I was talking to one of my distant relatives and told him this – “When you want to increase sales of a financial product, make it complex, and if you want sales to boost a bit more, increase the complexity a bit more!”. Because the moment a financial product is “complex”, investors perceive them to be more valuable and worth investing. When a product is simple, it does not look powerful to them. Let me break this myth to you today.

If you look at any financial product, it will either be simple product or a complex product. Let’s see what they are

1. Simple Products

Simple Products are those which are very very focused, with one intention and true to focus, they are easy to understand. Some examples are Fixed Deposits, Term Insurance, Mutual Funds, Health Insurance, Motor Insurance, Recurring Deposits, Govt Bonds etc.

2. Complex Products

Complex products on the other hand are those kind of financial products, which are built by combining two or more Simple products functionalities. Some of the examples are ULIPs, Endowment or Money-back plans, Fixed Maturity Plans, Child Plans , ULHP (unit linked health plans) etc. You will see that its much easier to sell complex products because they offer more than one feature and people feel that they are such an excellent products with some magic, but the truth is that they just have features of more than one Simple product.

For example if you take a ULIP, its just offers the functionality of term insurance and mutual funds. You can get life cover and also enjoy market linked investments, & just like that a endowment plan or money-back plan also offers the functionality of a term plan and a bond.

Simple Products are Powerful

If you have been a regular reader of this blog from some years, you would have realized by now that simple is powerful and that holds true for financial products also. All you need are simple things like a term plan, a health insurance policy, a SIP in mutual funds and an emergency fund and you are pretty much have completed your financial planning. You don’t need much more than these simple products. In my 1st book – “16 personal finance principles every investor should know” , I have stressed upon several simple concepts, which will how you how easy is the game of personal finance.

Complex Products have high CHARGES

I am not commenting on the usefulness of complex products, because they can also offer a great way of investing your money, but the one thing that’s really clear is that a complex product can charge higher fees just because someone has taken the pain of creating those complex products. Now because customers feel they are special, they will also be ready to pay high fees … and that’s exactly what happens. When you perceive something as powerful (complex seems to be powerful to many), you will be more ready to pay higher fees.

Do not look beyond Simple Products

For a common investor, I would say that most of the times Simple products are enough. When they come across a financial product, they should see how simple it is and what core functionality it provides. If it tries to do a lot of things and you are lost in its features, its probably a time to say NO to it and move on.

A lot of people have created more wealth by wrongly investing in Simple products that those who correctly invested in complex products. A simple law of Design is that “simple is powerful” and it’s true for most everywhere, including personal finance.that this article does not mean to say that all the complex products are bad and are not worth looking, we are just talking about a general principle!

What do you think about this simple principle and do you also observe the same thing?

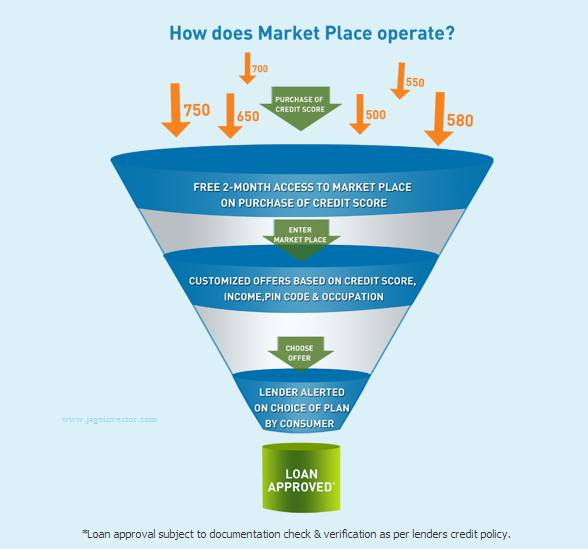

CIBIL has introduced a new facility called “Cibil Marketplace“, which will act like a portal where a person can get customized loan and credit card offers based on his cibil score. Right now, what happens is – when a person applies for some kind of loan or a credit card, the lending institution checks his credit report and credit score and based on their internal criteria and rules, reject or accept the application and move to the next step .

How does CIBIL marketplace work?

With CIBIL marketplace, the whole process is reversed. Here, you can find out which lending institutions are ready to give you different kind of loans, interest rates and other conditions based on your credit score. So a lot of lenders will participate in the cibil marketplace and will give their criteria and checklist, like what kind of customer they would like to offer loans. For example – A lender can say that they are ready to give Car loan @13% interest rate to a person having cibil score between 700-800 and @12% if cibil score is more than 800 . Thats one example .

Another lender can say that he is ready to give home loan to people who have credit score below 700 score, but on a condition that he should be working in a software job, however the interest rate would be as high as 15% – this is just an example of how it might look like. So this is how all the lenders will give their own criteria and when you enter the market place, after the filtering you will be shown only those lenders and loan offers which are exactly for your profile. So if you want to increase the number of loan offers, you need to improve your cibil score for that.

Right now the CIBIL marketplace is started with only Credit Cards. But very soon, you will see Home loans, Auto Loans, Personal Loans and even Business Loans on the portal. Just wait for some time or the next update from CIBIL on this.

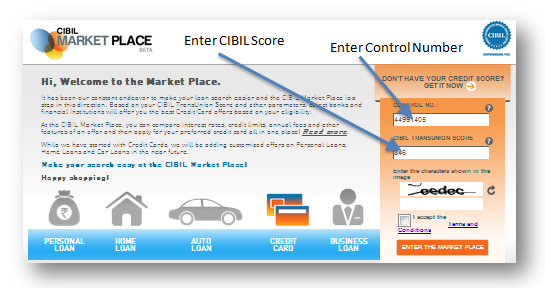

How to Apply for Loan with CIBIL marketplace ?

Step 1 : You need to first visit Cibil Marketplace website. When you go there you need to fill in two information.

Step 2 : You need to enter your Control Number (which is 9 digit number that is mentioned at the top right of the CIBIL report) and your latest Credit Score, which should be maximum 2 months old. That means, if you had applied for a credit score long back (more than 2 months back) , you will not be able to use that data to enter CIBIL marketplace. You will first have to apply for a latest cibil score (You can get your cibil score online) and only then you will be able to enter the marketplace. One reason for this is that, cibil score and report keeps getting changed each month when banks update the customers information with CIBIL. So ideally if you know control number and cibil score of some other person, you can enter the cibil marketplace with that information and see all the data . Therefore make sure you dont share this data with anyone whom you dont rely.

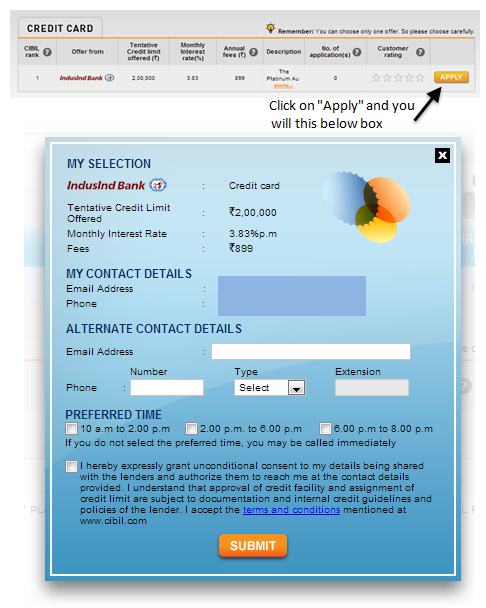

Step 3 : The next step is to go inside the marketplace. You can see different kind of loans section and how many lenders are ready to lend you in each section. For example you can see that only 1 lender is interested to lend in this example and that’s “credit card” section . As of now, only credit cards are offered as this is new facility. But in future you can see more lenders in different sections. All you need to do here is click on the kind of loan you want.

Step 4 : After you choose the section, you can see the list of all the lenders individually with some information like Tentative Credit Limit offer, interest rate, fees, charges and other information. You can click on “Apply” button and instantly a small box will appear where you can apply for the loan there itself. Now this will be a kind of pre-approved loan because this is customized to your cibil score, but the next step will be the documentation check, which is part of the check in general . For those who would like to learn more about CIBIL and Credit Score etc, there is a detailed 40 min video course on our Wealth Club.

So these are the 4 steps you need to do to take the benefit of CIBIL marketplace.

Few Important Points related to Cibil MarketPlace

You can choose only one offer in each category

While purchasing your CIBIL TransUnion Score (and CIR), please make sure you fill up your income details accurately. As this will ensure the offers that are displayed in your Market Place are the ones you are eligible for. Any incorrect income detail will mean incorrect offer eligibility and can be rejected by the lender at the time of verification.

It also depends how many lenders choose to participate in CIBIL marketplace. There might be lenders who choose not to.

Once you have selected an offer then the respective lender will get in touch with you. Please ensure the details entered by you in the CIBIL TransUnion Score (including CIR) purchase form is accurate. This will enable the lender to respond to you at the earliest. You can also provide alternate contact details while selecting and confirming the offer in the CIBIL Market Place.

Who will benefit with Cibil Marketplace ?

CIBIL marketplace is an innovative platform and will also be helpful to those people who have low cibil score and a bad credit report , but still want to go for some kind of loan, even if it means on certain terms and conditions. It may be the case that they might pay a little more interest, but that would be better than not getting loan at all. This platform might also be the first step in providing incentive to those customers who have excellent cibil score. They might get loads of loan offers from lenders with lower interest rates compared to normal customer. Only the time will tell how this platform will evolve.

Let us know what do think about CIBIL marketplace and is it useful for you ?

Some months back, when we were working with a Mumbai based client of ours, we noticed that one of his expenses of “Eating Out” was extremely huge. Their explanation was they were never able to control the number of times they went out. So we thought how about limiting the amount spent somehow ?

Envelope budgeting system

Today I am going to share Let me share with you all a simple and effective budgeting system which has been in use for centuries – worldwide! . It’s called the “Envelope Budgeting system”.

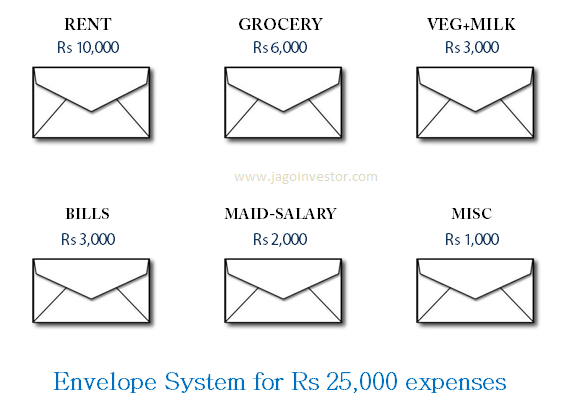

The common problem across families is that they keep spending money on various things from a single card or pool of money. The basic idea here, with this system is to label your different expenses, categorize them if you will, and keep an envelope with money dedicated to that category, in it.

When you need to spend on a category, voilà, you take the CASH for its respective envelope and spend. Let me give an example. Suppose your expenses are as below.

[table]

RENT

Rs 10,000

GROCERY

Rs 6,000

VEG+MILK

Rs 3,000

BILLS

Rs 3,000

MAID-SALARY

Rs 2,000

MISC

Rs 1,000

Total

Rs 25,000

[/table]

5 Simple points regarding Envelope Budgeting System

1. Once it’s gone, it’s gone

When you take some money out of an envelope, and spend it, it’s gone! You will be left with some remaining amount for that particular month. Now all you have to spend that month is the leftover. So spend it wisely.

If you still want only spend more than what the envelope contains, you just break the system. Better stop following it then. It’s not for you

2. Don’t transfer between envelopes

Just because you have some money left in some category, does not mean you can spend it on another category. This system is all about controlling your expenses in individual categories. Whatever is left in some envelope should go to your investments. It’s like a bonus leftover.

3. If you fail to follow, invest 10x the amount as penalty

It’s human to fall off the wagon. At times you will deviate from the plan and spend more money other than you allocated. In this case, you should penalize yourself for breaking the rule, by investing 10x the extra amount into some investments. For example, you have Rs 3,000 allocated to “Eating Out” you spend Rs 5,000 in a month. Then you are using an extra Rs 2,000. You should penalize yourself by investing Rs 20,000 (10 times) in some thing to offset this crime. This will be a good spin on just desserts!.

4. Emergency expenses, but settle later

Ideally your expenses should be planned and the money should come from the envelope, but you will have to spend sometimes on your credit/debit card (read various credit card cashback offers), which is fine at times, but make sure you settle things back when you are back at home.

5. Guilt-free shopping

The thing I like about the envelope budgeting system is the “guilt free spending.” Once you have allocated the money to different categories, then you can spend up to the limit, without thinking much. That’s the best part.

TIP : Libin informed me in comments section that there is an Android app called Easy Envelope Budget Aid (EEBA) for this envelope system ! ..

Yes, many times I feel bound but I know what I have got by following this system. Be it getting rid of a loan (worth Rs.2 lacs), renovation of my home (worth Rs.2.5 lacs), be it car (Alto), money for Jewelry (worth Rs.1.5 lakhs), 40 k cash as gift to near & dear ones in a span of 6 years. Right now I am saving for my daughter’s school admission.

I agree that I never spent for grocery, maid salary & rent being in a joint family but still I wonder that I was able to achieve these targets when my present salary is just around 26k and when I started following this system 5 years back, it was much less.

I started this as I had no choice, but believe me I am now addicted to this system.

It’s not for everyone

A lot of people use this envelope system and are pretty successful in following it for months and years. However many people start this, but fail somewhere in middle and are not able to continue. Its all about how serious you are about controlling your expenses and being disciplined. Do you think this Envelope system will work in your case ?

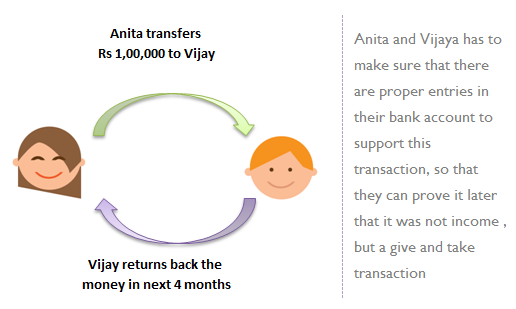

Do you know that, when someone deposits some money in your bank account, what is its taxation angle ? A lot of people take some loan from their friends for few months and then return it back, but never think twice about it from taxation angle? Your parents deposit some money to your bank account because you want to pay the down payment of your house. While it’s a help from your parents, have you ever thought if you have to pay tax on that amount or not?

In this article lets see all the aspects about these kind of transactions, when money comes and goes out of your bank account and what are the rules for income tax on gifts received from relatives or other people in India .

Let us first see what kind of situations we are talking about ?

You swiped your credit card for your friend Rs 20,000 purchase and then your friend paid back money to you by transferring it to your bank account.

You asked Rs 50,000 from your friend as loan and paid him back after 1 month.

You got Rs 50,000 cheque from your relative on your wedding.

Your father transferred some money you your bank account as help for some purpose.

These are few instances, which happens in our lives. But its very important for you to understand the tax implications in various scenarios and the possible issues which can come up in the future, if income tax department decides to scrutinize your income tax returns for example. By understanding the gift tax rules and precautions to take, you will be safe. So now, let’s look at 5 points which will help you understand rules about incomes tax on gifts in a better way.

By virtue of Section 56(2), any sum of money exceeding Rs. 50000 received without consideration by an individual or an HUF from any person is chargeable to tax as income under “other sources” subject to some exclusions . Below we are going to see all those exclusions and gift tax rules.

1. Upto Rs 50,000/year is not taxable

The first major rule which every person should know is that there is no tax to be paid on gifts received (cash or kind), if the amount of the gift is upto Rs 50,000 in a year. However if the total amount crosses Rs 50,000 . Then you will have to pay the tax on the total amount received (not additional). For example – If a friend of yours gifts you Rs 30,000 in a given year, you don’t have to pay any tax on that amount, as its below the limit of Rs 50,000 .

Now suppose you also get Rs 20,000 after that, still you don’t have to pay the tax as the total worth of the gift you got in the year was Rs 50,000 till now (less than the limit of Rs 50,000) . But now, if someone gifts you another Rs 10,000 . Your total gifts in a year is Rs 60,000, so you will have to pay tax on the total amount of Rs 60,000 , not just on additional Rs 10,000 . This Rs 60,000 will be included in your income and you will have to pay tax on this Rs 60,000, as per your tax slab. Note that this is exactly how the written law is.

Since 1/10/2009, Section 56(2) has been amended and the scope of ‘’gifts’’ will include even immovable properties or any other property besides sums of money under its ambit.

2. Any amount received by relatives is not taxable at all

Another rule for income tax on gifts, is that any amount received from specified relatives is totally tax free in the hands of recipient. So if a relative gives you gift in form of cash/cheque or in consideration, you will not have to pay any tax on the amount received.

Following is the list of relations which are considered as “relatives” for this

Your spouse

Your brother or sister

Brother or sister of your spouse

Brother or sister of either of your parents

Any of your lineal ascendants or descendants

Any lineal ascendant or descendant of your spouse

Spouse of the persons referred in above points

Example – So if you want to buy a house and your father/mother/sister/brother etc transfer Rs 20 lacs to your bank account. You don’t need to worry about the taxation part, because its a gift from your relatives and you will not have to pay any tax on this amount. However its a good practice to do the documentation for this, if the amount if pretty big like in this example. All you need to do is document this transaction on a paper which clearly states that who transferred the money and the reason for it, along with the signatures of both parties. In future, if there is any income tax scrutiny, this small piece of proof will be handy and will help you a lot.

Important – Note that, there is no income tax to be paid on the money received from relatives, however at times income clubbing provisions may apply, for example, if a husband gifts Rs 10,00,000 to wife, there is no ta to be paid by wife on Rs 10 lacs received, however when she invests that money and if any interest income is generated, it will be clubbed with husband income. Read all about income tax clubbing rules here.

3. Any amount received as Wedding Gift is not taxable

One of the few advantages of getting married is that any amount you get, as wedding gift is not taxable in your hands, either from relative or non-relative 🙂 . So even if you get Rs 1 crore as wedding gift from someone in your wedding, it’s not taxable in your hands.

Lets see some examples –

Suppose if your spouse parents give you some gift worth Rs 10 lacs on marriage, it will be treated as a wedding gift and will not be taxed. However, it is not clear by provision, whether the gifts should have been on the exact date of marriage, or a few days before or later. Normally, it should be sufficient if the gift is given just on the occasion of the marriage, means either on the day of the marriage itself or a day or two before or after. Practical common sense view would prevail in such cases.

4. Gift Tax on Movable/ Immovable properties

There is a valuation aspect involved in gifting of immovable properties

If the property is gifted without any consideration then if the stamp duty value exceeds Rs. 50000/-, stamp duty value will be taken

If the property is gifted for a consideration, then the actual value of the property will be taken

In case of other properties:

If gifted without consideration and fair market value exceeds 50,000, then the fair market value will be taken as the final value

If gifted for a consideration and the Fair Market Value (FMV) less consideration is greater than 50000, then the FMV less consideration amount will be taken as the value of the gift.

5. No tax on the amount received through WILL or Inheritance

When any sum of money or any property is received under a will or by way of inheritance, it is totally exempt from Gift Tax. So if you get a real estate worth Rs 50,00,000 and some other things worth Rs 30,00,000 through inheritance , you will not have to pay any tax on that amount received.

Be cautious about the take and give transactions

At times, we ask for money from our friends for some purpose and then give it back. One of the examples I can give is what I heard from one of the readers in comments section. He swiped his credit card for a friend for Rs 50,000 and then asked his friend to pay him back through online banking. Here if you see, the amount came to his account, however it was a reverse transaction and not actually a gift, so ideally this transaction should not be considered at all.

If its a small amount and can be justified with proofs, there is not much to worry about this. But in this case, lets say there is a income tax scrutiny, and tax inspector asks you about this “Rs 50,000” coming to your account. Now – You can clearly say that the money you got from your friend was a amount which you got back because you paid Rs 50,000 to him through your credit card. But just saying this will not be enough, He will ask you to prove it. Then you will have to bring your credit card statement, and prove to him that this was done by you for your friend and no one else.

The point here is – no matters how truthful you are, there should be something you can show to income tax officers in case this is questioned. So for any transaction like this, which involves a big amount, its always a good idea to have a proof, like in the example I just gave, the credit card statement will be handy along with a small note, where you friend signs saying that you swiped your credit card for him and he will pay back the money through netbanking.

In this same case, If you ccan’tprove that this money was just a “reverse entry” , you can imagine the situation. Even if you were clean, the whole amount would be added to your income and you need to pay income tax based on your tax slabs on the ground of unaccounted income.

Another point, worth noting is that just because you have a reverse transaction, the other party can get into trouble. For example, suppose you give Rs 20 lacs to your friend, who wanted the money for buying a house and then your friend gives back those Rs 20 lacs in 3 months. Note that now there is a clear entry that you gave your friend Rs 20 lacs, so in future income tax department can reach you through your friend and ask you about this Rs 20 lacs and from where you got so much of money. They can ask you to justify the source of this money. So always keep these points in your mind.

How to document Gift transactions, Registered Deed or plain paper?

A gift deed is a deed, that is executed and delivered in which the donor transfers title to the receiver without any payment or considerations. It a document which transfer the legal title of the property to the donor, where the consideration is not monetary but is made in return for love and affection. There is indistinctness with respect to compliance of the gift deed at times, Whether a gift deed is required to be made in every circumstance

When it is required to be stamped OR get registered?

Gift made by way of cash or cheque does not mandatory requires to be executed through a gift deed. Writing a plain typed note on a paper will generally suffice. It is not required to be stamped and registration is also not needed. You may simply mention the names of persons, their relation and that the gift is being given out of love and affection.

Gift made by way of movable property is required to be made in stamp paper and stamped by the notary or court, and registration of gift deed is not required in this case. For the purpose of making a gift of immovable property, the transfer must be effected by a registered instrument signed by or on behalf of the donor. Gift of immovable property which is not registered is not valid as per law and cannot pass any title to the receiver.

Conclusion on Income Tax on Gifts received

As far as you make the transactions which can be justified, there is not much to worry, however its always a good and safe practice to document things on a paper with proper signatures. This will help you because income tax scrutiny can go back to many years of your life. The stronger your documentation and proof, the smoother will the situation be.

Thanks to Rishabh Parakh (www.rishabhparakh.com), a chartered accountant who helped me while this post and gave his inputs. He is founder director of Money Plant Consulting (www.moneyplantconsulting.net ) a leading Tax & Investment Advisory service provider in Pune.

Budget 2013 was much awaited, however it did not excite investors as there was nothing much for them. It was a flopshow for investors considering they had high expectations from finance minister. Here is a quick summary for things which you should know

1. No Change in Tax Slabs

There was no change in tax slabs . Finance Minister said that the changes happened just last year and it was not possible for any increase this year. I could clearly see the discomfort in his voice when he said that. So no tax till Rs 2 lacs , 10% tax between 2-5 lacs, 20% between 5-10 lacs and 30% tax for above 10 lacs.

2. Rs 2,000 credit back for lower income group 1.8 crore taxpayers to benefit.

While there is no change in slabs, A Rs 2,000 credit back will be given to income tax payers in lower income group of Rs 2-5 lacs. I assume that you will pay Rs 2,000 less than your actual tax due to this. You can call it as a discount of Rs 2,000 in tax payment this time 🙂 .

3. Inflation Linked Bonds to be introduced

They are going to introduce something called as Inflation Linked Bonds, which will help you save your money in instruments which will match the returns with inflation . A lot of investors look at something on this kind, What do you feel ?

4. Claim upto Rs 2.5 lacs as tax exemption if home loan less than Rs 25 lacs in 2013-14

If you are planning to take a home loan of less than Rs 25 lacs, you can claim an extra deduction of Rs 1 lac in interest, over and above the 1.5 lacs, but only for year 2013-14 , not in all years. And this is applicable on fresh home loans, not on existing loans.

5. Service tax to be levied on AC restaurants of all kinds

Earlier, service tax was applicable for those AC restaurants which served liquor, but now service tax is applicable on all kind of AC restaurants, So your next eating out is going to be more costly!

6. 1% TDS on Real Estate Sale of Rs 50 lacs

For any Real estate transaction (other than Agricultural land) , the seller has to pay the TDS of 1% on the transaction amount if its more than 50 lacs. So if you sell a flat worth Rs 80 lacs, you will have to pay a TDS of 80,000.

7. RGESS first time investors income limit increased to 12 lacs

Earlier, RGESS scheme was only available to those investors whose taxable income is below 10 lacs, but now its increased to 12 lacs. Anyways, I feel RGESS is too complicated.

8. Reduction of STT on Derivatives , ETF’s and Mutual Funds

Trading in Equity, buying ETF’s and mutual funds would be a little cheaper. STT has been reduced in equity futures to 0.01%. MF redemptions from 0.25% to 0.001%. ETF purchases from 0.1% to 0.001% . So you can expect a minor reduction in your costs.

9. Dividend Distribution Tax on Debt Mutual Funds Hiked to 25%

Earlier only money market debt funds and liquid funds had a DDT of 25% , and rest other kind of non-equity funds had a DDT of 12.5% only, but now its going to be 25% DDT for all kind of debt mutual funds. So, if you have invested in MIP with dividend option, their will be more DDT paid on dividends by AMC and your NAV will down more than earlier . More on Deepak Shenoy’s Blog

10. Mobiles, High end SUV car’s are expensive

Due to increase in excise duty. you can expect mobile phones, set top boxes and high end SUV car to be more expensive.

What do you think about this budget ?

What do you think about this budget? Did you expect a lot of things from this budget? Apart from these there are lot of other updates as well, but I think these 10 points are enough to know for investors and one more thing . Direct Tax Code (DTC) seems to be taking shape and might be there next year 🙂

Is your health insurance cover enough at the moment? May be No! And you might want to increase it now. But if you feel that your health insurance coverage is sufficient right now, even then, it will need an upgrade after another 5-10 yrs.

Healthcare inflation is on rise in India and there is no way you can live with the tiny health insurance cover for rest of your life.

So let’s check 8 ways you can upgrade your health insurance cover.

If you have bought your own personal health insurance before 2010, in all probability, you have sum insured coverage of less than Rs.4-5 Lakhs.

While it’s great to hear that you at least have your own independent health insurance, and are not dependent on your employer health cover, it’s high time you realize that with the skyrocketing healthcare inflation, the sum insured you have is too low to even cover one hospital bill, leave alone cover you for your hospitalization expenses in your retirement years.

The amount of health insurance coverage you need has already been addressed in one of my earlier posts. What we are going to discuss here are the options available when one is looking for upgrading his/her coverage

8 ways to upgrade your Health Insurance Policy

There are various ways you can increase your health insurance cover. Below are some of them mentioned.

#1. Upgrade later, when needed

Though this may look like the most cost effective, ‘smart’ thing to do, mind you, this is the diciest options of all. Health Insurance companies will accept your upgrade request till you are young and healthy. No one wants you to enter their portfolio or books, once you are old, grumpy or dying.

Jokes apart, even if one of your family members suffer a chronic ailment like Diabetes, Thyroid etc. or worse make a claim in the health insurance policy, your chances of upgrade in the policy are almost zero.

If you are not aware, let me clarify – whenever you apply for an upgrade, you will have to make a fresh application to the Insurance Company for the upgrades giving declaration of any new diseases contracted etc. The insurance company will then evaluate the upgrade request similar to a new application and decide.

All said and done, even if the upgrade is approved, all waiting periods are applied to the upgrade part of the policy, from the year of upgrade, and not retrospectively.

#2. No procrastination. Upgrade your cover now

This is by far, the most ideal option if you have a lifetime health insurance plan and your family is reasonably healthy. Just apply for an upgrade to the highest coverage available first, before you try anything else, including a Top-up plan.

Yes, you will have to request for the upgrade at the time of renewal by filling an application, which will be subject to approval of the Insurance Company. If you one of you family members have had a claim for a chronic disease, you must explore upgrade for all the other members. If you are all covered under a floater, you can apply for a separate plan (explained in point 4).

If you are covered under individual plans, ask for upgrade for the remaining members in the same plan.

#3. Port your health insurance cover + upgrade

If the sum insured you have is the highest available with the current Insurer, you can explore the option of porting your policy to another product within the same insurance company, or another insurance company, which has higher coverage plans.

Note, for portability, in most cases, you need to apply to the new insurance company, 45 days in advance. While applying for portability you need to request for your preferred sum insured in the proposal form. Of course, you will get portability only for the existing sum insured and not for the upgraded sum insured. The waiting periods will start again for the upgraded part of the coverage.

#4. Buy second Health Insurance policy

If the sum insured you have availed is the maximum sum insured offered by the Insurance Company, and portability is not possible as explained above, another option is taking a second health insurance policy from another Insurance Company.

If you ever claim above the sum insured of Policy 1 you can always claim from Policy 2 for the rest of the claim. Ensure you inform about the existing policy in your proposal form for the new policy.

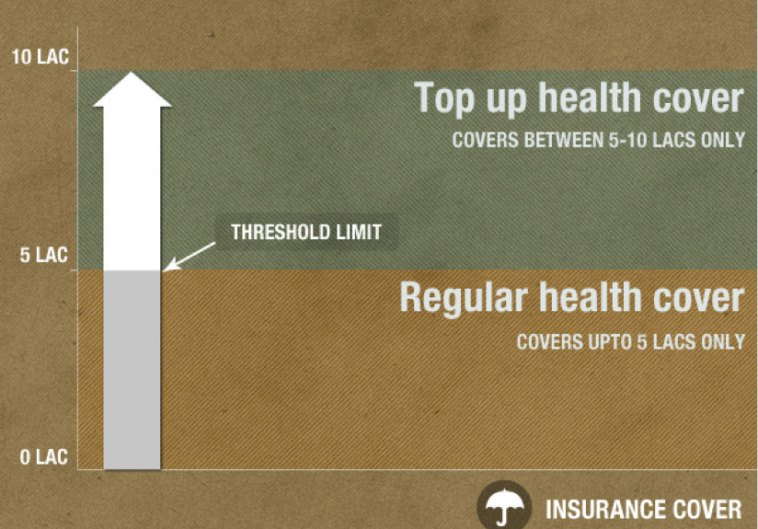

#5. Top-up Cover

Though Top-up plans are recently a popular option to increase your health insurance coverage, you need to understand how they work, before you sign-up for such plans. The policy provides a high coverage with a threshold amount upto which you cannot make any claims.

For instance, you buy a 10 Lakh cover with a 3 Lakh threshold (also called deductible) – you will be able to claim in this policy only when you have made claims of above Rs.3 Lakhs.

There are primarily two types of top-up health insurance plans :

1. Top-up health insurance:

Per claim deductible: Here the top-up coverage will trigger only when one hospitalization claim crosses the threshold sum insured.

For instance, if in the plan in the above example, there are 2 claims in a year of Rs.2 Lakhs and Rs.3 Lakhs each, the top-up coverage will not trigger since none of the 2 claims crossed the “per claim threshold” of Rs.3 Lakhs. On the other if there is one claim of Rs.4 Lakhs, then the top-up policy will pay the remainder Rs.1 Lakh, as per the terms and conditions.

2. Super Top-up health insurance:

As the name suggests, this is a better version of a top-up plan. Here the coverage will trigger even if the sum total of all claims made in a year cross the threshold sum insured. In the above example, where there are 2 claims made, both the claims will be paid, upto the sum insured of Rs.10 Lakhs.

Unfortunately, there is only United India which provides this plan (albeit, with a lot of reluctance) HDFC Ergo and Max Bupa are in the process of releasing such a plan, soon. Watch this space.

#6. Critical Illness Plans

In most cases, a high coverage of health insurance is required due to contraction of a critical illness like Cancer, Paralysis, Heart Attack, Kidney Failure, Bypass Surgery etc.

A Critical Illness Plan provides a lump sum benefit irrespective of the actual expenses incurred provided the insured person is diagnosed for a listed ailment and survives for 30 days. Taking coverage of around Rs.5-10 Lakhs for critical illness is a good option. The only flipside of this plan is risk of suffering an ailment not listed in the policy.

Ensure you take a policy which covers an extensive list of illnesses, at least till the age of 70. There are plans which provide coverage for a list of 20 ailments.

#7. Defined Benefit Plans

Defined Benefit Plans provide fixed compensations against list of surgeries, irrespective of the actual costs incurred. For instance one plan pays a fixed benefit of Rs.1.00 Lakh for Angioplasty, Rs.2 Lakhs for a Bypass Surgery. These plans pay such claims based on minimal photocopied hospitalization papers.

Additionally these plans provide a host of other fixed benefits including fixed amounts per day of hospitalization etc. These plans are different from Critical Illnesses which are based on diagnosis, while these plans are based on actual hospitalization and surgeries.

#8. No Claim Bonus Plans

Given a choice, if you are going for a fresh cover, go for plans which provide No Claim Bonus (Increase of sum insured every year) rather than No Claim Discount (decrease of premium). This helps an assured increase of your coverage every year till you don’t make a claim.

Most good plans provide a bonus of at least 50% of the base cover. Of course, this is not a long term as one claim completely wipes out this bonus at the time of renewal of the policy.

Watch this video to know 9 rules to keep in mind while buying a health insurance:

Top-up Vs. Super Top-up Vs. Upgrade Existing Policy Vs. Buying additional Policy

Most Insurance advisers recommend a top-up plan to increase your health insurance cover. In terms of convenience of purchase and claims, we would recommend upgrade of the same health insurance policy, as the best option. This is ofcourse, provided you are happy with the policy terms and services.

The second best option would be to compare available options of Super Top-up with option of Additional Mediclaim Policy. If the premium is more or less the same, we would recommend additional policy more than a Super Top-up.

After all the above options, look for the option of a simple top-up to increase your cover. Be sure you are aware of the fact, that this option is more useful in the very long term (6-10 years), since it will trigger only when your one claim goes above the threshold/deductible mentioned in the policy.

Other Important points when you plan for upgrading health insurance

1. Upgrade deadline

If you observe around you, lifestyle ailments are spreading like an epidemic across India, thanks to the sedentary lifestyle we live.

You will observe that most of the ailments start cropping up in the late 30’s or early 40’s. If you/your family are in your early 30’s and already have health issues (overweight, underweight, breathlessness, borderline high cholesterol etc.) it is recommended that you go for the highest coverage on mediclaim immediately, rather than get a restricted cover in case you suffer from a chronic ailment in the interim of your plan to increase coverage.

In any case, ensure you upgrade to desired coverage by the time you reach the age of 40 years.

2. Option of stepping up your upgrade plan

If you are in your early 30s, and you cannot afford a one-shot upgrade is too heavy on your current financial budget, create an upgrade plan. Spread the desired upgrade amount across your age upto 40 and upgrade the amount in a manner that you reach the upgraded amount by 40 years. For instance, increase your sum insured every year by say Rs.1 Lakh.

3. Upgrading Features of your plan

Moving to a plan with better features. If you are happy with the sum insured, but not with the features (limitations like room rent limits or co-pays etc. or maybe the network of hospitals) and you are looking at an upgrade, you need to first look at the same insurance company, and check whether they have an advanced plan you are looking for.

In case you like a plan from another Insurance company, you would have to opt for portability with this new Insurance Company 45 days before renewal of your existing policy. Do remember, in the real world (outside the IRDA guidelines) there are limitations on who can get portability, especially if your family is older than 45 years, has a claim history, or a chronic disease.

Go for any options you like above, the bottom line remains – TAKE ACTION. TAKE ACTION NOW. You have too many priorities in your life at home and work, to really be able to remember and act on this even tomorrow.

This article is from Mahavir Chopra of Medimanage. This article first appeared on medimanage blog

One day, a calf needed to cross a forest in order to return to its pasture. No one before this had ever ventured in to the forest. Without any rational, it forged out a long and difficult path full of bends, uneven ground and steep climbs. The next day, a dog took the same path following the calf’s footprints and a flock of sheep followed. As the path started taking some sort of visible shape, men started using the same and gradually, it became a well defined, accepted and the only way to cross the forest.

After many years, the trail became the main road to the village. Everyone complained about the traffic, cursed the long distance and treacherous turns, up and down hills but never thought of a better alternative. The old and wise forest smiled at how men tend to easily accept the way already open, without ever questioning whether it’s really the best choice.

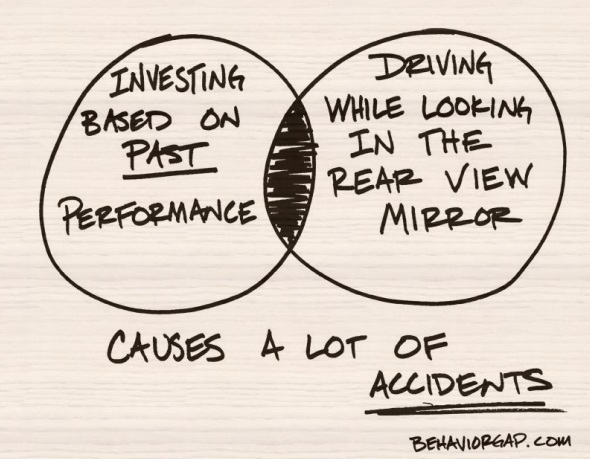

In the same way, if you look at, the mutual funds’ investors. They seem trapped in a similar kind of concept called as – The Past Performance.

Past Performance as selection Criteria

Since quite some time, Past Performance has become a major criterion if not the Holy Grail of the mutual fund selection system. In fact, one of the leading business magazines in association with one of the leading rating agencies went ahead and mentioned “We take into account a much longer period for mutual fund evaluation as that can serve as a serious guide to future performance”… (Their long term means 3 years in this particular case and they used return and risk adjusted numbers for analysis)

Further, rather than challenging the concept, there has been a continuous debate if investors should look at 1-3 year performance or a longer period like 5 years to make mutual fund selections. The treacherous path to the village is already created.

Proponents of the long-history case argue that a long term analysis ensures that the performance is analyzed over various market cycles and if the fund has done well across the long term horizon, it stands a good chance to do so in future.

Sounds logical. Is it really?

I wanted to examine if it really works. For me and for others like me who would like to know the truth and may be many more whose investments have been in red, thanks to these ratings. I gathered historical data of equity mutual fund schemes and worked out the numbers. (3rd chapter of my first book also has same kind of data)

The results were startling !

The core of the finding is “Past performance hardly relates to future returns”… and here we are, pumping our hard earned money into mutual funds, depending on these ratings that rely heavily on the past returns generated.

Analysis Details

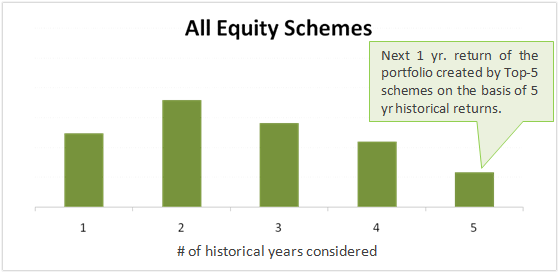

The top 5 schemes by their 1yr, 2 yr, 3yr, 4 yr and 5 yr returns were selected. Thus 5 portfolios consisting of Top 5 schemes were created.

The performance of these 5 portfolios was observed over the next 1 year (e.g. say for Dec-09 analysis, the return for 2010 was observed).

Steps 1 & 2 were repeated every quarter for the past 3 years. The objective was to establish if the relationship with past performance that exists consistently over the period of time.

Findings & Explanation

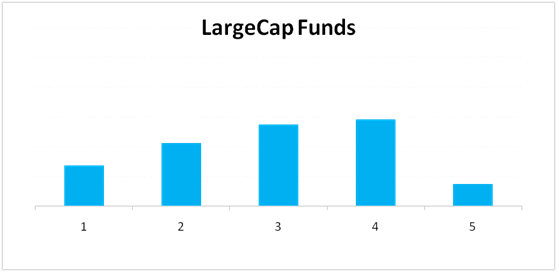

How to read this Chart ?

The graph shows 5 bars, each bar represents the average next 1 year return generated by the portfolio created on the basis of historical returns. The left most bar shows how much average return was generated by portfolio created on the basis of scheme’s past 1 year return; the second bar is the return of the portfolio created by past 2 year return and so on.

So say the analysis is done on Dec-09, the past 1 year refer to 2009 and the returns are calculated for 2010.The above graph shows aggregate returns of the analysis done every quarter.

The graph ‘suggests’ that the ranking by past 2 years is of greatest significance while the ranking by 5 years is least significant. Please note that this is just an observation and not a conclusion. Statistics is a sensitive subject and any data tortured, throws some outputs. It’s important to delve deeper and see if the outputs can be supported with reason and logic.

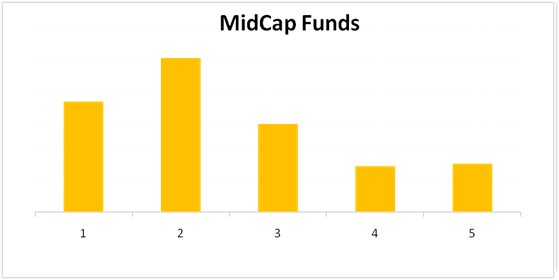

To validate if the inference really holds true and if it can be used for decision making, I dissected the data of all equity schemes into two parts: The Large Cap Schemes and The Mid/Small Cap schemes. The result of analysis conducted over Large and Midcap funds is presented in the charts below.

Take that. While the large cap funds ‘seem-to-be’ driven by their past 4 year returns, the mid caps ‘seem-to-be’ to be driven by their past 2 year returns. I have consciously quoted the word ‘seem-to-be’ as I can’t find a suitable reason to defend even these findings. There aren’t actually. For anything to be considered as a general rule, it should be consistently true. I couldn’t find that when I looked at individual analysis done quarter on quarter.

If I look at each analysis done across quarters, the 2 year return is not the significant driver of future returns always. A considerable number of times the other ones (1, 3, 4, 5 yr returns) gain importance. Just like “past performance” parameter, there are many other mistakes which an investor does in his financial life, and we have decided to talk on some other aspects like those in our upcoming workshop in Mumbai on 10th March. Incase you are in Mumbai, dont miss that event.

Dont use Past Performance to Predict Future

It is quite evident that the past returns cannot be a torch bearer for investment decisions. Following the past returns as a guide or using ratings that rely heavily on past returns is like shooting at a dart board in dark. For any doubts that remain, consider this

Reliance Equity Fund was the top performer in the Large Cap category in 2012, with a return of 41%. Did you know it was the worst performer amongst Large Cap funds by historical return? i.e. if you were in Dec-11 and would have picked up this fund’s historical analysis, it was the worst performer by 1y, 2y, 3y, 4y and 5y return.

Another best performer, SBI Bluechip Fund (2012 return: 38%), never beat more than 33% of its peers ranked by past 1y, 2y, 3y, 4y and 5y return as of Dec-11. Not surprisingly, a leading mutual fund star rating agencies top picks of 2011, underperformed the index in 2012. The agency boasts of using a good mix of longer period historical return and risk adjusted performance.

In my next blog, I shall discuss what can be the reasons of looking at past performance, where did the whole thought possibly evolve and where do things go wrong. The views expressed above are personal and for a change, I own them. All arguments and points welcome. I really value justified facts and accept only my wife’s opinions…!!!

PS: While I finished writing this, there is a news regarding S&P being sued for damages worth USD 5 Billion for misrepresenting the credit worthiness/rating of an issuer due to conflict of interest. (https://on.mktw.net/YRehB0)

Does it sound any bells?

About the Author

Sharad Singh, a serial-entrepreneur, has spent more than 14 years in the analytics domain and has done extensive big data work in finance. He runs Valuefy, an investment portfolio analytics firm that provides portfolio management solutions to BFSI clients. Valuefy has recently launched www.theFundoo.com, a niche portal that aims to make investment decisions easy and effective for individual investors. Sharad is an engineering graduate with PGDM from IIM, Ahmedabad.

Do you use past performance as one of the criteria when you select mutual funds ?

Does False and Misleading Advertisements come under the heading of “Mis-Selling” ? Have you ever saw a financial product advertisement where numbers are tweaked and framed in such a way, that the financial product looks very attractive and not-to-miss deal ?

You see the advertisement and nothing looks wrong to you and you just concentrate on numbers like 15% or 17.45%, as advertised ! . What about mis-selling by big financial institutions who are considered to be too-big-to-fail?

I came across the following advertisement (printed here only partly) in several media including the Company’s website. Even before that, one of our investors, was also flummoxed by the high yield indicated and asked us to explain how it is possible?

Well, a bit of creativity and lot of embellishment seems to have achieved the desired results.

This advertisement in question is about a 5-year deposit from one of the biggest PSU banks in India, which is also eligible for exemption under section 80C of Income tax act. No wonder, tax saving season has just arrived!.

Tax Saving Fixed Deposits, lets you invest a certain amount, on which you will receive tax exemption subject to maximum of Rs.1 Lakh. This would translate to reduction in your tax out go, depending on the tax bracket in which you will fall under – it may be either 10% or 20% or 30% and the cess applicable thereon.

A simple and straightforward situation.

Since it is a bank deposit, it is perceived to be safe. There is an additional layer of safety, because the bank in question may be bracketed under the category of government owned (major share) and it is too-big-to-fail.

What is the problem with this advertisement?

There are so many of these kind of advertisements, enticing you to invest in them because it is the tax planning season. In your interest, if there is little bit of embellishment of the numbers what is wrong with that?

Anyway, you need to be ‘sold’ something, otherwise you will end up paying lot of tax to the same Govt. Instead, just listen to the advertiser and put the moolah where the message belongs to.

At this juncture, let me make it clear the meaning of mis-selling and quote from one of the recent regulations by SEBI Securities Exchange Board of India.

For the purpose of this clause, “mis-selling” means sale of units of a mutual fund scheme by any person, directly or indirectly, by –

a) making a false or misleading statement, or

b) concealing or omitting material facts of the scheme, or

c) concealing the associated risk factors of the scheme, or

d) not taking reasonable care to ensure suitability of the scheme to the buyer.”

If we go by this definition of mis-selling, let us see where does the subject advertisement stands.

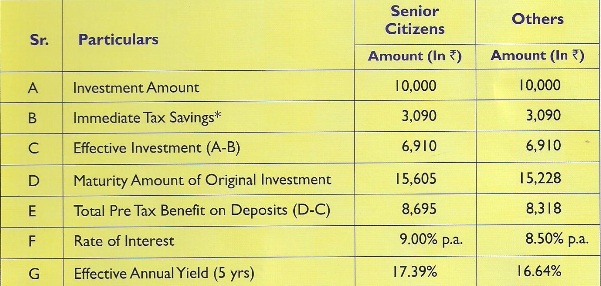

1. The advertisement does seem to make a false or misleading statement. While calculating the effective yield at 16.64% or 17.39%, it does not adjust the effective yield for income tax. Even though it says the return is pre-tax, it just stops there.

Why is it important to adjust the return to taxation? Because to arrive at Effective Annual Yield, it has assumed that the investor falls in the category of 30% marginal tax rate and hence he or she is eligible for “B. Immediate Tax Savings” of Rs.3,090/- which is 30% + 3% Cess thereon on Rs.10,000/- deposit.

When such being the case, how the advertisement can conveniently ignore the taxation on the interest income? Interest on bank deposits is taxable as “Income from other sources” either on cash/receipt basis or on accrual basis depending on the method of accounting followed by the investor.

It is a convenient forgetfulness on the part of the advertiser.

2. The advertisement appears to attempt concealing or omitting material fact such as taxability of interest income earned by the investor. It has also not highlighted the tax deduction at source applicability in case the interest income is beyond a certain threshold.

3. The advertisement (in its full form) also has not highlighted the risk factor of possible default or delay in payment of interest in time and the capital. Since bank deposits need no rating, no one bothers about the underlying risks.

4. The advertisement (in its full form) does not highlight the suitability of the scheme to the buyer. It brings in to its fold all investors under the category “Others”.

Therefore, it fails by all the four counts that are applicable for lesser mortals, such as mutual fund manufacturers and advisers. Of course, you can not apply one regulator’s dictum on others in letter; what about the spirit? Just because RBI is the regulators for bank, should bank not follow what is in interest of investors ?

What about Bank Social responsibility ?

What would be the state of mind of the investor, when she sees such a highly enticing advertisement? In the absence of a super-regulator or dialogue between various regulators, different regulators seem to have different yardsticks about mis-selling or mis-representation. But who cares as long as it is a big govt. owned entity?

It used to be the same case when govt was running a mutual fund business from early 1960s till late 1990s. The mutual fund scheme was also guaranteed by the Govt (remember UTI), was eligible for tax exemption and the fund house was considered to be too-big-to-fail in its time, even though such a coinage was not fashionable in that period.

Finally the mutual fund business did collapse under its own weight and thousands of investors lost their hard earned money. Even though the government stepped in to arrest a free fall, the sheen of guarantee was lost. No lesson seems to have been learned from then to now.

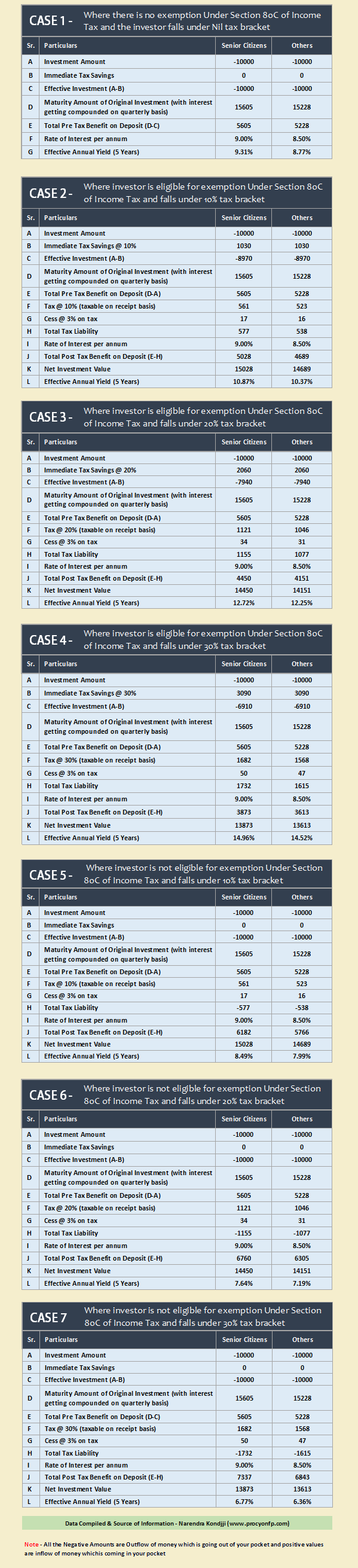

What is the actual situation therefore in the present instance?

Below are the various possible scenarios:

As you can see the effective annual yield in all the above scenarios is nowhere near the one mentioned in the advertisement the moment you take in to account the taxability of the interest income.

How many of the investors who are already in the marginal tax bracket of 30% would have the limit left to invest in this fixed deposit scheme and also would be able to receive tax exempt interest income?

They will be definitely in minority or possibly no one would meet both the conditions at the same time. What can one say about the tactics of highlighting a scenario applicable in minority cases to all investors?

Misleading or partially true advertisements

Why should you as an investor and we as financial planners be worried about such misleading advertisements? Are we not immune to such misleading illustrations by many of the financial products manufacturers already?

In fact recently the Finance Minister of the country mildly chided one type of financial product manufacturer not to mis-sell the products. He attributed the consistent fall in the market share of such a product to the past sales practices.

Herein lies the crux of the problem that investors are floating in a sea of distrust and when very big names keep publishing such misleading or partially true advertisements, the distrust would keep growing and that is not good for the saver or investor and in turn to the economy.

Already some of the insurance products and mutual funds have become the victims of mis-selling, perceived or otherwise. I am really surprised that such a big institution is indulging in a highly embellished communication of doubtful veracity when there is no need for such gimmicks. I am also worried because I and my family have our banking relationship with this too-big-to-fail entity.

About the Author – The article is written by Narendra N Kondajji, A bangalore based CERTIFIED FINANCIAL PLANNERCM (CFP) . His website is www.procyonfp.com and this article was originally appeared on his blog here

Do you know which is the best credit card in India in terms of rewards points which you can redeem at different categories ? Have you ever wondered how different or close these credit card reward points are ? Let me take an example!

Ever thought the difference between how does 5X rewards from Standard Chartered differ from 10X rewards from Amex, ever wondered whether taking a 5% cash back is better than going for 10X rewards. Ever thought how can you save in excess of 16K per annum only by having a few cards in your wallet, well continue reading.

Every credit card company offers rewards in the form of Cashback / Reward Points to its customers. These rewards are funded by what is called as interchange. Interchange is transaction fees charged by the bank from the merchant. Its usually 2 – 3 % of every transaction. This is the reason, why some merchants ask an excess 2% if you tell them you would be swiping your card instead of paying them in cash (Read some must know points about your credit card). Cash is the preferred mode for another reason and that is to save taxes, as every credit card transaction goes into the books of the merchant, but that’s a separate discussion and we’ll leave it to some other day.

A few disclaimers before I proceed. This article is about rewards points and how you can save maximum through credit cards. “A rupee earned is a rupee that earned 6 percent” – So lets save some money for all of you. Again the entire article has been based on my experience and research, so am open to suggestions and feedback. Also I haven’t included Airlines spend, as I still don’t fully understand the Points to Miles conversion for different Airlines.

Following are some of the points that I hope the readers will have a much better understanding of, by the end of the article.

Comparing Credit cards by their rewards proposition – If you have multiple credit cards, how to figure which one has a better reward structure?

Accelerated Rewards: Most of the credit cards have an accelerated reward structure. So how should that impact your spending pattern so as to maximize the rewards?

Wallet of Credit cards that one should own – Using the methodology explained above, this would be a list of credit cards that will help maximize your savings.

Credit Card Reward Points & Cash Back Benefits

Lets start of with , How should one go about comparing credit cards by their rewards proposition. To understand this, there are two important concepts that one should be aware of

Earn Rate: Earn Rate is number of points earned per amount spent.

Burn Rate: Burn Rate is the Rupee value of a reward point.

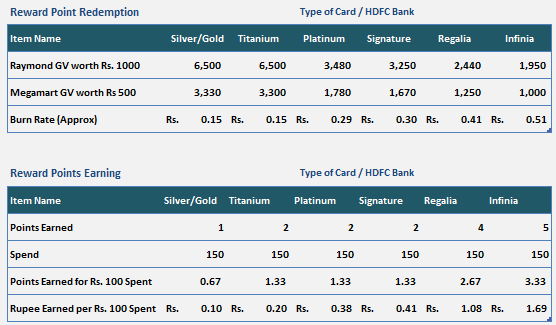

For Example – For a HDFC Silver/Gold card, you earn 1 reward point for Rs. 150 spent, so the earn rate is 1/150. Whereas each credit card reward point of a silver/gold card is worth 15 paise or Rs 0.15 only. So the burn rate is 15 Paise.You multiply the two and you will get a metric which you can use to compare credit cards from different companies.

Using the Burn Rate and the Earn Rate, I have come out with a very simple metric “Rupee earned per every Rs. 100 Spent” , which can be used to compare some of the top credit cards in the market.

Rupee earned per every Rs. 100 spent = Earn Rate (Calculated on Rs. 100 Spent) * Burn Rate

Also the comparisons below are based on the basic earnings. Most of the cards have an accelerated reward-earning proposition. We shall factor that when we calculate the monthly earnings from different spend scenarios. Also will show you how to create your own savings through your own spend numbers.

Example – 1

I will give you an example of how this metric would be useful to differentiate between two cards of the same bank or different cards across the bank.

The above tables give us an idea of hdfc credit card reward points benefits in the market. If you look at the value proposition of different cards, they are vastly different in terms of Rupee Earned per Rs. 100 spent. Rs.100 spent on a HDFC silver/gold card will give you Rs. 0.10 whereas spending the same amount on Regalia will give you a Rs. 1.08 in terms of reward points. But again Regalia and Infinia are fee based cards and hence one needs to factor this in when computing the relative reward proposition of the card.

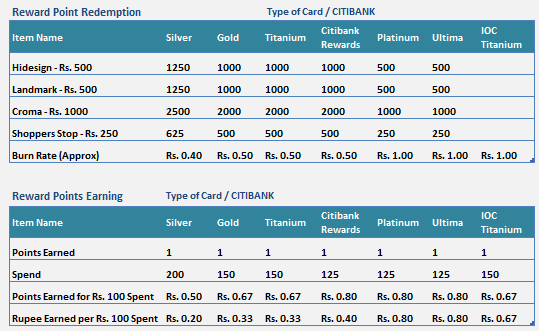

Example – 2

Now lets compare HDFC reward points with CITIBANK rewards points

If we compare the same metric Rupee Earned per Rs. 100 spent, Platinum and Ultima cards are decent options and in the premium segment HDFC provides better rewards.

Accelerated Rewards – Categories of Spend and Best card in each category

Apart from the basic reward proposition that’s present with every credit card, most of the cards in the market offer an accelerated rewards earning proposition. These accelerated rewards can be in a variety of forms. E.g. 5x rewards on Departmental Stores, 10X rewards on Online spends or a 5% cashback on Departmental Stores.

Now lets use the concept above and factor in the accelerated rewards propositions, (That some of these cards offer) to get to the best cards in each of the spend categories. The formula to calculate the rewards is a simple one: Just multiply the basic rewards earned above by the accelerated reward earning multiple.

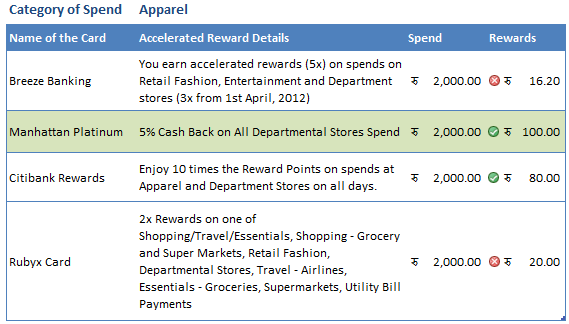

Example – Rewards earned if you have spent Rs. 2000 on Citibank Rewards card.

For Citibank Rewards, Rupee Earned per Rs. 100 spent = Rs. 0.4

Accelerated Reward Earning : 10X on Departmental Stores

Rewards Earned = 10*0.4*2000/100 = Rs. 80

A few disclaimers here:

A few credit card companies even though offer accelerated rewards proposition but offer it only on select merchants. For e.g. Amex offer 10X rewards on its partner merchants, CITI rewards card offers it on select merchants, etc.. If you do not shop on these merchants then you won’t be earning any accelerated rewards. That’s the reason I prefer credit cards which offer a flat accelerated rewards structure so that I get the freedom of shopping wherever I want to

Also some of these accelerated rewards have a validity, which means have an expiry date. You are eligible for accelerated rewards only in that period.

Also I have a preference for Cash back as compared to reward accumulation, reason being two fold. First: Cashback impact my outflows directly as compared to rewards (where one has to go through the process of reward redemption and its benefits). Second: Its faster.

Keeping the above in mind, lets factor in the accelerated rewards to the basic rewards proposition of credit cards and figure out which card will give you the maximum advantage. Also the following will give you a chance to rate your card with respect to the cards available in the market.

The data has been collected from the sites and catalogues of different credit card companies. Since the accelerated rewards are mostly provided in specific categories, so we shall consider each category separately and figure the best card in that category.

Winner – Manhattan Platinum Card

Even though it seems, owning a Citibank Rewards card will give you, Rs. 80 cash back, but that’s just superficial because the 5X rewards on Citibank card is limited to only a few stores. Lifestyle being the major one of them.For Manhattan Platinum card, even though the offer tells only about Departmental stores, it covers all kinds of retail spends. Spends in malls are covered by this offer

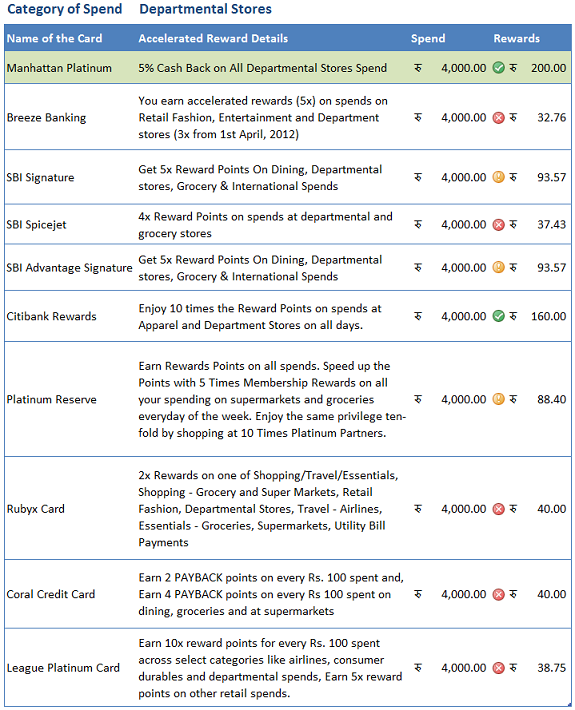

Winner – Manhattan Platinum

Again it’s a straight fight between Manhattan Platinum and Citibank Rewards. And Manhattan Platinum wins hands down.

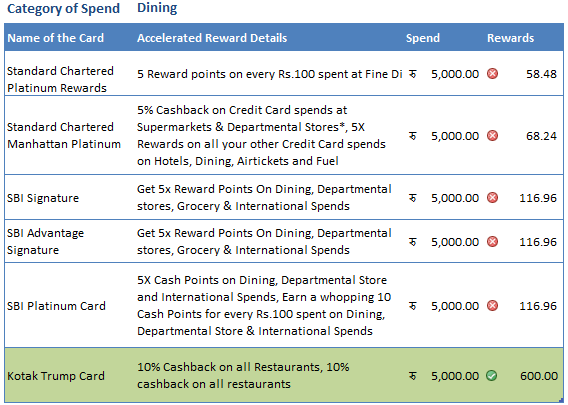

Winner – Kotak Trump Card

Clearly Kotak Trump card is the clear winner. With you saving almost Rs. 600 per month if you are a heavy diner. There are a few finer points, that the total spends on Movies and Restaurants should be more than Rs. 4000. There are a few other cards, where the card issuing companies have a tie up with specific restaurants in different cities. Citibank being one of them where they have tied up with more than 200 merchants across India and offer a 20 % discount flat.

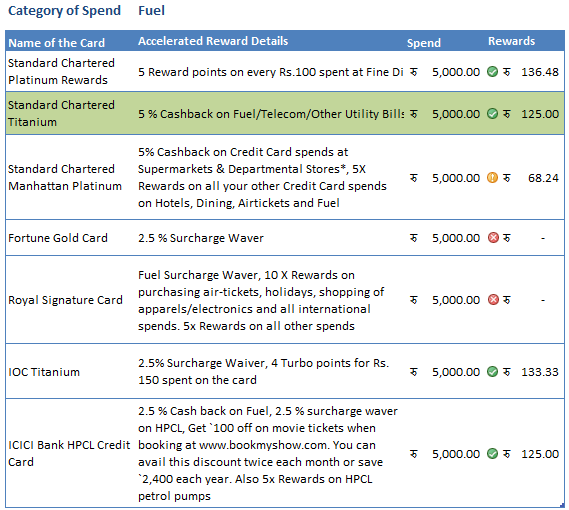

Winner – Standard Chartered Titanium

Standard Chartered Platinum Rewards, Standard Chartered Titanium, IOC Titanium and ICICI Bank HPCL card are quite close in terms of the monthly earnings. But I like cashback more than earnings through reward points. Also the 5% flat cashback on any petrol pump as compared to IOC and HPCL for Citibank and ICICI bank cards respectively make Standard Chartered Card a winner in this category.

Winner – Standard Chartered Titanium

Standard Chartered Platinum Rewards, Standard Chartered Titanium, IOC Titanium and ICICI Bank HPCL card are quite close in terms of the monthly earnings. But I like cashback more than earnings through reward points. Also the 5% flat cashback on any petrol pump as compared to IOC and HPCL for Citibank and ICICI bank cards respectively make Standard Chartered Card a winner in this category.

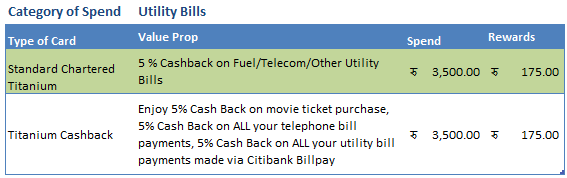

Winner – Standard Chartered Titanium Card

Again , both the cards are equally good, but the additional condition of paying your bills via Citibank billpay turns my preference towards Standard Chartered Titanium card.

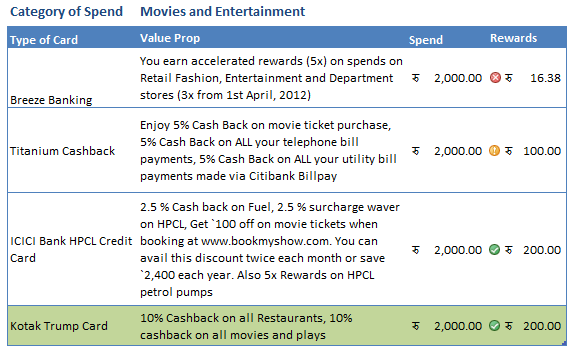

Carrying a similar analysis on categories of Movies and Entertainment and Utility Bills reveals that Kotak Trump card and Standard Chartered Titanium card emerge as the top card in the respective categories.

Wallet of Credit cards that one should own

Having done the hard bit of analysis, calculations and comparisons we come to the easier bit of creating a wallet of credit cards for you which will accelerate the reward earning and help you save a substantial amount over a period of time. To give you all an idea about savings that can be done by having this wallet, I have created a few scenarios and the respective savings. One can create his/her own spend/rewards scenarios using the table below.

Category of Spend

Name of the Card

Value Proposition

Monthly Spend

Monthly Savings

Annual Savings

Apparel

Standard Chartered – Manhattan Platinum

5% Cash Back on All Departmental Stores Spend, (This includes all kinds of Retail Spends)

2,000

100

1,200

Departmental Stores

Standard Chartered – Manhattan Platinum

5% Cash Back on All Departmental Stores Spend, (This includes all kinds of Retail Spends)

4,000

200

2,400

Dining

Kotak Trump Card

10% Cashback on all Restaurants, 10% cashback on all restaurants

5,000

600

7,200

Fuel

Standard Chartered – Titanium Card

5 % Cashback on Fuel/Telecom/Other Utility Bills

5,000

125

1,500

Movies and Entertainment

Kotak Trump Card

10% Cashback on all Restaurants, 10% cashback on all restaurants

2,000

200

2,400

Utility Bills

Standard Chartered – Titanium Card

5 % Cashback on Telecom/Other Utility Bills

3,500

175

2,100

21,500

1,400

16,800

This is a guest post by Gaurav Thakur, who is currently working as an analyst with a mutual fund company. An IIT Kanpur alumnus, he has primarily worked in the financial services industry, working with Citibank India Credit cards for a couple of years and also spending time in Citibank’s personal loans division.” This article has appeared first on gaurav blog here.

Which credit card you have already and are you satisfied with your credit card reward points and cash back benefits ? Did you get any insights from this article on credit card rewards points ?

DSP Blackrock Mutual Funds have started a Women Financial Literacy called – Sheconomy , which is a TV initiative under their Winvestor program in association with CNBC TV 18. The aim of the initiative is to guide independent women to adopt wealth creation strategies by answering their queries on personal finance and helps them become informed investors.

The show launched on 12th Jan 2013 with a panel discussion featuring a prominent matrimonial lawyer and a female psychologist who passionately believe that women must take care of their own finances. This is followed by seven episodes with various clusters of women such as homemakers, women entrepreneurs, working women, young mothers, senior citizens, fresh graduates and even a special episode with men and women talking to our Winvisors who answer queries and provide investment advice. The last episode would also be a panel discussion with some prominent women who passionately believe in the idea, share their views and experiences and talk about why they feel women need to be in charge of their own financial future.

The show airs every Saturday at 6 pm and is repeated at 4 pm on Sunday on CNBC TV 18. All the women investors should watch these shows if they want to learn more about personal finance and managing money. We feel women investors can greatly inspire other women investors. Three episodes are already aired, if you have missed them, you can watch them below .

Below are the names and schedule of all the 7 episodes of the Sheconomy initiative.

Episode Structure

Name of Show

Show Timings

Importance

Homemakers

19th Jan’13, Saturday at 6 p.m.

A homemaker plays an equally important role in her husband’s financial success as well as her own. Though this cluster of women don’t typically take up jobs, investing the money their husbands allocate to them for personal expenditure could prove to be of great help in time of need.

Women Entrepreneurs

26th Jan’13, Saturday at 6 p.m

Apart from all the investments which other women do, this cluster of women has another investment priority in their life ‘Their business’. It becomes imperative for them to invest in instruments that is not only safe but also provide the quickest returns so that money earned could be deployed into their business from time to time. Investments needs of women belonging to this cluster tend to be more dynamic than the rest

Working Women (Unmarried/ married)

2nd Feb’13, Saturday at 6 p.m.

Women in this cluster have the highest disposable income and the least responsibilities hence providing ample scope and capital for planning investments. The married women of today has come of age from being the typical housewife, in fact getting married is the beginning of various responsibilities that a woman needs to share with her better half at all times- Planning a baby, Bigger house, Better lifestyle, Retirement plan, monthly family budgeting, aging in laws and parents. There is an entire menu to choose from.

Young Mothers

9th Feb’13, Saturday at 6 p.m.

Mothering calls for the best in women. With this emotion in mind a lot of young mothers have various aspirations for their kids; these aspirations come at price which one needs to be prepared for well in advance. A good investment made from the beginning can help young mothers to provide their children the best and fulfill all their dreams, even if you are a single parent.

Senior Citizens

16th Feb’13, Saturday at 6 p.m

The life expectancy of women is higher than men So, the amount of retirement savings for women should also be higher. Statistics show that, on an average, women live 5 years longer than men, earn 25 percent less during their life time and work 11 years less in their careers and not many women are even aware enough of all of this. All these factors put together make this cluster of women extremely important to address when it comes to financial planning.

On ground forum with Men

Date yet to be finalized

A forum with the modern man on why he should encourage and empower the women in his life to take their own financial decisions. An educative forum for men that will teach them the upsides of their women being financial independent.

Fresh College graduates/ post graduates

Date yet to be finalized

Catch them young and make them grow a quote completely apt for youngsters who are about to plunge into their first corporate job. The need to understand basic money management skills such as living within a budget and handling credit and debt can lead to a solid financial foundation that in turn can lead to a lifetime of financial success.

What do you feel about these kind of initiatives ? We have also done a women centric 2 video series for our wealth members, incase you are already a member you can watch the series here .