Jagoinvestor

Jagoinvestor

December 23, 2013

December 23, 2013

A detailed information about Inflation Linked Bonds from RBI and investment in it

RBI has announced that its going to issue Inflation Indexed National Savings Securities – Cumulative (IINSS-C) for retail investors where one can invest and get returns equal to Inflation + 1.5%.

These bonds are now coming up in markets, as it was announced in the last budget that govt will bring inflation linked products very soon (RBI link here).

The minimum Investment amount for these inflation linked bonds is Rs.5,000 and the maximum can be Rs.5 lacs per applicant per annum. The inflation linked bonds are going to be available only for 9 days, starting from 23rd Dec to 31st Mar 2014 only (update – This date was earlier 31st Dec, later it was extended to 31st mar).

The best part about these bonds is the hedge against inflation, so you don’t have to worry if your investments will be able to beat inflation or not.

Returns from Inflation Indexed Bonds

As per the RBI guidelines, the return you would get is “Base rate of 1.5% + Inflation Rate based on Consumer Price Index (CPI) , compounded half yearly”. So assume that, CPI inflation number is 10%, so your final return would be 11.5% (10% + 1.5%) .

Actually because its compounded half yearly , the returns would be a little more than 11.5% . One important point to note is that in case of negative inflation (which we are all sure will not happen), you get 1.5% guaranteed.

The best part about these bonds is that the benchmark for returns is CPI inflation and not WPI !. Because CPI is one the best measures of inflation parameters available in India. CPI is more close to reality, tracking the change in prices of end-user numbers unlike is sister WPI (Wholesale Price Index), which tracks the price changes in wholesale market. Read more about WPI vs CPI here .

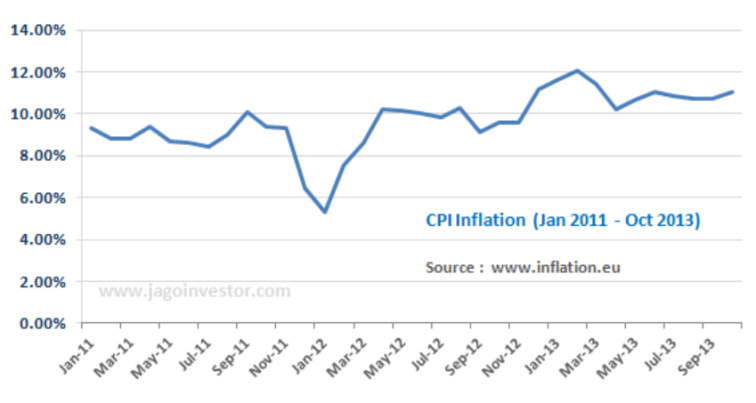

Below is the last 3 yrs history of CPI inflation for you to get an idea about what was CPI in last some years ! .

Taxation Angle ?

This can be disappointing for many, but there is no tax benefit when you invest in these RBI bonds. You do not get any income tax exemption at the time of investing under Section 80C or anything else, nor they are tax friendly at the time of maturity.

You will have to pay income tax on your returns as per your slab rates at the time of maturity. Now that’s the price you need to pay to get the guarantee that your investments will be hedged against inflation.

Can you get Loan by Pledging the Bonds ?

Yes, you will be able to pledge these bonds and get the loan against it. Given that the bonds comes from RBI and govt guarantee’s the returns part, the lenders would not mind lending you against the inflation linked bonds. However you wont be able to sell the bonds in secondary markets, like you can do some of the other bonds which came few years back.

Can NRI’s Invest in These bonds ?

NO. NRI’s are not allowed to invest in these inflation linked bonds from RBI. As per the guidelines from RBI declaration about bonds, only Individuals , HUF’s and Charitable Institutions and Universities are allowed to invest.

Premature Withdrawal

The bonds tenure is 10 yrs, however its possible to withdraw prematurely after 3 yrs of investments (with penalty charges) , however a senior citizen (65+ yrs) would be able to do premature withdrawal after just 1 yr. Note that premature withdrawal rates are high enough to discourage you to do so ! .

How to Invest ?

One can invest in these bonds at branches of SBI bank , all other nationalized banks (Vijaya Bank, Bank of Baroda, Maharashtra Bank, Bank of India etc etc … all of them) and 3 private banks which are ICICI bank, HDFC bank and Axis Bank.

Subscription to the Bonds will be in the form of Cash/Drafts/Cheque/online through internet banking. Cheque or drafts should be drawn in favor of the bank (those mentioned above), specified in paragraph 10 and payable at the place where the applications are tendered. I think its better to visit the bank for exact procedure incase you are interested.

Full Brochure about these bonds from RBI is below:

Who should Invest ?

At first glance the bonds look very good option to make long term investments who are too scared with inflation and it worries them to core.

Those investors who are approaching retirement and want some kind of security against inflation can surely look at these bonds, but then be ready to pay income tax on the returns part. Truly speaking your final return depends on various things like CPI inflation in future and the Taxation laws at the time of maturity.

I contacted some of the other bloggers and experts to know their opinion about these bonds and their comments and here they are !!

Karan Batra, A Chartered Accountant who writes on Income tax on his blog was not very excited about these bonds and says

These Bonds are only Inflation protected and not Tax protected but sadly the Tax Rates in India are much higher than the Inflation Rates in India. Therefore, it is always advisable that the investor should prefer to invest in tax-free instruments like PPF as they yield a better return.

Moreover, the computation of interest and principal readjustment is complex which leads to an even highly complex tax structure. These Bonds may give slightly higher returns but the complexities are so much that it I’m advising my clients to stay away from this issue and rather invest in PPF/Fixed Deposits

However when I contacted Deepak Shenoy to comment on these bonds from long term perspective, He was positive about these bonds and says

The product makes sense for anyone in income brackets that are less than 30%, but you have to buy the idea that inflation will remain fairly high over the next few years. If the CPI inflation falls, your return comes down appropriately. (In which case the fixed coupon tax-free bonds or PPF is a way better idea).

You can read the detailed posts from Deepak on these inflation linked bonds here and here.

Are you worried about inflation in future? Are your investments hedged against inflation? Please share your thoughts about it in comments section below !

Also be ready for the “Oh My God” Offer coming on 7th Jan, which will be a great one in a year offer from Jagoinvestor you can’t afford to miss. More information about it soon !

I want to know how to submit money in this bond via internet banking because I went through the form uploaded on rbi website and it does not mention any account number.Also posting link for RBI website without prior written permission from RBI is not allowed (as far as I know correct me if I am mistaken)

I am not sure if they are still available !

I went to ICICI bank, they didn’t knew about it at all. they said they will esquire & get back to me ! probably lack of advertising !

Yes, can happen . Not all branches might be aware of it !

RBI has extended the dates for these bonds. Instead of the bond closing on 31st December 2013, it is now closing on 31st March 2014. Just wanted to share it with everyone.

Thanks for sharing that Divya , was not aware of it !

I think one can invest in these if one is retiring when they mature in 10 years as he would have to pay less or no tax. Especially during this period Jan-Mar one has to concentrate on investing in products which reduce his tax payment for current financial year first of all. Well if one has extra money left after all his investments towards tax savings etc then he can put money in this to make that money grow along with inflation.

Thanks for sharing your views on this product !

I think this suits bet to those peoples who will retire and will most probably not come under any taxable bracket. Then only all this interest paid will be worth it.

I am recomending it to my DAD whio does not falls any taxable income bracket and is going to retire very soon.

Yea , I think you are thinking on correct lines !

No kidding! I’d rather do some at home gardening and negate the inflation than go for this CPI + 1.5% – TAX (= Net Loss!). Big brothers always manage to come up with big schemes to fill up their coffers at the expense of unsuspecting customers!

Vijay

So in that case, whats the alternative investment option for you ?

My thought is as follows – If I was retiring in another 10-yrs or less, I would gladly go for this investment with a ‘decent’ lump-sum (<~10 lakh or so). However, at high-twenties, one could just as well go for the long-term in equities with the added taxation benefit – why risk a certain 30% loss in the gain (making an effective returns of the order of 8% or less) over a 'possible' loss-free gain of 12-15%….

Additionally, there does seem to be quite a few complications in these RBI-Bond guys' calculations….not very comforting.

Thanks for sharing your views on this

I would not like to invest in these bonds based on below points:

– No fixed interest rate, rate of 1.5% at zero inflation is very low. It should have been savings account rate at zero inflation.

– Not tax free, as shown very well by Abhijit, post tax returns will not beat inflation.

– As per RBI’s own estimates, inflation will come down.

– Illiquid and very long term.

Tax free bonds / PPF are much better for tax purpose.

Company NCDs are better for returns purpose.

Ofcourse, equity is there.

Thansk for sharing your points . In that case you expect the future to be better in equity or other debt products

Nope, this one will be a pass from me. Seems very less returns and that too taxable….we all know that smart investing should “beat” inflation — the keyword here is “beat inflation” (after taxes ideally). Here we’re matching inflation + 1.5%. It wouldn’t be wise to invest on this in my opinion

Yes Ram

Thats how a long term investor should invest because the focus is on absolute return , but how about those who are retiring who want to hedge their returns in respect to inflation ?

Actually it is not suitable for anyone above 10% tax bracket. Considering you invest Rs. 100/- for example and inflation remains 10%, its value before tax will be Rs. 111.5/- (10% inflation + 1.5% base rate). But post tax returns are as follows:

For 10% tax bracket: Rs. 110.35/-

For 20% tax bracket: Rs. 109.2/-

For 30% tax bracket: Rs. 108.05/-

However, things that costed Rs. 100/- this year would cost Rs. 110/- next year.

From the above example, we see their is marginal gain of Rs. 0.35/- for investors in 10% tax bracket (at the time of redemption). Now who knows what will be your tax bracket after 10 years???

It’s too complex. It is better to invest in Equities (direct/mutual funds) to beat inflation.

What say Manish? Please correct me if wrong.

Yea . Simple analysis you have done . Its true that its not giving any real return, but overall you are moving with inflation !

As you rightly pointed out, this is for some one who is looking for a safer and risk free investment.Any way it is a good option when compared with other available options with better returns.

Thank you for the detailed article.

Thanks for your comment

http://www.rbi.org.in/scripts/FAQView.aspx?Id=91

Hi Manish ,

i was going through FAQ’s at rbi site and i found that WPI will be used and not CPI for the coupen calculation.

Check the correct FAQ’s

here’s the link – http://rbi.org.in/scripts/FAQView.aspx?Id=99

There were other bonds launched some months back where the base was WPI , I think what you are saying is that that bond , not this one !

Hi Manish,

I’m posting on behalf of my father. He’s going to retire by next year. How beneficial would it be for him to invest in these bonds, both from the returns perspective and the TDS perspective ?

p.s He wouldn’t have any income from next year onwards(once he retires) and he’ll commence his journey as a senior citizen also.

Hi Abhishek,

If your dad is a looking for a fixed income every year then long term bonds are not the answer. If your dad has fair amount of corpus at this point then I would suggest you to recommend a high interest FD. I have seen ads in HDFC (not the bank) centers about interest rates ranging from 10.2 to 10.5.

Since your DAD will not have any income next year it will take a whole lot of interest to get his income from FD eligible for higher bracket tax cuts.

Inflation linked Bonds are good however they are meant for long term investment as Manish has pointed out especially since there is a penalty if someone attempts a premature withdrawal.

Assuming your Dad would require year on year income from the corpus the LEAST risk free entity however one hovering close to the inflation index would be an FD with higher rate of interest. Risk can further be averted by choosing a reputed firm. You could also look at Ultra Short Terms Funds however this carries some amount of risk hence it is advisable to look into the portfolio of the fund to ascertain whether they are invested heavily in trustable entities (e.g. Notes from Reserve bank and FDs from nationalized banks etc.) however with this you will have the advantage of Long Term Capital Gains tax if you withdraw the amount after a year.

Thanks a lot AJ… Well the suggestion about the FD’s interest not crossing the tax bracket was something i hadn’t thought of….

Right now,we’re not considering the case for premature withdrawal or regular year on year income…. only thing was in terms of a long term investment…how good are the bonds…..Even though i don’t like the concept of lumpsum investing…but just wanted to get a second opinion from Manish and rest of the knowledgeable crowd at Jagoinvestor before going ahead with the investment….

He’s already investing systematically(monthly) in equity n hybrid debt MF’s along with PPF….and starting from May’14…he would also be eligible to invest in the Senior citizens saving scheme…. With your advice,I would definitely add FD’s to the list…..

Well, the Bonds are safest investment especially coming from Government entities.

Bond is debt instrument which means that the other party has an obligation to pay the amount back with interest (coupon rate). Bonds would be the first payoff done when an entity goes under. Since Equity (stocks) signifies ownership of the company the stock holders would be paid last (if anything is left).

You can also sell the bonds in the bonds market midway in case you want to cash out.

I would have recommended to your DAD to invest 30% in equities (or 3-4 good equity mutual funds) and rest 70% in income funds for stable income and little appreciation.

I think its a decent option, You already know that he will pay income tax based on his slab, but if the overall return is below the taxable limits, then he does not pay tax ! .

So,if i understand you correctly… the final payout(principal+interest) after holding it for 10 yrs….would decide which tax bracket he lies in…and he would’ve to pay tax accordingly… for eg. If the total payout is say 4lakhs…then he would come under the 10% tax bracket…right ??

Also,should the accrued income(yearly interest accrued) also be declared… i mean…while filing every year’s ITR ???

NO , It does not mean that way . If you get 4 lacs as total payment and out of that 2 lac was interest part . Then this 2 lacs will be added to your income in the final year . Now after adding 2 lacs to your other income, your TOTAL income will be lets say X , now whatever income tax bracket you fall in , it will be considered .

Manish