Jagoinvestor

Jagoinvestor

February 22, 2022

February 22, 2022

4 methods of calculating Networth, which no one will tell you

The Networth formula is quite simple

Networth = Assets – Liabilities

So, if you have assets of Rs. 2 crores and your liabilities are 50 lacs, your net worth is Rs 1.5 crores.

We have always been taught to calculate networth this way and there is nothing wrong with that, however, it’s a very simplified version of calculating your net worth, which does not give any kind of insights or information to you.

A lot of times, you may also get the wrong impression about someone because of this over-simplified formula. A lot of investors on paper are having good networth, but they never feel RICH or satisfied with what everyone thinks about them.

For example, imagine a person who lives in a house worth 2 crores (no loans) and also has another real estate worth 1 crore, plus mutual funds worth Rs 50 lacs.

Now, what is his/her net worth?

- Some will say that the person’s net worth is Rs 3.5 crores (2 cr+1 cr+ 50 lacs) as per our simple definition?

- Some will say that we shall not count his current house, hence it’s just 1.5 crores.

- And some may comment that because the real estate is not liquid enough, it shall just be seen as 50 lacs of networth?

- And what if this same person may also inherit shares worth 10 crores in the future? Then?

I hope you got my point. Just doing assets minus liabilities, gives you a one-point answer and that misses the details and gives you very superficial information.

4 categories of Assets

Recently, I created a framework using which it becomes simpler to visualize your networth. In this framework, the first step is to categorize all your assets into one of the 4 categories as below.

- Blocked – An asset is marked “blocked” if it’s not liquid and the money is blocked for many years. You can not liquidate, or do not wish to liquidate right now. However, in the future, you will liquidate it and use it for funding any goal.

- Free – An asset is marked “Free” if it’s possible to liquidate it in a few days/weeks and get the money in your bank account.

- Usable – An asset is marked “Usable” if it’s used for consumption purposes. So the house you live in shall mostly be counted as “Usable”. The gold jewelry at home shall be marked as “Usable”. However if you have a house where you live right now, but you know that in future, you will surely move to your home town and sell off the house or put it on rent, then that house shall be marked as “Blocked” and not “Usable”. A car can also be marked as “Usable” if you wish, however, it’s not recommended.

- Maybe – Another category is “Maybe”. An asset shall be marked as “Maybe” if you are unsure if it will come to you in the future or not. You do not want to count on it as of now, but if you are lucky, that will come to you. So any inheritance may be marked as “Maybe”. Some money which you gave as a loan to a friend may be marked as “Maybe”. However if you are very sure that its surely going to come to you, then you shall mark it as “Blocked” and not “Maybe”

Let me show you a sample data of how it looks like

[su_table responsive=”yes”]

Asset Name |

Current Worth |

Type |

| MF (Equity) | 15000000 | Free |

| MF (Debt) | 1550000 | Free |

| Flat in Bangalore | 5500000 | Usable |

| Land in Hyderabad | 2000000 | Blocked |

| PPF | 4000000 | Blocked |

| EPF | 2876000 | Blocked |

| Shares | 3000000 | Free |

| Cash | 130000 | Free |

| Plot in Home town | 5000000 | Maybe |

| NPS | 5000000 | Blocked |

| Fixed Deposits (Inheritance) | 1000000 | Maybe |

| Loan to someone | 50000 | Maybe |

| Gold | 1500000 | Usable |

[/su_table]

Note that if there is a home loan or car loan then please adjust the loan amount with the market value of the asset and only write the difference. So if a house is worth Rs 1 crore and the outstanding home loan is 40 lacs, then write value of house as only 60 lacs.

Visualizing your Assets

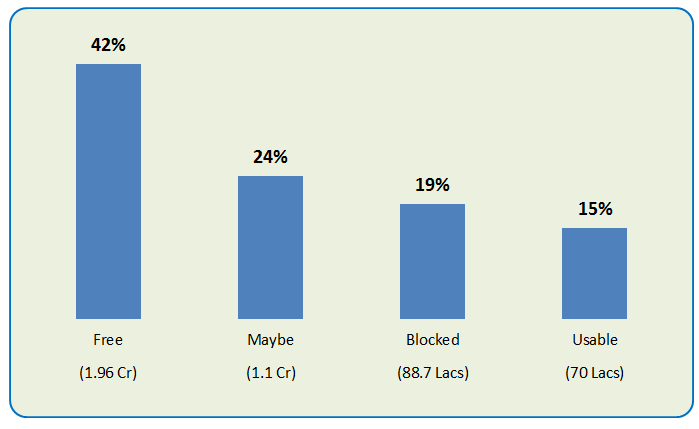

Once you categorize the assets into 4 types, you get clear information on how many assets you own in each category. It helps you a lot to make sense out of it.

Here you can see that by categorizing the assets into types, it’s so clear now that this person has a total of Rs 1.96 crores in those assets which are in Liquid form (FREE) and a major chunk of 1.1 crores (Maybe) is into assets that may or may not come to him. So it’s not very prudent to count on them for his future. If it comes to him/her, it’s a bonus.

Also, Rs. 88.7 lacs is blocked into various assets, so while all the relatives and friends consider it to be his net worth, it’s not available to him/her at the moment if need arises. So he is paper rich, but not in reality.

Also, Rs. 70 lacs is into those assets which is used for consumption purpose, which he will never liquidate for his goals (unless there is an emergency or in theory)

4 types of Networth

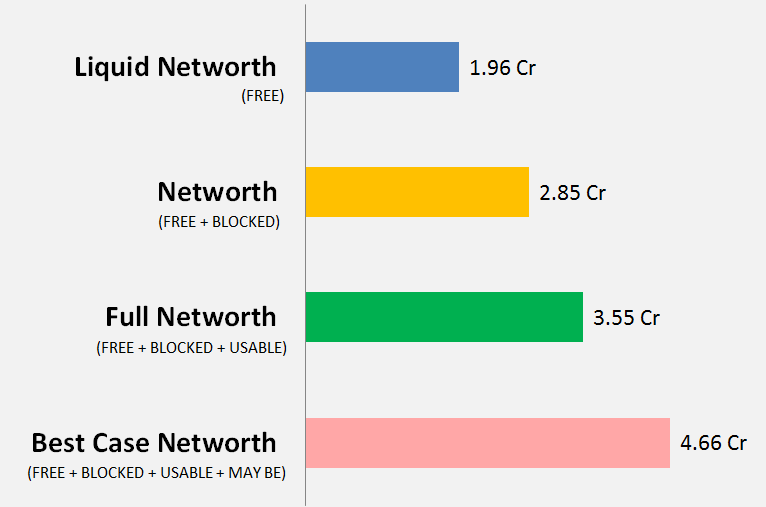

This brings me to the final and conclusive point – “What is his net worth”?

Here, we shall different kinds of networth rather than just looking at one single networth.

- Liquid Networth – You just add up all the FREE resources and call it your Liquid Networth. In the case above, its Rs 1.96 crores

- Networth – Add up your FREE and Blocked assets, which I will call “Networth” which totals to Rs 2.85 cr here, which is the traditional definition of net worth. I am not including the Usable and Maybe category of assets into this.

- Full Networth – This will include all your assets except the “Maybe” category. Full Networth means all assets which you own (either for investment or consumption), and you have full control over it. In this case, its Rs 3.55 cr

- Best Case Networth – This is the total of everything you own or can own in the future. This will be the same as full networth for those who don’t have any inheritance or assets which are probable to come to them. In this case, it’s Rs. 4.66 Cr

Here is what you shall do now

Put your assets in an excel sheet, and mark each one of them into FREE, BLOCKED, USABLE, and MAYBE. I am sure you will get a lot of clarity on how much of your assets fall in these categories and the various kinds of networth you have.

Do give me feedback if you liked this framework and if it helped you? This is just a framework and you can customize it as per your way of looking at things.

Based on Pattu Sir’s blog “How liquid is your net worth” I categorized my assets into 5 categories based on the “liquidity” factor. Those 5 categories were as follows:

1) Highest – Savings account (Immediately available for use)

2) High – Stocks, Mutual Fund, Endowment policy (Can be liquidated in 2 days to max 2-3 weeks)

3) Medium – EPF, Money lent to friends & family (Can be liquidated within a few months)

4) Low – Home (6 months to 1-2 years)

5) Lowest – PPF

Will carry out this exercise by tagging investments based on criteria mentioned in this post.

Thanks.

Great 🙂 thanks for sharing that!

Very helpful post in learning about net worth. It makes a lot of sense to use the liquid networth since that is what you can actually use to run your life on an immediate basis.

One of the best posts I’ve read about calculating networth ! All of my doubts are clear now. Thanks for sharing

Welcome .. thanks

This is really simple and easy to understand networth, as you said we are rich on paper and reality is totally diff. This also gives to have money as per goals, and so more clarity for short and long term goals.

Thanks Suvarna

gold is kind of free assets right as we can liquidate it quickly when in need.

You have to mark it as per your PLAN for future.

If you are going to liquidate it at some point of time (for sure) and then use it for some goal, THEN you shall mark it as BLOCKED

If you CAN liquidate , but will NOT liquidate in normal circumstances, then you shall mark it as USABLE!

Very practical approach and quite insightful and interesting. Thanks for sharing this

Thanks

After going through this article my assessment of people has got a radical change.I should recall an old version.When Nepolean was asked about the strength of his army he said : Two lakhs. But actually he had only one lakh personnel.When this was pointed out to him he said.I am worth one lakh and I have another one lakh people with me.

Haha .. good one !

A different and a realistic perspective indeed

Great!

Finally, I got a chance to share a great input for your research.

I really love your article and silently read and follow, without adding much to your insight story. Because I really do not find any valuable input from my side. So I kept mum.

This time I really got a great idea which I want you to explore for us.

In my view, and I also follow, “higher the cash flow a person generates higher the networth should be considered”.

One example – After independence many royal families decedent’s choose to sale their fort to full-fill their lifestyle expenses. So in my view, it’s false display of richness if as an individual not generating a healthy cashflow.

Second example – most of the people try to get job rather than starting a business (many who are in business or say small trade are not by choice) because a cash flow is almost guaranteed.

Third Example – Please correct me if I am wrong, banks give credit rating based on cash flow and not how much individual do have. I know my friend was having bad credit rating and was advised from the same recovery agent that use your card and pay in time, don’t worry how small it is, it will help improving the rating. Again a cashflow generating ability might be at stake.

Poor people often generates very poor cashflow

Middle class only accumulate cash and hence cashflow is still low on their part

Rich people earn more spend more (errrrr…..and save even more) and hence they are being viewed as rich most and accepted as rich in our standard society.

Thanks for sharing that!

Wonderful article! I am a regular reader of your posts from few years now. Must congratulate you for the way you present complex subjects in such a simple language. Keep up the good work

Welcome 🙂

I learned something new. Good article.

Glad to know that!

Worth knowing the real worth of the individual. Really informative and educative. These things nobody teaches or come across.

Glad to know that 🙂

while I may agree about the classification for convenience ultimately the networth of an individual remains the Best Case Networth.

This is what I have seen in last few years when I have seen sad demise of my friends.

apart from fixed deposits, shares ( free networth) all others were liquidated and could be used by the family for their needs. This includes plots and commercial premises also.

you may at best call them illiquid or not free but even the so called free net worth assets like shares or mutual funds if you have to use you might land up making losses as you see today market crashed very badly.

I have also seen people liquidating their assets or taking loans against so called illiquid assets like home during period of covid the free assets sold got them much lesser price than these loans against these illiquid assets. ( the assets regained their price as covid eased off)

All in all — the calssification is

Hi Subodh

We are not talking about DEATH case here.. We are talking about it from goals achievement point of view.

Excellent Article. Important insight on net worth Concept.

Thank you.

Glad to know that!

As per my opinion there should be two methods to calculate your networth i.e. liquid and iliquid. Liquid assets can be utilised immediately and iliquid assets take some time to realise.

YOu can do that way also 🙂

The above method of calculating Net-Worth is also as per the accounting principle of conservatism wherein all possible losses and expenses should be accounted for but probable incomes or gains should not be included in accounting. The article is very nice and provides new insights in knowing one’s true financial worth.

Thank You.

Glad to know that Sharad!

This is amazing and something new to think about. We are rich on paper but not in reality is an eye opener. I strongly believe that financial education must be inculcated at child hood to bring prosperity to every lively hood. The term poor is because of three things: 1. we don’t learn to attract money. 2. We failed to recognized between opportunity and threat. 3. We are unsure about our goals and plans.

Keep reading! Keep Sharing! keep Learning! keep Growing! So KEEP IT UP..

Thanks for sharing your views and appreciation 🙂

thats a nice way to net worth identification

Excellent full insight. Removes a lot of confusion and brings clarity of vision.

Greeat!

Thanks for the insight on this. Really helpful especially to inform kids our current position

Wonderful .. thanks for sharing

Very good classification

Thanks

Really insightful message..

Thanks