Do you know what happens when you are unable to repay back your home loan?

After how many missed EMI’s will the lender get hold of your property and throw you out of it? What are your rights as a consumer and what exactly are the steps involved in the foreclosure process?

When we buy a home with a home loan, there is lots of enthusiasm as we are becoming the owner of our dream home, and the future looks bright, but the reality of life is that there are many homeowners who face financial difficulties in their life due to job loss, accidents, medical problems that they are unable to pay back their Home loan EMI’s for many months and eventually get into a situation when they are not able to repay back.

Today I am going to tell you all you need to know about this topic. Let’s start

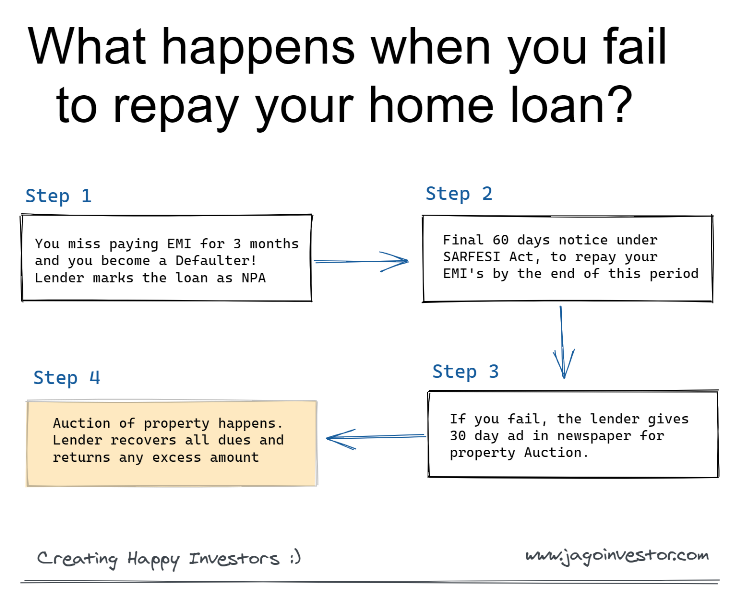

#1 – When you miss paying 3 months EMI

It may happen that you are miss 1-2 EMI payments due to some reason, in which case the bank will give you a reminder about it or give a small warning to pay back the missed EM next month. But if you miss paying the EMI for 3 consecutive months, that’s a big red signal and at this point, your loan account will be marked as NPA in the lender’s book.

This is a serious situation. The bank will mark you as a defaulter and the bank will send you a notice about it.

At this point make sure you do not ignore the bank notice and reply to them asap explaining to them about your situation and the reason why you missed paying the EMI’s. If your credit history is good and your reasons are very genuine, there is a possibility that the lender may give you some grace period for repayment.

If the bank is sure that they want to move ahead after you are marked as Defaulter, they will then send a full and final 60 days notice under a law called SARFESI Act (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interests Act).

Sarfesi Act empowers banks and other financial institutions to directly auction residential or commercial properties that have been pledged with them to recover loans from borrowers and lays down all the processes to be followed.

Before this act came into power in 2002, the lenders had to file a case against the homeowner and the matter went to court which was a lengthy process and very time-consuming. But after this act, now the lender can directly auction your property and evict you out of it. Even Co-operative banks are covered under the Sarfesi Act

This 60 days period is your final chance to repay your EMI’s, else the lender can take hold of the property and sell it off after 60 days’ notice. After this 60 days period, you are expected to settle down all the money you owe to the bank which is the outstanding loan amount. Either you pay it back to the lender on your own or the lender will auction the house and recover back their money.

During this 60 day notice period, you can put up your case in front of the assigned officer and share with them what best you can do to pay off the EMI soon. If they accept your explanation, then well and good, otherwise they need to give you a written letter of rejection within 7 days after which the next step starts.

During this 60 day period itself, you may also get recovery agents to your doors who may demand that you settle your dues. Note that as per the RBI rules you have certain rights when it comes to recovery agents like.

You can ask for the identity of the collection agents if you wish. They need to carry their ID Cards and an authorization letter from the bank

Recovery agent must be an authorized agent as per the Indian Institute of Banking and Finance

The recovery agent can visit only between 7 am to 7 pm and shall only talk to the defaulter and not family members (unless the defaulter is out of reach)

The loan recovery agent cannot be disrespectful or shall use any objectionable language or behaviour

In real life, the above rules are not followed properly and recovery agents are infamous to threaten and humiliate loan customers. If that happens, you shall complain to the bank and also take up the matter with the banking ombudsman

#3 – 30 days’ notice in the newspaper for Auction

As the next step, the lender will get the property valued from their valuer’s to find out the fair value of the property. Now starts the property auction process.

The lender will advertise the property details and mention all details like the reserve price (shall be around the fair value of the property), the date & time, address for the auction of the property.

If the property owner feels that the fair value of the property is too less or not correct, then they can object and talk to the lender.

#4 – Auction of property and refund of excess money

And as the final step, the property will be auctioned in the open market and the bank will recover back all its dues. Note that the bank is only liable to recover the dues and not the excess amount. If there is any balance left, it has to be paid back to the homeowner. So keep an eye on the auction amount. Nowadays most of the home auctions happen online (e-auctions) and you have the data online.

Sell off your house if you become a defaulter

Let me guide you a bit on what you should do if you are unable to repay back your home loan amount and are marked as a defaulter. Yes!, The best thing to do is to sell off your house on your own and pay back the dues to the bank.

Here are 2 reasons why you should sell off the house on your own

You will not get the best price in Auction – Home Auctions are distress sale from the bank side. Bank just wants to recover back their loan outstanding. Hence their focus is not on getting the best price for your house. If you sell the house on your own, you may get a much better price

It will take a lot of time as the property will be stuck at the bank hand – The auction process is lengthy and may take a lot of time which may not be suitable for your timeline. If you sell off the house yourself, you may do it faster as you may be open to negotiating and ready to give some great deals to potential buyers. You can also offer the brokers extra or double commission so they can also put all their energy into finding a buyer.

How to avoid getting into the defaulter list in future?

What are some of the best practices you should follow so that you do not get into the defaulter list? Here are some things

Try to keep your EMI amount less than 40% of your take-home – Always make sure that the EMI is not a big burden for you. Don’t go overboard and take a loan which is like a big burden for you.

Try to pay as much down payment as you can – If possible, do make sure you pay a big down payment so that your loan outstanding is a smaller amount that is manageable for you. I would suggest that you pay more than 40% in the down payment.

Restructure the loan – If the EMI is a big amount for you and each month you are on the edge of default, do try to bring down the EMI amount by increasing the tenure.

If you have any investments in debt assets like FD, Saving account, Insurance policies, PPF or even EPF. you can use that to pre-pay your loan to bring down the loan outstanding. This is only for those people who are overburdened with high EMI amounts each month

I hope this was helpful and you got some new information!. Do let us know if you have any questions!

Today we will discuss how you can convince your parents (assuming senior citizen) into mutual funds to get better returns on their investments with lower risk.

I am not saying that every parent needs to invest in mutual funds. But I have seen many parents retiring with insufficient corpus and investing that money in a very manner. It’s not tax-optimized and also earns the least return possible – all in the same of “Safety”

I understand that not all senior citizens want high returns, but in most of the cases, I have seen that there is some allocation which can be made in mutual funds.

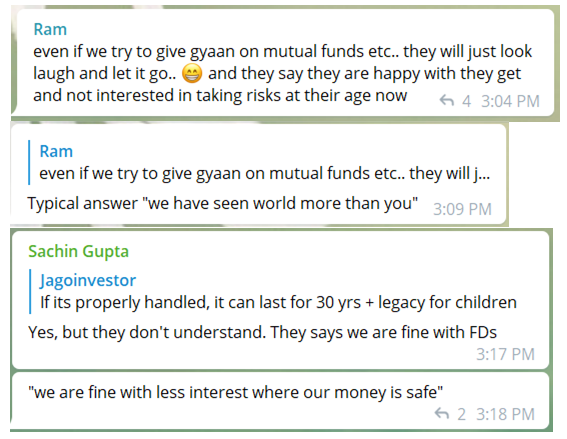

We come across many investors, who are investing in mutual funds and they have a good understanding of the product. They have full confidence in mutual funds investments, but their own parents are stuck in the old traditional way of investments. And these children are not able to convince their parents to invest their money in mutual funds or anything closely linked to stock markets, simply because parents come with the baggage of old beliefs about equity markets and poor understanding of the concept of Risk!

Old habits never go!

Most of the parents have all their life invested in Fixed Deposits, LIC policies, PPF, NSC and postal schemes which were simple and guaranteed return products. Their focus was always on “peace of mind” and “safety”. They were not obsessed with returns like we do today!

Parents outright reject the idea of investing in mutual funds or stocks the moment they come to know that its not a guaranteed returns product and there is RISK involved in these things.

To get some idea on this subject, I asked on our telegram group how their parents react for the investments in stocks and mutual funds, and here are 2-3 responses I got!

I know it’s going to be very very tough to convince them for investing in mutual funds, and most of the people will fail in this!. However, this is my small attempt to give some pointers to you on how you can start the conversation with your parents on this issue. Maybe it will work for you.

So here are simple things we can do.

#1 – Introduce them to Debt Mutual Funds

The first thing you can do is to not introduce the word “Mutual funds” directly to your parents. Tell them that there is one investment product which is similar to Fixed deposits, and the returns it has given over last many years have been a little better than Fixed deposits and has very less taxation (we see tax part in point #2 soon)

Tell them how this new “investment product” works very much like bank deposits. It also lends money to others and gets returns. But unlike bank fixed deposits, it does not give a lower but fixed return.

Instead, it keeps a small-fees and returns all the returns to its investors (which means that its a market-linked returns). There is its own share of risks which needs to be well understood and handled.

The next step is to show them how these debt funds have performed over the last few years like 5/10 yrs.

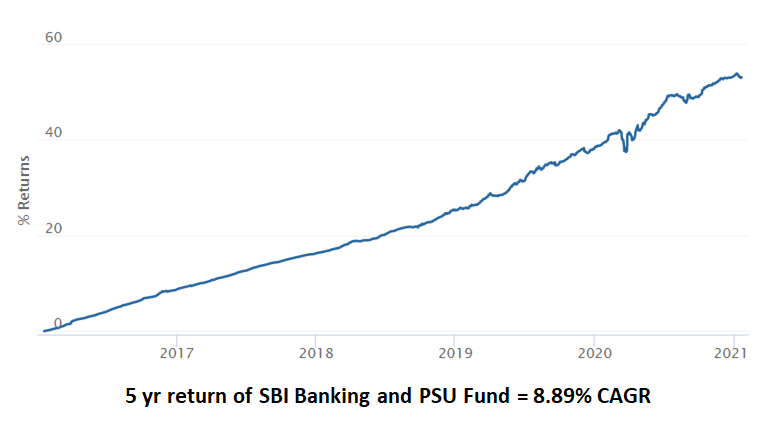

Start with Banking and PSU Category

You can start with a debt fund which comes from “Banking and PSU Fund” category because I have seen many senior citizens are very comfortable with the portfolio of that kind of debt fund/

Its a debt fund from SBI Mutual fund which invests a big portion of its money in bonds issued by various banks & PSU companies in India. The definition itself will be worth attention and parents may listen because of the word SBI (maybe!!)

That fund has given 8.89% returns in the last 5 yrs. The Journey for a fund has not been as a straight line, but it’s not wild like an equity fund. To a senior citizen who is struggling to get a 6% return in FD may be interested in looking at the past returns of this fund.

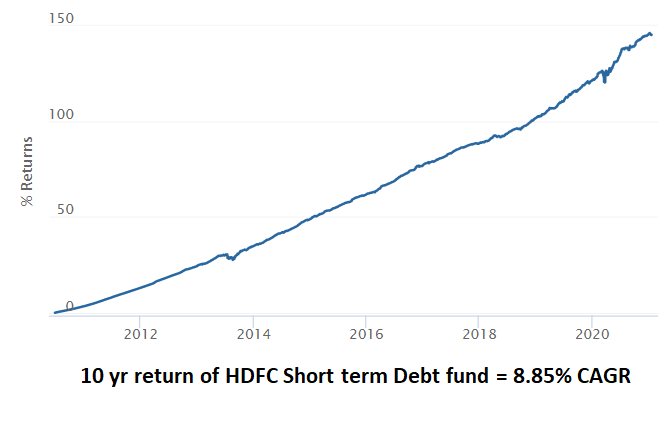

Apart from Banking and PSU category, you can also tell them about short term debt fund in case they want to invest their money for short term like a few months to a few years.

The stability of returns for short term debt funds category is quite strong as they invest in short term debt papers (incase this is technical for you, dont worry, you need to learn about debt funds)

Here is an example of HDFC Short term debt fund which has given quite stable returns over many years. Its return in the last 10 yrs is around 8.85% cagr! . No doubt that the fund is little volatile in short term, but over long periods you can see the line going up and up!

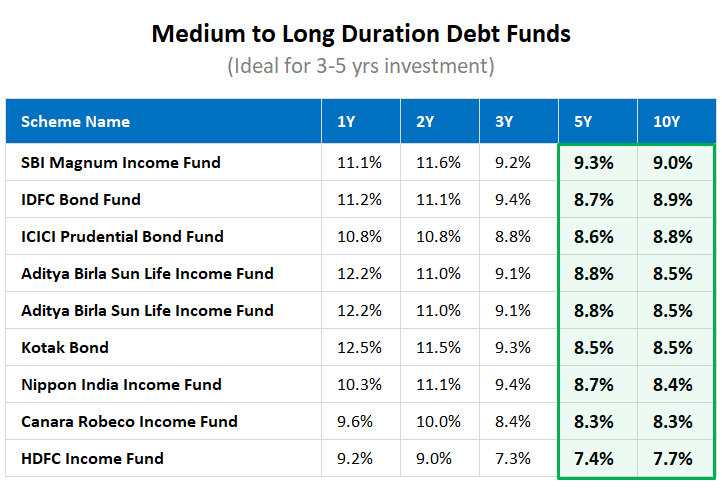

One more category is of Medium to Long term funds which are suitable for 3-5 yrs investment period and one can expect an 8-8.5% returns based on historical performance only (past returns are not a guarantee for future returns)

Here is a table showing what has happened in the last many years (Some funds with very low AUM is removed from the table and only bigger brands are taken)

So as the first step just show them these returns and low volatility of debt funds. This will be the foundation step.

Disclaimer: Debt funds are not as simple as what you are seeing above. There is credit risk and interest rates risk because of which the returns can be fluctuating. However, I am not going into the details of how debt fund works as it’s out of the scope of this article. If you are not clear on how debt fund works or chosen, its recommended to look for an advisor.

#2 – Show them the impact of taxation

One of the most overlooked aspects of investments is Taxation.

People do not think much about optimizing their tax-outgo while making investments. Investors still talk in terms of “Returns” and not “Post-tax Returns”.

When you invest in Fixed Deposits, Senior Citizen Saving Scheme, Saving Bank etc, you pay the tax on the slab rate. Which means that for very high amounts the tax will be at 30% rate for investors in the highest tax bracket. The worst is with FD, where you pay the tax on the entire year Fixed Deposits interest, not on how much you have redeemed!.

Can you believe that this tax can be lowered to 10% or 5% and sometimes even 2-3% for longer tenure investments (some cases). This is because the returns you get from debt funds are not categorised as “Interest Income”, but capital gains.

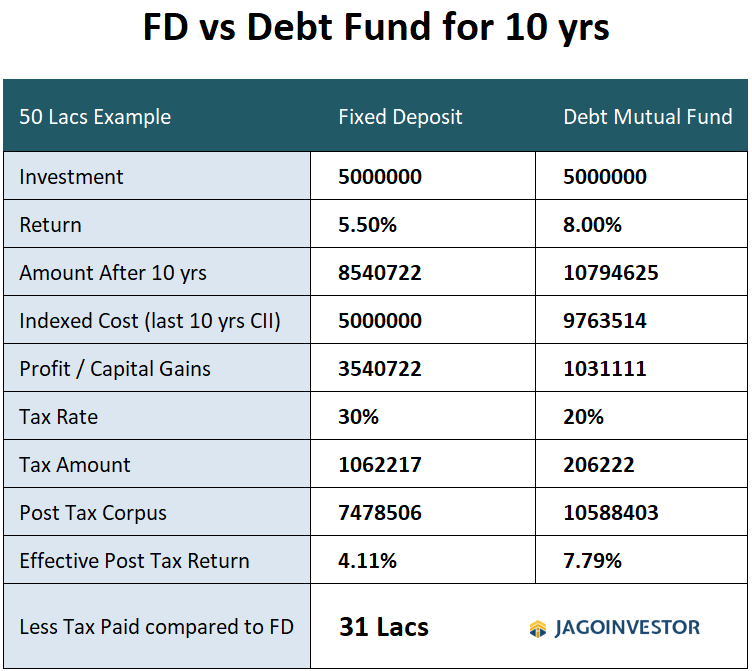

Let me show you a simple example of what happens when a Rs 50 lacs of money is invested for 10 yrs in a fixed deposit vs a debt fund. I have taken FD rate as 5.5% and debt fund returns at 8% as per the current situation and I have taken the last 10 yrs inflation numbers from CII Index.

You can clearly see that your FD becomes 85 lacs and Debt fund becomes 1.07 crores (indicative, but historical returns), Still, you pay 5 times more tax in FD than debt funds simply because of Indexation benefit.

The debt funds are surely not as predictable as a fixed deposit, but over 10 yr period, you can surely create a very strong portfolio and also diversify your investments across some quality debt funds. I think it’s worth taking that extra risk for the sake of making 31 lacs more!.

It’s not a small amount, it can mean 5 yrs extra money for retirement.

Most of the poorly designed portfolios lag on taxation. If you can just fix that part, that itself can mean alpha of 2-3% sometimes.

Here is a tweet I did a few weeks back where I was sharing how someone who retired with a big corpus (let’s say with 10 crores) will pay taxes in equity/debt fund/ FD

However, note that a smaller corpus can be still divided between husband and wife and then the taxation may be NIL or less due to the income not reaching the taxable limits. What I am referring to is mainly for big corpus.

#3 – Educate them about mutual funds in general

In case you fail in the 1st and 2nd step mentioned above and if your parents are still adamant about not changing their mindset of sticking with Fixed deposits or LIC policies etc, I must say you can’t do much and you lost the game.

However, if you feel they are showing some interest and will hear more on this subject, then its time to sit with them and educate them first about mutual funds in general.

I think most of the people who just reject mutual funds dont have a good understanding of the product and how it works. Here are 33 myths about mutual funds incase you want to look at them. Is time to educate them a bit about mutual funds industry and how established it is.

I feel there has not been a good attempt to educate senior citizens about mutual funds in the right way. Tell them a few things like.

a) Mutual Funds does not always mean the stock market

Firstly, tell them that not all mutual funds invest in the stock market.

There exists something called “Debt mutual funds” which do not invest in stocks and only invests in the debt market (bonds of companies and govt securities). Use the word “Bond” and “Debentures” as they might have heard these words and can relate to these.

Tell them that there are GILT funds (which only invest in govt securities) and then there are Corporate Bond Funds (which invests in big corporates) and in a way, they are comparable to corporate fixed deposits

b) Tell them about mutual fund industry size

Do you yourself know that Indian Mutual fund industry is one-fourth size of the banking industry? Yes – we have around Rs 30 lakh crore of assets invested in mutual funds which is very very big in itself.

A lot of senior citizens still feel that mutual funds are some kind of scam or not a well-regulated product. It’s your job to tell them that it’s a 25 yr old industry (actually much older if you look in the US and other counties) and a very well designed and well-regulated industry. Crores of investors invest through mutual funds now in our country and its growing at a very good speed.

Over the next few decades, my guess is the mutual fund industry will be bigger than retain banking Industry.

Dont force your thoughts on them at this point and just hear them out. If they have any apprehensions or issues with any point, do find the answer and go back and share with them about it. It can take them a lot of time to digest all this. No rush!

#4 – Tell them their corpus may not be enough for future

Not many people are retiring with huge corpus these days. Most of the parents are retiring with a smaller corpus than what they actually need for their long retirement. (Read why one needs 30 times their expenses as retirement corpus)

In your own way, you need to convey to them that their money may not be enough for future, and some part of their portfolio (if not all) has to be invested in equity too.

A lot of senior citizens are investing money in a way that it’s giving them terrible post-tax returns because of high taxes and low returns. All this in the name of “safety”. I know people who have put all their money in pension plans or just kept it in FD. They dont think about things like the liquidity of money or low-post-tax returns.

One issue is that in our country people think that once they cross 60 yrs, they have to just move every bit of their money into 100% safe products. This is not true for most of the cases.

A 60 yr old person can live up to 100 yrs also and that means they may have 30-40 yrs of life ahead. IF they make bad investments decisions which are not taxed optimized and do not create a positive real return, the wealth may get consumed pretty soon then they realise due to inflation.

So, if a retired person has Rs 30,000 expenses per month at age of 60 yrs, then by the time they turn 70 yrs, it will increase to 65,000 per month. However, a human mind is not able to access the impact of inflation over long periods of time.

In short, you need to convey that they need to generate a higher return on their investment and need to have a balance between safety and returns. Yes, some expenses may go down, but many other expenses may come up too. This is more true for those whose children do not live with them and they may end up living all by themselves.

A lot of senior citizens may not be thinking about these points.

#5 – Get them started with a very small amount

The next step is to get them started with a very small amount.

If they have 50 lacs of wealth, maybe you can invest just Rs 1-2 lacs in a short term debt fund and let them see how it’s moving in next 1-2 yrs. Show them the statements every 3-6 months to reinforce the thought that mutual funds are one of the options and they can diversify some part of their portfolio in debt mutual funds too.

I did the same thing when my mother in law wanted to invest a very small amount. She told me that she wants to put a small sum in Fixed Deposit and I told her that I will choose something better for her. I invested it in dynamic bond funds as the money to be put for the long term. Right now the fund CAGR in last 4 yrs have been around 8.8% CAGR.

Why Children should Educate their parents?

I also want to convey two points to you (the children) on why you should educate your parents about mutual funds.

1. Parents money may not be adequate

If your parent’s money is not enough and invested in a wrong manner, then the money will finish off sooner than they imagine and that would mean that you will be dipping into your own corpus to fund their retirement needs after 10-15 yrs.

Nothing wrong in that, as our parents have raised us and we are all successful because of their blessings, but when its possible to do better than what they are doing currently, there is no harm in pushing a bit into right retirement planning. A robust and tax-optimized portfolio shall be created which also generates better pension for them.

We at Jagoinvestor has been helping many retired or close to retirement clients (with corpus in range of 1-5 crores) to design and manage their retirement money. You can check out our retirement services brochure to know more

2. Legacy will come back to you

A lot of people do not get inheritance as the wealth is mismanaged by parents and is not put to the right use. If you make sure that your parent’s wealth is properly invested, that also means that a part of it may come back to you as an inheritance. And this may mean your own retirement corpus may get a bump.

If you are in your 30’s or 40’s right now, then your parent’s wealth will come to you as an inheritance after another 30-40 yrs and those many years of compounding can do wonders to your own retirement planning.

Conclusion – It’s not easy, but worth a try!

I know this is a tough nut to crack and many people may not be successful, but still, you can give it a try.

You never know if parents may be ok to invest some part in mutual funds. Just avoid asking them to shift all their investments to high-risk funds. As and when they get comfortable with mutual funds concept

Do let me know what are your thoughts on this and if you can share any tip on how to convince your parents to try out mutual funds investments?

Today I want to share something interesting with you. I recently asked my team to share with me some very unconventional and “hatke” financial goals of our clients.

Generally, when we all talk of financial planning, we feel its just about the boring-sounding goals like Retirement, Children education, Children marriage, Buying House & Home Renovation etc. But its not true. We all have very special and unconventional dreams which we want to achieve. So I just compiled some unconventional goals of some of our clients.

Here are 10 unconventional finance goals of some of our clients which my team was able to recall.

1. Taking a 2 yr break from work

One of the clients has a goal of taking a 2-3 yrs long break from his work. He wants to explore what he is good at or not?

He is great at his current job and love doing it. But somewhere deep down he wants to know if there exist other areas of life he can make his profession and that is not possible unless he takes a very long break.

He was already working from last 11 yrs and within next 4-5 yrs he wanted to take a big break for 2 yrs, so that he can pursue his interests, like travelling, writing, research, volunteering or other activities and also take some quality rest. I know this sounds a bit risky, but its his life and we better not judge others decisions.

2. Send Parents on a World Tour

One of the clients wants to gift her parents a world tour (travelling to different destinations in 5 yr period) and wants to create a big corpus specifically earmarked for this goal. Her childhood was full of struggle and her parents almost never took vacations. But now she is earning well and she wants to pay back to her parents in whatever way she can.

She wants to now create a big corpus in a few years, which can be used for regular international tours. I think its a wonderful thought. Somewhere deep down we all want to do this for our parents (and many do), but she chose to make a financial goal and work towards it

3. Reach financial freedom by 45 yrs

Generally, every investor has “retirement planning” as a financial goal, but few of the investors also want to achieve financial freedom much earlier than retirement.

Some people want to get financially free at age of 50, but folks from IT background always mention the timeline as 45 yrs.

Financial Freedom is a situation where you have not yet retired from work, but you have enough investments which can generate “enough monthly income” to support from financial life for the next 20-30 yrs.

4. Dedicated Corpus for Skill Upgrade

We had this amazing client from Bangalore, who was very sure that if you want to excel and do amazing in your career, you have to deeply invest in the constant upgrade of your skills.

So he wants to create a dedicated corpus which he can dip in every 1-2 yrs and do some courses/workshops for skill upgrade. It can mean taking up online certifications, go for specialized weekend courses in IIM’s (you can pay a fee like 80k to 1 lac and take these courses).

I think this is a sign of high-quality people who think like this for their career enhancement.

5. Medical Expenses Corpus for self/parents

This is not very rare, but not very common too.

Off late we are seeing many investors who want to create a dedicated corpus for the health-related expenses of their ageing parents and even for themselves. In many cases, people do not get health insurance for their parents because of some illness history and these people want to be prepared for large expenses and creating a corpus solely for that.

Even if you have health insurance, many times it may happen that due to emergency you will first have to incur the costs from your own pocket and then you will apply for reimbursement. So this kind of emergency medical corpus can come handy at that time!

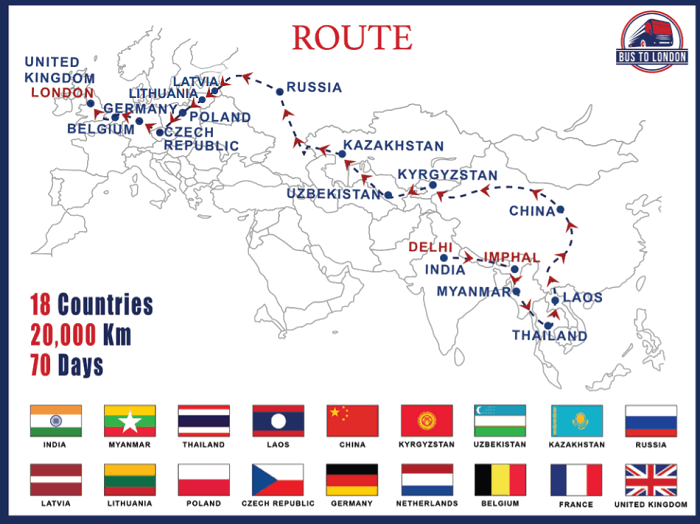

6. A road trip from India to London

Check out these 2 bikers from Bangalore who went to London on the bike and travelled 23,500 KM .. It was a dream come true for them. I watched their story and I also felt that someday I want to do it too.

But one of our clients actually has started planning for it, but not on bike!!. He will take a tour package and travel by bus.

There is a dedicated travel agency (https://bustolondon.in) which has started India to London Tour and it costs whooping 16 lacs (one side). However, its a 70 days journey and crosses 18 countries and I am sure this will be a trip of the lifetime!

7. Start Farming

Some investors are very sure that they want to get into farming after they reach the age of 50 in their corporate jobs and some have actually bought the land already and want to create a corpus to give their farming dream a serious shape.

They want to do the setup and also give it the of business. Most of these investors are clear that they don’t wont to be in jobs till 60th yrs and would like to move on to farming much before that. I am not sure if this will turn into reality for most of them or not. But there is no harm in trying out!

8. Legacy for future generations

Some clients also mentioned their strong desire to create a legacy which can be passed on to their next generation. They were not talking about the properties which will go by default to their family. Here they wanted to create a sum of money within a specified time which will be passed on to their children or grandchildren apart from the properties

9. Business Setup

A lot of investors who are in jobs also want to shift their careers at some point and want to move to business by the time they are in their mid 40’s or 50’s and they have already started accumulating money for the business setup.

A big chunk of these investors are from IT background and they often tell us that beyond 50 yrs they feel it’s going to get tough in the software industry and hence they want to plan out things for their future. Business is not a cakewalk either, but at least they are thinking of their plan B.

10. Charity / Social Work

Very less number of investors actually think about this, but some investors also show a strong desire to create a corpus which will be used for charity purpose itself. Many of our clients have shown deep interest in charity goals. Here are 2 of them

Example #1 – Create a pool of fund to do ongoing charity

One of our clients told us that since his college days, a close group of 5-6 friends had decided that in future they would like to keep doing various social work like for poor kids, senior citizens etc. Now, this clients wants to set up a 25 lacs corpus which will be used solely for this cause.

Example #2 – Create a Hospital in my village

One of our client comes from a very small village and now doing very well in life. His dream is to make a hospital in his village to serve his community and give back to society.

11. Buy a Harley Davidson (Fat Boy)

One of our client’s dream is to go on a long vacation and cover the whole coastal belt of India. He wants to do a solo trip but on a Harley Davidson bike (Fay Boy Model) which will cost around 18 lacs in today’s terms. He has already started saving for this.

What’s your “Hatke” financial goal?

Can you please share one unconventional financial goal for which you would like to plan out?

Also, I would like to hear how was this article and if you enjoyed it?

Do you think its a bad mutual fund, because it is not doing well from last many years?

A lot of mutual funds investors lose their patience looking at their mutual fund’s returns after they invest for 2-3 yrs. Its commonly suggested that an equity mutual fund will perform very good over the long term and one can expect double-digit returns, however, if the fund does not return back good returns within 2-3 yrs itself, the investors get very nervous and start judging their mutual fund quality and wonder if they made a right choice or not!

Today I will tell you how to judge the returns of mutual funds using “Rolling Returns” analysis, which will help you to get more confidence in your mutual fund and will help you learn many aspects!

Let’s start!

You Returns will invest a lot depending on when you invested!

Before we go into rolling returns, let’s understand the issue!

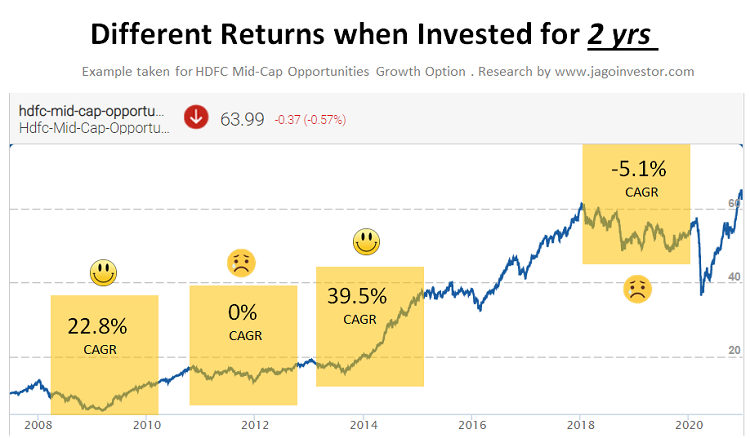

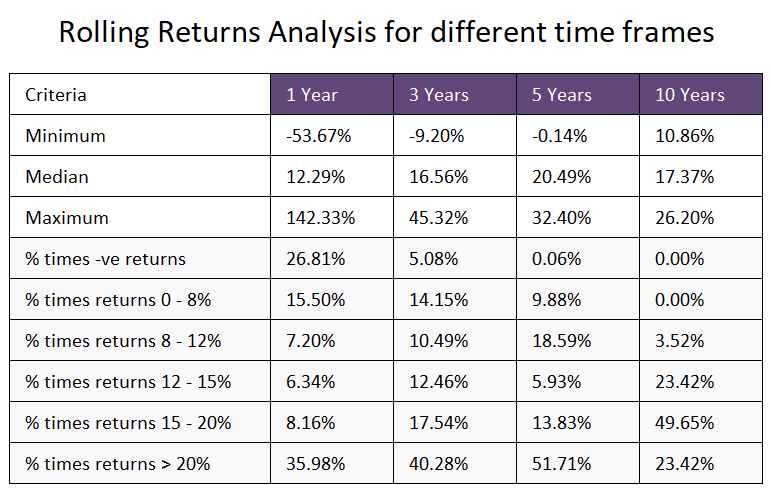

Take HDFC Midcap opportunities growth for example

10 yrs CAGR return: 14.96%

5 yrs CAGR return: 11.26%

At the time of writing this article, the returns from this fund are very good. But can this fund give bad returns in a 2 yr period. The truth is that this same “good fund” can give very different kind of returns in a 2/3 yr period depending on when you bought the fund.

Here is some data.

You can see that the 2 yrs return can be 22.8%, 0%, 39.5% or -5.1% depending on when a person entered the fund. So a lot depends on when you entered in the fund.

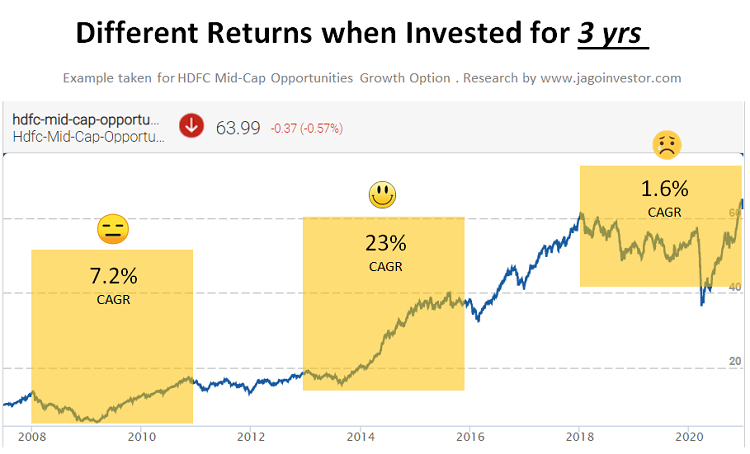

Now let’s see the same thing for 3 yr time frame.

Again, you can see that for a 3 yr period – the experience can be very very different. It’s not always possible to enter at the lowest point and many times, investors invest their money for the long term when the near term returns are going to be bad. However, they never get prepared for this.

Investor mind is also not designed to stay calm when returns go in negative and that’s when investors make a wrong choice of exiting the funds even if at the fundamental level, the fund has no issues and its just the volatility of the equity which is driving the fund into negative return zone!

You can see that this approach of just looking at the point to point return does not give you enough detailed information about the fund and its volatility.

Rolling Returns – What it is and How to look at it!

Rolling return means a series of returns data for each and everyday investment for a certain time frame.

So in our example of HDFC Midcap opportunities, lets assume a period of 14 yrs from 1st Jan 2007 to 30th Dec 2020. Thats approx 5110 days. If you do a 2 yr rolling return analysis, it means that a period if investing for 2 yrs and you are plotting the CAGR return for each day of investment from the start. (that’s 730 days of investment)

So you invest on

1st Jan 2020 and exit on 1st Jan 2022 (1st instance)

2nd Jan 2020 and exit on 2nd Jan 2022 (2nd Instance)

3rd Jan 2020 and exit on 3rd Jan 2022 (3rd Instance)

….

….

….

30th Dec 2018 and exit on 30th Dec 2020 (4380 instances: 5110 – 730)

So you can plot these 4380 data points and that graph is called a rolling returns graph. In the same way, you can have a 3 yr, 5 yr or even 10 yr rolling return graph.

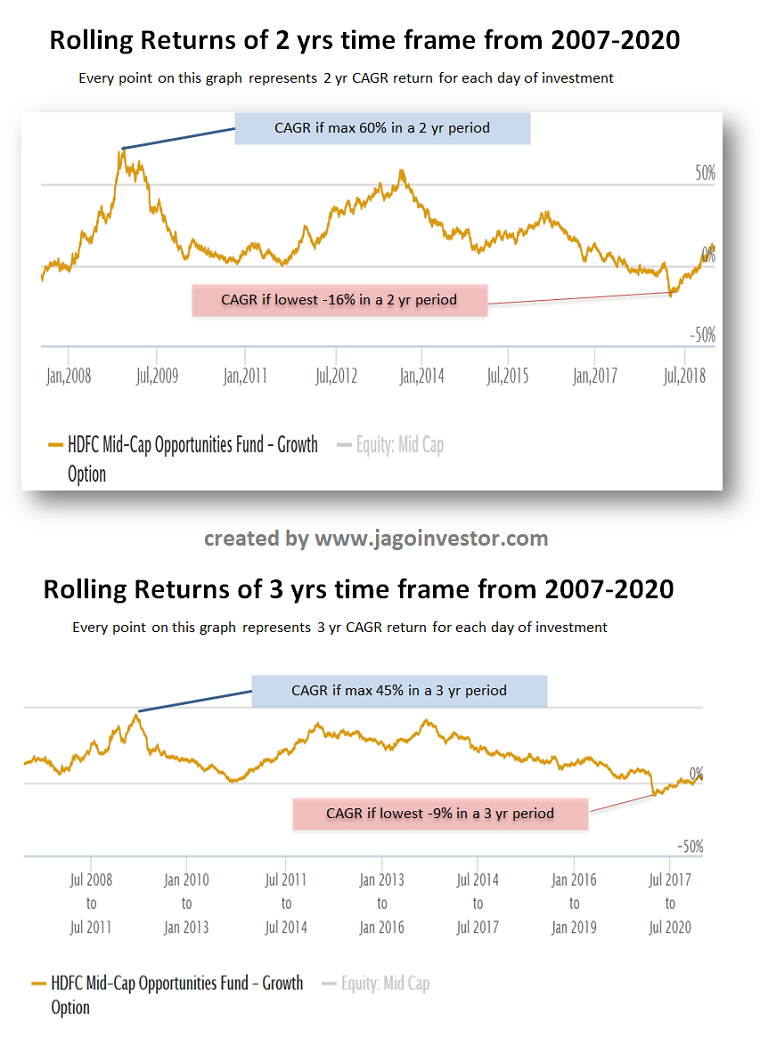

Check out the example of HDFC Midcap opportunities rolling return chart for 2 and 3 yrs period for last 14 yrs. You can see that in a 2 yr period, the highest CAGR has been around 60% and the lowest at -16% .. So it’s possible to see your investment go down by 16% in a 2yr period as per old data. The same kind of data is there for 3 yrs period too!

Rolling return graph will give you a deeper understanding of how volatile fund returns have been and even the probability of your return being in a certain range (only with past data). Note that its only historical data and the maximum and minimum returns can change depending on future performance.

If you look at the chart above, you can conclude that if you want to invest in this fund – then you can see a downside of up to 10% in a 3 yr period because it has happened in the past. Also, you can see flat returns even in 5 yrs period which has happened in the past.

This kind of analysis tells you that because of volatility even this kind of good funds can see a period of non-performance and flat returns.

I hope I was able to explain what is rolling return in a simple manner.

Conclusion

Remember that rolling returns exercise is a great tool for analyzing the mutual fund, but it’s not the final exercise in itself. There are many other kinds of analysis which is possible and this exercise alone does not give any final judgement.

If you are not happy with your fund performance, then I suggest going through this exercise!

In the last article – 10 benefits of being an employee vs an Entrepreneur, Manish has highlighted some amazing points with some interesting sharings from some real-life entrepreneurs. The article surely has struck a chord with many. After the article was published we decided to write a sequel to the article. We want to leave all you with a new possibility so that you can see your work or job with a fresh pair of eyes.

If you really want to become successful in life, I invite you to step beyond the job and business conversation. A lot of people debate on which is better – job or business?

In this article, we just want to add a fresh perspective to your work life. I have been into several jobs and businesses and I want to help you create a whole NEW relationship with your work.

Here are the 4 Empowering ways to look at your work

1. Job or Business is a SYSTEM you choose

Always look at a job or business as a system you choose to make a living.

At the end of the day, it is a system you choose in your life which helps you to earn money. Job or business both are different systems, now every system will have a different input and output attached to it. Our Business coach Mr Ravi Iyer is a system person. He sees life as a system. He finds a system in everything around him. Whatever system you have chosen, see that you respect and love your system.

Look at what is your relationship with your system (job or business). If you create an empowering relationship with your chosen system you always grow and shine in life, and if your relationship with your system (job or business) is weak it always leads to confusion and chaos.

Two different systems:

Job – This is a system that generates X amount every month for the person – one has to produce X for the company from which the person gets the share. This system is more stable and growth is predictable by nature. The system is linked with the performance and efforts you bring inside the company.

Business- This is a system that can lead to profits or loss at the end of each financial year. Here you cant predict things and the growth can be non-linear by nature. The system is linked with risk vs reward. As a business person – every day you have to find a job for yourself and for your team.

2. Your work has to be your SELF-EXPRESSION

Let me share my relationship with my work or what is right now in front of me.

Let me share how to fall in love with your system (job or business) and how you can grow and shine in your career. I look at my work as my true self-expression.

I love to write

I love to lead sessions

I love to train people

I love to empower people

Most of the time I am addicted to helping people help themselves. Right now I am writing this article as part of my self-expression. Trust me it is not about doing a job or business, it is about expressing yourself fully out in the world through work.

Just try it out, the next 7 days you will fully allow your work to BE your self-expression. In your job or business let your expressions flow, don’t worry about the outcomes just keep on expressing yourself.

For example: If you are a software engineer, express yourself through the software you can create for the world. Your everyday focus has to be on what can you create out in the world using your skillset and knowledge. You go to the office not for the targets or for completing the task, but to express your true self out in the world. You literally fall in love with your work when the game shifts from getting the work done vs. expressing your true self.

Let me give one more example, if you are an architect, give the best designs to the world. Let your designs be your expression, let your work become your expression. You are expressing who you are to the world, you are sharing a part of you with the world through your designs and creativity. Let self-expression be the context of your work and not getting the work done or achieving targets or trying to please someone.

In any field of work you can shine if you chose a different path, you choose a path of self-expression. Sharing WHO I really am with the world.

3. Learn to Operate as an Intrapreneur

I did my master’s in business entrepreneurship. After completing my graduation, I wanted to do a program that helps me to become an entrepreneur.

I finally found an institute which was not just creating manager but entrepreneurs. I gave the entrance exam and got selected. On the first day of college, I created my company “Integration consultancy” and I also got some visiting cards printed. On the first day of college, everyone had to introduce themselves to the stage.

I got on the stage and made a declaration. I said “Here is my company and I am going to to use the college training in setting-up my company”, my professors were amazed and everyone in the class was taken aback by my announcement. I always wanted to be into business but I also did all kinds of jobs in my career. I have worked in the call centre, I have worked in a cyber cafe, I use to write articles in Indian express, I have been into multiple jobs and organizations but not as an employee, but as an intrapreneur.

An intrapreneur is someone who operates or runs a unit within a business created by someone else. We have people in our team who really operates like an intrapreneur, we have Sagar Maheswari and Kunal Purohit (our team members at Jagoinvestor) who have demonstrated several times being an intrapreneur. My professors taught me to always operate like an intrapreneur and I invite you all to start operating like an intrapreneur. Trust me Life is not about business or job when you operate like an intrapreneur

4. Always Work and Operate Like an Artist:

When you are in a job or business, you do think about retirement, But do artists ever retire?

The answer is maybe NO.

An artist is into a job or business? or maybe none. They operate in a different zone, which we should learn to be in. An artist looks at his or her work as their self-expression and nothing else, you take their art away from them and they start shrinking.

A painter will think of something in his or her imagination and will start working on making the painting a reality. It can take a few days or months for creating that one thought a reality. Artists love the game of creating a future in their mind and then converting the future into a reality. Once you learn to master this art of creating, you start to enjoy the process of creation. You master creating wealth, you master the game of self-expression and you live a fulfilled life.

Talking about wealth creation, you can create a vision of creating your first 1 crore in the next 5 years and literally live into that future day in and out. Your vision has to wake you up in the mornings, your vision keeps you to stay in action. You start to enjoy the process as the process is driven by your vision. Artists are driven by vision and we can apply the same to wealth creation or any other important area of our life.

Conclusion

Be it a job or business – it is about loving your system and let your work become your self-expression. When I get on a call with someone, I get totally engrossed with the other person, I will express myself fully and will allow my humanness to touch the other person’s humanness. I know this will sound a bit weird or new to you, but when you connect with people at a deeper level through your work everything shifts. Your sales, numbers, financial goals, business targets everything becomes like a by-product in life.

Your work has to become your self-expression that is the main point we want to leave you with as an end conversation for both the articles. Our blog is a place for our self-expression and will continue to express our heart and soul with all of you.

Thanks for reading the article to the end. Thank you for being our partner in spreading financial literacy. Do share your comments below and let me know your thoughts

This article was written by Nandish Desai!

—

Online Workshops coming up in Jan,2021

Dear Readers, we are coming up with our workshops in online mode starting Jan, 2021. If you are interested to get early access to it, do share your interest in this form, and you will be the first to get information about it.

This is a long, but intense and immensely high-value article. So please read it fully!

Today I want to talk about some of the advantages of “doing a job”, rather than running a business or being an entrepreneur.

If you are someone who thinks that having your own business is “always” better than “doing a job”, I want to break your myth and point out several things which people don’t appreciate about doing a job.

There are lots of articles, videos, and podcasts about “leaving your job to pursue passion” and in almost all of them, a “job” is projected as some kind of modern slavery. It projects “doing the job” as working for someone else success and giving your life for others’ benefit.

I think it’s a gross over-exaggeration and while the job has its own limitations and issues, being your own boss has its own share of very big problems. I have also seen many salaried people complaining about their life, work culture, pay limitation, lack of opportunities, and their declaration about how they want to leave their jobs one day and achieve nirvana and ultimate success and get out of the rat race.

Before I tell you some good things about being in a JOB. Let me first share the bright side of “business”

When you do some business or try a startup – you surely become your own boss, you feel more in control of your career path and there is huge huge income potential.

However only when you “become your own boss”, you start missing many things which you get in a job. Only then you are able to appreciate those subtle benefits of a job, which you never realized while being in the job. Today I want to talk about those good things about being in a job that is often not appreciated or realized.

So I am going to talk about 3 primary and major benefits and 7 secondary benefits which not major, but matters a lot.

Lets Start

#1 – Less Headache

When you are in a job, your work is very focused as you are accountable for one single thing. You don’t need to take the headache of other departments and other small things. The way you operate is simple and you can blame others for anything which is not your core-domain.

This means that you have less headache and you can be very productive and focused on your work as you are clear of what is expected out of you. I used to love my job in Yahoo years back when I had very defined tasks in hand and my to-do list was clear and precise.

Compare this to your own business!

For the initial few years, it’s nothing less than a horror movie.

While you are the “BOSS”, you are also a peon.

You are the person who does salaries, buys office furniture, pays electricity bill, works on the website, open the bank account, talk to customers, talk to vendors, run around to deal with CA, get GST calculations done, do hiring, do training and tons of other small and big things!

If you feel that this is doing to happen for just a few months of starting the business. It’s not true. Businesses take anywhere from 5-15 yrs of establishing. There are many people who are having a small company now with few team members, but there are tons of things on their plate which they need to handle and with the changing landscape of business, competition, regulator, customer experience, and business cycles, its a never-ending circus for many entrepreneurs.

Sometimes you start wondering why you are doing everything OTHER than the main task.

When you are in a job, there are lots of invisible systems that are around you and speed up your work. You become a HERO in your company, mainly because you had a lot of focus and time to excel in what is your core job. The invisible support system around you helps you in that.

So in a job, even if you feel there are lots of headaches, it’s often at a minuscule level compared to your own business. So if you are someone who doesn’t want to do be lost in too many things and doesn’t like to handle multiple things in hand, a job is a wonderful place to be in.

The job comes with fewer headaches

#2 – Clear Separation of Work-life and Personal Life

When I had started working 13 yrs back in Yahoo, Bangalore, I remember Friday evenings.

It used to give a feeling that I am starting a new life altogether – The “Weekend Life”

For the next 48 hrs, I was detached from my work life and there was nothing on my mind. It was not my headache what is going to my company. That conversation started only on Monday morning.

Unless you are at a very top position or at some senior level, there is a very very clear separation of work life and personal life.

This becomes very tough when you start your own business. No matter what you do, there will be some thoughts of business that will crop up in your mind. This is simply because now you are not working for someone else. You are working for yourself. Your company is part of you.

Sadique Neelgund who started his entrepreneur journey with networkfp.com 10 yrs back shares his comment on this point.

As an Employee, one of the biggest benefit I enjoyed was fixed work hours – 8 hours per day – 5 days a week. Forget about work and boss, enjoy life with friends and family after work and on weekends. Tomorrow, take it as it comes. Resign and move forward if things don’t work out.

As an Entrepreneur, it’s actually work right from the time you wake up to the time you go sleep. Once you become an entrepreneur, your mind is always thinking what next; sometimes for growth and other times for survival. It’s strange many of us want to become an entrepreneur because we want freedom of time. Although we can take leave whenever we want, go to office late etc… But that really does not translate into freedom from thinking about work & business.

According to me, freedom of time in real sense is much higher as an employee than as an entrepreneur.

One of my friends was sharing about his relative who has started a restaurant business in Dehradun. Because he is the “chef” himself, the weekends are non-existent for him now. His business is such that the shop has to be opened almost every day.

Either he has to wait for his business to become much bigger when he can hire a staff who is as good as him or wait for some extreme situations or get SICK in order to enjoy a day off.

Also, some businesses are seasonal and their peak business happens in the holiday season. So be ready to forget holidays or full off time during the holiday season. This depends on business to business also. Imagine that you start a business which is related to “Gift items”. In that case, you will be super busy in all holidays. For you Diwali, Holi, New Year and this kind of time do not mean holidays, but double shifts!

So if work-life balance matters too much for you, a job is a wonderful place.

Note that while you sacrifice the work life balance in the start of your business. Once its established and things are in place, you enjoy a great amount of work life balance. Then you can be very flexible in your office timings, you can take off whenever you feel like and work on days as it suits. It gives a lot of flexibility to you.

#3 – Steady and Stable Income

One of the things many salaried employees do not appreciate well enough is the steady and stable income that comes with a job. Each month, you know how much you will make by the end of the month. You know that till you have your job, your income is assured and it will come without fail.

The business risk which your company takes or any short-term problems which happen with the company do not impact your paycheck. This also means that you can plan your life in a more clear way. You know much EMI you can handle, you know how much expenses you can do, etc etc.

However, in business, it’s a roller coaster ride. It’s like an equity mutual fund chart, where you know deep down that while in long run, you will do well and things will be in place, in the short term you have to face a lot of volatility. A good month/year does not mean that the next month/year is also guaranteed.

Business uncertainties sometimes can be very painful and can put you in a situation where you start wondering why the hell you are into business. This is more true in the businesses where you also have to deploy too much investment and the income stream is very volatile.

Checkout out more on this, in this video by Ankur Warikoo, the cofounder of nearbuy who shares his real-life experience on this matter

No doubt that over the long run, the business can give you an amazing payoff. Your income from business can be huge and you will forget all the initial painful years, however this an important point to consider.

I asked Amit Singh, an entrepreneur who runs a WordPress design and development Agency since 2009 to share his comments, and here is what he says.

To me, there are two good things about the job

1. Assurity Cashflow, that is as long as you have a job, your salary is guaranteed. This allows people to plan and focus on the work at hand. Another major advantage of this is that you get to take loans from banks easily for big-ticket items like Home or Car.

2. Time for hobbies, while this may not always be true but while I was working I used to regularly write blogs to share my learning, and build interesting side projects for myself just for fun.

If you are someone who needs a very predictable income, the job will give you that.

#4 – Flexibility to move on and easy withdrawal

If you are not happy with your job and can’t stand the stress, it’s comparatively easier to move on to some other company, role, or location.

In the end, you are not married to the company you work for. You can take the decision to move on to something else because at the end of the day you are a resource. The way you are replaceable by the company, even the company is replaceable by you.

You need to start the job hunt, plan out things, pack your bags, and move on. I am not saying that it’s a cake-walk, but there is a good level of flexibility on this front.

However, when you start your entrepreneurial journey, there is a good amount of financial & emotional involvement from your end for your venture. You give you time, effort, mind, soul. It’s like raising a baby. You can’t just leave it in between and move on.

If things start going wrong or if you face challenges, you get to fix it and stay in the mess. You cant back out so easily. I don’t want to sound as if I am trying to say that job-switching does not have its own challenges. It surely does! , but in comparison, there is a huge advantage in the job.

So if you are someone who enjoys this “weak attachment” and appreciate the flexibility to move on to something easier, the job is for you!

But let me also point the bad thing here. Even if you are working well, doing decent – there is always a risk to get fired from your company for various reasons. In the end, it’s not YOURS.

That thing never happens in a business. Jaise Bhi ho, Apna hai!

#5 – Social Standing & Recognition

“Hi – I am AVP of XYZ corporation” draws much more attention in social circle, than a “Co-founder of an ABC Struggling startup”.

If you are holding a key position in some big company, people want to talk to you, be friends with you and invite you for various events. You are also recognized on social media and getting this attention often pampers you and acts as a motivation for you.

You get your identity due to your designation/brand. Also if you are handling a key position or managing a big team, you also get a chance to experience giving orders to others and command things. You handle people

In business, this social recognition will come very late or may not come every. When you leave your big position in a company and do a startup on your own, it’s like from a happy, glossy Karan Johar movie, you are in a dark, realistic Anurag Kashyap movie

Let me give one more shot at it!

From Varun Dhawan of Humpty Sharma Ki Dulhania, you suddenly become Manoj Bajpayee of Gangs of Wasseypur.

Here what Mahavir Chopra who recently started beshak.org after leaving his job at a very big company shares with us

Entrepreneurship is an extreme sport. It’s a mental shift. It’s a rollercoaster journey of finding yourself that is not for the faint-hearted. When you take up an entrepreneurial journey, you are changing who you are.

You are no more the senior guy working in that successful company, who called the shots in the system and things worked. You are unarmed, you are vulnerable, you are naked in front of the world. From you representing a large company, a tiny company now represents you.

The romanticization, glorification of an entrepreneur shown in movies, shouldn’t be the reason you want to become an entrepreneur – that way all of us should become gangsters or serial killers :D. You should become an entrepreneur if you are ready to unlearn, rebuild your self while building an organization that generates value from scratch – when you are ready to test your strengths in the real world, you are ready to face your weaknesses.

If this social standing or commanding position is something you enjoy a lot, the job will be a perfect place for you.

#6 – Move up the ladder and access certain kind of roles/work

When you are in a job, you mostly move ahead and up the ladder.

If you are extremely skilled in something and your domain knowledge is incredible. Then as you move up the ladder, you can get a chance to lead a big team in your area of expertise.

If you feel saturated in a particular domain, you can think of trying out another domain in the same company or the same domain in another company once you switch the job. You mostly experience “progress” in your career when you are in a job.

Also in Job, you can use someone else success and hard work to lead a role that you want. You can let the business uncertainties be handled by someone else and dedicate yourself to learn a new skill of your liking (obviously it has to be related to your work).

For example, let’s say you are a good software programmer and have designed great front end websites. Now if someone doing a new startup, and you want to give a shot at leading the planning and creating of the front end of the startup. You can join the startup and fully focus on that new thing you to add to your resume. You can let the business owner worry about the funding, company future, salaries, and other things.

However, when you start your own business, you often start from scratch the rebuild things. You first do down, then move up which is quite volatile.

Let me explain with few more examples (ahh.. its not an easy thing to explain)

If I want to explore “teaching” a bunch of students. It’s almost impossible to do if I open my own school. I will then be running around for things like hiring teachers, renting or buying land, construction work, managing staff, design of curriculum, making a marketing plan for the school, and whatnot. I can’t be a teacher then.

If you want to lead a team of 20-50 people. Then if you are an expert in your field, then there is a possibility that within a few years you can move to another job where there is an opportunity to lead a big team.

If you think of starting the business, you have to first deal with a lot of petty tasks before you can do that years and years later. You will mostly be busy with so many things that you will hire someone else to lead the team at the end of the day!

I hope you are getting what I am trying to say. In a job, there a nice chance of incrementally become bigger because of other efforts and setup.

Here is what my friend Ameya Dhani says, who worked for more than 15 yrs and now started his own business as an Industrial solution provider

When I was engineering student, I always fascinated about corporate culture and dreamt of working with MNC. I was fortunate to have my dream come true and had chance to serve in Corporate offices of MNCs at various levels in my job tenure.

Working in a company will give u readymade identity at the professional & social world. You will have the knowledge required for completing your assigned task and if required, company will upgrade/polish it through their internal team or consultants. This will help you to learn new skills to master the task.

As every employee is responsible for the task assigned to him, this reduces the burden which helps in having a better work-life balance. At MNCs, at younger age you can sometimes visit new countries, meet new people and gain better knowledge of world. Also with job, its possible to have a better lifestyle at younger age. Timely salary and perks are icing on cake.

#7 – S0cial Life & Atmosphere

If you are doing a job, it’s almost a given fact that you have some office friends, a happening office atmosphere, birthday parties of friends, monthly/quarterly eat-outs, and yearly outings once in a while (obviously not in this corona phase)

You are part of a buzzing environment and there are people all around you. Even though you spend the highest time at your desk, you don’t feel lonely. I remember every day in the office we friends used to meet in the cafeteria and engage in silly chit chats while gulping that juice and sandwich. I remember my office friends, colleagues, and the whole ecosystem which used to give me a nice feeling.

Welcome to Entrepreneurship, which is often a lonely world!

You start working out of home, or some shared office or a tiny office which is nowhere close to that swanky office, and on top of it, you are paying the rent. You miss that big-office culture and often that can be tough to handle if you are too used to that kind of life.

A lot of people do not think about this small aspect, but for some people, it can matter a lot.

It takes time to reclaim that level of social life in your own business unless obviously you are starting your business with funding money and get a big team and office from 1st year itself.

#8 – Corporate Perks

When you are in a job, you also get tons of perks

Apart from various small perks, I want to first talk about two major benefits which are health insurance and EPF

One of the biggest perks, when you work in a job, can be the free group health insurance which covers you and your parents from day 1 for all kinds of illnesses. You know how big a perk this is if you are not getting health insurance for your parents or yourself when applying separately.

Another big perk is the automatic investments which happen in form of EPF. For most of the employees, a forced EPF deduction is nothing less than a big boon. At least this way they have some investments happening every month and over years, it compounds to a very big amount.

Let’s see what my long time friend Animesh Gautam who started his own business around 2 yrs back (after 13 yrs in the job) says

For me the most important think I relished about the Job was the PF contribution that were made compulsorily, it helped me at finally arriving at the decision of quitting my job, as the contributions in PF after 13 yrs of work were considerable enough to give me some financial stability and I was then able to take calls independent of financial constraints.

Then there are many small perks and advantages like

Free/Discounted food

An unlimited doze of free tea/coffee/cookies.

Creche

Free office cabs

Free Life Insurance

Corporate tie-ups with restaurants and brands

Gym Memberships

Tie up to get easy credit cards

Tie-ups with various loan providers

Being in the job, people really never appreciate how fast they get a loan by just giving their form 16 and ITR for last 3 yrs for any kind of loan (for business people its a headache to prove that they can repay the loan, we have to give our company balance sheets, income computation with CA attestation and what not!)

In short, there is a good amount of pampering happening which often you don’t realize.

One of my friends who works in the IT sector also mentioned that she is missing the super comfortable office chair in this WFH period. She never realized it, but only now.

I don’t know how true it is, but my Delhi friend said that many people in the North also love the fact that their offices are fully AC which they miss when they are back home (if they don’t have AC at home)

When you start your own business, you often start from a lower base with all these benefits and amenities gone. But once you are established with a nice office and staff to take care of things, you get some of it (still not FREE)

#9 – Set back due to mistakes or external factors is lower

In a job, the impact on you, because making a mistake is much lesser compared to a business.

Any mistake on your end will mean a direct loss to your company and an indirect or a delayed loss to you. It’s not that your next paycheck is at stake.

Even when there is some big mess up from your end, the maximum you can lose is the job, but you still have your skills and years of experience with you. Even when you are too stressed due to some office issue or a mistake done by you, you have an option to leave the job and move to some other company and feel guilty for some limited period. The case is closed for you.

Compare this to your own business, where you have to deal with the mistake and fix it. You cant leave it!. Also, the direct impact is on you.

#10 – No financial Investment

Finally, a very small benefit of a job is that you can do a job without incurring any financial investment. You just need the skill and that’s all. The best example of this is the restaurant business.

Imagine someone took up the job of a restaurant manager in a new upcoming restaurant.

Due to the corona pandemic, the setback for the restaurant manager is only his job. But for the restaurant owner, it may be a loss of huge capital.

So a job gives you an opportunity to earn money without any financial investment.

But if you want to do business, you should be ready to invest money in most of the cases

Apart from the 10 points I mentioned above, I also want to talk about a few more things .. Let’s see those

Am I glorifying Jobs?

When I finished writing this article, I felt as if I am glorifying jobs and giving an impression that one should not attempt doing business and always be in jobs as they are so great. However, I am just trying to put a point that you should love and respect your jobs a lot as they are amazing in certain aspects.

People in jobs will surely have a limited upside on their salaries (apart from exceptions) compared to a business person. Almost all the rich people in India are business owners and not a salaried class. However, there is no written rule that everyone should aim to become a billionaire. You can lead a happy and content life even being a salaried person and that’s absolutely fine.

Businesses even though have their own limitation score on many points which is not the agenda of this article and I am not going into it for now.

“Entrepreneurship is always better than just a job”

This is surely not true.

When we hear about entrepreneur stories, we often hear about the big success stories which are worth billions. We will hear about Bansals who used to be in a normal job in Amazon and who are now worth billions of dollars. But we will not hear about other folks who also used to work for amazon and left their jobs to start businesses which never took off and they had to return back to jobs and no one knows their stories.

No doubt that entrepreneurship has the potential for a very big payoff if things go in the right direction. But it’s not for everyone and should not be attempted just for the sake of trying.

There are tons of struggles in starting your own work and most people fail at it. Also, small successes are often not celebrated enough. You will not hear about the guy who left his job to build a 4 cr company and a team of 8 people after 12 yrs of hard work. You will not hear about the 2 partners who are making 5 lacs a month each after going through the hardships. These all stories are not “success” as per the startup world even though 99.9% of people end with exactly that kind of results.

In the end, it’s a decision between what you want to be – a “Small-time entrepreneur” or a “Big-time employee!”

You can be an “entrepreneur” while being in a job

Think of it like this.

An entrepreneur exists only because of the people who do the job. No entrepreneur wants to work in isolation.

He wants to have a salaried team that will help him grow his work. Salaried people are the backbone of any company. What you need is the mindset of entrepreneurship to make tons of money and command lots of respect.

Do your work as if you are the owner. Think from a business angle and contribute. You will become a valuable part of the organization and your compensation will also grow and be linked with the business.

Aditya Puri of HDFC bank was an employee, but his attitude was of an “Entrepreneur”. He retired with 800 crores worth of company stocks.

Sundar Pichai is also a salaried employee of Google. But he acts and thinks like an “Entrepreneur”. Last year, Pichai was granted a $240 million stock package on top of a $2 million annual salary.

If you create value and work with a giving attitude, then you automatically become an “Entrepreneur”, you don’t always have to start your own business.

I hate my job, so I want to start my own business

“I hate my job” is the worst reason to start your own business.

Most of the people who succeed in their “business” are those who were quite happy in their jobs.

They didn’t leave the jobs because they hated it. They left it for a bigger reason. Maybe they wanted to be in a commanding position, maybe they wanted to experience the tough path, maybe they want to execute an idea which they were not able to do in the job. Maybe they wanted more flexibility in their life which job was not providing them. Maybe they wanted to earn a lot of money, which they didn’t see happening in their job.

If you don’t like your job or are unhappy. Check out what is the reason is and then fix that.

Maybe it’s your boss

Maybe its the company environment

Maybe it’s your salary

Maybe it’s the lack of freedom.

Fix that.

Leaving the job is not a solution.

Don’t devalue the money you earn for the sake of “passion”

Pursuing a passion is highly overrated and full of fizz.

Most of the people who seem to be following their passion are just lucky people who started something and it clicked and they don’t hate it now. It was not a planned path they took.

Often, the stories of “he/she left his job to pursue his dream” don’t look at life realities and the importance of money in life.

You cant pursue your passion with worries of paying the next rent and thinking from where your kid’s fees will come next year. If you have studied well and got your hands on a well paying job, do value it and the money you make from it.

There is no problem is pursuing your passion, but do it with some good planning and once you are financially stable. Else things can go in the wrong direction.

I once came across an NRI who wanted to come back to India to pursue teaching. He had a decent networth. I asked him if he can stretch a bit more and work for 5 more years? He said YES.

I asked him to do that and delay his entrepreneur stint a bit late. That way he would be around 1.5 crores richer because he was able to save close to 3 lacs a month while in the job. I asked him to not devalue that.

I want to end this article with this point that even though I tried to share many benefits of a job in this article. I definitely don’t want to portray that the business world is bad or should not be pursued. All that I have said above is keeping in mind a larger population. There are times in life where all the logic does not work and doing what your mind tells you is the right thing to do.

A job even though has many benefits often puts you in your comfort zone and you are not able to explore your full potential. But anyway, I just wanted to make sure that people love their jobs and respect what it provides them.

We often don’t appreciate what we have in hand and just feel that we are missing out on something which others have.

I hope you will start seeing your job with a new perspective and become more valuable going forward.

There is good news for those loan borrowers who didn’t opt for the loan moratorium benefit which was introduced by govt due to the pandemic. The govt has decided to pay the interest on the interest of the loan outstanding and pass on the benefit in form of cashback to loan borrowers.

Let me explain

So those borrowers who have opted for loan moratorium benefit will only be paying the simple interest on the loan outstanding and not the interest on the interest. This means that all those who paid their EMI’s are in a way getting penalized for not taking the benefit. Hence govt has with this benefit where all those loan takers who have paid their EMI’s on time will also be just paying the interest on their loan outstanding and not the compound interest for the period of 6 months (from Mar 1 to 31st Aug 2020)

Note that the interest applicable for calculation purpose will be as on 29/02/2020.

However because the EMI payments have already been made, the govt will pay back the difference to your bank account in form of a cashback in a few days. Let me summarize it

What you have to pay : Only the simple interest on the loan outstanding as of 29th Feb, 2020

What you paid : Compound Interest on the loan outstanding as of 29th Feb, 2020

What you will get back : Difference between Compound and Simple Interest for 6 months

Example Calculation

Here is a sample calculation for a loan outstanding of Rs 50 lacs (as of Feb 29,2020) with an interest rate of @9%

So you will get back this amount in form of cashback

This benefit is available on

Housing Loans

Automobiles Loans

Credit Card Debt

Education Loans

Consumer Durable Loans

MSME Loans

Other Eligibility Criteria to get this benefit

The Loan Outstanding should be up to Rs 2 crore

The Loans should not be NPA as on 29/2/2020

This benefit will also be passed to someone whose loan is closed during the moratorium period. Do let me know if you have any questions on this and I will be able to answer that.

Do you have a daughter? Saving in gold for her marriage?

Nice! .. Nothing wrong with it.

Just that I wanted to tell you what your daughter wants?!

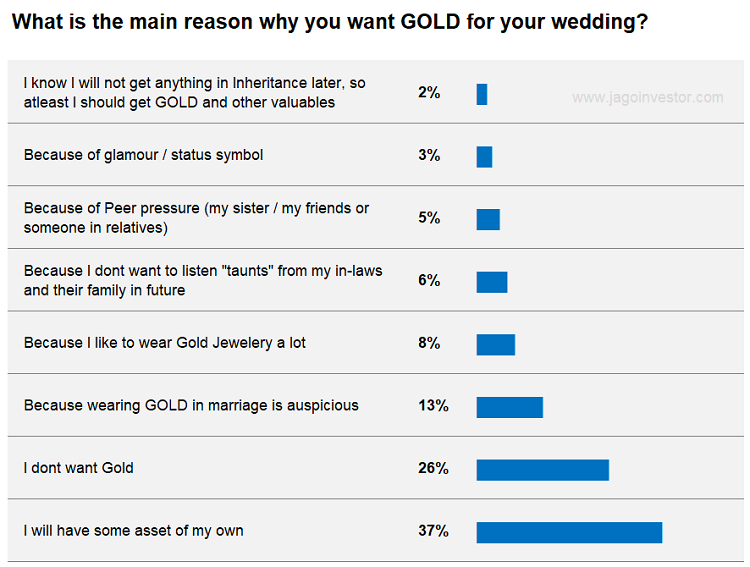

Yes, that’s exactly what we did. We ran a survey with around 1,996 people which was a mix of men and women and tried to get a perspective of how women (and men also) see the gold which is given in our Indian marriages.

Check out this 20 min video below where I have shared the results of the survey in detail and also gave my commentary.

Indian marriages are not complete without GOLD.

Every parent tries to give enough gold to their daughters in form of jewelry which is worn by the bride in marriage and it also kind of becomes a scorecard for others to compete. But do daughters really want gold from parents to that extent?

Here is what females replied to our question when we asked them “What is the main reason why you want GOLD for your wedding?”

Check our more survey results in our video above..

There is enough for me to talk on this on this topic, but I would save that for another day and rather point you to this excellent article which talks about GOLD, Dowry and what women have to go through in our country

My parents, however, decided to give me — a person who does not wear any jewelry, not even a wedding ring — a pound or two of gold jewelry. A matter of pride.

“Your father is a doctor and mother is a professor; people will expect you to wear some gold,” an aunt explained.

“What you do today will reflect on your sister and will affect her wedding,” another aunt said.

Weddings are hard, and I had no fight left in me. So I went along with it. I wore an armor of gold. The numerous chains were stitched onto my sari to keep them in place. I never saw that jewelry again after the wedding. My mother-in-law has it safe in a bank locker somewhere.

One of the first conversations I had with my mother-in-law was when she told me that her son had certain responsibilities to his sister. She then asked me to not stop him from fulfilling those.

Years later, I decoded that cryptic message.

She was trying to tell me that when the time came, I should support my husband in paying his sister’s dowry.

But I don’t think I can support a system that turns women into bargaining chips.

I would really love to get your comments and opinion about this topic. Please share that in the comments section.

Disclaimer: The survey results don’t claim to showcase what the whole of India thinks. The survey was taken by only 1,996 people and its not a very big same size as such, however it’s not very small though.

Congrats! – Health Insurance just got a lot better

IRDA has recently come up with some major changes in health insurance guidelines which are extremely customer friendly. These changes will reduce a lot of confusion that customers used to face while buying health insurance and will also help in smooth claim experience.

These changes are really good and it’s suggested that you should be aware of all the changes if you have a health insurance policy. It will take some time to understand these changes, but please read this article fully.

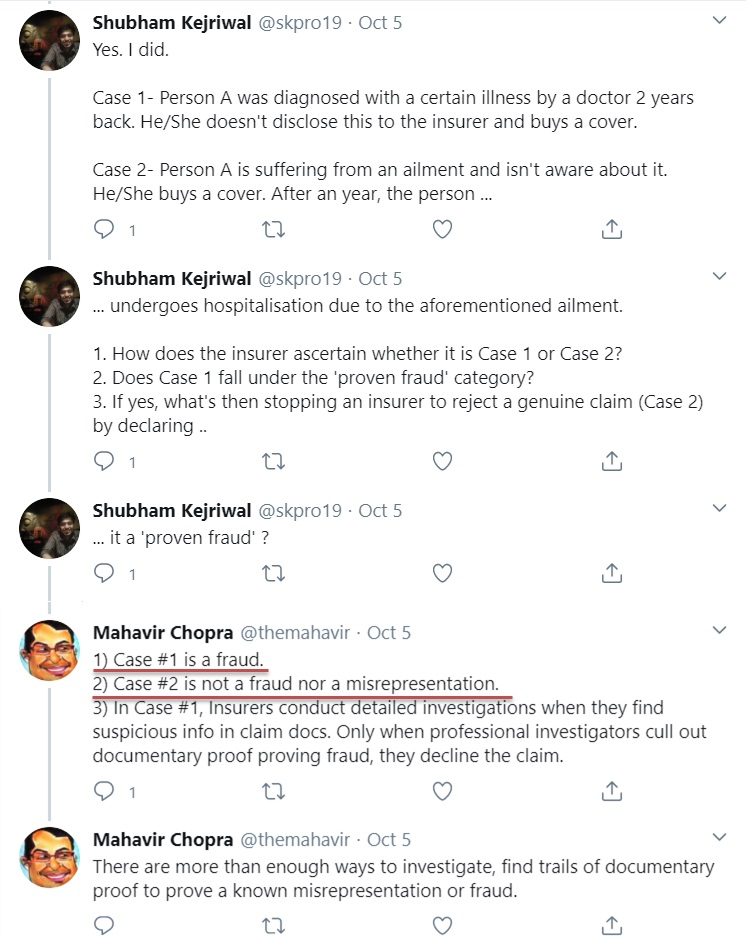

In case you like to listen, rather than read – here is a 35 min video discussion I did with Mahavir Chopra of Beshak.org who is an expert on this subject and a good friend too. While there are many big and small changes in the guidelines, the video talks about the top 10 changes which matters to you.

Change #1 – Standard definition of 18 exclusion

There are various exclusions in a health insurance policy and wordings for them differ from policy to policy. This confuses the policyholders while their decision-making process. Now IRDA has standardized the definitions and wordings for all kind of exclusions

One of the examples of this is the wordings for a pre-existing illness, 30 day waiting period, maternity, obesity, and many more. In various policies, the definition is different for these terms and it leaves a grey area many times.

Now with the new rule, every policy will have the same wordings and definition of the exclusions along with a CODE for each exclusion.

Change #2 – No ambiguous wordings or definitions

Apart from this, IRDA has also said that there should not be any ambiguity in the wordings which can create confusion in the future. For example – “Obesity is not covered, and any other illness which is derived out of obesity is also not covered”.

If you look at the example above, how will an insurer and the policy come to an agreement is something was because of obesity or not? There may be a disagreement in the future and companies can deny the claim citing some unreasonable thing.

Now, this practice ends…

Change #3 – Many Exclusions are disallowed

Now many exclusions which were part of policies earlier are disallowed, which means that companies will have to cover them. Some of the examples are as follows.

Treatment of mental illness

Behavioral and Neurodevelopmental Disorders

Genetic diseases or disorders

Puberty and Menopause Related Disorders

Injury or illness associated with hazardous activities