This is a little old news. RBI has finally abolished Prepayment charges or penalty on home loans with floating interest rates. Borrowers can now transfer to new lender which provides them less interest rates without paying any kind of charges or penalty. Damodaran Committee on customer service in banks, RBI) has been observed that banks have been unfair in asking for charges when home loan borrowers want to switch to some other lender with lesser interest rates. Now if you prepay the loan from your own sources or through another lender, you only pay the outstanding loan amount.

Here are the excerpts from the circular from RBI on abolition of fore-closure charges/pre-payment penalty

2. In this context, attention is invited to paragraphs 81 to 83 of the Monetary Policy Statement 2012-13 announced on April 17, 2012 with regard to home loans on floating interest rates. The Committee on Customer Service in Banks (Chairman: M. Damodaran) had observed that foreclosure charges levied by banks on prepayment of home loans are resented upon by home loan borrowers across the board especially since banks were found to be hesitant in passing on the benefits of lower interest rates to the existing borrowers in a falling interest rate scenario. As such, foreclosure charges are seen as a restrictive practice deterring the borrowers from switching over to cheaper available source.

3. The removal of foreclosure charges/prepayment penalty on home loans will lead to reduction in the discrimination between existing and new borrowers and competition among banks will result in finer pricing of the floating rate home loans. Though many banks have in the recent past voluntarily abolished pre-payment penalties on floating rate home loans, there is a need to ensure uniformity across the banking system. It has, therefore, been decided that banks will not be permitted to charge foreclosure charges/pre-payment penalties on home loans on floating interest rate basis, with immediate effect.

Prepayment Charges removal will help !

This new rule will surely be taken in good spirit by borrowers and end the discrimination done by banks between old and new customers. This will also make sure that the interest rates become more competitive in the overall system.

Have you prepaid your home loan just some time back with charges ? Are you going to prepay the loan soon after this Prepayment Charges removal ? What are your thoughts about this new circular !

Do you know what are the rules on PPF maturity if you want to withdraw your money ? Do you know that you can extend your PPF account a block of 5 yrs after it’s initial maturity of 15 yrs? A lot of people think that once the PPF maturity is over, they get a licence to withdraw the money at any point of time in what ever way they want, in the case of extension of PPF. Today let me highlight some important points that you should be clear about PPF withdrawal rule in case of extension and show you how to calculate your PPF maturity amount. To start with lets answer what Kailash Chandra asked me sometime back on his PPF

I had opened PPF account on 05/05/1995 and extended for 5 years. Now the balance is Rs.651000/- as on 30/04/2012 and want to withdrawal partly. What amount can I draw please intimate. (link)

Whats the answer?

Its 60% Surprised!… lets move on

Before we move forward, let me clear that Public Provident Fund or PPF is a life time account. One can extend it for next 5 yrs for infinite times, this means you can keep on extending it for another 5 yrs after the maturity is over. That would in a way makes it look like a 5 yrs closed fixed deposit earning you applicable interest rate with tax benefits and without any taxation involved, even having a partial withdrawal benefit 🙂 That’s one reason why you want to open your PPF account right now even if you don’t need it at the moment, so that the maturity is 15 yrs away from now. See it as a milestone!

1. PPF extended without any further contribution

The first situation is when you want to continue your PPF account, but do not want to put any further money in it . In this case all you want to do is just leave your PPF account as it is and let it earn the interest on the account accumulated. Note that if you dont take any action for 1 yr after your PPF matures, this option is default and automatically activates. Note that once its considered as “extended without any further contribution”, then later you cant put any further subscription in it. Now you can only withdraw from the PPF account, but cannot invest any fresh money in it. Note that in this case, you can withdraw any amount from your Public Provident Fund account, there is no limit. You can withdraw 10%, 50% or 90% as there is no limit. The balance amount will keep on earning the interest further. However you can withdraw only once a year, not more than once. (Learn how PPF account interest is calculated)

Interesting Fact : Now as you know this, can you see an interesting point here, this way PPF can be acting as a great Pension tool, where you can withdraw the interest part yearly once and then utilize it for full year. For example if a PPF account has 1 crore into it, and lets say the interest is 8% (just an example). You can withdraw 5 lacs out of the Public Provident Fund account and the remaining 95 lacs will earn 8% interest, which will be 7.4 lacs. This 7.4 lacs will be added back to 95 lacs and the total next year would be 102.4 lacs. This way one can keep on withdrawing some amount from it and let it grow too.

2. PPF extended with further contribution

In another option, you can choose to invest in your PPF account on regular basis even after extension. But this has to be done within 1 yr of PPF maturity (before the completion of 16 yrs in PPF). Note that in this case, you can only withdraw maximum 60% of your PPF amount in total within the entire 5 yrs block. Each year you can withdraw maximum once.

For example if your Public Provident Fund balance at maturity is Rs 1 crore. Then you can withdraw a total of maximum 60 lacs in entire 5 yr block. You can withdraw 20 lacs in first year, then 10 lacs in 2nd year and then 30 lacs in 4th year. But Once 60% is consumed , you cant touch any money further for the current block. Only when the 5 yrs are completed and new block of 5 yrs start, then your balance will be 40 lacs and then again the same rule applies. However note that at the start of a new 5 yr block, you can choose whether to continue the regular contribution or stop the contribution, like we discussed in point 1.

Important :If at the time of Public Provident Fund maturity , you will have the potential to invest more in your PPF account in coming years, then better invest more and more and only when its time to retire or when you cant contribute more, extend the PPF with “no further subscription” option.

Bank Officials have no idea about PPF Maturity Rules in detail

A lot of banks (SBI) and Post office officials have no idea about PPF rules in such a detail. They will tell you that it can be extended only 2 times and hence insist on closing your PPF account once 2 extensions happen after your PPF maturity. Tell them that you know what are the rules and also teach them.

In this article, we will discuss “Relationship managers” . I got an interesting comment about “Relationship Managers” on my facebook wall from Prasad when we were discussing recent HDFC Life offering on 100% Free Financial Planning through snapdeal. Here is Prasad’s sharing on his relationship manager and what happened with him.

I am totally disappointed with HDFC Bank , every time my RM calls, he wants me to sell an insurance plan. If i tell him that I have other commitments at this point of time, he tells me he can get me a credit card if I dont have one and use it to buy the insurance plan.. It can’t go down more !! had so much respect to this bank.. But the concept of RMs is the most misleading thing !!!

Focus on this comment and re-focus on one sentence – “he tells me he can get me a credit card if I dont have one and use it to buy the insurance plan” . What does it say? What comes to your mind when you read this? It shows that there is an extreme focus on performance, there is extreme pressure on meeting targets on relationship managers. Their jobs are at stake at times and there is a do or die situation.

What are Relationship Managers ?

Relationship Managers are generally assigned to a customer who have more money and resources than others, who has more longer-term relationship with Banks, you are told that you will be taken special care by this relationship manager, at times you can directly talk to him for any issues. All the people having more than a certain net-worth or salary are assigned, relationship managers.

You are told that he is supposed to help you out whenever you want and he will be available to you all the time when you need him. However relationship managers are generally MBA Marketing guys, who are hired to take the sales to go up, they are responsible to bring business by hook or by crook. The worst part of relationship managers is that their attrition rate is so high, that by the time you figure out that you 90% is-bought and were 10% missold a financial product, the relationship manager is not working in the same company anymore, he has moved to another job now.

Recently got a call from kotak mahindra bank regarding some bullshit insurance policy. Usually whenever marketing calls comes to my mobile, I use to say “sorry, Not interested”. But this time I decided to elaborate why I am not interested by telling a lie. All I told was “Actually I was interested in this product and had fixed appointment with your relationship manager on last friday. But he dint came. So not interested.” The marketing guy replied that he will check back. After two or three minutes i got a call from them again. “Sir we are extremely sorry. We called that relationship manager. He was not able to come to you because he met with an accident that day. shall he come today?”

What does a relationship manager know about you?

A relationship manager knows how much money do you have in your bank account, he knows for how long it is lying there. He knows the recent credit and recent debit from your bank account. He can figure out that one of your FD maturity and is now “available” for the massacre. He can then call you or meet you and show you an amazing product, if you want to invest and “if you have any money” . Obviously he knows you are sitting on a 10 lac cash right now. He is innocent, he is just telling you about something FYI, after all, that’s his job!

Remember, If a relationship manager recommends you some product and if you manage to make good returns or it turns out to be a good thing for you, it’s mostly accidental! So now, if you are an HNI or if you are going to get a relationship manager from your bank, broker or whatever it is, just make sure you know that its most probably going to add to your headache. He will keep on pushing you, convince you about opportunities and prove to you how your money is getting wasted sitting at your bank account. I remember a comment made by Subra on one of his articles on relationship managers and doctors.

“Doctors over-diagnose and Relationship Managers over-analyze your portfolio. Doctors recommend treatment and drugs, RMs recommend ULIP.”

Relationship Manager interview

I can only imagine the interviews which banks or companies take for hiring relationship managers.

Question : Tell me something about why you will be a good relationship manager at our bank ? And What qualities in you makes you a great candidate ?

Candidate 1 : I have completed this amazing course on portfolio construction which is internationally accepted. I always think from the viewpoint of the client and what will make his life more easy and great . His interest should come before mine and bank and I say this because I think from long term point of view.

Candidate 2 : I am a behavioural finance expert and with use of words I can create situations of guilt , excitement and trust . I can make sure that the clients common sense and logical reasoning will just go for a toss and I also know how to do this all without appearing too pushy and deceptive . I have completed PHD in powerpoint and excel and can use those tools at 3:00 am in the morning too to impress a client.

You know who gets hired !

Why did you hire me ? – Asked Candidate 2

“So that we can learn somethings from you , anyways they never tought us anything useful in our MBA” – Says Interviewers

“And Why did you reject me ” – Asked Candidate 1

‘Because you took the title we were offering you very seriously” – Said interviewers

Any comments or experiences?

Do you think this topic of “relationship managers” deserves a Satyamev jayate episode ! . I can see some crying face’s already here, not on the show. Did this article help you understand exactly what relationship manager do?

You can now enjoy FREE Online Tax Filing from taxspanner and clear tax websites. Tax filing season is on and I dont want jagoinvestor readers to wait till last moment. In all probabilities you have paid your taxes now and you are all set to file the returns now. We did Action Month last year were a lot of people completed a few important tasks in few days which were pending in their financial life. So now we are doing TAX FILING month where its an opportunity for you to file your returns online. So I have arranged for 1000+ Free tax filing coupons from 3 websites and you can file your taxes online for free. So Early action takers can file it for FREE, but later comers will have to bear there own cost.

ClearTax – Income Tax filing portal for Individuals. We aim to be the easiest to use & Perfect for first-timers. You can just upload Form-16 and ClearTax reads all the relevant values. Usable from any Mobile, Tablet or a Computer.

Taxspanner is the largest online tax filing firm in India providing ITR1, ITR2 & ITR4 and they are the only portal which is certified for security and vulnerability by CERT-IN

Perfios is the Leading and the most Automated Online Money Manager in India with more than 250000 registered users. Perfios is offering FREE Online Tax Filing for the jagoinvestor readers – for the first 50 Sign-Ups! If you miss it, you still get to file at a very economical rate of Rs.125″ Hurry Sign Up now !!

Free Online Tax Filing using the Govt Website

One can also file the taxes online using the official tax website of govt using the following steps.

Download the appropriate software from the website as per your case. This software is nothing but a nice detailed excel sheet (enable the macros)

Once you have the excel sheet on your computer, fill up all the details (if you dont have form 16, you can still fill all the details manually).

Once you fill up all the details, verify it once again and then export it to XML (the export button is there in the software itself)

Once you have the XML file with you, you need to login to the website (you will have to register for it once).

Once you are logged in there will be an option called “Upload Return” on the left side. Click on it

There will be two options called “Digital Signature” and “No Digital Signature” . As most of the people would not have a digital signature, just choose the option. Upload your XML file and just create your acknowledgment form called ITR-V, You need to download it. Once you have the acknowledge form, just verify it once again.

Just send this acknowledgment form using a regular or speed post (no courier allowed) to“Income Tax Department – CPC, Post Box No.1, Electronic City Post Office, Bangalore – 560100, Karnataka”

You will get the receipt of your ITR-V receipt by email in some weeks (takes time), you can track its status here

You can read the step by step procedure to file online taxes that are mentioned here in this article. I hope you know that tax refunds are processed faster if you file your taxes online. Ask your questions on tax filing here on this thread and I will try to bring in few experts on taxation to answer all your queries. I hope you have completed your FREE Online Tax Filing through these websites.

How many times have you ever faced an emergency situation in your financial life? I am talking about some situations when you needed cash within a few hours or days and it turned out that you had to seek monetary help from your relative for it or some friends, whom you didn’t want to ask?

Financial Planners and advisors suggest emergency funds to everyone saying that they should have it because there can be emergency situations in their life and they should always have a few month’s worths of expenses as plain cash for emergency purposes.

While it’s a good practice to maintain an emergency fund, a lot of people do not believe in it because for them emergency situation is something which will never happen to them. They always have fixed deposits which can be broken in hours/days and if its really required one can get it anytime. In the same way, mutual funds can be liquidated at a click nowadays and in the worst case, you always have relatives/parents etc who can lend you money in short term. So, in reality, a “real” emergency is really rare. This is how a lot of people think.

The real reason of having an emergency fund

But after a lot of introspection, I came to the conclusion that the real reason for having an emergency fund is something else. More than the “handling emergency situation”, It’s about your behavior about investing regularly. It’s helpful in stopping you from disturbing the investments which are all set in your life. Let me explain to you what I want to say with some examples.

Imagine a situation where you have started a SIP of 10,000 per month. You also have invested some amount in Fixed Deposits recently and few other investments. You all know that it’s damn tough to finally take actions and really start your SIP’s and actually make investments after a lot of thinking and analysis and “will surely do one day” thinking.

Now suppose you didn’t have an emergency fund, which is “6 months of expenses” for you. Now, what will be your natural reaction if you need money urgently? It’s very natural to break your FDs, liquidate your mutual fund’s investments and then say “let’s stop the SIP for few months till I am facing this cash crunch”. Put one hand on your heart and tell me, how many of us are really so dedicated to re-start our SIPs and investments after the situation is back to normal. We all get lost in our life and jobs and “problems” and then it only starts back after months and years of finding that perfect moment or if its “high time now” situation.

So as per my understanding, the real reason for having an emergency fund is to make sure that you do not disturb your investments which are already started and automated. The real reason for having it is so that you have dedicated funds which you will break before reaching out to your other goal-oriented investments. Think of it as a layer between your real wealth which you want to grow over the long term and money which you want to use in emergency situation. Think about this for a moment, its a little hard to imagine what I am saying here, but if you get my point, you will really appreciate the concept of this.

Did you understand what exactly Emergency fund does for your financial life?

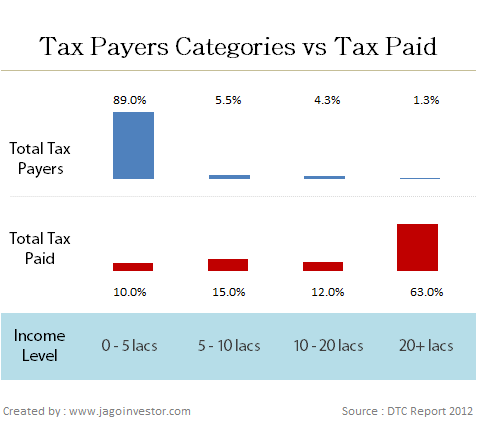

Do you know that 89% of tax payers in India have income of less than 5 lacs per year? Yes that’s true! Such is the case of most of the low earning people form the tax-paying population. However can you guess what is their share in total tax paid? It’s just 10%.

why doesn’t govt make income tax limit as 5 lacs ?

Yes, 10% of total income tax comes from 89% of taxpaying population. Now that brought a very interesting question in my mind, that why doesn’t govt make 5 lacs income as Tax free? Only those who have more than 5 lacs income will be paying tax. Imagine what will be the situation!!

In one shot, 89% of the tax-payers will be free from the headache of paying tax each year and the govt will still get 90% of the taxes. What they can do is increase the taxation rate a little bit, so that they still get 100% of the taxation recovered from the rest 11% tax payers (having income of more than 5 lacs). If you look at deep down into the statistics, do you know that 1% of tax payers earn more than 20 lacs income and they account of 63% of tax payment. Imagine this – 63% tax coming from just 1% tax payers.

Let’s come back to reality now. It was great to imagine that govt should raise the income tax limit to 5 lacs. But do you know that collecting tax from this segment is the easiest. Because these 89% tax payers are mostly salaried employees and the overall tax collected comes in the form of TDS. Companies hiring them have the responsibility of cutting the tax each month and paying it to govt. Hence Govt has almost no work to do to collect the tax from this section of 89%.

This brings us to a very important conclusion now, How should govt restructure the taxation rates and limits such that they increase their tax collection, but it impacts a small percentage of population? What about doubling the taxation rates for those having income of more than 20 lacs? What about making a marginal increase in taxation rates for those having income of more than 10 lacs?

I know I might be overlooking some important points here, but what do you think about it ? Dont you think govt should raise the income tax limit to 5 lacs or something like that ?

There have been too many fake phone calls in the name of IRDA these days to many people. It have been noticed that these IRDA fraud calls are made by anonymous people claiming that they can help you get your money back for your Insurance policies which have become a big headache those those who invested in ULIP’s traditional policies without understanding them and are stuck in those plans now. They know that IRDA is a body which handles them (do they?). At times investors are so fed up with their policies, their life situations and are so desperate to get help that they believe anyone who claims to help them.

So some very smart people starting calling up people claiming they are from IRDA and they can help them in getting back their money back or showing some kind of hope to help them. There are several instances where some people lost more money falling for these calls and believing in them. Lets see some examples of these fraud calls and how investors again believed them without doing their study.

Fraud Case 1 : Deepak lost Rs 25,000

I also Received a call from a number 01206470443 saying that he is from IRDA and I will get a bonus of atleast Rs. 20000- for the insurance policy that I had taken few years back from hdfcsl. However, I had to make an investment of Rs. 25000/- for birla sun life insurance company. but i have no recieved documents of birla sun life insurance company. Any one can tell what I do for my payment back. (link)

Comment

It was very obvious that their was a fraud done with him and he had either signed some cheque or given DD to someone without understanding what he was doing. He must be very excited to get back some bonus (which didnt exist). He

Fraud Case 2 : How S Dash lost 51,000

I received a call from a lady named Riya Malhotra who said she was from IRDA. She said that IRDA is helping out investors in getting back their long stuck up policy funds. I had one Bajaj Allianz policy which I wanted to close. She said she will help me do it if I take a new policy from Kotak Mahindra or Birla Sunlife

She said that this is a five year term, we pay one-time 51000 now (no more premium payment till 5 years) and we will get 50% of the 51000 in 45 days and after 5 years we will receive approx 76000. However we will get a life cover till I attain age of 100. Moreover we can also recover any insurance amount which we are unsatisfied with within 45 days also. It’s already more than 50 days since I made the payment of 51000 by cheque but I have not received any communications from her. I try calling her @ her mobile. No answer.

Please suggest what should I do? (link)

Comment

Note sure whom did she write the cheque for ? There was no rational on choosing a new policy just to get back the money from old policy, there is no relation between both policies.

Fraud Case 3 : How Vikas Lost Rs 3 lacs

Mere pass call aya ki birla sun life me policy one time karane par ek verna car gift ki ja rhi hai , lekin rupees cash dene hoge maine three lakh rupees de diye lekin aaj ek mhina ho gya na to koi bond paper aaya h na hi mere paise sir plz me kya kru (link)

Comments

I have no idea how a person can believe that if you if you buy a policy , you will be gifted a car ! . Thats too guaranteed ! , That too by giving cash ! .. While this was a fraud call , there was some common sense expected too !

Fraud Case 4 : How Sumit lost his money

In last December 2011 I got a call from IRDA (from number 0120-3050600 saying they are from IRDA) saying that your last policy premium will be recovered as we are from IRDA and we will give one regulatory to Birla Sun Life to return your money back but I’ll not get this amount directly to my account. What I need to do is to take a policy from Aegon Religare for the same amount Rs 36000. This policy will be actually for 16 years with 10 years locking period. But Due to IRDA intervention your policy will be for only 3 months locking period. Your first year premium will be paid by amount from Birla Sun Life policy and I need to pay another Rs 36000 as current year premium and I need to pay next year premium and then 4th year I can withdraw the amount which will be around 1.6L due to some calculation. Over and above that they committed that company will pay agent commission to my account which will be 25% of yearly premium. They will bypass agent from my policy.

They were continuously in contact with me till 18th Jan that I’ll get a separate statement. They know that I can cancel the policy within 15 days of receiving the documents so they were contacting me so that I’ll be convinced and cannot cancel the policy. But after 20th Jan they are neither picking my call nor calling me. So they have found a new way by picking weak vain of customer by giving promise that old lapsed policy amount will be recovered as well you will get agent commission. I had taken this policy bcaz of tenure will be 3 years as well as I’ll get agent commission with last policy lapsed amount.

The person whom I was in continuous contact was Anjali Oberai. Her mobile number is OXXXXXXXX and direct landline number is 0120-4396848. I have called many times on these two numbers to her. Before 20th Jan she entertained all my calls but now she is not picking my call. Also same policy benefits were explained to me by Neha Chaturvedi one of senior person of IRDA from Hyderabad. Anjali Oberai represented Neha Chaturvedias senior person from IRDA from Hyderabad and she came to NCR for some time. Many times I had doubt on them but due to greed of recovery of my loosed last policy amount and getting agent commission I was cheated by them. I know it’s completely my fault. But I would like to take in focus of all so that nobody can be cheated. (link)

Comment

I can see a clear gap in understanding of how life insurance industry works and too much faith in stranger who called up on the name of IRDA . If the policy was really taken from Aegon religare , it should be checked who was the agent in this whole process and nab him/her.

IRDA has clearly issued a notice saying that there is no initiative from IRDA like this

Insurance Regulatory and Development Authority (IRDA) is a regulatory body established by an Act of Parliament to protect the interests of the policyholders, to regulate, promote and ensure orderly growth of the insurance industry and for matters connected therewith or incidental thereto.

Some instances have been observed by the Authority that general public are receiving calls from individuals who claim to be representatives of IRDA and offering insurance policies of different insurance companies with various benefits (such as offering of scholarship along with policy etc.).

The general public is hereby informed that Insurance Regulatory and Development Authority is a regulatory body which does not involve directly or through any representative in sale of any kind of insurance or financial products. Any person making any kind of ‘transaction with such individuals/agents will be doing the same at their own risk. If any member of the public notices such instances he/she may lodge a police complaint in the local police station.

Sd/- (Kunnel Prem) Consultant and Special Officer (Life)

Don’t fall for IRDA Fraud Calls

IRDA is just a regulator for Insurance sector. They do not make any calls acting as mediator between you and company. All they can do is direct a company for some matter or ask them to follow a guideline. But they never work on individual cases and send people to collect money from you. Even if it did , it will never ask for Cash or any kind of cheque on personal names. These kind of calls are purely fraud done by those who know which policies you have (known somehow) and then they just try to see if you can fall for their false promises. Use common sense because making payment to anyone like this, do not pay any attention to these IRDA Fraud Calls.

Taking a Home loan is a big task in itself and one of the biggest financial decisions. A home loan is the longest debt in our life. At times 10-20 yrs, which makes demands a long term commitment. Each month you have to pay your EMI, sometimes you have to prepay some part of home loan, sometimes you need some documents and visit the bank. There are numerous things to be done during taking the home loan and after taking the home loan, hence you should be very clear that which is the best bank for Home Loan. Without much confusion, it’s very clear that everyone wants to go with the bank which makes your life easy at the time of taking a home loan and even after that. So the biggest question on everyone’s mind is “Which is the best bank for a Home loan?”

First thing first, you have to be very very clear that their cant is a single bank or loan institution which is perfect for everything and you will never face any issue with them. Also, there is no “best bank for Home Loan” which has always worked for everyone to date. But overall we can always pick some banks which have been better than others on different parameters. You can say that on a high level “Bank A” is better than “Bank B” and this is based on many loan takers’ experience over the years. So now in this article, we will try to understand the difference between different banks and how they differ with each other. We will also see a survey result done with the vast community of this blog and which bank they choose collectively as the best bank for a home loan.

Public Companies vs Pvt Companies

While researching on this topic, the first thing which came to my mind was “all banks are the same, everyone has a bad experience will all kinds of banks, whether PSU or private”. But we have to understand that while some people can have a bad experience with some banks, there are a positive experiences too and we have to see things from a very high level and not judge a bank just based on a handful of bad experiences. The first confusion which comes to any loan taker mind is “PSU bank or private bank?” and based on the experience here is the conclusion.

PSU Banks are good post-loan but not friendly at the time of taking the loan

Private banks are very fast and friendly at the time of disbursing the home loan, they will treat you like a king up-till the loan is disbursed, but once every formality is complete and your home loan is sanctioned, you are a trash to them! As they are extremely aggressive in the marketing of home loans, a lot of people fall for it, Private companies presentation and the way they approach you is good but only till you are not a home loan customer. A lot of times private companies make things easy for you and also bend some rules for home loans. the number of documents they need also is less compared to a PSU bank.

On the other hand, PSU banks are not that great at the start of home loan , their rules are very strict and stringent and they still operate in the “sarkari” style, however, once your loan process is complete and things start, their afterlife is much easier compared to private banks. The overall handling is much professional and as per the process. In short, they don’t suck your blood every now and then as private companies do.

Private banks are first to raise the interest rates

On the interest rates increase and reduction side, its seen that private companies are first to raise the interest rates after the rate increase from the RBI side, but private banks hide somewhere when there is a time for reducing the interest rates. However, PSU banks are more transparent on this front and much less annoying than Private banks. Also private banks arbitrarily increase the pre-payment charges ( like from 2% to 3%) the conversion fees are also charged heavily if you want to move down to lower interest rates.

Also the changes of fraud at employees level in Private bank is much higher than PSU Banks. I can’t say that PSU banks are not into the bad game, but it’s much much higher in Private banks because of sales pressure and targets. There has been cases of forced selling of home insurance and also cross selling of ULIP’s and other financial products along with the home loan

Which is the best bank for Home loan in India?

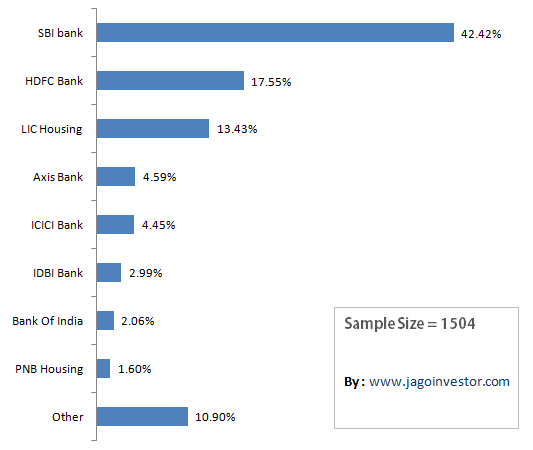

Now there are millions of people who have taken home loan and there are various parameters on which a bank can be ranked like Processing time for a home loan, Transparency in whole process, Attitude towards the customer, Interest rates and pre-payment charges, online tracking of your home loan after disbursement. But there is no ranking of banks on all these parameters. However still you can rank a bank overall as good or bad in total. I ran a survey on this blog and got around 1504 participants to vote for the best bank for home loans and based on that we can judge which banks are more preferable and more trusted. Here are the results.

If you see the survey above, you can clearly see that the top 5 banks for a home loan are SBI, HDFC, LIC Housing, Axis Bank and ICICI Bank and these 5 banks comprise 83% votes. While a big reason for this can be that these are big banks having a wide reach and has more customers and hence the results are a little biased. But at least you can see that out of 1504 people on this blog, 83% of them have a home loan from these 5 big banks, in which SBI tops the list.

1. SBI Bank

Based on the survey and overall reading’s done over the net and comments section of this blog. SBI bank seems to be the best bank for Home Loan. While SBI Bank still carries the hangover of Sarkari culture and they are strict in the overall process, which means you will have to run all over the bank and many times to get things done, but once the whole process is complete, maybe you will have a smooth experience overall. Things will be easy post home loan process if you need anythings from bank compared to other banks. For those who want to know why SBI is preferred, follow this thread

2. HDFC Bank

Overall HDFC bank seems to be have mixed reviews. Some people had a great experience and some had a very bad experience. HDFC Bank is overall recognized as the bank for the home loan itself. But overall the experience was very very mixed.

3. LIC Housing Finance

LIC housing finance seems to be a decent option after SBI. While they are not that great as SBI, still they seem to be a good choice after HDFC and ICICI bank. LIC Housing Finance has lesser documentation requirements, but one has to run around for smaller details. LIC seems to offer better rates and also giving the option to fix the interest rate for 5 years. One thing which many people do not know is that LIC reduces the interest rates for home loan for its customers having any insurance/investment policy with LIC by at least 0.25 %, but only if Sum assured of all policies collectively is more than 15,00,000 and all policies should be under the name of the loan applicant.

4. ICICI Bank

ICICI Bank seems to be very very fast and too friendly at the time of loan processing, but once the loan is done, life seems to be hell for most of the people. They are not very supportive most of the times and one gets too frustrated with their attitude. Overall their interest rates are also very high.

5. Axis Bank

Axis Bank is another good option as a big bank. One good thing about Axis bank is that they have NIL charges for any pre-payment. It’s a big surprise that Axis bank was more preferred than ICICI bank overall in the survey. While Axis Bank has few good options, there was one recent case from axis bank which I had highlighted on this blog on how they forced sell a life insurance policy along with home loan, While this was a negative thing from Axis Bank, we have to understand that good and bad experience are part of all the banks.

So what is the final answer ?

While there are positive and negative experiences from different banks, the clear answer coming out of different comments from readers and survey is that if one has to choose just one name, SBI bank is the best bank for home loans. We have seen most of the votes going to SBI Bank and all the pointers are suggesting that its the right choice.

Which bank do you have home loan with and what was your experience overall from start till the end. Can you share it in for others benefit?

With 45 people in a room at Shilton Royale hotel in Bangalore, the session started. Nandish started the conversation and then it just took off like it was a day made for a great interaction and huge learning for everyone. The session was highly useful for most of the participants and the biggest thing which they could see is “Offline” interactions are so different and some real sharings happen offline when we meet and sit together. The best thing which everyone liked was that there was no regular talk on products because we all know those things already. However it was more of a session where one learns the tricks of a successful financial life and what mistakes most of the people are doing in their financial life.

We shared with the group what we have learned by working with hundred of people and what our experiences are. Overall it was a great day. Here are few pictures from the session at Bangalore.

Participants Comments about the workshop learning

“It is a pleasure to listen to both manish and nandish. The simplicity of which the comcepts are explained is very appealing.The biggest take-away would be – keep it simple silly” – Priya Srinivasan

“Workshop was simple and transforming. I learnt to unlearn some old thinking. Looking forward to mroe sessions and workshop in advanced planning/actions” – Jnanesh Padiyar

“I twas a good learning. Passive income, shock therapy are key learnings . Appreciate that you did not try to sell any financial product not even your own book” – Jayaprakash Rao

“Your team has given me a new vision, to see what I really want in life, have the knowledge to get it in place and to take the actions required to achieve it. Thank You!” – Deepak Singhal

“It was a very good workshop. Really helped me understand my financial life much better.It has taken my financial life to the next level. I also feel there can be more case studies and may be more plays…Thank You !! “ – Pavani

“Its a really good workshop. I came here to just hear about financial life but it was not just finance but it is whole life” each and every aspect”. I am going back with some commitment for not just manage the money of what I earn but I need to develop myself, health and improve my intellectual property” – Shyammani Prasad

Video Testimonials

Register for Mumbai and Hydrabad

We are going to conduct 2 more workshops in July in Mumbai (Early July) and one in Hydrabad (Mostly end of July). If you are interested in attending those workshops. Please put your names for the workshop.

Those who were present in workshop and are reading this article, please let others know how it was overall and your comments .

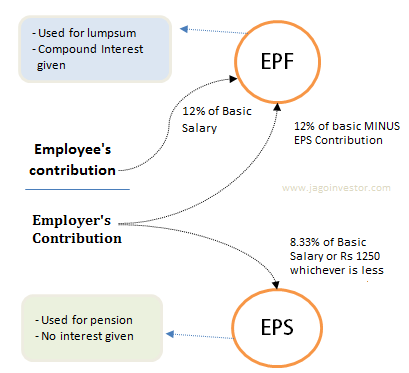

We will discuss few EPF rules today. A small part of your salary (12% of your basic salary) is invested in something called EPF or Employee Provident Fund and an equal amount is matched by your employer each month.

This is what 95% of people know, but there are many things which a lot of people don’t know and this article is going to open some not known secrets about EPF rules. So let’s take them one by one in point’s format.

1: You can also nominate someone for your EPF

Do you know that there is also a “nomination” facility in EPF? The nominee will be contacted at the time of death of the person and handed over the money from the provided fund. However, if the nomination is not present (which you should check), it can rise to all sorts of issues while claiming the money.

There is a form called Form 2 which has to be filled to change or update the nomination. Please contact your company finance department or directly send the form to the EPFO department.

2: One can get pension under EPF

Do you know that there is something called EPS (Employee Pension Scheme) in the provident fund? The EPF part is actually for your provided fund and EPS is for your pension.

The 12% contribution made by you from your salary goes into your EPF fully, but the 12% contribution which your employer makes, out of that 8.33% actually goes in EPS (subject to a maximum of Rs 1250) and the rest goes into EPF. To understand it this way, a part of your employer contribution actually makes up your pension corpus.

But there are some caveats to this.

One is liable for pension only if one has completed the age of 58.

One is liable for pension only if he has completed 10 yrs of service (in case of more than one companies, the EPF should have been transferred, not withdrawn)

The minimum Pension per month is Rs 1,000

The maximum Pension per month is subject to a maximum of Rs 3,250 per month.

Lifelong pension is available to the member and upon his death members of the family are entitled to the pension.

3: No interest is given on EPS (pension part)

You must be thinking that you regularly get compound interest each year on your contribution + employer contribution. But it does not work like that. The compound interest is provided only on the EPF part.

The EPS part (8.33% out of 12% contribution from your employer or Rs 1250 whatever is minimum) does not get any interest. At the time of PF withdrawal, you get both EPF and EPS.

4: You might not get 100% of your Provident Fund money

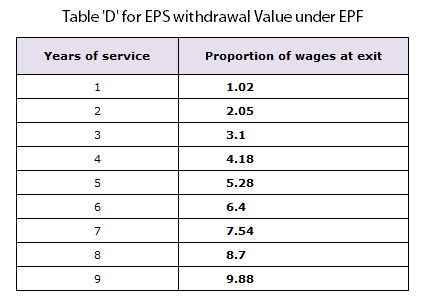

Imagine your contribution + employer contribution has been a total Rs 3,50,000 to date. Out of this 3,50,000 , suppose 2,50,000 has gone in EPF , and rest 1,00,000 has gone in EPS (for pension) . Now if you quit your job in the 6th year of employment and opt for withdrawal of your Provided Fund money (EPF + EPS actually), then do you think you will get a total of 3,50,000. NO!

That’s because you always get 100% of your EPF part, but for EPS there is a separate rule.

There is something called Table ‘D’, under which its mentioned how much you get at the time of exit from your job, there is a slab for each completed year and you get n times of your last drawn salary (depending on the completed year of service) subject to maximum to Rs 15,000 per month.

So if your salary, in this case, was Rs 30,000 per month, still you will be given only 15,000 * 6.40 = Rs 96,000.

Note that the table D is up to 9 yrs only, because if 10 yrs are crossed, then you are liable for a pension.

5: You can invest more in Provident Fund, its called VPF

You can always invest more than 12% of your basic salary in Employee Provident Fund which is called VPF (Voluntary Provident Fund). In this case, the excess amount will be invested in PF and you will keep on getting the interest, but the employer is not supposed to match your contribution. He will just invest up to a maximum of 12% of your basic, not more than that.

6: Withdrawing of EPF amount at job change is illegal

Almost everyone thinks that withdrawing of your Employee Provident Fund amount after a job switch is totally fine and allowed, however as per the EPF Rules, it’s illegal.

You can only withdraw your Employee provident fund money, only if you have no job at the time of withdrawing your money and if 2 months have passed. The only transfer is allowed in case you get a new job and you switch to it.

While there are no cases where EPF office tracks these things and takes up this matter, still just for your information you should know that if you got a new job and took it and then you are applying for withdrawal, it’s illegal as per law.

What in the case of EPS?

In the case of EPS, if the service period is less than 10 years, you have the option to either withdraw your corpus or get it transferred by obtaining a ‘Scheme Certificate’. Once, the service period crosses 10 years, the withdrawal option ceases.

Just for your information, you can withdraw your EPF money without the help of past employer signature by attesting your withdrawal form by a bank manager or some gazetted officer. I hope you are clear about EPF withdrawal rules.

7: One can opt-out of EPF if he wants

Yes!. I know this might be a surprising fact for many, but if one’s basic salary per month is more than Rs 15,000, he has an option to opt-out of PF and not be part of it. In which case he will get all his salary in hand (without anything deducted every month).

But the sad part is that one has to opt-out of Provident Fund at the start of his job. If a person has been part of EPF even once in his life, then he can’t opt-out of it. So if you have already had EPF in your life.

This option is not for you, but if you are new to the job and your PF account number still does not exist, you can tell your employer that you don’t want to be part of Employee provident fund. You will have to fill up form 11 for this.

8: Your EPF gives you some life insurance too

A lot of people might not know that in case a company is not providing group life insurance cover to its employees, in that case, the employee is given a small life cover through EPF. This is because there is something called Employees’ Deposit Linked Insurance (EDLI) scheme and your organization has to contribute 0.5% of your monthly basic pay, capped at Rs 15,000, as premium for your life cover.

However, companies that already have life insurance benefits to employees as part of the company, are exempted from this EDLI scheme. The bad part of this EDLI scheme is that the life cover under this option is very low and that’s the maximum amount of Rs. 60,000. While this is peanuts for most of the people in big cities.

For employees in small scale industries and small cities, this amount of Rs 60,000 will still count something.

9: You can use EPF money can be withdrawn at special occasions

So now you know that EPF withdrawal is not permitted if you are still working. But there are occasions when Employee provident fund withdrawal is allowed.

While you cannot withdraw it fully, you can withdraw a partial amount. Following is a list of events when you can withdraw the Provident Fund amount and the conditions you need to fulfill

1. Marriage or education of self, children or siblings

– You should have completed a minimum of seven years of service.

– The maximum amount you can draw is 50% of your contribution

– You can avail of it three times in your working life.

– You will have to submit the wedding invite or a certified copy of the fee payable.

2. Medical treatment for Self or family (spouse, children, dependent parents)

– For major surgical operations or for TB, leprosy, paralysis, cancer, mental or heart ailments

– The maximum amount you can draw is 6 times your salary

– You must show proof of hospitalization for one month or more with leave certificate for that period from your employer.

3. Repay a housing loan for a house in the name of self, spouse or owned jointly

– You should have completed at least 10 years of service.

– You are eligible to withdraw an amount that is up to 36 times your wages.

4. Alterations/repairs to an existing home for a house in the name of self, spouse or jointly

– You need a minimum service of five years (10 years for repairs) after the house was built/bought.

– You can draw up to 12 times the wages, only once.

5. Construction or purchase of a house or flat/site or plot for self or spouse or joint ownership

– You should have completed at least five years of service.

– The maximum amount you can avail of is 36 times your wages. To buy a site or plot, the amount is 24 times your salary.

– It can be avail of it just once during the entire service.

10: You can file an RTI application for EPF issues

Did you know that you can file an RTI applicable to get any kind of information regarding your EPF? You can file it if you are facing issues like no clarity about EPF balance, no action taken for your EPF withdrawal or transfer. To find out information about other issues on the Provident Fund. I have done a detailed post on how to file an RTI for your EPF issue.

Watch this video to know how to file RTI for EPF withdrawal or transfer issues:

UPDATES

In the recent budget 2015, the govt has made it clear that now an employee can choose between EPF and NPS. The employer will have to give this option.

Now the new system of UAN is in place for EPF, which has made a lot of things more simpler

Conclusion on EPF rules

The overall Employee provident fund rules are too complicated and very old. A common man does not know all these EPF rules, but knowing these minimum 10 EPF rules will help him in his financial life.