“Investors will not have to pay an entry load for investing in mutual fund schemes anymore. They will instead pay a commission to their distributor or advisor directly and the quantum of the upfront commission would be mutually agreed upon.”

More Competition and hence little cheaper for Investors

Now agents will not be getting commissions from Mutual Funds companies which means that now there is direct competition among Agents. The agents can only ask for more if he really gives good service to buyers else they have to settle with a low commission which will be decided by customers.

This means now we can bargain with the agent on commission percentage and if he is not ready with what we offer him/her. We can look for someone else who is better and fits us.

Higher Quality of Service and more transparency in Market

Now agents will have to deliver much better quality of service and be more transparent with investors as their bread and butter is directly linked with Investors and not with the Mutual Fund Companies.

Lots of agents will now move to sell ULIPS rather than Mutual Funds

This move will also force lots of mutual funds agents to shift their focus on ULIPS and similar products which have commission linked with premium paid by customers rather than fee based model like we now have in case of mutual funds. This means more miss-selling in ULIPS is on the cards.

See the following New Video To understand

Update: thanks to income.portfolio for this.

AMC’s are allowed to use 1% of redemption in mutual funds for commission to agents and all the marketing costs. Its the money from exit loads which has to be utilized in commissions and other marketing costs. Most of the mutual funds have less than 0.5% of 1% of exit loads at this point and with this rule of SEBI, it can not go above 1% in future. Also it can be “up to 1%”. So this 1% will be used for every type of cost incurred by mutual funds.

Now most of the funds will have exit loads only if investor gets out in short term like 6 months or 1 yrs. Hopefully it will not be after 1 yr. So its a concern for those who are short term investors. Its not a matter of concern for long term investors as far as I think.

Also, now there is no need for PAN Card for investing in mutual funds up to Rs 50,000 through SIP as per SEBI new rules.

I am out for a 2 day weekend Trek to Kumaraparvata. So no article till Monday morning. I will post the 2nd article of “How a newcomer should start in Stock Markets?” Read Part 1 Here .

This is going to be important and useful series of article. Today we will discuss how a new-comer to stock market should start. In these series of articles we will discuss following things.

Why stock markets attract and look easy

Understanding what you want to do exactly

What are important things when you are in stock market

How a new comer should start in stock markets

Why Stock Markets attracts?

You must have heard lots of stories about people who became millionaire over night or in a short span of time from stock markets trading.

There are two kinds of people who make money from stock markets:

# First kind, are the people who make money because of luck. They buy some thing, it goes up and they think it was their skill that made the profit. Next time they buy something again and wooo!!! It makes money again and now they are the king!!

Then comes one day when their “best time in the market” is over and they start loosing money and this time its “bad luck in market” as they say!! They keep on trying to prove that they are knowledgeable and have mastered the skill to understand how markets operate.

At last they go bust and return from where they started. Smart people in this category are those who make money once or twice because of luck and don’t come back. I appreciate their smartness.

# Second kind of people are those who are real game players, They have done their homework, failed lot of times, learned from their mistakes and worked hard to make money. They know the rules of stock markets and take it seriously.

They are successful traders or investors.

People hear that lots of people make lots of money in short span of time from stock market and how easy it is to just open your trading account then choose some stock, later on buy or sell and magic happens! You make money. This is Far from truth!!

This thinking that “Lots of money can be easily made from stock market without much hard work” is the main reason why stock markets attract lots of people.

Why it looks easy?

“BUY OR SELL”, that’s all you have to decide? Either you will Buy something or you have to sell something. One of the renowned trader Larry Williams says this is the reason why most of the people think that its an easy thing to make money in stock market because they have very less decisions to make i.e. BUY or SELL

This is a human psychology which tends to believe that anything with less decisions is easy and one can do it. Everyone thinks “I am different”, “I know all these people where not able to make money, but I can understand things better and I can do it in a different way”!

This thinking is appreciated but, until it becomes over confidence. It’s true that you are different and you can do it but each and every area has some ground rules and unless you follow it thoroughly it’s almost impossible for you to succeed.

What you must understand?

You have to understand that you are a newbie and a small player! A new born baby ,who cant even crawl in the world of stock markets, but dreams of running a marathon and that too on one leg 😉 . Each profession needs specialization and experience and Making money from stock markets is no different.

Just like becoming a Doctor, Engineer or anything like that demands extreme study, experience, knowledge and other things specific to that profession, stock market demands all of that. The people who want to make money without doing it can not sustain for long and will hurt themselves very very badly.

We will discuss more of this in 4th part of this article “How a new comer should start in stock markets?”.

In this post, we will discuss on why do you require a Financial Planner to do your financial planning? Each and every area has an expert who understand and has skills for that profession whether it be Doctors, Engineers, Lawyers etc!

Likewise, we have Financial Planners. Now, don’t confuse financial planners with Mutual Funds Agents or Insurance advisers! NO!

Let us see some Important Points on why we need a Financial Planner.

They see your Financial situation as a whole and not just specific Parts:

One of the major issues with our country is, here each area is seen separately and not as a whole. An Insurance Adviser will randomly suggest you a policy without understanding what is your Insurance Requirement.

All that they will say is that your Insurance requirement is 8-10 times of your annual income, which is not the right way of calculating the actual Requirement. Mutual Funds advisers will just pick some Mutual fund for you without understanding your Risk-Appetite and your Future Goals.

They don’t take care of your Tax planning, Estate Planning (wills and Legal Documents) or your Cash Flow etc etc.

A Financial Planner on the contrary acts as a Doctor to your Personal Finance, who will very closely study each aspect of your Financial Life.

He will understand your Risk Appetite, your current outstanding liabilities, your Future Goals, your Future Needs and Requirements, your Insurance Requirement, your Investment needs and finally come up with a Financial Plan and Recommendations which will take care of each aspects in total.

Financial Planner will Educate you:

Financial Planners will make you logical reasoning behind every suggestion he makes. He will make sure that you agree and understand everything, so that in future you can take similar decisions yourself.

Has any Mutual funds adviser told you why SIP is better for you? Or Why You should expect great returns in long term from Equity?

Financial Planner wants to make your Financial Life Better:

Financial Planner’s goal is not limited to Insurance planning or Investment Planning. In fact a Financial Planner is trying to make your overall Financial Life better and paves a smooth financial path for you, which you can start walking on.

Your overall Financial life is made up of different components Insurance Planning, Investment and Retirement planning, Estate Planning, Tax Planning etc etc. He will take care of all these aspects.

Financial Planners are Certified or they under Certification and have deep knowledge:

How many agents or any kind of Adviser you have seen is competent enough to advise you? What is their relevant experience in that field? Most of them are just under their respective company’s Training.

A Financial Planner should be a CFP or undergoing CFP qualification. CFP is the highest level of certification all over the world in the field of Financial Planning. You can also look for people who have deep understanding of Financial Planning and are undergoing the course.

As CFP is new in India, there are many students who are under the learning process and are very good Financial Advisers (You can count me one if you like).

They have good network base:

Good Financial planners will have excellent network of Agents and Other professionals who can be helpful to you in the best possible way. Like for example, if he recommends you to go for a Term Insurance, he may also recommend you some company’s Term Plan and may recommend you to some good and trusted Agents.

This will again be an important thing which you should consider. A Financial Planner may or may not have share in the Commissions.

Watch this video to know the importance of financial adviser:

What is the general Process Financial Planners Follow?

The first step they will follow is to get out each and every strand of information out of you that will help them to understand your situation correctly and in depth. They will try to capture each aspect of your Financial Life through a Questionnaire.

It’s like a Doctor trying to get every information about you to give you a prescription. Then they will analyse each aspect and come out with the Plan and recommendations.

They will not simply come to you and recommend you some mutual fund or insurance policy understanding if you need it or not. Infact they will do your Financial planning in the same way as you would have done yours if you were a Financial planner 🙂 .

They can also assist you in future in monitoring your Financial plan depending on your agreement with the financial planner. Just like you have your dedicated Family Doctor, see him as your Family Financial Planner.

I have enough knowledge about Products and Financial Planning, I constantly Read Financial Magazines and Blogs and keep updating my knowledge. Why should I hire a Financial Planner in that case?

Great!! If you are doing this, it’s much appreciated. You have to understand that

Financial planners are dedicated Professionals in the field. They have undergone tough training and may have much better detailed understanding of the nitty-grittes of Financial Planning which you may lack.

You may have good knowledge and understanding and you may your self take care of your Financial life to great extent. It’s you who have to answer how your Financial Life must be, “Not Bad” or “Excellent” & “Perfect”!

Also it may happen that its your un-true understanding that your understanding is very good. You may have good understanding in one field, but what about other fields?

A financial planner may also have good competence in understanding of Financial markets, Derivatives Markets, Law governing tax etc and these keep on changing and one needs to be updated with the information.

However if you have great interest in Personal Finance and already have great understanding and knowledge, you can enroll for CFP and start a new Career! Dont forget to keep in touch with me!! 🙂

What about the Cost?

Everything comes with the cost. Definitely and if you need Quality then you need to pay quality cost for it as well. But don’t be horrified by the fees you pay to Financial planners, you have to understand the difference between Price and Value.

Just seeing the numbers may make you feel over-charged, but when you concentrate on the value it adds to your life, you will be amazed. If you pay Rs X as fees to Financial Planners you will save many times of that because of the alterations and changes he has brought into your financial life.

Its like if you fall sick then you pay for medicines. No questions asked!! Either pay and save yourself and be happy OR just live in hope of it getting cured by itself, but it will actually get worse and one day kill you.

But my Financial life looks great to me, I don’t see any issues, my insurance cover is fine, my Investments are great…?

Baby, you don’t know a lot of things in that case… Life is waiting for you. There are many people who think they are totally fine and at last they are diagnosed by Cancer and most of the times its at the last stage, don’t wait so long get it checked now!!

My Family and Friends are forcing me to see a Financial Planner? what should I do?

No! You should only see a Financial Planner when you yourself realize that you need one. This is an issue with our country, most of the people do not know and do not realize that their Finances Stink!! Only when it goes out of control they will realise that time has come and by then its too late.

What is stopping you to at least get your financial checkup done by a Financial planner? He will make you realize first that you need it badly and once you agree you can hire him to fix it.

Conclusion

Majority of Indians are totally clueless about Financial planning and only it has happened that in recent years some awareness has been created about it. Most of us try to fix finances on our own without accepting that we are not competent enough to do it all!

WE need a professional. Don’t you pay to Doctor or Lawyer or any other Professional then why not hire a Financial Planner? Go for it!! Jago Investor!!

Note: For people who need my Financial Planning services can mail me

What do we do when we face some issue with Banks, Mutual Funds, Credit Card company, Insurance Company and so on?

The first thing we do is to file a complain with them for our problems and then we wait for their answer. What if we are not satisfied with there reply and want more justice.

We can then lodge a complain with their regulators Ombudsman and grievance cells. Let us see this in more detail.

What is Ombudsman?

The ombudsman is the internal complaint department for socially responsible organizations (governments, companies, societies, etc.). The ombudsman has complete access to the organization’s records and personnel, and the knowledge to understand how things work internally, in order to investigate complaints made against the organization.

So we have Bank Ombudsman, Insurance Company Ombudsman and Mutual funds companies Ombudsman etc.

When should you Approach Ombudsman ?

The first thing you should be doing is to contact your Bank/Mutual Fund Office/ Insurance Company and file a complaint with them. If you do not receive any response within some specified limit of days, you should further your complaint with the Ombudsman.

What If Ombudsman do not reply or take Action?

All the Ombudsman bodies comes under the purview of Right to Information Act (RTI act of 1995). They are legally bound to reply for any complaints made by them ,considering its as per the stated rules.

Note : Ombudsman are the next level of bodies to complain , first try to resolve matter personally with the Bank or Insurance company which is creating problem for you.

Let me tell you a small story which will help you to understand the power of compounding easily.

There once was a king whose daughter was very ill. The king announced to his people that whoever cured his daughter can marry the princess and ask for another reward. One young man came and cured the princess with his family owned secret remedy.

The king was so happy that he anxiously asked the young man what else he wanted besides marrying the princess as his 2nd wish. The young man pointed to a chess board with 64 squares on it and asked the king to put one grain of rice in the first cube and two in the second, four in the third, and eight in the fourth, and so on until the 64th square is filled up.

The king laughed and confirmed his wish that he really wanted rice grains and not GOLD!! The King did not realize what he agreed to at that particular time.

By the time they reach 32nd cube all the rice reserves of his Kingdom were exhausted! It was staggering 214 Crores grains of rice itself.. Each of the subsequent cubes required the King to double up the number of grains. King had to ask other Kingdoms for Grains and till he reached 45th cube the Rice Grain Reserves of all the kingdoms finished…

Eventually the king had to handover his entire kingdom to this clever person. That’s Power of Compounding!!

At first it may look small , but with patience and discipline in investing a sizable corpus can be built over long time. The secret of building huge corpus is to “Start” and “Keep doing it”.

In this post we will discuss why one should really be cautious about NFOs and why in general its better not to invest in any NFO. Have you heard about NFOs and IPOs hitting the markets while markets are doing bad? Why is it so? this is a question we must answer to.

The reason why most of the NFOs and IPOs hit the markets when markets are doing extremely good is to exploit the emotional buying of investors. Its a common thing that investors tend to get in rising markets then falling markets.

So when markets are flying high and all kinds of NFOs with fancy names (some good funds and some junk funds) will hit the market claiming how different they are and how they are ought to be a huge success.

Every NFO will come with its own idea and logic, but investing is never easy and you can see true colors only after few years. They can be success or failure!

So why to go for something which can either fail or succeed, instead why not go for some existing fund which already has proven its mettle, which has given superb returns over long term and has excellent management. These funds have high probability to continue their performance.

Its like: what would you prefer? Take risk of marrying someone you don’t know or someone who is already a good friend and you know him/her over years?

Cheap NAV at Rs 10:

Most NFO offer comes with NAV of Rs 10 and the biggest myth of investors is that its a cheap fund and hence better than a fund with NAV of 20 or 100. NAV growth is nothing but growth of investments and it does not matter what NAV rate is! Rs 10 NAV mutual funds and Rs 100 NAV mutual fund will grow with same rate if their investment quality is the same. There is no reason to invest in a fund that has low NAV.

Myth of High Dividend from Low NAV Fund:

Majority of our “Educated” Agents will tell you that buying low NAV fund will help you in getting more Dividend (if you choose Dividend option) because Dividend is declared on number of Units held. So you will get more units of mutual funds if you invest in low NAV funds!

Whatever he says is true, but he himself does not know that it’s the investor’s money coming back to him and NAV value will again go down by that much value. So in real money terms, there is no benefit of dividend option. See difference between growth and Dividend options

Agents will market it very well and try to push the NFO’s for Sale:

Everyone wants to make money! What other product can be better for a mutual funds agent than an NFO!!! Agents get High commission on selling NFOs and hence they will do anything to sell it. They will spend money aggressively for Marketing as its taken back from Investors eventually and not the AMC. Caution, Be-aware!

Does that mean all NFO’s are Bad?

No! Every existing mutual funds was NFO once upon a time. You should go through the NFO Offer prospectus to find out whether the offer seems interesting and logical enough for you to invest in it. Only then you can go for it. But just understand that only a handful of all NFO’s become good funds.

So out of 1000 mutual funds only a few like 20-30 will be extremely outstanding funds. So the decision is yours! Do you want to take the chance? Or you want to wait and let it show its true colors before you get into it.

Which is the new hot NFO in the Market?

Reliance Infrastructure Fund is the new name in the market these days. All the things which I talked above applied to this too. Before Investing in it read about it in acute detail. I will provide my short view on this.

Reliance Infrastructure Fund is a Sectoral Fund (Infrastructure). This sector looks attractive over next few years. The picture would be more clear after the Budget is out because that’s when we exactly know what is Govt plan in this particular sector.

If its a bad news then the stocks in these sector will take a hit and suddenly it can become a reason for suicide for its investors. Why not wait till the budget and then 😉

Conclusion: Investing in NFOs can be like shooting in dark for retail investors! A better idea for them is to invest in something which has more probability of performing well. NFOs can be extremely successful because of their unique idea or investing style but its too tough to choose them successfully. Better to avoid them!

Before anyone asks, I must tell that its taken by a normal point and shoot camera 🙂 Its just a result of Interest and Willingness to take some good pic + Macro Mode 🙂

Investments are similar to small plants; they need time to grow and flourish. Most of the investors make a common mistake of not giving enough time to their investments to grow and take a good shape.

If you think about how you plant a sapling and manage it well for years so that it can become a fully grown tree so give you the fruits, the process of investing through shares and mutual funds is the same way.

Lets take each case and see the similarities between these two concepts.

Growing Tree

You take a small plant (or a sapling), put it in soil and then water it, monitor it, take the weeds out, clean the plant and take care of it from pests which might be destroying your plant. It takes patience for the plant to grow and become a full grown tree. Then it servers you with the fruits which you deserve for your hard work and patience.

Imagine a different scenario: Now, you pick up a plant and put it in soil, 10 days later you go to see it expecting that you will get some fruits out of it. Obviously, you will be disappointed! It can’t give you any fruit and you think that either something is wrong with the plant or the soil is not the right type.

You take the plant out and put another plant, again 10 days later you come to see the plant, nothing happens. You take it out and put another and another and another and then you realize its not working. Now you think that the culprit is the type of soil, you take the same plant out of the soil and put it at another place which you think has better soil. But nothing happens there too!

Because your concentration and focus is on wrong things. It will definitely not grow if you don’t give it enough time to settle. It’s roots need to get hold of the soil, adapt to the conditions.

There will be different cycles of weather which will challenge and threaten the plant growth and you will have to take care of those scenarios. But one thing is sure that you have to give enough time to it.

Making Investments

When you invest in a share for Long term, the biggest mistake you tend to do is not give enough time for it to grow! If it does not move up quickly or as per your expectation, then you tend to think that you have picked a wrong share. You redeem your investment and again invest money in some other “better looking” share.

This keeps on happening, the prices of the share moves up, then down and it is never ending cycle. The volatile movements in share price gives sleepless nights to the investor and makes them believe that their investment might go in loss and hence its a good idea to liquidate it and finally shareholder sells it and takes the money out; Then again buys some other share.

This buying and selling goes on and on and one! The investor never gives one share enough time to grow. I am not saying that buying any arbitrary share and keeping it for long term will make you profits.

Picking good fundamentally strong stocks is a separate topic in itself. Here we are discussing about the scenario where assuming the investor has put his money in good stock but he just needs to give enough time to let it grow.

Later if the investor looks back and analyses his previously picked stocks, he will find that most of them have gone up or has crossed more than his expected levels. He then realizes that the only thing he missed was to give enough time for his investments and sit back tight without doing anything.

CASE STUDY

Imagine a person who invested Rs 10,000 in Wipro in year 1999 . What do you think the stock prices were in next 3 months or 6 months. What if the investor had sold the shares within a year because of a small loss or some good profit. In 1 or 3 yrs he might have got excellent returns ,which is fine. But the best returns comes when you give an excellent stock enough time. What do you think the stock was worth for in 28-29 yrs.

Rs 10,000 invested in 1979 was worth 200 Crores in next 28-29 yrs. The pick was good, no doubt! but it was the patience that got rewarded in the end.

What is it that makes it difficult for investors to keep patience with there investments?

Right from our birth, we are taught that life is ALL about winning, getting right and not making mistakes, being perfect. This has got inside our brains and its just not acceptable for us to be wrong, we want to achieve success, and be right.

When you invest in a share and it goes up in price, the first thing which comes to every mind is, “I should book it now and take the profit, else it can again go down and I may go in loss”. Actually in our mind we are saying “I should be out of this investment so that I can show others that I made a winning investment, or else I will make a loss and hence be called a loser”.

Have you faced this situation?

When you buy something at Rs 100 and it goes to Rs 99. Its so difficult to sell the share at Rs 1 Loss (that’s 1%). You just want it to come to Rs 100 back and then sell so that you are a winner and not a loser. But you only find it dropping further to Rs 90 and then Rs 80 and so on .. you are just helpless about the whole scenario.

Investments and Trading is not about Winning, its about making money and losing a little in case you are losing. Stop thinking in terms of Winning and Losing!!!

Think in terms of Keeping your losses at minimum and once you are in profits, let it run till you find a reason to sell the share. Selling a share just because its in profit is not a wise thing to do! You can make some profits out of it, but wealth is created by letting your profits run and run for a long enough time.

Note : This article from me was also appeared on Valuenotes.com .

Let us see some analysis of current market conditions. Most of the people are rushing to buy now for long term . but this may not be a market to buy for long term. I am myself Bullish now, but for short term not long term.

I would not be surprised to see markets rise by over 10-15% more over next 1-2 months till the Budget but sooner or later I expect.

– A nice correction if this is another bull market

– Bull rally coming to an end in the strong bear market

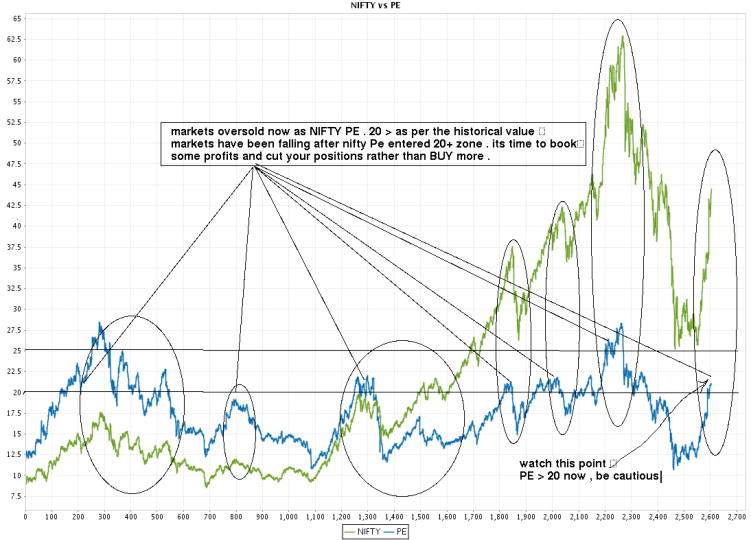

Historically Nifty has been considered and shown instances of being oversold in range of 10-13 and overbought in range of 20-25. Nifty has had a crash after after getting in the range of 20-25 and have rallied after touching the range of 10-13 .

OVERBOUGHT MOMENTS in Indian Markets

Click to enlarge , Data for last 10 yrs (Jan 1999 – 31st May 2009)

You will see that whenever nifty crossed 20. It was time to be cautious. its not exactly the time to go short sell, but at least book your partial profits and be cautious with further buying for long term.

Current situation : As I write this, Nifty PE is around 21. Its not a very good situation to madly buy for long term. Its a time when euphoria is at high point and it can take markets a little further. So you can jump in now with short term perspective, not long term !!, because markets may fall in some weeks or months.

Who all missed the current Rally? I missed it. there are two reasons, I am a trader not an investor for long term (at least currently).

So I do not concentrate on it. But you could have not missed it if you had read this concept earlier and had the guts to go against the so called “experts on CNBC” who were talking about 5k or 6k for NIFTY some months back.

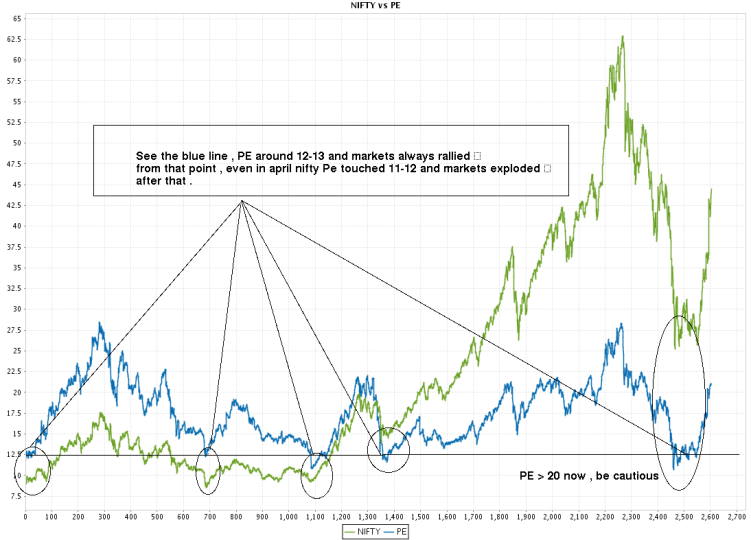

Click to enlarge , Data for last 10 yrs (Jan 1999 – 31st May 2009)

If you see the chart, you can see that after touching the PE levels of 11-13, markets have rallied back as it was too oversold !! Again, just touching these levels of PE does not signal a BUY, its only a signal to be cautious and make your mind for long side, and start the accumulation process without fear.

Markets will still make lower levels and experts on CNBC will still cry over economy conditions and world coming to an end. But market rewards the “risk assumption”, not the actions on obvious facts. You also have to decide how much money of your portfolio would you like to put in stock market after considering your risk-appetite.

What can we learn from this PE Concept?

“We can learn from history that we do not learn from History”

This is true for almost 95% of the long term investors all over the world. They do not learn things, they do not do any research, they do not go and read blogs or tons of informational sites, they just want tips from others and make money. the mathematical expectation of that kind of investing is negative and cant work for long term.

Lets develop a simple concept of PE based Investing. here it is:

BUY Signal : Once PE crosses below 13.

When NIFTY PE reached levels of 13 , start accumulating the stocks and invest your money in 4-5 installment over some months. Make sure that markets are going up and down and moving in a range . If PE crosses below 11 , its a must BUY !!

SELL Signal : Once PE crosses above 20.

Book the profit once NIFTY PE crosses above 20, Don’t book all profits at once. Book it in parts. PE crossing above 20 does not mean markets has to fall, its only an indication that markets may be oversold and now “smart people” will starting selling there shares to mad public.

Short sell the shares once PE and Markets start falling down from PE levels of 20. If PE crosses above 25, its a must SELL !!

There have been cases of PE going up to 25-28 levels. That will happen at the peak of strong bull markets like Jan 2008. In very strong bull markets you have to understand that PE will cross even above or below its extreme points. That’s the risk part of stock markets from which not even GOD can save you from !! 🙂

This is the time when your buying in parts and putting capital which you can afford to loose will help !!

Anyone who puts 100% of there money in stock market at once on one single time on a single bet has a secret affair with financial disaster which he/she himself is not aware of. So don’t put all your money at once. Only put a part of your capital at any point .

Where do you get the PE data for Indices? (Nifty and other Indices)

PE data : https://www.nseindia.com/content/indices/ind_pepbyield.htm

Note :

I have divided Nifty Value by 100 to make the graph look the way it is . In graphs , so on X axis if you see 40 , then read it as 4000 for nifty . but exact 40 for PE .

PE value will be separate for individual stocks as PE ratio for stock can go up or down for many other reasons . So if you are doing Stock analysis , see its historical PE values and find some pattern yourself . Innovate !!

I hope you have got a clear idea about Nifty PE. If you still have any confusion you can leave your query in our comment section. Also do let us know your opinion about this article.

I did a short and crisp review of some mutual funds for a friend . thought of sharing this here.

Franklin India Prima Fund – Dividend

151/208 138/157 61/75 are the ranks for 1 ,3 and 5 year . Not a great one to cheer about .

Risk Grade: Above Average

Return: Grade Average

Tata Infrastructure Fund-G

Not a very old fund but its a good one. Infrastructure space can be a big hit considering 4-5 yrs time frame and with the blessings of UPA. Better diversify money in this space along with other infrastructure Mutual Funds.

With 25% CAGR returns since launch , its looks good.

Franklin India Flexi Cap Fund – Dividend

Numbers look good but there are better funds available.

Birlasunlife Frontline Equity Fund-Growth

Extremely good fund to have in portfolio. It has shown strong performance in all the time frame of 1 ,3 ,5 yrs and 30% CAGR return since launch. Better to stop Franklin India Flexi Cap Fund and redirect the money to this one.

HDFC Equity Fund – Growth

Again a good fund to have in portfolio.

What would I do If I were at your place.

– Stop Franklin India Prima Fund

– Stop Franklin India Flexi Cap Fund – Dividend (5k)

– DSPBR Equity or DSP Black Rock top 100 or HDFC Top 200

– Increase your Exposure in Birla Sunlife Frontline Equity Fund

– Share your 10k in UTI Infrastructure and Tata Infrastructure

When an agent approaches you with ULIP product; before filling up forms, he should be explaining you What is a ULIP and how it works! You should ask him the following 6 questions to make sure you know what you are about to buy!

1. What are the returns offered by this ULIP?

As per the rules of IRDA, an agent should explain you the workings of ULIP with an assumptive illustration earning 6-10% returns. However, if he claims that in the long term the policy is expected to give more than 10% then this information is not misleading.

But if he claims that the policy ‘WILL’ earn 18-20% or even Million% returns, you need to stay away from such agents!

2. What are the Charges applicable in this ULIP?

He should give you detailed Information on all the charges that are/will be applicable to ULIP. The important charge you need to know is Premium Allocation Charges.

If he doesn’t disclose any Charge that is applicable then I am sure its not because of his dishonesty and no other reason. Ask him the company brochure mentioning the exact charges where all the charges are listed and explained in detail.

3. How does it suit my Risk Profile and fit in my requirement?

Before suggesting you the ULIP the agent should have asked you all the details about your Cash flow (Salary, Expenses) and your future goals with ULIP investment should be addressed.

He should also try to understand if you can take the risks associated with the ULIP. If he does not ask you these things then you ask him back why he has not asked you these questions. Get the word out of his throat!

4. How is it better than other ULIPS?

Ask him what is unique with the ULIPs he is recommending to you and make sure he does start all non-sense of Sec 80C benefit and high returns and all… Every ULIP has it! Ask him what are the special features with ULIP and how do they address your requirements.

If he claims that his company ULIP is the best and no other ULIP can match it then ask him for references if any states that. Just a plain claim from agents will not do. An agent must have enough knowledge to make you understand how to make best use of your ULIPS.

5. How does it score over Term Insurance + Mutual funds combination?

ULIPS are combination of Insurance and Investment produce, There is no point in taking it, if it cant perform better than Term Insurance + Mutual funds SIP. Switch benefits in ULIPS are the main benefit in ULIPS.

He must put pressure on that point, If not he is him self not aware of it. Refrain from taking the policy if he starts claiming that returns from ULIPS will be much higher than Mutual funds.

6. What was the performance during Market Crash?

Agents generally try to put up rosy picture and hence refrain from disclosing the funds performance in bad markets. If the fund has done bad, that is acceptable. Its investor responsibility to take care of switching and asset allocation.

So there is nothing wrong in performing bad in bad markets. Agents will first try to avoid the confrontation, but finally may tell you that they did bad and returns are very low. Ask him for exact number in return and try to find out how other ULIPS performed.

My personal Experiences

I have never come across any ULIP agent who has tried to sell the product in a professional manner. This has its own reasons like meeting Sales Target pressure or poor training to Agents. Anyways ,its not acceptable and can not be accepted . For so many years, Mis-selling is happening in India.

Conclusion :

Your hard earned money should go in proper investments. There should not be hurry in taking action. So don’t feel shy in asking questions once or twice or thrice, understand the product and its suitability with your requirement.

No product is good or bad, its only bad or good depending on your requirements. So be informed Investor and don’t fall prey to Idiotic agents.

Don’t do mistakes that are already done by tons of investors who took ULIPs for 3 years.

– To save tax

– Make exceptional returns from Stock markets

– Make them self believe its a happening product because it looks so complex

Please share with me if you have taken ULIP for wrong reasons

– Do you think that ULIPS will have any success in future… I feel yes