Jagoinvestor

Jagoinvestor

June 17, 2016

June 17, 2016

5 Asset Classes Explained – A simple guide for beginner Investors

Today I am going to teach you about “asset classes”, which is the most primary lesson every investor should go through. Understanding asset classes is very important for an investor because when you invest your money in any financial product, then in the background, it goes to a certain asset class only.

The world of personal finance has hundreds of financial products, which makes everything confusing for an investor, but if you understand which asset class it belongs to, then this whole world of personal finance will sound easy to you.

So if you are confused about whether to invest your money in a fixed deposit or a mutual fund? Or into gold ETF’s or PPF? How do you decide?

Just ask – “Which asset class does it belong to?”

Is a fixed deposit in the bank better or a PPF would be the right thing for you, this all questions might seem to be confusing to you if you do not understand which asset class they come from? So in this article, we will go deeper into the basics of investing and help you to get stronger into the primary level information.

What is the meaning of Asset Classes?

Asset classes can be seen as a big basket where all the financial products belonging to that asset class share common characteristics. Things like risk, returns, liquidity, and various other parameters are similar.

For example, a Fixed Deposit and PPF are different financial instruments, but at the deeper level they both are secure products, you do not lose money in these products, their returns are also predefined and there is predictability in their returns.

Can you see that both FD’s and PPF share some common characteristics? It’s because they both belong to the asset class “Fixed Income”.

Here is a video which gives an introduction to asset classes

In the same way, an equity mutual fund or direct stocks, both are different financial instruments from high level, but inside they both are high volatility instruments and have potential to multiply your investment amount many times in short period of time, this is because they both belong to same asset class called “Equity”.

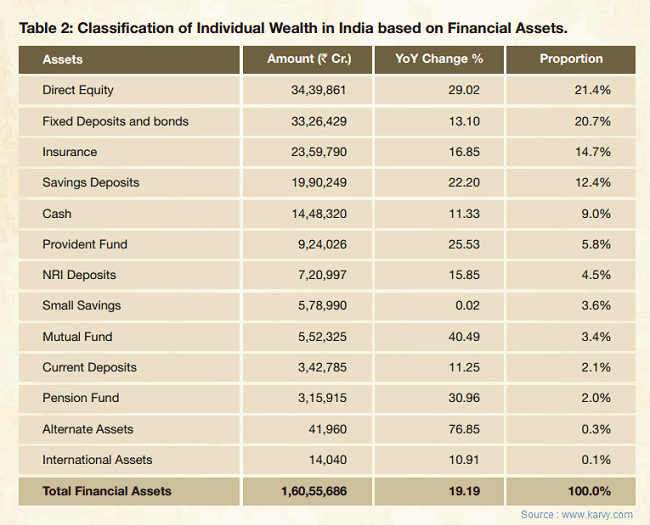

Below is a snapshot from the Karvy website which shows you the wealth distribution of Indian investors in the year 2015.

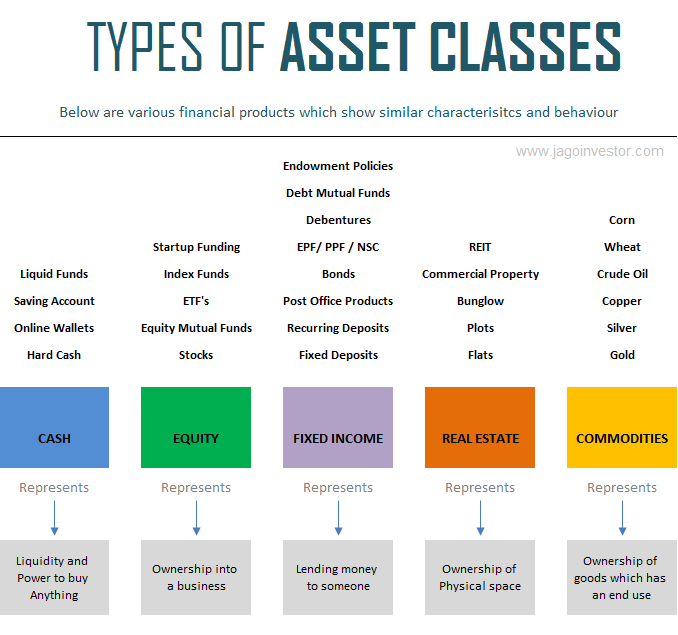

There are 5 asset classes

While there is no standard list or category of asset classes, widely it’s accepted that there are 5 types of asset classes namely

- Fixed Income

- Equity

- Real Estate

- Commodities

- Cash

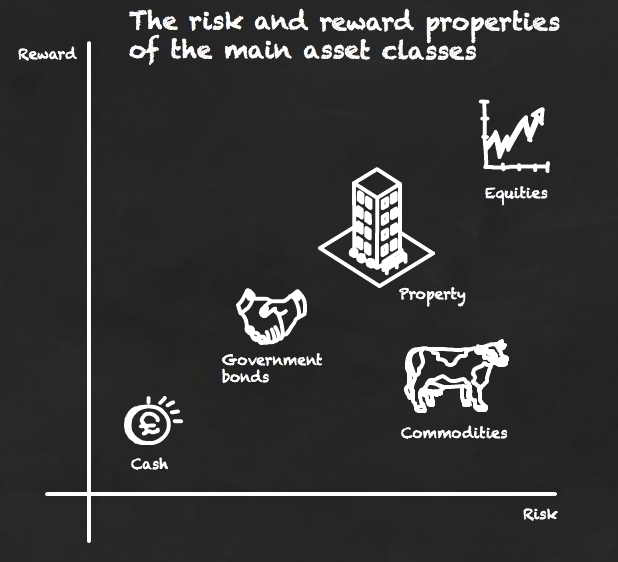

Every financial product you come across will fall into any of these 5 asset classes only. Each of these asset classes has their own set of behavior and they represent something unique about them. The chart below shows you financial products belonging to these asset classes and what these asset classes denote

Asset Class #1 – FIXED INCOME

Let’s start with the most famous and favorite asset class in India, which is “Fixed Income”. Fixed Income asset class refers to the class of financial products where your investment amount is more or less protected and the returns are either fixed or predictable to a great extent. There is almost no/less risk in these products which are from the fixed income asset class.

Investing in fixed income asset class is like lending your money to someone with the assurance of return with predefined returns. So when you make a fixed deposit in a bank, you are not exactly “investing”, but lending your money to the bank with a promise that they will return back your principle amount along with a pre-defined interest.

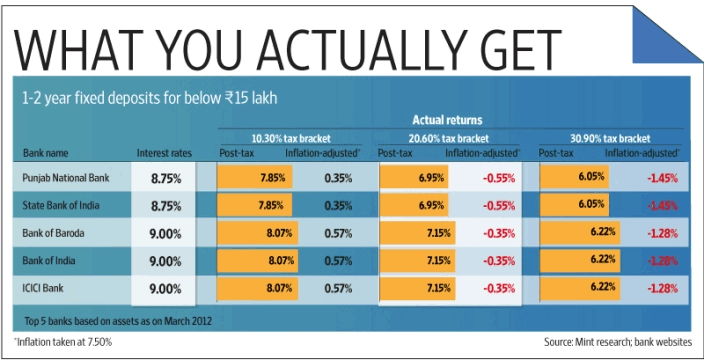

Fixed Deposits do not beat inflation

Even if you are getting an 8-9% return on your fixed deposits, many people do not realize that it’s the pre-tax return. As Fixed deposits are taxable (and every other debt instrument), once you pay the tax on the returns, the post-tax returns are only in the range of 6-7% and if you adjust the inflation of 8-10%, you are actually getting a negative return on your fixed-income investments.

Livemint has done a story on this topic in a detailed manner which you should read.

Risk is less in Fixed Income Asset class

All those who want to get a fixed return and do not want to take any risk should choose this asset class. It’s a human nature to seek assurity, and given that fact, fixed income instruments are a big hit. No wonder Fixed Deposits rule the world of investments, It’s simple and easy to understand the financial product.

Same goes for PPF, NSC, recurring Deposits and various govt bonds or debt mutual funds. However note that this asset class does not beat inflation or nearly matches it, hence over the long term, while the amount of your investment will become bigger in number, the purchasing power will remain stagnant or might drop. So this asset class is to only protect your money, not grow it.

Asset Class #2 – Equity

The equity asset class is an interesting asset class and slowly getting more and more acceptance from the last 1-2 decades.

Equity means ownership

So when you invest in equity, it means that you have bought ownership into a business. For example, when you buy stocks of Infosys or Reliance, you become a small owner of that business.

Even the RSU and ESPP which you get from your company makes you a small investor in the company and that’s “equity investment”

Now obviously when you invest in the business, you get a % ownership. And if that company becomes big someday in the future, your overall worth also goes up. But there is a problem, the business grows only over time and in between, there are ups and downs and that reflects in the stock price of the business/company.

If you look at all the rich people today (really filthy rich), it all happened with equity investors. Someone either opened their own company or invested in some company which was growing and held it over the long term.

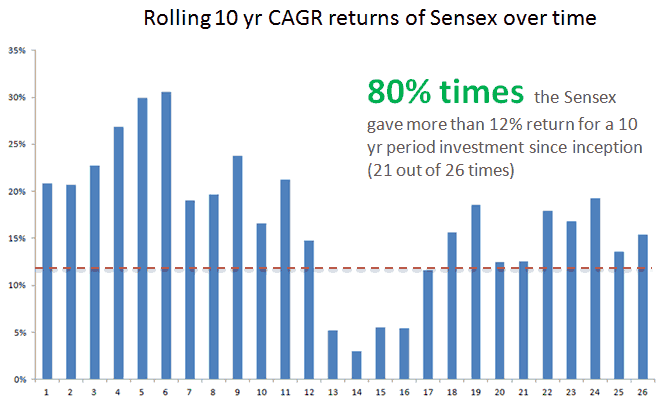

Equity Investing works in the long run

Below is the 10 yrs return chart for various years for Sensex. You can see that most of the time sensex has given more than 12% return (much more than that actually) every 4/5 times. This is since the time Sensex has been into existence.

Because the equity returns are very volatile, most of the people refrain from mutual funds investment or investing in direct stocks, but they are the real wealth builders for any investors. There are mutual funds from various Asset management companies that have a proven track record for building wealth for its investors.

Asset Class #3 – Real Estate

Real estate, as we all know refers to physical space, or physical structure like land, residential flats, commercial spaces, etc. These spaces are either used for living purpose or for doing the business and generate income. Should one invest in real estate or not is a topic of debate and I am not getting into that right now.

Over the last 2 decades, the real estate asset class has got tremendous interest from investors. Everyone wants to now own a home and real estate is very sought after asset class. As the country develops and expands, we see many upcoming areas in all cities and a location which was considered outskirt of the city becomes a very important location in the city and we see some amazing returns.

However, the fact is that we always hear the “good” stories and never the bad stories where one got bad returns from real estate or lost their money.

Returns from Real Estate

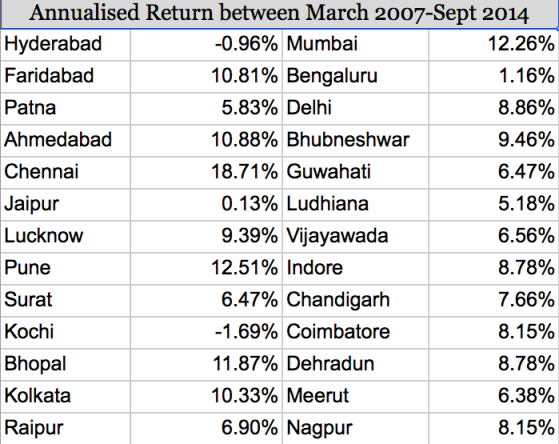

The real estate market has cycles of ups and downs and returns from real estate can be very volatile and can depend on various factors like city future, govt policies, political situations and many more. For example, if you look at Hyderabad, the returns in real estate have not moved anywhere in the last 7-8 years and we are talking about average returns here.

Bigdecisions.com has done a study based on NHB Residex to compute the real estate returns in various Indian cities from 2007-2014 and below were the results.

I am in on way saying if real estate is good or bad. All I am trying to do is make you aware of the characteristics of real estate as an asset class. You need a high ticket size for investment, the market is not regulated at all (only recently the regulation has been made) and it’s more or less one side market with a lot of opaqueness.

Asset Class #4 – Commodities

Commodities refer to various types of physical goods or products which we all can buy and sell for various uses. Gold, Silver, Copper, Rice, and Oil etc will be counted under this asset class. The price of these products depend on demand and supply in the market.

Commodities are for “Trading” and not investing

With my limited understanding, I came to the conclusion that commodities are not for investing for the long term, but mainly for trading, where you can benefit from the market cycles and predict demand and supply moves and get a profit or loss.

Returns from the commodities can be very volatile and each commodity has its own market and dynamics.

Only a handful of commodities like Gold or Silver can be invested in for a very long time because they can be stored without losing their usage. A common man can’t store other commodities in the same way, hence trading them for short term is a feasible option.

Asset Class #5 – Cash

When I say “cash”, I don’t just mean the hard cash bundles, but also the money lying in your saving bank account, or liquid mutual funds. I will refer all of these things as “Cash”.

The best thing about cash is that it gives you the freedom to “buy” anything you want instantly. You can buy a car, a house or a phone or invest your money in other asset classes.

The freedom you get with cash is very high and that’s one reason why most of the people prefer to hold a lot of cash. Also the cash cannot be tracked (unless it’s several multi-crore rupees) and many people keep their black money in form of cash.

It’s not uncommon to see many lakhs lying in a savings bank account just because the investor thinks “What if something goes wrong?”

However cash has one problem, it does not fight inflation at all or very little. The money lying in saving bank account just earns 4% and that does not help you as an investor.

Which asset class you should invest into?

Where should you invest your money? This question can only be answered if you are clear about your requirements like how much risk can you take and how much return do you expect out of your investment?

Are you ok with locking your money for several years or not? I have made a simple table that compares all asset classes on various parameters.

![asset class-] comparison](https://www.jagoinvestor.com/wp-content/uploads/files/asset-class-comparision.png)

I hope this article gave you a high-level understanding of all asset classes and cleared your basics. Please share which is your favorite asset class and why?

Hi Manish,

I’m a rookie investor and am happy that your blog is literally the only one that i keep coming back to.

Keep up the good work!

Glad to know that Augustus ..

If the Fixed Income from FD after the post tax is – or +.5 then keeping the money in the SB account will earn more right? they why you are mentioning FD is near inflation beat and cash in the bank is not?

thats above the limit of 10k exemption

Great article for young investors looking for greater returns

Thanks for your comment kunal

Very very important info. about asset class. Thanks…

Thanks for your comment AmitKumar

Manish, Nice Didactic article

Thanks for your comment Ankit

Clear and crisp article. Thank you Manish.

Very very informative, as usual!

Thanks for your comment Aravind

Thanks so much Manish

Thank you very much for the info.

Could you please post the ideal scenario of investment of a person in all 4 assets except Real Estate.

Consider a person having total income with 3L, 5L, 7L and investing them in all Assets. Just to show people how investments can be made and can help us to get greater returns in future.

Thanks again,

With such a close level of income (3/5/7 lacs) is not very different in my opinion. As the income increases, the potential to invest in real estate increases.

Very Informative.Thanks!

Thanks to Mr. Chauhan for a such a beautiful article. This is the best blog about financial planning I have found on internet so far. Thanks again

Thanks for your comment Koushikdas

Once again fantastic article

Thanks

Next looking for some article to educate NRI’s to build assets. Like people planning 10 years or less at abroad and want to come back and settle in India. like one stay in US can transfer 1 to 2L amt monthly to India and dont want to take risk of investing directly into any market.

That does not change anything . Quantum of amount invested has no related with asset classes choice!

Excellent Article

Thanks for your comment Pradeep

Very Nice post , valuable and easy understandable.The chart of risk and reward is too good.

Thanks for your comment Rathod

Informative Post in simple words! Thanks Manish for sharing.

Few Points:

1 Equity is going to be best investment class in the coming future.

2 Direct investing in stocks is good but requires experience and proper knowledge.

3 If you want to create long term wealth SIP is the easy and best option.

Yes Gaurav

You have summerized it well !

Awesome and very well explained to any no-vice investor!

Thanks for your comment SudhindraArsikere

Good explanation for the non commercial graduate .

Best wishes.

Thanks

Very informative using simple explanations and common usage terms. Thanks a lot.

Thanks

Hi, I am working for this distribution : 3 years expenses worth money in fixed assets. Remaining equally in Cash & Equity, Any comment ?

Yea looks good to me !

Thanks Manish. That boosts my confidence. I find this website very useful. you are doing excellent work