One of the most important factors of having a good financial life is a good and rising income. To create wealth, you need to constantly invest money and grow it over the years — but that journey begins with a solid income that keeps increasing meaningfully.

However, many of the people we work with often share their frustration: despite working hard and staying committed to their job, their income remains stagnant, and raises are uncertain.

Most people wonder why this happens. While external reasons — like company performance or market conditions — do play a role, in our experience, the bigger reason is internal: mindset, habits, and personal choices that silently block income growth.

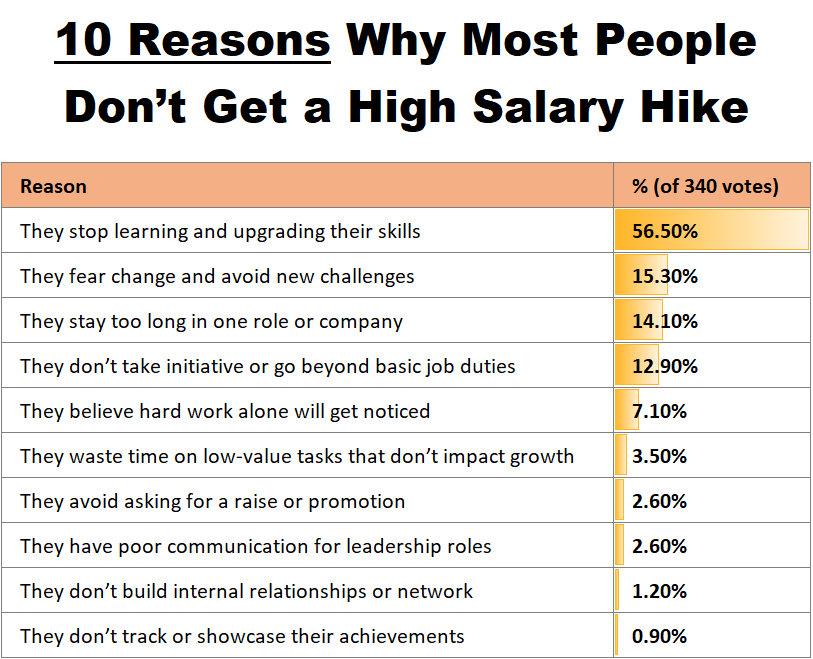

I asked 340 of our clients and community members

That’s when I decided to dive deeper and use the community wisdom to find out what most people think.

Why don’t people see a sharp rise in their income over time? I’m not talking about the standard 5–6% annual increment — I’m referring to those powerful 15–25% jumps that change your financial trajectory and speed up wealth creation.

So we ran a poll among our clients and network. The responses were insightful — and eye-opening.

Let me walk you through the real reasons why income doesn’t rise as much as it could.

1. They stop learning and upgrading their skills (57%)

This was the top reason why most people don’t see a meaningful increase in their income over time.

The world is evolving rapidly, yet many professionals stop learning once they settle into a job. They get into comfort zone and life gets complicated. They either are so consumed with life or they are not able to see the vision of where the company and sector is headed.

What made them valuable 3 years ago may now be basic or obsolete. Continuous skill upgrades — especially in tech, tools, and strategy — are essential to stay relevant and command higher pay. This is mostly true for IT field

2. They fear change and avoid new challenges (15%)

Around 15% of respondents felt that fear of change and discomfort with challenges is a major reason for income stagnation.

Career growth requires courage — the willingness to take on unfamiliar roles, lead new initiatives, relocate if needed, or even change jobs. But many professionals prefer the comfort of routine over the uncertainty that comes with growth opportunities. Not everyone embraces challenging tasks that push their intelligence and problem-solving ability.

Unfortunately, this fear often stalls progress and limits income growth. In most cases, people are paid in proportion to the initiatives they take, the risks they handle, and the results they deliver — not just the years they spend in a role.

3. They stay too long in one role or company (14%)

This is something we hear often during our annual reviews with clients. Many professionals stay in the same role or company for years, believing that loyalty will pay off or that staying put is the better path for compounding. While that sounds good in theory, the harsh reality is different.

Most companies don’t offer substantial hikes to existing employees, no matter how consistent or loyal they’ve been. Ironically, the same person — if hired externally — would often receive a significantly higher package. Staying in the same role too long without new responsibilities or promotions frequently results in being underpaid relative to market value.

Strategic job changes or internal role transitions are often necessary to reset and accelerate your income trajectory.

4. They don’t take initiative or go beyond basic job duties (13%)

One major reason many people don’t get significant salary hikes is that they operate strictly within the boundaries of their job description. They complete tasks as assigned — and while that’s appreciated, it’s rarely enough to justify a big raise.

As an employer myself, I’ve noticed that some employees do their job well, but they never think beyond what’s explicitly mentioned. They wait to be told, rather than sensing what needs to be done. But then there are others — a rare few — who operate like owners. They hear what’s unspoken, anticipate needs, and take charge like entrepreneurs within the system.

That level of ownership and initiative is what truly stands out. These are the people who unlock faster career growth — because companies reward those who think like leaders, not just doers.

Now lets look at some more reasons which got less than 10% votes and were not the top most reasons majority felt.

5. They believe hard work alone will get noticed

Hard work is important, but visibility matters too. Simply being reliable or clocking long hours won’t automatically lead to raises. Strategic contributions, aligned with business goals, and making them visible to the right people is what drives real income growth.

6. They waste time on low-value tasks that don’t impact growth

Being busy isn’t the same as being valuable. Many professionals fill their days with tasks that don’t move the business forward. Focusing on high-impact, strategic work is what separates average performers from high earners.

7. They avoid asking for a raise or promotion

Some employees assume management will notice their efforts and reward them. But in reality, raises often go to those who confidently advocate for themselves. Not asking is one of the simplest reasons people stay underpaid.

8. They have poor communication skills

No matter how skilled you are, if you can’t communicate clearly, influence others, or present ideas effectively, your leadership potential is hidden. Strong communication often unlocks bigger roles — and higher pay.

9. They don’t build internal relationships or network

Career growth isn’t just about what you know — it’s also about who knows you. Building relationships within your company helps with visibility, collaboration, and getting pulled into high-impact projects. Being invisible is a slow road to growth.

10. They don’t track or showcase their achievements

Many professionals do good work but never document or present it. Without showcasing results, managers may underestimate your contribution. Keeping track of your wins and communicating them is crucial for justifying a significant raise.

Don’t Let Your Income Plateau

Your income is one of the biggest drivers of wealth creation — especially in the first 10–15 years of your working life. Most people focus heavily on budgeting and saving, but overlook the single most powerful lever they have: increasing their earning potential.

If you’re serious about building wealth, reaching financial independence, or simply improving your quality of life — then you must treat career growth and income acceleration as non-negotiable.

Use this list as a mirror. Identify what’s holding you back. And most importantly — act on it.

Because while compounding works on your investments, it works even faster on your income — if you put in the effort.

Create your Wealth with Jagoinvestor Team

If you’re serious about transforming your financial life and avoiding these costly mistakes, the Jagoinvestor Team is here to guide you. We’ve helped thousands build meaningful wealth with clarity, discipline, and a proven roadmap. If you’re ready for real progress — not just information — join hands with us. Fill up this form and let’s start your wealth journey the right way, with the right support