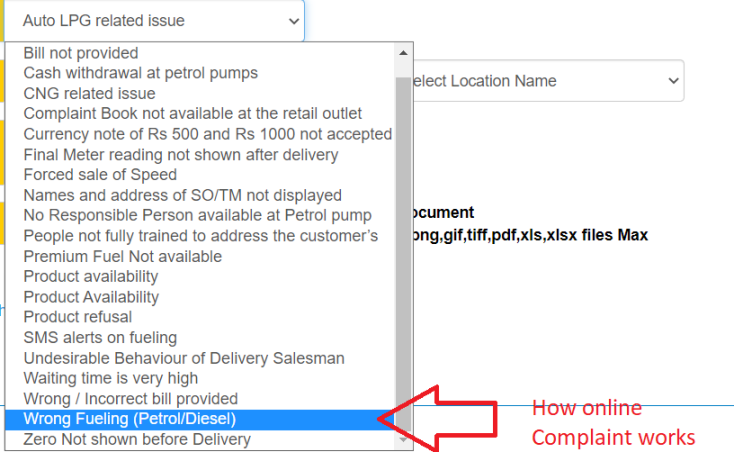

Where to complain against Petrol Pump?

The first step is to ask for the “complaint book” of the petrol pump and register your complaint locally. Each Oil company has a complaint register book at every petrol pump station which they look at during audits and inspection. The petrol pump attendant or owner/manager will first try to give you reasons for not having it or will persuade you not to register the complaint. But make sure you do it.

Apart from that you can lodge your complaint online on the oil company website. I did complain on Bharat Petroleum website about this issue

When I checked on internet, many people reported that it’s helpful and actions are taken in few weeks or months. Here is the links which you can use

[su_table responsive=”yes”]

If you are in car, always come out and keep a close watch at the meter and how they are filling the petrol

Always make sure the meter is reset to ZERO in front of your eyes.

Always make sure that the meter shows ZERO while the oil nozzle is entered in the car tank.

Always ask for the electronic receipt after the oil is filled. Make sure before filling the petrol you check if there is digital meter or not.

Always avoid talking or entertaining anyone in between as far as possible.

Make sure you pay at the end of the transaction

Incase meter is stopped for any reason, offer to just complete the transaction and fill the petrol at next station or next day.

In case you are not satisfied with anything or want to complain – do insist for the complaint book, as the oil companies take the complaint book very seriously.

Please share if you have any experience of getting scammed on Indian petrol pumps..

Our investor workshop “Design your financial life” has been a great learning experience for us and for our past participants. I and Manish always look forward to our live events because we get a chance to see many investors making fresh new commitments to bring a turnaround in their financial life. Wealth creation happens when an investor expands his or her capacity to take actions. Our workshop will help you to expand your action taking capacity; it will fill your financial life with new and empowering actions. you can skip this article and directly register for the workshop

2nd Aug – Jagoinvestor workshop in Bangalore (Sunday)

If you are from Bangalore we invite you to mark and block 2nd of August on your calendar (just one Sunday). Ask yourself – “Have you ever blocked one full day for your financial future?”

If the answer is NO, register and become part of our Bangalore event. For creating a wonderful financial life the first thing you have to give your financial life, is your time. Here are some pictures from our Mumbai Workshop recently

Why we conduct these workshops ?

We do offline workshops so that we can connect with some of our readers at a deeper level, round the year we write articles, reply to thousands of comments and work with a few hundred investors one on one and in that process we learn, grow and expand as an individual. Workshop gives us an opportunity to share outrageously all the knowledge and experiences that we acquire round the year. The program is an opportunity to get our readers more and more action oriented.

Why you should come for this workshop?

You will learn how to improve your financial life with your current set of resources and income.

You will learn how to plan for your financial life goals

You will interact and learn from other’s people’s financial life

You will dedicate one full day to get better with money management

You will learn to add new dimensions to your financial life

To understand that personal finance can also be fun

To give a whole new direction to your financial life

It’s time at add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and the experience has been amazing. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation. We do not teach tricks and tips to build wealth in fact we help you to discover your own personal process of creating wealth.

This time we want more and more couples to participate so that they can get on same page when it comes to personal finance. It is extremely important that husband and wife both take equal interest when it comes to money management. We are offering special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct are highly interactive, it has lots of activities and fun exercises which helps you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short there is something for everyone in this workshop.

Listen to workshop Participants who attended in Past

Register for Bangalore workshop on 2nd Aug, 2015 (SUNDAY)

Venue and Timing Details8:30 am – 6:00 pm , 2nd Aug (Sunday) , 2015

IRIS HotelIRIS HotelNext to Eva Mall,

70, Brigade Road, Bangalore Check Map

The hotel is walking from Eva Mall on Brigade Road

Lunch and Breakfast is included in the program fees

What you get as a workshop participant ?

One day workshop with some personal finance tools like budget sheet, Mutual fund tracker etc

Invitation to join our inner circle

Invitation to join and participate

From the bottom of our heart we invite you to join and participate in Bangalore workshop. Come alone or with your spouse or parents, siblings or friends but see that you do not miss this opportunity. Do not let time or money to get in your way and book your seat at the earliest because we will be taking only 35 participants this time and registration will close after some days.

This workshop is strictly for investors and not for advisors or finance professionals. If you have never participated in any personal finance workshop let this be your first experience. If you have any questions you can write in the comments section or you can mail us.

Today I am going to review features of “Care“, one of the good health insurance policies in the market. It was launched few years back and it’s really one of the most comprehensive health insurance products available in the market as on date. So what I will do is, share with you, its features one by one, so that you can know what all it covers, along with few disadvantages in the policy

I digged deeper in its policy wordings and I will explain them in detail, so that anyone who is looking forward buy a health insurance policy can take the decision in a better way by reading this Care review. Here you go..

1. High Sum assured up to 60 lacs is allowed

The sum assured offered by the policy ranges from 3 lacs to 60 lacs. Gone are the days when 2-3 lacs of sum assured was sufficient. Now it’s very common to see people buying a cover of 10-20 lacs. Many people even want to go for a cover of 30-40 lacs also and there are very less options right now if someone wants to buy a high enough health cover. Care gives you an option to buy up to 60 lacs of health cover, and the best part is the high cover comes along with added benefits which we will look very soon

2. Single Private Room (no rent limit)

If you choose the sum insured of more than 5 lacs, then you are eligible for a single private room. The wordings in the policy is of “Single private room” and not some percentage of sum assured.

Most of the policies cap the room rent limit, however this policy caps the room type. Here, if the user takes a room higher than the type eligible he still is required to pay the difference of the room rent as well as all other expenses which increase due to choosing of a higher room type

I love this point especially because room rent limit is such a critical factor while calculation of your claim amount, you can read how room rent limit affects your claim process if you choose the room with higher rent

3. Cashless treatment in network Hospitals

Care has a network of around 4,100 hospitals around the country. If your hospitalization is planned after few days, in that case, you don’t have to shell out any money from your pocket. You can choose to take cashless treatment and the bills will be settled by the health insurance company directly to the hospital.

This is not a special feature in Care. It’s present in almost all the health insurance policies these days. But I thoughts it’s a good mention in this article as we are looking at all the features. Also, note that cashless treatment is an additional benefit which helps a customer. You can always choose to not have a cashless treatment and pay the bills yourself and settle the claim later by submitting the bills. In case of emergencies, you anyways can’t choose cashless treatment.

4. FREE Health Check each year

You also get free health checkup’s facility every year for all the adult policy holder’s lifetime!. There are no terms and conditions for this. Just that the facility is there only for sum assured of more than 5 lacs. Also, the number of health checkups depends on the sum assured amount. You get more detailed checks done when your sum assured is high.

I have realized that a lot of people do not spend their own money for regular health checkup’s, so in a way it’s a great feature in the policy, due to which one will form the habit of regular checkup’s and will be informed about their health issues.

Each year you just need to contact the company and express your desire for the health checkup and they will schedule it for you in one of the centers they have tie-up with and which is also near your house. You can choose the timings and place as per your convenience. You can collect your health reports after 24 hours of the checkups. It’s a really great thing offered by any company.

Below is the health checkup list for various kind of sum assured slabs as per their brochure.

5. Restore of sum insured up to 100% amount

The policy has a feature called restore. In this feature, if there is a large claim in the policy due to which the sum insured is exhausted or reduced substantially, in case of a subsequent unrelated claim, if the sum insured falls short to pay the claim, the policy reinstates/restores to cover to 100%. Let me explain that in detail.

Let me give an example

Suppose you have a 10 lacs sum assured. Now due to some heart-related issue, you were hospitalized and the expenses were Rs 4 lacs. So your remaining sum assured is 6 lacs. You can utilize the 6 lacs sum assured for any purpose.

But if some another hospitalization comes up for an unrelated claim, and the expenses are more than your remaining sum assured, then your sum assured will be restored to the full amount of 10 lacs. Even your other family members can avail for the full sum assured even for the same illness. Note that in case of family floater plan, it’s highly beneficial because even the other family members can take benefit of full sum assured for the same illness.

6. No claim bonus up to 50% of sum assured

No claim bonus is a very simple concept, where you get rewarded if you don’t have any claim in a year. In Care, your sum assured gets increased by 10% of the base sum assured if you do not claim in a year and keeps increasing upto 50%. Which means that if your sum assured is Rs 10 lacs, then if you do not have any claim in a year, then next year it will increase by 10% (10% of 10 lacs) , and your sum assured will become 11 lacs . Again if you do not have any claim in the next year, it will increase to 12 lacs and so on..

So your cover of 10 lacs can go up to 15 lacs maximum if you do not claim for 5 yrs consecutive. A lot of policies (like Oriental Happy Family Floater), they reduce the premium by some percentage as no claim bonus and many people are happy about that, because that means less money going out of their pocket. But truly speaking what you need is the increase in sum assured, not a reduced premium, because every year due to inflation and rising medical costs, you need higher sum assured.

I don’t see a big benefit in saving few thousand or hundreds in premium in the name of no claim bonus.

Super No-Claim Bonus

This policy also gives an additional benefit called Super No-claim Bonus which will cost you extra premium if you wish to take it. In this super no claim bonus facility, your no claim bonus will be 50% extra each year up to the maximum of 100% of sum assured.

What that means is that if you do not have any claims, then within 1 yr, your sum assured will increase to 1.5 times and in 2 yrs, it will double. So if you have a policy of 5 lacs sum assured, then

Sum Assured in first year – 5 lacs

Sum Assured in 2nd year (assuming no claim made in previous year) – 7.5 lacs

Sum Assured in 3nd year (assuming no claim made in previous 2 years) – 10 lacs

And this super no claim bonus is over and above the no claim bonus which you anyways get in the policy. So truly speaking your sum assured can increase anywhere from 60% to 150% in some years if you take super no claim bonus option while purchasing the policy. At the time of applying for the policy itself you need to mention that.

7. Around 170 Daycare Treatments covered

The policy covers around 170 day care treatments (In-patient treatments) , which are mentioned in the policy document. A lot of times you don’t need to get hospitalized for many days or even 24 hours. Some treatments can be done in just few hours. You can get admitted in morning and get things done by the evening or just few hours.

Even these kind of in-patient treatments are covered in the policy. A common myth is that you need 24 hours of hospitalization to claim your health insurance benefits, but it’s not true. Many years back when health insurance was a new thing in India, it was probably true. But not anymore.

Below is a snapshot of the policy terms and conditions pdf and you can see some of the day care treatment names mentioned. There are total of 170 treatment names listed in the document.

Please do not confuse these day care treatments with OPD. OPD treatments are not covered in any health insurance policies

8. Second Opinion and Organ Donor Cover

If there are any expenses which are incurred on the organ donor, then even those expenses (along with hospitalization expenses) will be covered in the policy. The limit for this expense ranges from Rs 50,000 to Rs 3 lacs depending on the sum assured. A lot of times, in critical cases, if there is any organ which needs to be replaced and you get any donor, then you will not have to incur the expenses from your own pocket due to this feature. While this is an extreme care, still we should appreciate that the policy takes care of this point.

Also the policy has a feature called “Second Opinion”. In this, if any of the policy-holder is diagnosed with a critical illness, then the company will arrange a free discussion with a qualified medical practitioner for you. This is great feature, because a lot of times, you want to consult another doctor before taking a big decision like surgery, operation or any hospitalization. The policy lists down the critical illnesses for which you can take second opinion. Note that the second opinion facility is only for sum assured above Rs 5 lacs.

Below are the critical illness mentioned in the policy

Benign Brain Tumor

Cancer

End Stage Lung Failure

Heart Attack

Open Chest Coronary Artery Bypass Graft

Heart Valve Replacement

Coma

End Stage Renal Failure

Stroke

Major Organ Transplant

Paralysis

Motor Neuron Disease

Multiple Sclerosis

Major Burns

End Stage Liver Disease

Each member of the policy can avail the second opinion facility for each illness every year if required.

9 – Avail Medical Treatment anywhere in world

If you have opted for sum assured of 50+ lacs, in that case, you can avail the medical facilities through the world, where-ever you wish to , but it’s limited to only 5 major illnesses. Also, the benefit is available only on reimbursement basis only. Means you first have to spend the money from your pocket and then claim it back later. So I think this will mainly be helpful for the high net worth individuals and not to the middle class. Anyways a good feature, because some people might look forward to this.

10 – Pre and post hospitalization expenses

The policy also pays for any medical expenses related to the claim before and after getting admitted to the hospital. It covers 30 days of pre-hospitalization expenses and 60 days of post-hospitalization expenses. A lot of times a big amount is spent before and after the hospitalization in medicines, checkup’s and other things. It’s very important that a policy takes care of these facts. However, note that this is a basic feature, and almost all the policies in market gives this benefit.

11 – Domiciliary Expenses Covered

The policy covers the medical expenses incurred on the home treatment. A lot of times a patient is not in the condition to the hospital, in which case the treatment can be done at home. The policy will pay upto 10% of the sum assured in this case. The condition to avail this offer is that

The patient is no in condition to be moved to hospital

OR, there is non-availability of the room in hospital

Note that there are many illness for which the domiciliary expenses cannot be claimed, please check that list in the brochure of the policy.

12 – Lifetime renewal and no restriction on entry age

Once you buy the Care policy, you can then renew it lifetime. This is one of the most important points one should remember while buying any health insurance policy, because you buy the policy looking at a very long-term and not just for next few years. The policy should be able to help you when you are in your late years, because that’s when you really need it badly.

Also, there is no limit on the maximum age by when you can renew it. On top of it, even the entry is not restricted due to age factor, a person can buy the policy at any age, provided they fulfill the health checkups and the restrictions by the company.

Waiting period of 4 yrs for pre-existing illness

Under this policy, any pre-existing illness will be covered only after 4 yrs of taking the policy. This is a common exclusion in almost all the policies. However if you are a senior citizen, then the coverage for that particular illness might be excluded permanently, because once you cross the age of 60, the chances of you getting hospitalized due to that particular illness is high and it does not make any business sense to cover it.

This is precisely the reason why one should take their parents cover as soon as possible, especially before they cross the age of 60 yrs. Apart from the pre-existing illness, a lot of illness have their own waiting periods from 1-4 yrs, which is a standard thing in any kind of health insurance policies. Also nothing other than accidental hospitalization is covered for the first 30 days of taking the policy. I suggest you read this article which talks about exclusions in mediclaim policies in detail.

Other Points

Below are some other important points one should be aware about

If your sum assured is more than 5 lacs, then there is no sub-limit on the ICU charges, Doctors fees and Medical fees.

The policy provides ambulance expenses ranging from 1,000 to 3,000 depending on the sum assured

There is no age limit of buying a new policy. Anyone can buy the policy at any age, just the minimum age requirement is 91 days for family floater and 5 yrs for an individual policy.

Maximum 6 people can be covered in a single family floater plan

The policy like every other policies in market does not offer any dental care treatments

This plan does not cover maternity expenses, but that’s ok. Don’t over focus on this point, as it’s something you can take after yourself

You get 7.5% discount if you renew/buy the policy for 2 years and 10% discount of payment of 3 yrs in one-shot.

Disadvantage of Care Policy

Let me mention some the problem and disadvantages of the policy.

1. Average policy, if sum assured is less than 5 lacs

A lot of features are applicable in the policy only when the sum assured is more than 5 lacs, if you want to take a lower cover like 3 lacs or 4 lacs, in that case, Care is an average policy and not the best.

2. Room type capping

You already know that the policy caps the Room type instead of room rent. This was a good advantage also, but at the same time, this can be a disadvantage also. In this case, suppose the room type which your policy allows is unavailable, then you will have to go for some other type of room and in that case you might have to suffer the reduced claim amount. You are tied-up with a particular room type only.

Suppose there is some other policy, which caps the room rent limit at 1% of sum assured and imagine that your sum assured is 10 lacs, then you are eligible for any room with rent of up to 10,000 per day. In that case, you can choose either a single room without AC, with AC or a premium room. It’s totally your wish as far as the room rent is below 10,000. But in case of Care, if suppose you are eligible for a single private room whose rent is 6,000, and the next category of room costs Rs 9,000, then you can’t go for the Rs 9,000 room . You can surely take it, but then your claim amount will get affected. So make sure you think on this point properly before you buy the policy.

It’s totally your wish as far as the room rent is below 10,000. But in case of Care, if suppose you are eligible for a single private room whose rent is 6,000, and the next category of room costs Rs 9,000, then you can’t go for the Rs 9,000 room . You can surely take it, but then your claim amount will get affected. So make sure you think on this point properly before you buy the policy.

I suggest that you also compare Care policy with some other policies like Max bupa plans or Apollo Munich Optima Restore and then take a final decision.

3. Co-payment of 20%, if policy taken after 60 yrs of age

If at the time of entering the policy, the age of the policyholder is more than 60 yrs, then a 20% co-payment will apply. Which means that the policy holder will have to bear the 20% bill amount and only 80% will be paid by the company. But if you enter the policy before 60 yrs, its not the case.

Hence the policy becomes unattractive to senior citizens who are looking for health insurance. In comparision a policy from L&T insurance is better where 10% co-payment applies after the age of 80 yrs. The policy from Max Bupa called Heartbeat, does not even have the concept of co-payment. So the policy from Care scores low on this point.

Premium Chart for Care

Below I have listed down the premium amount 5 lacs sum assured, for various age range with two cases of a single person insurance, and another one is a family floater policy with 2 adults and 1 kid. You can check how the premiums will rise over the years when the policyholder will move to various age slabs. Note that now there is no claim based loading in the premium. Now as per new guidelines of IRDA, a policy premium increases when the policyholder moves in a different age range.

An important point to note in the premium chart about is how the premium is very less in the initial years, when you are below 60 yrs and how it increases when you become a senior citizen :), which is quite natural and explanatory. Also you should not be shocked to see these high premium values in today’s time, because these are all future values, and even though today these premium values might look big to you, but when you turn 60 or 70 yrs, at that time these premium values will look very normal to you.

Snapshot of the Care benefits

Do you want to buy the Care policy?

If you want to buy the policy or want to enquire about it, then just fill up the form below and you will get a dedicated phone call to help you choose the policy and explain you.

I hope you have got a fair idea about the policy. Note that this Care health insurance review is mainly for educating you on various features of the policy. Please check other policies details and make sure you choose the policy which suits your requirements.

Let us know what are the points you liked best about Care and which point you didn’t like ?

EDIT : This is not a paid review. We have started d0ing review’s of various policies and we will do review other products as well. This is just a point by point explanation of each important point in the policy. Also, we have added the disadvantages of the policies, not just positive’s. Care is definitely not the best in market in all respect, but a very good policy considering most of the profiles. Please see the article more as an attempt to help a person understand what all policy provide’s its customer.

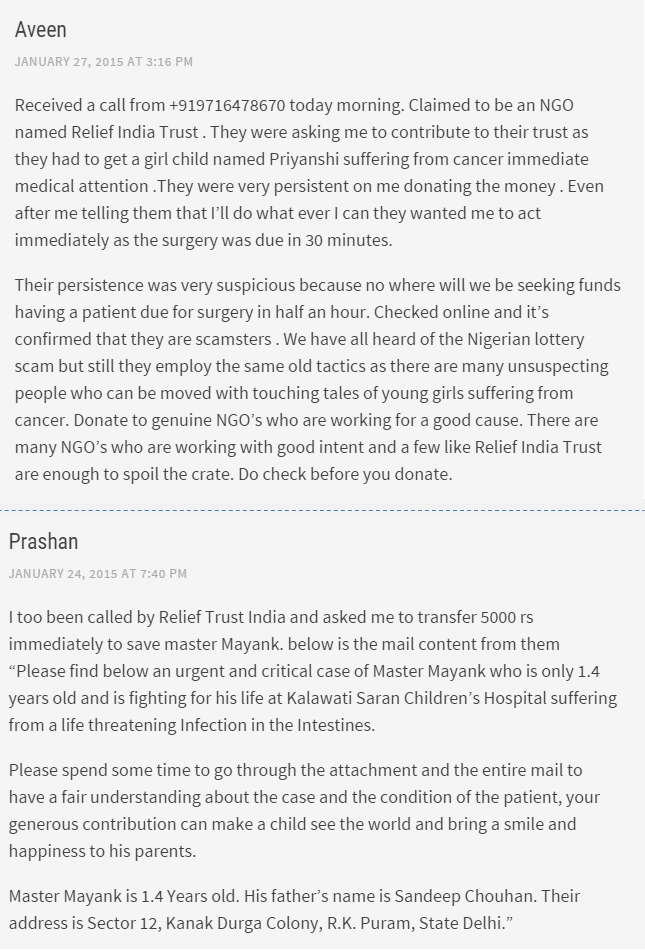

A few months back I got a call from an NGO based in Delhi. They were trying to help a small baby, which was a critical medical condition and needed immediate medical help and they were generating the money from all over India. Even there were social media campaigns around it. The girl talking to me told me its an urgent matter and how as a citizen, my help could mean a lot to the poor child.

I told her, she can mail me the details, so that I can look at what I can do from my side. After 1 hour, when I typed the NGO name and it turned out to be a big fraud campaign, which was widespread and many people reported their complaint.

But this was just one example. There are so many areas where various kind of frauds are going on all over the country and many uneducated people who do not understand the online world fall for it and lose their money. This is worst than mis-selling at times because in mis-selling you get bad returns or your money is stuck, but in these kinds of frauds you lose all the money forever. So I want to share some tricks used by people to do online frauds and their modus operandi. Here they are –

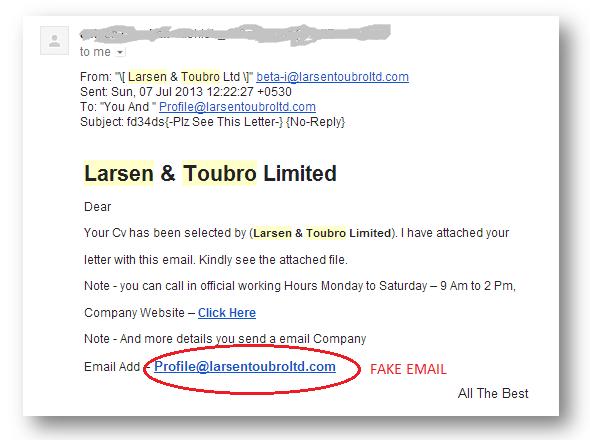

Fraud #1 – Fake Job Offer

Millions of people are unemployed in India and that has given birth to this job offer scam. In this, you get an email offer from a reputed company which invites you for their interview. You see all kind of numbers, venue, last date etc, and then you see a line mentioning that you need to deposit a security deposit or some basic fees, which will be refunded later.

Given so much of unemployment, a lot of people fall for this trick. The emails look very genuine when you read it, as it contains the company logo, or it might be on the letterhead of the company, but when you dive deeper and check the email id from which it was sent or the website link, you can figure out that something is wrong. Below is one such mail.

Remember that no company in its senses will ever ask you to deposit any kind of money with them for an interview. Below is an example of how people lose such a big amount in these kinds of fraud offers.

Cybercrime police in Bangalore, India have busted a fraudulent on-line job racket offering nurses jobs in the UK and arrested five persons including two Nigerians. The accused had cheated a nurse to the tune of Rs11 lakh by promising her a job at the Ealing Hospital there.

The nurse had responded to the email job offer at the Ealing hospital in UK by sending her CV and educational certificates. The accused subsequently got in touch with the victim on her telephone and asked her to remit money for anti-terrorism and drug trafficking safety certificates, WHO immunization insurance and skilled immigration permit certificates.

The victim remitted Rs 11,03,500 to different bank accounts as suggested provided by the accused before she realized she had been conned by the gang of fraudsters when she stopped getting responses from the accused.

Fraud #2 – Help a child in an Emergency situation

This is what I was talking about at the start of this article.

Just search for the term “relief India trust scam” and you will see how many people got a call from this so-called NGO claiming to raise money for medical treatment of some needy baby. I got a call myself 2-3 times, and every time I kept investigating the issue to understand how they work. When I enquired about their Registration number, they even gave me that, but then it’s not a big deal. You can always start an NRO with bad intention.

They were extremely pushy and didn’t have a lot of supportive information regarding their claim. There are many other scams going on in the name of helping someone. It can be on helping a poor girl education or for the treatment of a kid, who has no one in the family.

They even go to an extent of telling you that the baby is on the ventilator and the surgery is in the next 30 minutes. You often see this in train’s also where a lady comes with a pamphlet asking for help. I am seeing that same thing from last 30 yrs in sleeper class. Even I see the same thing on some buses.

Coming back to the online version of fraud Here is two such experience from this website

I don’t want to paint all the NGO’s with the same brush. There are many good NGO’s also, they are doing good work, but many NGO’s have sprouted up, only to take advantage of these kinds of situations and exploit emotions of people to make money.

Fraud #3 – I am calling from IRDA

This is a well-known scam these days. Almost every investor has some or the other kind of insurance policies, especially from LIC. So these fraudsters give a call to you and ask you about your policy and tell you that they are calling from IRDA and you are eligible for some bonus after many years and in order to get your bonus you will have to either send some money or buy some policy again.

A lot of times, they have some more details about you and your policy and they look genuine at times. And many investors fall for these scams. Here is an advertisement which cautions investor’s about it

You can also listen to some sample audio calls which was recorded by some investors. You can listen to them and see the tricks used by them to cheat and fool investors.

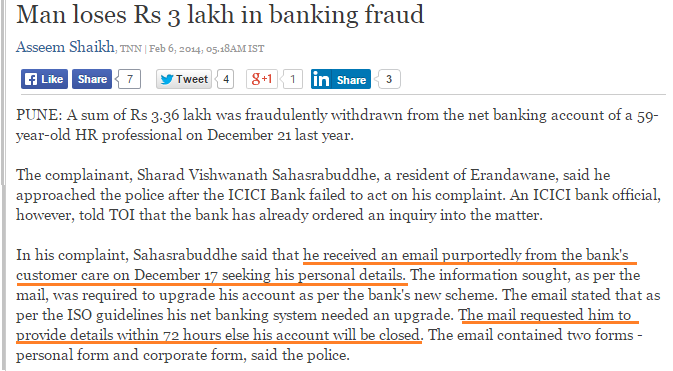

Fraud #4 – Verification Call from Bank using OTP

This might be a new thing for many investors. In this fraud, the target is generally uneducated investors who are not that much educated or who are very new to internet banking. The fraudster poses them as a bank verification officer and gets all the information like debit card number, expiry date, CVV number, and even OTP number while doing the online transaction parallelly.

This recently happened with one of my friend’s father who lives in Patna. His father was not that well versed with internet banking and used to do all his transactions in offline mode. So naturally, he was not aware of how the system works. One day he gets a call which goes like this

Fraudster : Hello , Mr PQR. I am XYZ calling from SBI bank . Your name is on our records who recently got a debit card. We are seeing some suspicious activity in your account recently, so this is a verification call to make sure that the debit card is in the actual account holder name.

Friends Dad : Oh ok .. What needs to be done to secure my account ?

Fraudster : Please verify your debit card number and the expiry date . It would be written on the card.

Friends Dad : (shares the numbers)

Fraudster : If you check on the back of card, there is a 3 digit number, its called CVV number. Please share it with me. Is it printed there ?

Friends Dad : Yes, its there .. Its 645

Fraudster : Ok , I have initiated the verification, I am now sending a 6 digit code to your registered mobile number, share that with me and then delete the sms. Please dont share it with anyone else

Friends Dad : Yea, I got it just now .. its 745523

Fraudster : Ok great , you will get a sms in sometime informing you about the verification success .. I am now disconnecting the call. Thanks for your time

Friends Dad : Thanks ..

( After 30 seconds …. there comes an sms )

"Dear Customer , Your Ac XXXXXXXXX567 is debited with INR 24,500 on 27th Apr .. Your available balance is INR 34,000"

The real story?

What happened in the background, is that the fraudster tried to make an online transaction on some website, which required a debit card number, expiry, and CVV number. After that, an OTP is required, which comes to the registered mobile number. Note that the modus operandi might deviate a bit, but the point is the same.

The fraudster tries to show himself as a bank verification officer and asks for all the details. I know you and I might quickly judge that this is a fraud call, but millions of people who are from a rural background or from past generations cannot.

Because first, they don’t understand the online world and the new way of banking which has come into the picture in the last 10 yrs and they are sometimes quite afraid of making a mistake. When they are told that their account is compromised and their money is at risk, they take wrong decisions in haste. Below is another real-life example of this kind of fraud

Hence, make sure you never share your card with anyone or share its details like CVV number of ATM pin. A lot of people do it in Restaurants and Petrol pumps. 99.9% of times, nothing happens, but we are talking about that 0.1% times when things can get nasty.

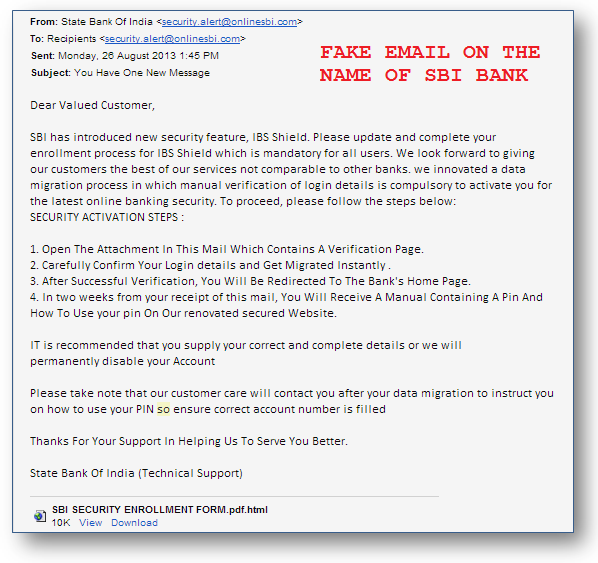

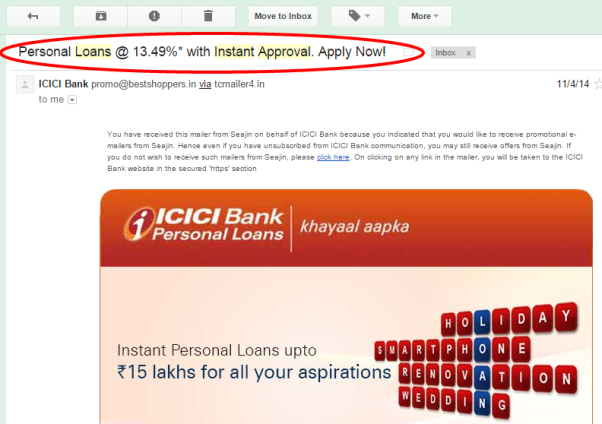

Fraud #5 – Please verify your bank details (Phishing)

It’s a very common kind of fraud in the online world. It’s called Phishing, which aims to steal your sensitive data like username, password or card details. You get an email asking you to verify your account or details, failing which your account will be closed.

When you click on the link, it takes you to the website which looks exactly similar to your bank or card company, you enter your details thinking that it’s your bank website only. But in reality, it’s a fraud website which captures your sensitive information, which later is used to do transactions and you lose the money. Below is a youtube video explaining how it works.

Here is an example of an email which I got on the name of SBI bank.

So make sure you do not fall for any kind of emails asking for your sensitive details like the password or PIN number. No bank asks for it ever.

Even I have received fraud call from a guy stating to be RBI Officer. He claimed that my bank account will be closed because it is not linked with my Aadhaar number. Fortunately, I recorded the call because I knew that he was trying to fool me so that he can know my card details. To win my trust he made his senior also talk to me.

How to prevent yourself from getting trapped in these situations?

From the last 10 yrs, this kind of online frauds has increased because the whole world has moved to the web and all kind of transactions are now online. It’s important to be attentive to your actions and with whom are you interacting.

You will never receive a phone from RBI or Other banks for reasons such an Aadhaar not linked etc.. Please be aware that if there is any recent activity such as if you have deposited some cheque then you might receive a call if bank officials want some information regarding the cheques. Otherwise, no calls from banks for any backdated activity.

Never share your card number, CVV number, OTP etc.. to anyone.

Download Truecaller in your phone. So if you receive a call from an unknown number who is asking your bank account details then you can check the number in Truecaller. Truecaller will tell you if this number is spam or not and if it shows to be spam then block the number.

Have you come across any other kind of online frauds other than listed above?

Have you ever dreamt of leaving your job and starting something on your own? Are you frustrated in your job and don’t see a future? If that’s the case, I am sure that, you must be excited by the thought of “being your own boss” someday. Hence, do read this article fully before you take any final decision.

Last year, when I wrote my own story of how I had quit my job and went full time working on this website, I saw that a lot of people were impressed with my story. Everyone said it was a brave decision. A lot of people could relate to my situation and said that even they are looking forward to quit their jobs sometime in future and jump into entrepreneurship.

Pursuing your passion and getting out of your boring corporate job is definitely an amazing experience. It gives you a great satisfaction, sense of achievement and can be extremely rewarding, but only if things go right.

But WAIT .. you know what !!

You probably don’t have much idea of the other side, the darker side and thats what I want you to read in this article.

“Pursuing your passion” is over-hyped

Yes, you heard it right!

I have realized that the positive side of entrepreneurship is often over-hyped. Surely there are many awesome things of being your own boss, but then there are challenges and issues involved, which are buried deep down in the entrepreneurship world, not openly shared or communicated in detail.

When you meet a young entrepreneur who left his well-paying job to pursue his passion, what do you see in his life? I am sure you must be seeing the freedom he has in his life, the exponential growth prospects, no boss to report to and the satisfaction on his face. Right ?

But you never see the problems, issues, challenges and frustration which arises out of being an entrepreneur. I know it very ‘cool’ to leave your job to pursue passion and it has created such a glorious image in the eyes of people, that majority of them want to try it out someday in their life. But remember the old saying …

“The grass looks more, greener on the other side”

5 side-effects of being an entrepreneur

I know how amazing it feels when you leave your job to pursue your dream. It’s an awesome feeling. I have done that and been there myself. There is growth prospects, freedom and sense of satisfaction and many other great points. But today we are not going to focus on that because you already know all that. Today, I want to share the darker side. I want to share the challenges and problems which a person faces in his entrepreneurial journey.

I have also contacted few business owners and asked them for their experience and real-life issues they are facing, which you will read below. It would be a great thing to be aware of these challenges, so that in future you can take an informed decision on what to do and which side you should move. So here we go ..

#1 – Be ready with the inconsistent income

The worst nightmare for a salaried person can be an unknown number getting credited in your account every month. When you are into a job, you get a number deposited in your account each month, not less not more. You know the date, you know the amount and you are clear that its going to come for sure.

Things like rent, EMI, household expenses, bills and many other things are already defined and dependent on your salary and for most of the people, they just can’t afford any cut in their salary because their monthly structure will fall like a pack of cards

When you are into your own work, a big problem is a variable income and this is more true in the starting years. Sometimes you get Rs 40,000 in a month and another month, it can be Rs 1 lac or nothing. Over time, this uncertainty goes down, as your work improves and your foundation gets strong. You slowly move to a more consistent income zone, but still the variability remains in the income.

A real life Experience

Amit Singh, who runs an IT company in Pune shared his real life experience of how he faced cash crunch at one point of time and how he felt about it

You will run out of money and unless you can handle the stress that will follow, you should not attempt to be an entrepreneur.

I will tell you my experience, in the initial days everything was as I had imagined, but then came a time when we had no projects for more then two months we run out of all our saved money, during that time the team I was counting on failed me, we had a very hard and stressful time, but it was ultimately my responsibility and blaming would not have solved the problem.

It took us six months to recover from that two months financial liabilities.

For most of us it’s long working hours and no holidays, for a long time you will not be able to take any vacation and you will be working for average 12-14 hours every day. You should also forget about work life balance, it will only be work.

#2 – You will doubt your decision many times

While a job has its own frustration, working on some venture also comes with its own set of psychological problems. You always wonder if you made the right decision or not, especially if your income is not as per your expectation or if you come across some challenge and that affects your business, you get many sleepless nights wondering if you took the right decision or not.

One of our readers, Rishikesh Sinha shared what he thinks about this point and he shared his thoughts and experience.

Sometimes when I feel low and analyse things around me in terms of monetary and relationships with people, including near and dear ones. I find, entrepreneurship is indeed tough and demanding. I don’t have enough money for disposal, to spend on things that brings happiness or comfort, though momentary it may be. Had I been an employee, atleast I could very well spend on necessary things without blinking an eyelid. But it is not in case of being an entrepreneur, a rupee spend has to be weighed upon. It seems the money I earn is not mine, it is of the customers.

This is about money. In case of relationships even, you find money plays a pivotal role. Being a brother, being a son, being a neighbour, being a husband, being a friend even, my monetary role — someway or other way — plays its role. And I find it hard to comply with all these roles. I see around, being an employee people have done what they could do the best with themselves. They are happy with no remorse.

Here I find, had I been an employee atleast I could have kept many people happy (if not all) in terms of monetary. People would have looked at me as a successful and resourceful person. But in case of entrepreneurship, since they don’t see money coming out of my pocket, my existence doesn’t count.

One more benefit, that I see being an employee is that he or she becomes the extension of the organisation. This is a great benefit as a person. You are being defined with your organisation. In case of entrepreneurship, it is not the case. You and your business are alone. You are always vulnerable to predators.

If one month goes bad, you start feeling tremors under your feet and it’s really very disturbing fact, because then you extrapolate that one bad month into distant future, and start thinking – “What if the whole year goes like this?”. Your imagination takes you to extreme possibilities and you are devastated. Job has its own challenges and doing your own work also brings its own set of challenges. The image below depicts it quite well.

Only after this has happened to you many times you overcome this feeling and stay relaxed.

#3 – Lack of focus in work

This point is one of my favorite. When I left job, I always thought that now, I am going to be my own boss, no one to disturb me and no one to questions me. I will focus all my energy and time in things which I love.

I was delighted and thought – “WOW – No one to monitor, no deadlines and no one to report to”

What an amazing situation it would be.

However, now after almost 4 yrs, I can assure you that my thinking was wrong. What seemed like a blessing turned out to be a curse. Because there was no one to monitor, and because there were no deadlines, things didn’t happen on time and the productivity went down. I didn’t report to someone, hence there was no one to push me to do things on time, I was my own boss and I always forgave myself for everything wrong I did.

When you are in job, you have a deadline, you have someone above you who will demand things and you are forced to focus on your work. But when you are on your own, its a big challenge to do things on time. The freedom comes at a big cost. I can start my work at 2 in afternoon and unless I have a great discipline, it affects my business. The above points are more true, if you have a home office kind of setup.

When you don’t have a boss or company tracking your progress, it’s easy to lose focus. Your freedom to do whatever you decide with your time will backfire if you don’t stick to a schedule and plan. Today, things like social media notifications can lead you down time-wasting rabbit holes.

So understand that when you are not into job, its really really tough to follow a 9-5 kind of schedule because it doesn’t exist at all and sometimes you wonder, if a strict timeline and someone yelling on you to be late was a blessing in disguise.

#4 – You can still be frustrated

It’s very much possible that in reality your plans might not workout as per your expectations. You had high energy and motivation when you begin, but then somewhere in between things start settling down and after a while, your whole excitement fizzles away and you get frustrated at your work and different things you have to deal with in life.

Hence, it’s very important that you carefully choose why you want to leave your job and start something on your own. Just because you hate your current job, can’t be a strong reason to quit. I suggest you to find a more stronger reason to quit, because boredom and frustration are part of any kind of work especially if you are not innovating after few years and you get into that cycle again.

A lot of people say “I hate my job” . But that alone cant be always a reason to follow your passion. Here is a comment made by a reader on this topic

But before quitting job just make sure that you are leaving your job because you reallyy passionate abt what you REALLY want to do or start. You simply love it..

It absolutely does not make sense that I hate my current job and that’s why I want to quit it. Always think why you hate your job. It’s because you lack somewhere or you are not having proper skill to do it otherwise you like your job. If that’s the case start working on areas where you are lacking (Comm skills, technical skills etc..)

I am also in Software field and in future my plan is to go in Education field because i think i can really make a difference there but before that i would like to make sure that i am really passionate abt it and i am working on it..

Just because you hate your current job, does not qualify as the reason for doing some business on your own because if your heart is not in that, you will again start hating it. One of my friend Nooresh Merani (appears on CNBC) does exactly that. He left his IT job to become a full time stock trader, not because he hated his job, but because he loved trading 🙂 . Below is his story in his own words ..

The biggest reason for an entrepreneur to become one is to love some work/hobby/ passion for which one is ready to make a lot of sacrifices.

So when i quit an IT job it was the love for being an advisor, trainer , trader and not because i hated my job. Well i loved the 6 months in that job as i was on bench and getting paid for having fun and also run the blog. The worst way to become an entrepreneur is to hate ur prev job.

A lot of entrepreneurs will talk about how when there is no revenue no income and working so much for it was a dark period. It makes all of us feel good as we have taken the other road. There is a tough part when you are doing good business , good income you have to make many more sacrifices as you are a boss 24/7 and not an employee 9-5.

So for example 2007 was equally tough for me in hindsight. As very rarely met my friends, sports reduced , had free tickets to ipl from friends ( he even took his barber ) and i could not make it for even one of the matches. Work was 24/7. Luckily i was single :).

Learnt from that and had a lot of fun in a lean period post 2008 where markets were sideways 😉 . An entrepreneur needs a support staff in his/her family as the toll comes on them for the sacrifices. Entrepreneurship is like another marriage where your wife ( if u have one ) ur mom/dad and friends accept your second wife.

For them to change , sacrifice is tougher.

One standard example – every entrepreneur needs capital/ raw material which can be intellectual, hard cash or money , technology. Also capital requirements are needed to for further growth. What you do not have ? Are you ready to stay on rent ? Are you ready to mortgage property ? Many tough questions.

You will not even get a home loan 🙂 or a car loan easily. I could stay on rent for 8 yrs because of support from parents and then my wife and in laws 🙂 i still do for comfort but have an own flat too.

I always remember these lines even if i plan to work for someone or myself. The monthly salary is one of the most harmful addictions and the only one which lets you live and not kill.

Nooresh has also done a nice presentation for those who love stock markets and wondering how to become a full time trader

#5 – Your work and life balance goes for a toss

When you get into your own work, the one big issue is that your work and life generally becomes one. Because now you are the boss. You sometimes work from home, you go to office sometimes, you might have few things to work on Sunday’s , early morning and round the clock few times.

The hardest part of being an entrepreneur is to draw a line between work and personal life. Especially those who started their journey before marriage, they will find it hard to balance the two life. Undoubtedly finding that balance is essential, as soon your personal life will start governing your professional life. Leaving the zone of being workaholic is not going to be an easy task, and here is one quote to help – “Family happiness is the ultimate reward for my hard work”

Success comes with a cost, and sometimes it’s too high. If your friends share the same vision or share the same bandwidth as yours, you will have no problem. If not, get ready to walk alone. Your friends will be supportive, will appreciate your work, but they won’t be there when you need to discuss an important idea or problem. Moreover, success begat loneliness, and when you move ahead in life, it would be harder to have new good friends.

The liberty of leaving your work as it is on friday evening, only to resume it back on monday morning is absent most of the times. You personal life gets affected due to this, because your family wants a separate time from you and they might find it frustrating that you are never completely out of your work.

Should you leave your job, even if you are earning a good enough salary ?

Given the kind of salaries some people are making these days, many a times I feel that one should work for few years even if they are not in love of their job and make some decent money and reach a milestone in their lives before plunging into entrepreneurship.

This is more true for sectors like Software, because I have seen some people making amazing salaries which is just not possible in first few years of struggle when you work on your own and given how important money has become in these times, I think its makes more sense (not always, but in most of the cases) to give some time with focus on making money only and acquire basic things in life first before you plunge to take risk

Example

One of our clients has just returned from Australia and is around 38 yrs old. He has been making good money from many years, and wanted to open his own restaurant in Pune and this thought was in his mind from the time he started working at age of 27. But the salary was too good to ignore. So he decided that for 10 yrs, he will focus all his energy into making money only and reach a milestone first. Today he has a flat with no EMI, a respectable bank balance and now he thinks, that it’s a better time to take the decision of leaving his job to pursue what he wants.

So if in your case, you need to decide if it makes sense to work a little more years only for the reason of making some more money and reach a situation which will allow you to take the decision of quitting you job more easily. Only you can decide that.

Entrepreneurship can be a very lonely world

I asked Ronak Hindhocha, one of my professional friends to share this views on this topic and what has been his experience and below is what he says

Entrepreneurship is a very lonely world unless you have a co-founder who totally understands your business. If not, it can be very difficult to build a team that can match up to a level where they start knowing what you go through day in and day out.

A lot of times, you’d feel like quitting. You can quit from inside but you can’t show it to the world. With each passing failure (whether big or small) things only get tough. To a point where you start questioning whether you’ve made the correct decision by venturing into the unknown.