Do you make a choice or take decisions in your financial life ? A lot of people have not taken lots of important actions in their financial life, which they should have taken long back!. You have to understand that you are making a choice by not taking those actions. When you take some action or do not take an action, deep down you are actually making a choice in your financial life, which we will see now.

Let me give you some examples

1. Buying Endowment & Moneyback Policies

Most of the people who take the decision of buying endowment and moneyback insurance policies , they say that they are buying it because they trust the company and want safe returns. Now that’s their decision, however they have to be understand that deep down they are making some choices which are unspoken …

- They are choosing to get below inflation returns on their investments

- They are choosing to put money in something which is illiquid and might not help them in emergencies

- They are choosing not to cover their family with a higher life cover

2. Not buying a Term Plan

“I don’t think I will die” or “It does not give back money at the end” – this is the general reasoning behind not taking a term insurance plan by many people. Now, again, it’s their decision based on their belief, but deep down they are making some choices which are

- They are choosing a life of struggle for their family, in case they are no more in this world

- They are choosing to pass on all the debt and tension to their spouse and children in future

- They are choosing that their children and family might not lead a great comfortable life in future if they are not around.

3. Not buying Health Insurance

“I will take is next month” and “I drive carefully and I am healthy , so I don’t need it” are the top most reasons given by those who avoid taking health insurance. Again, they feel it’s a right decision and I am not commenting if it’s right or wrong, but surely they are choosing few things in their life and for their family …

- They are choosing a situation where their entire wealth accumulated till date, might wipe out in health related expenses someday

- They are choosing to get into a situation where they might have to run around for money to fund health related expenses

- They are choosing to constantly worry about big ticket health related expenses if any

4. Not creating a WILL

It’s a decision taken by almost all of us. “We are still young”, “I will do it once my net-worth is at least 1 crore” etc., are the common reasons behind not making a WILL. However deep down you are making few choices and you have to accept them …

- You are choosing a lot of frustration, chaos and running around for your legal heirs

- You are choosing, that your family will have to meet lawyers, go to courts and spend lots of money and effort to get what they deserve

- You are choosing to create a confusing situation, where your legal heirs fight with each other and try to justify who deserves what

5. Not hiring a Financial Planner (when you really need it)

“I can do it myself, I was a bright student all my life”, “They charge a lot for what they do”, are some of the reasons given by investors for not hiring a financial planner for themselves. It’s their decision based on their beliefs, but deep down you are making some choices …

- You are choosing to still do trial and error and play with your financial life

- You are choosing to not organize your self and get into a dedicated structure which can improve your financial life

- You are choosing to focus on what you will spend rather than what you will get out of the whole exercise.

- You are choosing to delay your actions and rely on yourself for taking actions and get disciplined which most fails most of the times

6. Over spending right now like there is no tomorrow

“Life happens NOW”, “If I don’t spend, whats the point of earning well”, “I will earn more in future, let me enjoy today” – These are the top most things you will hear people saying who over spend (more than they should). One can comment easily if it’s right or wrong, but let’s not get into it, it’s their decision and there is nothing wrong in it, just that these people need to understand the choices they are making without realizing them

- They are choosing to have a struggling financial life in future in case tomorrow does not turn out to be like what they imagined

- They are choosing to have a better today at the cost of tomorrow

- They are choosing to be working for more years in future, because they will not have wealth when they are old.

- They are choosing to have a less comfortable life later in life, when responsibilities increase and opportunities decrease

Conclusion

At the end of the day, you always choose something in your life out of the decision you make. This is true for all the aspects of life, including your financial life. So understand that you are fully responsible for what you get.

Can you share your story in short and share what choices have you made in your financial life ?

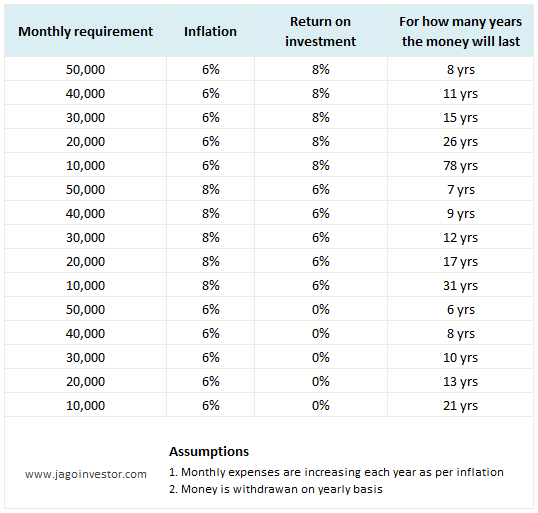

You can calculate this in many ways , but one of the ways you can do is by calculating it in excel sheet. We have this calculator on our upcoming

You can calculate this in many ways , but one of the ways you can do is by calculating it in excel sheet. We have this calculator on our upcoming