Saving account numbers will soon be portable in India. Finance ministry is working on this from some time and soon you will be able to change your banks without changing your Bank account number. Saving account number portability will be almost similar to porting your mobile number to different network carrier.

Why people don’t change banks?

A lot of people do not change their banks because there is a lot of headache involved in the procedures. If you change your Bank from ICICI to HDFC, it means you have to change the account numbers at different places (for ex SIP ECS). Also you will have to close the ICICI account

and open a new account in HDFC which means repeating the procedure all over again. These tasks stop people from taking action of moving from one bank to another. However with saving account number portability, you will be able to change your Bank account from bank A to bank B with less paper-work. The procedure is expected to be small as the KYC norms will also be taken care and no there will be no change in the Account Number.

Recently, with the Savings bank rates deregulation and NRE/NRO deposits deregulation has resulted in many banks increasing their saving bank interest rate to 6-7% (example YES BANK and KOTAK bank) and a lot of banks increased their NRE/NRO deposits rates from 3-3.5% to 8-9%, however a lot of people have not considered to change their banks just because of the WORK involved in the opening of new bank account. If saving account number becomes portable then a lot of people might have considered doing this.

Implementation of Saving account portability is a big task!

However this idea looks great to a lot of people, the whole idea of portability is not that easy and there are several challenges in this process. Those are

Renumbering the 500 million bank accounts – There is approx 500 million saving bank accounts in India and these account numbers are 12, 13 or 14 digits account numbers in most of the cases where the first few numbers are for branch code . Now the first task before portability is achieved is that all these account numbers will have to be renumbered and there has to be same format for these. So that your account number after changing the bank is still same. Now how will this be achieved? How much realistic this is and how investors will be able to accommodate this part in their banking life.

Different banks having their own KYC rules – At the time of opening a saving bank account with a bank, it has its own procedure and documentation and they feel that they do the best job in that. When portability comes into picture, there has to be same kind of KYC norms with all the banks and they should feel confident about it, as they would not like to rely upon others KYC. This part would be rather challenging.

Do you feel you need this saving account number portability or is it a stupid idea ?

Did you come across many errors in cibil report of your ? Was there any kind of mistake in cibil report ? Are you wondering how to clear yourself out of CIBIL defaulter list? Is your name in cibil defaulters ? In this article you will see what can be done to Correct the errors in CIBIL Report and remove your name from cibil ? Firstly let’s understand the type of errors that can be on your CIBIL report. Before that, the first thing you need to do , apply for your CIBIL Credit Report Online

1. Errors in CIBIL Report

Banks keep on updating CIBIL about your credit behaviour on monthly basis. So, at the time of entering some data, it might happen that some human error happens. Even though these are human mistakes, still they are responsible and correctly blamed for a lot of complaints. Let me give you an example – Suppose your outstanding credit was Rs 2,000, but accidentally it was entered as Rs 20,000. Similarly, there can be various things which can get wrong:-

Account/ Loan Type

Account Status

Ownership Type

Date of Last Payment

Date Opened

Date Closed

Sanctioned Amount/ High Credit

Current Balance

Amount Overdue

DPD/ Asset Classification

Remember that each of these little things are very important and different banks can have different criteria and weightage on a particular thing. So getting each thing right is very important for your future loans. Make sure you have them corrected.

2. Mistakes in your Basic details like Name , Address , Date of Birth

There can be at times mistakes in basic details like Name, address, Date of Birth etc… For Example, in my CIBIL report, my name “Manish Chauhan”, can be misspelt as “Manish Chavan” (like all the people in Pune do when they write my name). So if name is misspelt as “Manish Chavan” and tomorrow some real “Manish Chavan” runs away after taking Rs 50, 00,000 home loans, with help of human error, there are chances that this impacts me. Don’t take it lightly incase your name or any other detail is incorrect. The full list of details is as follows

Name

Date of Birth

Gender

Income Tax ID

Passport Number

Voter’s ID

Telephone Numbers

Address

State

PIN

3. Something Does not Belong to you or Has Duplicate Entry

At times you will see things which do not belong to you, it comes into the category of “human error” or actually it might be on your name, just that you are not aware of it, this might happen if your documents are misused by some other person. This happens and has happened with lot of people. So take this seriously. Note that you might not see a recent update in your CIBIL report if you have applied for a CIBIL report within 45 days of a transaction. It takes time to update it in CIBIL report.

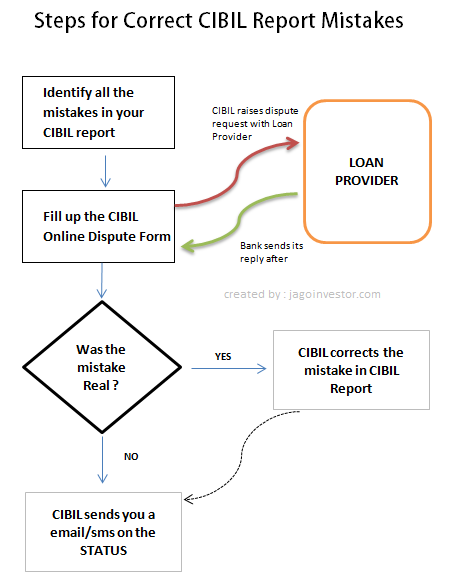

How to Correct your CIBIL report

Cibil has an online redressal mechanism for handling the mistakes in CIBIL Credit Report or to correct errors in cibil report, which is called “Dispute Resolution” .

Step 1 : Fill up a Dispute Resolution form

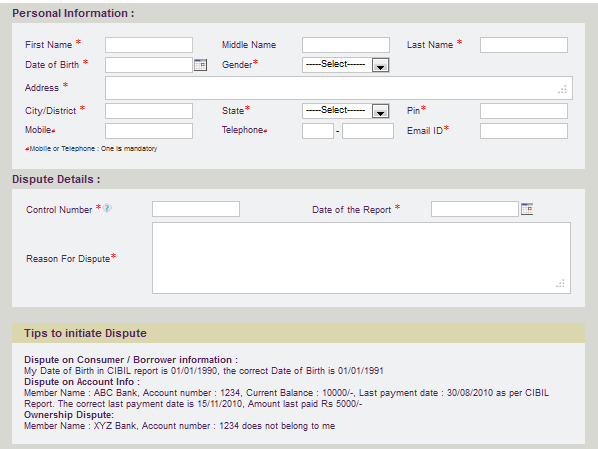

The first step is to fill up this CIBIL Online Dispute Resolution Form. Make sure you put all the information correctly. There is something called as CONTROL NUMBER which you will find in your CIR report, you have put fill this control number in this dispute form along with other details. You will also have to give them the exact mistake and the correct information. The Control Number is a unique 9-digit number found on the top right hand side of your CIBIL Credit Information Report and is generated every time a credit report is generated. Once you submit the form, you will be given a Dispute ID which you can use for future references. This Dispute id will also be emailed to you. The dispute resolution form looks like this

Step 2 : CIBIL communicated to Loan Provider to confirm Detail

Once you raise a Dispute request, CIBIL first tries to see if it can verify and rectify the details on its own but incase its unable to do so (which will be the case most of the times) it will then forward your dispute request to the loan provider (the bank which issued you credit card, home loan, car loan etc). Once the loan provider confirms that there is an error it will provide CIBIL with corrected data. CIBIL then updates the data and informs you as appropriate. Always remember, it is the duty of CIBIL to help you resolve your request.

Please remember that CIBIL does not make changes to any information on its own. It is only a custodian of information received from credit institutions. CIBIL is permitted to make changes to your credit information only when it is confirmed by the relevant loan provider(s).You will receive an email notification informing of the results for the dispute requested. It takes approximately 30 days to resolve a dispute request. Once the dispute is resolved, you can see the status of your CIBIL report by applying to it all over again. A lot of people wish if they could have a CIBIL Login and Password where they can view their report whenever they want. But that won’t happen soon

I hope you have got a clear idea on what to do when there are mistakes in your CIBIL report and you want to correct them. Just follow the steps suggested and you should be able to correct the errors in cibil report of yours and get out of CIBIL defaulter list !

I am happy to break the news today about my first upcoming book on personal finance called “Jago Investor” (The name of the book is changed now and its now called “16 Personal Finance Principles Every Investor Should Know“) with CNBC Network 18. It has been a long time I was waiting for this to be out in the market, but finally I got a go ahead to break the news to my blog readers. No, the book is not in talks – It’s going to hit the market (soon) this month itself. So you just have to wait for couple of more days to grab your copy.

OLD NAME & COVER PAGE

NEW UPDATED BOOK WITH CHANGED NAME

Some time in early 2010

I got a mail from CNBC sometime in 2010 about authoring a book on personal finance and I happily agreed. Since then I worked on the book, I was in Bangalore that time working with YAHOO (yea guys – I was an IT guy) and then I moved to Pune to start on my own. I worked on the book in last 1.5 yrs and now it’s complete.

The Vision of Jagoinvestor Book

It was a tough task to select what the book should be all about – but I was sure that it should not be a typical book . It should not be a book which does not leave an impact on someone who reads it. I wanted to make sure that a person who reads the book really introspects about his financial life. I wanted the book to make a person shake a bit after reading it. So the book had to awake a person reading it and make him feel “Now, I should do something for my financial life”. With that vision I have written the book. It’s about the principles of personal finance and how a person should think in different areas of financial life. I will it becomes one of the best personal finance book in India.

The book is not about financial products and how they work – NO! You can get it anywhere. I have talked about very important things which really matter. It works on your thinking level and makes you think in a more quality way rather than just increasing your knowledge. I have tried my best to keep the language simple along with numerous examples and images/tables to convey the concept. I have written this book considering myself as the reader. There is another version of this book which comes with a CD which contains 13 financial calculators and 2-3 templates.

Now let me introduce you to the book contents in crisp and short points.

Chapter 1

This chapter talks about early investing and how you lose a lot of wealth just because you don’t start your wealth creation on time. I have shown numerous examples/graphs which will give a clear idea on how powerful early investing can be.

Chapter 2

The second chapter talks about the protection of your family (Life Insurance). It also shows you right way of finding the required cover and how much your current cover will be able to sustain your loved ones. While this might look like “products talk” It’s actually not!.

Chapter 3

The 3rd chapter is all about Goals setting and how your should look at it . How goal based/linked investing can do better for you and improve your financial life style.

Chapter 4

This chapter clears the myth people have about equity and debt in general. It shows you reasoning/proof about how equity is not risky in long-term and how debt is extremely risky in long-term.

Chapter 5

This chapter talks mostly on the psychological aspects of your financial thinking and how your decisions are shaped up because of the way you think about money. This chapter has been contributed mostly by Nandish and he has really done amazing work.

Chapter 6

This chapter talks about how you can make your financial life more simple and robust using some simple rearrangements. This is mostly overlooked by indian investors who focus a lot on returns only.

Chapter 7

This chapter ends the book and it talks about 10 commandants you should incorporate in your financial life to make sure you become a better investor.

Thanks to you

If I had to thank only one person who made this book a success, it would be you. From past 4 yrs you have bombarded me with your doubts/questions and this has only made me learn and learn. This book does not belong to me alone its creation of this whole community and each one of you who is part of this blog from several years now. It did not take shape just in a day – it happened over years – slowly and gradually. I would like to say Thanks to you all for believing in jagoinvestor and really making it happen. We have a lot of things coming up in 2012 and our commitment is to give you guys more and more with each passing day.

“No” is one of the non-complicated word – Simply two letters. Yet saying “No” out loud is hard for most people. Welcome to the world of personal finance where saying NO is tough and 90% of the people reading this blog might have a messed up financial life because of a single reason that they didn’t say NO to a lot of things. Let’s start with my favourite ‘Life Insurance’. Almost everyone I have interacted with, had/have a sad story of some uncle selling him (wait wait …. the correct word is ‘forced him’) to buy a life insurance plan because he had to complete his target or his job was at danger or because he was trying to sell life time product. Saying ‘NO’ was not an option because ‘it won’t look good’ (I am sure it looks amazing right now).

“Yaar – Can you help my brother as he needs a car loan. Can you guarantee his loan, they want someone from the city itself and could you just give your PAN Card to my brother? As it is part of the procedure, kuch hota wota nahi hai ” . You can’t say NO. Months and years pass on … Friend’s brother loses job, can’t pay the EMI and obviously you are the defaulter now! Your home loan, car loan, credit card all kind of applications are getting Rejected. Either live with this situation or pay the balance Rs 4 lacs. This is the cost of avoiding a NO.

Are equity markets risky for you? And you want a equity + insurance product bundled which gives tax benefit and also gives benefit of rebalancing on its own, but you want guaranteed returns? Welcome to the world of “Highest NAV products“. Now you get highest NAV (but we will decide how the highest NAV is controlled… he ha he).

Wait… but it would be amazing if I can buy at the lowest NAV product. Arre no problem sir, jaan bhi haazir hai. Just close your eyes give me 10 min… zoom! Lowest NAV ULIP is here! Anything else? Now please don’t say NO. We did whatever you wanted, please be kind and don’t be so rude, please write a cheque. What? I can’t invest lot of money in one go… Ok then, we have a monthly investment option available. We can try every weekly too if you want.

Inventions in SIP and Insurance

There are “inventions” in SIP … SIP in Stocks (It does not work, think why) , weekly SIPs, daily SIPs, minute SIPs… we will extract the rupee cost averaging concept… Normal SIP, Flexible SIP, increasing SIP, decreasing SIP – They can read your mind.

People were scared of ‘Term Insurance plan’ about it not giving back the money paid as premiums – so let’s introduce Return of Premium Term insurance plan, now no one can say ‘NO’! We are giving insurance money if you die and your premiums back incase you live for the term of the insurance… what else you will want to say YES? Please be human and take it. I hope you are getting what I am trying to say – The more options we have, the more we believe that we need it. You need to learn to control your decisions and say ‘NO’ to most of the things. There are minimal options which you need and keep things extremely simple.

There is no reason in this whole world to have 10 insurance policies. There is no reason to have 15+ mutual funds in your portfolio. There is no reason to have try to beat the markets with direct stocks if you don’t know the rules of the game in equity markets or you are trying to learn the game of equities or have a past record of beating mutual funds or even index returns. There is no reason to have different kind of policies. There is absolutely no reason to own more than 2 credit cards.

There is no reason to have more than 2-3 Health Insurance products & overall there is no need to have savings account in so many banks unless you have extra cash to pay for the bank charges. However almost every portfolio we come across, we how there are many area’s where investors went shopping with craze at some point of their financial life . I have seen 45 insurance policies (yes , LIC policies) , 100 Mutual Funds in a portfolio (I really suspect the guy thought they are SHARES) , 12 health insurance plans , 8 credit cards with a close friend, and one of my relative with 7-10 bank accounts (with that attitude of “arre Rs 500 pada hai account me , rehne do, ja hi kya raha hai)

So what you need to do?

If you want a fairly simple financial life, all you need to have is:

4-5 good equity diversified mutual funds or balanced funds

1-2 term plan

1 health insurance product

1 credit card

1-2 bank accounts

Financial Discipline to say ‘NO’ to what you don’t need

We said No at wrong places

Now just like we didn’t say No at wrong places, we have said NO many times at right places. When we met an agent who was not ready to share his commissions in exchange of authentic and right advice, we said NO, we don’t want you. When we meet an advisor who didn’t give us discount on his fees but was a high quality advisor, we said NO, we won’t need people like you. When we wanted to go to a workshop or seminar on finance & money and we came to know that its PAID seminar, we said – Kya faaida – NO we don’t want to come.

I want to take this message very strongly in 2012 start and follow it though out your life – You don’t need to do a lot of advanced things in your financial life, provided you do not make a lot of mistakes and are ready to keep things simple and an attitude to say NO to fancy and complicated things in life . Thais the conclusion of this article. Also I am going to break a very good and big news to all readers in few days. Any guess ?

I got an interesting question in my mail box – “Can you please coach me on How can I overcome my casual approach towards my finances and live a good financial life?”

The thing is that deep down we already know how to live a good financial life; the issue is that we are somewhere unwilling to take the required actions. Personal finance is not a rocket science; it simply has some hand full of things that you need to do. It is not about “How to” live a good financial life; it is a matter of choosing wisely and to make commitments to the actions that are required.

Someday I am going to sit with my advisor and sort out my finances,

Someday I will go for financial planning,

Someday I will do something with the idle cash that I have

Someday I will alter my investment style

Someday I will buy a term plan

Someday I will increase my investments

Someday I am going to buy my own house

Someday I am going to complete all my pending actions

Someday I will read all the nice articles that are starred in my inbox

Someday I am going to read entire article archive of Manish

And Someday I am going to organize my finances?

Give me two days and I will show you what I can do with my finances. This Someday syndrome always keeps you away from wealth creation in life. I re-collect a line from a famous movie Day and Knight “Someday. That’s a dangerous word. It’s really just a code for never” .

The code to your financial success is in your hands. Today you can choose to bring a dramatic change in the way you live your financial life. What you choose today determines the quality of your financial future. The “Someday investor” is all about hoping, wishing, desiring and wanting things to happen in his/her financial life. The truth is this really does not serve you in your financial life.

Once an old Cherokee is teaching his grandson about life –

A fight is going on inside me, he said to the boy. It is a terrible fight and it is between two wolves. One is evil – he is anger, envy, sorrow, regret, greed, arrogance, self-pity, guilt, resentment, inferiority, lies, false pride, superiority, and ego. The other is good – he is joy, peace, love, hope, serenity, humility, kindness, benevolence, empathy, generosity, truth, compassion, and faith.

This same fight is going on inside you – and inside every other person, too. The grandson thought about it for a minute and then asked his grandfather, which wolf will win? The old Cherokee simply replied, the one you feed.

What are you feeding your financial life? – “specific actions or someday actions”. Specific is being committed, someday is being casual. When you make a choice to be in action you gain leverage over other investors. The more specific you are in defining your actions the better your financial life gets. Keep feeding your commitments. Keep choosing. Keep taking actions. This blog is your sacred space, it is for you to add different dimensions to your financial life, if some conversations trigger new thoughts or actions than allow that action to happen and don’t forget to share your actions with us. Leave your questions in comments section and we will try to incorporate them in future articles.

Lastly 2011 is about to close its doors, why don’t we take this opportunity to lock our “someday” behind the doors of 2011 and step forward with commitment in our hearts. Wish you all a very prosperous 2012.

This post was written by Nandish and this post was taken from our finacial coaching blog where we keep on writing these kind of coaching conversations from time to time.

What are the different types of loans you can take in India ? Do you always think about Personal loan when you want a loan? A lot of people despite having different kind of assets go for personal loan even if they have other options where they can mortgage an existing asset and take a loan at lower interest rate. In this article I will give you 5 alternatives to personal loans and tell you a little bit about each.

Before we move forward let us understand a basic rule of lending. There are two kind of loans , Secured Loan and Unsecured Loan. Secured loan is a loan where a lender has access to some kind of asset so that incase you run away, he can liquidate the asset and take his full or partial money back, as there is a sense of security in secured loans, you have to pay a lower rate of interest on these loans. However an Unsecured loan is a loan where the lender has no access to any asset and incase you run away, bank has no way to get back that loan , that’s the reason you have to pay very high interest rates on these loans, Personal loan and credit card are examples of these loans. The biggest reason why someone should go for these alternative loans is that the processing of these loans are much faster and better interest rates compared to a personal loan. So now lets see some alternatives to personal loan incase you posses an asset.

1. Loan against Gold

Lets me start with the best option to take a secured loan in India. You can pledge your Gold jewellery and take a loan from Banks and companies like Muthoot Finance or Mannapuram Gold. The best thing about gold loan is that the processing is extremely fast (from few hours to 2-3 days) depending on your case. The way it works in Gold loan is like this – The higher the margin of safety you leave , the lower the interest rate. Here is an example , if you have gold worth Rs 10 lacs and you are ready to pledge it for a loan of just 5 lacs, then you are leaving a comfortable margin of Rs 5 lacs for Bank (incase you run away or gold prices decline) . So in this case you will get a very good interest rate offer , but if you take a loan which is 80% or 90% of the worth , then you will be asked for a very high interest rate. Generally the interest rate asked is between 12% – 15% .

There are no pre-processing charges or too much documentation involved in gold loan, in most of the cases the only thing required is your address and id proof. that’s all and you can get a loan within 24 hours easily .

2. Loan against your Insurance Policies (LIC/SBI)

Lets talk about LIC policies here. You can also get a loan on your LIC policy incase its eligible for loan (most of them are) . But to get loan on your LIC policy, it should have a SURRENDER VALUE, which happens only after payment of 3 yearly premiums. Only after that you can avail for a loan which would be around 90% of Surrender Value. Lets see an example – Ajay has a LIC endowment policy which has a yearly premium of Rs 50,000 . He has paid 10 years premium (total 5 lac) , the surrender value of his LIC policy is around 3 lacs at the moment. So he can get a loan of around 2.7 lacs.

One can take a loan either from LIC itself (recommended) or from banks, for which they will have to pledge their LIC policy totally to them. So incase they are not able to pay the loan, their LIC policy will be surrendered and company will take their money back. The best part of these loans is that you get it only at an interest rate of 9-10%. So if you have a LIC policy and it has a respectable Surrender Value , then you can take Loan against these policies and not take personal loan which has hefty interest rates. Check the loan amount available on your LIC policy by just sending this SMS – ASKLICYOUR-POLICY-NUMBER LOAN to 56677

3. Loan against Fixed deposits

Incase you have a Fixed Deposit for long-term and would not like to break it in times of emergency, you always have an option to take a loan against that Fixed Deposit. The interest rate you will have to pay on that loan should be 1-2% higher than the interest rate earned on the FD and the loan amount available to you would be around 75% – 80% of the FD current Worth. For an example – suppose you have a FD which has its current worth at 10 lacs and you are earning 10% on that FD , then you can get around 8 lacs of loan at 12% interest rate . This is one good option incase you do not want to break the FD and also want to take a loan.

4. Loan against Property

You can also take loan against your property (Residential and Commercial) . Banks give loan upto 50% of market value of the property or 30-40 times your monthly income . The interest rate charges is in range of 13-16% depending on how big the loan is and how much margin you can leave. Loan against property is generally recommended for those who want a big amount as loan for purposes like expansion of business, wedding or some big-ticket expenses. Incase you need just 2-3 lacs of loan then it’s not recommended.

There can be processing and prepayment charges in these loan against properties (LAP) . A good place to compare the loans against property is policybazaar page . Public sectors banks like Bank of Baroda, SBI banks are known to not charge the prepayment penalties and have lower processing charges . All the loans against property comes at FIXED interest rates.

5. Loan against Other investments

Shares and Mutual Funds – There are loans offered against Mutual Funds and Shares , but there is a list of approved Funds and Shares which can get loan, also as the values of shares and mutual funds are highly volatile, there is high level of margin required on it , Means that if you have shares worth Rs 10 lacs , the amount of loan you can get is much lower than 10 lacs.

Public Provident Fund – You can get loan on your PPF account also , but there are some restrictions , you can only get loan from the 3rd year to the 6th year and the amount of loan will be only 25% of the balance in the account 2 yrs back . For example – If you want to take the loan in 5th year after opening your PPF account , then you will only get loan of 25% of the balance in 3rd year , if the balance was just Rs 2,00,00 in 3rd year, then you can only take loan of Rs 50,000 .

So I hope you have got a clear understanding of what options do you have incase you want to take loan against your assets. Note that the lower interest rates are one of the reasons why you should go for these alternative loans, but the bigger reason can be fast processing of these loans in case of emergencies.

Do you want to invest in your Public Provident Fund (PPF) account online without going to the bank physically? If YES, then there is a good news for you. You can transfer money to your Public Provident Fund Online netbanking. Whatever we are going to talk in this article is applicable to Public Provident fund in State bank of India. If you have a PPF account in post office of other banks , then first you will have to transfer your PPF account to SBI and then you can add your PPF account to your bank account as beneficiary and then transfer the money to PPF account anytime with a click ! .

Please note that this online transfer is possible only if the PPF account is at SBI , if it is opened at Post Office , then it would not be possible, because only SBI is authorised to get online payments for PPF. Many people have their PPF , spouse PPF and children PPF account, they can add any number of PPF accounts for online payment.

Steps for Online Transfer in PPF account

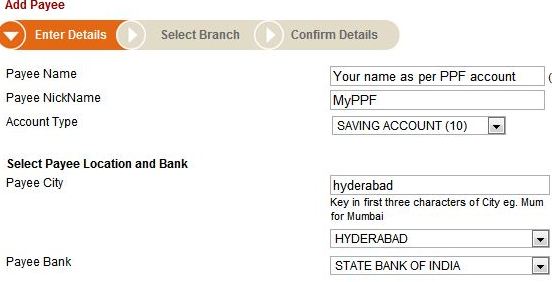

Step 1 : Add Public Provident Fund account as Beneficiary Account

The first step is to add your PPF account to your Bank account as third-party so that you can do a money transfer to them. I am using ICICI account screenshots, but all the steps must be same for other banks also.

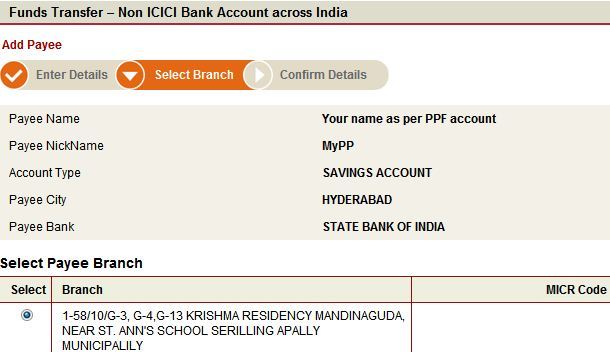

Step 2 : Choose the SBI branch Address

Next step is to choose the exact location of the BANK where the account was open . Note that if you opened a PPF account at a SBI branch where netbanking is not available , it will not be listed.

The best thing about have the bank account and PPF account linked is that you can also view the PPF details and balance at a single place .

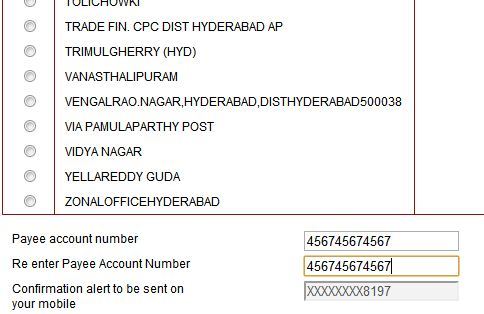

Step 3 : Add your PPF account as the Payee Account number

The last step is to add your PPF account as the Payee Account number and then click on the confirmation link . In ICICI you will first get an activation code which you will have to put to activate the account for first time .

Once you have completed these 3 steps you can see your PPF account as the 3rd party account where you can transfer the money just like you send it to any account.

Steps for State Bank of India (SBI)

Option 1 : If your PPF account and Bank account is at same branch

Incase you have your PPF account and SBI bank at the same branch, then you can see your PPF account already linked with your Bank account and you can transfer the money. Prasoon shares his personal experience

I already had an account in SBI, New Delhi. I went to SBI, Hyderabad for opening a PPF account. They asked for existing SBI account number, which I provided. Also, I submitted PAN card and Bank statement copy as proof documents. It took some 15-20 minutes to get a PPF passbook.

Now a pleasant surprise –

When I came back home and logged with my saving account user ID, I was able to see my PPF account under account section. I was able to see transaction I have done till then.

Also, there is no need to add PPF account as Third Party in this case. As the PPF account appears as separate account, I can transfer amount using fund transfer (not third-party transfer). Good thing is that, this transaction is real-time and the PPF account gets updated at the same time. Also, I am able to download statements, just like with normal account.

If you are not able to see the PPF account as “linked account” , then call customer care and ask them to activate it, if that does not work , then try to add your PPF account as the beneficiary account like I explained above . If even that does not work then try to go to your branch and then ask them to link the account to your bank account.

Option 2 : If your PPF account and Bank account are NOT at same branch

If your SBI Bank account and PPF account are not in same branch/city , then as the first step you can try to add your PPF account to your Bank account as third-party to do a money transfer. If that does not work then you can go to your Branch and ask them to link your PPF account to your bank account . Mostly this should work.

Netbanking works with all the Banks

As of now we know that this online transfer is working with ICICI , SBI , IDBI , Bank Of Baroda , IDBI bak, Union Bank of India . So with this information we can conclude that any bank which supports NEFT transaction can be used to transfer the money to SBI PPF account, by adding it as third party beneficiary. Let us know if this works for you.

But your Public Provident Fund account is not in SBI ?

Incase your PPF account is with Post Office or a non-SBI bank ,then may be its a great time to transfer your PPF account to SBI account ,all you need to do is submit a form for transfer of your PPF account. It will be one time task , so do it .

How to claim tax benefits

If you transfer the money to your PPF account online then you can do two things . First is to get your PPF passbook updated at your branch about the money transfer , you will get the PPF passbook updated and show it as your proof for claiming tax benefits. The other thing you can do is take the print out of your bank statement which will show the credit of the money to your PPF account. I am not sure but may be this is possible with SBI bank only . You can use this statement as proof to claim tax benefit.

NRI’s should make use of this online transfer facility

I think the best use of this facility can be made by NRI’s , who are already have a Public Provident Fund account , but could not go to bank branch to invest in PPF and waiting for information like this.

Just try this option with Rs 500

If you are wondering if this whole netbanking will work or not , I can tell you that there are countless number of investors already doing this and I am sure you will hear from other fellow readers that they are already doing this. It would be a great idea to test this by adding your PPF account and then test a transfer of Rs 500 and confirm once that it really got transferred .

Where you looking for information like this ? Will you test this with your Public provident Fund account and do a test transfer ! , please update your comments about it in comments section .

Thanks to Jayaprakash for sending me these screenshots and also confirming that he was able to transfer money from his ICICI bank to his PPF account.

This article will teach you how to apply for your cibil report online . Some months back, I had written an article on CIBIL report which was well taken. A lot of readers applied for CIBIL score and were shocked to see their CIBIL report was messed up because of some past sin committed in area of credit card, home loans, personal loans. A lot of you applied for CIBIL report which took some time, energy and lot of commitment, but majority of readers didn’t take any action and just told themselves “I will apply soon” .. that “soon” never happened and seems like CIBIL heard your prayers. CIBIL scores are now available online. Fill a form and make the online payment in 10 minutes, authenticate some questions and get your CIBIL score online in your email in next 4 days ! . I applied for my personal CIBIL score and I got it in just 2 days in my email . My score was 835 ! . yippee !

Procedure to get your CIBIL report online

Note that you can only get your CIBIL TransUnion Score (Including CIR) by paying Rs 450. You cant get CIR alone .

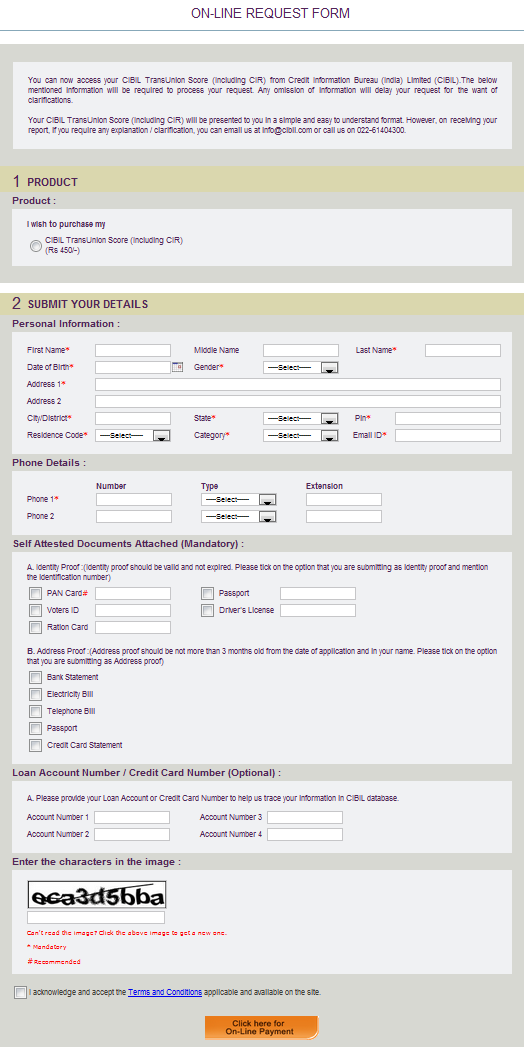

1. Fill up the online form

The first step is to fill up a form online here . It asks Name, address, Phone details along with Identity and address proof. At the end it would ask your Loan account number (credit card number in case of credit card) . Make sure you fill up the form correctly and also double-check that you are putting correct address, identity proof related number like PAN number , Passport number etc. Once you are done with this step, you move to step two, which is payment online.

2. Make an online Payment

Once you have filled up the form, and click on “Make Payment” button, you will be redirected to the payment gateway where you can make the payment of Rs 450 by credit card, NetBanking or other ways . I would suggest making a payment using net banking , because I used credit card option myself two times and it failed , but with Net banking option, I didn’t face any issue.

Make sure you do not close the page after making the payment, it will redirect you to a CIBIL page where the 3rd step will be performed. Note that before you move to 3rd step , you will get an IDENTIFICATION ID number , please make sure you note it down properly.

Tip : The reason why we keep getting transaction failures (with payments getting deducted) is because of the way the CIBIL website handles cookies. Its always better to clear off everything in your browser before attempting to pay for your report. I found this the hard way after my payments were deducted a couple of times (1 refunded and 1 waiting for refund). Thanks to Vijay for this finding

3. Authentication

Now from security point of view, now you will have to answer 3 questions which would be related to your credit history. Once you answer these questions, your authentication will be successful and you will get your CIBIL score card in your email in next 4 days. You will get this message once authentication is successful

We will e-mail your CIBIL TransUnion Score (Including CIR) within 4 business days*. The On-Line Payment Confirmation is emailed for your record. For any queries on the status of your request, you can write to us with your Transaction Id at [email protected] after 4 business days.

You will get a receipt of payment which you can print right away and you will also get an email with PDF copy of your payment and other details.

What if authentication fails ?

Incase the authentication step fails while applying for cibil report online, don’t worry .. all you need to do is take the print out of the payment receipt (you get it in email also) , self attested photo copies of the required documents (identity and address proof) which you had put in the form in the start , and send it to CIBIL address. You should get back your CIBIL score in next 10 days.

Documents Required & CIBIL address

1. Online Payment Confirmation

2. Identity Proof – PAN / Passport / Voter’s id (Identity proof should be valid and not expired)

3. Address Proof – Bank Statement / Electricity Bill / Telephone Bill / Passport / Credit Card Statement (Address proof should be not more than 3 months from the date of application and should be in your name)

Address

Consumer Relations – Disclosure Request,

Credit Information Bureau (India) Limited, Hoechst House, 6th Floor, 193,

Backbay Reclamation, Nariman Point, Mumbai 400 021.

Data Security ?

While CIBIL says that the whole process to apply for cibil report online is secure and there has been rigorous testing, I personally realised that it’s not 100% secure. First the email id where you want to order the CIBIL score can be any email id , all i need to know is your important documents numbers and your credit history and some numbers , which I feel a lot of people share with their close friends and relatives sometimes . So the real security would happen when you do not disclose your credit related data to anyone .

In last few months we have seen that there have been many complaints from hundreds of people on how they could not get a loan because of their low CIBIL score or some bad past record . Banks are seriously looking at these scores now and make sure you at least have a look at your CIBIL score once . So if you have any credit card or loan , you should apply for CIBIL score and have a look at it.

Try out ordering your CIBIL report online and let me know if you were successful or not . Also share your experience with CIBIL in comments section.

Did you ever know someone who met with an accident and he was the main bread-winner of the family? Mostly yes. A personal Accident Insurance plan is policies that cover a person from accidental death, accidental disability and several other features. There can be very bad consequences of meeting an accident like death or pause in income, ranging from a few weeks, months to even years.

A term plan can only help in death and a health plan can help in case you are hospitalized, some of these policies also offer accidental riders, but these riders are not as comprehensive as standalone Personal Accident Insurance policies have. In these articles, let’s see the benefits and features of Personal Accident Insurance policies.

Ajay was one of the best employees of his company based in Bangalore . He bought a term plan as soon as he realised the important of securing his life. He also bought a health coverage to secure his wealth (not health). He had recently bought a home through loan and he was also investing for his 2 kids future . Ajay was the only one earning in his family which also had his mother as dependent on him.

It was the last working day of the week just before Diwali holidays and he had to rush home early that day. He was as attentive while driving as he was always, but he forgot that accident happens not because you are careless , but because other can be damn careless … While Ajay was taking a u-turn another car slammed into his car which was coming with a lot of speed.

It was a serious accident and what Ajay never imagined happened ! . Both of his hands were non functional after the accident . Being a senior programmer in his company, he knew that his future is lost now . This one incident changed him life. While his income stopped, his expenses at the house, EMI etc had to still continue.

His term plan could not pay him because he was not dead. His health insurance plan covered the expenses for hospitalization, but only covered for a basic amount incase there was a temporary disablement. But Ajay case was not covered in any of his existing insurance policies. At this point in time, if Ajay had a Personal Accident Insurance Policy, it might have helped him a lot.

If you are a reader of this blog. Most probably you must be living in a big city, most probably you are salaried class and obviously you must be travelling from home to office and office to home, you will do it every day, for months and years .. that would be thousands of days. The chances of death or getting hospitalized for some illness is far lower than the chances of meeting an accident these days. So in today’s world more than a Life Insurance and Health Insurance, the first thing which you need is an accidental insurance policy and why not. Its costs so less that one can afford it very easily. You can buy a 10 lacs accidental cover anywhere from Rs 800 to Rs 1,500 per year depending on the company and benefits. But one thing is sure that it’s very cheap.

what a Personal Accident Insurance policy gives you?

Think for a moment, what all can happen if one meets an accident, what can happen, what are different kinds of end results of it? An Personal Accident Insurance policy covers almost all of them. Below is a table that gives you an idea of what kind of situations are covered by accidental policies.

1. Death

In case of a death due to accident, the policy would pay 100% Sum Assured to the nominee. Some companies also pay a “Children?s Education Bonus” of 5000 or 10000 for a maximum of 2 children.

2. Permanent Total Disablement

This means that in case there is a permanent total disability, in which a person is disabled for life, the SUM assured is paid to the person. Some companies also pay around 125% or 110 %, depending on the company. Example – Loss of

both hands or both feet

one hand and one foot

one (hand or foot) and an eye

loss of sight of both eyes OR speech OR Hearing of both ears

3. Permanent Partial Disablement

In this case, a small percentage of SUM assured is paid on a weekly or monthly basis. For example – 1% of the sum insured is paid every week up to 100 weeks. Example below

Loss of Index Finger or thumb

Loss of hearing in 1 ear

Loss of 1 eyesight

Loss of 1 hand

4. Temporary Total Disablement

This means that for some weeks or months a person is totally disabled and will not be able to work and earn money. In this case, most of the companies pay a part of the sum assured, some pay 100% and some pay 50 %, there is also a cap in this case, like a maximum 5 lacs or 10 lacs. Example below

Bed rest of next 3 months

Fracture in hands or legs

Other Features

Some companies cover claims arising out of Terrorism or acts of Terrorism

No health check-up required for policy issuance

Worldwide coverage of the policy

It gives coverage starting from 5 lacs to 50 lacs

Free lookup period of 15 days

5% per claim free year to a maximum of 50%.

Family discount of 10%

What is not included (Exclusions)

Accidental policies do not cover Deaths or disablement because of

Intentional self-injury, suicide or attempted suicide.

Influence of intoxicating liquor or drugs

By committing any breach of law with criminal intent

Suffering from any pre-existing condition or pre-existing physical or mental defect or infirmity.

Aircraft pilots and crew, Armed Forces personnel and Artistes engaged in hazardous performances are totally excluded

Premiums do not dependent on AGE

The premium of accidental policy does not depend on age. So if you are 25 yrs old or 50 yrs old, the premiums would be the same, rather it would depend on your working conditions and the nature of your job. If you are a software engineer working in Bangalore, then your chances of meeting the accident are different from an army personal working in the border or a worker in a factory that has dangerous machinery. So each kind of job profiles are divided into different risk level, sometimes it’s 1,2,3 and sometimes it’s just 1,2. Risk level 1 are those who are less risky and their premiums are lower and risk level 2 are high risky category and their premiums are higher. Let me give you an example

underground mines, explosives, magazines, workers whilst involved in electrical installation with high tension supply, jockeys, circus personnel, engaged in activities like racing on wheels or horseback, big game hunting, mountaineering, winter sports, rock climbing, potholing, bungee jumping.

Note that some companies have a list as 3 different risk levels – 1,2,3

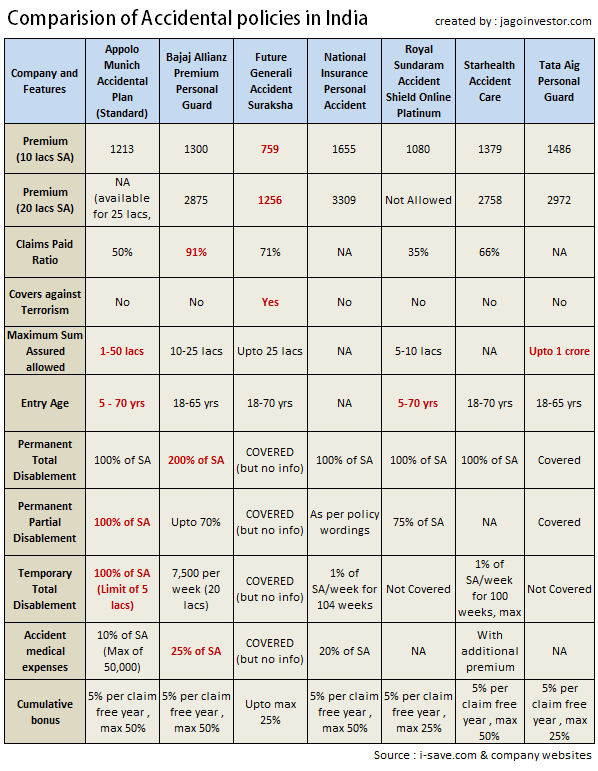

Examples of some good accidental policies

Below I am listing down some of the accidental insurance policies and their different features. If you see all of them, you will realize that all the policies have something good or bad in them. This chart is made by collecting information from different portals and companies’ websites. Note that the premiums below are for Low-risk professions (Level 1)

If you see the above table, you can see that on absolute level Bajaj Allianz seems to be the best option and it’s the recommended one. The best part is that the claim settlement ratio is high and that’s the biggest parameter people look for.

Please comment on what do you feel about Personal Accident Insurance policies and what has been your experience in that?

Why some idiots don’t Plan out things in life? – Hey, we are not saying this but it’s a message from a “one minute fly” to all of us. The fly is here to ask you one question what do you want to achieve in the one precious, unrepeatable life that you have? Really go deeper and figure out what do you REALLY REALLY RALLY want in your life. What kind of house you would like to live in? What kind of places you would like to visit? What kind of people you would like to meet?

What kind of charity you would like to do? What kind of retirement you would like to have? What kind of wild things you would like to do in your life? What kind of legacy you would like to leave? We all have one financial life and we should make the most out of it. We tell this to all our coaching clients at the end our financial life will either will be a “warning” or an “example”. It is up to us how we create our financial life like an example.

One of the Financial coaching Principles is “Start living a good financial life rather than trying to live a good financial life”. Personal finance is not about what you are going to do next month or next year it is all about what you are doing right now.

We would like you to watch a video and learn some life-changing lessons from it; you can learn the importance of planning from a One Minute Fly.

The video “One Minute Fly” Teaches us the true meaning of life. It teaches us some very important life lessons on how we should live our life. One of our clients after watching the video said “We are the same as this Fly in the video”, he is so true we are just the same. We are here on this earth for a limited period of time and we have to do our best. We have many things to wrap up in the one life we have.

It is therefore important to figure out the important goals of your life and start planning for them. Let me tell you something. This life goes by so fast you cannot believe it. One day you are 25 looking forward to all that life has to offer it, and the next day you are 52. You suddenly get on the other side of those dreams, looking back and wondering where in God’s name all the time went.

You are lucky if you have more time ahead of you than behind you. If not now than when will you start planning. This is the right moment in which you can start creating your financial life. So step fully into your financial life and start making the most out of it. This is not an article, this is life, so dust casualness and laziness from your financial life. We want to leave you with a beautiful poem from the movie Zindagi Na Milegi Dobara

If you have eagerness in your heart, it means you are alive, If your eyes are filled with dreams, it means you are alive Learn to be free like the wind, Learn to flow freely like the river, Embrace every moment with open arms, See a new horizon every time with your eyes, If you carry surprise in your eyes, it means you are alive, If you have eagerness in your heart, it means you are alive…

Once you are through with the video take a blank piece of paper and make a list of 100 things that you want to do before you leave this world. It would be great if you can share some of your dreams and goals with us in the comments section. In this moment you can declare your goals with courage, play for your goals with courage and live your goals with courage. If on your own you are not confident take some professional help, spend some money on yourself and get a financial plan or get a financial coach and start taking actions and make the most of the one financial life you have. And don’t forget to comment on what did the FLY TEACH YOU.