So the topic of debate today is “Is Cryptocurrency like Bitcoin be considered as an asset class?”

Till now we all know that there are many asset classes like Equity, Fixed Income, Real Estate, Cash and Commodities. Some people also argue if “Art” is an asset class or not.

And now, there is this new debate is crypto is the new asset class in itself or just an alternate currency or at best a speculative instrument?

Does Cryptocurrency fall under the definition of “Asset Class”?

An asset class is a grouping of investments that exhibit similar characteristics and are subject to the same laws and regulations. Asset classes are made up of instruments which often behave similarly to one another in the marketplace.

If you look at “fixed income” asset class and see various instruments under it like Fixed Deposit, PPF, EPF, Senior Citizen Saving Scheme, NSC, Debt mutual funds etc. you will see that they have common characteristics (As they all are basically a loan given to someone) and various laws and regulations are similar across the country and globally (though the names of products can be different)

The same thing can be said to the Real estate asset class where Land, bungalow, REIT, Commercial shops all are physical spaces and their prices go up and down mainly due to similar reasons.

Can this be said for various cryptocurrencies also?

While all of the cryptocurrencies are basically a digital payment alternative based on blockchain technology, we are not very sure if it can also be considered a “store of value” unlike other asset classes. Also, there is no common agreement on how various countries want to see cryptocurrency? While there are various countries that have legalized crypto, there are many that have not done that.

At the same time, a large chunk of crypto investors is buying it mainly for speculative reasons and not as a fundamental investment instrument where they want it to grow in value due to some fundamental reason linked to the economy or its usage.

Why I personally don’t want to consider Crypto as an asset class?

Cryptocurrencies have gained extreme popularity in the last 3-4 yrs and major crypto’s like Bitcoin, Ethereum, Tether etc has seen its market cap go into billions. It’s a complex world based on a very complex technology, which is again not like other asset classes which are quite easy to explain and understand for a common man.

Try explaining Real Estate or Equity to someone against the Crypto mining process and you will understand what I am trying to say.

Another reason why I personally don’t consider Crypto as an asset class is that cryptocurrency is in the end purely a software code. While it’s widely accepted and used, Are we saying that something which is so much dependent on a computer and electricity is considered as an asset class? What will happen if one day the world runs out of energy or all computers crash?

In the same case, things like equity, debt, real estate, cash (in any form), commodities, art all will survive and be there in some form.

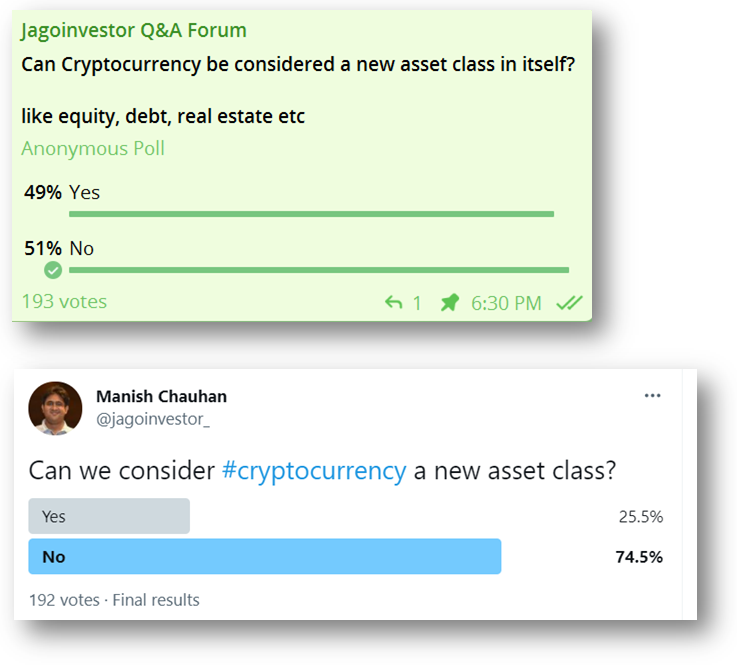

When I asked this question on our telegram group and on Twitter, here were the responses.

Do you consider Crypto as another asset class or just a new-age online payment technology?

Coming to you, it’s also a matter of perception if you want to consider it as an asset class or not. Can you please share your thought process around it? What do you consider it?

Disclaimer: I am not saying that cryptocurrencies will not rise in value? All I am debating is if it shall fall under the definition of asset class or not?

Do you know that there is a possibility that your grandparents or someone else in the family might have some bank account or some policy that you are not aware of till today and the money is lying unclaimed for decades?

Yes, that can happen!!

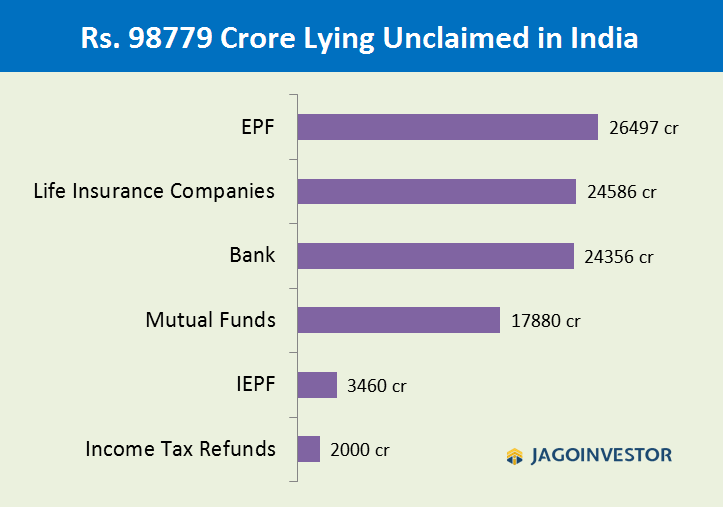

Can you believe that a whopping Rs 98,779 crore is lying in various investment products in India like banks, EPF, PPF, Mutual funds, LIC, and many other entities!!

In the last 18 months, so many people lost their lives and their families had no idea of the investments made by them, or if they had any life insurance policy or not. A lot of them still don’t know and will never come to know probably.

What happens to that money? How will family members get access to them? How will they claim it?

They WON’T!

Here is the breakup of how much money is lying unclaimed at various places in India, have a look!

Let’s talk about these

Rs 24,356 in Banks

As per the RBI report, Rs 24356 crore is lying unclaimed in around 8.1 crore bank accounts as of December 31, 2020. This turns out to be close to Rs 3,000 on an average per bank account. The biggest share in this unclaimed money is in SBI bank and then other private sector banks.

Rs 26,497 crores in EPF

This is the amount of money lying unclaimed in EPF accounts across the country. Some of this money may be of those people, who have not withdrawn the money after changing or leaving jobs, but a bigger chunk is lying there for years and years and many of them may never be claimed as the families are not aware of these investments

Rs 17,880 crores in Mutual Funds

A big chunk of money is also lying in inactive folios which is close to Rs 17,880 crores. A lot of investors have invested in mutual funds in physical format decades back and many family members may not be aware of these investments after their demise. This unclaimed amount is close to a little less than 1% of the entire AUM of mutual funds.

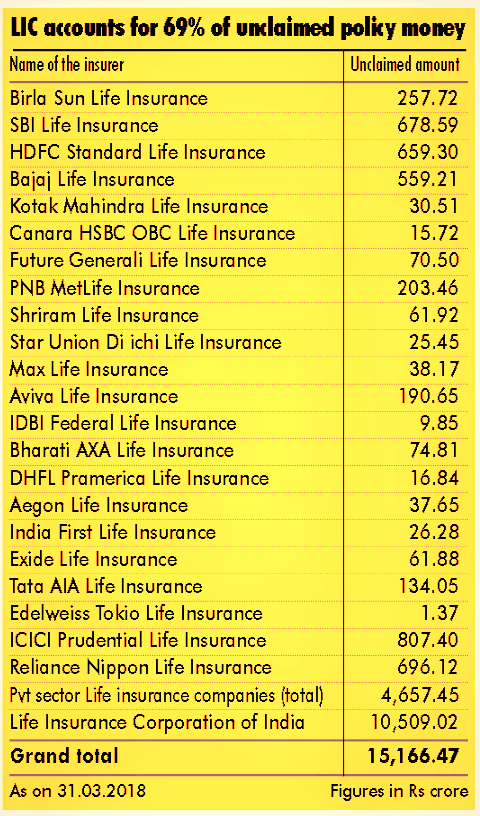

Rs 24,586 crore with Insurance Companies

LIC alone had close to 10,509 crores lying unclaimed with them as of Mar 31, 2018, and another 4,657 crore was with private insurance companies. The current figures as per IRDA is at a whopping 24,586 crore with all the insurance companies combined. Most of this is with LIC and you know there are so many policies that are never claimed after maturity due to various reasons.

Here is the old breakup of these amounts companies wise as per financial chronicle report

Rs 3,460 crores with IEPF

A big chunk of money is also lying with IEPF in form of unclaimed dividends and debentures etc., which were lying idle and no one, claimed them back on time. These amounts are transferred to something called IEPF after 7 yrs which is then used in things like investors’ awareness and protection of the interests of investors. Moneylife did an extensive story on this entire topic

Rs 2000 crore from Income Tax Refunds

As per a 2015 report by NDTV, close to Rs 2,000 crore of tax refunds were lying unclaimed with them. If a person pays the extra tax due to excess TDS deduction, one can claim the refund back by filing the returns (for the last 6 yrs). However many times investors are not even aware of these refunds or due to laziness, they don’t file the returns. Now the figures must be on the higher end.

Where does all this unclaimed money go?

The question is – If all this money is unclaimed, who exactly gets benefitted? Does the bank or insurance company keep all this money and just use it for their own benefit unless someone does not claim it back?

The answer to that is that govt has formed some of the FUNDS where these amounts shall get transferred after some number of years and that fund will be used for some purpose. Here are those funds

1. Senior Citizen Welfare Fund (SCWF)

All the unclaimed money from EPF, PPF, Insurance companies and postal deposits go to Senior Citizen Welfare Scheme which works for the betterment of senior citizens who are below poverty line in the country. I am really not clear which are the schemes or ways they do it.

2. Depositor Education and Awareness Fund (DEAF)

All the money which is lying claimed in the banks like saving bank account, fixed and recurring deposits, demand drafts etc. is transferred to this fund called DEAF and it’s used for depositor’s awareness and protection.. Which I really don’t understand what it means !

3. Investor Education Protection Fund Authority (IEPF)

IEPF is another fund which is created for investor protection and financial awareness and it gets all the unclaimed dividends, shares, matured unclaimed dividends etc. I have already written about how to claim refund from IEPF here

Make sure your money does not become part of unclaimed money in future

The learning from this is that you shall make sure that all your investments details etc. are shared with your family properly and they shall be aware of it.

For the last 2-3 yrs, more and more investors want to diversify beyond Indian equities and want to invest in other countries stocks.

We all have seen news of how some international stocks like Amazon, Facebook, and Tesla etc are doing wonderful and today we will see how Indian investors can also invest in these international stocks in 3 ways

#1 – Directly through a Broker website

One of the ways to invest in global equities is through a brokerage house by opening a Demat/trading account.

This can either be an Indian brokerage house like ICICIDirect, Motilal Oswal which has tie-up with a foreign brokerage house again. Or it can also be some new-age startups like Vested, IndMoney which has a direct tie-up with the global brokerage houses.

Once your account is opened, you can transfer the money to that account and do the buy and sell transactions. However note that these are quite expensive in nature, simply because there are transfer fees (while sending and while taking back the money in your account) which can make them quite expensive especially if your ticket size is quite small.

Here is a simple illustration given in this tweet on only Rs 6,166 get invested when you put Rs 10,000 because a lot of money gets eaten up in the charges etc.

Tempted to invest in US Stocks directly?

Hold your horses✋

If you can’t invest at least ₹1 Lakh at a time, you’re doomed to make significant losses the moment you transfer???? into your US broker a/c.

Huge remittance charges (per transaction) is the devil no one talks about ???? pic.twitter.com/OJX39TvXTK

This simply means that this route is only for someone whose transactions is of large size, and someone who wants the fun of selecting the stocks themselves and reviews them on their own. I feel this is a cumbersome method of investing out of India, simply due to the paperwork and hassles involved.

#2 – Investing through a mutual fund

Another way to invest in international stocks is through a mutual fund. The best part of this is that for a retail investor, there is no change in process and no extra paperwork. You can simply buy the units of mutual funds or do the SIP in the same manner.

Another great advantage is that you get tons of variety and options you get through a mutual fund. If you want to invest directly in stocks through a broker, mostly you will see the option for investing in US-based companies only.

However, with mutual funds, you can get options based on countries, emerging markets, sectors or geographies.. Here are some examples

By Countries / Region

These are mutual funds that focus mostly on a specific country or a region.

Edelweiss Greater China Equity Off-shore Fund

DSP US Flexible Equity

Edelweiss US Value Equity Offshore Fund

Edelweiss Europe Dynamic Equity Offshore Fund

Edelweiss Asean Equity Off Shore Fund

HSBC Brazil Fund Gr Dir

Global or Emerging Markets Funds (which invested in various countries)

These are funds that mainly are not linked to any country, but are ready to invest in various countries stocks depending on growth sectors and opportunities spotted.

Kotak Global Emerging Mkt

ABSL Global Emerging Opp

PGIM India Global Equity Opp

Sundaram Global Brand Fund

Edelweiss Emerging Mkts Opp Equity Offshore Fund

Mirae Asset NYSE FANG + ETF FOF

Kotak NASDAQ 100 FOF

Motilal Oswal S&P 500 Index Fund

Funds based on a theme/sector

Finally, there are funds that are focused on a specific sector or theme and feel that it’s too promising. It can be technology, Real estate or consumption etc.

Edelweiss US Technology Equity FOF

Axis Global Innovation FOF

Invesco India Invesco Global Consumer Trends FOF

DSP World Gold Fund

Kotak Intl REIT FOF

DSP World Energy

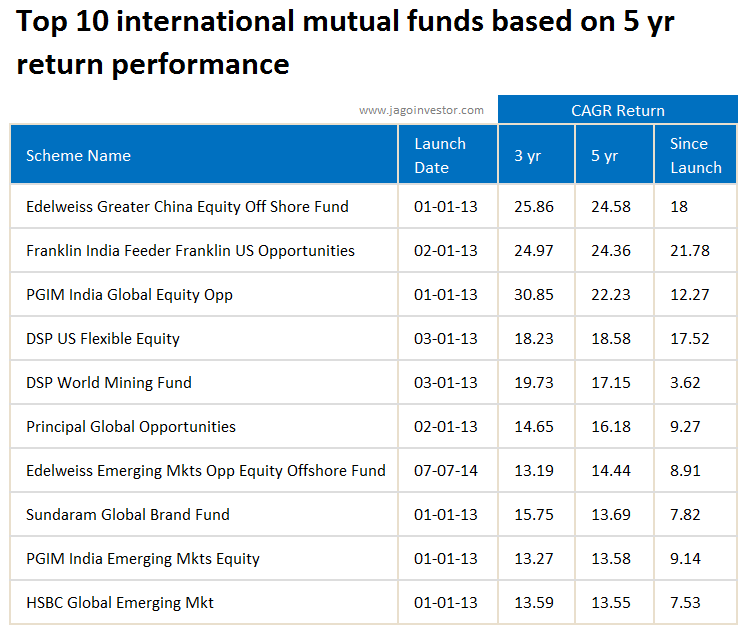

I would to also show you the top 10 international mutual funds based on 5 yrs returns.

Know this, before you invest in international mutual funds

Note that it’s also quite fancy to think that you are investing in an international portfolio, so many people go overboard and put a very high amount in these funds. Look at these funds mainly as a way to diversify your portfolio and reduce the dependence on Indian equities only. There is no compulsion that you have to invest out of India.

Also, on the taxation front, one big disadvantage of these international mutual funds is that they are taxed like a debt fund. Yes- so any profits you earn before 3 yrs, they will be treated as a short term capital gain and taxed at your income slab rates.

Final point is that these are all mostly funds of funds at the end of the day, which means that they are just a mutual fund that is buying the mutual fund units of another foreign mutual fund (that’s totally ok). So their expense ratio may be a little on the higher side!. But if they are saying you from all hassles, paperwork and guesswork, I think it’s worth paying the fees and participate in the fund.

Do let me know if you have any questions on investing in global equities?

Model Tenant Act, 2021 is very soon going to be a reality in India and it’s mainly to set up the rules and protect the rights of tenants and property owners from each other.

The rental market of properties is a very vibrant and deep market in India and every year millions of people rent out properties (residential and non-residential) in India.

At one end, tenants think that property owners are bloodsuckers, who just want to withhold the security money at any cost and try to dominate them. On the other hand, property owners feel tenants are also horrible who do not care for properties and do a lot of damage which forces them to keep enough security deposit with them.

10 Important Rules under Model Tenancy Act 2021

Many times, though an agreement is made legally, on the ground level things don’t work out and there is a lack of professional relationships. This Model tenancy Act 2021 is trying to exactly solve this and wants to lay down enough guidelines, rules which will help both parties.

Here are some of the most important rules you should be aware of the model tenancy act, 2021

1. Heavy Penalty if the tenant does not vacate premises on time

Once the agreement is over, there is a maximum of 6 months of extension on the same conditions and rules which are mentioned in the agreement. But if even after this 6-month extension, (or if the tenancy is terminated by notice or order) the tenant does not leave the premises, then there are heavy penalties levied on them. They will have to pay double the rent for the first 2 months, and then 4 times rent for another 2 months and then 6 times the rent for another 2 months.

2. The security deposit can’t exceed more than 2 months’ rent

As per the law, the security deposit which homeowners take from tenants can’t be more than 2 months of rent. In cities like Bengaluru, one has to deposit the security deposit as high as 10-12 months of rent, which many tenants complain about. However, at the same time, a lot of homeowners feel, it’s too little money to cover the risk of having the premises damaged by the notorious tenants. Note that this limit of 2 months’ rent is only for residential properties. In the case of non-commercial premises, the security deposit can be a maximum of 6 months’ rent.

On Twitter, Krish gave his real-life example which shows us how 2 months of the deposit is not enough in real life for property owners

All wood work gone, taps broken, geysers gone, electrical wiring got burnt, dampness & cracks on the walls, painting peeled off, tiles broken in bathrooms, huge dust in lot of places.

I was abroad and couldn’t visit. Full interiors redone and sold off for peace of mind.

3. Separate Rent authorities, courts & tribunals set up in each district

A separate 3 tier system will be created in each district for handling the cases related to the rental market. A civil court will not have jurisdiction over these cases which come under Model Tenancy Act. At the first level, there will be rent authority, then a rent court and finally a rent tribunal will be set under each district. This will make sure that a separate resolution system will be set up for these things.

4. Written Agreement is mandatory

Now a written agreement is mandatory when any premise is given on rent. I guess anyways most of the people were making a proper agreement, but now it’s a law in itself. This agreement is also to be submitted to the concerned rent authority within 2 months of the agreement date. There will be some digital platform that will be set up for this as per the current wordings.

5. The landlord cannot stop the essential supplies of the premises

It mentioned that the property owner cannot stop the supply of any essential supply like water, electricity etc. just because there is some dispute with the tenant. In real life, it’s seen that if there is any dispute or argument, the homeowners take these steps to “teach a lesson” to the tenants. It is mainly to protect the rights of tenants as far as they have occupied the premises. If the homeowner still does this, the tenants can complain to the rent authority and order can be passed by them to restore the services and also put a penalty on the homeowner

6. No structural changes or sub-letting of property

The tenant cannot make any structural changes in the property, nor they can sub-let a portion of the property to someone else without the consent of the property owner. If sub-letting is to be allowed, a supplementary agreement has to be made and even that has to be submitted to the rent authority

7. Eviction of the tenant on certain grounds

If the tenant has to be evicted, then the property owner can’t just appear one day and order the eviction. It has to be done only by seeking eviction through the rent authority and it can be done on certain grounds like

refusal to pay the agreed rent ;

failure to pay rent for more than two months;

parting of possession of part or whole of premises without the written consent of landlord;

misuse of premises even after receiving written notices to desist from such misuse; and

structural change by the tenant without written consent.

8. Rent Revision can happen only as an agreement

The rents can’t be increased arbitrarily now, it has to happen only as per the agreement which was written and agreed on. This will help the unorganized rental market where many times, homeowners increase the rent many times just to make sure people leave the house on their own.

9. Respect of Privacy and Rights of Tenants

The law also tries to establish the fact that once the tenant has occupied the house, the property owner can’t treat them in the wrong way and can enter the premises anytime without notice just because of the fact that they are the owners. They have to inform that tenant about their visit 24 hrs. before the entry (through an electronic medium). No doubt that this is not applicable if your relationship with the other party is cordial and friendly. This point is mainly there to protect their rights and privacy.

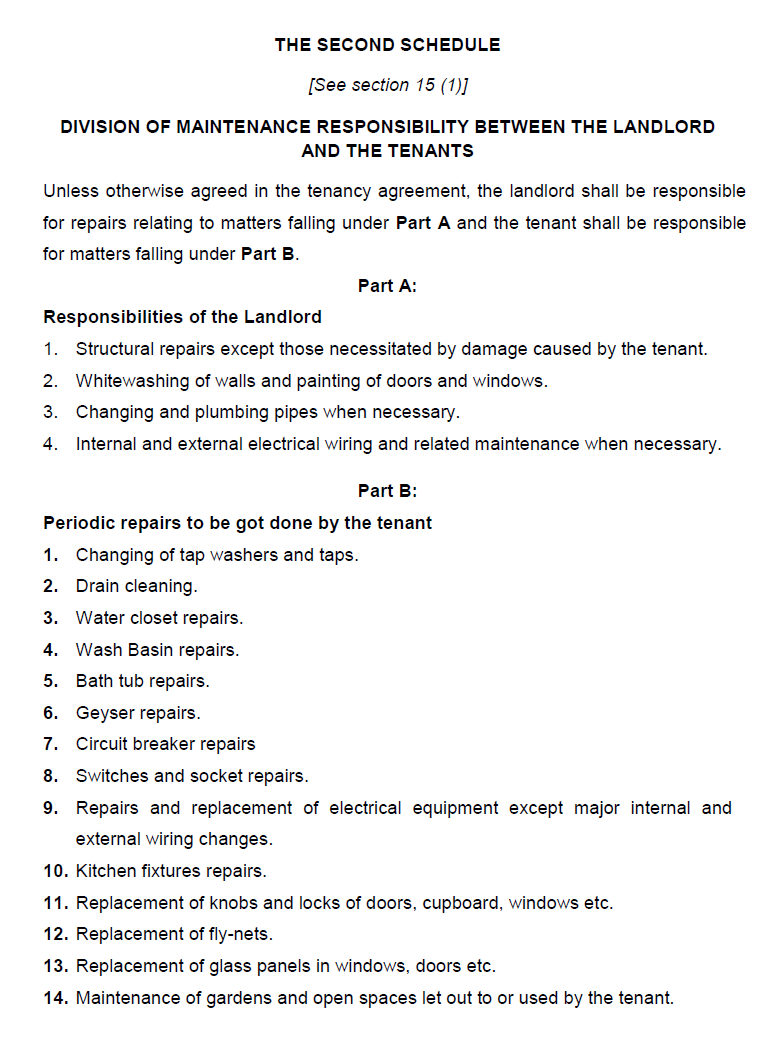

10. Roles and Responsibilities of both parties

The law also defines the roles and responsibilities of landlords and tenants and tells what has to be fixed by whom. For example, It is the tenant responsibility to do most of the repairs and replacement of small components like Wash Basic Repair, Taps, switches and sockets. On the other hand, the landlord is responsible for the whitewashing of walls (hello Bengaluru). In the 2nd schedule of the act, all the details are given which I am putting below

Important Points

These rules will not be on a retrospective basis and will not impact the old agreements. It’s only for new one’s

These rules do not apply for premises like hotels, lodges, or any central or state govt owned properties, or even premises owned by corporates, universities or religious entities etc

Will Model Tenancy Act 2021 really work on the ground level?

Many people raised the point of this act will really work at ground level or not. One person said to me on Twitter that the Indian rental market is a seller’s market and all these laws won’t work, as property owners will also find some other way to get away.

I feel that over time, the law will get implemented, if not in short term. The country is huge and any law like this takes a lot of time to get into the system. But the good part is that at least govt is thinking about this issue and trying to fix things. The law may not be 100% perfect, but things get amended over time and that will happen with this one too.

One feeling which I was getting is that the law is trying to micro-manage many things and in real life, I think it should have not done that.

What do you think about this new law? Please share your opinion in the comments section below

Today I will tell you about loan against property (LAP)

If you have a property that is free from any loan, then you can take a loan by keeping that property as collateral

Loan Against Property (LAP)

A Loan against Property (LAP) is a secured loan availed against a commercial or residential property kept as collateral with the lender. As the funds come with no end usage restriction, borrowers can utilize the funds for various purposes such as business expansion, weddings, child’s education, etc.

Benefits of LAP –

Simple approval process

Attractive interest rates

Continuous ownership

Easy and hassle-free documentation

Optimum use of a property

Claiming the interest as expenses (only for business person)

Eligibility criteria for LAP

A loan against property is offered to the following individuals –

a) Salaried– An individual who is in permanent service in the government or a reputed company. Further, he/she should be above the age of 24 years at the time of loan commencement and up to the age of superannuation.

b) Self-employed Businessmen – Any individual filing Income Tax Return (ITR) and who is over 24 years of age at the time of loan commencement and up to 65 years at the time of maturity.

c) Self-employed Professionals – Professionals such as doctors, engineers, dentists, architects, chartered accountants, cost accountants, company secretaries, and management consultants can apply. The age criterion is similar to that of self-employed individuals.

Documents required for LAP

[su_table responsive=”yes”]

Salaried Individuals

Self-Employed Professionals/Businessmen

Application form, photograph attached

Application form, photograph attached

Valid photo identity (such as Voter Id card, Passport, Aadhaar Card, Pan Card, Driving License)

Valid photo identity (such as Voter Id card, Passport, Aadhaar Card, Pan Card, Driving License)

Proof of current residence

Proof of current residence

Latest salary slips (minimum 3)

Proof of business existence, Certificates of educational qualifications

Form 16

For Professionals – Last 3 years IT returns (self and business), Last 3 years Balance Sheets and P&L statements.

For Businessmen – The business profile, Last 3 years IT returns (self and business), Last 3 years Balance Sheets and P&L statements.

List of Directors and Shareholders with their individual shareholding certified by a CA / CS in case of the business entity being a company.

Memorandum and Articles of Association of the Company.

A partnership deed in the case of the business entity is a partnership firm.

Bank statements of the last six months

Bank statements of the last six months – both business and personal in case of businessmen

A cheque for processing fee

A cheque for processing fee

[/su_table]

FAQs –

What are the types of properties against which LAP can be taken?

Self-Owned and Self-Occupied Residential Property

Self-Owned but Rented Residential Property

Self-Owned Piece of Land

Self-Owned Commercial Property

Self-Owned but Rented Commercial Property

Can I take a loan against the property for any reason?

Loans against the property can be taken for the following purposes. They are as follows –

For Business Expansion

Getting your son/daughter married

Sending your son/daughter for higher studies abroad

Funding your dream vacation

Funding medical treatments

What is the maximum loan amount a person can get in LAP?

The maximum loan amount a person can get against LAP is up to Rs 25 crore. However, the LAP should not exceed above 60% of the market value of the property. The maximum loan availed will vary from bank to bank.

What is the minimum credit score required to get a LAP?

What can be the maximum repayment tenure and interest rate of the LAP?

The maximum repayment tenure of LAP is 15 to 20 years. Whereas the interest rate will vary from bank to bank but the interest rate will range somewhat between 9.80% p.a to 16.60% p.a.

Conclusion –

This was all that I wanted to share in this article. You all can post queries in the comment section.

Today we are releasing a FREE, very exhaustive and detailed google sheet for everyone which can act as a single point of information for your family to access all your data and information related to your financial life.

In this COVID Pandemic, a lot of families lost a family member and in many cases, it was the main breadwinner of the family. This left them in a situation where they had no idea about the insurance and investments made. They had to literally find each and every small piece of information from scratch and it was a very frustrating experience.

A lot of this be avoided if one just creates a master document file (also called as BlackBox file) and save all the information in that and share that file with their family.

Can I request you to like the tweet and also retweet the same so that it can reach more and more people.

What all does this BlackBox file has?

Various Investments Details

Various Insurance Details

Various Contact Details

Various Important ID

Assets and Liabilities Section

Checklist of what to do after the death of account holder

Term Insurance Claim Process

Banking Claim Process

Mutual Funds Claim Process

PPF & EPF Claim Process

NPS Claim Process

Property Claim Process

Demat Claim Process

Video on 20 things to do post-death of a family member (English & Hindi)

Intro video on about this Sheet

Please copy the master file in your google account and fill it up and then share it with your spouse/family members. Do share this link in your office platform or other WhatsApp groups you are part of.

Also, do share your feedback about the sheet and if you liked it?

Do you exactly understand what the Claim Settlement Ratio in Insurance is?

A lot of people just look at the claim settlement ratio and make an opinion about an insurance company. In this article, let me break some myths and help you understand more about the claim settlement ratio.

What is Claim Settlement Ratio?

In simple words, the claim settlement ratio is the percentage of claims paid in a financial year.

Claim Settlement Ratio = (No of Claim Paid / No of Claims Received)

So if a company gets 1000 claims in a year and pays 985 of them, then its claim settlement ratio for that year will be 98.5%. An important point to note here is that it’s about the number of claims and not the number of claims.

What type of Claims is considered in the Claim Settlement Ratio?

Generally, most of the people willing to buy a term plan look for this ratio as they are concerned about the claim getting paid in case of their early death. But claim settlement ratio is not the same as the “death claim settlement ratio”

In the calculation of the claim settlement ratio (in the case of life insurers), all types of claims are considered like.

Death Claim: The claims once the policyholder dies

Maturity Claims: Policies that are maturing and needs to be settled

Surrender Claims: Policies that are closed prematurely and surrendered

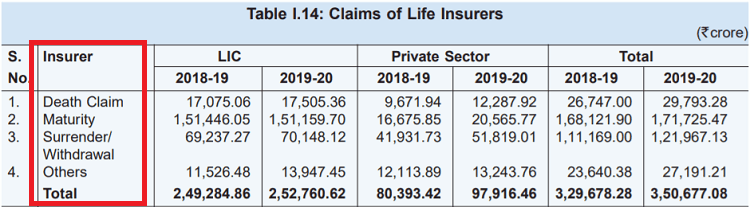

Here is the breakup from the IRDA report of 2019-2020, where you can see the number of claims for LIC and private insurers

Is Claim Settlement Ratio a probability?

One of the biggest myths about CSR (Claim settlement ratio) is that it’s a probability of claim settlement. This is not true and often leads to misjudgment of an insurance company.

CSR is simply a way of representing the data and nothing else. It does not tell you about the intention of the company. Let me share this with an analogy

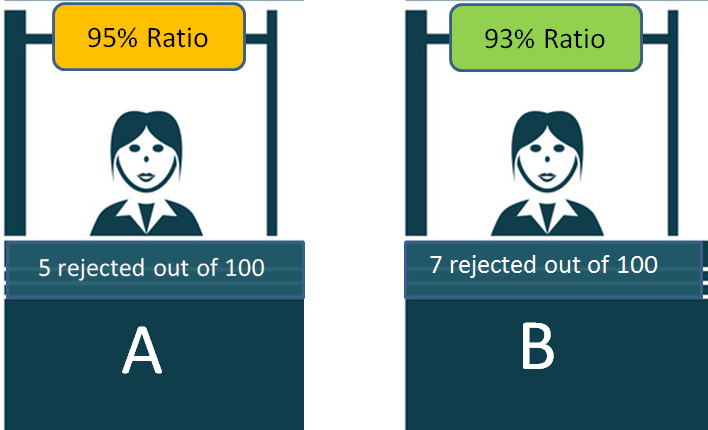

Imagine there are two VISA processing counters which are looking at documents of people and giving the VISA or rejecting it.

Now if the Visa will be approved or rejected depends mainly on how proper are the documents and the person and not depend on the person who is processing the Visa. If the documents and case fall into the rules set, then it will be approved, else it will not.

So imagine there are two counters A and B . Counter A rejects 5 people out of 100 and Counter B rejects 7 people out of 100.

Now, this simply means that counter A got 5 people who did not fit into the set rules or their documents had issues. In the same way counter, B got 7 people who had incomplete documents.

One cannot mistake these 93% (A) and 95% (B) as the probability of their visa getting rejected.

Hence, in the same way, the claim settlement ratio just tells you about what kind of claims did the insurance company received and how many of those claims were rejected. It’s not a probability.

Investors mostly have a very bad view of companies and attribute these rejections to their intentions, which is not a correct way to look at this ratio.

Does Claim Settlement Ratio depend on the policyholder?

Yes

A claim that will be rejected or accepted depends mostly on the policyholder itself. There are many people who file a claim which is bound to get rejected as it’s not valid as per the terms and conditions of the policy document.

Many policyholders also have a very vague and wrong impression of what is covered and what is not. They file claims based on flimsy assumptions and for things that are out of the scope of rules.

Let me give you an example.

Imagine a person who lied to the company while taking a term/health insurance, that he is a smoker and also went through some surgery in past. He lied to the company.

After some years the claim was filed (person died or got hospitalized) and now the company finds out the information provided by the insured person was false and hence the claim should not be paid in this case and it’s totally valid rejection.

So here it’s not the company who had the wrong intention but the customer who created a situation that led to claim rejection. Most of the policies which are rejected fall into this category.

From your end, you have to understand one thing. If you have bought your policy properly and revealed all the information properly, your claim will not be rejected. However, if you give reasons for the company to reject your claims, it will surely be rejected and there is nothing wrong with that.

What is Claim Intimation Ratio?

Claim Settlement Ratio tells you about “number of policies”, whereas Claim Intimation Ratio tells you about the “AMOUNT”

It tells you what percentage of the claim amount was paid out of the total claim amount which was claimed in a year.

Claim Intimation Ratio = (Amount Paid / Total Claim Amount)

Most people are not aware of this ratio, and this gives you better clarity about the claims paid by a company. It may happen that a company has a high claim settlement ratio, but its claim intimation ratio is lower than the other company.

Here is an example of how the Claim settlement ratio can be high despite a low intimation ratio

Company A and B receives 10 claims in a year as follows

9 claims of Rs 10 lacs each

1 claim of 1.1 crore

[su_table responsive=”yes”]

Company A

Company B

Claim Rejected

1 claim of 1.1 crores is rejected

2 claims of 10 lacs are rejected

Claim Settlement Ratio

9/10 = 90%

8/10 = 80%

Claim Intimation Ratio

90 lacs / 2 crores = 45%

1.8 crore / 2 crore = 90%

Comment

Claim settlement ratio is high, but not the amount paid

Claim settlement ratio is low, but the higher amount paid

[/su_table]

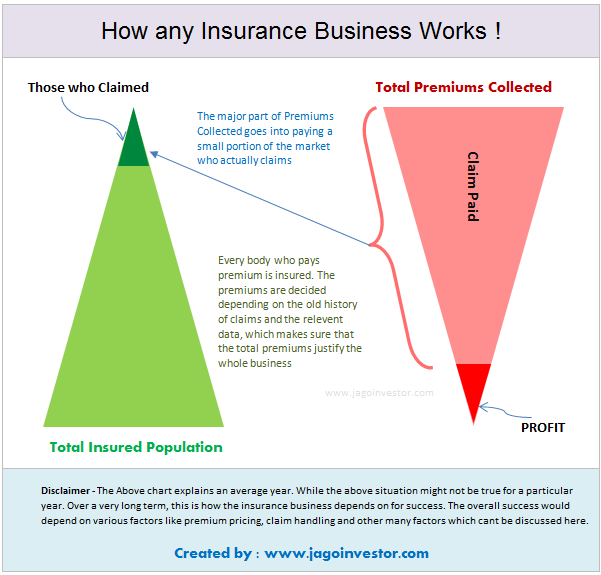

Business Model of an insurance company

As a customer, you should be very clear about the business model of an insurance company. An insurance company is a for-profit organization whose intention is to stay profitable and work for its profitability and also serve its customers as well.

The insurance company collects a small premium from a large number of people, but that money eventually goes only to a handful number of people who file for a claim. So in a way, it’s a shared resource which is given to those who are valid claimants.

In order to stay in business and be profitable, an insurance company has to reject all the claims which are not valid. If they start paying each and every claim without proper verification, they just won’t survive and it’s not in the customer’s interest.

This simply means that a company with not the best claim settlement ratio, in reality, is a good company because knows how to protect itself and not let a fraudster make a wrong claim.

A very important point to note is that a new insurance company will mostly be getting death claims in the starting 8-10 yrs and not any maturity claims which means their claim settlement ratio may look on the lower side.

How to buy an insurance policy?

Basically here is a high-level step by step process

Look at a company whose name you trust

Choose a company which has been few years old (this depends on you)

Choose a company whose product you like (features etc)

Check out the experience of other investors online about the company

Buy a policy with full honesty and by disclosing all information

Don’t lose your sleep over Claim Settlement Ratio

In the end, I just want to say that the claim settlement ratio is not a useful metric for any purpose and you should not lose your sleep over it. Don’t worry too much.

Shall you buy a single big health insurance policy or divide it between two policies (Base cover + a super top-up policy) for a cheaper premium?

The whole insurance industry is busy promoting and selling super top-up policies as a “cheaper way of upgrading” your health insurance cover. But no one is educating investors on the limitations of such combo or exactly why they are cheaper compared to a single cover.

Today, I will do that to the best of my abilities.

Investors have bought various combinations of base plan + super topup plan

5 lacs + 5 lacs

5 lacs + 10 lacs

10 lacs + 10 lacs

3 lacs + 7 lacs

10 lacs + 20 lacs

and many more…

Recently, we also saw health insurance policies of “Rs 1 crore” sum assured for unbelievable premiums and many investors have also opted for those. Basically, they are simply a combo of Rs 5 lacs + 95 lacs cover (with 5 lacs deductible).

Was that a great choice?

Let’s dive deeper!

Let’s start with an example!

A family of three people (with age 37 yrs, 36 yrs and 6 yrs) wants to buy a 25 lacs health insurance cover. They can do two things

[su_table responsive=”yes”]

Option

Policy

Premium

1st Option

Buy a single policy of 25 lacs sum assured (Max Bupa Reassure as an example)

Rs 28,091

2nd Option

Buy a base policy of 5 lacs (max Bupa reassure) with a premium of 15,104

And Buy a super topup policy of 20 lacs with 5 lacs deductible (Max Bupa Recharge Plan) with a premium of Rs 2,803

Rs 17,907

[/su_table]

In this case, the premiums of the combo (2nd option) is 37% cheaper.

Most of the investors think that both the policies are a “25 lacs cover policy” and the 2nd option is exactly the same as the 1st option but with a cheaper premium.

This is obviously not true!

How is it possible that you get the exact same thing, but with a cheaper premium?

If a combo is cheaper, surely it will also have its own limitations or will fall short of in some situations? That’s exactly what we are going to look at today.

Disclaimer – “Super Top-up” policies are a great choice

I don’t want to sound against super topup plans. They are a wonderful product and have a great role in health insurance, but problem is that people are buying them as a replacement for a strong base cover policy and living in the illusion that they are getting the exact same deal as a big cover.

Let’s start to get into details now.

1. Two Claims instead of a single claim

What does a person wish for at the time of a health insurance claim?

The answer is a smooth and hassle-free claim experience.

I have already made 3 different claims (2 in my own policy and 1 in my father in law policy) in the last few years and hence I can tell you that the claim process is something you dont want to complicate.

When you have a single policy, it means a single claim each time.

What happens when you have a combo plan? Let’s see!

If both policies are from the same insurer

If the base policy and super topup cover are from the same company, then it’s quite a smooth and seamless process, as they can internally cross-check things and coordination is much better. Basically, they have to technically anyways settle both claims, so they will combine them and process the whole thing faster and easily.

If both policies are from a different insurer

However, if both your policies are from different insurers, then it can get complicated and confusing. Don’t worry, you are not losing any money here, but surely it’s a bit of hassle and delay in follow-ups and coordination if the super topup plan gets triggered (which will happen when your base plan is not large enough). Also,

You will have to keep hold of 2 health insurance cards

Dealing with 2 claim forms especially for pre & post hospitalization claims (even in case of a cashless claim)

Communication for 2 policies (this may be easy when the insurer is the same)

And finally, in case of reimbursements, more documentation (hospital bills/prescriptions)

With 2 insurers, there may also be a wait time involved for getting the xerox of the bills/claim settlement letter

Also, imagine the scenario of how your family will be able to claim if you yourself will get hospitalized (due to any emergency). Will your spouse/family have enough understanding to follow the intimation and claim process from both the policies.

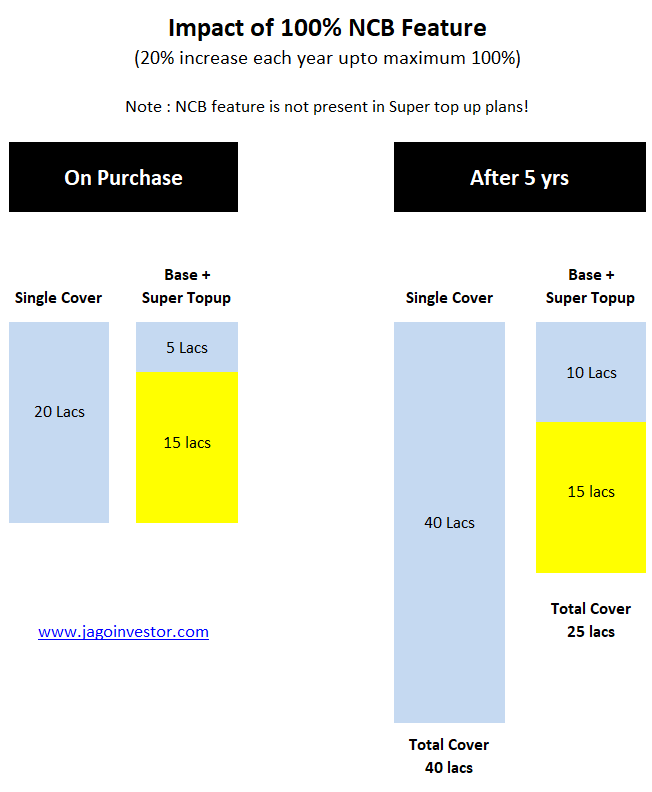

2. Lower Coverage due to NCB missing in Super topup

Contrary to popular belief, the combo (base + super top-up) gives you a lower coverage compared to a single large cover, simply because of the NCB component which many do not consider!

Surprised?

Almost all the policies come with the NCB feature (No Claim Bonus), where your sum assured keeps going up for every claim-free year. Here are some of the examples

[su_table responsive=”yes”]

Policy

NCB

Care Insurance

10% increase in sum assured up to a maximum of 50% of sum assured

Max Bupa Companion

20% increase in sum assured per year up to a maximum of 100% of sum assured

HDFC Ergo Optima Restore

50% increase in sum assured per year up to a maximum of 100% of sum assured

[/su_table]

Now let’s see a case.

Assume a person wants to buy a policy with a sum assured of 20 lacs. He has two options

[su_table responsive=”yes”]

Option

Option 1 – Single Cover

Option 2 – Combo

Combination!

The single policy of 20 lacs

The single policy of 5 lacs (base plan)

Super Topup cover of 15 lacs (with 5 lacs deductible)

NCB Benefit

20% each year (up to 100%)

20% each year (up to 100%) applies only on the base plan

NCB feature is NOT applicable in Super topup policies

Total Sum Assured at the start (when you buy policy)

20 Lacs

20 Lacs

Total Sum Assured after 5 yrs (claim-free years)

40 lacs

(base policy X 2)

25 lacs

(base policy X 2 + super topup)

[/su_table]

Now you understand why the premiums for super topup cover is less than the single large cover.

Here is the pictorial representation of the above example

So, you can see how after a few years there will be a gap of 15 lacs in sum assured in the combo plan. Now do the maths for a total cover of 10 lacs. What will happen if you divide it into a 5+5 combo?

3. Lower Coverage due to Recharge Benefit (2 large claims in a single year)

There is something called “Recharge benefit” in health insurance policies these days, which refills your policy again up to the sum assured when the sum assured reduces due to any claim. Like if you have a 10 lacs cover, and you claim for 4 lacs, then the policy will come down to 6 lacs, but then due to recharge benefit, the sum assured will again rise to 10 lacs (the added sum assured can not be used by the same person for same illness for which he/she claimed)

Now, let’s imagine a case

Assume, that in the worst case there are two big claims in the same financial year. Like what happened with few people in this Pandemic. Imagine one person getting hospitalized due to corona and then after 4-5 months, another person in the family also getting hospitalized. Or imagine someone in the family getting treated for a big illness and then after a few months, another family member getting hospitalized due to a severe accident also.

Very low chances of this happening. RIGHT?

Yes, but it can not be ruled out at all!. It’s the extreme end I know.

How will be the claim experience in both cases? Let’s compare the same example (forget NCB for the moment)

[su_table responsive=”yes”]

Option

Option 1 – Single Cover

Option 2 – Combo

What?

Single cover of 10 lacs

Single Cover of 5 lacs (base plan)

Super Topup cover of 5 lacs (with 5 lacs deductible)

1st Claim by husband for Rs 8 lacs

The claim will be paid for 8 lacs

5 lacs claim paid by the 1st base policy

3 lacs claim will be paid by super topup policy

2nd claim by a spouse in the same year for Rs 10 lacs

Because of the recharge benefit, the spouse will be able to claim for a total of Rs 10 lacs

Because of the recharge benefit, the base policy will pay 5 lacs

But the super topup will pay the remaining 2 lacs only.

3 lacs will have to be paid by policy-holder

LOSS of Rs 3 lacs here compared to 1st option

[/su_table]

The point is that recharge benefit can also come into play in some very unlikely situations, but that feature is missing in super topup plans.

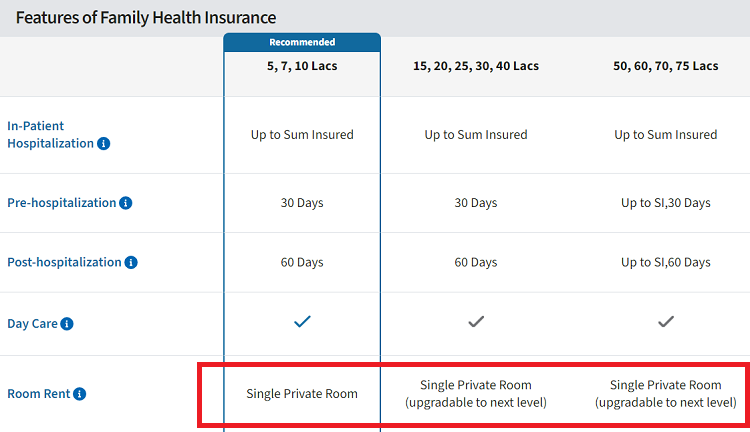

4. Difference in room rent limit

One major thing you have to consider is the difference between room rent limits in both base and super top-up.

Here is an example.

At the time of writing this article MaxBupa Reassure plan (recently launched) has no room rent limits.

However, its Health Recharge plan (the super topup policy) mentions that you only get a single private AC room in the plan.

Note that there are various types of single private AC rooms in a hospital. What you get from your insurance policies is the cheapest “Single Private AC room”.

Now let’s see 2 cases with an example

Total health cover: 20 lacs

The room category: A higher grade single AC room (higher quality and better facilities). Imagine the cheapest AC single room was not available or you wanted to go for the better facilities.

Final Bill amount: Rs 11 lacs

Case 1: You have a single policy of 20 lacs (Maxbupa Reassure, just for example)

In this case, because there is no room rent limit, your total claim amount is admissible and your claim process will happen smoothly.

Case 2 : Now imagine that you have a 20 lacs cover but in combo form.

You have a 5 lacs base plan (Reassure policy) + 15 lacs of super topup with a deductible of 5 lacs (Maxbupa Health Recharge)

Now the first policy will pay the claim of 5 lacs easily because there was no room rent limit in the policy.

However when you go to claim the additional 6 lacs in the super topup, here is what will happen.

If you had chosen the cheapest AC single room, your total claim of 6 lacs would have got admissible and processed. However, because you choose a higher category room, you will not be paid proportionately only.

If the room rent for the cheapest AC private room was Rs 8,000 per day whereas you choose the one whose rent was Rs 12,000 per day. You will be paid just 66.66% (2/3rd) of the claim amount, which is only Rs 4 lacs

This is called a Proportionate claim in health insurance. This may happen in reality if your base cover is a small amount and a big claim arises. If you choose the cheapest single private AC room, then there won’t be any issues, but otherwise, there can be issues and this can happen even if you bought the policies from the same insurer (like in this example I gave)

Another example is of Care Plan from “Care Insurance” formally known as Religare Care.

In Care Insurance the room rent for a 5 lacs base cover and 15 lacs of super topup cover is “Single Private AC Room”

Whereas if you take a larger single cover, the room rent is “Single Private AC room (upgradable to next level). This gives you enough flexibility and freedom to enjoy better quality health care and facilities. Sometimes, the single PVT AC room of the lowest category may not be what you wish for.

Imagine you need a bigger space and better facilities in the room, in that case, more deluxe rooms will be required by you. This is where you may lose in a big way (not today, but maybe in future or in case of large claims).

Old Policies – If someone has taken 3-5 lacs of sum assured a few years back (especially from PSU companies), there is a good chance that there is a room rent limit of 1% of sum assured (example – Oriental Happy family floater plan). Now if you are buying a super topup plan, there will surely be a difference in the room rent limit.

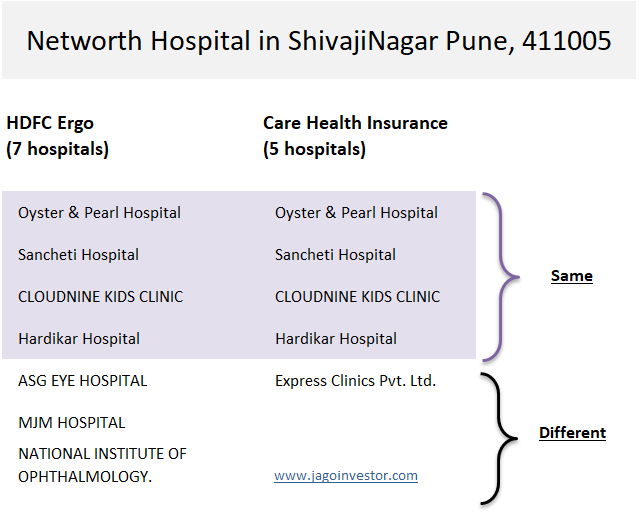

5. Different Cashless Network of Hospitals

If your base policy and super topup policies are from different companies, there may be a possibility that the hospitals in their cashless network are different to some extent. You may face some issues in future due to this.

Here is an example

I checked for network hospitals between HDFC Ergo and Care Insurance for Pincode 411005, which is Shivajinagar, Pune.

I found that HDFC Ergo has 7 hospitals and Care Insurance had only 5 hospitals in their network (in March 2021). Out of these 4 hospitals were common, the rest were different.

Now, what if your first policy is cashless but your sum assured in the first policy is small. In that case, the 2nd policy (super topup) will get triggered, but here you will first have to spend the money as it’s out of the network of the 2nd insurer)

You will then have to file a reimbursement claim later and do the documentation part too.

This will not be the case if you had a single large cover from the 1st company itself. You may argue that you will plan well before getting admitted to the hospital and try to match the one which is there in both policies, but trust me, in real life it will be tough.

When a doctor tells you or recommends that you get admitted to hospital XYZ (often he is also a practising doctor in that same hospital), it becomes quite tough to challenge that or counter his suggestion.

6. If policy tenures are different for both policies

In some cases, you can face issues in the claim, if you purchased both base and super topup policies in different months (same or different insurer, does not matter).

It may happen in some specific cases that your claim is not admissible under any policy.

This is explained very well by Mahavir Chopra of Beshak.org in his article here. I am just sharing what he wrote originally.

Say you have the following Combo plan.

Base plan of Rs. 2 Lakh (Plan year: January 2021 to December 2021)

Super Top-up of Rs. 5 Lakh with an annual deductible of Rs. 2 Lakhs (Plan year: April 2021 to March 2022). (This means for the Super Top-up to pay, the hospitalization expenses should cross Rs. 2 Lakhs in the policy period in question – which is April 2021 and March 2022.)

Now, say you undergo two hospitalizations in the year 2021.

The first one happens in January 2021, the bill amount is Rs. 2 Lakh. Now this is covered by your base-plan there is no confusion, and the claim amount is paid.

Next – you undergo a hospitalization in April 2021. And the bill comes to 1.5 Lakhs.

Now, take a guess on – who will pay for this?

A. Base-plan

B. Super Top-up

C. You

If you guessed A or B – then you’ll be up for a BIG surprise! Here’s how your two insurance plans will look at the second claim.

Your base plan will not pay: Because – you have already exhausted the cover amount available for the year (January 2021 – December 2021)

Your Super Top-up will not pay: Because the Super Top-up plan pays only when the hospitalization expenses during the policy period of April 2021 to March 2022 crosses the deductible of 2 Lakhs. In this case, the total hospitalization expenses during the period in question (Apr 21 to Mar 22) are only Rs. 1.5 Lakhs – hence the claim won’t be payable.

These were some limitations of the super top-up you should be aware of. It’s better to get educated about this aspect, rather than getting shocked and disappointed in future.

Some other small Differences

Apart from the major points discussed above, there are other minor but important points you should know

Annual Health Checkup Benefit: With a single large cover, you may get superior annual health checkup packages that cover more tests. But with combo plans, you may get normal test packages in both base policy and super topup, which is of less use as no one will do the test twice just for the sake of it. Some policies also offer health checkups only once in two years for smaller covers.

Hospital Cash Benefit – In many small base plans like 5-10 lacs, the hospital cash limit is Rs 1,000 per day. However for a bigger sum assured, the hospital cash will be in the range of 3000-4000. If you stay in the hospital for 10 days, this means getting 10k only in combo plan vs 40,000 in a single bigger cover.

Organ Donor Cover / Ambulance Charges – Again, a lower sum assured plan night have a lower benefit compared to a single big cover.

Waiting period – It might happen that the waiting period for pre-existing illness is different in both policies, just check that.

Pre & Post Hospitalization Tenure is different – It may also happen that both policies have different pre & post hospitalization tenure.

Other Minor Changes – Apart from the points above, there are many other minor differences in the bigger sum assured (single policy) which may be useful for you in some specific cases, which we are not covering here

How to look at Super Top-up policies? What is the right combination?

Everyone shall have a large enough cover with a single policy as the first step.

With NCB benefit, that large cover will also get ballooned to every large cover. And with recharge benefits, you will also get those edge cases covered. This will make sure that for many years to come, this single policy will be enough for you.

There are very low chances that in some worst cases, you may still have a very big claim when this single big large cover will not be enough, and that’s when super top-up cover shall come into the picture and that’s exactly why they were designed for.

To cover those extreme end cases!!!

But investors have just started using them with a small cover for the sake of saving some premiums. No doubt you will have a few thousand for many years to come, but there are also limitations which we talked about.

Considering the point above, the minimum base sum assured which I feel one shall take in 2021 is Rs 10 lacs. With NCB benefit, it may become a 15/20 lacs cover, which is good enough for the majority of claims. Anyways the average claim is quite small!

Does it mean you need to take a 50 lacs cover? NO 🙂

So what combination to buy?

Speaking for the majority, I think a Rs 10 lacs base policy with an NCB of 50%/100% and a super topup of 30-40 lacs with Rs 10 lacs deductible is a good enough choice right now. This will balance the premiums and coverage. If you want an even high single cover policy like 15-20 lacs, go ahead!

But also remember, that within the next 10-15 yrs, even the 10 lacs coverage may look like a small one and you may feel that the base policy should have been for at least 20-30 lacs. So take your decision after careful thought.

You can always upgrade your base cover sum assured at the time of renewal.

Do let me know if you have any queries or comments?

Credits – Thanks to Mahavir Chopra of Beshak.org to correct me on some points in this article and also give his valuable insights from time to time because of which I was able to bring depth to this article. Mahavir Chopra is a veteran and a well-known name in the insurance industry and they are doing some cool stuff on beshak.org in the area of insurance. Do check out their website!

This is a guest post by our reader Phani Kiran, who has tried to see personal finance from the software industry perspective. It will be more clear to software people but I think the way its written, everyone can understand it. Over to Phani Kiran

—

Hi All

DevOps needs no introduction to people working in the Software industry.

It is a set of best practices where Developers (Dev) and IT Operations (Ops) work together in delivering Software faster, cheaper and with better quality. This article tries to explain how DevOps can be applied to the world of “Personal Finance”.

For those who are hearing the term ‘DevOps’ for the first time, a rough analogy can be made with the FIRE (Financial Independence, Retire Early) movement. Both are best practices where we need to change our thinking, behaviour and tools but at the same time there’s nothing cast in stone and no one size fits all approach.

DevOps is needed as old software methodologies are no more relevant in a world where innovation needs to happen faster. Same with personal finance habits and practices – we need change as we move towards a lower PPF, EPF and Savings rate regime.

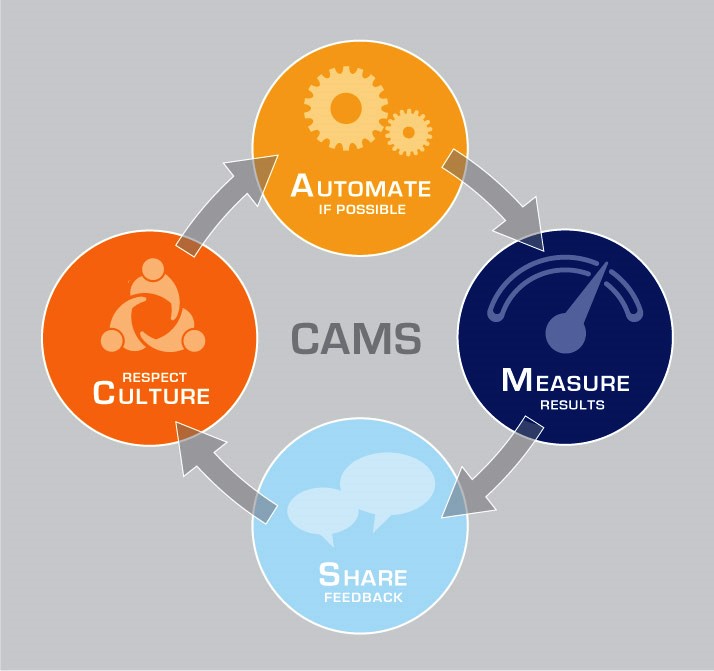

DevOps is frequently explained by CAMS Model (not your CAMSOnline :)). CAMS stands for

Culture

Automation

Measurement

Sharing.

Let’s see how each of these can be applied to Personal Finance.

C – Culture

Investors need to start moving away from the culture of only investing in ‘fixed’ income investments. As Warren Buffet, mentioned in his recent annual letter – “fixed-income investors face bleak future”.

Culture of treating tax saving as a separate and as a year-end only activity needs to be done away with.

Need to stop combining insurance and investment needs and start saying ‘No’ when resorted to pressure tactics from a so-called relative or a well-wisher selling ULIPs.

Start focusing on goal setting, risk profiling and asset allocation.

A – Automation

SIP (Systematic Investment Plan) is the automation you can make to your personal finance. In her book – ‘Let’s Talk Money’, Monika Halan talks about keeping investments on an auto-pilot mode using 3 different bank accounts. (Salary, Investment & Spending accounts)

Automating SIP or RD instalments inculcate discipline and removes personal biases. This can be your first step towards ‘passive investing’ as you no longer will be focusing on – if Market is High or Low.

For those who are prone to more discretionary spending, SIPs can be scheduled in the first half of the month so that you will establish a ‘Culture’ of Saving before Spending.

M – Measurement

The portfolio needs a periodic (quarterly or half-yearly depending on one’s perspective) review of performance. This is possible only when you have a target goal – ie. ‘target corpus’.

As they say about your year-end KPI (Key Performance Indicator) goals, equally personal goals like retirement, child’s education need to be SMART – Specific, Measurable, Achievable, Realistic and Timely.

Investment deductions on Auto-Pilot mode need course-correction as and when required. This doesn’t mean too much ‘Action’ (churning) though.

Measuring and monitoring returns and tracking whether you are on the path to achieving the desired goal or not needs more emphasis as equity returns can be volatile.

As SIPs automate the corpus-building phase, you can use SWPs (Systematic Withdrawal Plan) to move accrued investments to safer avenues once you are nearing a target goal.

S – Sharing

Keep your family in the loop about your financial and insurance decisions and documents.

Be a life-long learner and don’t hesitate to learn and talk in ‘numbers’ (compounding, inflation etc)

Read good blogs and attend personal finance workshops (Even DIY (Do It Yourself) needs some framework and strategy).

Just like DevOps improved software delivery productivity and reliability, following these principles should lead to a ‘virtuous cycle’ of prosperity. Keep your corpus build-up ‘flow’ by following a CI (Continuous Investment) strategy and let your periodic portfolio reviews provide the required ‘feedback loop’.

Happy Coding. I mean Happy Investing 🙂

–

So share if you liked this article or not in the comments section. And I thank Phani Kiran to give an attempt in writing this article.

Lots of people in India want to buy land, especially investors from big cities as land is a scarce commodity and it sounds amazing to build your own house on a piece of land instead of staying in apartments.

However, do remember that there are no specific loans available to buy agricultural land. The only loans available to buy the plot are for “residential plots”, which means that if you take these “plot loans”, you need to also construct a house within 2-3 yrs of buying the plot. You can’t just buy a residential plot and skip building the house.

However, many people do that. Some intentionally and some out of ignorance.

What exactly happens when you dont build the house on a plot taking on a loan?

Is there a penalty?

Can there be any actions against you?

What happens if you dont build the house on the plot?

When you take a plot loan, it comes at a lower interest rate because the assumption is that you will be building the house on that land within 2-3 yrs. But if you fail to do that and dont submit the required documents (completion certificate) to the lender on time, your loan will be converted to a normal loan and the interest rates will be increased by 2-3% with a retrospective starting date as per the agreement between you and the lender.

This means that your loan outstanding amount will go up by some amount due to this change and you will have to now pay that additional amount. At the end of 3 yrs, the bank will ask you for the proofs of construction, and if you fail to submit them, you will have to pay an additional amount.

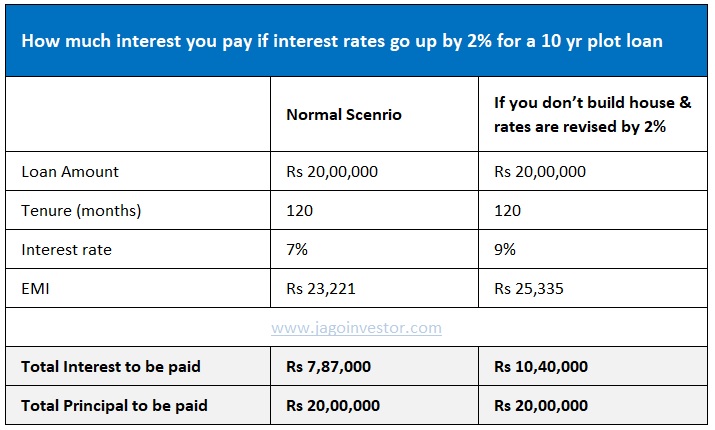

Here is an example of a Rs 20 lacs plot loan which is taken for 10 yrs @7% interest rate. The interest to be paid in this case will be 7.87 lacs apart from the 20 lacs principal amount.

Now if the interest rates are revised to 9% (2% increase) the interest, in this case, will increase to 10.4 lacs, which is 2.53 lacs more than the original amount.

Is there a single loan for plot and house cost?

Some banks like SBI (as told to me by a representative) first issue a plot loan and then after 2-3 yrs issue another home loan for the purpose of constructing the house (two separate loan account numbers), whereas some banks may issue a single loan itself for both purposes and it will be mentioned in the agreement (for example 40% amount is for plot and 60% for house construction).

Note that you can avail of 80C benefits as these loans are issued as home loans (the part of the loan which will be used for house construction).

Wrong information was given by the bank representatives

Many times you may get wrong and misleading information from the bank representative. They may tell you that “Nothing will happen after 3 yrs, dont worry” or “These are all just formalities..” mainly because he is interested in getting the loan approved due to their targets. This is wrong and makes sure you dont believe them. Always rely on what is written in the agreement.

Note that the loans are given at a cheaper rate for plots because there is a bigger agenda of RBI and govt that everyone shall access to housing. If you are buying the residential plot simply because you can sell it off in future for profits then you cant get the benefit of the lower interest rates.

For you, the interest rates will be revised because you will have to construct a house on the plot after 2-3 yrs as per rules.

Up to 60% to 70% of the property price is given as a loan depending on the bank.

These loans are given for a maximum of 15 yrs tenure

Points to remember before going for the plot loan

Make sure you take these plot loans only in case you are really interested in building the house. You can also ask the bank to first disburse only the loan amount for the plot and later release more amount at the time of house construction. It’s really not worth playing around with bank and playing tricks as it will mostly waste your time and you won’t gain much in case you dont want to build the house.

Here are some more important points which were shared by our reader Jayaprakash Reddy

Generally, banks calculate plot value based on the sale deed value, most of the cases sale deed value is lesser than the market value. Also, as mentioned above, banks like SBI will only consider sale deed value but some private banks might also look at market value in that area and which will be derived through their certified valuers. SBI will give a loan on plot purchase (House construction in future is intended) up to 60% of the sale deed value and it is the same with even private banks but that will be on market value.

There is no clarity even with bankers about what happens if you sell the plot within a year or two without construction, most of the representatives told me that it will be like closing a home loan but I guess that’s a false statement and depends on the bank and agreement if mentioned specifically in it.

The total loan again depends on the construction value in that area. For example in the area where you are purchasing a plot, the construction cost could be 1500/sqft. Then based on the sqft you are planning to construct the total loan amount will be derived. Let me put it in numbers:

Plot Area: 300 sq yards. – SBI bank loan – Sale deed value is 10000/sqyd – 30 lacs. For plot purchase – 60% of 30lacs will be given to you as a loan. 18lacs loan will be provided by the bank, this is given as cheque payment directly to the seller. For the construction of the house, they will provide it based on the sqft permission you got. For example, in a 300sqyrd plot if you are constructing G+2, then you might get permission to build ~3000sft (not an exact number). So the construction value of the house will be 3000*1500 = 45lacs, out of this bank will give you up to 80% loan, which again depends on your credit rating.

In total, you can get a 63 lacs (18+45) loan, provided you are eligible for such a loan based on your income.

To prevent malpractices, in the case of a home loan, the bank keeps the sale deed of the plot. With documents not available, one can not legally sell the plot. There can be a word of mouth agreement whereby the buyer can give money to the seller to release the loan and documents and then purchase.