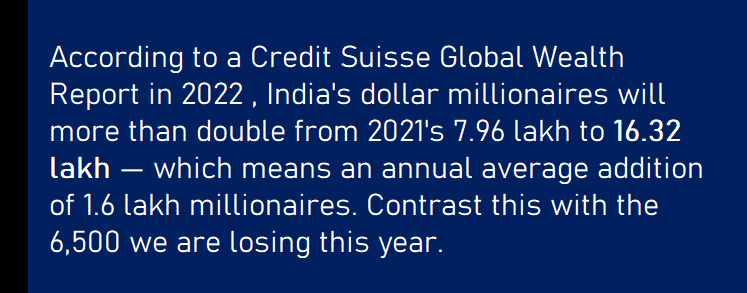

Recently, I came to know that around 6500 Indian millionaires have migrated to other countries this year.

The moment I heard this, the first thing which came to my mind is “How many millionaires are there in India? and entire world?”

Are you part of that list of millionaires? And if NO, then when will you be on that list?

When we say “Millionaire”, it means someone who has a total net worth of around $1 million, or Rs 8 crore in Indian currency apart from the house they live in!

0.7% of people in the world are millionaires

We all want to create a big retirement corpus and achieve financial freedom, but what if we keep it simple and just think of reaching $1 million first in our life? And if we can do that by the time we turn 50 yrs of age, that would be a wonderful achievement.

Especially because there are just 0.7% of people in the world who are millionaires!

Yes, you heard it right!

Only approximately 56 million people on their earth are millionaires (many of them are multimillionaires and billionaires also). We have close to 8 billion people on Earth, so that makes 0.7% of people on Earth as millions.

What about INDIA?

If you specifically talk about India, as per the official data, there are close to 796,000 millionaires out of 140 crores people and that makes it just 0.06% of the population. The US alone has around 2.55 cr millioanires, while China has around 62 lacs.

So if you achieve a wealth of $1 million, then you are amongst the topmost cream layer of the country.

But how easy is it to create $1 million in India by the time you turn 50 yrs?

Truly speaking it’s not an easy task per se.

One has to be super aggressive when it comes to investing money, from an early age if one wants to reach that kind of target, especially because we also have to buy a house (most people take home loans) and clear off the loan too. Apart from these, we have other goals like buying a car, vacations, children’s education and marriage etc.

Forget creating $1 million, most people will struggle to close off their home loan by the age of 50 and create enough corpus to meet their children’s education by the age of 50.

However, A tiny percentage of people who earn very handsomely and invest smartly create good wealth and many of them will become a $ millionaire too. A good thing is that while many are leaving the country, the rate at which millionaires are getting added every year is very high.

What is required to create $1 million by the time you turn 50 yrs?

Let’s deal with the idea of what exactly is required to become a millionaire ($1 million or approx Rs 8 crore) by the age of 50. Here are some assumptions before we start!

Assumptions

- This amount is apart from the primary house and any other financial goals like kids’ education, car, vacations etc

- We will also assume that the person can increase their SIPs by 8% every year and the return on investments is around 10% (net of taxes)

- We are assuming the same Dollar Rupee conversion rate in future also.

Note: In future (after 10-15 yrs), even $1 million will not be of same worth like today in India, however we are mainly focused on the calculation part here.

If we go with the above assumptions, here is what is required at different ages (an example)

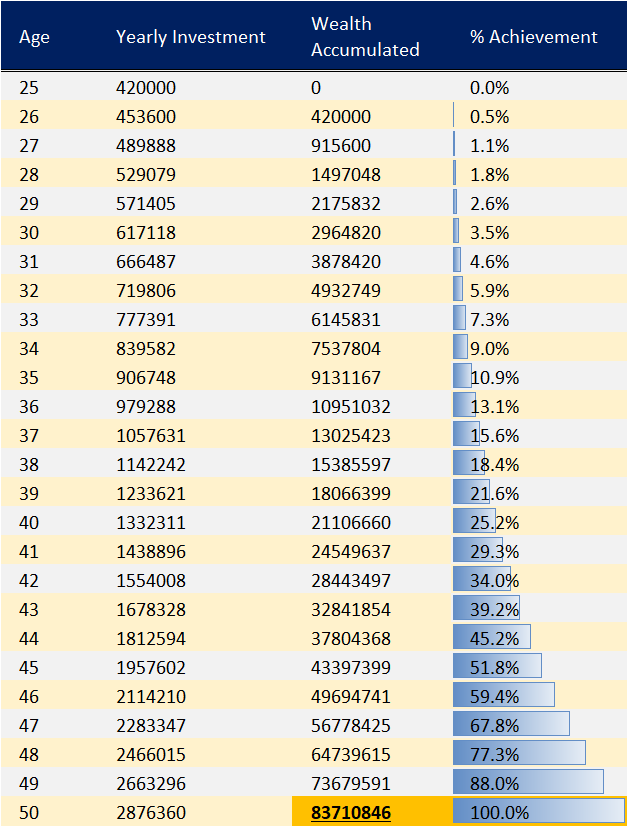

Case 1: Age 25

- Current Wealth : 0

- SIP required: Rs 35,000 per month

A 25 yr old person, with no wealth in their hands, wants to become a millionaire by the age of 50, then they will have to start a monthly investment of approx 35,000 and then continue that for the next 25 yrs. Here is how the growth will look like

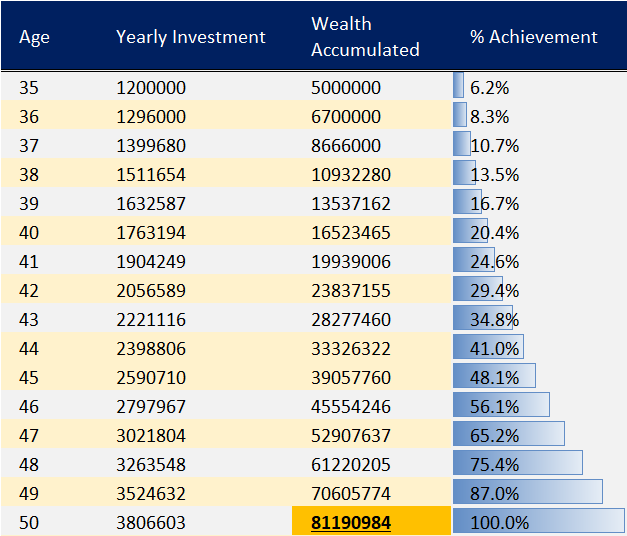

Case 2: Age 35

- Current Wealth: 50 Lacs

- SIP required: Rs 1,00,000 per month

A 35 yr old person, with around 50 lacs in hand, wants to become a millionaire by the age of 50, then they will have to start a monthly investment of approx 1,00,000 and then continue that for the next 15 yrs. Here is how the growth will look like

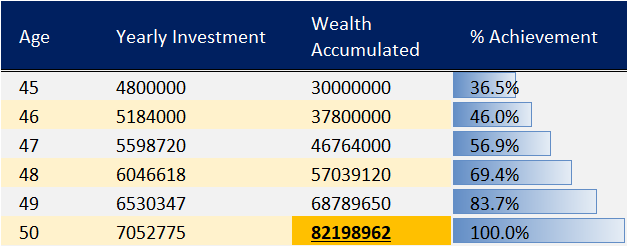

Case 3 : Age 45

- Current Wealth: Rs 3 cr

- SIP required: Rs 4,00,000 per month

Finally, let’s also talk about someone who is 45 yr old. They must have approx 3 cr in hand and shall be able to invest around Rs 4 lacs per month (this is just one combination), if they want to become a millionaire by the age 50. This is quite tough for most people, but still, an example has to be given.

As you can see, it’s not a child’s play to become a millionaire by age 50 yr. One has to start early and start very well and continue for a very long time to do that.

Hence, The topmost thing to focus on has to be your income-generating capability which will be income on the table and then the next step will be your discipline to continue your wealth creation path.

I hope you were able to get insights from this article. In case you want to start/continue your wealth creation journey with right-hand holding, then our wealth creation services can be helpful for you. Please click here and reach out to us to explore how we can help you in reaching your millionaire target by age 50.